A Frayed and Fragmented System of Supports for Low-Income Adults Without Minor Children

Table of Contents

Overview: Current System Leaves Great Unmet Need, Lifts Few Out of Poverty

SNAP Restricts Nutrition Assistance for Low-Income Non-Elderly Adults Not Living With Minor Children

State General Assistance Programs Provide Cash Aid to Few Low-Income Adults

Overview: Current System Leaves Great Unmet Need, Lifts Few Out of Poverty

By Joseph Llobrera and Lauren Hall

Over 100 million people — about a third of the country’s population — are non-elderly adults who don’t have minor children in the family[1] and don’t have severe disabilities. More than 1 in 8 of these adults are in poverty.[2]

Our system of economic and health supports — such as Medicaid, the Supplemental Nutrition Assistance Program (SNAP), and refundable tax credits — is geared largely toward helping children and their parents, people with disabilities, and the elderly. The nation’s basic supports for low-income, non-elderly adults without children, particularly for those who do not meet a rigorous disability standard, are weak, fragmented, and often highly restrictive, leaving many of these individuals without help they need to afford the basics. These adults need stronger supports to help meet essential needs, a problem that the hardships inflicted by the COVID-19 pandemic have magnified.

Compared to the larger population of non-elderly adults, low-income non-elderly adults are more likely to be young, have lower educational attainment, or have a disability that may not be severe enough to qualify for Supplemental Security Income (SSI) or Social Security Disability Insurance (SSDI) but nonetheless prevents or limits work. Due to systemic racism and other factors that have resulted in fewer educational and employment opportunities, non-elderly adults who identify as Black or Latino are more likely to have low incomes.

Most of these adults who are able to work do so, but they often hold jobs with greater turnover and volatility that don’t pay high enough wages to enable these adults to meet basic needs such as adequate, nutritious food and safe, stable housing. Often these jobs also do not provide benefits like employer-based health insurance.

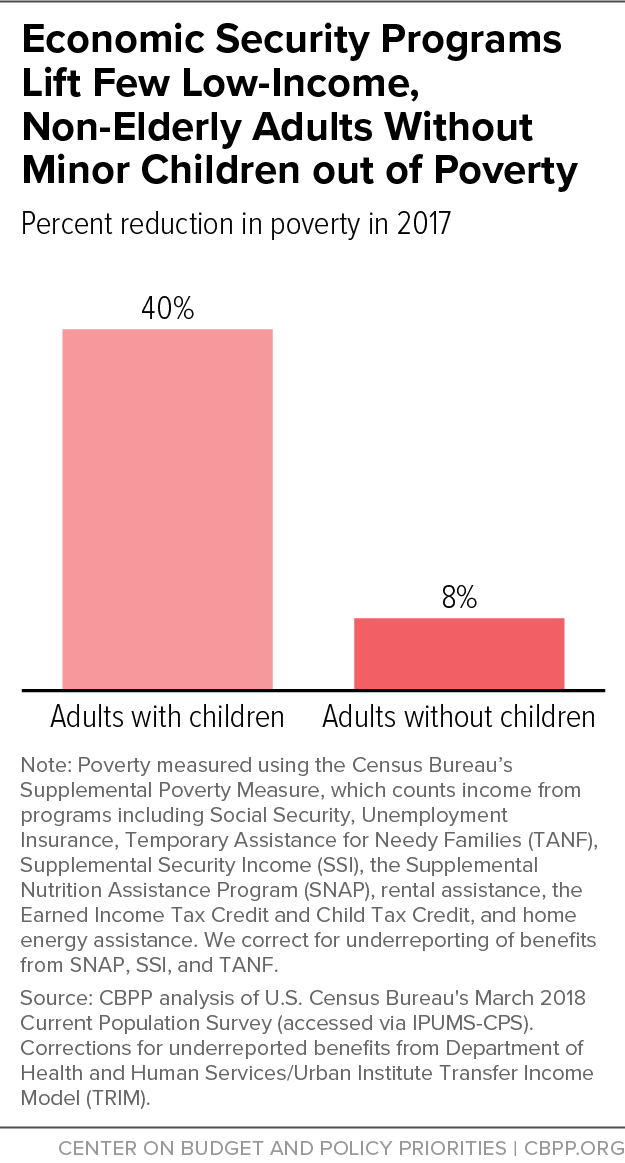

The nation’s system of economic and health supports often leaves these adults unassisted or aided to only a small degree. While the current system of economic security programs reduces the number of non-elderly adults with minor children in poverty by 40 percent by lifting their family incomes above the poverty line, these programs reduce poverty by only 8 percent for non-elderly adults without minor children. (See Figure 1.)

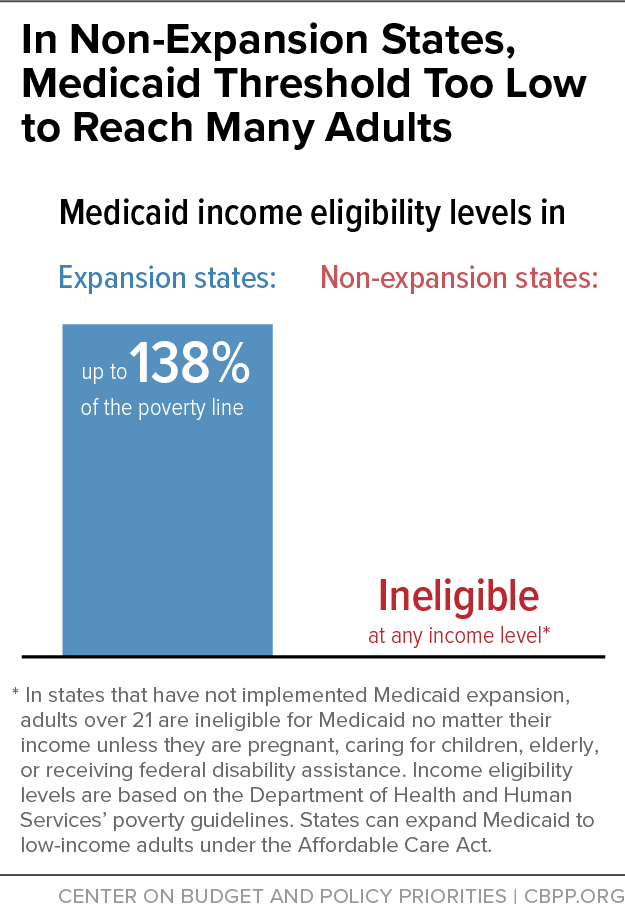

- Low-income, non-elderly adults not living with a minor child are more likely to lack health insurance (29 percent) than those living with children (24 percent).[3] This problem is most severe in the 14 states that haven’t implemented the Affordable Care Act’s (ACA) Medicaid expansion, where these adults are ineligible for health insurance through Medicaid (unless they have a serious disability).

- One in ten households without minor children experienced food insecurity in 2019. For the subset of this group that consists of low-income, non-elderly adults who aren’t living with minor children and don’t have a disability, food assistance is available through SNAP for only three months out of every 36 while they aren’t employed or participating in a work or training program at least half time, unless they live in an area temporarily exempt from this restriction because of elevated unemployment.

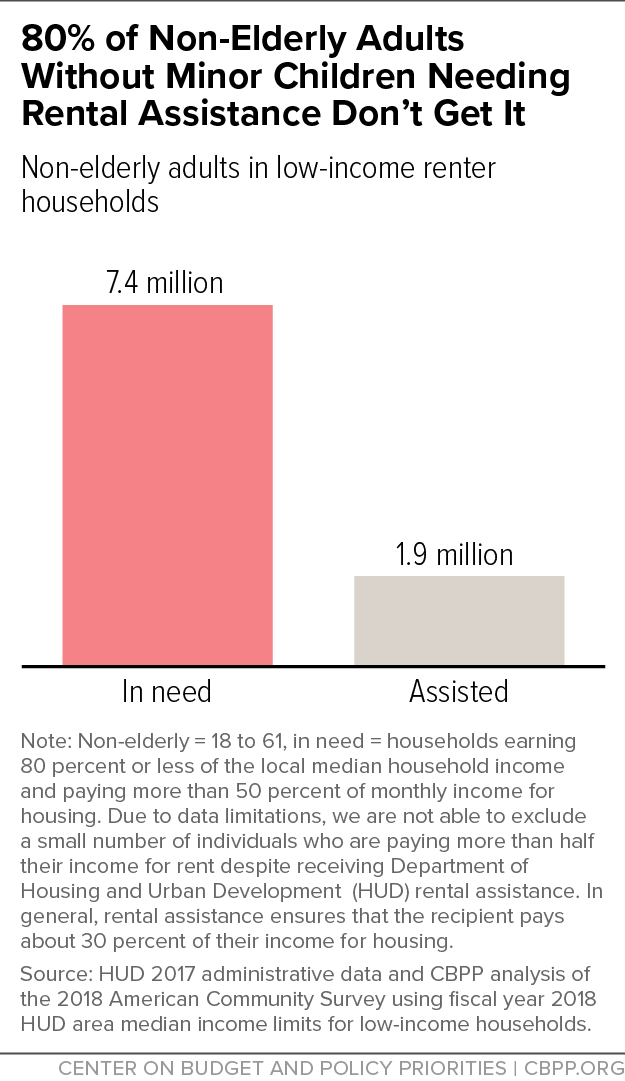

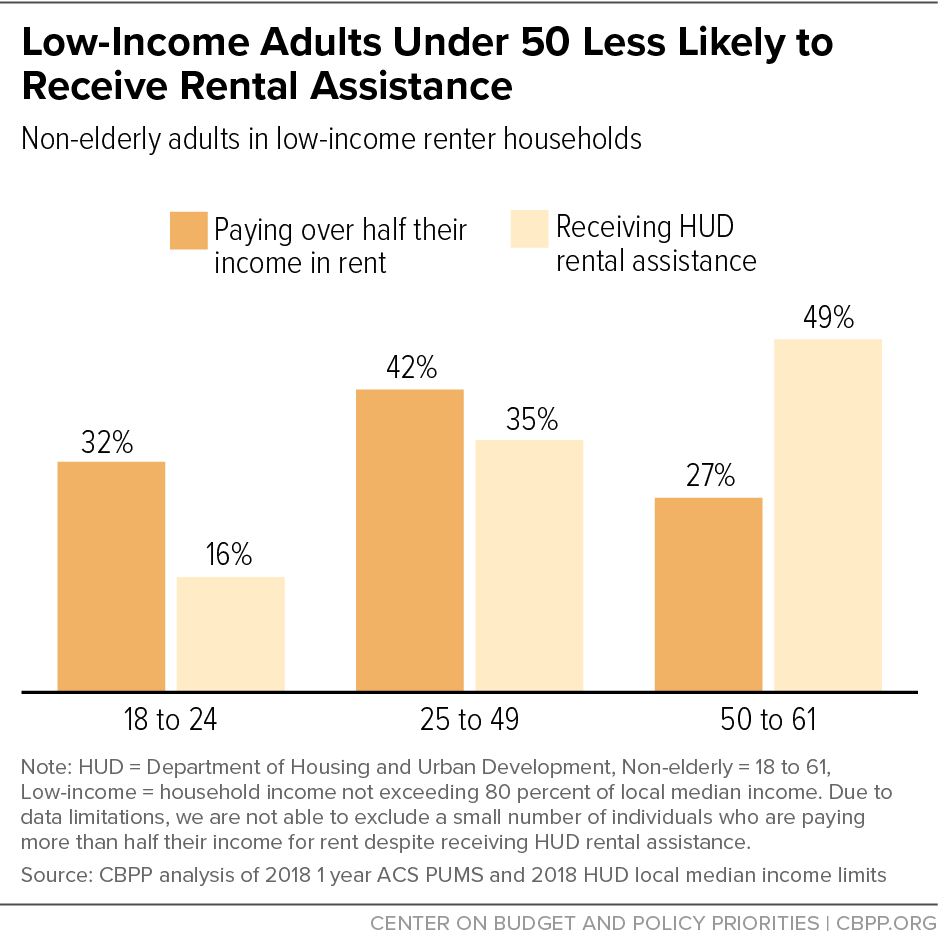

- Some 9.3 million non-elderly adults not living with minor children both meet the eligibility criteria for federal rental assistance and pay more than half of their income for rent, but only 1.9 million of them — 1 in 5 — receive any such assistance. Housing assistance is very constrained due to funding limitations, resulting in large unmet need.

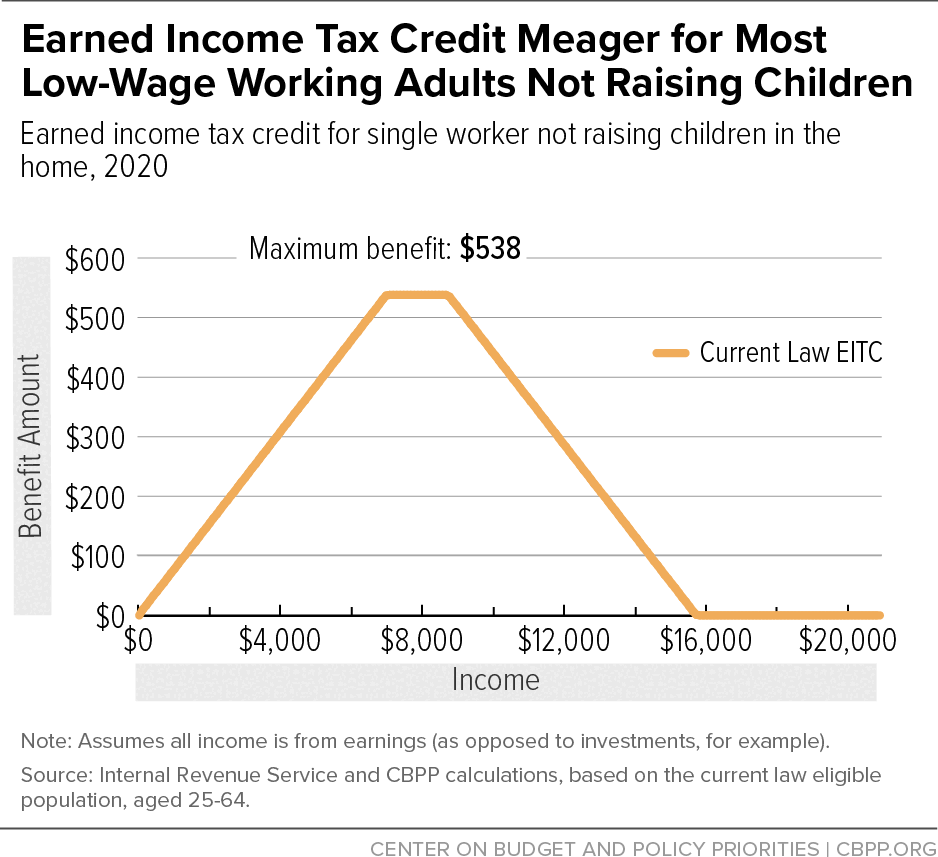

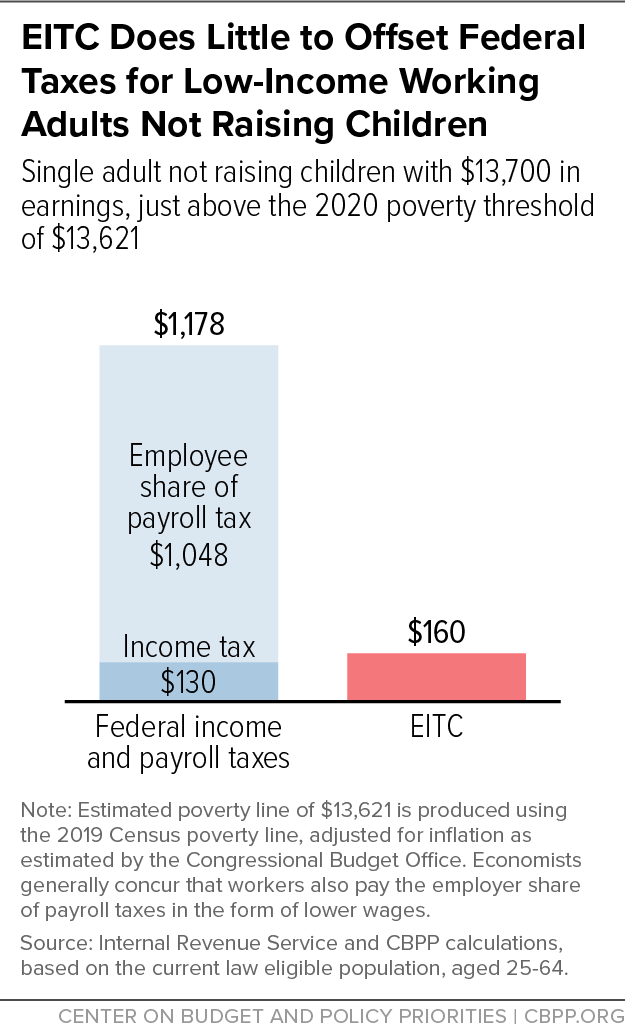

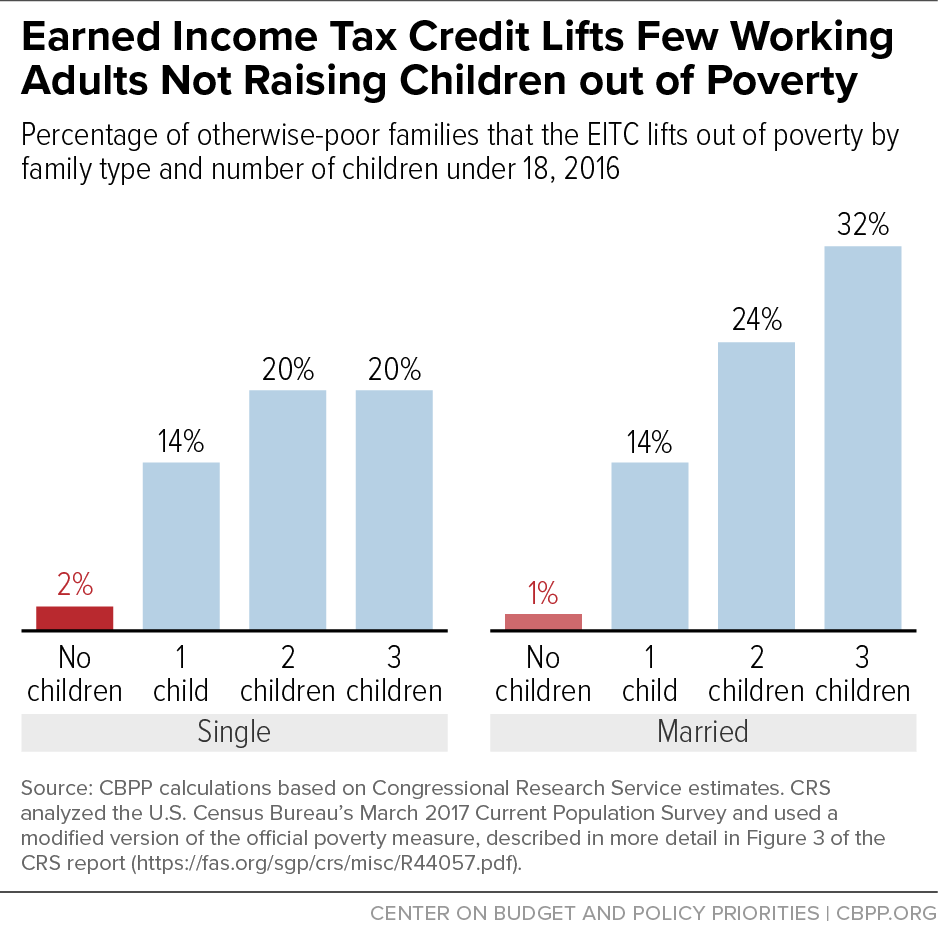

- Workers without minor children are the only demographic group that contains people whom the federal tax system taxes into, or deeper into, poverty. That’s in part because they are eligible only for a tiny Earned Income Tax Credit (EITC) that is too small to offset the federal taxes (primarily payroll taxes) they owe, or are eligible for no EITC at all.

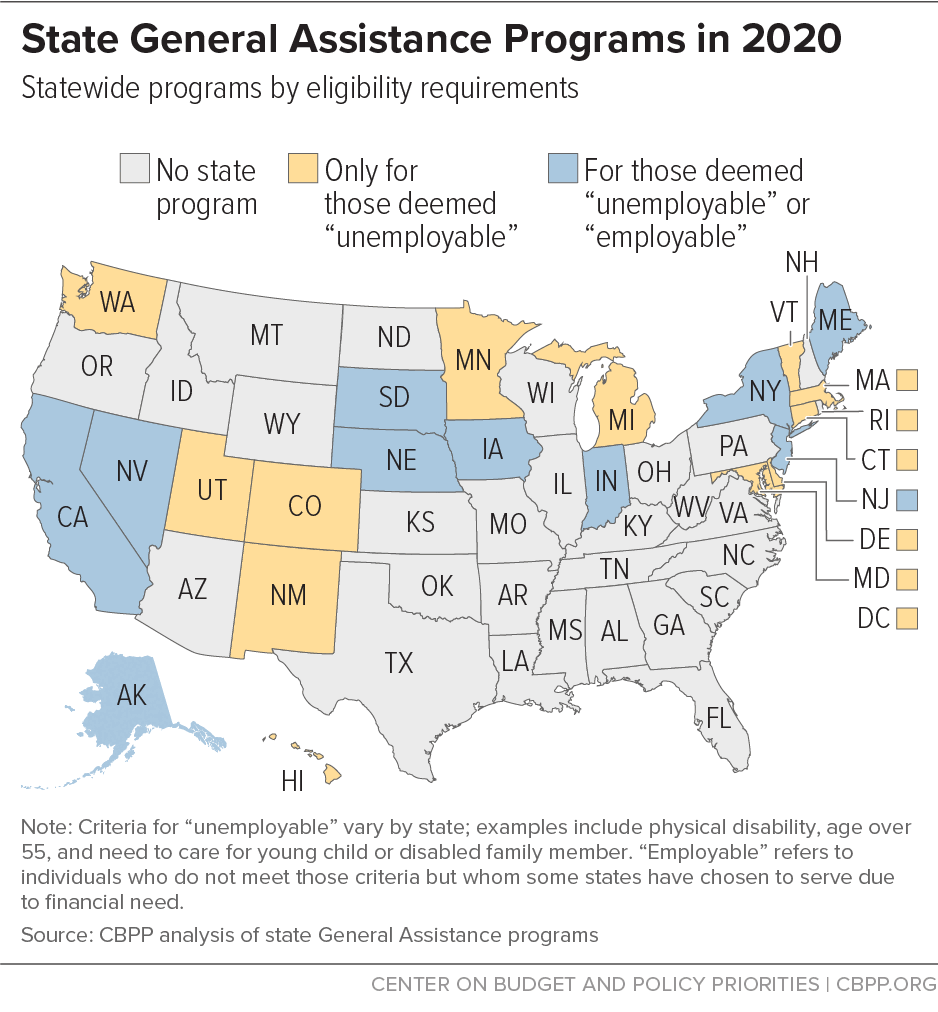

- Only about half of the states have General Assistance programs that provide basic cash aid to very poor people without minor children in the home, and fewer than half of those states provide any such benefits to people who don’t have a disability or other specified barrier to employment.

Many non-elderly adults without children have disabilities or illnesses that make working difficult. Most federal programs that provide benefits to individuals with disabilities, however — such as SSI and SSDI — generally provide benefits only to individuals with severe and long-lasting impairments. Many people with work-limiting impairments are ineligible for disability benefits despite being out of work or able to work only modest amounts.

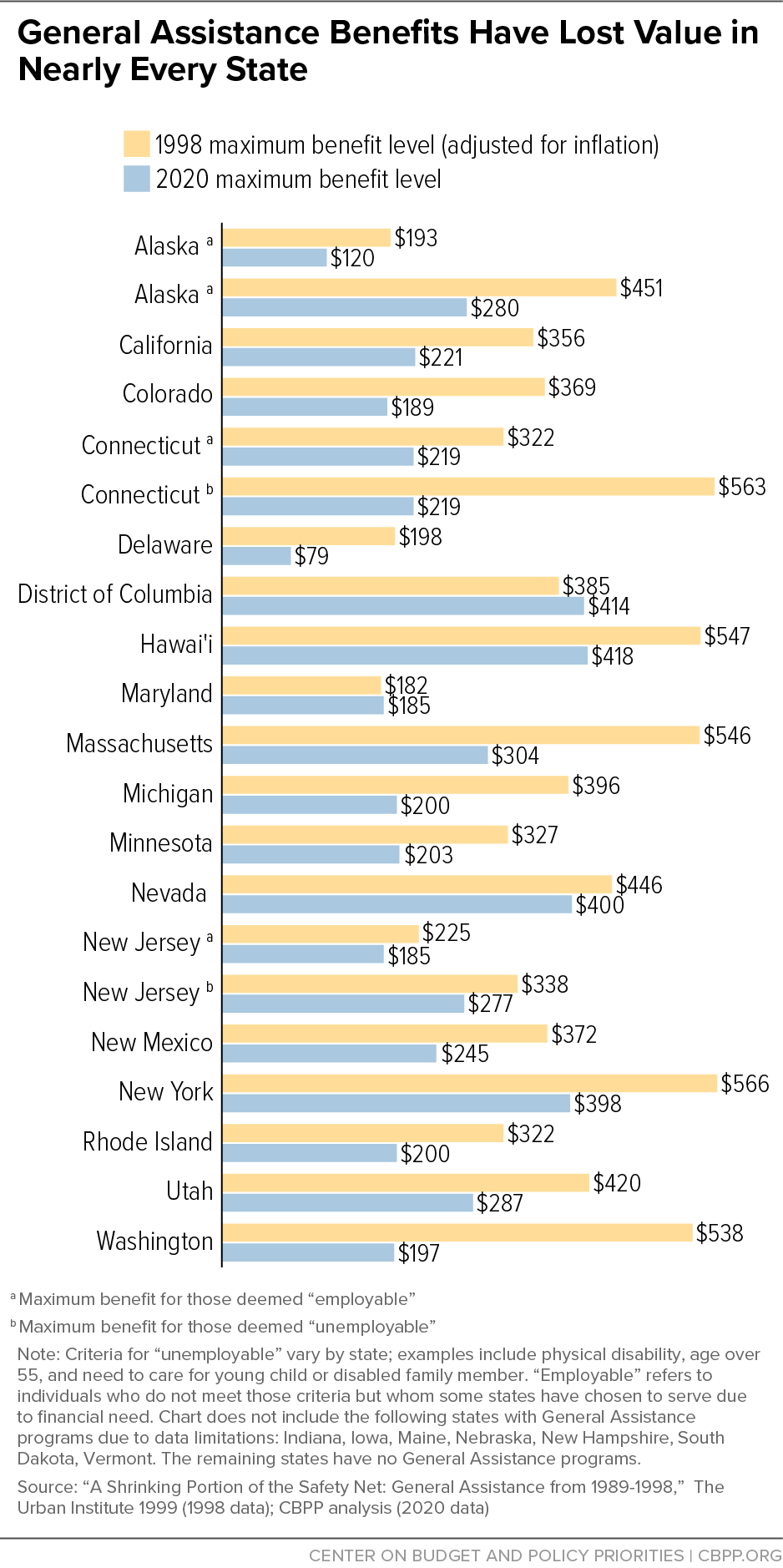

The federal government has left it up to states to decide whether to provide any cash assistance to low-income, non-elderly adults without children who don’t meet the disability standard for SSI and SSDI. If states do provide such help, it’s entirely up to them to decide how much to provide and under what conditions. Most states have never provided substantial support for this group. Moreover, income support for these individuals has weakened substantially over the past 30 years and continues to erode.

The COVID-19 pandemic and the economic hardship it has caused have further exposed critical gaps in America’s system of economic and health supports. Low-income, non-elderly adults without children have been particularly hard hit, due to their low incomes and disproportionate employment in low-paid industries that have experienced larger job losses. In addition, Black, Latino, and Indigenous people as well as immigrants have been affected disproportionately by both the health crisis and its economic fallout.[4] With millions of people unemployed or facing substantial income losses during the COVID-19 economic downturn, the lack of stronger economic and health supports for this group is having a particularly acute impact.

Who Are the Low-Income, Non-Elderly Adults Without Children?

In 2017, there were over 100 million 18- to 64-year-old adults in the United States without children in the family who didn’t receive Social Security or SSI.[5] One in five had income below 200 percent of the official poverty line (about $25,500 annually for a single individual in 2017); 1 in 10 lived below 100 percent of the official poverty line (about $12,800 annually for a single individual in 2017).[6]

Using the Census Bureau’s Supplemental Poverty Measure (SPM), 13.1 percent of non-elderly adults without children lived in poverty in 2017 after accounting for government benefits and certain expenses (such as out-of-pocket medical expenses).[7] This group is more likely to experience poverty than are non-elderly adults with children, whose poverty rate under the SPM was 10.9 percent in 2017.[8] The SPM poverty rate among children, themselves, was 13.6 percent.

The slightly higher poverty rate for children than for non-elderly adults without children in part reflects the smaller family sizes for the latter group. The income level that puts families of one or two members above the SPM poverty line is low ($13,400 for a single individual) compared to the corresponding level for a larger family with children (the SPM poverty line for a family of four is $28,900).[9] Supports for low-income, non-elderly adults without minor children are much less effective at lifting those adults above the poverty line than are the supports available to families with children.

The population of low-income, non-elderly adults without children or disabilities is a dynamic one: employment status and economic status for any individual may change over time. In addition, disability may be short term or longer lasting and may vary in severity over time. And whether the adult has a child in their home may change as they or a child joins or moves out of a home.

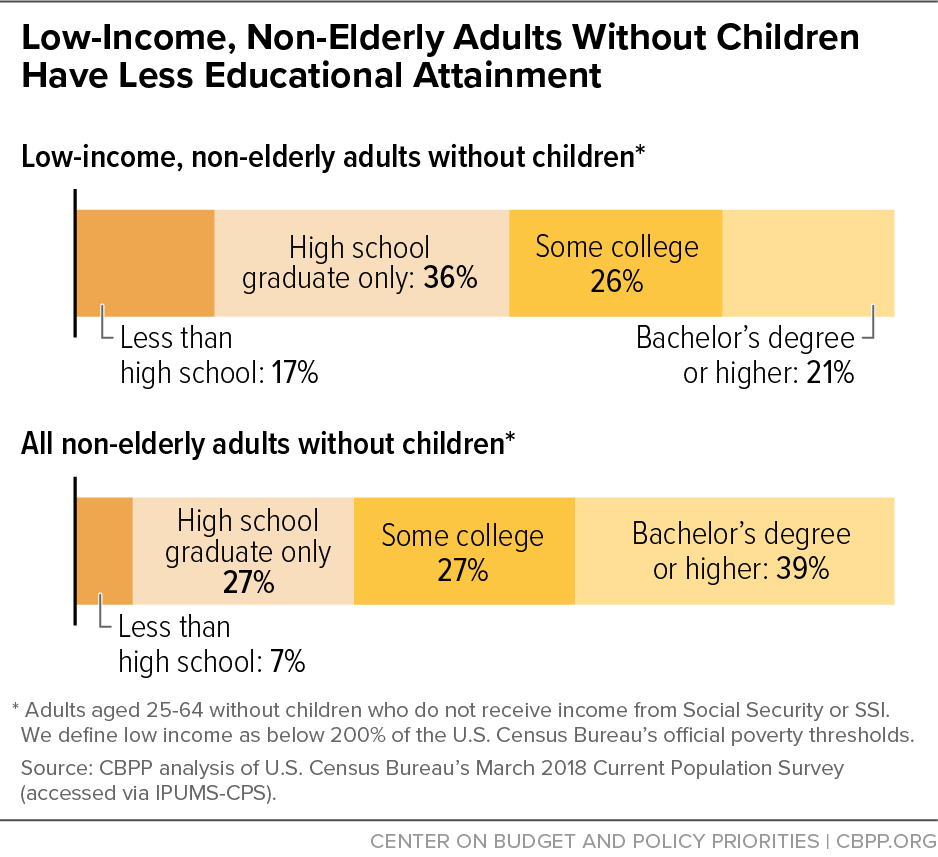

Low-income adults without children generally tend to be younger than all non-elderly adults without children: about 60 percent are under age 45, compared to 52 percent for all non-elderly adults. While the majority of non-elderly adults without children are white, Black and Latino people are overrepresented among those with low incomes, indicative of historical racism and other factors that have led to wide disparities and unequal treatment in housing, education, and employment. And while over one-third of all non-elderly adults without children have a college degree, low-income non-elderly adults without children are only about half as likely to have a college degree, which often limits their employment and economic opportunities. (See Figure 2.) Low-income non-elderly adults without children are also twice as likely as all non-elderly adults to have a disability that limits or prevents work.[10]

Eligibility for some programs is limited to people who are unable to work, and some programs’ definitions of disability do not account for certain physical, mental, or other health conditions that limit the kind or amount of work an individual can do. In some programs, eligibility for non-elderly people who aren’t employed is limited to people receiving SSI or SSDI. But SSI[11] and SSDI[12] have arduous (and lengthy) disability determination processes, and many people with disabilities don’t receive those benefits. Of the more than 46 million adults reporting a disability in 2014, only about 40 percent received cash assistance such as SSI or SSDI.[13] Many did not qualify because their disability did not meet the strict criteria for these programs, which can relate to both the severity and the duration of an individual’s condition.

If an adult is deemed able to work, they often are expected to work in order to qualify for benefits. In actuality, work status for this group fluctuates; many people work significant periods of time but also experience periods of joblessness. Work status for this group is better considered over time than at a single point in time.

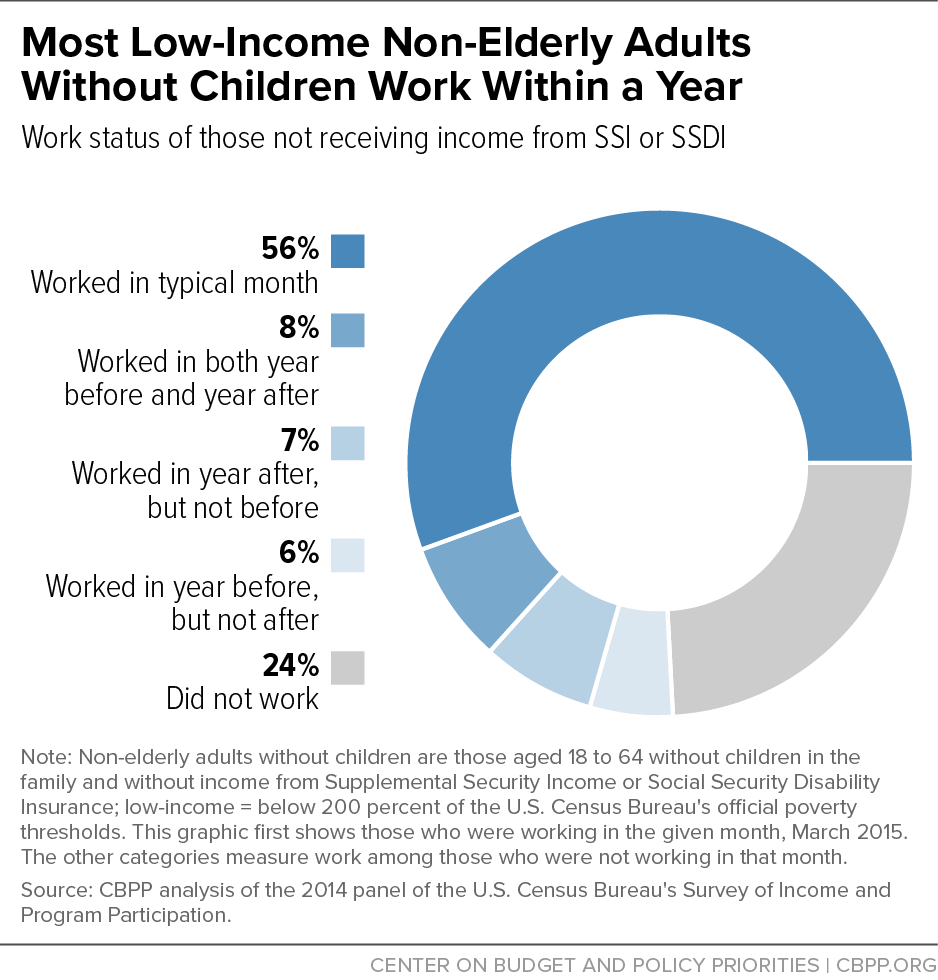

Most low-income, non-elderly adults who can work do so. Using the most recent longitudinal data from the Census Bureau’s Survey of Income and Program Participation (SIPP),[14] we examined the employment data pertaining to low-income, non-elderly adults who don’t have children in the family and don’t receive SSI or SSDI. (See Figure 3.)

An adult may be out of work for a period of time for a variety of reasons, including health reasons, school attendance, or the need to care for a family member. Others cannot find work or have been laid off. People who are not working within a year are more likely to identify as having a disability than those who are working. If benefits are contingent on employment, non-elderly adults without children may find themselves ineligible for important assistance, including at times when they need it most.

Educational attainment often plays a role in the availability of employment opportunities. For example, the SIPP data show that people who weren’t employed 12 months before or after the given month we examined tended to have less education than people who worked within that period. An adult’s educational attainment is the result of many factors, including their family’s income when they were children and the quality of the schools they attended. Due to racism and discrimination, people of color disproportionately face barriers to educational and employment opportunities. This is reflected in the SIPP data, which show that people of color were somewhat less likely than those identifying as white to work 12 months before or after a given month, though most people of every racial or ethnic group work.

Moreover, the COVID-19 pandemic and recession have exacerbated systemic barriers to economic mobility that people of color face. Due to factors including the lack of adequate educational and employment opportunities, Black and Latino workers were more likely prior to the pandemic to be employed in low-paid industries that have seen disproportionately large job losses during the pandemic.[15] Low-paid industries accounted for more than half of the jobs lost from February to December 2020, our analysis found.[16] Similarly, people with a college degree have seen jobs return far more quickly than people without a college degree, exacerbating racial disparities in unemployment.

Economic and Health Programs Often out of Reach for Low-Income Adults Without Children

When these adults do receive assistance, health and economic security programs can increase their access to health insurance, their food security, and their housing stability, ultimately improving their health outcomes and economic well-being. For example, SNAP keeps millions of people out of poverty, reduces food insecurity, and has been linked to positive health outcomes among adults, such as fewer physician visits, fewer days missed due to illness, more positive self-assessments of health status, and a reduced likelihood of demonstrating psychological distress.[17] In addition, the coverage provided by the ACA’s Medicaid expansion yields significant benefits for those who gain coverage, including improved access to health care, better financial security and economic mobility, and better health outcomes such as lower morbidity and mortality.[18] Rental assistance is highly effective at reducing homelessness and housing instability among those receiving it, and by lowering rental costs, it allows low-income people to spend more on other basic needs like food and clothing.[19] The EITC and General Assistance raise low incomes and reduce poverty.

These programs reach far fewer adults without children than the number who need such assistance; many non-elderly adults without children receive little or no assistance despite experiencing serious hardship. Cash aid provided through General Assistance was never substantial and continues to erode, and uneven coverage and restrictive policies limit the ability of various federal economic and health supports to adequately address needs like food, housing, and health care. Although economic security programs reduce the number of non-elderly adults with minor children in poverty by 40 percent, these programs reduce poverty by only 8 percent for non-elderly adults without minor children.[20] Strengthening these supports for non-elderly adults without children would be particularly important to improving the well-being of people of color and immigrants, who typically have fewer assets to fall back on during hard times.

In addition, many immigrants with very low incomes are ineligible for various forms of public assistance due to their immigration status, including people with Deferred Action for Childhood Arrivals or Temporary Protected status, people with temporary visas related to a variety of factors like schooling, people filling jobs needed in certain economic sectors, and lawful permanent residents who are in their first five years of having that status. These restrictions in accessing support place many immigrants and members of their families in an especially vulnerable situation amid the COVID-19’s pandemic and economic crisis. In other cases, lawfully present immigrants or members of their families are eligible for help from programs like SNAP or Medicaid but often forgo that assistance out of fear of the Trump Administration’s harsh “public charge” policies, which can place immigrants at risk if they receive those benefits despite being eligible for them.[21] If immigrants and their family members are afraid to access help for which they qualify, they are more likely to face serious hardships like eviction, poor health outcomes, homelessness, and hunger.

The economic and health programs discussed in this paper cover non-elderly adults without children to varying degrees, but the programs’ eligibility restrictions with respect to this population leave many adults in need with little or no assistance. Furthermore, the differences in eligibility across programs can be complex and cumbersome for people to understand and navigate. (See Table 1.) And wide variations across states mean that two otherwise-similar people living in different states may have varying types and levels of assistance available to them.

Medicaid. States have the option to expand Medicaid coverage to low-income adults with incomes below 138 percent of the federal poverty level, or $17,608 for a single person in 2020. If a state does not adopt the expansion, then among adults who aren’t elderly, disabled, or in need of long-term care, only parents (often only parents with exceedingly low incomes) can qualify for Medicaid. Other non-elderly, non-disabled adults are generally ineligible for Medicaid in these states regardless of how low their incomes are or whether they have access to other coverage.

Thirty-six states and Washington, D.C. have implemented the ACA Medicaid expansion, with two more states planning to implement it in the near future as a result of successful ballot initiatives in 2020. More than 15 million adults had health insurance coverage in 2019 through the Medicaid expansion. But an estimated 6.5 million more would have been covered had all states adopted the expansion. (The figures cited here include both adults with children and adults not raising children in their home.)

SNAP. SNAP provides food assistance to nearly 5 million low-income working-age adults not living with minor children. Nearly 3 million of these individuals, those aged 18 to 49, face much tougher eligibility rules than other participants. In general, they can only receive SNAP benefits for three months out of every 36 months unless they are working or participating in a qualifying work program for at least 20 hours per week, regardless of the availability of work or training programs in their area. People who search diligently for work but can’t find it are cut off the program after three months despite their search efforts. States can waive the three-month time limit for this group for areas within the state that meet certain unemployment thresholds. In 2019, 34 states, the District of Columbia, Guam, and the U.S. Virgin Islands had a waiver from this time limit in place in parts of the state with high unemployment. The time limit has been temporarily suspended nationally during the COVID-19 pandemic.

Federal rental assistance. Rental assistance makes housing affordable by allowing low-income families to pay 30 percent of their income for housing, with a federal subsidy covering the rest. Rental assistance helps about 10 million renters keep a roof over their heads. It also helps people with disabilities; nearly half of the non-elderly (aged 18 to 61) adults without children receiving rental assistance have a disability.[22] Insufficient funding prevents most people in need from receiving any help with the rent, however. Fewer than 1 in 5 eligible non-elderly adults without children receive any rental assistance.

EITC. The Earned Income Tax Credit is a federal tax credit for low- and moderate-income households that increases in value as a person’s earnings rise (up to certain income thresholds); only households with earnings in that year qualify. The credit amount depends on whether tax filers have qualifying children (and if so, on the number of children). For people in certain income ranges, the credit amount also depends on marital status. (This part of the EITC structure is designed to address marriage-penalty issues.) The EITC boosts incomes and reduces poverty, but is far stronger for low-income families with children than for low-income working adults without children, who are eligible only for a small credit or none at all. Largely as a result of the EITC for these workers being so small, the federal tax code taxes about 5.8 million adults between the ages of 19 and 65 who aren’t raising children in their home into, or deeper into, poverty; the federal payroll (and in some cases, income) taxes these workers owe are larger than any EITC they receive. In addition to the federal EITC, some 29 states plus the District of Columbia and Puerto Rico have enacted their own versions of the EITC, which typically are set at a modest percentage of the federal EITC.

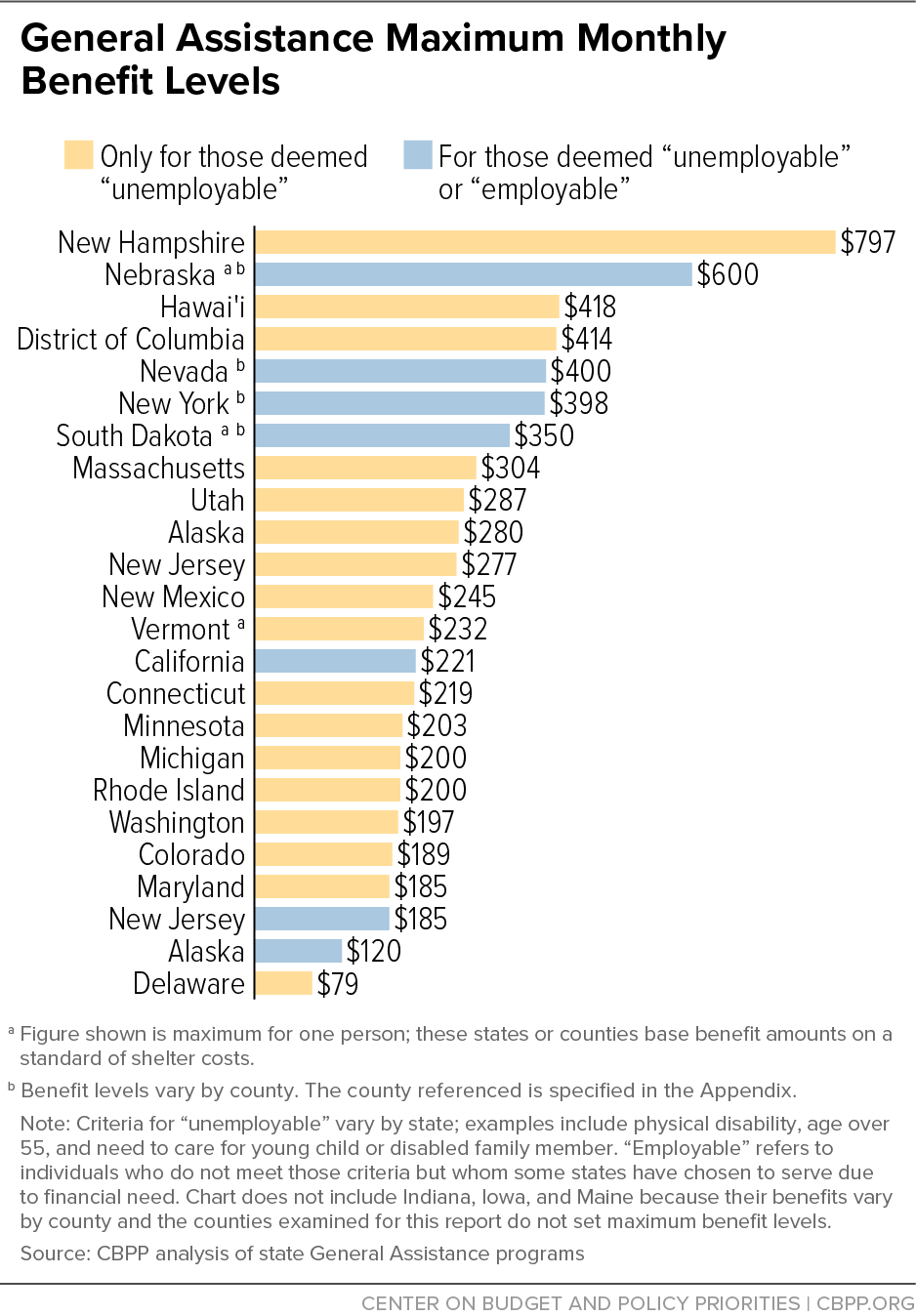

General Assistance (GA). General cash assistance is entirely funded with state or local dollars. States can choose whether to have a program at all, and if so, they set their own eligibility criteria and benefit levels. Half the states do not provide any type of GA. Of the 25 states that do, only 11 provide any GA benefits to individuals who are deemed “employable,” meaning that they don’t have a disability or certain other barriers to work. State GA programs served fewer than a half million poor households in December 2019. Benefit levels are very low: maximum benefits fall below half the federal poverty level in most states with GA programs, and below a quarter of the federal poverty level in half of these states.

Policymakers Can Strengthen Supports for Low-Income Adults

The system of economic and health supports for low-income, non-elderly adults without children should be strengthened to close gaps in the current spotty system of assistance. These programs have the potential to substantially reduce financial, housing, and food hardship that many low-income, non-elderly adults without children face. This is especially urgent in response to the COVID-19 pandemic and economic downturn and the increased hardship that low-income households confront. To ensure households have the assistance they need when they fall on hard times, policymakers should:

Expand program coverage and strengthen program benefits. Due to some programs’ limited coverage and benefits, many low-income non-elderly adults are receiving little or no assistance. Expanding program coverage and boosting benefits would provide greater assistance to this group and lift more people out of poverty. For example, all states should adopt the ACA’s Medicaid expansion for low-income adults (and federal policymakers should consider new financial incentives to encourage the remaining states to do so), and the federal government should modify the ACA marketplace coverage that’s offered to low-income adults to better ensure quality affordable coverage in states that continue to decline to expand Medicaid.

Make assistance available to those who don’t have jobs. As described above, some programs make benefits available only to non-elderly adults who are employed or meet a strict definition of disability. This lack of assistance leaves many in need without help and overlooks key nuances about this population. Ultimately, more significant income assistance and fewer eligibility restrictions are needed to reduce poverty and hardship among this group.

Reduce significant variation across states in program rules. Reducing the variation in access to programs and benefit amounts would allow low-income adults to receive more equal support, regardless of residence.

Prevent further restrictions in eligibility and benefits. Some federal and state policymakers have proposed measures that would further restrict eligibility and benefits for key needs-based programs, lessening their ability to provide assistance and meet the needs of low-income adults. Given that economic and health programs can improve health, educational, and employment outcomes, while also alleviating hardship, policymakers should reject efforts to curb access to these benefits.

The chapters that follow describe eligibility criteria, participation data, and measures of effectiveness for low-income, non-elderly adults without children across five types of health and economic security programs: Medicaid, SNAP, HUD rental assistance programs, the EITC, and state General Assistance programs. The table below briefly explains how each program defines and determines eligibility, the benefits available to participants, and variation among states in administering these programs.

| TABLE 1 | |||

|---|---|---|---|

| Economic and Health Supports Are Fragmented, Weak for Low-Income, Non-Elderly Adults Without Minor Children in the Family | |||

| Program | Eligibility Affecting Non-Elderly (18- to 64-year-old) Adults Without Minor Children in the Family | Benefits | State Variation |

| Medicaid | States have the option under the ACA’s Medicaid expansion to cover adults aged 19-64 with incomes at or below 138 percent of the federal poverty level — including adults who don’t have children living in the home and don’t otherwise qualify for Medicaid (i.e., they don’t have a federally recognized disability). | Access to comprehensive health care that improves health outcomes, financial security, and economic mobility. | Access to Medicaid for this group largely depends on whether a state has adopted the Medicaid expansion. Currently, 36 states and D.C. have implemented the Medicaid expansion, with future implementation anticipated in two more states as a result of the approval of ballot initiatives. |

| Supplemental Nutrition Assistance Program (SNAP) | Otherwise-eligible adults aged 18-49 (who generally must have gross income below 130 percent of the federal poverty level) who aren’t physically or mentally unable to work, pregnant, or in a household with a minor child can receive SNAP benefits for only three months (out of every 36 months) in which they are not employed or participating in a qualifying work or training program for at least 20 hours per week. Searching for work but being unable to find work does not count as a qualifying work activity. | Nutritional support to purchase food at designated SNAP retailers. In 2018, the average monthly benefit for one-person households consisting of adults aged 18-49 without minor children was $172. | The three-month time limit can be lifted in some areas if the state receives a temporary waiver from the time limit, based on elevated unemployment in those areas. In 2019, 34 states, D.C., Guam, and the Virgin Islands had a waiver from the time limit in place, in most cases for part of the state. |

| Federal Rental Assistance | Adults aged 18-61 without minor children and with incomes at or below 80 percent of the local median income are eligible for housing assistance, but funding is limited. Due to insufficient funding, 7 million eligible households consisting of non-elderly adults without children that pay over half their income for rent are unable to receive any rental assistance. Available resources are targeted to individuals with disabilities; nearly half of non-elderly adults receiving rental assistance have a disability. | Rental assistance makes housing affordable by allowing families to pay 30 percent of their income for housing, with a federal subsidy covering the rest. | There are variations in how the program is administered by state and local housing agencies and in how those agencies use the program funding they receive. For example, state and local housing agencies administering Housing Choice Vouchers may choose to prioritize people with disabilities when taking renters from a waiting list for assisted housing. |

| Earned Income Tax Credit (EITC) | Adults aged 25-64 who aren’t raising children in the home and who have earned income below a certain threshold (in 2020, $15,820 for someone who isn’t married, $21,710 for married couples). | The EITC is a federal tax credit for low-income workers that raises their incomes and reduces poverty. There is a small EITC specifically for workers without children. It provided an average credit of $302 in 2018. Even with the credit, many in this group still owe net federal taxes, despite being below the poverty line. | States can create their own version of the federal EITC to help low-income working people meet basic needs. Currently, 29 states, D.C., and Puerto Rico have enacted a state EITC, with varying inclusivity and credit amounts. |

| State General Assistance (GA) | Very low-income adults who are not elderly, do not have minor children in the home, and do not qualify for SSI (or are waiting for an SSI benefit determination) sometimes qualify for GA, depending on whether their state offers a GA program and, if so, its eligibility criteria. Available benefits may differ depending on whether an adult has some disability or barrier to employment. | Basic cash assistance to supplement income and provide for basic needs. Benefit levels have eroded over the years, and eligibility has become much more restrictive in many states. Currently, benefits are below half the federal poverty level in most states with GA programs and below a quarter of the federal poverty level in half of these states. | States determine whether or not to provide GA and which groups of individuals to serve. Currently, only 25 states have GA programs at all, and only 11 states provide benefits to individuals who do not have some disability or barrier to employment. Benefit levels vary from state to state. |

ACA Medicaid Expansion Offers Long-Needed Health Insurance Coverage to Low-Income Adults Without Children

Created in 1965, Medicaid is a public insurance program that provides health coverage to low-income families and individuals, including children, parents, pregnant women, seniors, and people with disabilities; it is funded jointly by the federal government and the states. In 2014, the Affordable Care Act (ACA) gave states the option to expand Medicaid eligibility to low-income, non-elderly adults who do not have children of their own living in the home and who do not otherwise qualify for Medicaid for reasons such as having a federally recognized disability.

By October 2020, 36 states and the District of Columbia had implemented the ACA Medicaid expansion option.[23] More than 15 million low-income adults had health coverage in 2019 through the Medicaid expansion, the large majority of them newly eligible for Medicaid because of the ACA.[24] Another 6.5 million would have been covered by Medicaid had all states expanded, the Urban Institute estimates, including roughly 4.6 million low-income adults without children of their own living in the home; more than half were instead uninsured, while most of the rest instead had coverage through the ACA marketplaces, which requires higher premiums and cost sharing.[25] Since the ACA’s major coverage expansions took effect in 2014, Medicaid has helped to reduce the number of uninsured low-income adults without children of their own living in their home from 10.5 million to 5.2 million.

With millions of people newly unemployed or facing sharp income losses during the COVID-19 recession, the need for Medicaid coverage has been growing, as it does during all economic downturns. The states that have expanded Medicaid are better positioned to respond to the COVID-19 public health emergency and to prevent the resulting economic downturn from worsening access to care, financial security, health outcomes, and health disparities.

Medicaid expansion coverage yields significant benefits for those gaining coverage, including improved access to health care, financial security, economic mobility, and better health outcomes.[26] Perhaps most striking, rigorous studies have found that Medicaid expansion — and ACA coverage more broadly — save lives.

Background

Each state operates its own Medicaid program within federal guidelines. Federal policymakers have revised these guidelines over time, both to expand Medicaid eligibility to more low-income individuals and to make new health benefits available to them, such as home health care services and prescription drugs. States have considerable flexibility in designing and administering their programs, so eligibility and benefits vary from state to state.

In 2019, 95 million low-income people were enrolled in Medicaid over the course of the year. In any given month, Medicaid served 31 million children, 27 million adults (mostly in low-income working families), 6 million seniors, and 9 million people with disabilities, according to Congressional Budget Office (CBO) estimates.[27]

Medicaid is an “entitlement” program, which means that anyone who meets eligibility rules has a right to enroll in Medicaid coverage. It also means that states have guaranteed federal financial support for part of the cost of their Medicaid programs, ranging from 50 percent to 77 percent of costs, with states with lower personal income bases receiving greater federal financial assistance.

In order to receive federal funding, states must cover certain “mandatory” populations:

- children through age 18 in families with income below 138 percent of the federal poverty line ($29,974 for a family of three in 2020);

- people who are pregnant and have income below 138 percent of the poverty line;

- certain parents or caretakers with very low income; and

- most seniors and people with disabilities who receive cash assistance through the Supplemental Security Income (SSI) program.

States may also receive federal Medicaid funds to cover “optional” populations. These include: people in the groups listed above whose income somewhat exceeds the limits for “mandatory” coverage; seniors and people with disabilities not receiving SSI and with income below the poverty line; “medically needy” people (those whose income exceeds the state’s regular Medicaid eligibility limit but who have high medical expenses, such as for nursing home care, that reduce their disposable income below the eligibility limit); and other people with higher income who need long-term services and supports. And, as discussed below, under the ACA, states can also cover — with enhanced federal funding — adults aged 19 through 64 with income below 138 percent of the poverty line, including those without children living in the home and those not receiving federal disability assistance. This chapter focuses on these adults — identified in this chapter as “Medicaid expansion adults” — who either are enrolled in Medicaid due to the ACA expansion or who are uninsured but would be eligible and could enroll if their state expanded coverage.

Federal rules also require state Medicaid programs to cover certain “mandatory” services, such as hospital and physician care, laboratory and X-ray services, home health services, and nursing facility services for adults. States can — and all do — cover certain additional services as well. All states cover prescription drugs, and most cover other common optional benefits, including dental care, vision services, hearing aids, and personal care services for frail seniors and people with disabilities. Although these services are considered “optional,” they are critical to meeting Medicaid beneficiaries’ health needs.

Not all people with low income are eligible for Medicaid. In the 14 states that have not implemented the ACA Medicaid expansion (as of October 2020), adults over 21 are generally ineligible for Medicaid no matter how low their incomes may be unless they are pregnant, caring for children, elderly, or receiving federal disability assistance. (See Figure 4.) And, in the typical (or median) non-expansion state, even those who are parents are ineligible if their income exceeds just 41 percent of the poverty line ($8,905 for a family of three),[28] unless they are pregnant or receiving federal disability assistance.

ACA Expands Medicaid to Low-Income Adults Without Children of Their Own in the Home

Prior to the implementation of the ACA’s health insurance coverage provisions, health insurance coverage options were quite limited for low-income adults without children of their own living in their home. Medicaid coverage was available to non-elderly adults not receiving federal disability assistance and without children of their own living in the home only in a small number of states that applied for waivers.[29] The individual insurance market was expensive and often denied coverage or offered only partial coverage, particularly for those with pre-existing conditions. Employer-sponsored coverage was (and continues to be) less available to low-wage workers and often out of reach financially.[30] As a result, in 2013, nearly half — some 48.6 percent — of these adults were uninsured.[31]

The ACA changed the health insurance coverage landscape dramatically for low-income adults without children of their own living in the home. It gave states the option to expand Medicaid coverage to all adults[32] with family income at or below 138 percent of the federal poverty line — $17,608 for a single individual and $23,791 for a couple in 2020.[33] Like all other Medicaid enrollees, these adults are enrolled in comprehensive health coverage with minimal cost sharing. As of October 2020, 36 states and the District of Columbia had implemented the Medicaid expansion for low-income adults.[34] (Two others had adopted Medicaid expansion through voter initiatives but not yet implemented it.)

The federal government finances 90 percent of the cost of Medicaid expansion on a permanent basis. While states pay the remaining 10 percent of the cost, Medicaid expansion has produced net budget savings for many states by lessening the burden on a patchwork of largely state-funded programs that connect people who are experiencing homelessness, have substance use disorders, or have other serious needs with critical health care services.[35]

The ACA also reformed the individual health insurance market, making it more accessible to low-income adults. Each state was required to create an individual insurance marketplace, either federally directed or operated by the state, in which premium tax credits and cost-sharing subsidies help low- and moderate-income families afford health coverage. Financial assistance is available to marketplace enrollees with income between 100 percent and 400 percent of the federal poverty line. And individual market plans now must cover ten categories of essential benefits, including physician care, laboratory services, and hospitalization. Insurers can no longer discriminate against people with pre-existing conditions in the individual market, which is particularly critical given that roughly 54 million non-elderly people have health conditions for which insurers commonly denied coverage.[36]

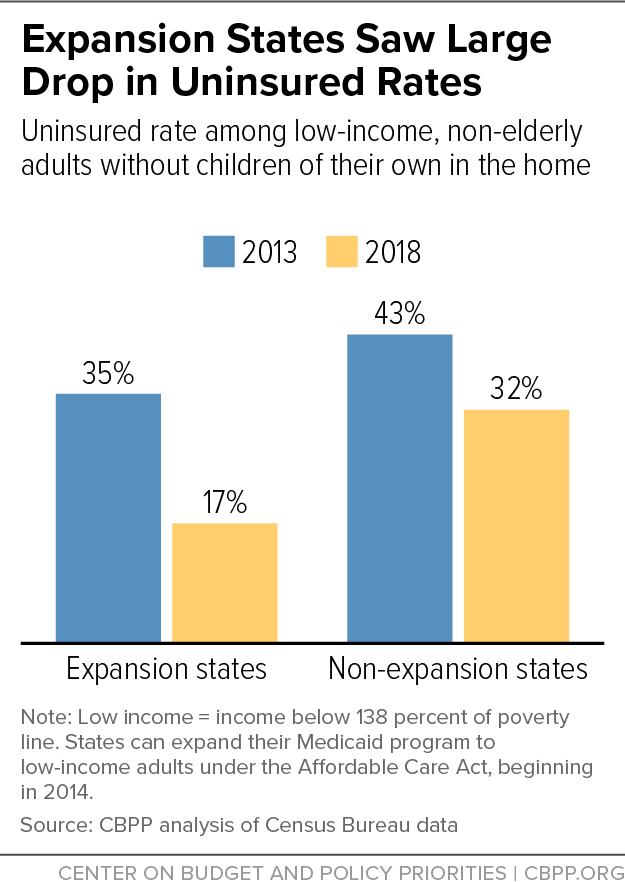

The ACA has led to historic gains in health insurance coverage, improved access to care, reduced financial burden, and improved health for Medicaid expansion adults.[37] The uninsured rate among these adults dropped from 48.6 percent in 2013 to 28.7 percent in 2018, the most recent data available. Gains have been greatest in states that have adopted the ACA Medicaid expansion for low-income adults.[38] (See Figure 5.)

Studies also show that Medicaid expansion leads to more low-income adults having a personal physician and getting preventive care and regular care for chronic conditions, reductions in the share of low-income adults struggling to pay medical bills, better access to credit, improved diabetes and hypertension control, and fewer premature deaths among older adults.[39]

With millions of people newly unemployed or facing sharp income losses during the COVID-19 recession, the need for Medicaid coverage has been growing, as it does during all economic downturns. While comprehensive data are not yet available, preliminary data for a subset of states show enrollment is rising. Among 29 states with July 2020 data, enrollment is up 8.4 percent since February. The 36 states (plus the District of Columbia) that have expanded Medicaid are better positioned to respond to the COVID-19 public health emergency and to prevent the resulting economic downturn from worsening access to care, financial security, health outcomes, and health disparities; enrollment among Medicaid expansion adults rose 10 percent between February and June in the 16 states with available data.[40] At September’s 7.9 percent unemployment rate, non-elderly Medicaid enrollment would be expected to rise by 3 million to more than 5 million people, Urban Institute projections indicate.[41]

The ACA Medicaid expansion was intended to be implemented nationwide and to fill historical gaps in Medicaid eligibility for low-income adults, with premium tax credits for individual marketplace coverage envisioned as the vehicle for covering moderate-income adults. A June 2012 Supreme Court ruling, however, deemed the Medicaid expansion optional. Thus, in the 14 states that have not adopted the ACA Medicaid expansion, there remains no subsidized health insurance option for low-income adults without a federally recognized disability and without children of their own living in the home. These adults fall into what is widely known as the “coverage gap.”

Who Are Medicaid Expansion Adults?

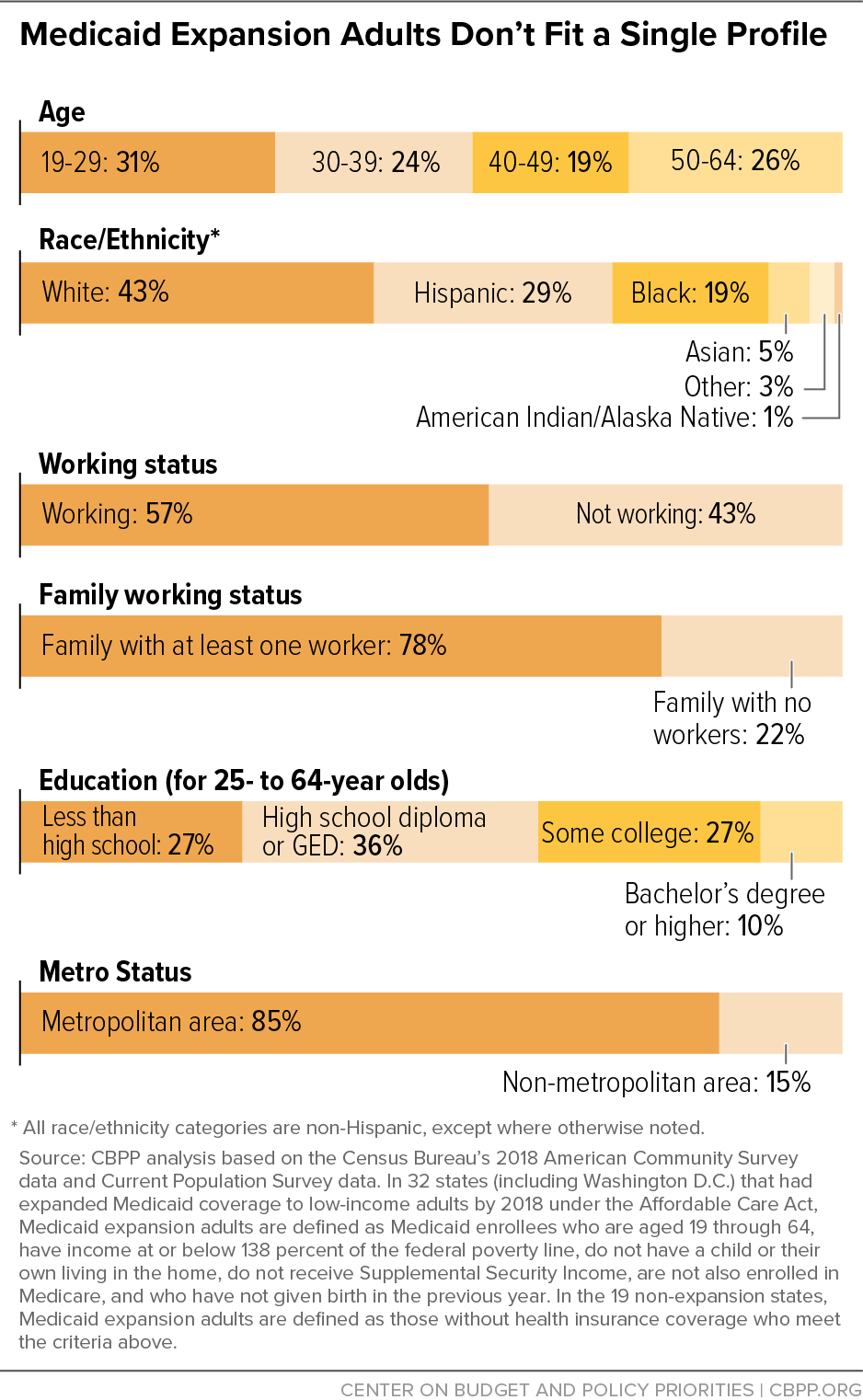

More than 15 million low-income adults were enrolled in Medicaid under the ACA Medicaid expansion in 2019 in the 34 states (including the District of Columbia) that had implemented Medicaid expansion coverage by that time, according to the most recent administrative enrollment data.[42] Roughly three-quarters of those Medicaid expansion enrollees, or nearly 12 million, were low-income adults without children of their own living in the home, with the remainder being parents with income above their state’s eligibility level for parents but at or below 138 percent of the federal poverty line.[43] Likewise, an estimated roughly 6.5 million low-income adults would be eligible for Medicaid if their state expanded Medicaid coverage, including roughly 4.6 million low-income adults without children living in the home.[44] The remainder of this section considers, as one group — which we refer to as “Medicaid expansion adults” — both low-income adults enrolled in the Medicaid expansion who don’t have children of their own in the home and uninsured low-income adults without children of their own in the home who would be eligible if their state expanded Medicaid.[45] (See Figure 6 and Appendix Table 1.)

Age. Medicaid expansion benefits adults of all ages, but particularly young adults and those nearing retirement age. Roughly 31 percent of Medicaid expansion adults are aged 19 to 29, while roughly 26 percent are aged 50 to 64.[46] Medicaid is a needed support for young adults joining the workforce, often in entry-level or low-wage jobs in which employer-sponsored coverage is less available and affordable. Likewise, Medicaid serves many near-elderly adults transitioning out of the workforce and in need of health insurance coverage before reaching Medicare eligibility age.

Race and ethnicity. Medicaid expansion helps to reduce longstanding racial and ethnic disparities in health insurance coverage. More than half of Medicaid expansion adults are people of color, with roughly 29 percent Hispanic, 19 percent Black, and 6 percent Asian American, Native American, or Alaska Native. The uninsured rate gap between white people and people of color, especially Black people, has narrowed significantly since the implementation of the ACA’s coverage provisions, particularly in states that have adopted the Medicaid expansion. Still, racial gaps in coverage and access to care remain even in expansion states, which shows that longstanding economic and health system inequities, as well as limits on immigrants’ eligibility for Medicaid coverage, continue to harm people of color.

Disability status. Nearly 1 in 5 Medicaid expansion adults are living with a disability. Before the implementation of the ACA Medicaid expansion, the primary path for adults with a disability to qualify for Medicaid coverage was to declare an inability to work and go through a disability determination to qualify for SSI. However, many people with disabilities do not meet the strict SSI qualifying standards and so do not qualify for Medicaid based on that criterion.

Medicaid expansion helps address that gap.[47] Some 17 percent of Medicaid expansion adults have at least one condition that impairs daily functioning and their ability to work, including deafness or serious difficulty hearing, blindness or serious difficulty seeing, serious cognitive impairment, serious difficulty walking or climbing stairs, difficulty dressing or bathing, or difficulty doing basic daily activities. Furthermore, an even greater share of Medicaid expansion adults have a serious chronic condition, such as diabetes, asthma, or a mental health condition.[48] Medicaid expansion serves as a vital support for these individuals. For example, employment rates for workers with disabilities have risen in Medicaid expansion states while falling in non-expansion states, research shows.[49]

Workers. Most Medicaid expansion adults are working themselves or are in a working family. Some 57 percent work during the year, with 36 percent working in at least 40 weeks of the year. Furthermore, 78 percent are in a working family, and 63 percent are in a working family with an individual working at least 40 weeks of the year. During the COVID-19 pandemic, Medicaid expansion has been an important source of coverage for essential workers. In 2018, 25 percent of Medicaid expansion adults worked in industries that have been considered essential or front-line industries during the pandemic, including hospital workers, home health aides, food manufacturing workers, grocery store workers, farm workers, employees of pharmaceutical manufacturers, pharmacy workers, bus and truck drivers, and warehouse workers. Among those who are not working, most report potential barriers to work such as illness or disability, caregiving responsibilities, or attending school.[50]

Education. Medicaid expansion helps to reduce health insurance coverage disparities by education levels. Roughly 60 percent of Medicaid expansion adults have not attended college, compared to only 37 percent of non-elderly adults without children with income above the Medicaid income threshold. Although the great majority of Medicaid expansion adults are working or in working families, lower levels of education are associated with lower-wage work, which is less likely to offer affordable employer-sponsored coverage. Medicaid expansion coverage provides critical support; among those who have not attended college, the uninsured rate in Medicaid expansion states fell from 28.3 percent in 2013 to 16.0 percent in 2018.[51]

Geography. Medicaid expansion adults reside in both urban and rural areas. Roughly 85 percent live in a metropolitan area, while 15 percent live in a non-metropolitan area. Medicaid expansion adults are slightly more likely to live in a non-metropolitan area than are non-elderly adults generally.[52] In addition to providing health insurance coverage to low-income adults, Medicaid also supports and sustains hospitals, particularly in rural areas.[53]

Military experience. Some 2.2 percent of non-elderly adult military veterans are Medicaid expansion adults, and they represent 2.0 percent of all Medicaid expansion adults. Like the overall population, most veterans get health coverage through their employer, but large gaps exist for those without access to job-based coverage. While many veterans receive coverage through the Department of Veteran Affairs (VA) health system, some do not qualify, some do not live near a VA facility, and some are not aware of VA care. Medicaid expansion helps provide coverage for the lowest-income veterans without children living in the home. Medicaid reduces unmet health care need and medical debt among veterans and provides needed services such as behavioral health, prescription drug coverage, and home health care services.[54]

Policymakers Should Reject Efforts to Restrict Medicaid Coverage and Access

Despite the Medicaid expansion’s unmitigated success in meeting the health care needs and reducing the financial burdens of low-income adults without children of their own living in the home, debate continues over certain policies related to Medicaid expansion that are clearly harmful to enrollees. Furthermore, the Trump Administration and 18 state attorneys general, led by Texas, have petitioned the Supreme Court to strike down the ACA.[55] An estimated 21.1 million more people would be without health insurance coverage in 2022 were the ACA to be repealed.[56]

Debate also continues about whether to require work of Medicaid expansion adults as a condition of Medicaid eligibility and whether to impose premium and cost-sharing payments on this group. These debates continue both in various states that already have expanded Medicaid coverage under the ACA, such as Arkansas and Indiana, and in states that are considering expanding Medicaid, such as Missouri. Such policies threaten to lessen the benefit of Medicaid expansion and, in states that have adopted the expansion, to reverse some of the recent progress made in covering low-income adults without children of their own living in the home.

Taking coverage away from people who do not meet a work requirement is at odds with Medicaid’s central objective of providing affordable health coverage to people who would not otherwise have it. Yet, nine states have received approval from the Trump Administration to take Medicaid coverage away from adults who do not meet work requirements. In Arkansas, the only state so far to implement work requirements for Medicaid — which since have been suspended by a judicial injunction — it is increasingly clear that the work-requirement policy failed on its own terms.

Some 18,000 Arkansans — nearly 1 in 4 of those subject to the state’s work requirement — lost Medicaid coverage over the course of just the seven months in which the work requirement was enforced. Far more Arkansans lost Medicaid coverage than the number of people in the presumed target group of people who weren’t working and were ineligible for exemptions to the policy. Evidence suggests that many people who were working and many people with serious health needs lost coverage due to red tape. Large numbers of enrollees who lost coverage reported that they did not know about the work requirement or that it applied to them.

Harvard researchers found that among low-income Arkansans subject to the work requirement, the uninsured rate rose, yet there were no significant increases in employment, number of hours worked, or the overall rate of community engagement, including looking for a job, training for a job, or providing community service.[57] Furthermore, Arkansas’ own data show only scant evidence of increased work due to the work requirement.[58]

Six states — Arizona, Indiana, Kentucky, Maine, New Hampshire, and Virginia — have now reversed or suspended their plans to take Medicaid coverage away from people who don’t meet work requirements. These states cited legal challenges and significant pending coverage losses, among other reasons.

On another front, current rules limit premiums and cost sharing in Medicaid to facilitate low-income people’s access to coverage and care, but some states have received waivers to impose premiums. For example, Indiana requires adults enrolled in the state’s Healthy Indiana Plan (HIP, its version of the Medicaid expansion) to pay a monthly premium. Adults with income above the poverty line who don’t pay the premium are locked out from Medicaid coverage for six months, while adults with income below the poverty line are limited to significantly narrower benefit coverage — for example, exclusion of dental and vision care.

The preponderance of research shows that premiums reduce enrollment in coverage and co-payments often prevent Medicaid beneficiaries from accessing needed medical care.[59]

Medicaid is very effective in providing health insurance coverage to the most vulnerable. With the ACA, that includes coverage for low-income adults without children of their own living in the home, a group historically left out of health care coverage assistance efforts. Since the ACA’s major coverage expansions took effect in 2014, Medicaid has helped to reduce the number of uninsured low-income adults without children of their own living in the home from 10.5 million to 5.2 million. Perhaps most striking, rigorous studies have found that Medicaid expansion — and ACA coverage more broadly — save lives.[60] Further progress could be made if the 14 states that have not implemented Medicaid expansion did so, and if states implemented policies that encourage enrollment among eligible individuals rather than policies that discourage enrollment, like work requirements and cost-sharing requirements.

| APPENDIX TABLE 1 | |

|---|---|

| Demographics of the Medicaid Expansion Adult Population | |

| % of total Medicaid expansion adults | |

| Age | |

| 19 to 29 | 31% |

| 30 to 39 | 24% |

| 40 to 49 | 19% |

| 50 to 64 | 26% |

| Race/Ethnicity | |

| White, non-Hispanic | 43% |

| Black, non-Hispanic | 19% |

| Asian, non-Hispanic | 5% |

| American Indian/Alaska Native, non-Hispanic | 1% |

| Other, non-Hispanic | 3% |

| Hispanic | 29% |

| Working Status | |

| Working | 57% |

| Not working | 43% |

| Family Working Status | |

| Family with at least one worker | 78% |

| Family with no workers | 22% |

| Education Level (for 25- to 64-year-olds) | |

| Less than high school | 27% |

| High school diploma or equivalent | 36% |

| Some college | 27% |

| Bachelor’s degree or higher | 10% |

| Metropolitan Status | |

| Living in a metropolitan area | 85% |

| Living in a non-metropolitan area | 15% |

SNAP Restricts Nutrition Assistance for Low-Income Non-Elderly Adults Not Living With Minor Children

By Joseph Llobrera, Catlin Nchako, and Lauren Hall

Introduction

The nation’s largest anti-hunger program, the Supplemental Nutrition Assistance Program (SNAP), provides nutritional support for low-wage working families, unemployed workers and their families, and low-income seniors and people with disabilities. Unlike most means-tested benefit programs, which are restricted to particular categories of low-income individuals, SNAP provides benefits broadly to low-income households that meet the program’s eligibility requirements. SNAP’s coverage of non-elderly adults not living with children at home, however, is heavily restricted, with the result that many such people can secure neither food assistance nor other forms of aid, regardless of how poor they are.

In 2018, SNAP provided food assistance to nearly 5 million individuals aged 18 to 64 who weren’t living with minor children and didn’t have severe disabilities. SNAP requires most of these individuals (those aged 18 to 59 who aren’t employed) to register for work and to accept any reasonable work offer.

But for a subset of this group — individuals aged 18 to 49 who don’t live with minor children and aren’t severely disabled — the eligibility requirements are much more restrictive. With some exceptions, SNAP rules limit benefits for these individuals to just three months in any 36-month period when the individuals are not employed or participating in a work or training program for at least 20 hours a week.[61] States are not obligated to offer the affected individuals a work or training program slot, and most do not. SNAP recipients in this group who don’t have jobs generally have their SNAP benefits cut off after three months, irrespective of whether they are searching diligently for a job or willing to participate in a qualifying work or job training program.

In reality, this rule is thus a time limit on benefits, rather than a work requirement, as it is sometimes described. By restricting access to food assistance benefits, the time limit increases the risk of food insecurity and hunger for adults who are subject to these requirements.

In addition to being a harsh policy that punishes individuals who are willing to work but can’t find employment, the rule is one of the most administratively complex and error-prone aspects of SNAP law. Many states also believe that the rule undercuts their efforts to design meaningful work requirements, because the time limit imposes unrealistic dictates on the types of job training that can qualify. For these reasons, many states have long sought the restriction’s repeal.

The number of households that struggle to put enough food on the table has risen dramatically due to the economic effects of the COVID-19 pandemic. In late November and early December 2020, more than 27 million adults (or 13 percent) reported that their household didn’t get enough to eat sometimes or often in the last seven days. Even after the public health emergency ends, access to SNAP benefits will be critical in reducing the risk of food insecurity and hunger for all households, including those with adults not living with minor children, during what could be a long recovery from the economic damage from the COVID-19 crisis.

Background

SNAP is an effective program, lifting millions out of poverty and improving participants’ food security and health. A CBPP analysis using the government’s Supplemental Poverty Measure (SPM, which counts SNAP benefits as income) and correcting for the underreporting of benefit receipt in government surveys, found that SNAP kept 6.3 million people out of poverty in 2017, and lifted 4 million people out of deep poverty (defined as being below 50 percent of the SPM poverty line).[62]

SNAP enables low-income households to afford more adequate and healthy food. Rigorous studies have yielded compelling evidence that SNAP reduces food insecurity (which can occur when households lack the resources to have consistent access to nutritious food). Research in the past decade has also found associations between SNAP participation and positive health outcomes among non-elderly adults, such as fewer physician visits, fewer days missed due to illness, more positive self-assessments of health status, and reduced likelihood of psychological distress.[63]

SNAP eligibility and benefits are, for the most part, set at the federal level and uniform across the nation, though states have flexibility to tailor certain aspects of the program, such as the value of a vehicle that a household may own and still qualify for benefits. Eligibility and benefits are determined based on a household’s income and expenses. The benefit levels are tied to the Department of Agriculture’s Thrifty Food Plan, a diet plan intended to provide adequate nutrition at minimal cost. In 2019, SNAP helped 35.7 million low-income individuals in a typical month, down from its peak of 47.6 million in 2013.[64] In a typical month in 2019, SNAP benefits averaged about $130 per person per month, or about $4 per person per day or $1.40 per meal.

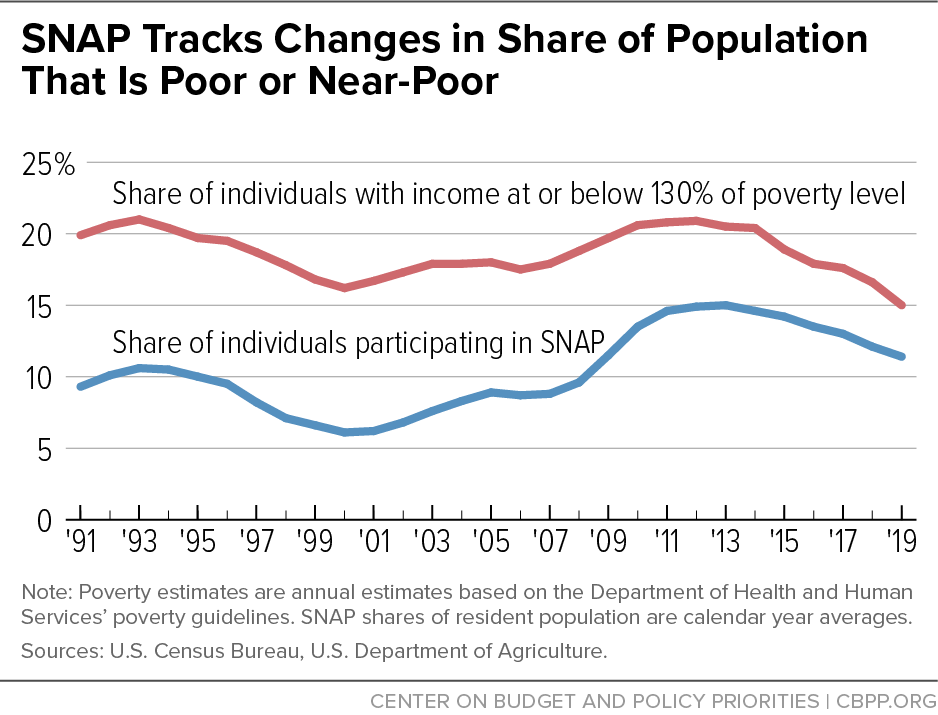

SNAP benefits are an “entitlement,” which means that all applicants who qualify under program rules can receive benefits.[65] After Unemployment Insurance, SNAP is the federal program most responsive to changing economic conditions, expanding to meet rising need during economic downturns and then contracting when conditions improve. By design, SNAP is an effective form of economic stimulus — participation and spending expand automatically when the economy experiences a downturn that raises unemployment and reduces household incomes. This allows SNAP to respond quickly to increased need by providing households with more income to purchase food. (See Figure 7.) During a weak economy, every dollar in new SNAP benefits increases gross domestic product by about $1.50, according to a recent USDA study.[66]

SNAP has expanded at an unprecedented rate during the economic crisis spurred by COVID-19, as millions of people have lost jobs and income and struggled to afford food. Among states that provided preliminary data in late summer, 6 to 7 million people had applied and been approved for benefits since February — a 17 percent increase in participation.[67]

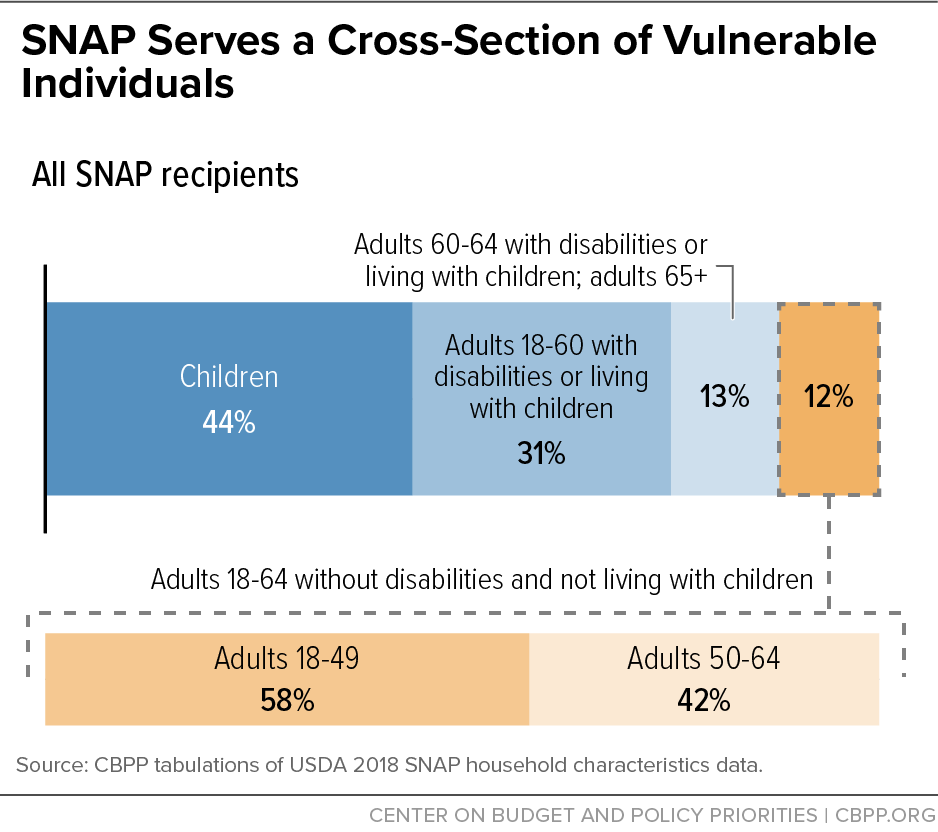

SNAP Supports Millions of Non-Elderly Adults Not Living With Minor Children

Like most income-support programs, SNAP primarily serves three vulnerable groups: low-income children and their parents and other household members (who make up close to 70 percent of SNAP participants); people with disabilities; and the elderly. But unlike other such programs, SNAP also serves a very broad cross-section of those with little income and few resources — including non-elderly adults without minor children or severe disabilities. In 2018, nearly 5 million adults aged 18 to 64 who weren’t living with minor children in the home (and didn’t have a severe disability) participated in SNAP in an average month. This group makes up 12 percent of the SNAP caseload. These individuals lived in households with an average of one household member and average gross income of $376 a month. They received an average monthly SNAP benefit of $183 while participating in SNAP.

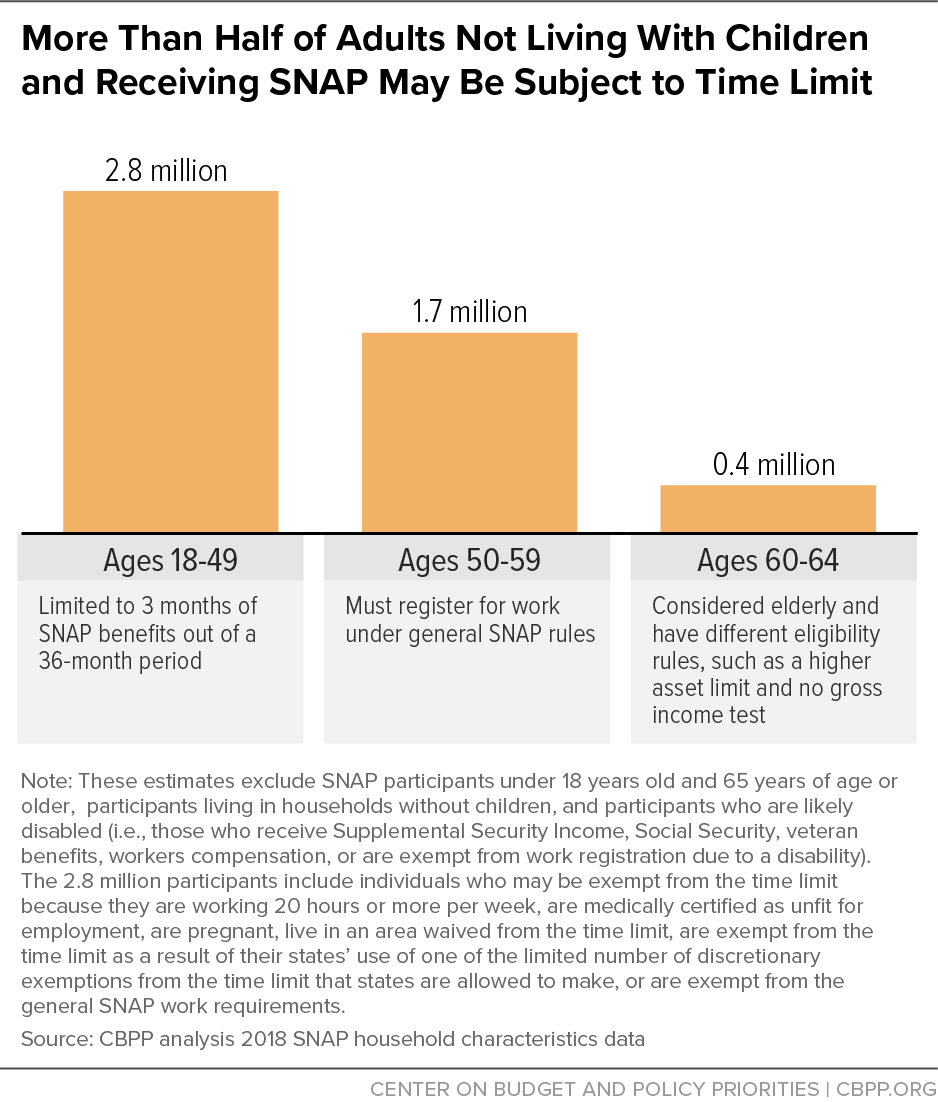

About 1.7 million of these nearly 5 million SNAP recipients were adults aged 50 to 59, who must — unless they are unable to work due to a physical or mental limitation — register for work and accept any reasonable work offer, but otherwise face the same general eligibility rules as most other SNAP participants.[68] Another 400,000 of the aforementioned 5 million adults are aged 60 to 64 (which is considered elderly in SNAP).[69] Households that have elderly or disabled members face somewhat different eligibility rules; they don’t face a gross income limit (they still must meet a “net” or disposable income limit), and asset limits are set somewhere higher for them.

But 58 percent of the 5 million adults aged 18-64 participating in SNAP in 2018 who neither were living with minor children nor had a severe disability — some 2.8 million people — were aged 18 to 49. These individuals face more restrictive eligibility criteria, including the limit on benefit receipt of three months in any 36-month period when they are not employed or participating in a work or training program for at least 20 hours a week (see Figure 8).[70]

Adults Potentially Subject to the Time Limit Are Demographically Diverse; Many Face Barriers to Employment

Most SNAP participants aren’t subject to the time limit because they are children, are age 50 or over, are caring for a child, or have a disability. But the adults who are potentially subject to the time limit are a highly vulnerable group. As noted, there were 2.8 million such individuals, accounting for 7 percent of all SNAP participants, in fiscal year 2018. (See Figure 9.) The rest of this chapter focuses on this group.

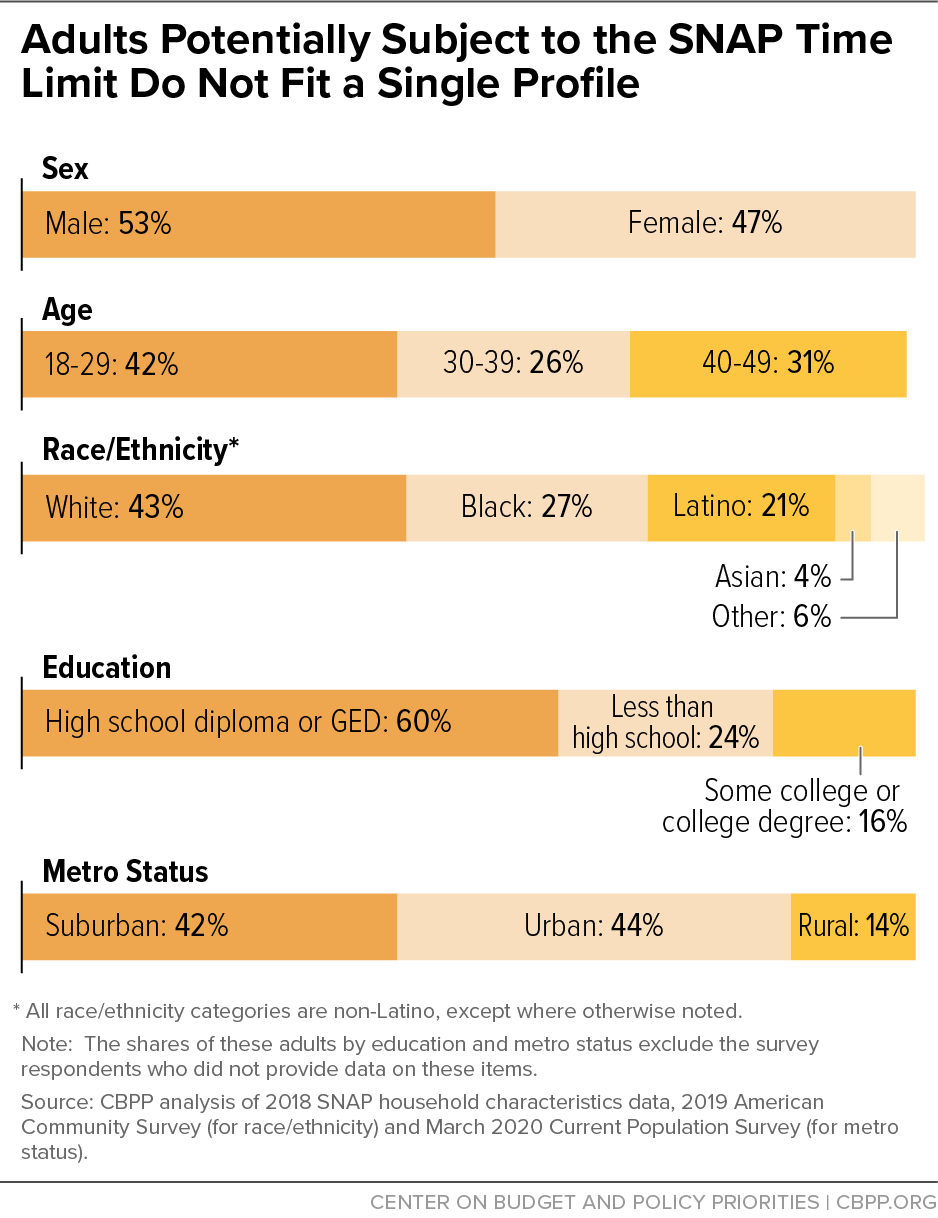

The adults who are potentially subject to the time limit are diverse; no single profile dominates. (See Figure 10.) Nearly half of them (47 percent) are women, and 31 percent are over 40 years old. Among those who reported their education, nearly a quarter (24 percent) have less than a high school education, and 60 percent have only a high school diploma or GED. They live in all areas of the country; among those for whom data on metropolitan status are available, about 44 percent live in urban areas, another 42 percent in suburban areas, and 14 percent in rural areas.[71] Nearly 80 percent live in single-person households. A small share are veterans.[72]

In no small part due to historical factors including ongoing structural racism and discrimination, people of color are more likely to experience hardship, face higher rates of unemployment, and have less access to adequate housing and health care.[73] Food insecurity is part of the nexus of hardship that people of color disproportionately encounter, resulting in lower access to nutritious food or fewer resources to acquire enough food to eat. In 2019, Black- and Latino-headed households were about twice as likely as white-headed households to be considered food insecure, consistent with historical disparities.[74]

SNAP helps reduce racial disparities by targeting benefits to those who need them most. Of the nearly 5 million non-elderly adults not living with minor children who receive SNAP benefits, about a quarter are Black and nearly one-fifth are Latino. Among adults potentially subject to the time limit who report their race, about two-fifths are white, over one-quarter are Black, and about a fifth are Latino. In contrast, the overall U.S. population is about 72 percent white, nearly 13 percent Black, and 18 percent Latino.[75]

Many low-income adults potentially subject to the time limit face multiple challenges to independence and self-sufficiency, including homelessness, physical and mental health limitations, language barriers, unstable employment histories, and criminal records.

Physical and mental health issues can lead to job loss, complicate reentry into the workforce, and limit job opportunities. Moreover, limited education, lack of training, and a sporadic work history often lead to low-skill, low-wage jobs that don’t lift workers out of poverty.

Most Adults Potentially Subject to the Time Limit Are Poor, Attached to the Labor Force

In general, adults potentially subject to the time limit are extremely poor. Like many others, these adults often turn to SNAP when they’re no longer able to make ends meet — for example, when they lose a job, have their hours cut, or can only find low-wage employment. Their household income during the months they participated in SNAP averaged $4,500 in 2018 on an annualized basis (about 37 percent of the poverty level for a single-person household in 2018). Among those in this group who weren’t working at least 20 hours a week and thus faced being cut off of SNAP after three months, average household incomes while on SNAP were lower, at an annualized level of just $2,700 in 2018 (about 22 percent of the poverty level for a single-person household that year).

In addition, only 47 percent of the adults potentially subject to the time limit lived in households with any income.[76] And more than three-quarters lived in households with incomes below half of the poverty level, while nearly all (95 percent) lived in households below 100 percent of the poverty level.

Earnings are the most common income source among adults potentially subject to the time limit. In fiscal year 2018, a little over half (55 percent) of the adults in this group who had any income received some income from earnings in a typical month while on SNAP. About 12 percent received income from General Assistance or Social Security. Even smaller shares received Temporary Assistance for Needy Families (TANF) or Supplemental Security Income (SSI).

While many adults potentially subject to the time limit have limited education, which can restrict their job opportunities, most receiving SNAP who can work do so (otherwise, they would be cut off from SNAP at the three-month point). Although the research evidence is sparse, the evidence that does exist suggests that SNAP participation doesn’t discourage adults potentially subject to the time limit from working when jobs are available.[77]

Many workers turn to SNAP during periods of unemployment, so one would expect employment rates among adults potentially subject to the time limit to be relatively low in the months they are on SNAP. Even so, in a typical month while on SNAP, the share of these adults who are working ranges from a quarter to half.[78]

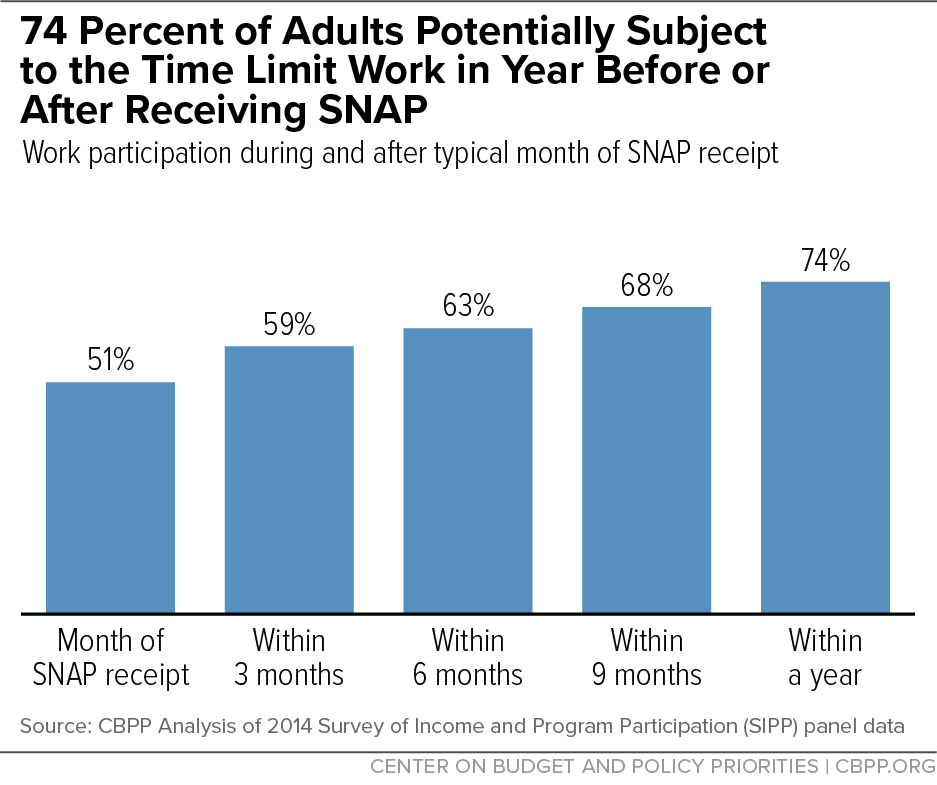

About 74 percent of these adults worked at some point in the year before or year after receiving SNAP. (See Figure 11.) And research conducted on the impact of the time limit following its enactment in 1996 found that three-quarters of all low-income adults who weren’t living with minor children and didn’t have a severe disability (not just those on SNAP) worked in 1997, while 86 percent were in the labor force (that is, either working or actively looking for work).[79]

Most adults potentially subject to the time limit who do work undertake a substantial amount of it. Among those adults who either worked in a typical month while receiving SNAP benefits or worked at some point during the following year, two-thirds worked full time (35 hours a week or more) at least at some point during the year. Over a third (36 percent) worked full time for six months or more of the year. Only 19 percent worked only part time (between 20 and 34 hours per week) for less than six months or worked fewer hours than that.

SNAP Eligibility and the Time Limit

Until the mid-1990s, SNAP was widely available to low-income, non-elderly adults with no children at home and without a severe disability. The Personal Responsibility and Work Opportunity Reconciliation Act of 1996 changed that by imposing the three-months-out-of-36 time limit. As noted, the time limit cuts off benefits after three months for people subject to it who aren’t employed or in a qualifying work or training program for at least 20 hours a week, doing workfare, or living in an area with high unemployment where the three-month limit is temporarily waived.[80]

Since most states don’t provide half-time employment opportunities to SNAP recipients, the only way that a person who can’t find employment can maintain SNAP eligibility during normal economic times generally is to find 20 hours a week of job training or activities under another work program or to find a workfare slot.[81] Job search, the lowest-cost activity for a state to require and monitor, does not count as a qualifying work program.[82]

As noted, states aren’t required to offer these recipients a place in a work or training program for 20 hours a week, and few states do. This leaves it up to individuals who can’t find a job to try to find training or work program openings on their own, which few are able to do, especially since most training programs have insufficient resources to meet demand, resulting in substantial waiting lists. A person who wants to work and is searching diligently but has been unable to find a job, and is willing to participate in job training but has had no opportunity to do so, loses all of their SNAP benefits at the three-month point.

Because this provision denies basic food assistance to people who want to work and will accept any job or work program slot offered, it is effectively a harsh time limit rather than a work requirement as such requirements are commonly understood. Work requirements in economic support programs typically require people to look for work and accept any job or employment program slot that’s offered. But they don’t cut off people who are willing to work and looking for a job simply because they can’t find one. And SNAP itself has separate work requirement authority of that nature for other categories of SNAP participants, under which states can require individuals to participate in job search or a training program but can’t terminate them if no program slot is available.

Studies of people potentially subject to the time limit who exited SNAP in the late 1990s after the time limit went into effect showed that these individuals reported significantly higher rates of food insecurity with hunger, as compared to other low-income adults not living with minor children.[83]

Temporary Waiver of the Three-Month Time Limit

The 1996 law allows states to request a temporary waiver of the three-month limit in areas of the state with elevated unemployment. The time limit provision doesn’t require states to offer workfare programs or job training to people who aren’t able to find a job. As explained above, most states do not offer these programs.

The temporary waiver option for areas with high unemployment has provided significant protection for people who face the three-month limit. Nearly every state suspended the time limit during and after the Great Recession of 2007-2009, due to soaring unemployment, to ensure that poor jobless workers would have access to food.[84] As unemployment rates fell during the economic recovery, fewer areas qualified for these waivers.

Governors across the political spectrum have used this flexibility to secure waivers for high-unemployment areas of their states. Every state except Delaware has used its waiver authority at some point over the last 23 years to temporarily suspend the three-month limit in at least part of the state.

Many of the states that have waivers from the three-month limit do impose other SNAP work requirements on unemployed 18- to 49-year-old adults in the waived areas who aren’t living with minor children, such as requiring them to look for work or participate in a training program if one is available to them. Individuals who don’t comply with those work requirements are subject to having their benefits cut off. But individuals living in areas of a state with waivers are not terminated from SNAP simply for being unemployed and unable to find a slot in a work or training program, as long as they comply with their state’s other applicable work requirements.

Two major events that occurred in 2020 underscore how significant these waivers are to providing food assistance for adults potentially subject to the time limit. A new USDA rule that was slated to take effect on April 1, 2020 would have sharply restricted states’ ability to continue securing waivers to protect unemployed adults from the time limit if they live in areas with elevated unemployment. The rule would have substantially narrowed the criteria that states most commonly use to qualify for waivers, thereby greatly shrinking the number of areas that could qualify for this relief. According to USDA’s own estimates, the rule would have cut off basic food assistance for nearly 700,000 SNAP participants ages 18 through 49 who aren’t living with minor children.[85] On March 13, 2020, a federal district court issued a nationwide injunction blocking the new rule from taking effect until the court decided the case on its merits, and on October 18, the court struck down the rule.[86]

Meanwhile, the Families First Coronavirus Response Act, enacted in March 2020, temporarily suspended the SNAP three-month time limit nationwide as of April 1, 2020. The rapid increase and high levels of unemployment and unemployment claims as a result of the pandemic qualify nearly every state in the country to offer extended unemployment benefits, which also makes states eligible for statewide waivers from the three-month SNAP time limit. This has enabled adults without minor children to continue receiving SNAP benefits during the pandemic.

The Families First provision suspending the time limit is temporary, however. A longer-term solution is needed, given that the economic downturn’s impact on the job market for workers in low-wage occupations will likely endure for a period beyond the end of the pandemic.

Policymakers Should Eliminate or Significantly Revise Time Limit

Low-income adults not living with minor children, who generally have limited education, skills, and employment prospects even in normal economic times, aren’t well served by the nation’s system of economic and health supports. While most who can work do so, many remain extremely poor and struggle to meet basic needs. SNAP is one of the few forms of support available to them. But attempts at the federal and state levels to restrict states’ ability to protect unemployed adults from SNAP’s severe three-month time limit have caused serious hardship.

SNAP was created to protect the well-being and food security of low-income individuals and families by helping them afford a more nutritious diet. By restricting access to food assistance benefits, the time limit increases the risk of food insecurity and hunger for adults not living with minor children. The best course would be for Congress to eliminate the three-month time limit and restore access to food assistance benefits for these individuals on the same basis as applies to other non-elderly or disabled participants.

At a minimum, Congress should revise this rule to better accomplish its stated goal of testing individuals’ willingness to work. For example, Congress could make the three-month limit in a given state contingent on the state offering a qualifying job or training position to all non-disabled adults not living with minor children subject to the limit who don’t otherwise find work. This would establish a principle that indigent individuals shouldn’t be deprived of basic nutritional assistance simply because they can’t find a job or a place in a qualifying training or work program.

| APPENDIX TABLE 1 | ||||||

|---|---|---|---|---|---|---|

| Characteristics of Adult SNAP Participants Not Living With Minor Children Monthly averages | ||||||

| Adult SNAP Participants 18 to 64 Years Old Not Living With Minor Children | Adult SNAP Participants 18 to 49 Years Old Potentially Subject to the Time Limit | Adult SNAP Participants 50 to 64 Years Old Not Living With Minor Children | ||||

| Number (in millions) | Share | Number (in millions) | Share | Number (in millions) | Share | |

| Total | 4.9 | 100% | 2.8 | 100% | 2.1 | 100% |

| Sex: | ||||||

| Male | 2.5 | 50% | 1.5 | 53% | 1.0 | 46% |

| Female | 2.4 | 50% | 1.3 | 47% | 1.1 | 54% |

| Age: | ||||||

| 18-29 | 1.2 | 24% | 1.2 | 42% | - | - |

| 30-39 | 0.8 | 15% | 0.8 | 26% | - | - |

| 40-49 | 0.9 | 18% | 0.9 | 31% | - | - |

| 50-59 | 1.7 | 34% | - | - | 1.7 | 81% |

| 60-69 | 0.4 | 8% | - | - | 0.4 | 19% |

| Race/Ethnicity:* | ||||||

| White, not Latino | 2.3 | 46% | 1.2 | 43% | 1.1 | 46% |

| Black, not Latino | 1.2 | 25% | 0.8 | 27% | 0.5 | 25% |

| Latino (any race) | 1.0 | 19% | 0.6 | 21% | 0.4 | 19% |

| Asian, not Latino | 0.2 | 4% | 0.1 | 4% | 0.1 | 4% |

| Other, not Latino | 0.2 | 5% | 0.2 | 6% | 0.1 | 5% |

| Education:* | ||||||

| Less than high school | 1.1 | 25% | 0.6 | 24% | 0.5 | 25% |

| High school diploma or GED | 2.7 | 59% | 1.6 | 60% | 1.1 | 59% |

| Some college or college degree | 0.7 | 16% | 0.4 | 16% | 0.3 | 17% |

| Individuals with Income From: | ||||||

| Earnings | 1.3 | 25% | 0.8 | 27% | 0.5 | 24% |

| More than 20 hours a week*** | 0.7 | 15% | 0.5 | 16% | 0.3 | 14% |

| Less than 20 hours a week | 0.5 | 10% | 0.3 | 11% | 0.2 | 10% |

| TANF | ** | - | ** | 1% | ** | - |

| Social Security | ** | 1% | ** | - | ** | 1% |

| Supplemental Security Income | ** | - | ** | - | ** | - |

| Unemployment Insurance | 0.1 | 1% | ** | 1% | ** | 1% |

| Veterans Affairs | ** | - | ** | - | ** | - |

| Workers’ compensation | ** | - | ** | - | ** | - |

| Other governmental assistance, including General Assistance and energy assistance | 0.3 | 6% | 0.2 | 6% | 0.1 | 6% |

| Contributions and charity | 0.1 | 2% | 0.1 | 2% | 0.1 | 3% |

| Earned Income Tax Credit | ** | - | ** | - | - | - |