BEYOND THE NUMBERS

Update, June 5: We’ve corrected a number in this post.

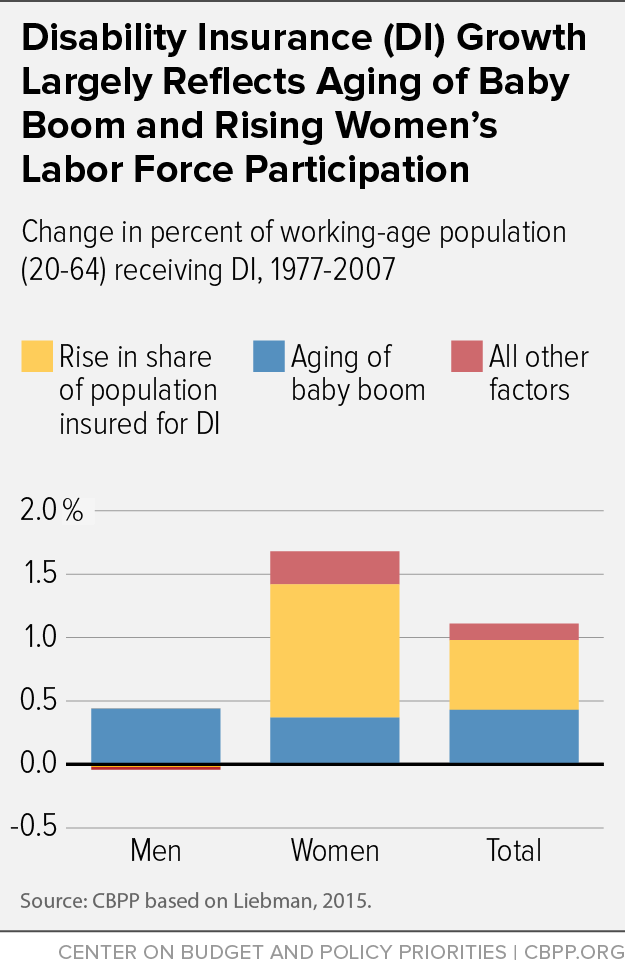

In a new analysis, Harvard economist Jeffrey Liebman finds the aging of the population and the rise in women’s labor force participation explain most of the recent growth in the Social Security Disability Insurance (DI) rolls. It reinforces three major points in our 2014 paper: the share of DI growth attributed to demographic factors depends on the measure of growth used; it depends on the period examined; but over any reasonable span, most of the cause is demographic. Liebman’s analysis thus confirms that DI is not in crisis.

Liebman examined how the share of the working-age population receiving DI benefits has been affected by the aging of the baby boomers; the growth in labor force participation (especially among women); and changes in the rates at which people are newly awarded benefits and leave the rolls due to death or other reasons (typically, improved health). That exhaustive modeling surpasses what other experts — including CBPP as well as oft-quoted researchers David Autor and Mark Duggan and staff at the Federal Reserve Bank of San Francisco — have achieved.

Since Liebman focused on changes in DI’s receipt rate, not the number of DI recipients, population growth didn’t affect his calculations. Nor did the rise in Social Security’s retirement age, since he concentrated on people aged 20-64. We’ve explained how those factors have boosted the number of DI beneficiaries.

Liebman found:

- About 90 percent of DI’s growth between 1977 and 2007 stemmed from the aging of the baby boomers and the rise in women’s labor-force participation, which enabled a greater share of women to qualify for DI if they became disabled (see graph).

- Over the shorter 1993-2007 period, over 70 percent of DI’s growth reflected those two factors.

- In contrast, using 1985 as the base year produces a smaller “demographic” contribution — about 45 percent — because the DI receipt rate was unusually low that year. That was due largely to the lingering effects of the Reagan Administration's aggressive implementation of new powers enacted in the 1980 Social Security Amendments, which unjustly ended or denied benefits to hundreds of thousands of people. Reforms in response to the crackdown gradually pushed rates of receipt back to more typical levels.

While Liebman’s analysis is sound, one point deserves clarification. Liebman ascribed part of the “bounceback” in DI receipt rates in the mid-1980s to the 1984 Disability Benefits Reform Act (DBRA) but, in reality, that law essentially ratified reforms already underway. DBRA directed the Social Security Administration to weigh the combined impacts of multiple impairments, publish new standards for evaluating mental disorders, and document medical improvement before terminating benefits. It didn’t expand the definition of disability or relax the requirement that applicants provide substantial medical evidence from qualified sources; and soon after Congress passed it unanimously, Social Security’s actuaries judged that it would worsen DI’s financial outlook by a negligible 0.01 percent of taxable payroll — which certainly does not reflect a lax or liberalized program.

In short, the main causes of DI’s growth are well understood and don’t depict a program that’s “out of control.” Lawmakers should redirect a modest portion of Social Security payroll taxes toward this essential protection and strengthen the overall solvency of Social Security, a vital and popular program.

{kind=link}