Commentary: ACA Repeal Even More Dangerous During Pandemic and Economic Crisis

Despite the COVID-19 pandemic and resulting major recession, the Trump Administration and 18 state attorneys general, led by Texas, continue to petition the Supreme Court to strike down the entire Affordable Care Act (ACA).[1] President Trump has been adamant about his commitment to ACA repeal, recently asserting that a Court decision striking down the law would be “a big WIN” for the country.[2] While the legal arguments against the law are extremely weak, the threat to the ACA has likely grown with the death of Justice Ruth Bader Ginsburg and the President’s nomination of a judge who has been critical of the Supreme Court’s reasoning for upholding the ACA in prior cases.[3]The stakes in this case... are even higher now amidst a global pandemic and an economic crisis that has caused more people to lose health insurance and become eligible for help from the ACA.The stakes in this case, always extraordinarily high, are even higher now amidst a global pandemic and an economic crisis that has caused more people to lose health insurance and become eligible for help from the ACA.

The Supreme Court will likely decide the case in the spring of 2021, when the unemployment rate is expected to still be about 9 percent and likely amid a continuing COVID-19 public health crisis.[4] Before the crisis, ACA repeal was expected to cause 20 million people to lose coverage; millions more would likely lose coverage if the law were struck down during a recession, with commensurately larger impacts on access to care, financial security, health outcomes, and racial disparities in coverage and access to care. Striking down the ACA would also impede efforts to address the public health crisis. And eliminating the ACA’s protections for people with pre-existing conditions could make it harder for the more than 7 million people who’ve had COVID to obtain affordable, comprehensive coverage in the future.

Repeal Lawsuit Lacks Legal Basis

The lawsuit’s argument is “absurd,” “ludicrous,” “cringeworthy,” “far-fetched,” and “flimsy,” in the words of legal experts across the political spectrum.[5] The crux of Texas’ argument is that the Supreme Court’s 2012 decision in National Federation of Independent Business v. Sebelius upheld the ACA’s individual coverage requirement under Congress’ taxing power, and the 2017 tax law zeroed out that tax penalty. Without the tax in place, they claim, the coverage requirement is unconstitutional, making the rest of the ACA also unlawful. This argument ignores Congress’ choice to leave the ACA intact when it zeroed out the tax penalty and the Court’s well-established doctrine that a law should be left as intact as possible, even if one of its provisions is struck down.

The Trump Administration has repeatedly refused to defend the ACA, first asking the courts to strike down its protections for people with pre-existing conditions, and then endorsing striking down the entire law. Its initial decision not to defend the law apparently led two senior career attorneys to withdraw from the case and one to resign.[6]

Despite the weakness of the case, District Court Judge Reed O’Connor ruled in favor of the plaintiff states and invalidated the entire ACA in December 2018 in a decision that was panned even among the ACA’s harshest critics, from the Wall Street Journal editorial board and National Review to legal scholars who had advocated for striking down the law in previous Supreme Court cases.[7] In December 2019 the Fifth Circuit concurred that the individual mandate was unconstitutional but sent the case back to Judge O’Connor to determine which, if any, portions of the ACA could remain. A group of Democratic attorneys general led by California intervened to defend the law in court following the Trump Administration’s refusal to do so.

Following the Fifth Circuit decision, these attorneys general appealed to the Supreme Court, which has agreed to hear the case, now called California v. Texas, on November 10.

Dozens of insurers, health care providers, economists, policy experts, and legal scholars have filed briefs at the Supreme Court cataloguing the harmful effects of repeal and rebutting the specious arguments against the law.[8]

Coverage Losses Would Be Larger During a Deep Recession

The consequences of repeal by judicial fiat would be dire for many millions of people. Striking down the ACA would increase the number of uninsured people by 20 million, the Urban Institute estimated in December.[9] These coverage losses would stem primarily from eliminating the ACA’s expansion of Medicaid to low-income adults and its premium tax credits to help moderate-income people afford individual market health insurance.

But this estimate doesn’t account for the historic public health and economic crises that have made more people eligible for help from the ACA. Forecasts predict that economic hardship will continue through next spring, when the Supreme Court will render its decision. At that time, with unemployment projected to be about 9 percent and more people relying on Medicaid expansion and the marketplace’s premium assistance, many more people could lose coverage than projected pre-crisis.

Medicaid enrollment has risen significantly since the start of the crisis, with especially large increases in Medicaid expansion enrollment.[10] The Congressional Budget Office now expects an additional 2 million people to have coverage through Medicaid expansion in 2021, compared to its pre-crisis projections.[11]

In the marketplaces, states that responded to the pandemic by creating emergency special enrollment periods open to all who apply saw strong demand. And more people who have lost job-based health insurance will likely turn to the marketplaces for coverage during the 2021 open enrollment period.[12]

In addition, the ACA provision allowing young adults to stay on their parents’ health plans until they turn 26 is likely taking on greater importance during the recession. Four in ten young workers (ages 18 to 24) lost their jobs during the pandemic, as of May.[13]

A large body of research finds that the coverage gains caused by the ACA have improved access to care; improved financial security, including by reducing medical debt, improving access to credit, and reducing housing evictions; and improved health outcomes, with strong evidence that both Medicaid expansion and coverage through the ACA marketplaces save lives.[14] Reversing these coverage gains would therefore be expected to worsen all of these outcomes. And during the recession, with even more people losing Medicaid expansion and marketplace coverage than had gained it through 2019, the adverse impact would be even greater.

Repeal Would Worsen Racial Disparities

Striking down the ACA would also worsen health disparities. Prior to the ACA, uninsured rates for Black and Hispanic people were much higher than for white people, reflecting economic gaps and barriers to accessing coverage that are a legacy of systemic racism, barriers in access to coverage for immigrants and their family members, and other economic and health system inequities. Black and Hispanic people were also more likely to avoid using health care due to cost. While the ACA did not eliminate these gaps, it narrowed disparities in both coverage and access to care significantly, and striking down the law would widen them once again.[15]

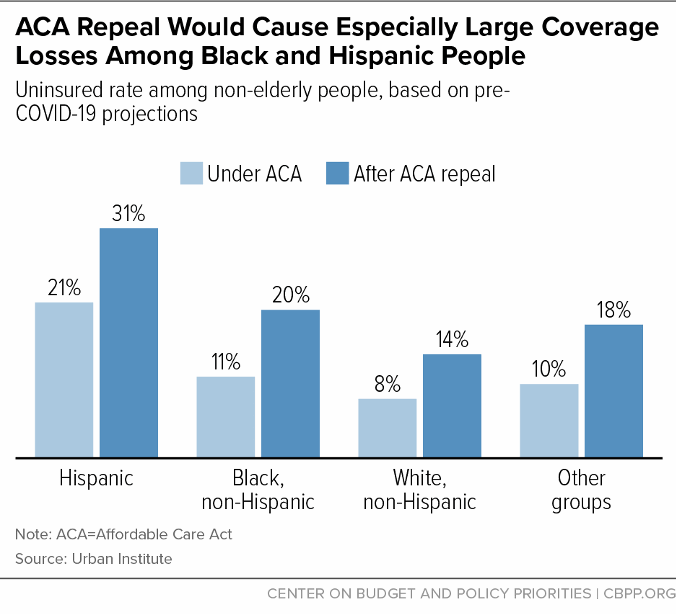

In their pre-crisis forecast, the Urban Institute researchers projected that, among the non-elderly, ACA repeal would cause nearly 1 in 10 Black people and 1 in 10 Hispanic people to lose coverage, compared to about 1 in 16 white people. The result is that about 1 in 5 Black people and nearly 1 in 3 Hispanic people would be uninsured. (See Figure 1.)

The COVID-19 economic crisis is likely to exacerbate the lawsuit’s impact on health disparities. During the Great Recession (which predated the ACA), gaps in uninsured rates and access to care between white people and people of color, particularly Black people, widened. Between 2007 and 2010, the uninsured rate rose by 24 percent among Black people, compared to 9 percent for white people. (The uninsured rate rose only slightly for Hispanic people.) The share of people skipping needed care due to cost rose by 45 percent for Black people, 23 percent for Hispanic people, and 13 percent for white people.[16]

ACA coverage programs are likely to mitigate these increases during this recession, since they will make subsidized coverage available to most people who lose their jobs or experience sharp reductions in income. But if the law is repealed, widening economic gaps due to the recession may once again translate into widening gaps in uninsured rates and access to health care.[17]

Repeal Would Impede Efforts to Address Public Health Crisis and Fallout

While it is difficult to predict where the public health crisis will stand in the spring of 2021, it is clear that repealing the ACA would make it harder to resolve the crisis and to deal with the fallout. Judicial repeal would end not only the ACA’s major coverage expansions but other important protections as well, harming tens of millions of people who would remain insured. Of particular concern during and in the wake of a pandemic, a Trump Administration victory would:

- Eliminate the ACA’s prohibitions on denying coverage or charging higher premiums to people with pre-existing conditions, at a time when more than 7 million people will have just acquired a new pre-existing condition: having had COVID-19.[18] People experiencing long-term health effects from COVID-19 could have coverage for all of those related conditions excluded or be denied coverage altogether.[19]

- Allow insurers to rescind coverage if someone develops health problems linked to an undisclosed pre-existing condition. For example, an insurer could cancel the insurance of someone with an expensive heart or lung condition if it turns out they have coronavirus antibodies, since COVID-19 could have exacerbated the condition, even if the person didn’t know they had been exposed to the virus.

- End the requirement that all insurance cover preventive services, including vaccines, without cost sharing, just as the nation hopes to be working to vaccinate much or all of the population.

- Allow insurers to impose annual and lifetime limits on benefits and exclude certain essential health benefits, at a time when people may still be facing potentially catastrophic COVID-19-related medical costs or may be managing yet unknown, long-lasting effects of the virus.[20]

- Cut funding for Centers for Disease Control and Prevention public health efforts.

The coverage losses from ACA repeal would themselves also make it harder to combat the pandemic, since people who are uninsured may forgo testing or treatment for COVID-19 due to concerns that they cannot afford it, endangering their health while slowing detection of the virus’ spread.

Moreover, these coverage losses would lead to sharp spikes in uncompensated care costs. Since the ACA’s major coverage provisions took effect, uncompensated care costs have fallen by 38 percent as a share of hospital budgets (more in states that adopted expansion).[21] Uncompensated care costs have also fallen for other providers, and states and localities have seen reduced costs for uncompensated care at public hospitals and for programs that reimburse providers for some of their uncompensated care. The large increases in these costs as a result of the lawsuit would come at a time when providers will likely still be reeling from large revenue losses due to delayed and forgone care during the pandemic, which are threatening the survival of some community-based providers and safety net and rural hospitals.[22] And the added costs would add to the financial burden on states and localities during an unprecedented state budget crisis.

If the courts threw out only parts of the law, the result would still be devastating. For example, allowing insurers to again discriminate based on health status would jeopardize coverage for millions, perhaps including people with a COVID-19 diagnosis, who could be charged more, denied coverage for certain diagnoses, or blocked from individual market coverage altogether. Eliminating ACA protections could also let insurers charge higher premiums to women and people in certain occupations and reimpose pre-existing condition exclusions in employer coverage. And it would make premium tax credits nearly impossible to administer, raising questions about how millions of low- and moderate-income people could continue to afford coverage.[23]

The Administration and state attorneys generals’ effort to repeal the ACA through the courts has always threatened health and financial hardship for millions. Doubling down on it in a time of crisis only adds to what would be devastating results.

End Notes

[1] “Suit Challenging ACA Legally Suspect but Threatens Loss of Coverage for Tens of Millions,” CBPP, updated August 21, 2020, https://www.cbpp.org/research/health/suit-challenging-aca-legally-suspect-but-threatens-loss-of-coverage-for-tens-of.

[2] President Trump, September 27, 2020, https://twitter.com/realDonaldTrump/status/1310219962024439808.

[3] Amy Goldstein and Alice Crites, “Judge Barrett’s writing criticizes the Supreme Court decision upholding Obama-era health law,” Washington Post, September 28, 2020, https://www.washingtonpost.com/health/judge-barrett-aca-health-care-law/2020/09/28/429d165e-ff4c-11ea-b555-4d71a9254f4b_story.html.

[4] Congressional Budget Office, “An Update to the Economic Outlook: 2020 to 2030,” July 2, 2020, https://www.cbo.gov/publication/56442 .

[5] Dylan Scott, “The new anti-Obamacare lawsuit heads to court today. Scholars think it’s ‘absurd,’” Vox, September 5, 2018, https://www.vox.com/policy-and-politics/2018/6/8/17441512/obamacare-lawsuit-texas-trump; Robert VerBruggen, “The New Obamacare,” National Review, January 28, 2019, https://www.nationalreview.com/magazine/2019/01/28/the-new-obamacare/; Justin Baragona, “GOP Sen. Lamar Alexander Says He’s ‘Disappointed’ in Trump’s Ongoing Obamacare Lawsuit,” Daily Beast, May 10, 2020, https://www.thedailybeast.com/gop-sen-lamar-alexander-says-hes-disappointed-in-trumps-continuing-obamacare-lawsuit; Senator Lamar Alexander, Press Release, “Alexander Statement on Texas Obamacare Court Case,” June 12, 2018, https://www.alexander.senate.gov/public/index.cfm/pressreleases?ID=5AA8743C-F4FD-46A4-B282-0DE797E79ED4.

[6] Devlin Barrett and Matt Zapotosky, “Senior Justice Dept. lawyer resigns after shift on Obamacare,” Washington Post, June 12, 2018, https://www.washingtonpost.com/world/national-security/senior-justice-dept-lawyer-resigns-after-shift-on-obamacare/2018/06/12/b3001d7c-6e55-11e8-afd5-778aca903bbe_story.html.

[7] Editorial Board, “Texas ObamaCare Blunder,” Wall Street Journal, December 16, 2018, https://www.wsj.com/articles/texas-obamacare-blunder-11544996418; VerBruggen, Scott, op. cit.

[8] See the Supreme Court docket at https://www.supremecourt.gov/search.aspx?filename=/docket/docketfiles/html/public/19-840.html. CBPP also joined a brief on the devastating consequences of repeal at https://www.supremecourt.gov/DocketPDF/19/19-840/143451/20200513142138930_Nos.%2019-840.19-1019tsacFamiliesUSA.pdf.

[9] Jessica Banthin et al., “Implications of the Fifth Circuit Court Decision in Texas v. United States,” Urban Institute, December 2019, https://www.urban.org/sites/default/files/publication/101361/implications_of_the_fifth_circuit_court_decision_in_texas_v_united_states_final_121919_v2.pdf.

[10] Matt Broaddus, “Medicaid Enrollment Continues to Rise,” CBPP, September 9, 2020, https://www.cbpp.org/blog/medicaid-enrollment-continues-to-rise.

[11] Congressional Budget Office, “Federal Subsidies for Health Insurance Coverage for People Under 65: 2020 to 2030,” September 29, 2020, https://www.cbo.gov/publication/56571.

[12] Rachel Schwab, Justin Giovannelli, and Kevin Lucia, “During the COVID-19 Crisis, State Health Insurance Marketplaces Are Working to Enroll the Uninsured,” Commonwealth Fund, May 19, 2020, https://www.commonwealthfund.org/blog/2020/during-covid-19-crisis-state-health-insurance-marketplaces-are-working-enroll-uninsured.

[13] Mathieu Despard et al., “COVID-19 job and income loss leading to more hunger and financial hardship,” Brookings Institution, July 13, 2020, https://www.brookings.edu/blog/up-front/2020/07/13/covid-19-job-and-income-loss-leading-to-more-hunger-and-financial-hardship/.

[14] CBPP, “Chart Book: Accomplishments of the Affordable Care Act,” March 19, 2019, https://www.cbpp.org/research/health/chart-book-accomplishments-of-affordable-care-act; Sarah Miller et al., “Medicaid and Mortality: New Evidence from Linked Survey and Administrative Data,” NBER Working Paper No. 26081, August 2019, https://www.nber.org/papers/w26081; Jacob Goldin, Ithai Z. Lurie, and Janet McCubbin, “Health Insurance and Mortality: Experimental Evidence from Taxpayer Outreach,” NBER Working Paper No. 26533, December 2019, https://www.nber.org/papers/w26533.

[15] Jesse C. Baumgartner et al., “How the Affordable Care Act Has Narrowed Racial and Ethnic Disparities in Access to Health Care,” Commonwealth Fund, January 16, 2020, https://www.commonwealthfund.org/publications/2020/jan/how-ACA-narrowed-racial-ethnic-disparities-access.

[16] CBPP calculations from National Health Interview Survey data available from https://www.cdc.gov/nchs/nhis/healthinsurancecoverage.htm and https://www.cdc.gov/nchs/nhis/erkeyindicators.htm.

[17] For a discussion of how economic gaps are already widening, see LaDonna Pavetti and Peggy Bailey, “Boost the Safety Net to Help People with Fewest Resources Pay for Basics During the Crisis,” CBPP, April 29, 2020, https://www.cbpp.org/research/poverty-and-inequality/boost-the-safety-net-to-help-people-with-fewest-resources-pay-for?.

[18] Karen Pollitz, Jennifer Kates, and Josh Michaud, “Is COVID-19 a Pre-Existing Condition? What Could Happen if the ACA is Overturned,” Kaiser Family Foundation, September 30, 2020, https://www.kff.org/policy-watch/is-covid-19-a-pre-existing-condition-what-could-happen-if-the-aca-is-overturned/.

[19] Stephanie Armour, “For Many Pandemic Victims, Lingering Effects Stress Insurance Coverage,” Wall Street Journal, August 25, 2020, https://www.wsj.com/articles/for-many-pandemic-victims-lingering-effects-stress-insurance-coverage-11598347801.

[20] See, for example, Lisa Du, “Virus Survivors Could Suffer Severe Health Effects for Years,” Bloomberg, May 12, 2020, https://www.bloomberg.com/news/articles/2020-05-12/covid-19-s-health-effects-can-last-long-after-virus-is-gone.

[21] Matt Broaddus, “ACA Medicaid Expansion Drove Large Drop in Uncompensated Care,” CBPP, November 6, 2019, https://www.cbpp.org/blog/aca-medicaid-expansion-drove-large-drop-in-uncompensated-care.

[22] Tina Reed, “April was ‘worst month ever’ for hospital finances: report,” Fierce Healthcare, May 21, 2020, https://www.fiercehealthcare.com/hospitals-health-systems/april-was-worst-month-ever-for-hospital-finances-report# ; Kirk Johnson and Abby Goodnough, “Just When They’re Needed Most, Clinics for the Poor Face Drastic Cutbacks,” New York Times, April 4, 2020, https://www.nytimes.com/2020/04/04/us/coronavirus-community-clinics-seattle.html; Diane Arnos and Fredric Blavin, “To Weather COVID-19, Rural Hospitals Might Need More Support,” Urban Institute, April 6, 2020, https://www.urban.org/urban-wire/weather-covid-19-rural-hospitals-might-need-more-support;

[23] Margot Sanger-Katz, “The New Obamacare Lawsuit Could Undo Far More Than Protections for Pre-existing Conditions,” New York Times, June 12, 2018, https://www.nytimes.com/2018/06/12/upshot/the-new-obamacare-lawsuit-could-undo-far-more-than-protections-for-pre-existing-conditions.html.

More from the Authors

Areas of Expertise