Health Care Lifeline: The Affordable Care Act and the COVID-19 Pandemic

Testimony of Aviva Aron-Dine, Vice President for Health Policy, CBPP

Before the House Energy and Commerce Subcommittee on Health

Chairwoman Eshoo, Ranking Member Burgess, and members of the committee, thank you for the opportunity to testify before you today. My name is Aviva Aron-Dine. I am the Vice President for Health Policy at the Center on Budget and Policy Priorities (CBPP), a non-profit, non-partisan policy institute located in Washington. The Center conducts research and analysis on a range of federal and state policy issues affecting low- and moderate-income families. Previously, I served in government in a number of roles, including as the chief economist at the White House Office of Management and Budget (OMB), as Acting Deputy Director of OMB, and as a Senior Counselor at the Department of Health and Human Services (HHS), where my portfolio included Affordable Care Act (ACA) implementation and Medicaid, Medicare, and delivery system reform policy.

We would be in a far weaker position if the law had been repealed in 2017 or if it is struck down in court, as the Administration and 18 state attorneys general continue to urge. The title of today’s hearing is apt: the ACA, along with the broader Medicaid program, is indeed providing a lifeline for millions during the COVID-19 pandemic and recession. We would be in a stronger position to address these crises had the law been fully implemented nationwide and if policies adopted over the past four years hadn’t chipped away at ACA coverage gains and protections. But we would be in a far weaker position if the law had been repealed in 2017 or if it is struck down in court, as the Administration and 18 state attorneys general continue to urge. Going forward, there are many opportunities for Congress to continue to strengthen our health care safety net for this and future crises.

Coverage Programs Are Growing to Meet Need

As we are all well aware, the COVID-19 pandemic has brought economic devastation in its wake, with tens of millions of people losing their jobs or experiencing sharp reductions in income. Alongside increases in other forms of hardship, the deep recession is putting upward pressure on the uninsured rate, since job losses cause people to lose job-based coverage, and income losses can make it hard for them to pay premiums (whether for employer or individual market health plans). While the precise magnitude is uncertain, data confirm that large numbers of people have lost job-based coverage since the start of the recession.[1] These losses are likely to grow.

Medicaid has long played a critical role in protecting coverage during recessions, especially for children. During the Great Recession period, much of the loss in private coverage was offset by an increase in public coverage, resulting in a net coverage loss of about 5 million people, much smaller than the drop in private coverage. The children’s uninsured rate remained stable (and then fell following the enactment of children’s coverage improvements at the start of 2009).[2]

But prior to the ACA, many of the people most vulnerable to losing their jobs during recessions were excluded from Medicaid. In the typical state, parents were ineligible for Medicaid if their income was above about two-thirds of the poverty line, while adults without children were not eligible for Medicaid at all. For adults with incomes too high to qualify for Medicaid and without coverage through their jobs, individual market plans were generally unsubsidized, expensive, full of benefit gaps, and often unavailable altogether to people with pre-existing health conditions.

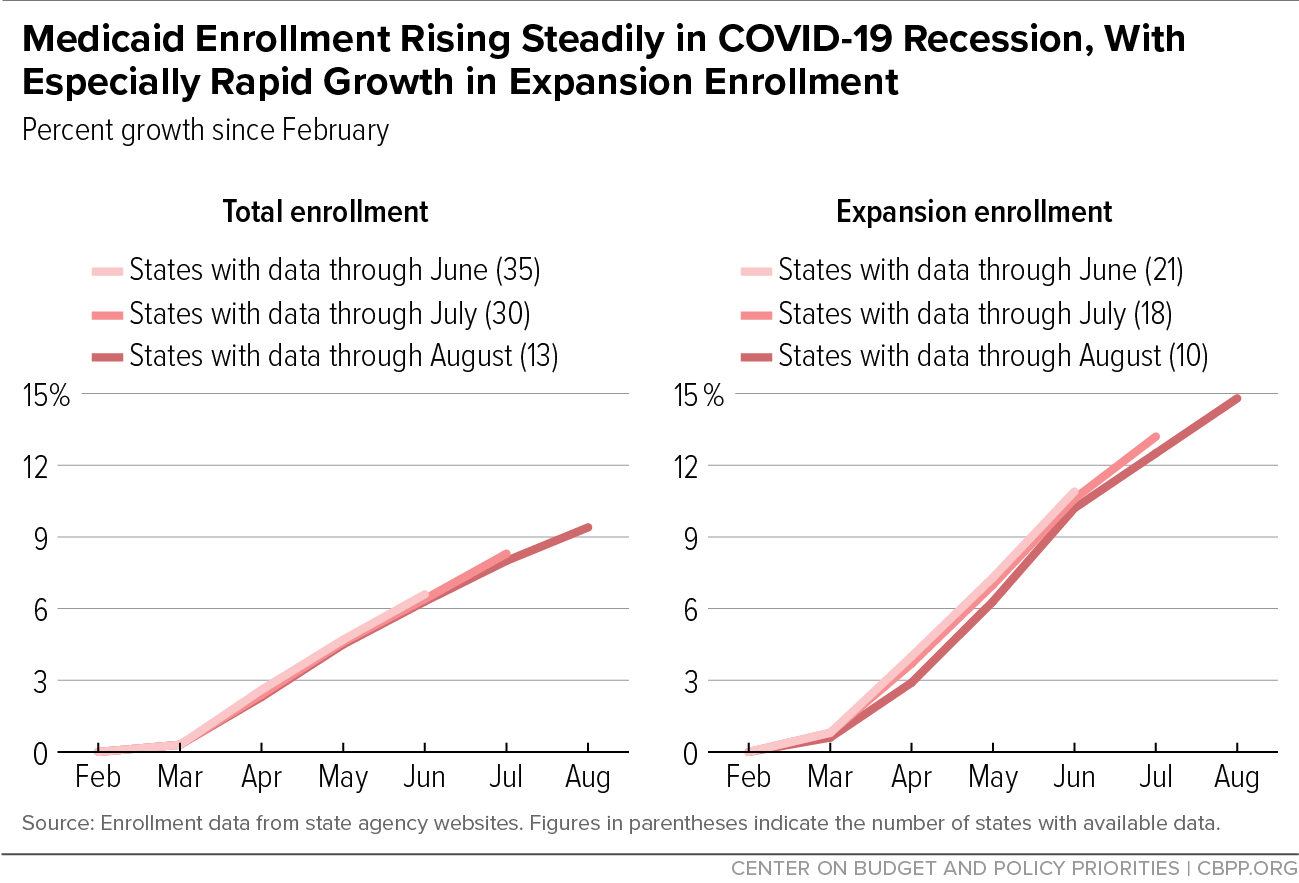

With Medicaid expansion and the ACA marketplaces now offering coverage to this group, we’d expect health coverage programs to be even more responsive to need during this recession than in the past. Data on Medicaid enrollment suggest this is indeed the case. Overall Medicaid enrollment has risen by 8.3 percent through July in 30 states for which the Center has been able to obtain data, and by 9.4 percent through August (with data available for 13 states). Meanwhile, expansion enrollment has risen by 13.2 percent through July across 18 states and by 14.8 percent through August (with data available for ten states). (See Figure 1.)[3] If one were to extrapolate the July figures nationwide, they would imply that total enrollment has risen by about 6 million people, with about a quarter enrolling through expansion.

Evidence suggests mid-year sign-ups for ACA marketplace coverage have risen as well, particularly in state-based marketplaces that created special enrollment opportunities and conducted other outreach during the pandemic.[4] It’s worth noting that, during a recession, we would expect more people to enter the marketplaces after losing employer coverage but would also expect fewer people to enter from Medicaid and more people to shift from marketplace to Medicaid coverage. Thus, total marketplace enrollment might not rise (or rise only a little), even though the marketplace is playing a critical role for people losing employer coverage.

The hope is that, as solid data on 2020 uninsured rates become available, they will confirm that the ACA’s improvements to the health safety net are largely working as intended, and coverage losses will be smaller than during the Great Recession period.[5]

Policies Undermining ACA and Medicaid Have Weakened Response to Crisis

Fewer people had coverage at the start of the pandemic, and more will become uninsured during the downturn, due both to some state policymakers’ refusal to take up the ACA’s expansion of Medicaid and to federal policies that have undermined Medicaid and the ACA marketplaces. The consequence is that more people will go without needed care or will incur unaffordable medical expenses during the crisis. Higher uninsured rates also weaken the response to the pandemic, since some people without health insurance may forgo testing or treatment for COVID-19.[6]

Non-Expansion States Less Prepared for Crisis

Prior to the crisis, 3.9 million people were uninsured due to state decisions not to expand Medicaid, the Urban Institute estimates.[7] Black and Hispanic people are more likely to reside in states that have not expanded Medicaid and are less likely to have other sources of coverage, so they make up a disproportionate share of this group: more than half, compared to less than a third of the U.S. population.

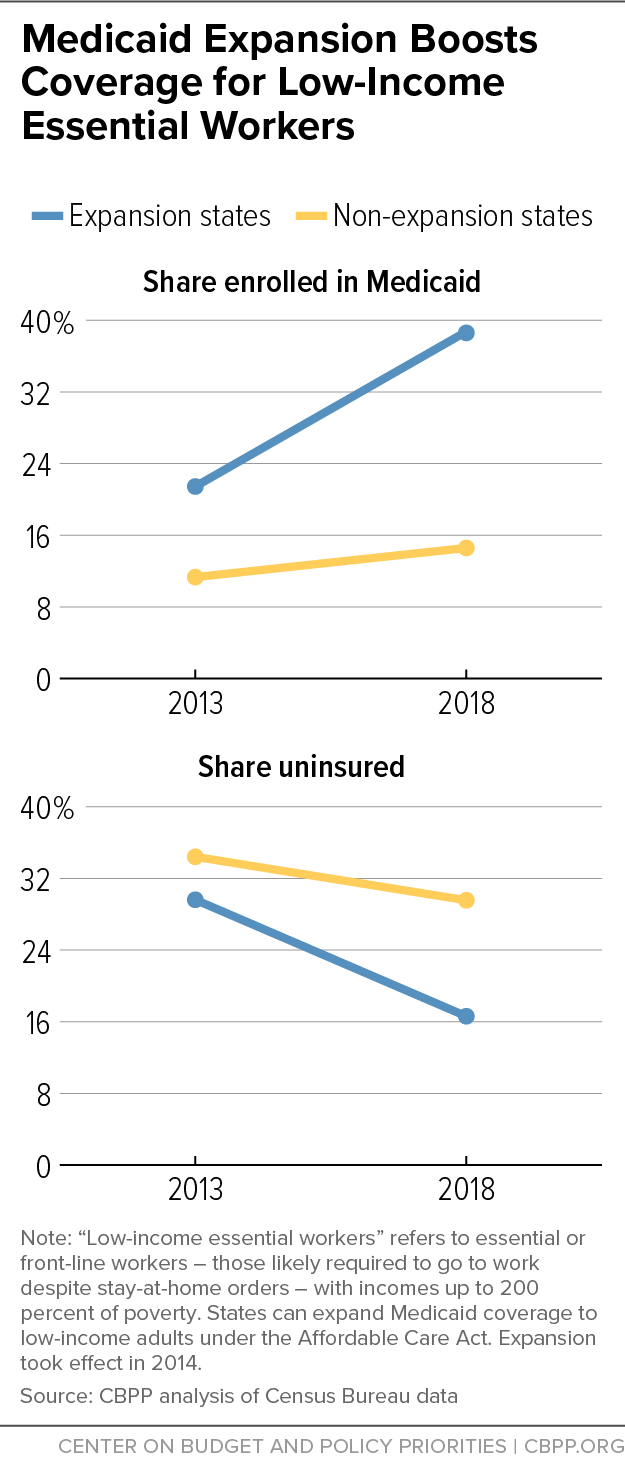

State decisions not to expand have heavily impacted low-income workers such as home health aides, hospital workers, grocery store workers, public transit and truck drivers, food production and pharmaceutical manufacturing workers, pharmacy workers, and warehouse workers — the “essential workers” whose jobs have often put their health at risk during the pandemic. The uninsured rate for low-income people with these jobs was about twice as high in non-expansion states than in expansion states, prior to the pandemic.[8] (See Figure 2.)

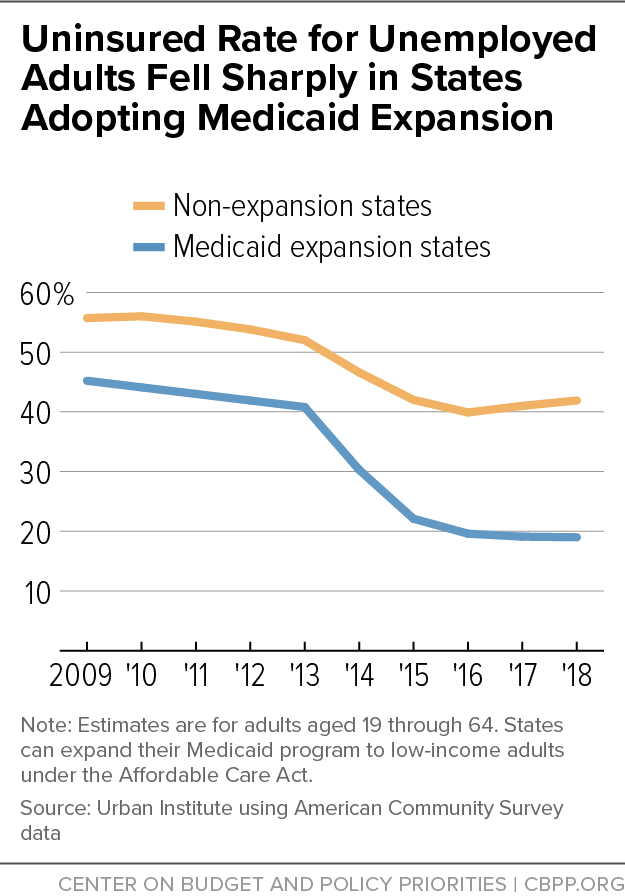

Non-expansion states’ already higher uninsured rates are also likely to increase more during the downturn, since many people losing coverage will fall into the coverage gap, ineligible for Medicaid but with incomes too low to qualify for marketplace premium tax credits. Uninsured rates for unemployed adults fell in both expansion and non-expansion states between 2013 and 2018, due to the availability of marketplace coverage, tut they fell but far more dramatically in expansion states. (See Figure 3.) Prior to the pandemic, more than 40 percent of unemployed adults in non-expansion states were uninsured, over twice the rate in expansion states.[9]

Federal Policies Have Eroded ACA Coverage Gains

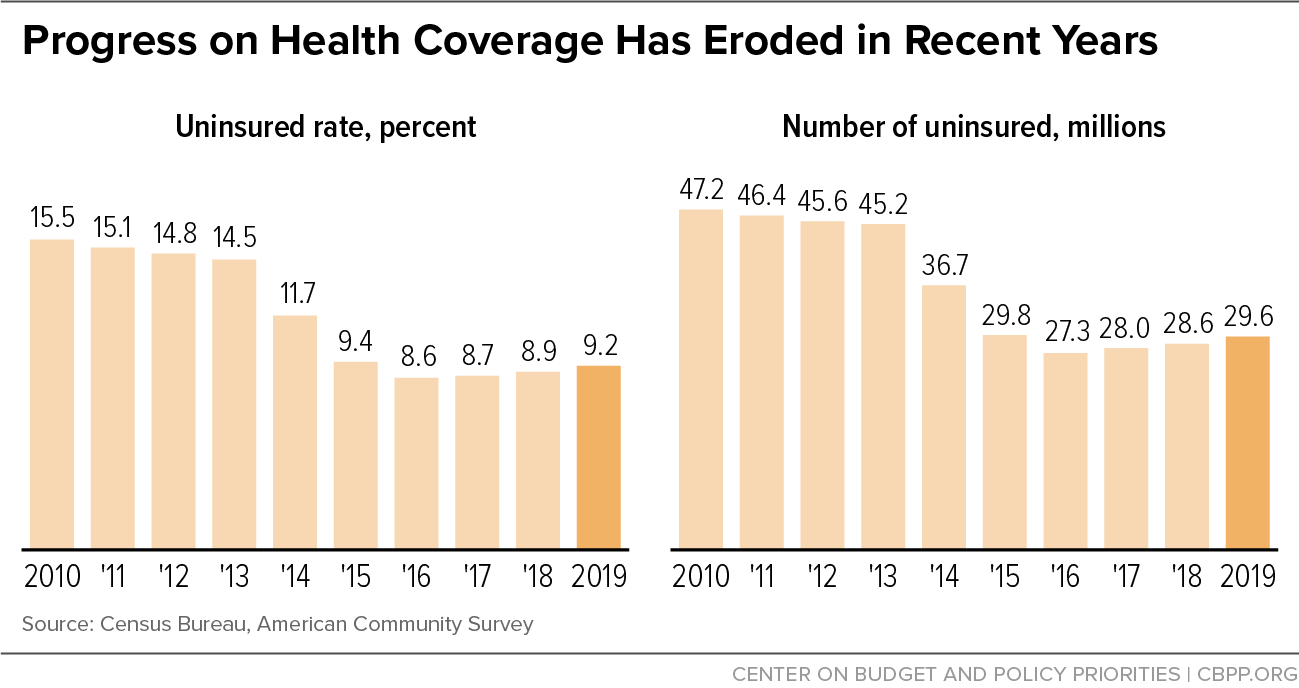

Meanwhile, Census data released last week show that the number of Americans nationwide without health insurance rose by 2.3 million between 2016 and 2019, including an increase of over 700,000 in the number of uninsured children.[10] (See Figure 4.) This erosion happened during a period when the unemployment rate fell substantially and several states were implementing Medicaid expansion, meaning that we would have expected the uninsured rate to fall, or at least remain stable.

Among the policies likely contributing to the increase were:

- The Administration’s policies toward immigrants, including the so-called “public charge” rule. These policies have created a climate of fear among families that include immigrant members, deterring some eligible people from enrolling in Medicaid or marketplace coverage.[11] Hispanic adults, Hispanic children, and children not born in the United States— groups disproportionately affected by this chilling effect — all experienced much larger-than-average increases in uninsured rates in 2019, with Hispanic people experiencing by far the largest increase of any racial or ethnic group.

- State policies, some encouraged or required by the Administration, that have made it harder for people to get and stay covered through Medicaid.[12] For example, states have introduced new procedures requiring people to provide additional paperwork or document eligibility more often.[13] Consistent with administrative data, the Census data show a large decline in Medicaid coverage over the last couple years. They also show an increase in uninsured rates for low-income people in 2019, refuting the claim that Medicaid enrollment declines were largely driven by people finding other coverage.

- The ACA’s individual mandate penalty (the requirement that people have health coverage or pay a fee) was repealed starting in 2019. This likely contributed to the increase in uninsured rates for middle-income people evident in the Census data.

- Cuts to outreach and enrollment assistance. In 2017, the Administration cut outreach and enrollment assistance by 80-90 percent. It has maintained those meager funding levels since, despite new evidence that outreach leads people to enroll in coverage, improving their health and even saving lives.[14]

The Administration also refused to make use of ACA coverage programs to respond to the crisis. In particular, despite recommendations and requests from governors of both parties, insurers, consumer advocates, and others, the Administration chose not to create an emergency special enrollment period for marketplace coverage. This likely reduced the number of people enrolling in HealthCare.gov this spring and summer. It barred the door to people who were already uninsured but experienced income losses that newly qualified them for premium tax credits, while making enrollment more complicated and confusing for people losing job-based coverage (who qualify for a special enrollment period, but one with more complex rules than a blanket emergency option).[15]

Instead, the Administration relied on resources from the CARES Act Provider Relief Fund to reimburse providers for certain COVID-19-related expenses for people who are uninsured. Not only does this approach leave out people with other health care needs, it has also fallen far short of health insurance coverage even for people with COVID-19. Uninsured patients with COVID-19 report incurring large bills for expenses that don’t qualify for reimbursement (such as treatment for other conditions while hospitalized due to COVID) or simply because providers failed to make use of the fund.[16] Meanwhile, the fund had paid out less than $800 million for uninsured patients’ care through mid-September.

ACA Repeal Would Make Things Far Worse

While Administration policies contributed to coverage losses that have eroded about 10 percent of the ACA’s coverage gains, the uninsured rate remains far below pre-ACA levels. But on November 10, the Administration, along with a group of 18 states, will argue before the Supreme Court that it should strike down the entire ACA.[17]

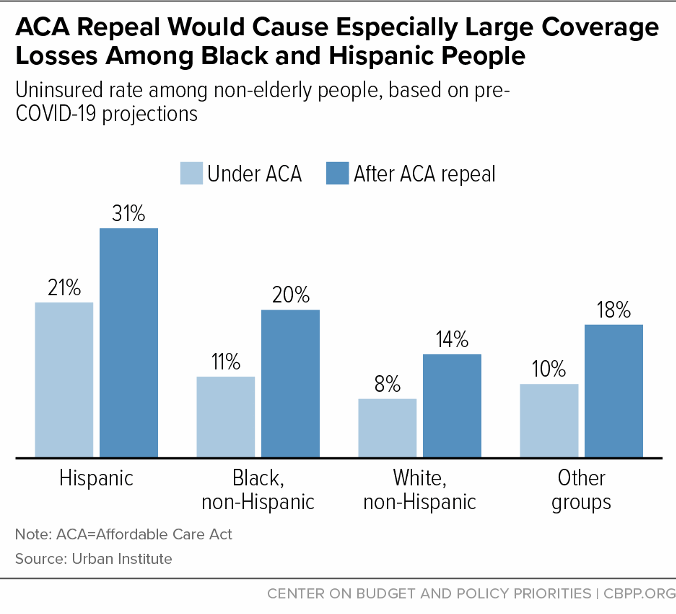

While all racial and ethnic groups would experience large coverage losses, nearly 1 in 10 Black people and 1 in 10 Hispanic people were projected to lose coverage, compared to 1 in 16 whites.A decision striking down the ACA would end Medicaid expansion, eliminate the marketplaces and premium tax credits, end protections for people with pre-existing health conditions, and eliminate the requirement that insurers let young adults remain on their parents plans until age 26. As a result, prior to the pandemic, Urban Institute researchers projected that striking down the law would cause 20 million people to lose coverage, increasing the uninsured rate by nearly two-thirds.[18] While all racial and ethnic groups would experience large coverage losses, nearly 1 in 10 Black people and 1 in 10 Hispanic people were projected to lose coverage, compared to 1 in 16 whites. (See Figure 5.) Today, striking down the law would cause even larger coverage losses, since, as discussed above, the recession is causing many more people to turn to ACA coverage programs for help.

Sudden coverage losses on this scale would be completely unprecedented. And they would be all the more devastating this year or next given that the nation will still be still grappling with the pandemic and many of those losing coverage will also be struggling to afford food, rent, and other necessities due to the economic downturn.

Striking down the ACA would also weaken coverage for those who have it, further undermining the response to the pandemic and worsening access to care and financial hardship more broadly.[19] For example, it would:

- Eliminate the ACA’s prohibitions on denying coverage or charging higher premiums to people with pre-existing conditions, at a time when millions of people will have just acquired a new pre-existing condition: having had COVID-19.

- Allow insurers to rescind coverage if someone develops health problems that could be linked to an undisclosed pre-existing condition, including if a person develops a condition that could be a long-term consequence of having had COVID-19.

- End the requirement that all insurance cover preventive services, including vaccines, without cost sharing, at a time when the nation hopes to be working to vaccinate much or all of the population.

- Allow insurers to impose annual and lifetime limits on benefits and exclude coverage for essential health benefits, such as maternity care, prescription drugs, or substance use treatment.

- Cut funding for Centers for Disease Control and Prevention public health efforts.

Strengthening Health Coverage Programs for This and Future Crises

There are many ways Congress could strengthen health coverage programs for this and future crises.

Additional Coverage Expansions

While the national uninsured rate was 9.2 percent in 2019, seven states and the District of Columbia had uninsured rates of about 5 percent or less: Massachusetts, D.C., Rhode Island, Hawaii, Vermont, Minnesota, Iowa, and New York. All of these states have expanded Medicaid, and many have additional policies in common:[20]

- Most provide some form of additional financial assistance to moderate-income people, on top of the ACA’s premium tax credits.[21] (California is now doing this as well.)

- Most have adopted policies to make it easier for people to get or keep Medicaid and/or marketplace coverage. For example, six have state-based marketplaces, some of which undertake additional outreach compared to HealthCare.gov. Four make it possible for moderate-income people to enroll in coverage year-round, versus just during the annual open enrollment period (or by qualifying for a targeted special enrollment period).[22] And New York provides 12 months of continuous eligibility for both adults and children in Medicaid.

- All of these states have opted to waive restrictions on Medicaid coverage for children who have a lawfully present immigration status, and some have filled in coverage gaps for certain other groups that do not meet the immigration-related eligibility restrictions. (Nationally, uninsured rates for immigrants, including naturalized citizens and non-citizens who are lawfully present, are higher than for other groups.)

- Most prohibit or limit substandard plans that do not meet ACA coverage standards.

These policies are certainly not all that is needed to achieve universal, high-quality health coverage. But federal policies along these lines could be adopted and implemented quickly. They would sharply reduce uninsured rates, both during the current crisis and going forward, and would better prepare us for future economic downturns, by improving coverage options for people without employer plans and by making it easier for people to transition among different forms of coverage. And, if premium tax credit improvements were adopted and implemented quickly, that would also provide timely, targeted support to the economy, by increasing disposable income for moderate-income people very likely to spend the additional funds.

Many of these policies are included in H.R. 1425, the Patient Protection and Affordable Care Enhancement Act, passed by the House in June. That bill would also create new financial incentives for the remaining states to expand Medicaid, and it would make premium tax credits available to middle-income people for whom marketplace premiums cost more than 8.5 percent of income.

Protecting Medicaid By Addressing the State Budget Crisis

Just as important, Congress also needs to prevent the existing health coverage safety net from fraying under strain from the recession. As discussed above, Medicaid is playing a critical role in covering both adults and children impacted by the downturn, through both expansion and the pre-ACA Medicaid program. States have also used Medicaid authorities to meet other needs resulting from the pandemic. For example, some states have increased payments to nursing homes or home- and community-based services (HCBS) providers, broadened access to HCBS, and expanded the use of telehealth.[23]

But increased need for Medicaid coverage and new demands related to the pandemic coincide with a historic state budget crisis. State revenues have already fallen sharply, and states are projecting large budget shortfalls for this and the next fiscal year.[24]

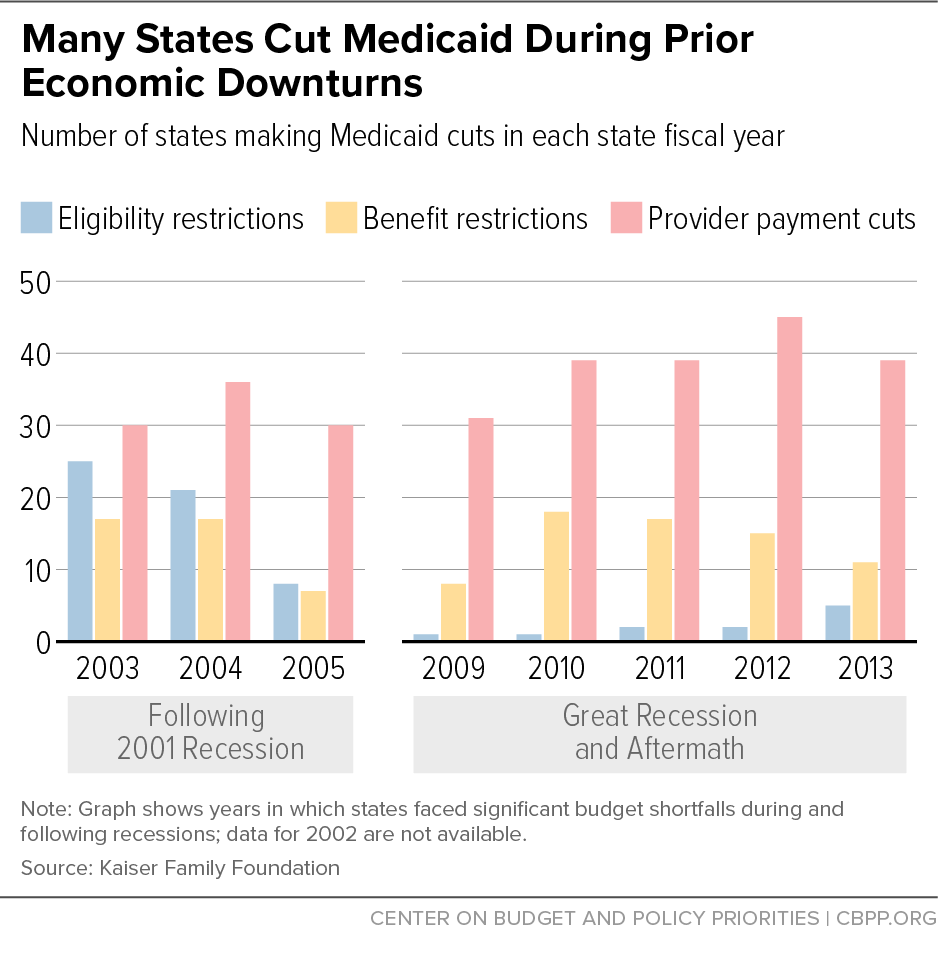

The state budget crisis could easily produce a serious health care crisis as well. During past budget crises, states restricted Medicaid eligibility, including for seniors, people with disabilities, and pregnant women; made it harder for eligible people to get and stay covered; eliminated or cut key benefits; and cut payments to physicians, hospitals, nursing homes, and other providers. (See Figure 6.) They also cut non-Medicaid health programs. For example, during the Great Recession period, state-funded behavioral health programs were often targeted for cuts, with roughly 3 in 4 states cutting mental health budgets in each of 2009, 2010, and 2011.[25]

Early in the pandemic, with bipartisan leadership from this committee, Congress did two very important things. First, it adopted a 6.2 percentage-point increase in the Medicaid match rate (FMAP) for the duration of the public health emergency, providing about $40 billion per year in aid to states.

Second, it tied those additional federal funds to protections for Medicaid beneficiaries. States receiving the additional funds cannot introduce new eligibility restrictions.[26] They also cannot take away people’s coverage during the public health emergency. That continuous coverage requirement is a version of the continuous eligibility policies many states already apply to children, which research has shown improve coverage and access to care by preventing children from losing Medicaid and becoming uninsured due to paperwork barriers and short-term income fluctuations.[27]

But as the state budget crisis continues and more states exhaust options to delay budget cuts, the 6.2 percentage point FMAP increase — about half the maximum increase Congress provided during the Great Recession — is now insufficient. A number of states have already made or are considering Medicaid cuts, including reductions in provider payments, reversals of planned and needed coverage improvements (such as extensions of post-partum Medicaid coverage), and furloughs and hiring freezes impacting eligibility workers, which will likely delay access to coverage for some applicants. States are also cutting behavioral health programs and, even in the midst of the pandemic, are cutting their public health budgets.[28]

Congress should heed recommendations from the National Governors Association, the National Association of State Medicaid Directors, health plans, providers, consumer advocates, and many others and provide additional federal Medicaid funding to help states weather the crisis. The best way to structure this additional assistance would be to tie the amount and duration of the increased federal funding to state unemployment rates and to make these unemployment rate triggers permanent. That way, federal Medicaid match rates would rise automatically in future recessions, then fall back to normal once state economies and budgets have recovered. Legislation introduced in the House (H.R. 6539 and H.R. 6379) and in the Senate (S. 4108) provides a model for how to do this.

In providing additional assistance, Congress should also maintain strong protections for beneficiaries. These “maintenance of effort” protections are critical to ensuring that the additional funding achieves the goal of protecting health coverage during the ongoing public health and economic crises, even as it helps states avoid cuts to Medicaid provider payments, non-Medicaid health programs, education, and other critical services.

End Notes

[1] Kaiser Family Foundation analysis, drawing on data from the National Association of Insurance Commissioners, shows a 1.3 percent drop in fully insured group market coverage from March through June. If extrapolated to the full market, that would imply a roughly 2 million drop in employer coverage, though coverage losses among workers at self-insured firms may have been smaller. Urban Institute analysis of Census Household Pulse survey data shows a 3.3 million drop in job-based coverage from late April/early May through July, although the underlying data are quite noisy. The drop in job-based coverage is likely to grow over time, because people who lose their jobs do not always immediately lose their coverage and because a larger share of early job losses during the pandemic were temporary layoffs, while a larger share of subsequent job losses were permanent. Even so, coverage losses may be smaller than some initially expected, because job losses in the recession to date have been unusually concentrated among low-wage workers who did not have coverage to start with. See Cynthia Cox and Daniel McDermott, “What Have Pandemic-Related Job Losses Meant for Health Coverage?” Kaiser Family Foundation, September 11, 2020, https://www.kff.org/policy-watch/what-have-pandemic-related-job-losses-meant-for-health-coverage/ and Anuj Gangopadhyaya, Michael Karpman, and Joshua Aarons, “As the COVID-19 Recession Extended into the Summer of 2020, More Than 3 Million Adults Lost Employer-Sponsored Health Insurance Coverage and 2 Million Became Uninsured,” Urban Institute, September 2020, https://www.urban.org/sites/default/files/publication/102852/as-the-covid-19-recession-extended-into-the-summer-of-2020-more-than-3-million-adults-lost-employer-sponsored-health-insurance-coverage-and-2-million-became-uninsured.pdf.

[2] These calculations are based on the National Health Interview Survey.

[3] These figures update those published in Matt Broaddus, “Medicaid Enrollment Continues to Rise,” Center on Budget and Policy Priorities, September 9, 2020, https://www.cbpp.org/blog/medicaid-enrollment-continues-to-rise. Methodology and sources can be found in Aviva Aron-Dine, Kyle Hayes, and Matt Broaddus, “With Need Rising, Medicaid Is At Risk for Cuts,” Center on Budget and Policy Priorities, July 22, 2020, https://www.cbpp.org/research/health/with-need-rising-medicaid-is-at-risk-for-cuts.

[4] Sarah Lueck and Matt Broaddus, “Emergency Special Enrollment Period Would Boost Health Coverage Access at a Critical Time,” Center on Budget and Policy Priorities, July 30, 2020, https://www.cbpp.org/research/health/emergency-special-enrollment-period-would-boost-health-coverage-access-at-a-critical.

[5] Of the established federal health insurance surveys, the first data on post-pandemic coverage will come from the National Health Interview Survey, which generally releases second-quarter estimates in mid-November. While the Census Household Pulse survey (a new survey introduced during the pandemic) provides an initial glimpse at trends since late April/early May, the health coverage numbers in the new survey have fluctuated significantly from week to week. However, the Urban Institute analysis of these data referenced above does find that increases in public coverage have offset well over half the loss in job-based coverage among adults in states that have expanded Medicaid, which is a larger share than for adults nationwide during the Great Recession.

[6] An April Gallup survey found that 14 percent of Americans would forgo care for COVID-19 symptoms due to cost, with higher percentages for groups with higher uninsured rates. Dan Witters, “In U.S., 14% With Likely COVID-19 to Avoid Care Due to Cost,” Gallup, April 28, 2020, https://news.gallup.com/poll/309224/avoid-care-likely-covid-due-cost.aspx.

[7] Michael Simpson, “The Implications of Medicaid Expansion in the Remaining States: 2020 Update,” Urban Institute, June 2020, https://www.urban.org/sites/default/files/publication/102359/the-implications-of-medicaid-expansion-in-the-remaining-states-2020-update_0.pdf.

[8] For an explanation of how we define low-income essential workers, see Jesse Cross-Call and Matt Broaddus, “States That Have Expanded Medicaid Are Better Positioned to Address COVID-19 and Recession,” Center on Budget and Policy Priorities, July 14, 2020, https://www.cbpp.org/research/health/states-that-have-expanded-medicaid-are-better-positioned-to-address-covid-19-and.

[9] Anuj Gangopadhyaya and Bowen Garrett, “Unemployment, Health Insurance, and the COVID-19 Recession,” Urban Institute, April 2020, https://www.urban.org/sites/default/files/publication/101946/unemployment-health-insurance-and-the-covid-19-recession_1.pdf.

[10] For additional discussion, see Matt Broaddus and Aviva Aron-Dine, “Uninsured Rate Rose Again in 2019, Further Eroding Earlier Progress,” Center on Budget and Policy Priorities, September 15, 2020, https://www.cbpp.org/research/health/uninsured-rate-rose-again-in-2019-further-eroding-earlier-progress.

[11] See for example Hamutal Bernstein, Dulce Gonzalez, Michael Karpman, and Stephen Zuckerman, “Amid Confusion over the Public Charge Rule, Immigrant Families Continued Avoiding Public Benefits in 2019,” Urban Institute, May 18, 2020, https://www.urban.org/research/publication/amid-confusion-over-public-charge-rule-immigrant-families-continued-avoiding-public-benefits-2019.

[12] For further discussion, see Matt Broaddus, “Research Note: Medicaid Enrollment Decline Among Adults and Children Too Large to Be Explained by Falling Unemployment,” Center on Budget and Policy Priorities, July 17, 2019, https://www.cbpp.org/research/health/medicaid-enrollment-decline-among-adults-and-children-too-large-to-be-explained-by and Samantha Artiga and Olivia Pham, “Recent Medicaid/CHIP Enrollment Declines and Barriers to Maintaining Coverage,” Kaiser Family Foundation, September 24, 2019, https://www.kff.org/medicaid/issue-brief/recent-medicaid-chip-enrollment-declines-and-barriers-to-maintaining-coverage/.

[13] See for example, Lexi Churchill, “The Trump Administration Cracked Down on Medicaid. Kids Lost Insurance,” Pro Publica, October 31, 2019, https://www.propublica.org/article/the-trump-administration-cracked-down-on-medicaid-kids-lost-insurance.

[14] Jacob Goldin, Ithai Z. Lurie, and Janet McCubbin, “Health Insurance and Mortality: Experimental Evidence from Taxpayer Outreach,” National Bureau of Economic Research Working Paper 26533, December 2019, https://www.nber.org/papers/w26533.

[15] See Sarah Lueck and Matt Broaddus, “Emergency Special Enrollment Period Would Boost Health Coverage Access at a Critical Time,” Center on Budget and Policy Priorities, July 30, 2020, https://www.cbpp.org/research/health/emergency-special-enrollment-period-would-boost-health-coverage-access-at-a-critical.

[16] Abby Goodnough, “Trump Program to Cover Uninsured COVID-19 Patients Falls Short of Promise,” New York Times, August 29, 2020, https://www.nytimes.com/2020/08/29/health/Covid-obamacare-uninsured.html.

[17] For background on the lawsuit, see Center on Budget and Policy Priorities, “Suit Challenging ACA Legally Suspect But Threatens Loss of Coverage for Tens of Millions,” updated August 21, 2020, https://www.cbpp.org/research/health/suit-challenging-aca-legally-suspect-but-threatens-loss-of-coverage-for-tens-of.

[18] Jessica Banthin et al., “Implications of the Fifth Circuit Decision in Texas v. United States,” Urban Institute, December 2019, https://www.urban.org/sites/default/files/publication/101361/implications_of_the_fifth_circuit_court_decision_in_texas_v_united_states_final_121919_v2.pdf.

[19] For additional discussion, see Tara Straw and Aviva Aron-Dine, “Commentary: ACA Repeal Even More Dangerous During Pandemic and Economic Crisis,” Center on Budget and Policy Priorities, June 24, 2020, https://www.cbpp.org/health/commentary-aca-repeal-even-more-dangerous-during-pandemic-and-economic-crisis

[20] These policies are, of course, not the only reasons for these states’ low uninsured rates, but examining the policies the states have in common is still instructive.

[21] Massachusetts and Vermont provide additional financial assistance to lower-income marketplace consumers; D.C. extends Medicaid eligibility above 138 percent of the poverty line; and Minnesota and New York provide more affordable coverage to lower-income people through Basic Health Programs. Hawaii, meanwhile, has more stringent requirements for employers to offer coverage than apply nationally under the ACA.

[22] For a discussion of Massachusetts’ approach and implications for federal policy, see Sarah Lueck, “Proposed Change to ACA Enrollment Policies Would Boost Insured Rate, Improve Continuity of Coverage,” Center on Budget and Policy Priorities, June 5, 2019, https://www.cbpp.org/research/health/proposed-change-to-aca-enrollment-policies-would-boost-insured-rate-improve.

[23] Jessica Schubel, “States Are Leveraging Medicaid to Respond to COVID-19,” Center on Budget and Policy Priorities, updated September 2, 2020, https://www.cbpp.org/research/health/states-are-leveraging-medicaid-to-respond-to-covid-19.

[24] See, for example, Lucy Dadayan, “State Tax Revenues Surged in July 2020, But Cumulatively Are Down During COVID-19 Period,” Urban Institute, September 16, 2020, https://www.urban.org/sites/default/files/2020/09/16/monthlystrh_july2020.pdf and Center on Budget and Policy Priorities, “States Grappling with Hit to Tax Collections,” updated August 24, 2020, https://www.cbpp.org/research/state-budget-and-tax/states-grappling-with-hit-to-tax-collections.

[25] Aviva Aron-Dine et al., “Larger, Longer-Lasting Increases in Federal Funding Needed to Protect Coverage,” Center on Budget and Policy Priorities, May 5, 2020, https://www.cbpp.org/research/health/larger-longer-lasting-increases-in-federal-medicaid-funding-needed-to-protect.

[26] A similar rule in place during the Great Recession explains why far fewer states restricted eligibility during the Great Recession than during the shallower recession of the early 2000s, as shown in Figure 6. Aviva Aron-Dine, “Medicaid ‘Maintenance of Effort’ Protections Crucial to Preserving Coverage,” Center on Budget and Policy Priorities, May 13, 2020, https://www.cbpp.org/blog/medicaid-maintenance-of-effort-protections-crucial-to-preserving-coverage.

[27] Judith Solomon, “Continuous Coverage Protections in Families First Act Prevent Coverage Gaps by Reducing ‘Churn,’” Center on Budget and Policy Priorities, July 16, 2020, https://www.cbpp.org/research/health/continuous-coverage-protections-in-families-first-act-prevent-coverage-gaps-by.

[28] Aviva Aron-Dine, Kyle Hayes, and Matt Broaddus, “With Need Rising, Medicaid Is at Risk for Cuts,” Center on Budget and Policy Priorities, July 22, 2020, https://www.cbpp.org/research/health/with-need-rising-medicaid-is-at-risk-for-cuts.

More from the Authors