Testimony by Jared Bernstein, Center on Budget and Policy Priorities

Chairman Brady, ranking member Levin, I thank you for holding this important hearing on economic growth and opportunity.

While the range of issues I cover, including taxes, health care, trade policy, poverty, preparing for the next recession, and more, may seem disparate, there is, in fact, a strong unifying theme that links them. In every area, these are policies under this committee’s purview that can help or hurt working families. My testimony will highlight a positive policy agenda by which Congress can support growth and help families facing challenges in today’s economy.

Before I get to the specific policy areas, however, I begin with a brief overview of the current economic context within which these policy challenges are taking place.

Current conditions

The current US economy is characterized by very solid labor market trends, low unemployment, steady (if plodding) GDP growth, and unusually cheap energy.

Energy: Oil that sold for about $100/barrel two years ago is now selling for around $30. This sharp drop in energy prices has both reduced consumer prices and roiled global markets. From a macro-perspective, this price decline—a function of both increased supply of various energy sources and weakening global demand, particularly from China—is a significant problem for countries that are net exporters of this commodity and a potential advantage for net importers.

Though the US is still a net importer, President Obama meant it when he endorsed an “all of the above” approach to energy. The US has doubled its domestic oil production since 2008, as the shale boom has added 3 million barrels per day to the global energy market, while the administration continues to work to develop renewables. So, while we’re still a net importer, more jobs, families and towns are now engaged in both the extraction of fossil fuels and the development of renewable energy. Thus, while price declines help American consumers broadly, and, by holding down inflation, boost real wage growth, some communities that have invested in energy extraction in recent years are hurt by oil’s very low price.

Jobs and Wages: Job growth has been particularly strong. Net payroll gains in 2015 amounted to 2.7 million, slightly below the 2014 addition of 3.1 million jobs. That cumulative addition of 5.8 million jobs over the past two years marks the strongest two years of payroll gains since the late 1990s. Private businesses have now added 14.1 million jobs over 70 straight months, a record consecutive streak.

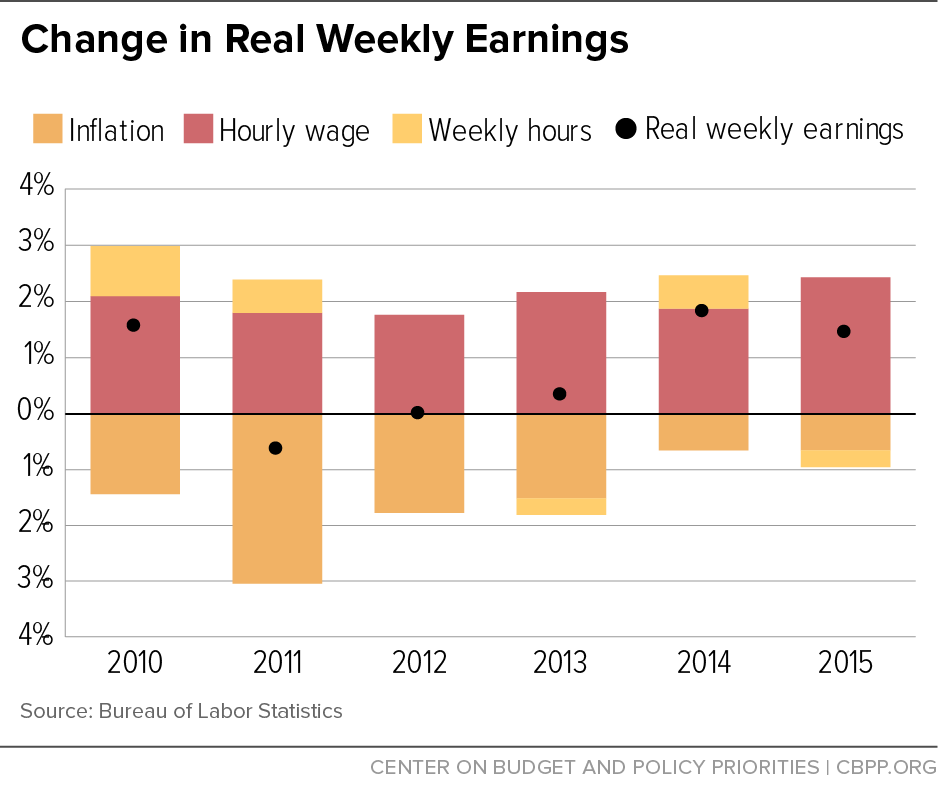

Figure 1 shows the components of real weekly earnings for middle-wage workers over the past few years: hourly wages, weekly hours, and inflation.[1] After falling for three years, real weekly earnings rose in both 2014 and 2015, by 1.8 percent and 1.4 percent, respectively, for these middle-wage earners. The figure also shows that while nominal wage growth has slightly accelerated, the largest factor driving real earnings gains is lower inflation. While hourly wage growth picked up a bit last year, growing 2.4 percent in 2015 as opposed to the about 2 percent of the prior two years, the big difference was the sharp energy-induced decline in the price index.

Though the actions of the Federal Reserve are beyond the purview of this committee, I note that even with their recent acceleration, recent wage gains are far from inflationary, a point underscored by recent inflation readings. Thus, from a monetary policy perspective, it is important that the Fed is cautious in its rate-raising campaign. The job market is clearly improving, and doing so at a faster clip than in recent years. But we are not yet at full employment, and I see no sign of a nascent inflationary threat. To the contrary, recent developments in the global economy may pose more of deflationary risk.

Slow productivity growth: There are two longer-term macroeconomic problems that I would bring to the committee’s attention: slow productivity growth and our lack of preparedness for the next recession. I return to the second of these at the end of my testimony.

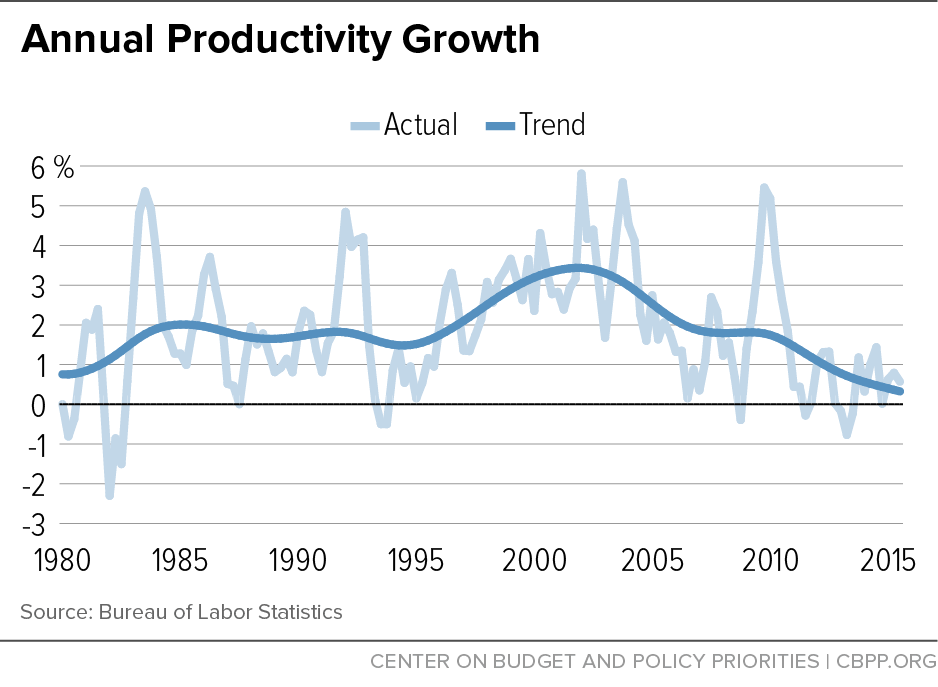

A key concern of today’s hearing is the pace of real growth in the US economy, which has averaged about 2 percent since year-over-year real GDP growth turned positive in 2010. While that’s about twice the growth rate of the Eurozone, it is moderate growth, held down by sluggish growth in productivity and a slower growing labor force. While part of the slower labor force growth—maybe one-half to two-thirds—is an expected function of our aging workforce, the extent to which the growth of output per hour (productivity) has slowed deserves greater attention from policy makers.

Figure 2 shows yearly productivity growth along with a trend line that picks up the underlying movements of the series. Since 2010, trend productivity growth has been running at an annual rate of around 1 percent, well below its growth in the 1990s, when the trend accelerated from about 1.5 percent in 1995 to over 3 percent in 2000. Slower productivity growth is a bit like the weather: everyone complains about it but no one knows what to do about it. That said, in a recent analysis of the problem, I identified and reviewed three explanations: mismeasurement, capital misallocation, and persistently weak demand.[2]

While there’s some evidence that increased measurement error is biasing productivity’s growth rate down, measurement error is not a large factor, a point echoed in a recent analysis by Federal Reserve economists. Instead, there appears to be a significant role for capital misallocation. The opportunity cost of devoting an increasingly significant share of GDP to those parts of the finance sector that helped to inflate the housing bubble of the 2000s may be lower economy-wide productivity growth. That doesn’t mean the level of investment is too low, though business investment as a share of GDP is not quite yet back to pre-recession levels. It means too much of our investment is non-productive.

Another source of slow productivity growth may well be the absence of full employment. Very tight labor markets lead firms facing higher labor costs to find efficiencies they otherwise didn’t need to maintain profits. As economist Larry Summers recently noted: “In a period of zero interest rates [corresponding to periods of weak demand] … it is very easy to roll over loans. And therefore there is very little pressure to restructure inefficient or even zombie enterprises.” In this sense, it is likely not a coincidence that the last period of strong productivity growth roughly corresponded with the full employment period of the late 1990s.

You will surely hear analysis that ties the productivity slowdown to the desired policy outcome of one advocate or another. It will be blamed on corporate taxes, “Obamacare,” regulations, and whatever other boogiemen partisans choose to invoke. I urge members to be skeptical of such facile causes. Taxation, health care reform, or regulation are particularly implausible targets, as they would presumably raise the cost of capital and slow productivity through a channel of diminished investment. But capital is extremely cheap and has been for some time, and firms are sitting on historically high levels of cash reserves.

Achieving full employment and more productive capital allocation are not quick fixes (though greater investment in public infrastructure is an example of smart, productivity-enhancing capital allocation, one I urge the committee to consider). While faster productivity growth is an essential goal of policy makers, beware of advocates trying to sell tax cuts and deregulation as the way to get there; their misguided thinking can be summed up by the old adage: “if your only tool is a hammer, everything looks like nail.”

I now turn to the specific policy areas under the purview of this committee, with an emphasis on how public policy is supporting, or failing to support, growth and the well-being of American families.

Health care

The Affordable Care Act has been remarkably successful: it has reduced the number of Americans without health coverage and contributed to the slower growth of health care costs. The former is a major advance in terms of reducing economic insecurity. Given the predominant role of health care spending in terms of our present and future fiscal outlook, the latter—slower-growing health care costs—is essential in the pursuit of sustainable fiscal policy.

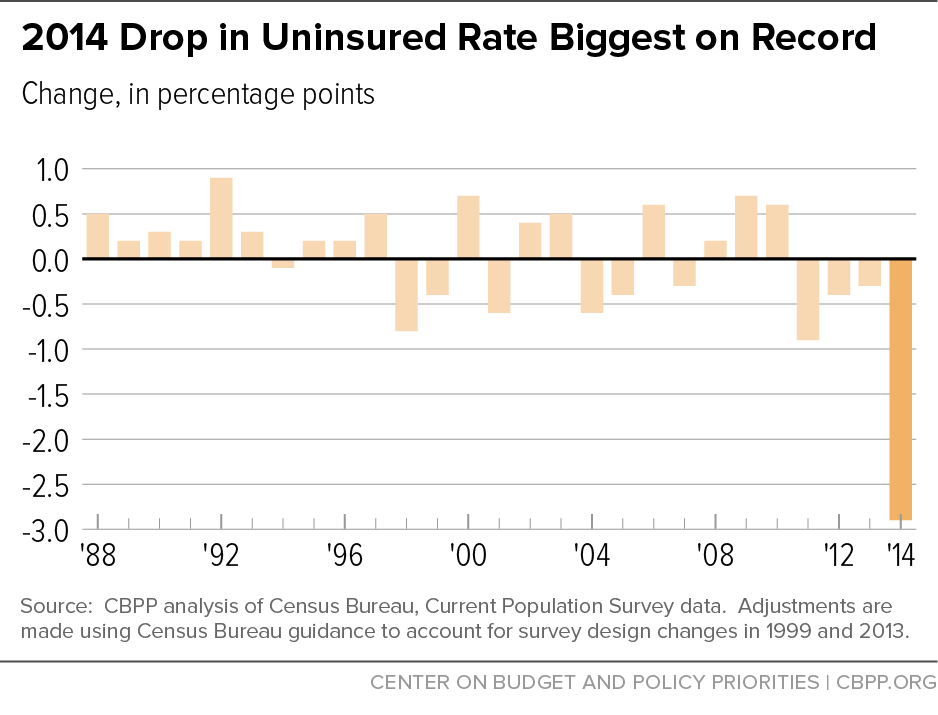

Coverage: The number of uninsured people fell by 8.8 million and the uninsured rate declined by 2.9 percentage points in 2014, the year the Medicaid expansion and exchanges kicked in; as figure 3 shows for the uninsured rate, these changes were by far the biggest single-year improvements on record. While coverage gains occurred in every state, the gains were greater in the 25 states (including DC) that adopted the Medicaid expansion by January 2014. The uninsured rate in expansion states is now 9.8 percent, while the uninsured rate in other states is 13.5 percent.

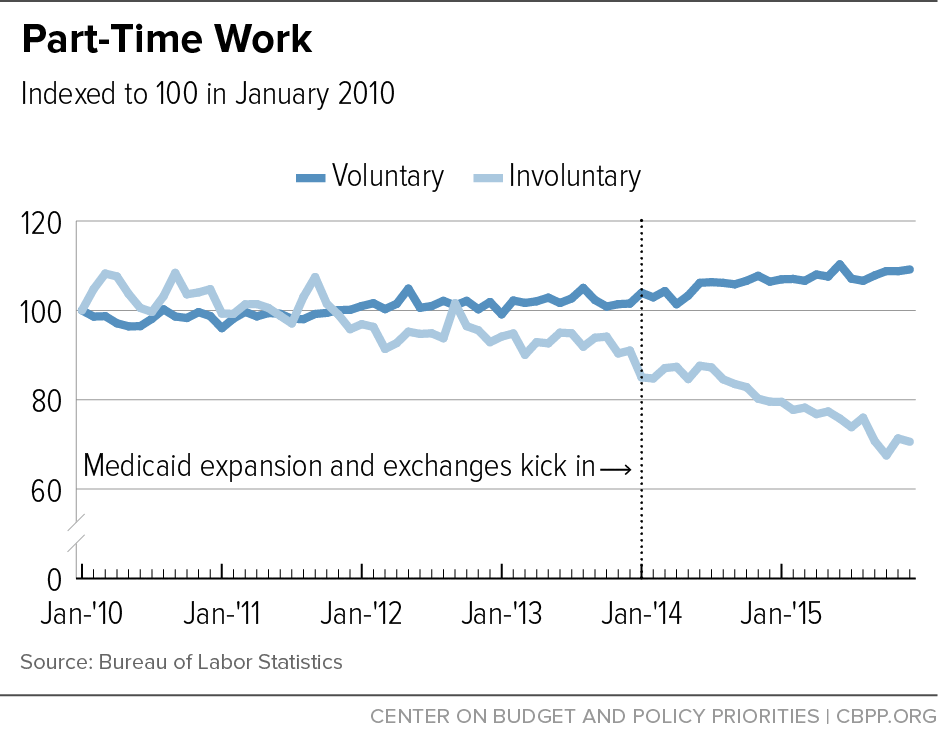

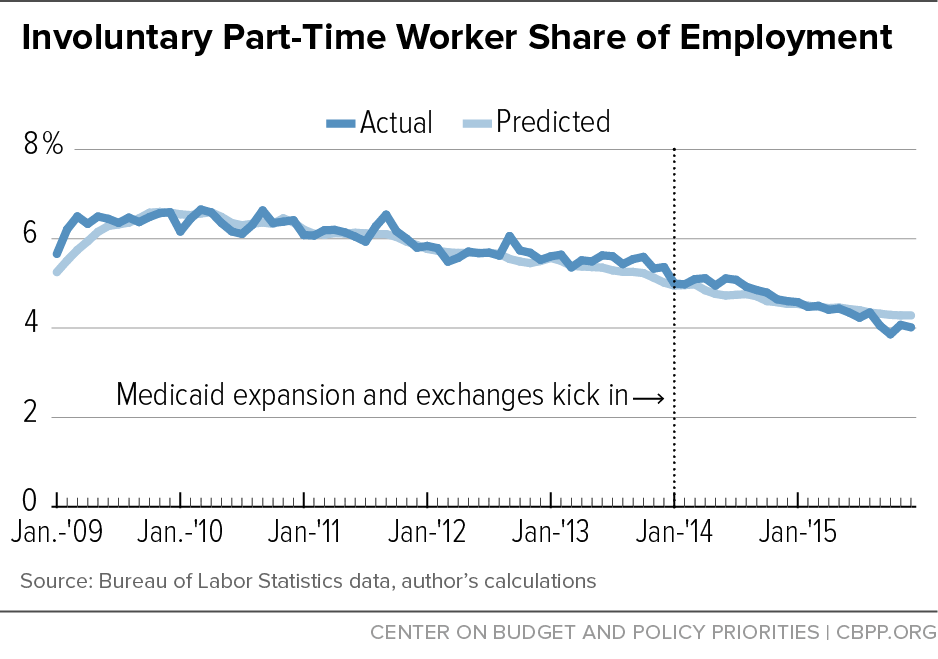

Some ACA critics maintain that these gains have come at the expense of job growth. This critique is hard to reconcile with the overall jobs numbers cited above, but what about more nuanced attacks? For example, because employer mandates, phased in over 2015-16, apply to firms with over 50 full-time workers, it is argued that the ACA is forcing people into part-time work. If so, we would expect to see an increase, relative to trend, of involuntary part-time work.

The next two figures show that’s not happening. The figure 4 illustrates that involuntary part-time work has fallen; the decline appears to have accelerated since the ACA’s exchanges and Medicaid expansion went into effect in 2014. Meanwhile, voluntary part-time work is up, perhaps, as economist Dean Baker has suggested, due to the ACA-induced release of “job-lock,” where workers who would rather work part-time previously worked full-time in order to get employer-provided health benefits.

Of course, since we expect involuntary part-time (IPT) work to decline in a recovery, particularly one with solid job gains, a better assessment of the question of whether the ACA is leading to more IPT work requires a “counterfactual,” i.e., what trend we would expect had the ACA not been implemented. The figure 5 shows a predicted trend in IPT work (as a share of total employment) based on a simple model using the unemployment rate as a predictor. I ran the model using data through 2009 (pre-ACA passage) and predicted the trend in IPT work thereafter using actual values of the unemployment rate. The fact that the predicted trend hugs the actual trend suggests that IPT work is falling as it usually does in a recovery.

In other words, there is little, if any, evidence to support the claim that the ACA is a “job-killer.”

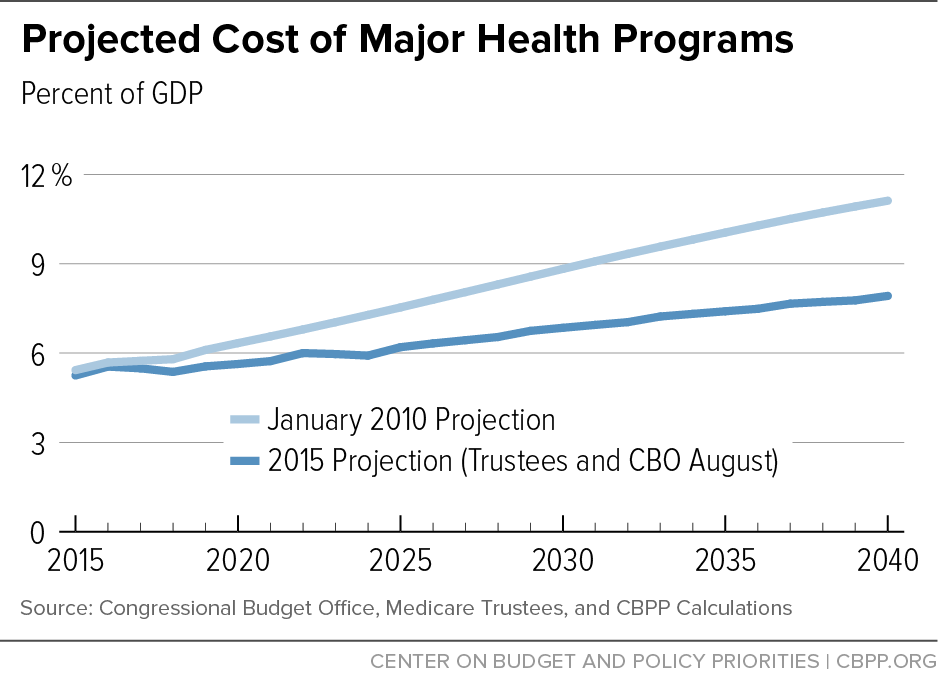

Health care costs: It is widely documented that health care costs have been growing more slowly in recent years. This trend is critically important, as cost pressures from the health sector—driven by both the aging of the population and the “excess cost burden”[3]—are a major contributor to our fiscal challenges. Projections of federal health spending are now substantially lower than they were in 2010, before the ACA was enacted.

Figure 6 provides more detail of these different projections. Each line represents CBO’s projected spending on major government health care programs as a share of GDP. The top line shows the 2010 projection of Medicare, Medicaid, and CHIP costs. The lower line, from CBO’s 2015 forecast,[4] includes the same programs as the earlier projection and also includes the ACA. Remarkably, total projected federal health care costs have shrunk substantially even though health care coverage has grown substantially. By 2023, the costs of these major health programs are down by 1 percent of GDP relative to the 2010 projection; by 2030 they are down 2 percent of GDP; and by 2038, by 3percent of GDP.

Health reform has reduced spending directly by scaling back excessive payments to Medicare providers. It has also accelerated the shift to new Medicare payment models that seek to reward quality of care rather than the volume of services. In addition, many analysts believe that health reform has indirectly encouraged structural changes in the health care payment and delivery system that will generate further savings. For example, interventions like “bundled payments” (an overall fee covering all the care related to a procedure), “accountable care” models (providers have monetary incentives to reduce spending below a set level while maintaining quality), and bonuses for reducing re-hospitalizations may be helping to slow cost growth. Other factors are surely behind these cost savings as well, as costs began to slow even before the new law was in place, but the ACA is having an undeniable impact.

Trade[5]

Given this committee’s role in international trade and trade agreements, I wanted to note a few points and concerns regarding the Trans-Pacific Partnership, or TPP, from the perspective of economic growth and opportunity.

Contrary to simple textbook trade theory, the increase in international trade has not been an unequivocal good for all working families. In fact, more realistic theories of trade are quite clear on the point that trade creates winners and losers, with the latter typically including those thrown into competition with cheaper workers abroad. Still, our highly productive workforce can compete globally, as long as the playing field is not tilted against them.

If the benefits of trade are to be more broadly shared, two things have to happen. First, our trade agreements must be more than handshakes between investors. They must provide workers from all signatory countries with the rights and protections they need to capture some of the benefits of trade. Second, we in the US must be able to lower our large and persistent trade deficits through enforceable rules against currency interventions that give our trading partners an unfair price advantage.

The TPP goes further than past agreements in various ways that could protect workers both here and in other signatory countries from unfair labor and wage practices. For example, the USTR worked out bilateral “consistency plans” with Vietnam, Malaysia, and Brunei that specify ways these countries must change their laws and practices to meet the general obligations in the TPP’s labor chapter. Of course, such provisions underscore the need for stepped up enforcement, an area where the US record has not been strong enough. A nonpartisan Government Accountability Office survey of this issue concluded that “monitoring and enforcement [of labor provisions in prior trade agreements] remain limited.”

An even greater concern is the absence of a consistency plan for Mexico, particularly because US auto production has been sharply increasing there. Mexican workers are typically unable to unionize or collectively bargain, and they make less than a fifth of what US autoworkers are paid. This combination of accelerated outsourcing of auto production to Mexico and suppression of workers’ rights there reduces living standards and increases inequality on both sides of the border.

Thus, in the spirit of trade that is both pro-growth and pro-worker, I urge this committee to carefully consider both enforcement and oversight provisions in the TPP, and the need for a plan to improve labor rights in Mexico.

On currency, the existing side agreement to the TPP has some positive features but no enforcement mechanism. As economist Joe Gagnon points out, the “TPP partners merely reiterate the obligation they already have as members of the International Monetary Fund (IMF) to ‘avoid manipulating exchange rates … to prevent effective balance of payments adjustment or to gain an unfair competitive advantage.’” The side agreement may well provide the information needed to quickly identify currency manipulators, but voluntary agreements only work if key actors, such as those at the US Treasury, take corrective action in the face of evidence. Unfortunately, our history here is lots of evidence and virtually no action. In the face of obvious currency management by China, for example, the US Treasury has been extremely hesitant to label them a currency manipulator.

The absence of a currency chapter in the TPP suggests the need for Congress to legislate enforceable currency rules outside of the trade agreement. For example, back in 2010, this chamber, while no less divided than it is today, overwhelmingly passed legislation that, if it had been enacted, would have allowed the Commerce Department to treat currency management as an unfair subsidy, calling for countervailing duties. Given the long history of voluntary measures being inadequate to the task of pushing back on currency manipulation, such enforceable rules would be preferable to the voluntary approach.

Other aspects of the TPP also warrant close scrutiny. The fact that investors are using the investment dispute settlement procedure under NAFTA to challenge the administration’s decision on the Keystone pipeline underscores the importance of making sure our sovereign rights are adequately protected. The agreement also has weaker rules of origin for automotive products than past trade agreements (e.g., NAFTA), which could hurt employment opportunities along our supply chains for cars and car parts.

Tax Reform

Both Congress and the administration have argued for broad reforms in the tax code. From the perspective of economic growth and broadly shared opportunity, I would urge the committee to consider two important criteria when it comes to tax policy: making the tax code more effective at reducing, rather than exacerbating, pretax income and wealth inequality, and ensuring ample revenues with respect to fiscal obligations (based on demographic pressures alone, we will need more, not less, revenues moving forward). One way to achieve these goals simultaneously, often with the added bonus of improving the economic efficiency of the tax code, is to eliminate or reduce tax subsidies and loopholes that contribute to wealth inequality, reduce investment, and incentivize the overseas outsourcing of American jobs. I specify numerous examples below.

In the spirit of these two criteria, I would also urge the committee to be extremely wary of what are essentially “trickle-down” tax cut arguments. Yes, our corporate tax code – with its internationally high statutory rate, much lower effective rate, and shrinking base – needs serious attention. But there is no basis for arguments that sharply reducing business or individual tax rates or not taxing foreign earnings will return large growth, job, and wage effects that will, in turn, lift the living standards of middle- and low-income families.

As tax expert Bill Gale (and colleagues), recently wrote, “At the federal level, there is virtually no evidence that broad-based [corporate] tax cuts have had a positive effect on growth…That has been amply demonstrated at the national level, where tax cuts have eroded revenue without discernable effect on economic activity.”[6]

While claims of tax cuts leading to large positive shifts in investment, productivity, and incomes are often heard in these hallways, in the real world, Gale’s observations have been proved time and again. National expert Joel Slemrod has found that “there is no evidence that links aggregate economic performance to capital gains tax rates.” The non-partisan Tax Policy Center finds “no statistically significant correlation between capital gains rates and real growth in gross domestic product (GDP) during the last 50 years.[7] Jane Gravelle, a tax analyst at the Congressional Research Service who has examined research purporting to show large gains from corporate tax cuts, points out that claims that “behavioral responses could cause revenues to rise if rates were cut do not hold up on either a theoretical basis or an empirical basis…Cross-country studies to provide direct evidence showing that the burden of the corporate tax actually falls on labor [such that tax cuts will help workers] yield unreasonable results and prove to suffer from econometric flaws that also lead to a disappearance of the results when corrected…[C]laims that high U.S. tax rates will create problems for the United States in a global economy suffer from a misrepresentation of the U.S. tax rate compared to other countries…”

To be very clear, there is room for significant improvements in our tax code. Especially the business side of the code, as noted, is riddled with subsidies and loopholes that generate lots of work for tax lawyers and lobbyists figuring out new schemes for tax avoidance. In fact, the most recent CBO budget outlook predicts that “increasing erosion of the corporate tax base” due to “transfer pricing,” tax inversions, and other avoidance techniques will lower corporate income tax receipts by about five percent over the next decade.[8]

It is in attacking this sort of problem, as opposed to the pursuit of supply-side tax cuts, where I believe this committee could be most effective: cutting back or closing wasteful, costly subsidies and loopholes that exacerbate inequality, generate inefficiencies, and increase budget deficits.

-

In a town where every tax break has someone to defend it, the carried interest loophole stands out as an exception: it is widely recognized by partisans on both sides of the aisle as providing an unfair tax break to a group that doesn’t need it. Investment fund managers get to pay the lower capital gains rate—about 24 percent as opposed to about the 40 percent they should pay—on a large part of their earnings generated by returns from the funds they manage. Note that these managers are not investing their own capital; the fund returns they get are thus a form of compensation. As such, they should be taxed like regular earnings. Ten year savings: $15.6 billion over 10 years.

-

In the spirit of economic growth, efficiency, and tax fairness, it would be extremely useful for Congress to “increase the bar” against corporate tax inversions. Though the US Treasury has attempted to reduce the incentives to invert through rule changes, the most recent example—the Johnson Controls/Tyco inversion—shows that more is needed.

It is well documented that these restructurings are not in the interest of uncovering economic efficiencies, but in the interest of tax avoidance. According to news accounts, Johnson was already paying a relatively low effective tax rate of 19 percent, yet by merging with Tyco, headquartered in Ireland, it can lower its rate to 14 percent, a rate far below those seen in any plausible corporate tax reform plan floated in recent years. Instead of our companies figuring out ways to book more of their earnings in tax havens, we need them to focus on production, innovation, and job creation here in the US. Congress should thus make the inversion bar higher by requiring that historic shareholders of the US entity hold no more than 50 percent of the value of the newly formed company (as opposed to the 20 percent they must hold under current rules). If a merged company is managed, controlled, and has significant business activities in the US, it should be considered a US corporation for tax purposes. Finally, an “exit tax” could be another useful “speedbump” to discourage inversions.

-

Another loophole that partisans might be able to agree to close is the “step-up basis” provision by which the wealthy can pass capital gains on to their heirs tax free. When the unrealized gains of someone who dies are passed on to an heir, the appreciation is untaxed. President Obama has proposed to close this loophole, subject, as explained by tax experts Marr and Huang, “…to large exemptions to ensure that middle-income and even most upper-income people aren’t affected.” There is no good economic rationale for this loophole. To the contrary, it creates a tax incentive—a “lock-in” effect—to hold assets until death, even in cases in which realizing their appreciated value and investing those resources elsewhere might be more productive from an economic standpoint. The only score we have for the 10-year savings generated by closing this loophole includes the President’s proposal to raise the capital gains rate to 28 percent: $233 billion.

-

The President's FY 2016 budget proposes several other ways to reduce inefficient and wasteful loopholes around estate taxes. These include lowering the estate tax exemption threshold from $5.43 million to $3.5 million for individuals ($10.86 million to $7 million for couples), increasing the top rate from 40 percent to 45 percent, closing a loophole which allows an estate to put an investment in a trust to avoid paying capital gains (the Grantor Retained Annuity Trust loophole), and simplifying the tax exclusion rules for gifts to heirs. Under these changes, the estate tax would still affect only about 0.3 percent of decedents. Savings: $153 billion.

-

Instead of fighting over every one of the hundreds of tax deductions and expenditures in the tax code, limiting them to 28 percent instead of the top income tax rate of almost 40 percent would both improve efficiency (by ceasing to overly subsidize behaviors that would occur anyway, like saving for retirement or buying a home) and generate savings of $525 billion over 10 years. Note that this cap on deductions does not end such deductions; it just reduces the disproportionate extent to which these tax benefits accrue to high income households.

-

The fact that our tax code allows US multinationals to indefinitely defer overseas earnings provides greater incentives to book profits and create jobs abroad than here at home. Surely, this incentive pushes the wrong way in terms of creating opportunity for American workers. Moving to a territorial system would supercharge those incentives, threatening to hasten profit-shifting, offshoring and outsourcing. A better approach would be a minimum tax on foreign earnings – provided it was set at an adequate level – after which firms could repatriate their earnings without further taxation. Also, to reduce the incentives for deferral, Congress should consider prohibiting US multinationals from deducting interest expenses on loans that support overseas investments when they are deferring taxes on the profits generated by those investments.

These are but a few of the many loopholes and inefficient subsidies within our tax code. Addressing them would improve the code’s fairness and efficiency and boost revenues. In that regard, doing so should be regarded as a key part as a positive growth and opportunity agenda.

Poverty and inequality

Since economic inequality began to rise in the 1970s, middle-class prosperity in the US has not been a function of growth alone. As a much larger share of economic output has accumulated at the top of the income scale, fewer pre-transfer resources have reached middle-class and poor families. As a result, poverty rates have become more “sticky”—less responsive to growth—and market incomes of the middle class have grown more slowly due to wage stagnation. To the extent that low- and middle-income families have gotten ahead over these years, it has been due to more hours of work at slower-growing or declining real hourly pay rates, increased government transfers (especially those associated with work, like the Earned Income Tax Credit, or EITC), and the unique period of full employment in the late 1990s.

These facts are particularly germane in the context of this hearing, as they link the two aspects of the themes at hand: growth and opportunity. Too often, it is assumed that overall GDP or productivity growth will yield opportunities for less advantaged families, but growth can’t help them if it fails to reach them. Here, then, are policy ideas I urge the committee to pursue to help achieve not just growth, but broadly shared growth.

-

Areas I’ve discussed already, including health care, trade, and tax reforms, are germane here as well. By providing affordable coverage with subsidies for low- and middle-income families, the ACA helps to offset the dis-equalizing impacts of growth. Enforcing global labor rights and fair currency practices helps put our factory workers on a more level playing field. And closing loopholes like step-up basis and blocking corporate inversions will prevent the tax code from further exacerbating pretax inequalities in the distribution of market outcomes.

-

This committee’s purview over many safety net programs underscores its essential role in anti-poverty policy. Moreover, House Speaker Paul Ryan’s recent discussions of poverty policy suggest that while strong differences remain between the parties in this area, there may be potential for some bipartisan actions.

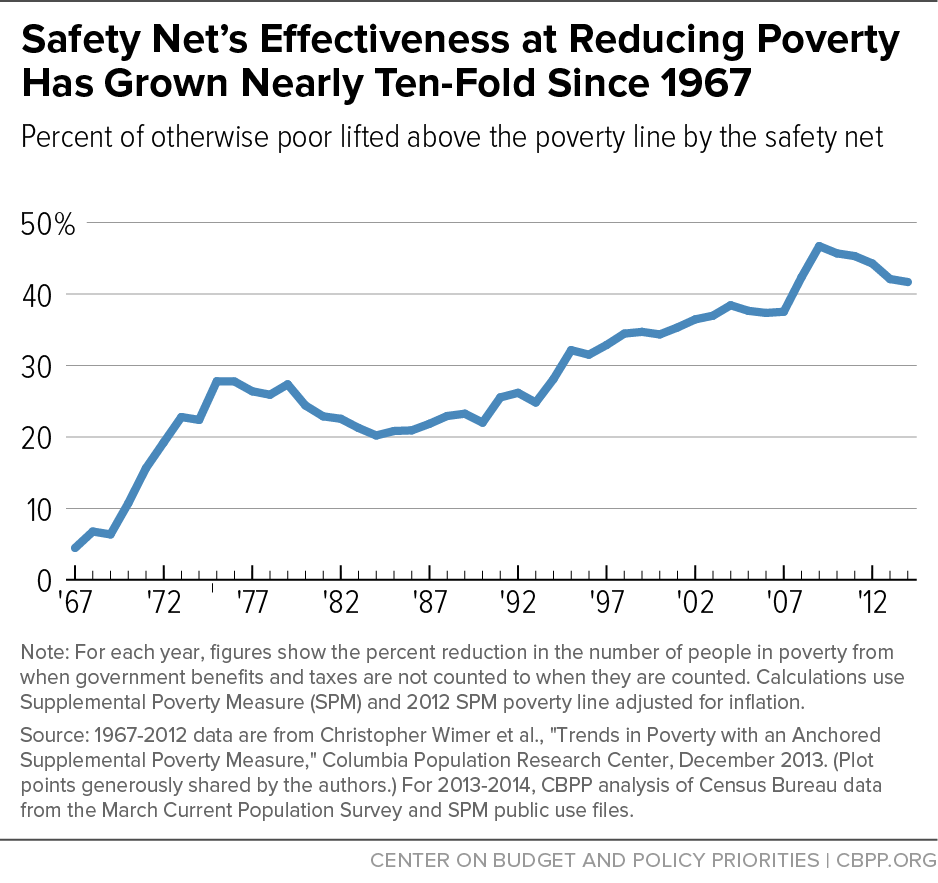

Research at CBPP has highlighted two important facts regarding the impact of the safety net. First, when properly measured—when tax and noncash benefits are factored in—the anti-poverty effectiveness of the safety net has grown considerably over time. The figure below shows that in the late 1960s, anti-poverty measures lifted about 4 percent of the poor out of poverty. Now, they lift about 40 percent, a tenfold increase in the safety net’s anti-poverty effectiveness.

Figure 7

Unfortunately, one anti-poverty policy has become less effective over time at reducing hardship: Temporary Assistance to Needy Families, or TANF. TANF expert Donna Pavetti has shown that when welfare reform was passed in 1996, 68 percent of poor families with children received cash benefits from the program, compared to 23 percent today. Pavetti also points out that states devote only half of their TANF funds to basic assistance, child care, and work activities (only 8 percent goes to helping recipients prepare for work).

These shortcomings relate to the decision to remove TANF’s individual entitlement to benefits by turning the program’s funding into a block grant, thus undermining the program’s ability to respond adequately to increased need. In the last recession, for example, many states’ TANF programs responded inadequately or not at all to the large rise in unemployment, leaving large numbers of families in severe hardship. In 16 states, TANF caseloads rose by less than 10 percent between December 2007 and December 2009; in six states, caseloads actually fell. This performance contrasts sharply with SNAP (food stamps), a program where funding still expands in response to rising need. In fact, the number of SNAP participants rose by 45 percent during the period noted above.

These very different responses to increased need should be foremost in members’ minds when considering Speaker Paul Ryan’s “opportunity grants” idea—consolidating numerous programs, including SNAP, into a large block grant. This idea would likely increase poverty, not reduce it.

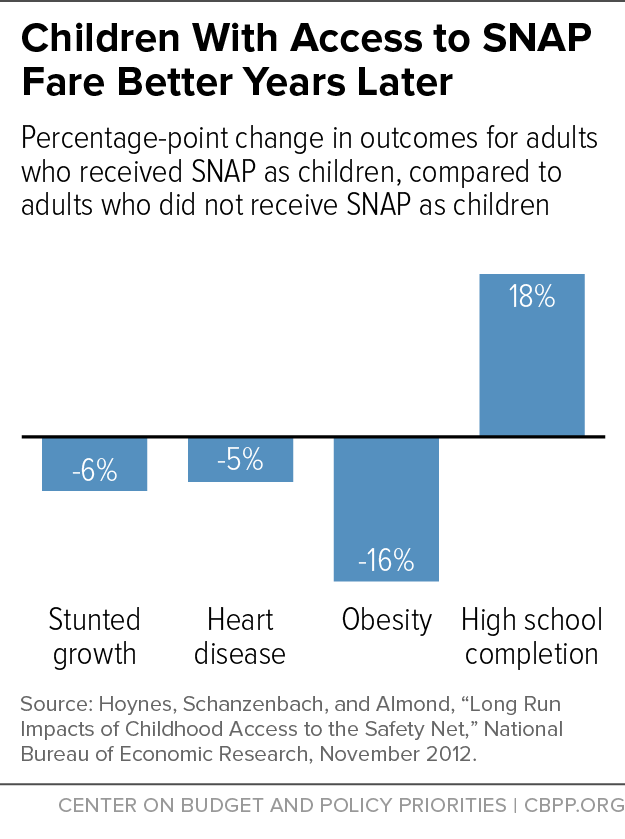

Figure 8 Second, while conservatives claim that anti-poverty measures keep people poor, longitudinal research that tracks children into adulthood has found that, to the contrary, the receipt of certain benefits acts more like a long-term investment than a simple boost to immediate consumption. For example, as the figure to the right shows, adults who received food stamps when they were children were 18 percent more likely to complete high school and 16 percent less likely to be obese than peers who did not benefit from nutritional assistance. As explained by poverty expert Arloc Sherman, other studies show that EITC receipt “…increases the likelihood of children being born at a healthy birth weight, having higher reading and math test scores in school, being more likely to go on to college, and having higher earnings in adulthood.”

Sherman also summarizes the mobility-enhancing benefits of “well-designed” rental assistance programs: “young children whose families were living in public housing and used rental vouchers to move to low-poverty neighborhoods fared better in various respects — such as earning 31 percent more by age 26 — than similar children whose families were not assigned vouchers under the demonstration project.” These findings are particularly important for low-income African American and Hispanic children, as they are more likely to grow up in neighborhoods of extreme poverty that impinge on their economic mobility.

Policy changes that would diminish or underfund these safety net functions must thus be avoided, particularly as economic inequality and the absence of full employment labor markets mean that growth today is less likely to reach the poor.

-

Pro-work, anti-poverty tax credits: Because it was not paid for, the bipartisan tax deal at the end of last year lowered expected revenue and thus increased the budget deficit. But by enshrining major improvements to two major anti-poverty tax credits—the EITC and Child Tax Credit (CTC)—into permanent law, Congress took an important step toward increasing the living standards and opportunities of working poor and near-poor families. These improvements included reducing the earnings threshold needed to qualify for even a partial CTC to $3,000 (from $14,600), increasing the threshold at which the EITC phases out for married filers (to $5,000 above the threshold for single filers, up from $3,000), and boosting the EITC for families with more than two children. Altogether, making these improvements permanent benefited 50 million people and raised around 16 million people out of poverty or closer to the poverty line in 2013; roughly half of the beneficiaries are children. As one example of the improvements’ impact, a single mother of two working full time at the federal minimum wage will be able to earn a $1,725 CTC; if these key provisions had been allowed to expire, she would have lost her entire benefit.

One other priority I urge the committee to consider is to boost the EITC for childless adults. Low-income, childless workers receive no credit if they’re under 25 and a very small credit if they’re 25 or older; as a result, they are the only group of people the federal government taxes into or deeper into poverty. Again, boosting the EITC for childless workers is a bipartisan idea: both Speaker Ryan and President Obama have issued nearly identical proposals to help fix this problem. Their plans would drop the eligibility age down to 21, increase the credit’s phase-in rate, and raise the maximum credit to $1,000.

-

Periods of full employment have been relatively few and far between over the period when inequality has risen, a fact that is not at all a coincidence. Especially given the low rates of union membership in the US, the tautness of the job market is one of the main determinants of the bargaining power of middle- and low-wage workers. At very low unemployment, employers must bid up compensation to get and keep the workers they need, enforcing a more equitable distribution of productivity growth. These dynamics are particularly beneficial to the poor, who benefit disproportionately from full employment.

Public policies that would help promote full employment, outside of those of the Federal Reserve, include reducing the trade deficit (and thus minding the currency issues raised above), investment in public infrastructure, better oversight of financial markets (to prevent the inflation of recession-inducing bubbles) and, particularly for the poor stuck in “job deserts,” direct job creation.

Policy changes that would reduce or underfund these safety net functions must thus be avoided, particularly as economic inequality and the absence of full employment labor markets mean that growth today is less likely to reach the poor.

Getting ready for the next recession

Though global markets have been roiled by the sharp fall in oil prices and the slowing of growth in emerging economies, particularly China, the US economy continues to generate steady growth rates and strong job growth. That said, there is another recession out there somewhere—economists cannot reliably predict when it will hit—and given the broad purview of this committee, it is worthwhile to examine the condition of the nation’s countercyclical policies.

The first point to make here is that, contrary to oft-repeated prejudices driven more by anti-government ideology than fact, the full spate of countercyclical interventions aimed at the last recession were highly effective. A recent review by economists Alan Blinder and Mark Zandi finds that the combined impact of these interventions, including those of the federal government and the Federal Reserve, cumulatively saved about 10 million jobs between 2009 and 2012. Blinder and Zandi’s analysis of the fiscal stimulus—the American Recovery and Reinvestment Act (ARRA) especially—is particularly germane. They estimate that temporary boosts in spending on SNAP (food stamps) and unemployment insurance benefits had the largest “bang for the buck” of any of the fiscal stimulus provisions; for example, they estimate that every $1 spending increase on SNAP generated a $1.74 boost to the economy in the first quarter of 2009. According to their model, ARRA had increased economic growth by 3.3 percent and added 2.6 million jobs at the height of its impact in 2010.

With those lessons and findings in mind, consider that the US economy faces two related challenges regarding the next recession. One challenge is technical: the “zero lower bound,” or ZLB, which is the risk that the Federal Reserve’s main tool against recession—the interest rate it controls—could be quite low by the time the next recession hits. This rate will have little room to fall, and thus little room to provide much in the way of monetary stimulus.

The ZLB elevates the importance of a countercyclical fiscal policy response, which brings me to the second challenge, a political one. Namely, policy makers must recognize the following principles:

- Budget deficits should expand in recessions and contract in expansions. In fact, they have done so since the so-called Great Recession, as the deficit topped out at about 10 percent of GDP in FY 2009 and was most recently found by CBO to be 2.5 percent of GDP in FY 2015. It is also important to remember that it is not temporary spending measures that drive deficits over the long term. It is permanent measures (spending increases as well as tax cuts) that are not paid for. “Austerity” measures—fiscal contraction in weak economies—have been shown to be harmful to growth, jobs, wages, and incomes both here in the US and even more so in Europe.

- Countercyclical programs should trigger on in a timely manner and not trigger off too soon. Unemployment insurance (UI), state fiscal relief, increased nutritional benefits, housing vouchers, and direct job creation were all helpful in generating the Blinder/Zandi results just noted. But the stimulus from many of these programs relied on legislation from Congress; it would be better to make these programs more automatically responsive to future recessions. Doing so won’t obviate the need for Congress to act when hard times hit, but it will help to ensure that stimulus “triggers on” in a more timely fashion, that it is calibrated to need, and that it lasts for an appropriate period of time. My CBPP colleague, Ben Spielberg, and I will shortly release an analysis of these dynamics which includes ideas to improve the responsiveness of the countercyclical programs mentioned above.

- State-level finances for the UI system should be improved. Given this committee’s role in maintaining a strong and responsive UI system, there are serious concerns about developments in some states in recent years. Some states have restricted UI by reducing the basic number of weeks available, cutting benefit levels, and introducing more restrictive eligibility requirements. In addition, 34 state trust funds currently fail to meet DOL's minimum standard for being prepared for a recession.[9]

Part of the problem is that many states only tax a small share of worker wages and have not adjusted this level for many years. California, for example, taxes only the first $7,000 of wages, the minimum required under federal law, and 17 other states also set their taxable wage base under $10,000. In this regard, I urge the committee to consider an increase in the federal government’s $7,000 wage base, which serves as the minimum for states and has not been increased in over 30 years.

Conclusion

The US economy has been growing steadily since the second half of 2009, payrolls have been on a solid growth path, and as the job market edges closer to full employment, nominal wage growth has slightly accelerated. These dynamics, along with unusually low-inflation, have led to real earnings gains for middle-wage workers in both of the past two years.

However, in our age of high levels of economic inequality, macroeconomic growth is necessary but not sufficient to raise middle incomes and lower poverty. In the testimony above, I have suggested a positive policy agenda in the areas of trade, tax reform, poverty, inequality, health care, and countercyclical policy that will help reconnect American families to overall growth. Taking steps to enforce rules against currency management, building on the successes of the ACA, passing a bipartisan expansion of the EITC for childless adults, closing inefficient and inequality-increasing tax loopholes, not falling prey to wasteful, “trickle-down” tax cuts, and ensuring our countercyclical policies are ready for the next recession are all ways this committee, with its encompassing purview, can help bring about this reconnection. I look forward to working with you to achieve these goals.

End Notes

[1] The data are for the 82 percent of the private workforce that are blue-collar workers in manufacturing and non-managers in services.

[2] http://jaredbernsteinblog.com/the-productivity-slowdown-mismeasurement-or-misallocationor-both/

[3] The excess cost burden refers to the historical trend of health care spending per capita growing faster than GDP per capita, leading health care spending to be an increasing share of GDP.

[4] This analysis uses CBO’s August baseline as opposed to their most recent one, which I did not have time to incorporate. The update would yield essentially the same picture, as the new CBO baseline reduces the gap between the two projections by just a tiny amount.

[5] This section reflects my own views, and not those of CBPP, which does not take a position on trade policy.

[6] http://assets1c.milkeninstitute.org/assets/Publication/MIReview/PDF/05-12-MR68.pdf

[7] https://www.cbpp.org/research/presidents-capital-gains-tax-proposals-would-make-tax-code-more-efficient-and-fair

[8] https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/51129-2016Outlook.pdf

[9] Defined as having an “Average High Cost Multiple” below 1.0. This number is as of the third quarter of 2015, the latest data is currently available. See http://www.ows.doleta.gov/unemploy/content/data_stats/datasum15/DataSum_2015_3.pdf.