New House Republican Tax Proposal Fails Fiscal Responsibility Test, While Favoring the Wealthiest

The House is expected to vote later this month on its “2.0” tax plan, a tax-cut bill that would double down on the 2017 tax law’s flaws by once again delivering substantially more to high-income households than to those with low and moderate incomes, adding considerably to the nation’s long-term fiscal challenges, and creating opportunities for tax avoidance by wealthy filers.[1] The centerpiece of this tax-cut package is the permanent extension of the 2017 tax law’s individual provisions that are slated to expire after 2025.[2] House leaders have introduced other bills that include other provisions, though they are dwarfed by the outsized effects of continuing the 2017 tax law’s individual provisions. The permanent extension of those provisions would:

Rather than enacting legislation that would double down on the 2017 tax law’s flaws, policymakers should set a new course by restructuring the 2017 tax law.

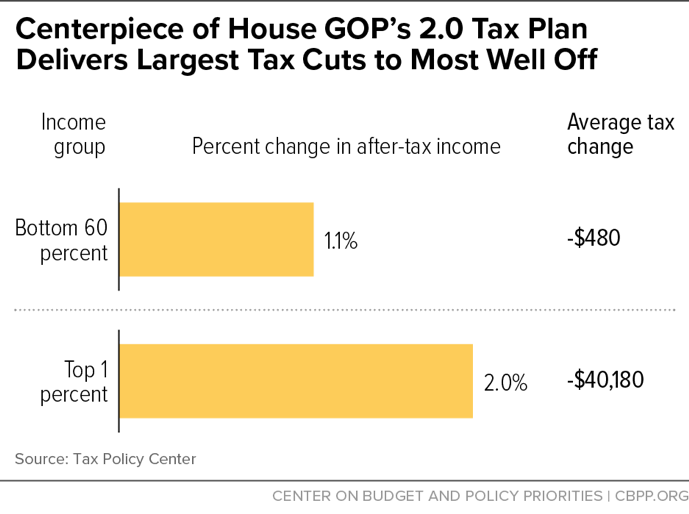

- Ignore decades-long working-class wage stagnation and exacerbate income inequality by benefitting households in the top 1 percent about twice as much as those in the bottom 60 percent, measured as a share of income, according to Tax Policy Center estimates. Average after-tax incomes of the top 1 percent (those with incomes above $836,200 in 2026) would rise 2.0 percent, with an average tax cut of $40,180, while the incomes of the bottom 60 percent (those with incomes below $95,000) would rise by only 1.1 percent, with an average tax cut of $480. (See Figure 1.)

- Aggravate the need for more revenue to address the nation’s fiscal challenges by delivering another unpaid-for tax cut. Extending the 2017 tax law’s individual provisions would cost $631 billion between 2019-2028, according to the Joint Committee on Taxation (JCT).[3] But this understates the fiscal damage; the estimate doesn’t show the true long-run costs because virtually all of these provisions would have effect only in the final years of the decade. By 2027, extending these provisions would cost about $250 billion a year, or more than 0.8 percent of GDP. These provisions would cost about $2.8 trillion in the first ten years after becoming permanent (2026-2035). The cost of making them permanent in the decade after the 2019-2028 budget window (2029-2038) would be $3.2 trillion, according to the Tax Policy Center.

- Risk undermining the integrity of the tax code by making permanent the 20 percent deduction for “pass-through income,” a provision that encourages tax gaming and avoidance schemes. The deduction — which is available to certain owners of businesses such as partnerships, S corporations, and sole proprietorships — creates a strong incentive for high-income individuals to recharacterize their wage and salary income as pass-through profits so they can take advantage of this tax break.

Rather than enacting legislation that would double down on the 2017 tax law’s flaws, policymakers should set a new course by restructuring the 2017 tax law.

Ignores Working-Class Wage Stagnation and Shifts More Income Upward

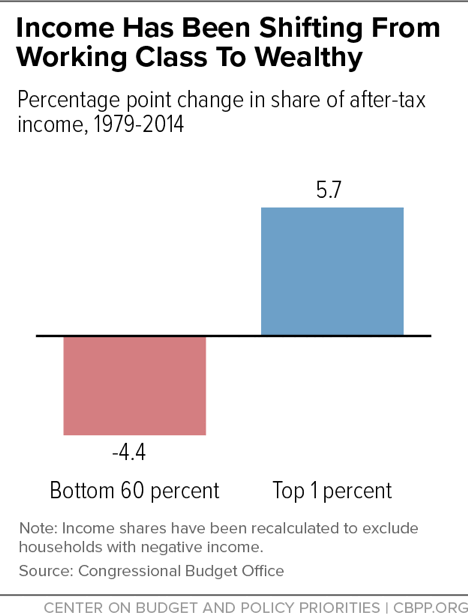

The economic environment in the last few decades has been particularly difficult for working-class households (defined here as families with working-age adults in which no one has a college degree).[4] The after-tax income of a typical working-class family of three would have been about $9,600 higher ($58,300 instead of $48,700) in 2015 if its income had grown at the same rate since 1979 as that of a typical household with a college degree.[5] Meanwhile, incomes at the top of the spectrum have increased dramatically, leading to a pronounced income shift. Between 1979 and 2014, the share of income flowing to the bottom 60 percent fell by 4.4 percentage points, while the share flowing to the top 1 percent rose by 5.7 percentage points, Congressional Budget Office (CBO) analysis shows.[6] (See Figure 2.)

The 2017 tax law exacerbated this trend and will further increase income inequality by delivering larger tax cuts, measured as a percent of after-tax income, to the top 1 percent than to the bottom 60 percent. And any tax bill the House considers this fall will do the same if its core is making permanent the individual tax provisions enacted in 2017 that are set to expire after 2025.[7] Like the 2017 tax law as a whole, the individual provisions’ benefits are tilted heavily toward those at the top of the income spectrum. Making these changes permanent, as the bill would do, would lock this skewed distribution into the tax code.

Making the 2017 tax law’s individual provisions permanent would deliver an average tax cut of $40,180 to households in the top 1 percent (those with incomes above $836,200), increasing their after-tax incomes by 2.0 percent. That’s about double the after-tax income gain to households in the bottom 60 percent of the income spectrum (those with incomes below $95,000), which would receive average tax cuts of $480, boosting their after-tax incomes by 1.1 percent.[8] (See Figure 1.)

It’s not surprising that the benefits of making the individual provisions permanent flow overwhelmingly to the well-off, given the major provisions of that part of the package:

- The 20 percent deduction for pass-through income. Pass-through income is income that the owners of businesses such as partnerships, S corporations, and sole proprietorships report on their individual tax returns. Before the 2017 law, it was taxed at the same individual rate as a business owner’s other ordinary income, like wages and salaries.

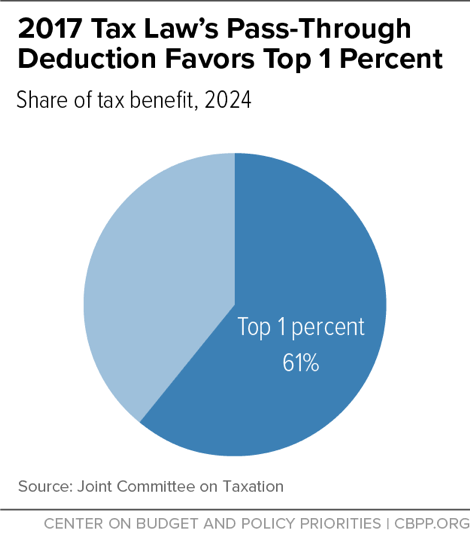

The deduction for pass-through income effectively cuts the marginal individual tax rate on this income by one-fifth. This provision will deliver 61 percent of its benefit to households in the top 1 percent, according to the Joint Committee on Taxation.[9] (See Figure 3.) It is heavily tilted to high-income households for three reasons. First, they get a disproportionate share of pass-through income; the top 1 percent alone receives more than half of such income. Second and relatedly, pass-through income makes up a much larger share of the income of high-income households than of low- and middle-income households. Third, each dollar of pass-through income that is deducted is worth more as a tax break for high-income people, since they face higher regular individual tax rates.

- Cutting the top individual income tax rate to 37 percent. The 2017 law reduced the top individual income tax rate from 39.6 percent to 37 percent. For married couples, this benefits those making over $600,000 in taxable income. By itself, this rate cut will give a couple with $2 million in taxable income a $36,400 tax cut each year.[10] Wealthy households also benefit from the law’s cuts in the other individual rates: together, the rate cuts produce a tax reduction of $56,765 each year for a married couple with $2 million in taxable income.

- Weakening the Alternative Minimum Tax (AMT). The AMT is a parallel tax system designed to ensure that higher-income people who take large amounts of deductions and other tax breaks pay at least a minimum level of tax. The 2017 law raised both the amount of income that’s exempt from the AMT (from $86,200 to $109,400 for a married couple) and the income level above which this exemption begins to phase out (from $164,100 to $1 million for a married couple). The House GOP tax proposal locks in this weakened AMT, extending this tax cut for affluent households.[11]

- A $22 million-per-couple estate tax exemption. The proposal locks in the doubling of the amount that the wealthiest households can pass on tax free to their heirs, from $11 million per couple to $22 million. This is many times the lifetime earnings of a typical high school graduate.[12] Moreover, the few estates large enough to remain taxable — those worth more than $22 million per couple — receive a tax cut of $4.4 million apiece. Much of the wealth that the new estate tax provisions shield from taxation consists of “unrealized” capital gains that have never been taxed, with the result that those who inherit the money won’t ever have to pay tax on these windfalls.[13]

The benefits of the 2017 tax law’s individual provisions — and the House tax bill — are skewed to the top for another reason as well, because they fail to do much to help low- and moderate-income working-class families. One of the most important provisions in the tax code for those families is the Earned Income Tax Credit (EITC), and a well-designed EITC expansion could significantly raise working-class incomes. The House Republican leaders’ new tax proposal, like the 2017 law, ignores the EITC. Moreover, the proposal continues to deny the 2017 law’s full increase in the Child Tax Credit to millions of families with low-wage earning parents.[14]

Making the 2017 tax law’s individual provisions permanent could also leave low- and moderate-income households worse off in the long run. The roughly $250 billion permanent annual cost of doing so will have to be paid for at some point, through program cuts and/or tax increases that likely would reduce many low- and middle-income families’ incomes more than the tax cuts increase them. Using the scenario for paying for the law that most closely resembles the recent House Republican budget — which includes $1.5 trillion in cuts to Medicaid and Affordable Care Act premium tax credits[15] — we find that the average $480 tax cut for households in the bottom 60 percent would become an average $1,130 reduction (2.6 percent) in their after-tax incomes.[16]

Loses Substantial Revenue Despite Need for More

The aging of the nation’s population will create obvious fiscal pressures, pushing up the cost of programs such as Social Security, Medicare, and Medicaid. When combined with other factors such as rising interest rates, a decaying infrastructure, inadequate child care for working families, and a range of other unmet needs, the federal government will need to raise more revenue to prevent an unsustainable rise in the nation’s debt ratio in future decades. Despite these needs, the 2017 tax law is expected to cost $1.9 trillion between 2018-2027, according to CBO. The House GOP’s 2.0 plan would make all of this drain on revenues permanent.

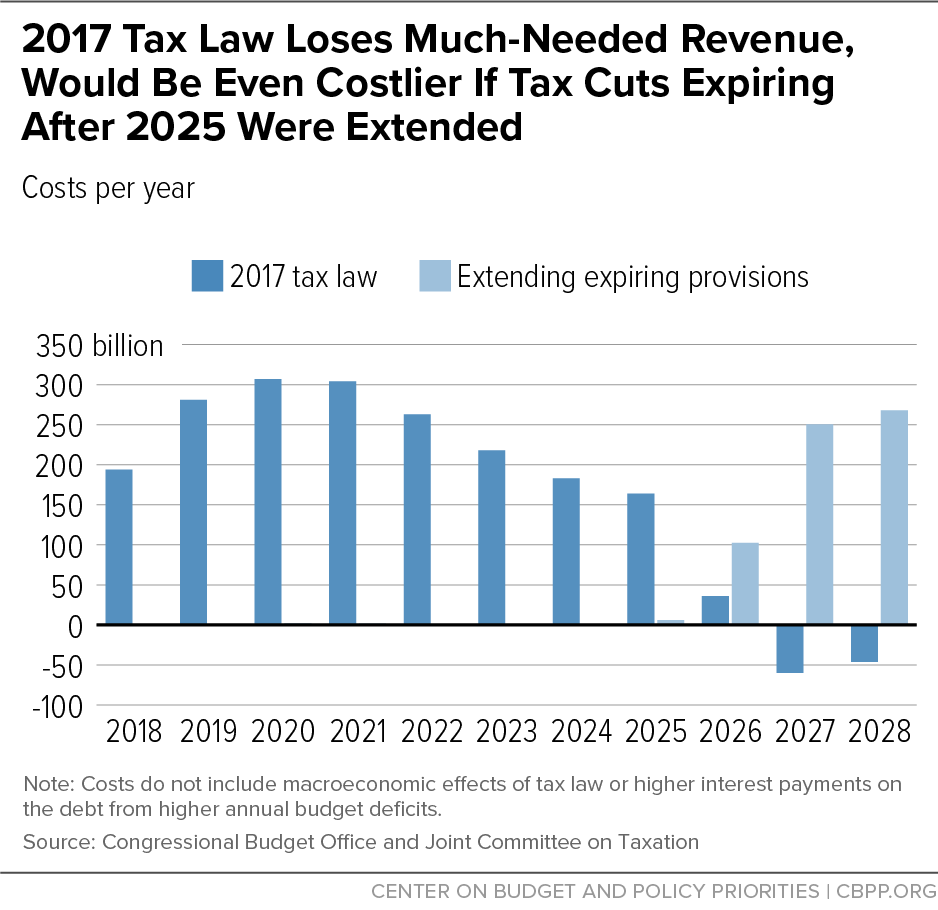

Making the individual provisions permanent would cost $631 billion between 2019-2028 according to JCT, but that cost estimate mostly reflects the additional cost of extending the tax cuts for 2026, 2027, and 2028 and thus doesn’t reflect the true long-run cost.[17] Making those individual provisions permanent would cost $250 billion in 2027 alone (see Figure 4), amounting to more than 0.8 percent of GDP. If the cost of these provisions remained constant as a share of GDP, the cost of making them permanent in the first ten years they will all be in effect (2026-2035) would be about $2.8 trillion, we estimate. The cost of making them permanent in the decade after the 2019-2028 budget window (2029-2038) would be $3.2 trillion, according to the Tax Policy Center.[18]

Extending the 2017 tax law’s individual provisions would put revenue as a share of GDP at 17.7 percent in 2027.[19] While this would be slightly above the average level over the last 40 years, the foreseeable upward pressure on spending, combined with an already elevated debt-to-GDP ratio, means that policymakers will need to raise significant additional revenue over the next two decades. To keep pace with the estimated spending growth, revenues would need to rise to 20.5 percent of GDP by 2035 to stabilize the debt-to-GDP ratio.[20] Extending the individual provisions of the 2017 tax law would put the United States further from the level of revenue needed to adequately finance critical national needs without letting debt continue to rise inexorably as a share of the economy.

Encourages Tax Gaming and Avoidance

The 2017 tax law encourages rampant tax gaming and is an open invitation to wealthy people to try to avoid the top individual tax rate. It “has turned us into a nation of tax shelter hunters,” the Tax Policy Center’s Howard Gleckman has observed.[21] Among the most egregious of these opportunities is the deduction for pass-through income — an ill-conceived provision that the tax bill would make permanent rather than fix.

As described above, before the 2017 law, pass-through income was taxed at the same individual rate as the business owner’s other ordinary income, like wages and salaries. The new law makes it eligible for a 20 percent deduction, creating an incentive for high-income individuals to reclassify as much of their salaries as possible as pass-through income. Making this provision permanent would further encourage high-income taxpayers to use complex tax avoidance schemes to lower their taxes.

To take just one example, many S corporation owners receive both wages from the S corporation and a share of the S corporation’s profits. They pay payroll tax only on the part received as wages. Even before the 2017 tax law, this gave them an incentive to underreport the share of their income that consists of “reasonable compensation” for their labor and overstate the share that is due to profits, in order to shrink their payroll tax liability.[22]

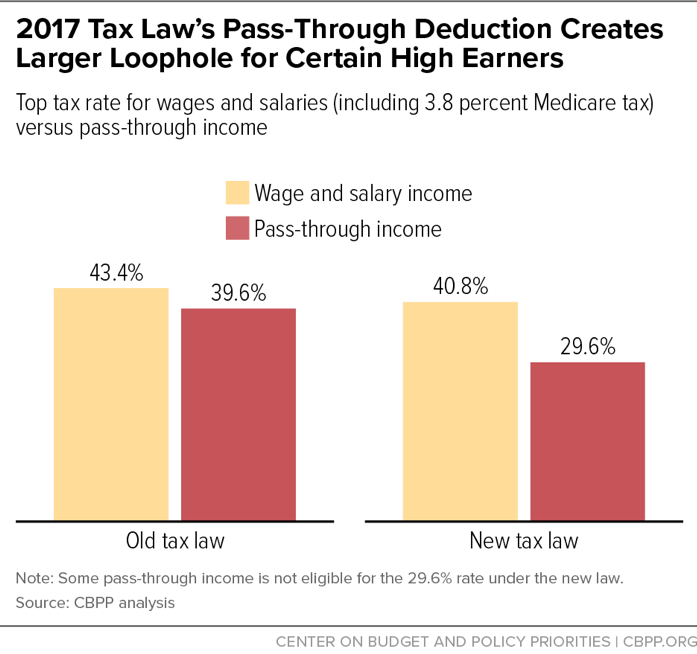

S-corporation owners previously could reduce their tax rate by 3.8 percentage points (reflecting the Medicare payroll tax that high earners pay) through this maneuver. Under the 2017 tax law, however, the tax-rate differential between wage and salary income and pass-through income eligible for the new 20 percent deduction has jumped from 3.8 percentage point to 11.2 percentage points, nearly tripling the tax break from converting ordinary income into income eligible for the pass-through deduction[23] (See Figure 5.) These taxpayers now have a much greater incentive to recharacterize wage and salary income as pass-through-profit income.

End Notes

[1] For an examination of the 2017 tax law’s shortcomings, see Chuck Marr, Brendan Duke, and Chye-Ching Huang, “New Tax Law Is Fundamentally Flawed and Will Require Basic Restructuring,” Center on Budget and Policy Priorities, updated August 14, 2018, https://www.cbpp.org/research/federal-tax/new-tax-law-is-fundamentally-flawed-and-will-require-basic-restructuring.

[2] One of the other bills includes a “Universal Savings Account” (USA) proposal. For an analysis of USAs, see Brendan Duke, “’Universal Savings Account’ Proposal in New Republican Tax Bill Is Ill-Conceived,” CBPP, updated September 11, 2018, https://www.cbpp.org/research/federal-tax/universal-savings-account-proposal-in-house-republican-tax-framework-is-ill.

[3] When including the cost of the the tax plan’s other provisions not related to extending the 2017 tax law, the cost rises to $657 billion. Joint Committee on Taxation, “Estimated Revenue Effects of H.R. 6760,” September 12, 2018, https://www.jct.gov/publications.html?func=startdown&id=5136.

[4] Though much commentary, especially about the 2016 election, has focused on the “white working class,” the working class is diverse and working-class households of different races and ethnicities have secured only modest gains over the 1979-2015 period. See Chuck Marr, Brandon DeBot, and Emily Horton, “How Tax Reform Can Raise Working-Class Incomes,” CBPP, updated October 13, 2017, https://www.cbpp.org/research/federal-tax/how-tax-reform-can-raise-working-class-incomes.

[5] Ibid.

[6] The share of income going to the top 1 percent increased from 7.4 to 13.1 percent, while the share going to the bottom 60 percent fell from 36.3 to 31.9 percent. Congressional Budget Office, “The Distribution of Household Income, 2014,” March 19, 2018, https://www.cbo.gov/publication/53597. Income shares have been recalculated to exclude households with negative income.

[7] The 2017 tax law’s two permanent provisions other than the permanent corporate tax cuts were the repeal of the Affordable Care Act’s individual mandate, which results in health care cuts and higher premiums in the individual insurance market, and changing the inflation measure by which key tax parameters are adjusted for inflation, which will push households into higher tax brackets over time and reduce the value of the Earned Income Tax Credit. See Chuck Marr, “Republicans Chose Corporate Shareholders Over Working Families,” CBPP, December 19, 2017, https://www.cbpp.org/blog/republicans-chose-corporate-shareholders-over-working-families.

[8] Tax Policy Center Table T18-0133, https://www.taxpolicycenter.org/model-estimates/hr-6760-protecting-family-and-small-business-tax-cuts-act-2018-introduced-1.

[9] Chuck Marr, “JCT Highlights Pass-Through Deduction’s Tilt Toward the Top,” CBPP, April 24, 2018, https://www.cbpp.org/blog/jct-highlights-pass-through-deductions-tilt-toward-the-top.

[10] Marr, Duke, and Huang 2018.

[11] To be sure, some provisions of the 2017 tax law raise taxes on high-income households, such as its limit on the deduction for state and local taxes. But the progressive provisions are overwhelmed by the regressive ones, resulting in a highly regressive law overall, as the Tax Policy Center analysis cited in the text shows.

[12] Christopher R. Tamborini, ChangHwan Kim, and Arthur Sakamoto, “Education and Lifetime Earnings in the United States,” Demography, 52 (4) (2015): 1383-1407.

[13] Chuck Marr, Brandon DeBot, and Chye-Ching Huang, “Eliminating Estate Tax on Inherited Wealth Would Increase Deficits and Inequality,” CBPP, updated April 13, 2015, https://www.cbpp.org/research/federal-tax/eliminating-estate-tax-on-inherited-wealth-would-increase-deficits-and.

[14] CBPP, “2017 Tax Law’s Child Credit: A Token or Less-Than-Full Increase for 26 Million Kids in Working Families,” August 27, 2018, https://www.cbpp.org/research/federal-tax/2017-tax-laws-child-credit-a-token-or-less-than-full-increase-for-26-million.

[15] Joel Friedman and Richard Kogan, “House GOP Budget Retains Tax Cuts for the Wealthy, Proposes Deep Program Cuts for Millions of Americans,” CBPP, June 28, 2018, https://www.cbpp.org/research/federal-budget/house-gop-budget-retains-tax-cuts-for-the-wealthy-proposes-deep-program-cuts.

[16] For an analysis of the distributional effect of the entire 2017 tax law once financing is taken into account, see William Gale et al., “Effects of the Tax Cuts and Jobs Act: A Preliminary Analysis,” Tax Policy Center, June 13, 2018, https://www.taxpolicycenter.org/publications/effects-tax-cuts-and-jobs-act-preliminary-analysis, p. 13.

[17] Joint Committee on Taxation, “Estimated Revenue Effects of H.R. 6760.”

[18] Jeffrey Rohaly et al., “Analysis of the Protecting Family and Small Business Tax Cuts Act of 2018,” Tax Policy Center, September 12, 2018, https://www.taxpolicycenter.org/sites/default/files/publication/155760/hr6760_wm_forpub_2.pdf.

[19] Congressional Budget Office, “The Budget and Economic Outlook: 2018 to 2028.”

[20] Paul N. Van de Water, “Federal Spending and Revenues Will Need to Grow in Coming Years, Not Shrink,” CBPP, September 6, 2017, https://www.cbpp.org/research/federal-budget/federal-spending-and-revenues-will-need-to-grow-in-coming-years-not-shrink.

[21] Howard Gleckman, “The Downmarketing of Tax Shelters,” TaxVox, January 18, 2018, https://www.taxpolicycenter.org/taxvox/downmarketing-tax-shelters.

[22] Matthew Smith et al., “Capitalists in the Twenty-First Century,” July 23, 2017, https://eml.berkeley.edu/~yagan/Capitalists.pdf.

[23] Wage and salary income previously faced a top marginal tax rate of 43.4 percent (39.6 percent in ordinary income tax + 3.8 percent in Medicare taxes), while pass-through profits faced a top tax rate of 39.6 percent, a differential of 3.8 percentage points. Under the 2017 tax law, wage and salary income faces a top marginal tax rate of 40.8 percent (37 percent in ordinary income tax + 3.8 percent in Medicare taxes), while pass-through profits eligible for the deduction face a top rate of just 29.6 percent (37 percent x 80 percent because of the 20 percent deduction). The differential between the top rates on wage and salary income and pass-through profits eligible for the deduction thus is now 11.2 percent (40.8 percent versus 29.6 percent).

More from the Authors

Areas of Expertise