BEYOND THE NUMBERS

Sixty-one years ago today, President Eisenhower signed a bill creating Social Security Disability Insurance (SSDI). Many Americans don’t know much about this vital program — even though, by working, they’re earning coverage that protects them against financial ruin if they become too sick or hurt to support themselves. We’ve updated our SSDI backgrounder and chart book to help you learn more.

How do I earn SSDI protection?

You earn SSDI protection in case of disability by contributing about 1 percent of your earnings — automatically deducted from your paycheck — toward the program. To meet SSDI’s earnings criteria, you must have a solid work history that includes recent work. More than 150 million workers have earned SSDI’s protection for themselves and their families. To qualify for benefits, you also need to meet SSDI’s strict medical criteria: beneficiaries must suffer from a severe physical or mental impairment and must be unable to perform substantial work.

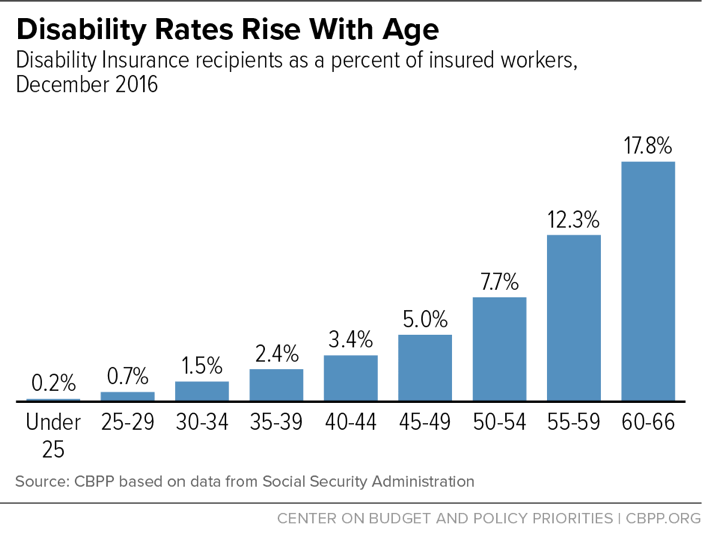

What are the chances that I’ll need SSDI benefits?

While people don’t like to think about becoming disabled and unable to support themselves, disability can happen to anyone — and becomes likelier as a person ages. (See graph.) A worker starting out faces about a 1 in 4 chance of becoming disabled before reaching retirement age.

Why are SSDI benefits important?

Becoming disabled can have serious financial consequences, causing medical and other expenses to rise and making work hard or impossible. Many people with disabilities struggle to afford basic needs — but SSDI helps. Benefits replace about half of a worker’s final earnings before becoming disabled and average less than $1,200 a month (or just under $14,000 a year). By helping people with disabilities afford housing, food, transportation, and other essentials, benefits protect against poverty, homelessness, and bankruptcy.

Will Social Security still be there for me if I become disabled?

Yes. The payroll taxes that workers contribute out of every paycheck fund most of SSDI’s costs. As long as Americans work, those revenues will continue to pay for benefits. In addition, SSDI has built up trust fund reserves, which Social Security’s trustees estimate will last until 2028. At that point, tax revenues will be large enough to pay for 93 percent of benefits even if policymakers don’t strengthen Social Security’s financing — though they always have in the past. Those who claim that Social Security won’t be around for today’s workers either misunderstand or misrepresent the facts.