Unfinished Business From the 2017 Tax Law

Testimony of Chye-Ching Huang, Director of Federal Fiscal Policy, Before the House Ways and Means Subcommittee on Select Revenue Measures

Chairman Thompson, Ranking Member Smith, and distinguished members of the Subcommittee, thank you for the opportunity to testify on temporary tax provisions and other aspects of the 2017 tax law that leave us facing uncertainty and unfinished business.

I will outline four sources of unfinished business stemming from the 2017 tax law:[1] 1) uncertainty surrounding the “extenders,” temporary federal tax breaks mainly for corporations that expired in 2017 or 2018; 2) costly individual provisions set to expire after 2025; 3) corporate provisions that create new sources of instability; and 4) the 2017 law’s failure to meet the nation’s challenges, meaning that the law requires fundamental restructuring to address those needs.

I then recommend a path towards better tax reform that prioritizes low- and moderate-income Americans, raises revenue, and closes loopholes. Meanwhile, any legislation addressing the 2017 tax law’s unfinished business should address its greatest shortcoming: that it largely left behind low- and moderate-income workers and their families while doing the most for the already well-off. For example, if Congress chooses to extend any of the expiring tax provisions known as “extenders,” lawmakers should not again leave behind low- and moderate-income workers and families, but should improve the Earned Income Tax Credit and/or Child Tax Credit, thereby taking a step towards fixing one of the 2017 law’s most glaring omissions.

Unfinished Business Stemming From the 2017 Tax Law’s Failures

The 2017 tax law left in its wake a series of policy failures that create uncertainty and instability, through missed opportunities, temporary tax policy, and choices to prioritize the well-off and profitable corporations over struggling workers and families. Four examples are:

1. Extenders

Twenty-nine federal tax breaks, mainly for corporations, expired at the end of 2017 or 2018. Most are known as “tax extenders” because policymakers have routinely extended them for a year or two at a time, at least in part because temporary extensions hide their significant long-term cost. In a December 2015 tax and budget deal, which many lawmakers said would put an end to extenders, lawmakers made a number of them permanent while giving others only temporary extensions. The 2017 tax law, in large part, was silent on these extenders.[2] Retroactively extending these remaining provisions through 2019 would cost some $18 billion over ten years.

Key lawmakers who negotiated the 2017 tax law said they valued certainty.[3] Yet the 2017 tax law did not make permanent various provisions that some of those same lawmakers now propose to extend, without paying for them. Keeping them off the tab in 2017 had the effect of hiding their cost, thus allowing for more new tax cuts in the 2017 tax law, but meant less eventual certainty. Enacting extenders retroactively for 2018 in particular would confer wasteful tax breaks for activity that has already occurred. The cost of any further extensions should be paid for.

2. Individual provisions set to expire after 2020

The 2017 tax law prioritized deep, permanent corporate rate cuts above other concerns, and so most of its individual tax provisions expire after 2025.[4] But far from correcting the 2017 tax law’s mistakes, extending the individual tax cuts, as some lawmakers favor, would compound the law’s flaws[5]:

- It would add to deficits. Making the individual provisions permanent would cost $245 billion more in 2027 alone.[6] That would further swell the cost of the 2017 tax law that already costs $1.9 trillion over ten years, leaving the nation less prepared to address the retirement and health needs arising from the retirement of the baby boomers, as well as other national needs.[7]

-

It would promote and prolong tax gaming. The 2017 law created a 20 percent deduction for certain pass-through income — income that the owners of businesses report on their individual tax returns, which previously was taxed at the same individual tax rates as business owners’ other ordinary income. Making the pass-through deduction permanent would be heavily tilted to the wealthy: more than two-thirds of the tax cut from it flows to the highest-income 1 percent, and it also makes it easier for wealthy people to game the tax system.[8]

The deduction creates so many opportunities for wealthy filers to reclassify their salaries as pass-through profits that NYU Law School Professor David Kamin has called it “one of the worst provisions that’s been added into the tax code in the last several decades.”[9] One financial advisor told his colleagues at a conference:[10]

This is, without a doubt, one of the biggest areas of planning that we can have under the new law. This is why, in large part, they should have just renamed the [2017 tax law] the tax professional, lawyer and financial advisor job security act of 2017.

The [pass-through] deduction leaves a gaping hole in the tax code, and the goal by the end of the presentation today is to make you guys the bus drivers, or the truck drivers, to drive right through that hole with your clients.

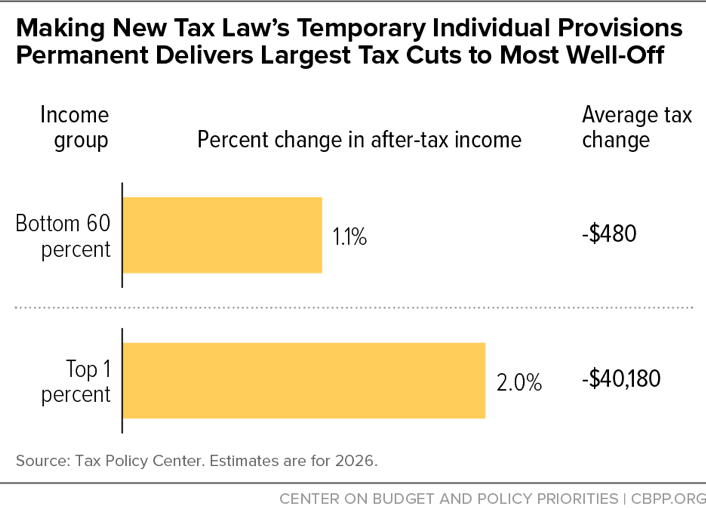

- It would most benefit those in the top 1 percent, again largely leaving workers and their families behind. Making the 2017 tax law’s individual tax provisions permanent would raise after-tax incomes by about twice as much (in percentage terms) for the top 1 percent of households as the bottom 60 percent, the Tax Policy Center estimates.[11] (See Figure 1.) That means a tax cut averaging more than $40,000 annually for those in the top 1 percent (whose after-tax incomes will already average more than $2 million).

The individual provisions of the 2017 tax law are so skewed to the top in part because it failed to use key tools such as the Child Tax Credit (CTC) and Earned Income Tax Credit (EITC), which lift the living standards of millions of working families. A growing body of evidence links income from these tax credits to better infant health, improved school performance, higher college enrollment, and projected increases in earnings in adulthood for children in families that receive them.[12] The 2017 tax law could have substantially helped low- and moderate-income households by boosting the EITC and CTC for them, but instead it:

-

Ignored and even eroded the Earned Income Tax Credit. The EITC lifts millions out of poverty and supplements the wages of a diverse group of workers who do needed jobs but receive relatively low pay, from truck drivers to cooks to home health aides.[13] It can be strengthened to do more for workers who have faced decades of wage stagnation.

In particular, the EITC should be strengthened for workers not raising children in the home (including non-custodial parents). They are the lone group of workers still taxed into or deeper into poverty by the federal tax code, in part because their EITC is much smaller than for workers with children.[14] But no boost in their EITC was even proposed for the 2017 tax law. The 2017 tax law thereby left these “childless workers” to continue to be taxed into or deeper into poverty — even while it lavished tax cuts on the heirs of the wealthiest estates in the country. For example, a single worker who made poverty-level wages in 2018 of roughly $13,000 paid about $1,100 in federal (employee share) payroll and income taxes and received an EITC of just $168, leaving her more than $900 below the poverty line. The law also missed a prime opportunity to boost the EITC for low-paid workers with children.

Indeed, to help pay for its permanent corporate tax cuts, the law erodes the value of the EITC for millions of working-class people. Since the law moves to the slower “chained” Consumer Price Index (CPI) to adjust tax brackets and certain tax provisions each year to account for inflation, the maximum EITC will rise more slowly over time. A married couple making $40,000 with two children will see their federal EITC shrink by $283 in 2027 (from $5,025 to $4,742) compared to prior law. A single worker earning $13,500 (below poverty-level pay) would see their already small EITC of $415 shrink by about $30 (from $415 to $384) by 2027, and their total tax liability would rise by the same amount; the federal tax code will tax them even deeper into poverty because of the 2017 tax law.

- Increased the maximum Child Tax Credit from $1,000 to $2,000 per child — but denied that full increase to 26 million children in low- and moderate-income working families.

- Some 11 million children in low-income working families will receive a token CTC increase of just $1 to $75. For example, a single mother with two children who works full time at the federal minimum wage and earns $14,500 a year gets just $75.

- Another 15 million children in low- and modest-income working families get a CTC increase of more than $75, but often far less, than the full $1,000-per-child increase. For example, a married couple with two children making $24,000 will get an $800 increase in their total CTC — well below the $2,000 maximum.

- The largest CTC increases go to high-income families. The credit now begins to phase out for married couples making $400,000 a year, compared to $110,000 under prior law. A married couple with two children making $400,000 are newly eligible for a full $2,000-per-child CTC, a $4,000 increase.

The law’s drafters chose this outcome: negotiators agreed last-minute to a deeper cut in the top individual tax rate, after President Trump was lobbied at a fundraiser by wealthy hedge fund managers.[15] But President Trump and other GOP lawmakers rejected calls from Senators Rubio and Lee to use the same funding source — a slight reduction in the law’s cut in the corporate tax rate — for a less inadequate CTC increase for children in low- and moderate-income working families.[16]

Such choices mean that making the individual provisions of the 2017 tax law permanent would double down on its deep flaws. Lawmakers should instead prioritize boosting critical tax credits for low- and moderate-income workers and families who were largely left out of 2017 tax law due to its focus on the well-off and profitable corporations.

3. Corporate provisions that create new sources of instability

The 2017 tax law prioritized permanent, deep corporate tax cuts. It cut the corporate rate from to 21 percent from 35 at a cost of more than $1.3 trillion over ten years. And it permanently set an even lower tax rate for U.S.-based multinationals’ foreign profits. The law fell far short of containing enough corporate provisions that “broaden the base” and raise revenues to cover the full cost of its corporate tax cuts in the long run. So, to pay for the remaining cost of its corporate provisions, the law made two other provisions that raise revenue permanently: an increase on taxes on individuals across the board with the chained CPI, and a provision that effectively cut resources for health care and coverage.[17] But even the law’s superficially permanent corporate provisions mask uncertainty:

-

Delayed revenue-raising provisions. The law contains a number of provisions that raise revenue from corporations but do not take full effect immediately. For example, the minimum tax on certain foreign profits (known as “GILTI”) is slated to rise from 10.5 percent to 13.125 percent after 2025, as is a new low tax rate intended for so-called intangible profits (known as “FDII”), from 13.125 percent to 16.406 percent. Another example is the amortization of research expenditures (deducting the cost of those expenses more slowly over five years rather than immediately), set to take effect in 2021. A “trigger” provision that was in early versions of the law sent a clear signal that many Republican lawmakers would prefer that those provisions never take effect. The trigger would have automatically prevented these and other revenue-raising provisions from taking full effect had revenues hit certain levels[18] — automatically giving still deeper tax cuts to corporations rather than doing more for low- and middle-income Americans.

The trigger was stripped from the bill because it did not meet the requirements of the “reconciliation” process that lawmakers used so that the bill could pass the Senate with a bare majority rather than the 60 votes that most legislation requires. But the delayed effective date of the corporate revenue-raising provisions remains, leaving time for lobbying to try to prevent them from taking effect.

- Legal uncertainty in the international provisions. The law moved the U.S. international tax system towards a “territorial” system, where most profits that a U.S. parent company earns from its foreign subsidiaries aren’t subject to U.S. tax under certain conditions. That risks a big, permanent incentive for U.S. multinationals to shift overseas not just profits on paper, but also actual investment, in ways that could hurt U.S. workers’ jobs and wages. The law has several poorly designed provisions to try to limit the damage this basic incentive could cause, but still leaves in place a large incentive to shift profits offshore. Further, one of those provisions, the Foreign Derived Intangible Income regime (FDII), likely violates World Trade Organization obligations, so experts believe it could “reignite a three-decades long trade controversy between the United States and the European Union,” and create “serious legal uncertainty.”[19]

4. The 2017 tax law failed to meet the nation’s challenges and will require fundamental restructuring to address national needs.

Perhaps the largest source of instability created by the 2017 tax law is its failure to meet the nation’s most pressing needs — necessitating fundamental restructuring. As I have detailed in testimony to the House Budget Committee, the law is fundamentally flawed in three ways:[20]

- It’s tilted to the top. In the face of stagnant working-class wages and growing inequality, the law delivers its largest tax cuts to the most well-off, while largely leaving behind low- and moderate-income Americans — and even hurting many.

- It shrinks revenues. The nation needs more revenue given the retirement and health needs arising from the baby-boom generation’s retirement as well as other national needs, but the law added $1.9 trillion to deficits. Federal revenues will total just 16.5 percent of GDP in 2019, the Congressional Budget Office projects, well below the 17.4 percent average over the last 40 years.

- It undermines the integrity of the tax code. True tax reform would close loopholes and make the tax code more efficient, but the law encourages rampant tax avoidance and gaming that will undermine the tax code’s integrity.

Only a basic restructuring of the 2017 tax law can fix these flaws because they stem from the law’s core provisions. For example, the corporate rate cut and the pass-through deduction contribute to all three major flaws. Tinkering cannot solve these problems. Lawmakers should not wait for the law’s major individual tax provisions to expire at the end of 2025 to undertake true tax reform.

Recommendations

I have two recommendations to offer for policymakers looking to move forward:

1. Fundamentally restructure the 2017 tax law and deliver true tax reform. True tax reform can prioritize people with low and moderate incomes, raise revenue to meet national needs, and strengthen the integrity of the tax code.

2. If lawmakers decide to take steps this year to address unfinished business left by the 2017 tax law, they should address the most pressing unfinished business: that the law left behind millions of hard-pressed workers and their families.

For example, if Congress decides to address some of the 2017 tax law’s uncertainty by moving an extenders package, it should not do so without also helping the most vulnerable workers and families that were left behind in 2017. Any extenders legislation should include improvements to the Earned Income Tax Credit and/or Child Tax Credit:

-

Low-wage workers without children in the home should be able to earn a meaningful EITC that protects them from being taxed into or deeper into poverty. The 2017 tax law left workers without children in the home as the lone group that the federal tax code taxes into poverty.

Many lawmakers, including Chairman Neal and other members of the Ways and Means Committee and Select Revenue Measures Subcommittee, have recognized that the pro-work benefits of a robust EITC should be extended to more workers without children in the home, and have advanced proposals to do so.[21]

-

The millions of children in working families largely left behind by the 2017 tax law’s CTC changes should receive a more adequate CTC.

As noted above, despite doubling the maximum CTC for high-income filers, the law left 11 million children in low-income working families with $75 or less, and another 15 million children in modest-income working families receiving less (and often far less) than the much-touted maximum increase of $1,000 per child. Ensuring a more adequate CTC for these families is high on the list of unfinished business from the 2017 tax law.

The final details of the 2017 law’s CTC provision were in flux until very late in the process. Senators Rubio and Lee proposed to do something more for the children largely left out, by: 1) ensuring that families could qualify for the CTC starting at the first dollar of their earnings; and 2) eliminating the 2017 tax law’s new, artificial and harmful cap on the amount of CTC that can be received as a refund. That would a be a move in the right direction, while still falling well short of making the CTC fully refundable.

Such modest changes would be a down payment toward more fundamental reform that truly prioritizes the workers and families in the way that lawmakers promised the 2017 law would do.[22]

End Notes

[1] The law’s official name is “Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018.” Its original title, the “Tax Cuts and Jobs Act,” was stricken from the bill.

[2] During the debate over the 2017 law, several of its supporters effectively tried to argue that the true cost of the bill, then estimated at $1.5 trillion, should be reduced by the cost of extenders it did not made permanent. That is even though some of those extenders are now being reconsidered, and even while the law created new expiring provisions. For more on how extenders were considered during the debate on the 2017 tax law, see Seth Hanlon, “Written Statement Before the House Ways and Means Subcommittee on Tax Policy, Hearing on Post Tax Reform Evaluation of Recently Expired Tax Provisions,” March 14, 2018, https://docs.house.gov/meetings/WM/WM05/20180314/106946/HHRG-115-WM05-Wstate-HanlonS-20180314.pdf; Hanlon, “The Senate Tax Bill Is Even More Costly Under Current Policy Assumptions,” Center for American Progress, December 13, 2017, https://www.americanprogress.org/issues/economy/news/2017/12/13/444103/senate-tax-bill-even-costly-current-policy-assumptions/; and Chye-Ching Huang and Brandon DeBot, “‘Current Policy’ Baseline Would Hide $439 Billion in Tax Cuts Worth at Least $40,000 a Year for the Top 0.1 Percent,” CBPP, August 16, 2017, https://www.cbpp.org/research/federal-tax/current-policy-baseline-would-hide-439-billion-in-tax-cuts-worth-at-least-40000.

[3] Sally Persons, “Kevin Brady: House plans to make tax cuts permanent,” Washington Times, July 12, 2017, https://www.washingtontimes.com/news/2017/jul/12/kevin-brady-house-plans-to-make-tax-cuts-permanent/.

[4] Chuck Marr, “Republicans Chose Corporate Shareholders Over Working Families,” CBPP, December 19, 2017, https://www.cbpp.org/blog/republicans-chose-corporate-shareholders-over-working-families.

[5] Burgess Everett and Rachel Bade, “Tax cuts, Round 2: GOP looks to punish Democrats in 2018,” Politico, March 27, 2018, https://www.politico.com/story/2018/03/27/tax-cuts-gop-2018-midterms-482158.

[6] Chye-Ching Huang, “Permanent Extension Would Double Down on 2017 Tax Law’s Fundamental Flaws,” CBPP, May 2, 2018, https://www.cbpp.org/blog/permanent-extension-would-double-down-on-2017-tax-laws-fundamental-flaws.

[7] The Joint Committee on Taxation estimated in December 2017 that the 2017 tax law would cost $1.5 trillion between 2018 and 2027, but an April 2018 Congressional Budget Office (CBO) analysis raised the cost to $1.9 trillion. CBO, “The Budget and Economic Outlook: 2018-2028,” April 2018, https://www.cbo.gov/system/files/115th-congress-2017-2018/reports/53651-outlook.pdf.

[8] Chuck Marr and Brendan Duke, “New House Republican Tax Proposal Fails Fiscal Responsibility Test, While Favoring the Wealthiest,” CBPP, updated September 13, 2018, https://www.cbpp.org/research/federal-tax/new-house-republican-tax-proposal-fails-fiscal-responsibility-test-while.

[9] Chye-Ching Huang, “Senate’s Hearing Testimony Highlights 2017 Tax Law’s Fundamental Flaws,” CBPP, April 25, 2018, https://www.cbpp.org/blog/senate-hearing-testimony-highlights-2017-tax-laws-fundamental-flaws.

[10] Emily Horton, “Tax Planner: Drive Wealthy Clients Through ‘Gaping Hole’ in Tax Code,” CBPP, May 31, 2018, https://www.cbpp.org/blog/tax-planner-drive-wealthy-clients-through-gaping-hole-in-tax-code.

[11] TPC Table T18-0133. See: Marr and Duke, 2018.

[12] Chuck Marr et al., “EITC and Child Tax Credit Promote Work, Reduce Poverty, and Support Children’s Development, Research Finds,” CBPP, updated October 1, 2015, https://www.cbpp.org/research/federal-tax/eitc-and-child-tax-credit-promote-work-reduce-poverty-and-support-childrens.

[13] Jennifer Beltrán, “Working-Family Tax Credits Lifted 8.9 Million People Out of Poverty in 2017,” CBPP, January 15, 2019, https://www.cbpp.org/blog/working-family-tax-credits-lifted-89-million-people-out-of-poverty-in-2017.

[14] Chuck Marr et al., “Strengthening the EITC for Childless Workers Would Promote Work and Reduce Poverty,” CBPP, April 11, 2016, https://www.cbpp.org/research/federal-tax/strengthening-the-eitc-for-childless-workers-would-promote-work-and-reduce.

[15] The Hill Staff, “How the Trump tax law passed: The final stretch,” The Hill, September 30, 2018, https://thehill.com/policy/finance/409042-how-the-trump-tax-law-passed-the-final-stretch.

[16] Chye-Ching Huang, “Trump Favors Larger Corporate Tax Cuts Over More Help for Children in Low-Income Working Families,” CBPP, November 30, 2017, https://www.cbpp.org/blog/trump-favors-larger-corporate-tax-cuts-over-more-help-for-children-in-low-income-working.

[17] Marr, “Republicans Chose Corporate Shareholders Over Working Families.”

[18] Chye-Ching Huang, “Obscure Provision Tilts Senate Tax Bill Even More to Corporations,” CBPP, November 22, 2017, https://www.cbpp.org/blog/obscure-provision-tilts-senate-tax-bill-even-more-to-corporations.

[19] Rebecca M. Kysar, “Critiquing (and Repairing) the New International Tax Regime,” Yale Law Journal, October 25, 2018, https://www.yalelawjournal.org/forum/critiquing-and-repairing-the-new-international-tax-regime.

[20] Chye-Ching Huang, “Fundamentally Flawed 2017 Tax Law Largely Leaves Low- and Moderate-Income Americans Behind,” CBPP, February 27, 2019, https://www.cbpp.org/federal-tax/fundamentally-flawed-2017-tax-law-largely-leaves-low-and-moderate-income-americans.

[21] Committee on Ways and Means, “House Democrats Introduce Tax Package to Support Middle-Class Americans & Working Families,” press release, February 2, 2017, https://waysandmeans.house.gov/media-center/press-releases/house-democrats-introduce-tax-package-support-middle-class-americans.

[22] Similarly, any “technical corrections” to fix mistakes in the 2017 tax law should not move unless the package address the law’s much bigger mistake of leaving low-income workers and families largely behind. For example, former Ways and Means Chairman Brady proposed last year a technical corrections package that would have helped restaurant and retail owners but do nothing directly for their workers. No technical corrections package that delivers a valuable fix to business owners or other high-income filers should be passed unless it also makes progress for workers and children. Chuck Marr, “House GOP Tax Fix for Restaurant, Retail Owners Leaves Out Millions of Their Workers,” CBPP, December 6, 2018, https://www.cbpp.org/blog/house-gop-tax-fix-for-restaurant-retail-owners-leaves-out-millions-of-their-workers.

More from the Authors