BEYOND THE NUMBERS

House Republicans’ New Tax Plan Doubles Down on 2017 Tax Law’s Flaws

Update, July 25th: We've updated this post.

The House Republicans’ “Tax Reform 2.0” framework doubles down on the 2017 tax law’s fiscal irresponsibility, regressivity, and opportunities to game the tax code. Its centerpiece is a permanent extension of the 2017 tax law’s individual provisions, which are set to expire after 2025. That would add substantially to the nation’s long-term fiscal challenges, deliver far more to those with high incomes than to low- and middle-income filers, and make permanent some of the law's provisions that most encourage tax avoidance by wealthy filers.

The framework touts its new retirement- and education-related incentives but, in fact, many of them are also likely tilted to high-income filers and fail to transform a bill that prioritizes the those at the top of the income ladder over low- and moderate-income families.

Rather than build on the 2017 tax law, policymakers should fundamentally restructure it to fix its flaws. Instead, the new framework:

- Weakens revenues at a time when the nation needs to raise more. The 2017 tax law costs an estimated $1.9 trillion over ten years (2018 to 2027). Making the individual tax provisions permanent would exacerbate the tax law’s fiscal irresponsibility, costing another $250 billion in 2027 alone, the Congressional Budget Office estimates. This would increase the nation’s long-term deficits and debt, leaving it less prepared to address the retirement and health needs arising from the baby-boom generation’s retirement and other national needs. Meeting these fiscal and policy challenges will require more revenue, not less.

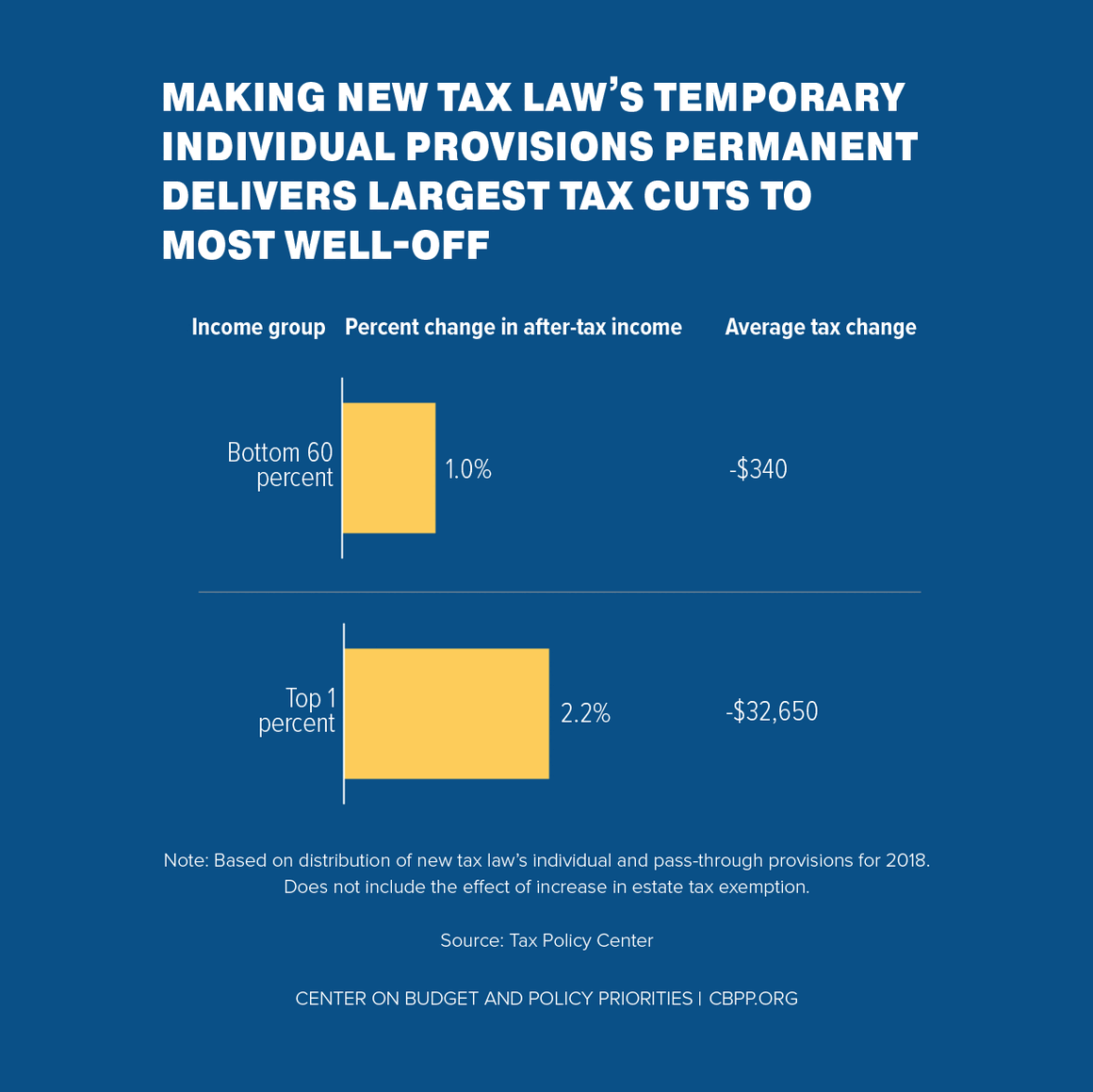

- Is tilted to the well-off. The 2017 tax law increases income inequality by delivering far larger tax cuts to those at the top than to the bottom or middle. The new framework repeats the same mistake since its most important provision — making the 2017 individual tax provisions permanent — would deliver far larger tax cuts to the top 1 percent than to the bottom 60 percent. (See figure.) For instance, the 2017 tax law’s individual tax provisions include a cut in the top tax rate, which only benefits high-income filers. (The framework is not specific about making all the individual provisions permanent — but it appears to envisage doing so as it cites Tax Foundation estimates that assume all the individual income tax provisions are made permanent.)

- Promotes and prolongs opportunities for tax gaming. The 2017 tax law encourages rampant tax gaming and avoidance and risks undermining the integrity of the tax code. It “has turned us into a nation of tax shelter hunters,” the Tax Policy Center’s Howard Gleckman observed. Among the most egregious of these opportunities is the deduction for “pass-through income,” which the framework would make permanent. Pass-through income is income that the owners of businesses such as partnerships, S corporations, and sole proprietorships report on their individual tax returns. Before the 2017 law, it was taxed at the same individual rate as the business owner’s other ordinary income, like wages and salaries. The new law makes it eligible for a 20 percent deduction, creating an incentive for high-income individuals to reclassify their salaries as pass-through income. Making this provision permanent would further encourage high-income taxpayers to use complex tax avoidance schemes to lower their taxes.

The framework proposes a new set of retirement- and education-related tax benefits, but such measures don’t transform the proposal’s primary focus on the wealthy. In fact, while the framework doesn’t provide details on many of these provisions, some of them are also likely tilted to the top. For example, it proposes “Universal Savings Accounts” (USAs), an idea promoted by Rep. Dave Brat and Sen. Jeff Flake. Notably, there are no income limits on the Brat/Flake USAs and their tax benefits would also be highly skewed: a married couple making less than $100,000 that faces a 0 percent long-term capital gains tax rate may receive no tax benefit from a USA, whereas a married couple making $1 million facing a 20 percent long-term capital gain rate would get a benefit of 20 cents on the dollar.

Rather than doubling down on the 2017 tax law’s flaws, policymakers should set a new course and deliver true tax reform — one that raises revenue to meet national needs, benefits low- and moderate-income working people far more, and improves economic efficiency by strengthening the integrity of the tax code.