How the Federal Tax Code Can Better Advance Racial Equity

2017 Tax Law Took Step Backward

Executive Summary

The federal tax code does not explicitly benefit one race over another. Yet historical racism and continuing racial prejudice and discrimination, through both public policies and private acts, have helped to shape factors that determine households’ tax liability, such as their income, wealth, and consumption. Racial barriers to economic opportunity have played a substantial role in determining today’s income and wealth distribution, in which households of color are overrepresented at the bottom of the scale while non-Hispanic white households (hereafter referred to as “white households”) are heavily overrepresented at the top. Thus, the tax code, specific tax provisions, and the way the code is administered and enforced can affect different races and ethnicities in widely disparate ways, and changes in tax policy and administration can widen or narrow racial disparities. Further, racism helped shape the tax code’s historical development in ways that continue to influence tax policy today, as in the current debate over a wealth tax and direct taxation.

Racism helped shape the tax code’s historical development in ways that continue to influence tax policy today.This report provides examples of how the federal tax code affects racial disparities and explains why the tax-cut law enacted in 2017 — the most recent major overhaul of the tax code — widens income and racial disparities. The report also identifies several types of tax policy changes that would advance racial equity, including: raising significantly more revenues in a progressive manner and investing the revenues in ways that improve economic opportunity and reduce racial disparities; strengthening aspects of the tax code that are efficient, progressive, and inclusive while overhauling regressive or unproductive tax breaks; and administering the tax code in more equitable ways.[1]

Federal Tax Code Reduces Racial Inequality in Income and Wealth But Can Do More

The tax code, and the public investments and other programs it funds, reduce racial disparities, but they would be more effective if the nation raised more revenue and did so in a progressive manner. Black and Latino households are one-and-one-third times likelier than white households to be in the bottom 60 percent of the income scale, while white households are three times likelier than Black and Latino households to be in the top 1 percent. As for wealth, 9 in 10 of the wealthiest 1 percent of households are white. These disparities reflect historical and continuing racial bias and discrimination, which have systematically reduced economic opportunity for households of color.

The federal tax code is progressive, meaning that high-income and wealthy people pay a greater share of their incomes (or wealth) in taxes than do lower-income people, reflecting their greater ability to help finance governmental functions and public investments. This progressivity modestly reduces the income and wealth gaps between the top and bottom of the income distribution, and hence racial disparities. Federal tax revenues also help to fund economic security programs and other investments that can reduce racial inequality, including by strengthening after-tax income and economic opportunities for those lower on the income scale and by improving policies in areas such as infrastructure where low-income communities of color have often been neglected or harmed.

It also should be noted that part of the progressivity of the federal tax code simply offsets regressive state and local tax codes, which tend to increase inequality, including racial disparities in after-tax income and wealth. Furthermore, when counting all levels of government, the United States collects less revenue as a share of the economy than most other developed countries; this limits both the tax code’s ability to reduce inequality directly and the nation’s ability to make public investments that expand economic opportunity and narrow racial disparities in that way as well.

While some targeted tax provisions intended to boost people’s opportunities to succeed in the economy are largely effective and inclusive, others are likely to help entrench or even widen racial inequities. Tax provisions that are largely effective and inclusive across races include the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC), which reduce poverty and raise the after-tax incomes of working families in low-paying jobs and are particularly important to African American and Latino households. Research indicates that income from these credits also has long-term benefits for children, helping them do better (and go further) in school and earn more as adults.[2]

But many other tax provisions, such as the deductions for mortgage interest and college savings plans, are “upside-down”: they go overwhelmingly to higher-income — and disproportionately white — households who least need help and likely would do what the tax break is designed to encourage (such as buying a house or going to college) even without the incentive. These provisions can exacerbate racial income and wealth inequality and reinforce discrimination and other barriers that households of color face. In addition, as this report explains, those barriers mean that even when households of color have similar income and wealth levels as white households, they often are less likely to benefit as much from these tax breaks.

The tax code also provides several significant tax breaks to income from wealth that income from work does not enjoy. For example, income from capital gains — that is, the increase in the value of a household’s assets when the assets are sold — is taxed at lower rates than income from work (at a top rate of 23.8 percent instead of 40.8 percent, counting federal Medicare taxes). And if a wealthy person holds onto an asset until he or she dies, its increase in value from the time the individual acquired it until their death will never be subject to tax. These and related tax preferences enable households that already have substantial wealth, including fortunes accumulated across generations, to build still more wealth.

How the IRS administers and enforces the tax code can also have different effects across races. Deep cuts in IRS funding in recent years have led to sharp reductions in audit rates for the largest corporations and the highest-income filers, who are overwhelmingly white, even though they contribute disproportionately to the “tax gap” (taxes owed but not paid voluntarily and on time). Policymakers’ unfortunate decision in 2015 to again outsource some tax-debt collection to private collectors — an approach that failed to produce results in the past — may pose particular risks for households of color, given the private debt collection industry’s history of racial discrimination.[3]

On the other hand, two IRS-sponsored programs seek to make tax administration more equitable and racially inclusive: Volunteer Income Tax Assistance, which provides free tax preparation to low-income filers, and Low-Income Taxpayer Clinics, which help low-income filers navigate disputes with the IRS. Both programs pay particular attention to overcoming language, cultural, and other barriers that communities of color may face in dealing with the IRS.

2017 Tax Law Took Step Backward

Rather than using the tax code to advance racial equity, such as by building on the EITC and other successful provisions and reforming upside-down tax breaks, the 2017 tax law made changes that will increase racial inequities.

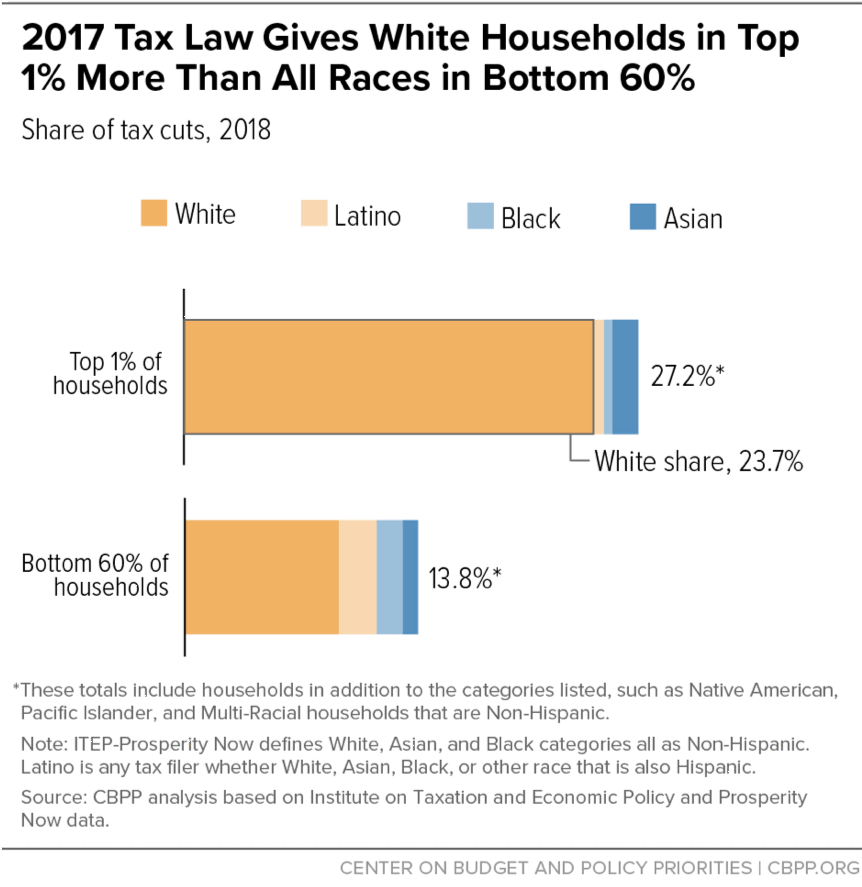

White households in the highest-earning 1 percent receive 23.7 percent of the law’s total tax cuts, far more than the 13.8 percentage share that the bottom 60 percent of households of all races receive.Its core provisions tilt heavily towards households at the top of the income distribution: white households in the highest-earning 1 percent receive 23.7 percent of the law’s total tax cuts, far more than the 13.8 percentage share that the bottom 60 percent of households of all races receive, a report from the Institute on Taxation and Economic Policy (ITEP) and Prosperity Now shows.

The 2017 law deeply cut the corporate tax rate, lowered the top individual income tax rate, weakened the Alternative Minimum Tax, and dramatically reduced the estate tax. It also created a new upside-down tax break: a deduction for pass-through business income, which costs more than $50 billion a year.

By contrast, the 2017 tax law generally treated low- and moderate-income households, disproportionately households of color, largely as an afterthought. For example, 11 million children under 17 in the lowest-income working families — who under prior law received only a partial Child Tax Credit or no credit at all — received either no improvement in the credit or a token increase, even as households with incomes as high as $400,000 received large CTC increases.

In addition, the 2017 law eliminated the CTC for about 1 million children in low-income working families because they lack a Social Security number. These children are overwhelmingly “Dreamers” with undocumented status whose parents brought them to the United States.

Moreover, the 2017 law will add $1.9 trillion to deficits over ten years at a time when the nation needs more revenues, not fewer, as the baby-boom generation moves deeper into retirement. In addition, the law could prove even costlier than estimated, as it also created lucrative new tax-avoidance opportunities for wealthy households and corporations to exploit. These higher deficits will likely create pressures in future years for cuts in various social programs, including those that help reduce racial inequities by enabling low- and moderate-income families to meet basic needs or by making investments that can improve low-income households’ educational opportunities and earnings potential.

Sound Reforms Could Better Use the Federal Tax Code to Advance Racial Equity

Policymakers could significantly bolster the tax code’s contribution to reducing income, wealth, and racial inequities by raising more revenues and doing so in a progressive manner, such as by strengthening the estate tax, otherwise taxing income from wealth that now goes untaxed, and repealing or curtailing various regressive, unproductive tax breaks. Such steps would not only reduce racial inequities directly but also generate revenue that could fund effective and inclusive public investments.

Policymakers could also bolster effective federal tax credits like the EITC and CTC while overhauling “upside-down” tax breaks disproportionately benefiting higher-income households for things like saving, higher education, and homeownership, when low- and moderate-income households most need support with these activities. And they could make tax administration and enforcement more equitable by giving the IRS adequate resources to conduct the more complex audits and other enforcement activities needed to better ensure that high-income filers and large corporations pay the taxes that they owe.

Federal Tax Policy Is Deeply Intertwined With Race

This introductory section of this paper sets out three important themes. First, federal tax policies and their administration need not be explicitly race-based either to entrench or worsen longstanding racial inequities or to promote racial equity and inclusion,[4] as many researchers have noted.[5] Second, racism and racial bias have helped shape the tax code in both explicit and implicit ways. Third, tax policy changes may affect racial equity in different ways than policymakers intended.

Tax Code Appears “Race-Neutral” But Some of Its Impacts Reflect Racism and Bias

Historical racism and contemporary patterns of racial discrimination and bias deeply affect a household’s income, types of income, saving, and consumption, so they also influence the federal tax code’s impact on households of different races.Since the tax code does not determine tax liability explicitly on the basis of race, it appears “race-neutral” on its face. Federal tax liability is based on factors such as total income, sources of income, saving, and spending on certain items such as mortgage interest or college expenses. But historical racism and contemporary patterns of racial discrimination and bias deeply affect a household’s income, types of income, saving, and consumption, so they also influence the federal tax code’s impact on households of different races.

Researchers have detailed the history and present-day systems of racism, bias, and racial inequality that have had large impacts in generating racial disparities in income, wealth, consumption, and other outcomes.[6] Historically, racist actions by policymakers and government officials disenfranchised people of color and deprived them of economic opportunity, from the laws upholding slavery to the confiscation of Native American tribal lands to the forced internment of Japanese Americans during World War II. More recent examples of discrimination include the deliberate residential segregation of households of color from white households,[7] barriers to high-quality education and jobs for people of color,[8] and discrimination in hiring and salaries that holds back many workers of color, including graduates from highly selective colleges.[9]

In addition, the criminal justice system can trap low-income individuals — often Black and Hispanic people — in cycles of debt and criminal justice involvement. The Sentencing Project finds that “African Americans are more likely than white Americans to be arrested; once arrested, they are more likely to be convicted; and once convicted, and they are more likely to experience lengthy prison sentences. African-American adults are 5.9 times as likely to be incarcerated than whites and Hispanics are 3.1 times as likely.”[10] And, for incarcerated people, “the overwhelming majority now accumulate mounds of debt due to numerous fees while behind bars,” researchers find.[11] These and other factors severely limit opportunity for people of color and can affect their well-being and economic outcomes for generations.

This means that the ways tax policies distinguish among households — such as taxing income from work differently than income from wealth and giving homeowners a tax break in the form of the mortgage interest deduction — can have very different effects for different races and ethnicities.

Racism and Racial Prejudice Helped Shape Tax Code

What the federal government can tax and how have been debated since the nation’s founding, and racism and efforts to protect the institution of slavery influenced key constitutional and other policy decisions that have shaped (and continue to shape) the tax code.[12] A central example — one that’s newly relevant given current debates over a proposed wealth tax — concerns direct taxes.

Article I, Section 2 of the U.S. Constitution requires any “direct tax” to be “apportioned” among the states based on their populations, meaning it would need to raise revenue from each state in proportion to that state’s share of the U.S. population. The same clause originally included the infamous requirement (since superseded) that each slave count as three-fifths of a free person for apportioning those direct taxes and determining the state’s number of House seats.[13]

Many historians, constitutional scholars, and judges have argued that the requirement for direct taxes to be apportioned was intended to protect southern states from the federal government levying taxes on the ownership of slaves.Many historians, constitutional scholars, and judges have argued that the requirement for direct taxes to be apportioned was intended to protect southern states from the federal government levying taxes on the ownership of slaves, including by making it harder to levy such taxes at rates so high as to effectively tax slavery out of existence.[14] Scholars still debate which taxes are “direct taxes” under the Constitution, but the clause clearly was part of the white framers’ so-called “compromise” over slavery.[15]

In practice, the clause requiring direct taxes to be apportioned among the states based on their populations placed an institutional barrier in front of tax measures to reduce racial income and wealth inequality that traces back to slavery.[16] After the 1894 enactment of a federal income tax — which proponents intended as a way to reduce reliance on regressive tariffs, ensure that wealthy Americans and extremely profitable corporations paid federal tax, and “shift the burden from the less wealthy to the wealthy”[17] — the Supreme Court invalidated it in a series of controversial decisions,[18] ruling that it was a “direct tax” and hence should be apportioned among the states. A justice dissenting in one of the cases argued, in the words of tax historian Alan Dixler, that “the apportionment requirement was written into the Constitution to protect the interests of the southern slave states; with the end of slavery, the purpose for the apportionment of direct taxes had vanished, and therefore direct tax should be construed narrowly.”[19] The dissent also remarked that the decision to strike down the tax “involves nothing less than a surrender of the taxing power to the moneyed class.”[20]

Thus, the Constitution, as the Supreme Court majority in 1895 interpreted it, prevented the federal government from creating an income tax that would have made federal taxes overall more progressive. It took nearly two decades, until 1913, for the federal government to levy income taxes without apportioning them, after the Sixteenth Amendment to the Constitution effectively overruled the Court’s decision by allowing a federal income tax.

Yet large amounts of income from wealth continue to go untaxed today or are taxed at lower rates than income from work. One way to help address that problem and reduce inequality (especially racial inequality) is through some type of tax on wealth. Many have expressed concern, however, that the Supreme Court could rule that a wealth tax, depending on its design, is a “direct tax” that violates the Constitution.[21] (Some constitutional scholars argue that with the historical rationale for the direct-taxation provision gone, the apportionment clause should be very narrowly construed and not prohibit a federal wealth tax.[22]) Regardless, the current discussion starkly illustrates the continuing impact of the constitutional legacy of slavery on debates about certain tax measures that could reduce racial inequality.

Tax Policy Changes May Have Unintended Impact on Racial Equity

Because there are no regular official estimates of the impact by race of current tax provisions or proposed changes (see box, “‘Colorblind’ Tax Data Pose Challenges for Racial Equity in Tax Policy”), these impacts can be difficult to understand — and easy for policymakers to neglect. But tax policies can widen or narrow racial disparities even when policymakers do not consider those impacts. To fully understand how their choices can advance or impede racial equity, policymakers should explicitly assess those impacts, both when considering new proposals and when assessing existing features of the tax code.

To be sure, even tax policies motivated by a desire to reduce racial disparities may fail or prove harmful. Tax incentives for economic development are one example. While they are often intended to benefit communities of color,[23] there is scant evidence that most such tax incentives generate meaningful benefits for residents.[24] Sociologists Kasey Henricks and Louise Seamster cite a history of such incentives that can leave Black and Latino communities behind.[25] Most recently, the 2017 tax law’s “opportunity zone” tax break for investing in certain geographic areas, which some supporters argue will enhance economic opportunity for communities of color, may turn out to lack sufficient protections for current residents against gentrification and displacement.[26] The provision does not require investments qualifying for the tax break to generate any benefits for communities or even anticipate doing so, which raises questions about whether its main effect will be simply to boost investors’ profits.[27]

Nevertheless, considering race systematically when crafting or evaluating tax policies may, over time, help policymakers more deliberately and effectively craft policies that promote opportunity broadly for all races rather than maintaining or amplifying current racial disparities.

“Colorblind” Tax Data Pose Challenges for Advancing Racial Equity in Tax Policy

“The IRS, Treasury, and Joint Committee on Taxation have [consistently] omitted race and ethnicity from the statistical analysis of tax data for over a century,” George Washington University Associate Professor of Law Jeremy Bearer-Friend has written,a adding that “[t]hese omissions are exceptional relative to other areas of public policy where federal data on race and ethnicity are readily available.”b

Tax returns only collect information that’s necessary for processing tax returns and do not ask filers their race or ethnicity (perhaps for good reasons, such as concerns about violating privacy or potentially deterring people from filing).c And federal agencies rarely fill that gap with other methods of data collection or analysis to estimate by race the impacts of the current tax code or tax policy proposals. This lack of information hampers attempts to understand how the tax code affects racial disparities and to develop tax policies to reduce racial inequity.

Most analyses of the impact of the tax code and tax policy changes are based on a sample of (anonymous) data from tax returns.d As a result, they tend to focus on how existing tax provisions or a proposed tax policy change might affect households at different income levels, of different sizes, or in different geographic areas, because income, family size, and geography are reported on tax returns and embedded in tax data, while race is not.

One approach that some researchers have used to determine how the tax code or tax changes affect households of different races or ethnicitiese is to estimate households’ race based on income or other characteristics that are strongly linked to race and are part of the tax-filing data, such as having a certain level of income and living in a certain area. But this approach is less useful for examining whether the tax code has differential impacts by race within particular income bands or particular regions (that is, holding those factors constant).

For this reason, no detailed estimates exist of whether the federal tax code has impacts on tax filers that differ by race at each level of income or wealth.f However, researchers have shown that specific elements of the tax code do have such differential impacts. For example, as this paper explains, a household of color may be less likely than a white household with the same income and wealth to benefit from the mortgage interest deduction or tax breaks on income from wealth.

Policymakers and the agencies that conduct tax analysis to inform policymaking should aim to provide regular, detailed, accurate analyses that illuminate whether, how, and why existing tax policies and proposed changes have differential impacts by race. This requires evaluating the benefits and risks of options that alter data collection and analysis to support analyses by race — as well as providing adequate funding to maintain and expand tax data collection and analysis.g Further, lawmakers and agencies may be able to make some immediate progress without legislative changes or substantial new resources. For example, some agencies intermittently produce reports that evaluate various tax code provisions, and these agency reports often summarize academic research on the impact of those provisions. These reports could do more to incorporate the limited data and research available that shed some light on the impacts of various tax-code provisions by race, and to note where such data and research are lacking.h

More explicit attention to the racial impacts of tax policymaking won’t guarantee more racially equitable tax policy. Indeed, it comes with risks that some lawmakers who oppose various tax measures that would improve racial equity could use data on the impacts of various tax policy proposals by race to try to foment resentment and opposition to various policies that would improve equity and inclusion. Nevertheless, policymakers can more readily and effectively design tax policies that advance racial equity if they have more data and analysis on the differential impacts of tax policies by race.

a Jeremy Bearer-Friend, “Restoring Democracy Through Tax Policy,” Great Democracy Initiative, December 2018, https://greatdemocracyinitiative.org/wp-content/uploads/2018/12/Tax-and-Democracy-121118.pdf, p. 18.

b “Should the IRS Know Your Race? The Challenge of Colorblind Tax Data,” 73 Tax Law Review, forthcoming; abstract available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3231315.

c For example, filers in immigrant families might be concerned that government agencies could attempt to unlawfully misuse race/ethnicity information provided on tax returns, especially in the current climate, where the Administration has sowed widespread confusion and fear in immigrant families about the potential government misuse of data to subject immigrants to harsh treatment. See Sharon Parrott, Shelby Gonzales, and Liz Schott, “Trump ‘Public Charge’ Rule Would Prove Particularly Harsh for Pregnant Women and Children,” Center on Budget and Policy Priorities, May 1, 2018, https://www.cbpp.org/research/poverty-and-inequality/trump-public-charge-rule-would-prove-particularly-harsh-for-pregnant; and Arloc Sherman, “Census Chief Scientist: Citizenship Question Reduces Accuracy, Raises Costs,” Center on Budget and Policy Priorities, June 12, 2018, https://www.cbpp.org/blog/census-chief-scientist-citizenship-question-reduces-accuracy-raises-costs.

d Limited access has been granted to some researchers to link data from tax returns to Census records (which do include information on race) for research purposes, but this approach is not widely available to researchers. For examples of this approach, see: Raj Chetty et al., “Race and Economic Opportunity in the United States: An Intergenerational Perspective,” NBER Working Paper No. 24441, March 2018, https://opportunityinsights.org/wp-content/uploads/2018/04/race_paper.pdf; and Shannon Mok, “An Evaluation of Using Linked Survey and Administrative Data to Impute Nonfilers to the Population of Tax Return Filers,” Congressional Budget Office, September 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/workingpaper/53125-nonfilers.pdf.

e For example, see the ITEP analysis of the 2017 tax law discussed in this paper.

f Some analyses show that within an income or wealth band (such as the middle fifth of the income distribution), a tax provision may affect the average white household differently from the average Black or Latino household. But income and wealth are so skewed by race that even within an income or wealth band, white households may have substantially higher average incomes than Black or Latino households. Comparing the average impact of a tax policy by race within an income band may therefore show more about the skew of the underlying racial income or wealth distribution — and the tax policy’s effect given that distribution — than about the policy’s impact on households of different races but the same income.

g For example, Bearer-Friend suggests options that include government agencies conducting more regular and systematic analyses using the technique of linking tax and Census records, as described at note (d) above. It might also be possible to supplement emerging synthetic data approaches to make analysis by race more widely available to researchers while protecting privacy. For more information, see Leonard Burman et al., “A Synthetic Income Tax Return Data File: Tentative Work Plan and Discussion Draft,” Tax Policy Center, June 30, 2017, https://www.taxpolicycenter.org/sites/default/files/publication/142421/2001396-a-synthetic-income-tax-return-data-file-tentative-work-plan_and_discussion_draft.pdf.

h For example, federal law requires the Congressional Research Service (CRS) to produce for the Budget Committees a report that examines tax expenditures. The most recent volume (https://www.govinfo.gov/content/pkg/CPRT-114SPRT24030/pdf/CPRT-114SPRT24030.pdf), of 1114 pages, includes — for each tax break examined — an assessment section and a selected bibliography that summarize some of the potential impacts of the tax break and the relevant literature on its impacts, with the discussion pointing out the gaps in the research where appropriate. Nevertheless, the CRS report does not discuss the research compiled in this paper or other surveys about the potentially differential impacts of particular tax expenditures by race. Likewise, the Joint Committee on Taxation regularly publishes background descriptions and overviews that include analysis of the impact of various tax provisions, drawing on relevant literature. These evaluations, as well, usually do not cite relevant literature related to racial impacts or note the lack of such relevant literature.

Federal Tax Code Reduces Racial Inequality in Income and Wealth But Can Do More

The federal tax system does push back in some ways against racial inequities.[28] But it can do much more.

Reducing Income Inequality to Lower Racial Disparities

Today’s income and wealth distribution reflects a long history of policies affected by racism, combined with continuing racial bias and discrimination, that systematically reduce economic opportunity for households of color.[29] Black and Latino households are one-and-one-third times likelier than white households to be in the lowest-income 60 percent of the income distribution, while white households are three times likelier than Black and Latino households to be in the top 1 percent.[30] Fully 90 percent of the wealthiest 1 percent of households are white, well above their 65 percent share of households overall. (See Table 1.) If current trends continue, it will take the median Latino family over 2,000 years just to match the current wealth (financial and housing assets) of the median white household, and Black families will never catch up with white families’ current level.[31]

| TABLE 1 | ||||

|---|---|---|---|---|

| Households of Color Overrepresented at Bottom of Wealth Distribution, White Households Overrepresented at Top | ||||

| Race/Ethnicity of Household | Share of All Households | Share of Households in Top 1% | Share of Households in Bottom 60% | |

| White | 65% | 90% | 54% | |

| Black | 15% | 4% | 20% | |

| Hispanic | 10% | 3% | 14% | |

| Other | 10% | 4% | 11% | |

A progressive tax code, meaning one in which high-income and wealthy people pay a greater share of their income or wealth in taxes than lower-income people do, reduces after-tax inequality.[32] In so doing, it can reduce racial inequities as well.[33]

The current federal tax code reduces inequality in this way because it is progressive overall. The lowest-income 60 percent of households will pay about 7 percent of their incomes in federal taxes in 2019, the Tax Policy Center estimates, while the top 1 percent will pay 30 percent, on average.[34] The federal income tax is clearly progressive. But other parts of the federal tax code, such as payroll and excise taxes, are regressive, meaning that they fall more heavily on low- and middle-income households than high-income households as a share of their income.[35]

Moreover, part of the overall progressivity of the federal tax code simply offsets the regressive impact of state tax codes. In nearly every state, the lowest-income households pay a higher share of their income in state and local taxes than the highest-income households, on average. This partly reflects most states’ heavy reliance on sales and excise taxes, which are highly regressive. Fees and fines, such as various fees paid by car owners, telephone users, those charged with a traffic violation, and others make overall state revenue systems even more regressive. Thus, nearly every state tax code worsens inequality — and therefore racial income and wealth gaps.[36]

(While this paper focuses on the relationship between the federal tax code and race, it is important to note that racism and racial bias have also influenced various state constitutional and tax policy decisions that helped create regressive state tax codes, as a CBPP analysis has detailed.[37] For example, highly restrictive property tax limits in Alabama’s constitution protected white property owners in the state from the possibility, in the years after Reconstruction, that African Americans and their allies could return to power and increase property tax rates substantially to fund education and other such measures. These property-tax limits have been in place for over 140 years, producing a harmful cumulative effect. Some more recent property tax limits in other states and localities also have produced racially discriminatory results.[38])

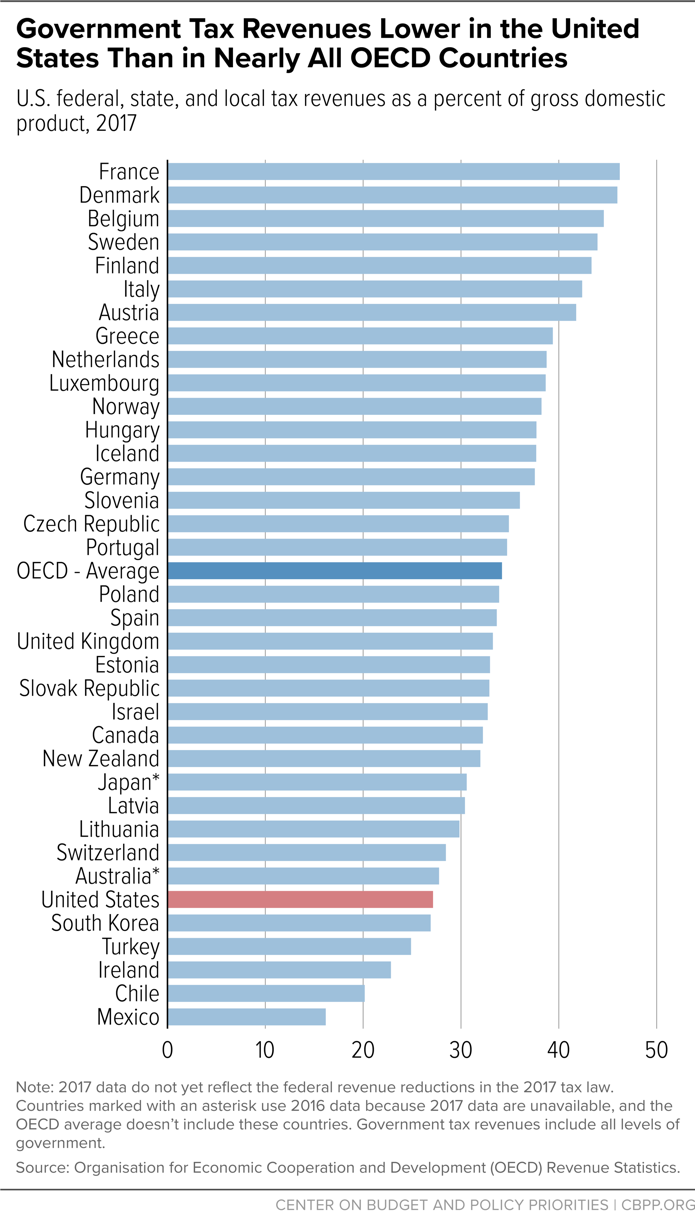

Another limitation of the U.S. tax system is that while it is progressive as a whole (federal plus state and local),[39] it collects less revenue as a share of the economy than the tax systems of most other comparable countries.[40] (See Figure 1.) This makes it less effective at reducing income and wealth gaps, for two reasons. First, even a highly progressive tax system will do relatively little to reduce inequality if it raises relatively little revenue. (As an extreme example, a system that levies $1 on the highest-income individual and nothing on anyone else would be highly progressive but do virtually nothing to reduce income inequality.) Second, the amount of revenue that a tax system raises heavily influences the size of public investments the government can fund, including investments that can improve economic opportunity and reduce racial inequity. Because of these two factors, the U.S. system of taxes and cash transfer programs (such as Social Security) does less than that of 27 other high-income countries to reduce post-tax inequality, the most recent and complete data from the Organisation for Economic Cooperation and Development (OECD) show.[41] Thus, a crucial way that the U.S. tax code could do more to reduce racial inequality would be to raise more revenue overall and do so in a progressive manner, with the revenue then being used to fund investments that advance racial equity. (See box, “Funding Investments to Advance Racial Equity.”)

Research suggests that racial prejudice may help explain why the U.S. tax system raises relatively little revenue. [42] Some studies examining the history of specific proposals to cut public investments or hamper progressive revenue-raising have concluded that racist attitudes were a factor in generating support for those policies.[43] University of Chicago Professor Robin Einhorn argues this pattern stretches back to slavery and includes the constitutional bargain discussed above.[44] In addition, empirical studies find that people are less likely to support increased public investments that they believe will disproportionately benefit other racial or ethnic groups, even if their own group would also benefit,[45] and some have found links between respondents’ negative attitudes to various safety net programs and racist stereotypes about the people of color whom they assume to be the programs’ primary beneficiaries.[46] Tax revenue levels are highly related to the level of public investments, so such findings indirectly suggest that racial prejudice may be linked to levels of taxation.[47]

Some researchers argue that certain interest groups have used “dog whistles” to stoke racial animus against people of color. This has had the effect, for instance, of reducing support among low- and moderate-income white households for tax and spending policies that would benefit low- and moderate-income people across all races, while reducing the concentration of income and wealth among the most-well-off, who are overwhelmingly white.[48] Pointedly, in 1981, Republican strategist Lee Atwater listed cutting taxes as one of the “abstract” policies that can tap into racist attitudes, serving as a substitute for explicit racial denigration of Black people, because a perceived “byproduct” of tax cuts may be budget cuts that result in “blacks get[ting] hurt worse than whites.”[49]

Progressive tax policies and public investments that advance racial equity are nevertheless achievable, and public attitudes toward policies that advance racial equity can improve. For example, the Affordable Care Act (ACA) raised progressive tax revenues to fund new investments that led to large gains in health coverage and care.[50] The gains were widely shared across all races, and the large coverage gains among people of color narrowed longstanding racial disparities in health coverage that will likely reduce disparities in health outcomes over the long term.[51] While surveys over time consistently show less support for the ACA among white than Black or Latino respondents,[52] support among all races has risen substantially over time as the ACA’s effects have become better understood and more widely felt.[53]

Funding Investments to Advance Racial Equity

The main purpose of a tax system is to raise revenue to finance governmental functions and priorities. While these investments and other expenditures are not themselves this report’s focus, they are a central way that federal taxes can advance racial equity. Federal investments in nutrition, health care, housing, education, infrastructure, retirement security, and many other areas can be designed and administered to help people afford the basics, remove barriers to opportunity for both adults and children, and reduce racial inequities. They also can help redress previous federal policies that imposed barriers to economic success on households of color.a

Reflecting a variety of factors — which include a history of underfunding these investment areas and discrimination in hiring, pay, and housing — Black and Latino households tend to have higher poverty rates and lower wealth, and they are more likely to live in high-poverty, low-opportunity neighborhoods.b Thus, they are likelier to qualify for and participate in programs targeted on low-income people or communities.

Economic security programs such as SNAP, housing assistance, and health coverage assist millions of households each year. These programs not only help families improve their living standards immediately but can also have longer-term benefits. The National Academy of Sciences finds that “income poverty itself causes negative child outcomes, especially when it begins in early childhood and/or persists throughout a large share of a child’s life,” and “programs that alleviate poverty either directly, by providing income transfers, or indirectly, by providing food, housing, or medical care, have been shown to improve child well-being.”c In addition, studies show that various economic security programs help children do better in school and increase their earning power in adulthood. Some evidence also suggests that for children at the same income level, the gains from added income may be larger for children of color.d

Well-designed federal investments can also promote economic growth and opportunity more broadly, including by addressing the legacy of federal fiscal policies that impeded economic success for households of color.e For example, investing in public transit can offer benefits such as reducing both traffic congestion and carbon pollution, but communities of color historically have been underserved by public transit even though residents in those communities are less likely to have access to private cars.f And low-income children of color face greater risk than white children of exposure to toxic lead, unsafe water, air pollution, and other environmental hazards due to policymakers’ neglect of infrastructure needs in their communities over many decades. Carefully designed investments to help address the historical neglect of many communities of color could help reduce these disparities, securing safer living conditions and greater access to economic opportunity.g

The examples of investments that can promote opportunity and reduce racial inequities extend well beyond infrastructure. For example, the United States invests much less than other developed countries in child care, early education, and paid leave, which can improve economic, health, and other outcomes for low- and moderate-income parents — particularly women of color, who are overrepresented in the low-wage workforceh — and their children. Child care assistance benefits both parents and children, helping parents afford the high cost of care so that they can work or go to school, while providing young children with positive early learning experiences important for healthy development. Research shows that child care assistance improves employment outcomes for parents, including both higher employment rates and greater job retention.i But child care assistance has long been underfunded. In 2015, just 1 in 6 children who qualified for child care assistance under federal rules received any help.

a For examples of unmet needs, including in programs that serve low-income individuals who disproportionately are people of color (such as Head Start and child care), see Sharon Parrott, Richard Kogan, and Roderick Taylor, “New Budget Deal Needed to Avert Cuts, Invest in National Priorities,” Center on Budget and Policy Priorities, March 1, 2019, https://www.cbpp.org/research/federal-budget/new-budget-deal-needed-to-avert-cuts-invest-in-national-priorities. For a discussion of the need to better target infrastructure investments on low-income communities and communities of color, see Chye-Ching Huang and Roderick Taylor, “Any Federal Infrastructure Package Should Boost Investment in Low-Income Communities,” Center on Budget and Policy Priorities, April 4, 2019, https://www.cbpp.org/research/federal-budget/any-federal-infrastructure-package-should-boost-investment-in-low-income.

b Leachman et al.

c National Academies of Sciences, Engineering, and Medicine, “A Roadmap to Reducing Child Poverty,” National Academies Press, 2019, https://doi.org/10.17226/25246.

d For a discussion of the research on the positive impact of economic security programs on families and children, see Arloc Sherman and Tazra Mitchell, “Economic Security Programs Help Low-Income Children Succeed Over Long Term, Many Studies Find,” Center on Budget and Policy Priorities, July 17, 2017, https://www.cbpp.org/research/poverty-and-inequality/economic-security-programs-help-low-income-children-succeed-over.

e Huang and Taylor.

f Monica Anderson, “Who Relies on Public Transit in the U.S.,” Pew Research Center, April 7, 2016, https://www.pewresearch.org/fact-tank/2016/04/07/who-relies-on-public-transit-in-the-u-s/.

g Huang and Taylor.

h Farah Ahmad and Sarah Iverson, “The State of Women of Color in the United States: Too Many Barriers Remain for This Growing and Increasingly Important Population,” Center for American Progress, October 2013, https://cdn.americanprogress.org/wp-content/uploads/2013/10/StateOfWomenColor-1.pdf.

i For a review of the research, see Gregory Mills, Jessica Compton, and Olivia Golden, “Assessing the Evidence about Work Support Benefits and Low-Income Families,” Urban Institute, February 24, 2011, https://www.urban.org/research/publication/assessing-evidence-about-work-support-benefits-and-low-income-families. Also see Douglas Rice, Stephanie Schmit, and Hannah Matthews, “Child Care and Housing: Big Expenses With Too Little Help Available,” Center on Budget and Policy Priorities and Center for Law and Social Policy, April 26, 2019, https://www.cbpp.org/research/housing/child-care-and-housing-big-expenses-with-too-little-help-available.

Expanding Economic Opportunity in a Racially Inclusive Way

The federal tax code contains a raft of targeted tax breaks (credits, exemptions, and deductions) collectively known as “tax expenditures,” some of which aim to help households and children succeed in the economy.[54] Those provisions can improve families’ opportunities in ways that advance racial equity, with the EITC and CTC in particular being both effective and inclusive. But many other tax breaks intended to help families send a child to college, buy a house, or save for retirement provide many of their benefits to those who need them least, while doing far less to aid those who would benefit most. Such tax breaks likely exacerbate racial inequities. And a different group of large tax breaks allows income from wealth, including fortunes accumulated across generations, to be taxed at lower rates than income from labor or escape tax altogether, further entrenching existing racial income and wealth gaps.

Tax Credits for Low- and Modest-Income Working Families Advance Racial Equity

The EITC and CTC raise the after-tax incomes of families in low-paying occupations.[55] The increased concentration of economic gains at the top of the income ladder and the lack of more broadly shared prosperity harm millions of workers, especially people of color: Black and Latino workers are far likelier than white workers to work in low-paid occupations, a development reflecting both the legacy of severe discrimination and continued structural barriers to opportunity.[56] These tax credits serve a larger number of white households than any other racial or ethnic group (because there are more white households in the United States) but serve a larger proportion of people of color.[57] The EITC and CTC also disproportionately serve Black, Latina, and Native American women.

Beyond boosting incomes directly, the EITC and CTC have long-term benefits for the life trajectories of children in families that receive them. That’s a key reason why the credits advance racial equity, since child poverty is nearly three times as high for Black and Latino children as for white children, we estimate using the Supplemental Poverty Measure (a more comprehensive metric than the official poverty measure, which counts only cash income). Studies indicate that these credits improve health outcomes at birth, raise reading and math test scores in middle school, increase high school completion and college entry rates, and may lift lifetime income. Studies also show that the benefits of larger EITC benefits extend to children of all racial and ethnic groups, with some evidence that the benefits are larger for children of color.[58]

Upside-Down Tax Breaks Exacerbate Racial Inequality

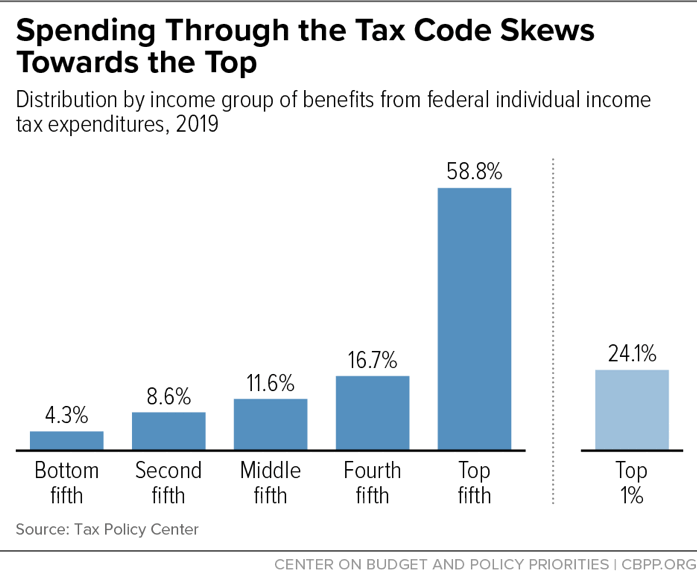

By contrast, many other federal tax breaks intended to help boost economic opportunity are neither effective nor racially inclusive. For example,[59] those aimed at encouraging activities to build economic resources, like owning a home, attending college, or saving for retirement, are tilted heavily toward higher-income and higher-wealth households. That’s in part because the bulk of these tax breaks are delivered in the form of deductions, exemptions, or exclusions, whose value rises with household income; the higher one’s tax bracket, the greater the tax benefit for each dollar deducted, exempted, or excluded. It’s also because higher-income households have more income and wealth that they can apply to deductible purposes like buying a home or amassing savings for college or retirement. As a result, these tax breaks are upside down: they provide their largest subsidies to high-income households (which are disproportionately white) even though those are the households least likely to need financial incentives to engage in these activities and most likely to buy a home, go to college, and save substantial amounts for retirement regardless of whether they receive a tax break for doing that. Overall, the bulk of spending through the tax code skews to high-income filers. (See Figure 2.)

Since households of color are disproportionately low or moderate income, they receive much smaller benefits from many of these tax breaks, and in some cases are locked out altogether. Furthermore, due to the legacy of racial barriers and continuing discrimination (such as discrimination in housing and lending markets), even among households with similar incomes, white households may be more likely, on average, to be able to claim these tax breaks and to secure a larger benefit from them than households of color. Thus, these tax breaks likely exacerbate racial gaps in income and wealth.[60]

The mortgage interest deduction is one example. It is heavily tilted toward filers with higher incomes, who are likelier to buy a house even without the tax break, likelier to own a costly house, and likelier to get a larger tax break per dollar of mortgage interest deducted because they are in higher tax brackets.[61] Sixty percent of the federal mortgage interest deduction went to the 2.7 percent of claimants with incomes over $200,000 in 2018, the Joint Committee on Taxation (JCT) estimates.[62] Not surprisingly, research shows that the deduction, rather than increasing homeownership among those who couldn’t otherwise afford it, tends to encourage people who would already own a home to buy a larger or more expensive one or simply adds to their after-tax income and wealth.[63] This tilt to high-income households means recipients of the deduction likely are disproportionately white. The deduction also leaves out renters, who are disproportionately households of color and low income, and who may be locked out of homeownership for a variety of reasons, including housing discrimination and barriers to well-paying jobs and other economic resources.[64]

Thus, while the IRS does not collect data on the race of filers claiming the mortgage interest deduction, income and geographical patterns suggest that it has highly differential impacts by race. “Zip codes with high claiming rates [for the deduction] tend to be disproportionately white, middle-aged, and married,” a 2014 Urban Institute analysis found.[65] Even among households with similar incomes, barriers influenced by racism may mean that households of color are less likely to be able to buy a home, claim the tax break, and gain wealth from increases over time in the home’s value. Findings from two studies, for example, suggest that due to discriminatory practices in the housing and mortgage lending markets, white households in many areas are better able than Black households to buy a home and hence claim the mortgage interest deduction and to gain wealth from increases in their home’s value, even when their incomes are the same.[66]

For similar reasons, many other tax breaks intended to help households build economic resources by encouraging activities like saving and attending college likely exacerbate racial inequities. And, by reducing revenue, they limit policymakers’ ability and willingness to make direct investments in areas like education that might be better targeted to advancing racial equity.

Tax Breaks for Income Derived From Wealth Entrench Racial Income and Wealth Gaps

The federal tax code accords income from wealth several tax breaks that income from work does not enjoy, taxing it at lower rates, taxing it less frequently, or allowing it to escape taxation entirely.[67]

For example, wealthy households derive much of their income from capital gains, or the increase in value of their assets. This income is taxed at lower rates than income from work (at a top rate of 23.8 percent instead of 40.8 percent). And, while workers pay taxes on their wage and salary income in the year they earn it (through payroll and income taxes deducted from their paychecks), wealthy filers can delay paying taxes on their capital gains income for years or even decades, because capital gains taxes are only due when the gain is “realized,” usually when the asset is sold.

In addition, if a wealthy person holds on to an asset until they die, its increase in value from the time they acquired it until their death will, in most cases, never be subject to tax. This provision, known as “stepped-up basis,” is one of the tax code’s largest subsidies for wealth. It encourages wealthy people to report as much of their income as possible as capital gains and to hold on to their assets until death, when they can pass them to their heirs — who won’t owe any income or payroll tax on them. More than half of the value of the nation’s largest estates consists of unrealized capital gains that have never been taxed. And while some of those accumulated gains may face the estate tax, policymakers have weakened that tax to the point where fewer than 1 in 1,000 estates face it, and taxable estates owe just 16.5 percent of their value in tax, on average.[68]

In sum, those who already have substantial wealth, including fortunes accumulated across generations, benefit from tax breaks they can use to accumulate even more wealth.[69]

Even among households with comparable overall income or wealth, white households may gain more than others from the largest tax breaks on income from wealth. “[To] maximize the tax benefit of many of these provisions, an individual needs not only to own property, but to own the right types of property,” Vanderbilt University Law Professor Beverly Moran and University of Wisconsin Law Professor William Whitford argued in a 2008 analysis.[70] Controlling for income and overall wealth, they found that Black households are less likely to receive tax-free gifts or inheritances, to own financial assets that generate tax-advantaged capital gains, or to generate capital gains at the same rates as white households.[71] More recent data show continuing disparities between Black and white households and similarly large disparities between Latino and white households.[72]

Tax breaks on income from wealth thereby likely further entrench today’s concentration of income and wealth among the most well-off, who are overwhelmingly white.[73] Furthermore, tax breaks on income from wealth accumulated and transferred across generations essentially reward racial patterns of economic exclusion and privilege established when racial discrimination was more blatant than it is today.

It is worth noting that if the federal income tax of 1894, which the Supreme Court struck down as a “direct tax” in 1895, had remained in place, some of this wealth would surely have been subject to tax. Indeed, the 1894 income tax explicitly included in taxable income any increase in net wealth, such as inheritances and gifts, because “Congress wanted to reach the vast accumulations of intangible wealth that had previously gone untaxed,” according to tax historian Richard J. Joseph.[74] The legacy of this constitutional provision still hangs over current tax debates about progressively raising revenue by taxing accumulated wealth.[75]

Administering the Tax Code Fairly

Decisions about how to interpret and administer the tax code may appear race neutral but can significantly affect racial inclusion and equity in either direction, as the following three examples illustrate: audit rates for individuals and corporations; outsourcing tax collection to private debt collectors; and tax filing assistance for low-income households.[76]

Audit and enforcement decisions. The IRS conducts audits and other enforcement activities to ensure filers pay the taxes they legally owe. While it selects returns for audit “without regard to race or where the taxpayer lives,”[77] policymakers’ decisions about funding IRS enforcement, and tax administrators’ decisions about how to use the funds, can produce geographically and racially disparate audit rates.

Policymakers have cut overall IRS funding by 21 percent since 2010, after adjusting for inflation. IRS enforcement has been particularly hard hit, with its funding cut by 25 percent in real terms and enforcement personnel reduced by 31 percent.[78]

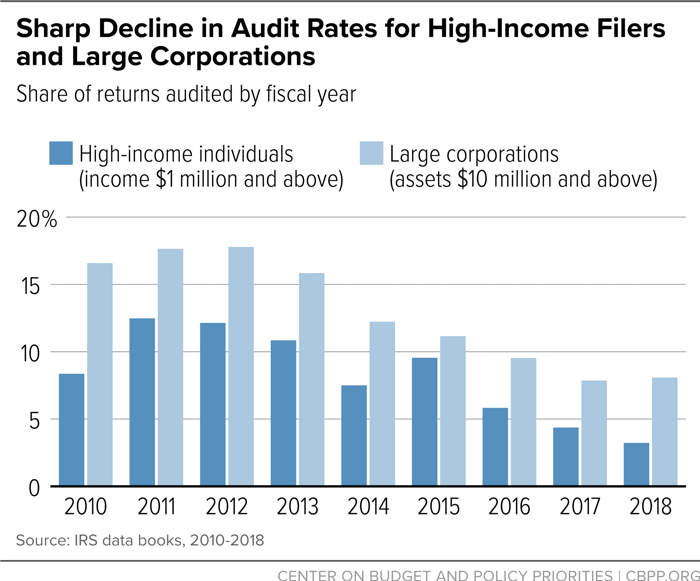

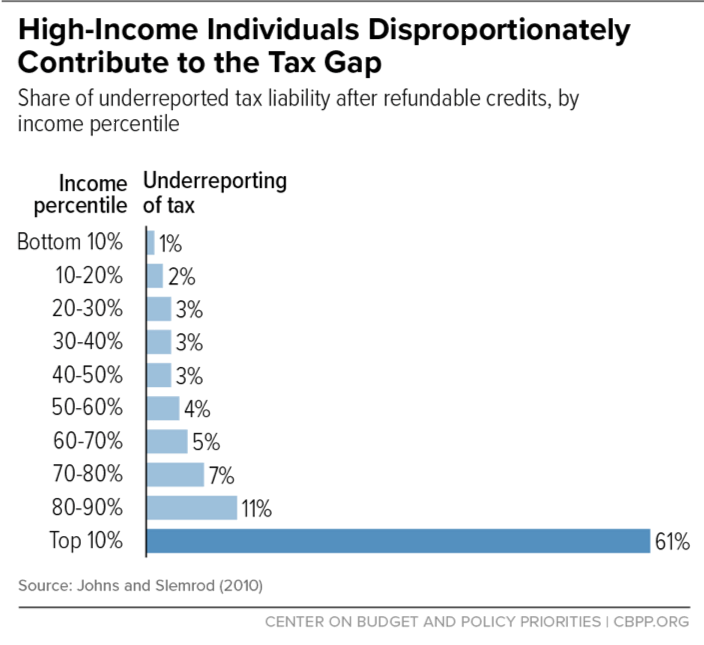

Funding cuts have led the IRS to audit less. Audit rates are down by more than 40 percent overall[79] and have dropped particularly steeply for the largest corporations and highest-income filers. (See Figure 3.) Audit rates among low-income filers have fallen less sharply,[80] so they have risen as a share of total audits, from 34 percent in 2010 to 39 percent in 2018.[81] This shift has occurred even though overpayments in the EITC, the main tax provision that prompts audits of low-income filers, make up less than 5 percent of the tax gap.[82] In contrast, the highest-income 10 percent of filers account for 61 percent of taxes owed on income that should be taxable but is not reported.[83] (See Figure 4.)

To prevent unscrupulous filers from trying to escape audits, the IRS does not publicly describe how it decides whom to audit, but there may be several factors. For instance, Congress has called for the IRS to increase scrutiny of the EITC and placed much less emphasis on oversight of tax breaks that high-income filers use.[84] Cuts in IRS enforcement funding also likely contributed to this upside-down pattern; audits of high-income and corporate returns can be both time- and personnel-intensive for the IRS because of these filers’ complex financial affairs. Further, the wealthy can hire large numbers of lawyers and accountants to stretch the tax code to their advantage. “It can take years for IRS investigators just to understand a transaction and deem it to be a violation,” a ProPublica investigation found.[85] This means that audits of high-income people may be particularly vulnerable to cuts when IRS funding is tight. By contrast, it costs relatively little for the IRS to conduct a “correspondence examination” of a low-income filer, requiring the filer to mail in relevant documents to prove eligibility.[86]

But while audits of higher-income individuals and businesses are costlier to undertake, they yield much larger average collections than those of lower-income taxpayers, a recent Congressional Budget Office report found.[87] Moreover, an OECD-World Bank report explains that “[while] viewed as distinct crimes, tax crime and corruption are often intrinsically linked.”[88] Thus, inadequate tax enforcement among wealthy filers and large corporations likely weakens detection and prosecution of criminal corruption, with the beneficiaries of that lack of greater enforcement being disproportionately white.[89]

At the other end of the income scale, enforcement measures can generate particular challenges for low-income filers, especially households of color. The IRS’ National Taxpayer Advocate, Nina Olson, points out that correspondence examinations of low-income filers “may be especially challenging for taxpayers with a language barrier, who may benefit from a face-to-face conversation,” noting the large share of Hispanic filers eligible for refundable credits and thus potentially subject to a correspondence audit.[90] Moreover, the vast majority of EITC filers audited don’t have representation from a tax lawyer or other tax professional.[91]

Private debt collection. In 2004, policymakers allowed the IRS to privatize some of its debt collection efforts. This program “undermined effective tax administration, jeopardized taxpayer rights protections, and did not accomplish its intended objective of raising revenue,” the National Tax Advocate concluded.[92] Indeed, it lost money, according to the Joint Committee on Taxation. Although this program was terminated in 2009, Congress in 2015 authorized the IRS to start contracting with private firms again to collect delinquent tax debt — despite the National Taxpayer Advocate’s warning to Congress that there was no reason to expect a better outcome and a warning by civil rights and consumer groups that “year after year, the Federal Trade Commission receives more complaints about debt collectors than any other specific industry.”[93]

Since then, the National Taxpayer Advocate has documented the private debt-collection program’s adverse impact on low-income households.[94] The report found, “of taxpayers who entered into installment agreements while their debts were assigned to private collection agencies, 40 percent had incomes at or below their allowable living expenses, meaning they agreed to pay the IRS when they were unable to pay their basic living expenses.” A recently enacted provision stops the IRS from referring households with income below 250 percent of the poverty level to private debt collectors, but this will not help many other households with limited resources. Some 28 percent of filers who made payments after their debts were assigned to private collectors had incomes between 250 and about 550 percent of poverty, the National Taxpayer Advocate report found.

The impact may be particularly harsh for households of color, and not just because they are likelier to have modest incomes. Private debt collectors have a long history of discriminating against Black and Latino households,[95] and such patterns may persist in the current IRS program. Despite this history, the 2015 law included no requirement to monitor the program for racially disparate impacts.

Filing assistance. Low-income households spend a greater share of their income on complying with the tax code than high-income filers do.[96] But two important IRS-sponsored programs make tax filing more accessible and inclusive than it would be otherwise.

The Volunteer Income Tax Assistance (VITA) program trains volunteers to help millions of low- and moderate-income people file their taxes by providing accurate, free, and trustworthy tax-preparation assistance in sites across the country. These sites serve people making less than $55,000, enabling them to keep more of their money to care for their families, a significant benefit given that the average commercial tax preparation costs nearly $300. VITA services such as Virtual VITA and drop-off tax preparation also help expand the reach of free tax preparation.

VITA serves low-income filers of all races and promotes racial equity in other ways. Many IRS and volunteer outreach efforts for VITA seek to overcome the unique barriers that communities of color may face in tax filing. For example, the IRS and VITA conduct outreach to inform Native American filers of their potential eligibility for the EITC,[97] including through tailored activities that take into account the history of profoundly negative interactions between Native Americans and the federal government, which may cause some eligible workers to hesitate to claim the credits.[98] Also, many VITA sites have multilingual volunteers who can assist filers with limited English skills. Further, many VITA sites connect clients to other resources like bank accounts or health coverage programs, which may be particularly important for households of color who face barriers to accessing those resources.[99]

The second program, Low Income Taxpayer Clinics (LITC), assists low-income individuals who have a dispute with the IRS and provides education and outreach to those who speak English as a second language. It aims to “[protect] taxpayers’ rights by providing access to representation for low income taxpayers, so that achieving a correct outcome in an IRS dispute does not depend on the taxpayer’s ability to pay for representation.”[100] For a clinic to receive a grant to run an LITC, 90 percent of the taxpayers it serves must have incomes at or below 250 percent of the poverty level.[101] As a result, these clinics likely help Black and Latino households at higher rates than white households.

2017 Tax Law Took Step Backward

Crafting the 2017 tax law, which alters the tax treatment of trillions of dollars of income, gave policymakers an opportunity to make the tax code one that better advances racial equity by addressing some of the issues in tax policy and administration discussed above. Instead, policymakers enacted a law that further widens the gap between the overwhelmingly white households at the top of the income ladder and everyone else. It also created new loopholes that wealthy taxpayers and corporations are certain to exploit. And by shrinking revenues, the law will make it more difficult to invest adequately in priorities that can benefit all racial and ethnic groups, such as health care and well-designed infrastructure.

Because the law’s core provisions tilt heavily toward households at the top of the income distribution, it increases after-tax income inequality and widens racial disparities.[102] White families are three times likelier than Black and Latino families to be among the highest-earning 1 percent, a report from the Institute on Taxation and Economic Policy (ITEP) and Prosperity Now notes.[103] These highest-income white households make up just 0.8 percent of all households but receive 23.7 percent of the law’s total tax cuts, far more than the 13.8 percent of the tax cuts that the bottom 60 percent of households (of all races) combined receives, according to the ITEP report.[104] (See Figure 5.)

The law deeply cut the corporate tax rate (from 35 percent to 21 percent), which will particularly benefit wealthy shareholders and highly compensated employees such as CEOs. It also lowered the top individual income tax rate and weakened the Alternative Minimum Tax. As Roosevelt Institute Fellows Darrick Hamilton and Michael Linden explain in their examination of how the law exacerbates racial inequities, it:

dramatically cuts the estate tax for the extremely wealthy — a group that is far whiter than the overall population — making it even easier to pass along their often inherited advantages to another generation of heirs. . . . This policy is especially galling considering that inheritance is the single variable with the greatest explanatory power of the overall racial wealth gap.[105]

To be sure, the law trimmed some upside-down tax breaks such as the mortgage interest deduction, and it limited some costly business tax provisions such as deductions for interest expenses, but it used the revenue to help pay for tax cuts that widened income and racial inequality overall. In addition, the law created a large new upside-down tax break: a deduction for pass-through business income — that is, income from businesses such as partnerships, S corporations, and sole proprietorships that business owners claim on their individual tax returns. This deduction will cost more than $50 billion per year. Some 61 percent of the benefit will go to the top 1 percent, JCT estimates.[106]

By contrast, the 2017 tax law treated low- and moderate-income households, which are disproportionately households of color, largely as an afterthought. Its tax cuts for the bottom 60 percent of households are worth only about 1.1 percent of their pre-tax income, on average, less than half the 2.6 percent average boost that households in the top 1 percent receive on their vastly higher incomes. This skew disproportionately affects Black households (which make up 10.2 percent of filers but 12.5 percent of those in the bottom 60 percent) and Latino households (which make up 11.9 percent of filers but 14.2 percent of those in the bottom 60 percent).[107] In addition, the law did relatively little to expand tax credits in ways that are well targeted and inclusive: its CTC increase largely or entirely excluded 11 million children in low-income working families,[108] and the 2017 law will weaken the EITC somewhat over time.[109]

Further, the law’s ultimate impact on low- and moderate-income Black and Latino households could be more detrimental than the above figures suggest:

- The ITEP-Prosperity Now numbers cited above do not reflect a provision of the 2017 law that specifically targeted immigrant families, that is, elimination of the Child Tax Credit for 1 million children in low-income working families because they lack a Social Security number.[110] These children are overwhelmingly “Dreamers” with undocumented status whose parents brought them to the United States.

- Low-wage U.S. workers, who are disproportionately people of color, may be hurt over time by the law’s new incentives for businesses to offshore and outsource jobs. The law’s international tax provisions encourage corporations to shift profits and even investments offshore, which may harm jobs and wages in this country.[111] In addition, the pass-through deduction may contribute to “workplace fissuring,” in which firms obtain the services of workers without hiring them directly (i.e., by contracting out various functions), which can undercut workers’ wages, benefits, and employment protections.[112]

- The law will add $1.9 trillion to deficits over ten years at a time when the nation needs more revenues, not fewer, as the baby-boom generation moves deeper into retirement.[113] These higher deficits are likely, sooner or later, to create pressure for cuts to programs that help low- and moderate-income families meet basic needs or invest in building their human capital or revitalizing their communities. For example, some lawmakers who supported the 2017 law have since called for large cuts to programs like Medicaid to address budget deficits.[114]

The law’s overall tilt toward largely white, already well-off, households could grow further over time for another reason, as well; the law creates lucrative new opportunities for wealthy households and corporations to try to game the tax code to avoid taxes, including by lobbying to make the regulations implementing the hastily drafted law as favorable to them as possible. Tax advisors and lobbyists have referred to the law as a “bonanza” and a “giant present to the tax lobbying community.”[115] An increase in the use of tax shelters to escape taxes could cause the 2017 law to lose even more revenue than estimated over time, and likely would exacerbate the law’s income and racial inequities since tax avoidance is worth the most to wealthy individuals and profitable corporations.

Sound Reforms Could Better Use the Tax Code to Advance Racial Equity

As this report shows, some parts of the federal tax code advance racial equity, but sound reforms could significantly bolster its contribution to reducing income, wealth, and especially racial disparities. They include:

Raising progressive revenues to reduce inequality and invest in inclusive programs. Raising revenues in progressive ways would enable the federal tax code to do more to reduce inequality and thereby help close racial income and wealth gaps. In addition, the added revenues could fund investments in economic security programs that can improve racial equity. (See box, “Funding Investments to Advance Racial Equity.”)

Revenue-raising policies that are especially well-targeted include those that would tax income from wealth, which now either goes untaxed or is taxed more lightly than income from work — especially wealth accumulating untaxed across generations.[116] Since a large share of the nation’s wealth is concentrated in the hands of a few and since very wealthy people are overwhelmingly white, this extreme wealth concentration reinforces barriers that make it harder for people of color to make economic gains. New York University Law Professor Lily Batchelder, summarizing the empirical evidence, writes, “30 percent of the correlation between parent and child incomes — and more than 50 percent of the correlation between the wealth of parents and the wealth of their children — is attributable to financial inheritances.”[117]

Many sound options exist to raise revenues in a progressive manner and thereby reduce inequality, especially racial inequality. Some of the approaches are complementary. For example, policymakers could: address current provisions of the tax code that allow large amounts of capital gains to escape taxation (such as through “stepped-up basis”); raise the tax rates on income from wealth closer to the rates on income from work (through such means as raising tax rates on capital gains and more adequately taxing corporate income, which ultimately flows primarily to affluent shareholders); and close loopholes, including various tax shelters that wealthy filers use to avoid or minimize the estate tax, as well as strengthening the estate tax itself. Policymakers also should consider more fundamental reforms, such as taxing certain gains in the value of assets each year as they accrue, a wealth tax, and inheritance taxes.[118]

Bolstering well-designed tax credits to make them even more inclusive. The EITC and CTC reduce poverty and boost opportunity across generations, but they can be made still more effective and inclusive.

For example, the current EITC and CTC disproportionately serve households of color because they are more likely than white households to work for low pay due to racial barriers to economic opportunity, and these credits are well-targeted to low- and moderate-income families. However, many children in the lowest-income families are currently locked out of the maximum CTC, or any CTC at all. This is because the amount of CTC that a family can receive as a refund is severely limited for families with incomes too low to owe much federal income tax. Roughly half of non-Hispanic Black and Hispanic children do not receive the full CTC because their families earn too little (including children in families with no earnings) as compared to about 23 percent of white, non-Hispanic children, Columbia University researchers have found.[119]

A number of proposals would make both the CTC and EITC more effective by making more low- and moderate-income families eligible for the credits and/or boosting their tax credits. For example, a bill from Senators Sherrod Brown, Michael Bennet, Richard Durbin, and Ron Wyden and 42 cosponsors and the companion House bill from Representatives Dan Kildee and Dwight Evans would make the CTC fully refundable so that it reaches children in the poorest families and also would boost the EITC both for workers not raising children in their homes and for workers with children.[120]

The proposal would help low- and moderate-income working families of all races and benefit 17 million Black and Latino households.[121] Black and Latino households would be aided disproportionately by the CTC proposals because they are likelier than white households to have incomes too low to benefit fully from the current credit. They would be aided disproportionately by the EITC improvements as well because, as noted above, they are likelier to earn low wages. The bill would also reduce poverty and “deep poverty” rates (the share of households that live below half of the poverty line) by the largest percentages among households of color, our analysis indicates.[122]

The proposal would also provide funding to help Puerto Rico expand its new, Commonwealth-funded EITC. Puerto Rico residents (excluding federal workers) don’t qualify for the federal EITC; supplementing the Puerto Rico EITC would help combat the island’s very high poverty rate and quite low labor-force participation rate.

This is just one of a number of sound proposals to make the CTC and EITC more effective and inclusive. In particular, Rep. Rosa DeLauro and others in the House and Senator Michael Bennet and others in the Senate have introduced legislation that would both make the CTC fully refundable and substantially expand the generosity of the CTC for children up to age 6.

Curbing or reforming upside-down tax breaks. Policymakers should address federal tax breaks that are ineffective, inefficient, and not racially inclusive. Such tax breaks deliver the bulk of their benefits to the already well-off. Options include paring them back, restructuring them to more effectively target their incentives, eliminating them, or a mixture of approaches.[123]

For example, if policymakers want to maintain a tax incentive for homeownership, they could convert the mortgage interest deduction to a credit so it reaches more lower-income households that need help affording a home,[124] including more households of color. Many households of color would still be locked out of the new credit due to discrimination and other barriers to homeownership, but policymakers could couple it with a new tax credit for renters.[125]

Some tax expenditures should be pared back or eliminated altogether.[126] Savings from eliminating or shrinking inefficient or inequitable tax breaks could go toward expanding refundable tax credits, bolstering key social programs focused on people of limited means, funding more effective and inclusive investments, or reducing budget deficits.

Reforming other parts of the tax code to reduce barriers to building income and wealth. Due to historical and systemic factors as well as policy choices, households of color are especially likely to face barriers preventing them from building significant economic resources. For example, while 40 percent of all households are liquid-asset poor — that is, unable “to cover basic expenses for three months if they experienced a sudden job loss, a medical emergency or another financial crisis leading to a loss of stable income” — the figures for Black and Latino households are 62.7 percent and 62.5 percent, respectively.[127] This makes it harder to weather a financial emergency like a car breakdown without taking on debt. Discriminatory lending practices also make it harder for households of color to access affordable credit.

In designing tax policies intended to help households of color build income, savings, and wealth, policymakers should pay particular attention to helping these households overcome these barriers and secure some of the foundational elements needed for economic stability, security, and prosperity, such as liquid savings. For example, a bill sponsored by a bipartisan group of senators, including Cory Booker and Todd Young, would allow low-income households to use some of their EITC and CTC to create accessible, interest-bearing emergency savings accounts.[128]

Making tax administration and enforcement more inclusive. The IRS needs adequate resources to conduct complex audits and other enforcement activities to better ensure that high-income filers and large corporations — the largest contributors to the tax gap in dollar terms — pay the taxes they owe.[129] This should be coupled with a more aggressive focus on analyzing and reporting on how high-income filers and corporations contribute to the tax gap and how enforcement activities can close it.