Indexing Capital Gains for Inflation Would Worsen Fiscal Challenges, Give Another Tax Cut to the Top

Republican lawmakers are considering “indexing” capital gains for inflation, a change that, like the 2017 tax law, would increase budget deficits, disproportionately benefit the very well-off, and create new opportunities for wealthy filers to avoid taxes by gaming the tax code.[1] Bills to index capital gains have been introduced in both the House and Senate, and House Ways and Means Chairman Kevin Brady has stated that he may add such a provision to the tax package that his committee will likely consider this month (dubbed “Tax Reform 2.0” by House Republican leaders).[2] Recent reports have also indicated that President Trump may direct the Treasury Department to issue a legally questionable regulation that would index capital gains for inflation, bypassing the legislative process altogether.[3]

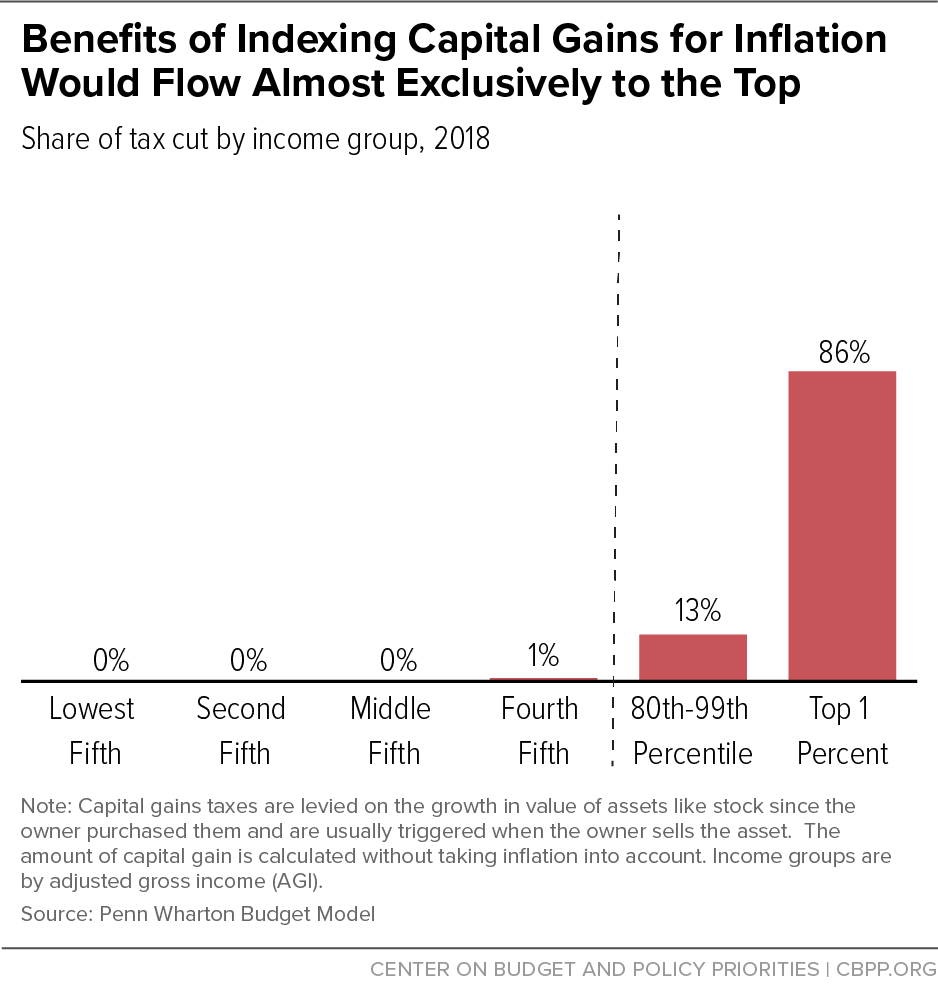

Indexing capital gains for inflation would ultimately cost roughly $100 billion to $200 billion over ten years, Tax Policy Center (TPC) and Penn Wharton Budget Model (PWBM) estimates suggest. [4] The top 1 percent of households would receive an estimated 86 percent of the tax benefits, PWBM estimates.[5] (See Figure 1.)

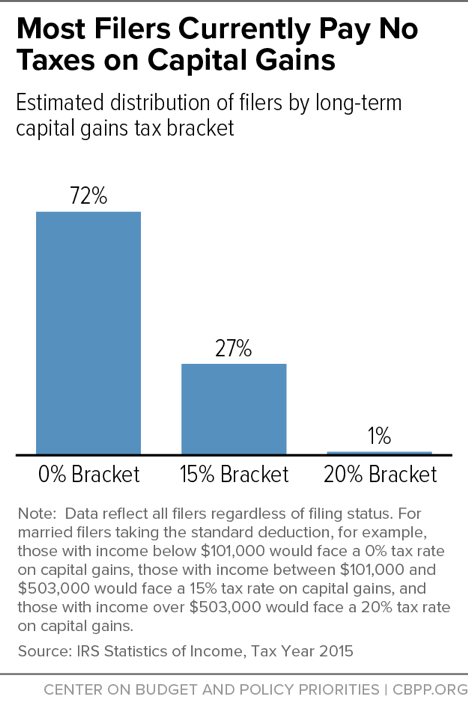

Income taxes on capital gains are levied on the growth in the value of assets like stock since the owner purchased them and are usually triggered when the owner sells the asset. While short-term capital gains are taxed at the ordinary income tax rates that apply to salary and wages, gains on assets held longer than a year are taxed at the “long-term” capital gains rates, which are substantially lower:[6] the rates are zero percent (for most low- and middle-income households), 15 percent, and 20 percent (for the very highest-income households).

The resulting cost would worsen budget deficits, with the benefits flowing overwhelmingly to the wealthiest households, while low- and moderate-income households would see virtually no benefit.The amount of capital gain upon which taxpayers face these rates is calculated without taking inflation into account, so some portion of the taxable capital gain reflects inflation instead of a real gain. Republican lawmakers in the House and Senate have introduced bills to exclude that portion from taxation; this would be accomplished by adjusting upward the purchase price (the basis) of the assets, using adjustments for inflation between the time that the asset was acquired and the time that it was sold.[7] Indexing capital gains for inflation thus would reduce the amount of capital gains subject to taxation, resulting in a tax cut for some households with capital gains, especially those who are affluent. The Trump Administration is apparently considering whether it can achieve the same result through regulation.

Either way, the resulting cost would worsen budget deficits, with the benefits flowing overwhelmingly to the wealthiest households, while low- and moderate-income households would see virtually no benefit. It would create new opportunities for economically inefficient tax avoidance, and, contrary to proponents’ claims, would be unlikely to contribute to economic growth.

Plan Would Lose Much-Needed Revenue, Worsen Long-Term Fiscal Challenges

Indexing capital gains for inflation would ultimately lose roughly $100 billion to $200 billion in revenue over ten years, initial rough estimates from TPC and the PWBM suggest.[8] This would be in addition to the revenue losses from the 2017 tax law, which is projected to cost $1.9 trillion over ten years, and would be on top of Chairman Brady’s proposed permanent extension of the 2017 tax law’s individual tax provisions, which would cost $250 billion in 2027 alone.[9]

Assuming that indexing would apply to gains in the value of assets that accumulated before the legislation was enacted (i.e. “retroactively”), the cost of indexing would be roughly $100 billion to $200 billion over ten years, TPC and the PWBM estimate.[10] (This is almost certainly the way that indexing by regulation would have to be implemented.) Further, the estimates don’t try to account for increased specific tax-avoidance activity that indexing proposals could encourage.

Some approaches to indexing capital gains for inflation would mask part of the cost, as they are designed in a way that much of the cost shows up only outside the ten-year budget window that is used in estimating the official cost of legislation. For example, the PWBM estimates that if capital gains indexing were applied “prospectively” so that only the capital gains accumulated after the legislation’s effective date were indexed for inflation, the cost would be about $50 billion over the first ten years.[11] But that cost would grow as the years passed, as taxpayers sold more assets acquired after the effective date. Over time, a greater and greater share of capital gains would be indexed for inflation.[12]

The bills introduced in the Senate and House follow this route — they would index for inflation gains on assets acquired after the legislation went into effect.[13] Accordingly, they would cost less over the first ten years. But that cost would mount beyond the ten-year budget window as filers sold assets that they acquired after indexing had taken effect.

Regardless of how it is implemented, indexing capital gains would further weaken revenues, increasing the nation’s long-term deficits and debt and leaving it less prepared to address the retirement and health needs arising from the baby boom generation’s retirement as well as other national needs. Meeting these fiscal and policy challenges will require more revenue, not less. Indexing capital gains would move us further from that goal.

The move could also cost state governments billions in lost revenue, as most states base their income taxes on the federal definition of capital gains.[14] Since states must balance their budgets each year, each dollar of reduced tax revenues results in less investment in areas that states fund such as public education, health care, public safety, and human services.

Plan Would Give Another Tax Cut Overwhelmingly to the Wealthiest Households

Nearly all the benefits from indexing capital gains would flow to the wealthy: 86 percent of the total benefits from indexing capital gains would flow to the top 1 percent of households and 99 percent of the benefits would flow to the top fifth of households, the PWBM estimates.[15] Congress and the Administration are considering this policy change on top of the 2017 tax law, which itself included several other large tax giveaways to wealthy households, including a cut in the corporate tax rate, a new deduction for pass-through income, a cut in the estate tax, and a reduction in the top individual income tax rate.[16]

The benefit of indexing capital gains would flow overwhelmingly to those at the top because:

- The most well-off households hold the bulk of all wealth. The wealthiest 1 percent held nearly 39 percent of all wealth in 2016, while the bottom 90 percent held less than 23 percent, the best survey data show.[17] Those with the most wealth reap the greatest share of the gains in wealth’s value — and the largest tax cuts from reducing taxes on those gains.

- Low- and moderate-income people hold much of their savings in tax-preferred accounts that are already not subject to capital gains taxes if the accounts grow in value. To the extent that low- and moderate-income people have savings, they hold a large share of them in tax-preferred retirement accounts such as 401(k)s and Individual Retirement Accounts (IRAs).[18] The growth in the value of assets in these accounts isn’t reported as capital gains, and hence doesn’t face the capital gains rate schedule. (All income in 401(k)s and traditional IRAs is taxed at ordinary income tax rates when funds are withdrawn from those accounts.)

So, both because high-income people hold the most wealth, and because much of the wealth of low- and middle-income people is held in accounts that don’t face taxes on capital gains, a full 69 percent of the capital gains subject to capital gains tax rates flowed to households in the top 1 percent in 2017. Over half of all capital gains subject to capital gains taxes flows to households in the top 0.1 percent, TPC estimates.[19]

- When low- and moderate-income people receive capital gains income outside of tax-preferred accounts, the bulk of those gains face a 0 percent capital gains tax rate. The tax benefit of indexing capital gains is proportional to the tax rate on capital gains that households face. The tax rate on long-term capital gains for a married couple making $1 million is 20 percent, but the rate is 0 percent for a married couple making up to about $100,000.[20] Thus, the bulk of middle-income families would receive no additional tax benefit from indexing capital gains for inflation, since they already face no tax on such gains. More than 70 percent of filers would fall into this group, according to IRS data.[21] (See Figure 2.)

By contrast, the highest-income households would save up to 20 cents per dollar on all capital gains that were exempted by indexing capital gains for inflation. That’s why the tax cut from indexing capital gains for inflation is even more concentrated at the top than capital gains income itself. (See Figure 1.)[22]

The PWBM estimates of the share of the tax cut flowing to the top include the distribution of only the federal tax cut resulting from indexing capital gains. As noted, this change also would result in cuts in state (individual and corporate) income taxes on capital gains in states that use the federal definition of capital gains in their tax codes. These state capital gains cuts would similarly be concentrated on the wealthiest households and would make state tax systems even more regressive than they already are.[23]

Some proponents of indexing capital gains, like National Economic Council Director Larry Kudlow, gloss over the host of preferences in the tax code that capital gains already enjoy.[24] For instance, the 20 percent top tax rate on long-term capital gains is significantly lower than the current top rate of 37 percent on wages and salaries. Further, because taxes on capital gains are due when assets are sold rather than when gains are made, asset owners have considerable discretion over when they pay the tax. One justification offered for the costly and regressive preferences for capital gains income already featured in the federal income tax code is that they roughly adjust for the lack of inflation indexing for capital gains.[25] Even if one were to accept that argument, indexing capital gains without addressing its current very generous preferences would amount to a second helping of tax breaks purportedly to adjust for inflation.

Plan Would Invite High-Income Taxpayers to Game the System

Indexing capital gains without indexing other parts of the tax code would create new opportunities for tax avoidance.[26] Consider, for example, a taxpayer who borrows funds to buy an asset. Her interest payments, which partly reflect the expected impact of inflation, are deductible. Adjusting only her capital gain for inflation — and not the deduction of her interest payments — would thus affect only half of the tax equation. For example, if the asset grew in value at the rate of inflation, she would owe no taxes on the capital gains she received but could still deduct the full amount of her interest payments. This means that an individual could engage in transactions with no real economic change in order to reduce his or her taxes.

The various bills introduced in Congress to index capital gains do not make the adjustments elsewhere in the tax code that would be needed to prevent gaming of the type described above. And indexing capital gains by regulation couldn’t attempt to stop such tax avoidance; doing so would require altering various other parts of the tax code, and not even proponents of indexing capital gains by regulation have asserted that the Administration has the legal authority to do that.

Cutting Taxes on Capital Gains Unlikely to Spur Economic Growth

Supporters of indexing capital gains argue that reducing taxes on capital gains will have a “profound pro-growth impact” on the economy. In fact, as the nonpartisan Congressional Research Service has noted, “it is unlikely […] a significant, or any, effect on economic growth would occur from a stand-alone indexing proposal.”[27] Furthermore, lowering taxes on capital gains by indexing gains could harm economic growth over the long run by increasing budget deficits, reducing revenues for investment in priorities that can help the economy to grow, and encouraging economically inefficient tax avoidance shelters.

- There is little evidence that lower capital gains taxes increase private savings and investment. Multiple studies have noted that capital gains tax rates appear to have little or no effect on private saving.[28] These findings match billionaire investor Warren Buffett’s observation that “I have worked with investors for 60 years and I have yet to see anyone — not even when capital gains rates were 39.9 percent in 1976-77 — shy away from a sensible investment because of the tax rate on the potential gain. People invest to make money, and potential taxes have never scared them off.”[29]

- Indexing is costly: it would increase budget deficits and reduce national saving. As discussed above, indexing capital gains for inflation would ultimately result in revenue losses of roughly $100 billion-$200 billion over ten years, compounding the $1.9 trillion cost of the 2017 tax law and further increasing federal budget deficits.[30] As cutting taxes on capital gains for the wealthy would likely have little impact on private saving, national saving (which is the net of private saving and government dissaving through running budget deficits) would decrease. Most economists who have studied this matter conclude, based on empirical studies, that large reductions in national saving mean that less capital ultimately would be available for investment in the economy and interest rates would eventually rise. While interest rates — and the cost of government borrowing — are currently low (and are projected to stay low in the near term under current policies), they won’t necessarily stay low, especially if debt rises inexorably as a share of the economy.

Alternatively, if capital gains tax cuts are ultimately funded by cutting productive public investments that help support growth (such as education, job training, basic research, and infrastructure), that also could harm the economy.[31] Further, as noted above, indexing could cost states billions in lost revenue and lead to less investment by states in priorities that can strengthen their economies and that of the nation over the long term.

- Indexing would encourage more economically inefficient tax avoidance. As discussed above, capital gains are already taxed at substantially lower rates than other salaries and wages. This disparity fuels tax shelters “devoted to converting fully taxed income into capital gains.”[32] Further reducing the taxes on capital gains would provide even greater incentives for wealthy people to use tax shelters to reduce their tax liabilities. Tax shelter schemes are inefficient because, as noted tax policy expert Leonard Burman has observed, “shelter investments are invariably lousy, unproductive ventures that would never exist but for tax benefits” and money directed to them then isn’t available for activities that could otherwise contribute to economic growth.[33] Moreover, the resources devoted to setting up these shelters, such as engaging tax lawyers and accountants, may divert resources and talent away from more productive activities.

Trump Administration Lacks Legal Authority to Index Capital Gains Through Regulation

The Treasury Department and the Department of Justice conducted a rigorous legal analysis in 1992 and determined that Treasury does not have the legal authority to index capital gains for inflation.[34] The analysis found that under section 1012 of the Internal Revenue Code (IRC), the “cost” of an asset used to calculate capital gains does not mean “inflation-adjusted cost” as indexing proponents argue, but rather the nominal price that the owner paid for the asset. (To reach this conclusion, Treasury carefully examined both the dictionary definition of “cost” and the term’s context in section 1012.)

Proponents of indexing capital gains argue that legal developments since 1992 should enable Treasury to reinterpret “cost” as “inflation-adjusted cost.” However, a recent paper by Daniel Hemel and David Kamin shows that this argument is baseless, and if anything, Treasury’s authority to index capital gains is weaker than it was in 1992:[35]

- Indexing proponents cite the 2002 Verizon Communications case, in which the Supreme Court stated that dictionary definitions don’t determine the meaning of “cost” in a section of the Telecommunications Act and that in the specific context of the Telecommunications Act, “cost” was inflation indexed. But as noted above, Treasury’s 1992 analysis relied not only on the dictionary definition of “cost” but also on a range of other interpretive tools, including an investigation of the term’s meaning within the context of the IRC. And the Verizon Communications decision emphasized that when interpreting statutes, context is vital.

- In addition, a number of courts, including the Supreme Court in a 1936 case, have suggested over time that “cost” in section 1012 (or its predecessors) is unambiguous and refers to the nominal amount paid for property. Indexing proponents suggest that a 2005 Supreme Court case (Brand X) indicates that those previous decisions — and Treasury’s long-standing interpretation — do not eliminate Treasury’s latitude on this issue and that Treasury would be owed deference if it were to change the interpretation. Hemel and Kamin explain, however, that indexing proponents are misreading the Brand X case and that its logic, in fact, cuts against their position. Specifically, Brand X says that if courts previously found the meaning of a statute to be unambiguous, those decisions would determine the outcome; Treasury would only have leeway if the decisions were made in the face of ambiguity as to the statute’s meaning. And the best reading of those previous cases suggests that the courts found there wasn’t any ambiguity in section 1012 regarding the meaning of “cost.” That’s also consistent with Treasury’s 1992 analysis.

- Indexing proponents note that in the 2012 Mayo Foundation case, the Supreme Court made clear that the “Chevron” approach to interpreting statutes — which states that if a statute is ambiguous and the administrative agency’s interpretation is reasonable, courts will defer to the agency’s interpretation — should be used in tax law just as in other areas of law. But the Mayo case doesn’t call Treasury’s 1992 analysis into question, Hemel and Kamin explain, because Treasury already assumed in 1992 that the Chevron approach was appropriate for analyzing Treasury’s discretion when it came to indexing. Using that framework, Treasury still found that there wasn’t discretion here, given the lack of ambiguity in the statute.

- Hemel and Kamin also cite a major doctrinal development since 1992 making it even less likely that the courts would allow Treasury to assert the IRC gives it discretion to index capital gains. A series of Supreme Court decisions have narrowed agency discretion and the application of Chevron deference, especially when it comes to questions of “vast economic and political significance.” As Hemel and Kamin explain, these decisions suggest that “linguistic ambiguity on its own,” even if that existed in this context, wouldn’t necessarily cause the courts to defer to an agency’s interpretation of the word “cost.” According to these decisions, “courts must consult contextual clues and common sense before concluding that Congress has delegated a decision of ‘vast economic and political significance’ to an agency.” For several reasons, including the huge cost of indexing capital gains, Hemel and Kamin find that “it simply belies common sense to conclude that Congress would delegate to Treasury what is essentially a binary choice: cut the effective tax rate on capital gains by one-third or not at all.”

If Treasury were to nevertheless assert that it possesses the authority to index capital gains and then did so, a number of parties could plausibly challenge it in court, Hemel and Kamin note. But they argue the specter of being challenged in court shouldn’t be the only thing that dissuades the Administration from this course: “As a policy matter, indexing [capital gains] for inflation via regulatory action would be a recipe for arbitrage, revenue losses, and even wider wealth inequality. As a legal matter, the same arguments that led officials in the first Bush administration to reject the idea in 1992 are applicable today.”

End Notes

[1] Brendan Duke, “House Republicans’ New Tax Plan Doubles Down on 2017 Tax Law’s Flaws,” CBPP, July 24, 2018, https://www.cbpp.org/blog/house-republicans-new-tax-plan-doubles-down-on-2017-tax-laws-flaws; Chuck Marr, Brendan Duke, and Chye-Ching Huang, “New Tax Law Is Fundamentally Flawed and Will Require Basic Restructuring,” CBPP, updated August 14, 2018, https://www.cbpp.org/research/federal-tax/new-tax-law-is-fundamentally-flawed-and-will-require-basic-restructuring.

[2] Bernie Becker, “How do you get a floor vote?,” Politico, July 25, 2018, https://www.politico.com/newsletters/morning-tax/2018/07/25/how-do-you-get-a-floor-vote-296963; H.R. 1261: Capital Gains Inflation Relief Act of 2007, https://www.congress.gov/bill/110th-congress/house-bill/1261/text.

[3] Alan Rappeport and Jim Tankersley, “Trump Administration Mulls a Unilateral Tax Cut for the Rich,” New York Times, July 30, 2018, https://www.nytimes.com/2018/07/30/us/politics/trump-tax-cuts-rich.html; John Micklethwait, Margaret Talev, and Jennifer Jacobs, “Trump Says He’s Thinking About Indexing Capital Gains to Inflation,” Bloomberg, August 30, 2018, https://www.bloomberg.com/news/articles/2018-08-30/trump-says-thinking-about-indexing-capital-gains-to-inflation.

[4] Leonard Burman, “Should Treasury Index Capital Gains?,” Tax Policy Center, May 10, 2018, https://www.taxpolicycenter.org/taxvox/should-treasury-index-capital-gains; John Ricco, Efraim Berkovich, and Richard Prisinzano, “No Bang for the Bucks – Indexing Capital Gains Doesn’t Lead to Economic Growth,” Penn Wharton Budget Model, August 20, 2018, http://budgetmodel.wharton.upenn.edu/issues/2018/8/20/no-bang-for-the-bucks-indexing-capital-gains-doesnt-lead-to-economic-growth.

[5] John Ricco, “Indexing Capital Gains to Inflation,” Penn-Wharton Budget Model, March 23, 2018, http://budgetmodel.wharton.upenn.edu/issues/2018/3/23/indexing-capital-gains-to-inflation. TPC has not yet issued an estimate of the distribution of the tax cut from indexing capital gains for inflation.

[6] Chye-Ching Huang, “Indexing Capital Gains Would Be Yet Another Tax Cut For Top 1 Percent,” CBPP, August 1, 2018, https://www.cbpp.org/blog/indexing-capital-gains-would-be-yet-another-tax-cut-for-top-1-percent.

[7] H.R. 6444: Capital Gains Inflation Relief Act of 2018, https://www.congress.gov/bill/115th-congress/house-bill/6444/text?format=txt; S. 2688: Capital Gains Inflation Relief Act of 2018, https://www.congress.gov/bill/115th-congress/senate-bill/2688.

[8] Burman, 2018; Ricco, Berkovich, and Prisinzano.

[9] Letter from Thomas A. Barthold to Warren Gunnels, “Revenue Estimates of Making Permanent Certain Provisions Enacted in 2017,” September 4, 2018, https://twitter.com/BBKogan/status/1037353559963193344.

[10] Burman, 2018; Ricco, Berkovich, and Prisinzano.

[11] Ricco, Berkovich, and Prisinzano.

[12] Ibid. Penn Wharton estimates that the cost of a prospective indexing policy grows to about $160 billion over a 20-year budget window.

[13] The bills would therefore create an incentive to sell and “reacquire” existing assets as soon as the law went into effect.

[14] Huang, “Indexing Capital Gains Would Be Yet Another Tax Cut for Top 1 Percent.”

[15] Ricco, 2018.

[16] Chuck Marr, Brendan Duke, and Chye-Ching Huang, “New Tax Law Is Fundamentally Flawed and Will Require Basic Restructuring,” CBPP, updated August 14, 2018, https://www.cbpp.org/research/federal-tax/new-tax-law-is-fundamentally-flawed-and-will-require-basic-restructuring.

[17] “Changes in U.S. Family Finances from 2013 to 2016: Evidence from the Survey of Consumer Finances,” Board of Governors of the Federal Reserve System, September 2017, https://www.federalreserve.gov/publications/files/scf17.pdf; Chad Stone et al., “A Guide to Statistics on Historical Trends in Income Inequality,” CBPP, updated August 29, 2018, https://www.cbpp.org/research/poverty-and-inequality/a-guide-to-statistics-on-historical-trends-in-income-inequality. While there is considerable overlap, the top 1 percent of the income distribution does not contain the identical group of people as the top 1 percent of the wealth distribution.

[18] CBPP analysis of Survey of Consumer Finances data, using tables from Edward N. Wolff, “Household Wealth Trends in the United States, 1962 to 2016: Has Middle Class Wealth Recovered?” NBER Working Paper No. 24085, November 2017, http://www.nber.org/papers/w24085. The benefit of these tax-preferred retirement accounts is still skewed to the highest-income filers, as they have the most wealth to save in these accounts and also receive the greatest benefit per dollar of tax savings. See Chuck Marr, Nathaniel Frentz, and Chye-Ching Huang, “Retirement Tax Incentives Are Ripe for Reform,” CBPP, December 13, 2013, https://www.cbpp.org/research/retirement-tax-incentives-are-ripe-for-reform.

[19] TPC Table T17-0082. In 2018, only 8 percent of households in the middle 60 percent of the income distribution reported any long-term capital gains that might face potential taxes on capital gains, compared to 59 percent of households in the top 1 percent, according to TPC Table T18-0053.

[20] Brendan Duke, “Universal Savings Account Proposal in House Republican Tax Framework Is Ill-Conceived,” CBPP, August 14, 2018, https://www.cbpp.org/research/federal-tax/universal-savings-account-proposal-in-house-republican-tax-framework-is-ill.

[21] Internal Revenue Service, Table 3.4: All Returns: Tax Classified by Both the Marginal Rate and Each Rate at Which Tax Was Computed, by Marital Status, Tax Year 2015 (Filing Year 2016), https://www.irs.gov/statistics/soi-tax-stats-individual-statistical-tables-by-tax-rate-and-income-percentile. The 2017 tax law’s capital gains tax brackets were designed to almost exactly replicate the ordinary income tax brackets that were previously used to set capital gains tax brackets. This means that the proportion of households in the 0 percent bracket under the 2017 tax law should be roughly the same as for tax year 2015.

[22] Ibid.

[23] Nicholas Johnson, “State and Local Tax Systems Disproportionately Burden Lower-Income Families,” CBPP, January 30, 2013, https://www.cbpp.org/blog/state-and-local-tax-systems-disproportionately-burden-lower-income-families

[24] Larry Kudlow, “Index capital gains for inflation, Mr. President,” CNBC, August 11, 2017, https://www.cnbc.com/2017/08/11/index-capital-gains-for-inflation-mr-president.html.

[25] Chuck Marr and Chye-Ching Huang, “Raising Today’s Low Capital Gains Tax Rates Could Promote Economic Efficiency and Fairness, While Helping Reduce Deficits,” CBPP, September 19, 2012, https://www.cbpp.org/research/raising-todays-low-capital-gains-tax-rates-could-promote-economic-efficiency-and-fairness.

[26] Chye-Ching Huang, “Research Note: New Paper Sets Out Policy and Legal Case Against Indexing Capital Gains by Regulation,” CBPP, June 11, 2018, https://www.cbpp.org/research/federal-tax/research-note-new-paper-sets-out-policy-and-legal-case-against-indexing-capital.

[27] Ryan Ellis, “Not just Mr. Moneybags: Ending the capital gains inflation tax helps ordinary Americans too,” Washington Examiner, August 8, 2018, https://www.washingtonexaminer.com/opinion/not-just-mr-moneybags-ending-the-capital-gains-inflation-tax-helps-ordinary-americans-too; Jane G. Gravelle, “Indexing Capital Gains Taxes for Inflation,” Congressional Research Service, July 24, 2018, https://fas.org/sgp/crs/misc/R45229.pdf.

[28] Chuck Marr and Chye-Ching Huang, “Raising Today’s Low Capital Gains Tax Rates Could Promote Economic Efficiency and Fairness, While Helping Reduce Deficits,” CBPP, September 12, 2012, https://www.cbpp.org/research/raising-todays-low-capital-gains-tax-rates-could-promote-economic-efficiency-and-fairness.

[29] Corbett Daly, “Warren Buffet wants to pay higher taxes,” CBS, August 15, 2011, https://www.cbsnews.com/news/warren-buffett-wants-to-pay-higher-taxes/.

[30] Burman, 2018; Ricco, Berkovich, and Prisinzano.

[31] Chad Stone, “Economic Growth: Causes, Benefits, and Current Limits,” CBPP, April 27, 2017, https://www.cbpp.org/economy/economic-growth-causes-benefits-and-current-limits.

[32] Len Burman, “Mitt Romney’s Teachable Moment on Capital Gains,” Forbes, January 18, 2012, https://www.forbes.com/sites/leonardburman/2012/01/18/mitt-romneys-teachable-moment-on-capital-gains/#3a9303ce7a4e.

[33] Ibid.

[34] Timothy E. Flanigan, “Legal Authority of the Department of the Treasury to Issue Regulations Indexing Capital Gains for Inflation,” September 1, 1992, https://www.justice.gov/file/20536/download.

[35] Associate Professor Daniel Hemel (University of Chicago Law School) and Professor David Kamin (New York University School of Law), “The False Promise of Presidential Indexation,” SSRN, May 24, 2018, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3184051.

More from the Authors