President’s Capital Gains Tax Proposals Would Make Tax Code More Efficient and Fair

The tax code strongly favors income from capital gains — increases in the value of assets, such as stocks — over income from wages and salaries. These preferences are economically inefficient: they promote tax schemes that convert ordinary income into capital gains and encourage people to hold assets just to escape tax, even if they have better investment opportunities. They are also highly regressive, since capital gains are heavily concentrated at the top of the income scale. The President has proposed to make the tax code more efficient and equitable by reducing one of the biggest subsidies for capital gains (a preferential rate compared to wage and salary income) and largely eliminating another (the ability to avoid capital gains tax completely by holding on to an asset until death).

These changes would allow investments to flow to where they are most productive and reduce investment in creating tax avoidance schemes instead of in real economic activity, among other economic benefits. And, because the benefits of the current preferences for capital gains flow overwhelmingly to the top, fully 99 percent of the revenue from the President’s capital gains proposals would come from the top 1 percent of filers, the Treasury Department estimates.

Capital Gains Enjoy Costly, Regressive Preferences

Capital gains enjoy three main tax preferences over “ordinary” income from salary and wages.

- Preferential rates. The top capital gains tax rate is 20 percent, or 23.8 percent when the surtax on very-high-income households’ investment income is counted. This is well below the top 39.6 percent rate on income from employment.

- Deferral — the ability to delay paying taxes on capital gains. Workers pay taxes on their income from salary and wages in the year that they earn it — through payroll taxes deducted from their paychecks and through annual income taxes. The same is true for interest on savings accounts, which is taxed annually. In contrast, filers who get capital gains income can delay paying taxes on those gains for years, even decades, because taxes on capital gains are only due when the gain is “realized,” usually when the asset is sold.

Consider a wealthy couple, the Joneses. If they buy $100,000 worth of stock in one year and the stock price rises by 15 percent over the next few years, their shares will be worth $115,000, having increased in value by $15,000 — their capital gain. But if they don’t sell their stock, the gain isn’t “realized” and they won’t have to pay tax on it when they file their tax return. And if the stock keeps growing in value year after year, they can keep deferring paying capital gains taxes on all of those gains until they sell the stock. - Step-up basis — the ability to wipe out capital gains tax liability altogether. If a person holds on to an asset until he or she dies, the increase in its value from the time he acquired the asset until his death will never be subject to capital gains tax. This provision, known as “step-up basis,” is one of the tax code’s largest subsidies for wealth; it encourages wealthy people to turn as much of their income as possible into capital gains and hold on to their assets until death, when they can pass them to their heirs.

Suppose the Joneses held onto the stock they purchased for many years and the share value continued to climb until the stock was worth $300,000. Since they originally invested $100,000, they now have a $200,000 “unrealized” capital gain on this asset. If they sold the stock, they would owe capital gains taxes on that $200,000 gain. But if they held on to that stock until they die, neither they nor their heirs would pay capital gains taxes on the $200,000 increase in value.

As explained below, these preferences fuel inefficient tax avoidance and asset hoarding, which is why the President’s proposal to address two of them would promote economic efficiency. These preferences are also extremely regressive because the top 1 percent of households hold about 42 percent of total wealth.[1]

Proposals Would Reduce Tax Code’s Tilt Toward Capital Gains

The President proposes two measures to significantly reduce the tax code’s tilt toward capital gains:

- End step-up basis. The President proposes to repeal this subsidy — subject to large exemptions to ensure that middle-income and even most upper-income people aren’t affected — by taxing “unrealized” capital gains before they are passed to heirs, just as would occur if the owner sold the assets shortly before he or she died. This is similar to a proposal included in the budget plan that Erskine Bowles and Alan Simpson, co-chairs of the presidential fiscal commission, issued in December 2010.[2]

The President’s proposal includes robust protections for most families as well as small businesses. The first $100,000 of unrealized capital gains per individual — $200,000 per couple — would be exempt, as would $500,000 in capital gains on personal residences (which could cover more than one home). It’s important to note that these exemption amounts apply to the amount of capital gains, not total assets. In most cases, filers with total assets substantially over $200,000 (not counting their homes) would not face the tax.

The proposal has additional protections for small, family-owned businesses. Owners would owe no tax until they sold the business, for example, and closely held businesses (i.e., ones in which a small group of shareholders own most of the stock) could take up to 15 years to pay the tax.

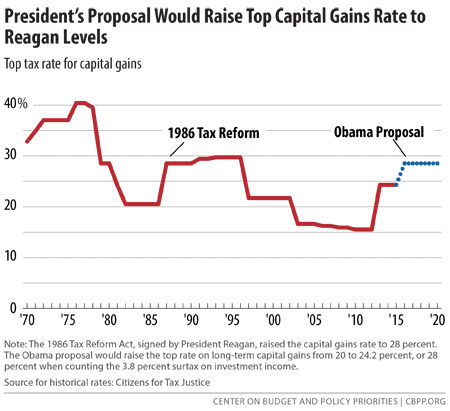

Thus, this measure wouldn’t affect ordinary families. It would touch only wealthy filers who have avoided large amounts of capital gains taxes on unrealized capital gains. (And for the tiny fraction of wealthy estates that face the estate tax, any capital gains taxes paid at death would be deducted from the value of their estate.) - Raise the capital gains rate to Reagan-era levels. President Obama proposes raising the top capital gains tax rate from 20 percent to 24.2 percent for married filers with incomes over about $500,000 (and single filers with incomes over about $430,000). When one adds the 3.8 percent surtax on investment income for high-income households, the top rate on capital gains would be 28 percent — the same as the rate enacted under the landmark Tax Reform Act of 1986 with President Reagan’s support, and well below the 39.6 percent top rate on income from employment. (See Figure 1.)

Proposals Would Improve Economic Efficiency

Ending step-up basis would remove an inefficient and regressive distortion in the tax code. It would:

- Allow investments to flow to where they are most productive. Step-up basis gives wealthy people an incentive to hold assets in order to escape tax, even if they have better investment opportunities. This “lock-in” discourages capital from flowing to where it is most productive. “Failure to tax capital gains at death encourages lock-in of assets, which in turn means less current turnover of funds available for investment,” the Congressional Research Service (CRS) has explained.

Thus, as Tax Policy Center (TPC) Co-Director Len Burman has previously noted, “taxing capital gains at death would go a long way toward removing the lock-in effect. Taxpayers could still defer capital gains liability by avoiding asset sales, but they could no longer avoid it entirely by holding assets to death.”[4] - Reduce investment in tax avoidance schemes instead of real economic activity. Wealthy filers go through all sorts of financial gymnastics to convert ordinary income into capital gains and then often to hold them until the tax liability can be wiped out. This diverts resources and skills into tax avoidance activities instead of more economically productive uses. As Burman notes, “taxing capital gains at death would enhance efficiency by deterring expensive tax-avoidance schemes.”[5]

- Make the tax code fairer. To benefit from step-up basis at all, a filer must be able to afford to hold on to assets until death, so the subsidy doesn’t benefit ordinary filers who accumulate assets in order to spend them in retirement. Instead, as CRS notes, the tax break is “most advantageous to individuals who need not dispose of their assets to achieve financial liquidity.”[6] And the bulk of the value of the tax break flows to extremely wealthy filers, who accumulate vast stocks of assets that have grown in value.

In large part because this benefit is so tilted toward the very wealthiest filers, 99 percent of the revenue from the President’s capital gains proposals would come from the top 1 percent of filers, the Treasury estimates. More than 80 percent of the revenue would come from the top 0.1 percent.[7]

The capital gains proposals would address certain other inequities in the tax code as well. For example, middle-income people with 401(k)s, IRAs, or other retirement accounts must begin withdrawing funds from their accounts (which virtually always include some capital gains earnings) no later than age 70½ and pay taxes on the withdrawals. This rule is designed to ensure that the tax-advantaged funds in the accounts don’t escape income tax altogether. But wealthy individuals with vast stock portfolios need not withdraw any of their assets and pay taxes on them and can escape taxes on their capital gains by holding the assets until they die.

Ending step-up basis is a far better solution to problems created by unrealized capital gains than other options proposed by some policymakers. For instance, some have proposed that the unrealized gains should carry over to the heirs, rather than being eliminated through step-up basis. Under “carryover basis,” heirs would then have to pay tax on all the accumulated gains when they sell the asset. This is not a good solution, for two main reasons. First, it exacerbates the problem of the inefficient lock-in of assets, as heirs would face the same incentive not to sell assets to avoid paying capital gains tax. Second, carryover basis is very difficult to administer, as it requires record-keeping that could span multiple generations.

Reducing the gap between the top capital gains tax rate and the top rate on earned income — by raising the capital gains rate — is, like ending step-up basis, economically sound as well as progressive. It:

- Reduces tax avoidance. Like step-up basis, the preferential rate for capital gains encourages wealthy filers to use shelters to convert ordinary income into capital gains. As Leonard Burman has noted:[8]

[Tax s]helter investments are invariably lousy, unproductive ventures that would never exist but for tax benefits. And money poured down these sinkholes isn’t available for more productive activities. What’s more, the creative energy devoted to cooking up tax shelters could otherwise be channeled into something productive. . . Bottom line: low rates for capital gains are as likely to depress the economy as to stimulate it.

- No evidence that it would affect national saving, investment, or growth. There is no evidence that modestly raising the capital gains tax rate as the President has proposed would hurt the economy or national saving or investment. University of Michigan tax economist Joel Slemrod, one of the nation’s leading tax policy experts, has found that “there is no evidence that links aggregate economic performance to capital gains tax rates.”[9] Similarly, Tax Policy Center analyses found no statistically significant correlation between capital gains rates and real growth in gross domestic product (GDP) during the last 50 years.[10]

Nor is there evidence that raising capital gains tax rates would depress private saving rates or national saving and investment. While a higher marginal tax rate could lead someone to work and save less by lowering the net benefit of the extra work and saving, it could also lead someone with a fixed savings goal, such as a fixed amount to help pay for a child’s college education, to work and save more in order to offset the tax increase. The empirical evidence suggests that for capital gains tax cuts of the magnitude enacted over recent decades, these two effects roughly offset each other.[11] - Reduces an extremely regressive tax preference. Capital gains are heavily concentrated at the top of the income scale. This means that the benefits of the tax breaks for capital gains flow overwhelmingly to the highest-income taxpayers, while delivering negligible benefits to the large majority of taxpayers.

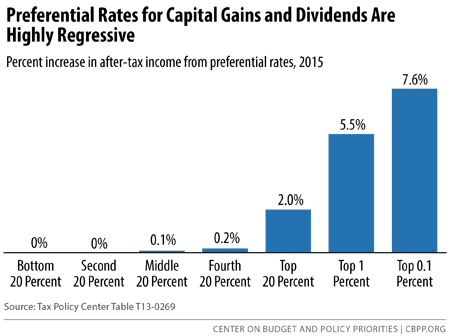

TPC estimates, for example, that in 2013, about three-quarters of the benefit of the preferential rates for capital gains and dividends (which also are taxed at a lower top rate than ordinary income) flowed to the top 1 percent of households.[12] Under current law, these preferences will raise the after-tax incomes of the top 0.1 percent of filers by 7.6 percent — an average of about $450,000 for each such taxpayer in 2015 — while raising the after-tax incomes of the middle fifth of households by just 0.1 percent, or an average of $57 per taxpayer. (See Figure 2.) Shrinking the gap between the top tax rates on capital gains and earned income would reduce this stunning disparity.

Plan Provides for Sound Uses for New Revenues

The President’s capital gains tax proposals would reduce economically inefficient tax avoidance and address “lock in” that keeps substantial investment capital from being invested in the most economically productive ways.

Not only do the revenue proposals represent sound policy in their own right, but the President’s plan would use the new revenues to finance policies that support work and help working families build skills and savings. [13] The plan includes proposals to expand the child and dependent care tax credit and establish a tax credit for secondary earners in two-earner families. The President has signaled that he will also release shortly a related budget proposal for new investments to boost child care access and quality. In addition, the President’s plan would simplify, consolidate, and better target tax subsidies for higher education, and finance the President’s recently unveiled proposal to make two years of community college free of charge.

Further, the President has reiterated his support for extending the pro-work and anti-poverty effects of the Earned Income Tax Credit (EITC) to low-income workers who aren’t raising children and for making permanent key provisions of the EITC and the Child Tax Credit slated to expire after 2017.

This means that the President’s plan would benefit large numbers of middle- and lower-income working families, and also increase work, educational attainment, and retirement savings — thereby making the labor force larger and more productive and thus promoting long-term economic growth.

Together with the capital gains tax reforms, these policies would also help to ease the enormous and growing income and wealth disparities and ensure that the benefits of the economic recovery are somewhat more widely shared.

End Notes

[1] Emmanuel Saez and Gabriel Zucman, “Wealth Inequality in the United States since 1913: Evidence from Capitalized Income Tax Data,” NBER Working Paper 20625, October 2014, http://eml.berkeley.edu/~saez/saez-zucmanNBER14wealth.pdf.

[2] See footnote to the Tax Policy Center distribution analysis of the illustrative analysis of the plan. TPC Table T10-0255, http://taxpolicycenter.org/numbers/displayatab.cfm?Docid=2854.

[3] Congressional Research Service, “Tax Expenditures: Compendium of Background Material on Individual Provisions,” S. Rep. No. 45, 112th Cong., 2d Sess., http://taxprof.typepad.com/taxprof_blog/2013/03/crs-.html p.430.

[4] Leonard Burman, The Labyrinth of Capital Gains Tax Policy, Washington, D.C., Brookings Institution, 1999, p. 138.

[5] Id.

[6] Congressional Research Service.

[7] White House Fact Sheet “A Simpler, Fairer Tax Code That Responsibly invests in Middle Class Families, January 17, 2015, hhttp://www.whitehouse.gov/the-press-office/2015/01/17/fact-sheet-simpler-fairer-tax-code-responsibly-invests-middle-class-fami.

[8] Leonard E. Burman, “Under the Sheltering Lie,” Marketplace Commentary, December 20, 2005, http://www.taxpolicycenter.org/publications/template.cfm?PubID=900918.

[9] Joel Slemrod, “The Truth About Taxes and Economic Growth,” Interview in Challenge, vol. 46, no. 1, January/February 2003, pp. 5-14.

[10] Troy Kravitz and Leonard Burman, “Capital Gains Tax Rates, Stock Markets, and Growth,” Tax Policy Center, November 7, 2005. See also Leonard Burman, “Capital Gains Tax Rates and Economic Growth (or not),” Forbes blog, March 15, 2012, http://www.forbes.com/sites/leonardburman/2012/03/15/capital-gains-tax-rates-and-economic-growth-or-not/. Burman also found no statistically significant effect lagged up to five years: Leonard Burman, The Labyrinth of Capital Gains Tax Policy, Washington, D.C., Brookings Institution, 1999, p. 81.

[11] See Chye-Ching Huang and Chuck Marr, “Raising Today’s Low Capital Gains Tax Rates Could Promote Economic Efficiency and Fairness, While Helping Reduce Deficits,” Center on Budget and Policy Priorities, September 19, 2012, p. 14, https://www.cbpp.org/cms/?fa=view&id=3837.

[12] TPC Table T13-0269

[13] Statement of Robert Greenstein on the President’s New Tax Proposals, Center on Budget and Policy Priorities, January 17, 2015, https://www.cbpp.org/cms/index.cfm?fa=view&id=5259.

More from the Authors

Areas of Expertise