Long-Term Budget Outlook Remains Challenging, But Recent Legislation Has Made It More Manageable

5/5/14 Note: This report has been updated to reflect newly available data. Click here to view the new analysis.

Summary

Despite marked improvement since our previous projections of 2010, the long-run budget outlook remains challenging and will ultimately present policymakers with difficult choices, according to CBPP’s updated projections through 2040.

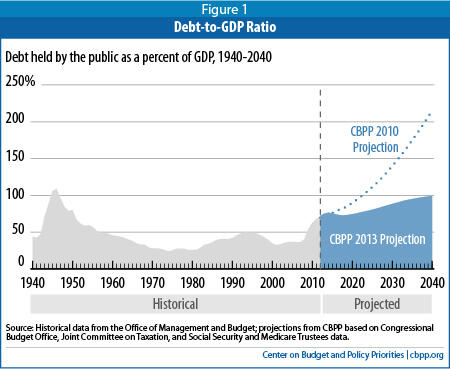

Under current budget policies, the federal debt will edge down as a share of the economy in the middle of this decade but then resume a gradual rise. The projected ratio of debt to gross domestic product (GDP) — which was 73 percent at the end of fiscal year 2012 — will reach 78 percent in 2023 and 99 percent by 2040. (See Figure 1.)

Our updated long-term projections are the product of several months of analysis and incorporate the recent Social Security and Medicare trustees’ reports and the new budget baseline that the Congressional Budget Office (CBO) issued in May. Our new projections come at a time of renewed attention to fiscal policy challenges, with White House officials and some senators beginning to meet to seek paths forward on sequestration, the debt limit, and possibly broader budget issues.

Long-Term Outlook Has Improved Substantially Since 2010

Recent legislation and other factors have substantially improved the long-term budget outlook. Health reform (the 2010 Affordable Care Act, or ACA) and other developments have significantly slowed the projected growth of Medicare spending. The 2011 Budget Control Act (BCA) has sharply cut projected discretionary spending. And the American Taxpayer Relief Act (ATRA), enacted in January, and the ACA have increased tax revenues. Along with these policy changes, interest rates have remained unusually low and health care spending growth has slowed for reasons that go beyond the ACA’s direct effects.

Three major policy uncertainties affect the fiscal outlook for the years immediately ahead: (1) whether sequestration will remain in effect after fiscal year 2013 and, if not, whether policymakers will replace it with measures that yield equivalent savings; (2) whether policymakers continue to block scheduled deep cuts in Medicare physician payments and, if so, whether they offset those costs; and (3) whether policymakers extend a group of largely corporate tax expenditures (the “tax extenders”) that are scheduled to expire every year or two and, if so, whether they offset those costs.

For this long-term analysis, we have elected to pursue the most cautious course by assuming that policymakers will cancel sequestration and the scheduled Medicare physician cuts and extend the expiring tax provisions, all without offsetting the costs. (Here, we depart slightly from the standard ten-year baseline that we, CRFB, and some other groups use for budget analyses.[5] ) Had we made different assumptions on these policy issues, our projected debt-to-GDP ratio in 2040 would be lower than 99 percent. For example, if we assumed that the tax extenders either will be allowed to expire or will be offset — as do the baselines that CRFB and we have traditionally used — the debt ratio in 2040 would be 91 percent.

Our new projection is more favorable than an oft-cited CBO projection of June 2012.[6] Although the ACA and BCA were in place by then, the near-term budget outlook has improved considerably for other reasons since CBO issued that projection 12 months ago, and those improvements affect the long-term outlook as well. More important, CBO’s projection did not purport to represent current tax and spending policies.

In June 2012, CBO produced two long-run budget paths, and most observers have focused on the more pessimistic of the two. The more optimistic path, which CBO called the “extended baseline,” strictly followed current law as it stood a year ago and, thus, assumed that policymakers would let all of the tax cuts enacted in 2001 and 2003 expire as scheduled after 2012. Most analysts viewed that assumption as highly unrealistic — correctly so, since President Obama and Congress made most of those tax cuts permanent as part of ATRA — and focused on CBO’s more pessimistic path (the “alternative fiscal scenario”) as the more realistic one.

That alternative fiscal scenario diverged from current policy in several significant ways. Besides assuming that all of the 2001-2003 tax cuts would be extended, it also assumed that the President and Congress would repeatedly cut taxes in the coming decades to keep revenues flat at 18.5 percent of GDP after 2022, by cancelling out the effects of real bracket creep and other provisions of tax law that would otherwise cause revenues to edge up gradually. On the spending side, this CBO scenario assumed that various cost-control provisions of health reform will not remain in effect after 2022. And it assumed that policymakers will restore federal spending for programs outside of Social Security and health entitlements to its average share of GDP over the previous two decades rather than allow the current downward trend to continue.

Due to these assumptions, which effectively undid much of the deficit reduction in the BCA and health reform, the debt in CBO’s alternative fiscal scenario grew to 227 percent of GDP by 2040. Although this path was based on highly pessimistic fiscal assumptions of repeated future tax cuts and program expansions, despite the nation’s fiscal problems, many commentators treated it as if it represented current budget policies.

Projections Reflect Likely Outcome of Continuing Current Budget Policies

Our long-run budget projections are neither a forecast nor an expression of desirable budgetary policy. Rather, they show what will likely happen if policymakers continue current laws and policies governing federal taxes and spending without changes (that is, without making changes either to constrain deficits or to cut taxes or expand programs without covering the cost).

We base the first ten years of our long-run projection on CBO’s May 2013 current-law baseline, with certain adjustments that policy analysts typically make to reflect current policies. Some of these adjustments increase deficits relative to the CBO baseline — for instance, we assume that sequestration, which is scheduled to run through 2021, does not continue after 2013; that scheduled cuts in Medicare physician payments do not take effect; and that certain tax cuts do not expire. We make other, commonsense adjustments that result in lower deficits — for instance, we assume a phase-down in war funding in accordance with current Administration and congressional policy and assume that the unusually high disaster funding in 2013 associated with Hurricane Sandy does not continue year after year (as CBO is required to assume in its baseline). In total, the adjustments result in deficits that are somewhat higher than those in CBO’s current-law baseline. We adopt CBO’s underlying economic and technical estimating assumptions.

After 2023, we assume that:

- Revenues will edge up gradually as a share of GDP, largely reflecting increases in real income that gradually move taxpayers into higher marginal tax brackets.

- Social Security, Medicare, and other health entitlements will grow in response to increases in enrollment and will pay the full benefits specified in law (except, as noted, we assume that the scheduled reduction in Medicare physician payment rates does not take effect).

- All other program spending — primarily discretionary, or annually appropriated, spending — will keep pace with inflation plus population growth, thereby maintaining the same level of real services per person.

- Interest costs will be shaped by the projected size of the debt and the level of interest rates, using CBO’s interest-rate projections.

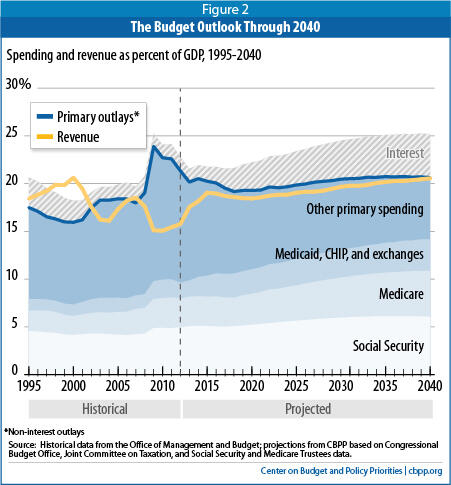

Under these assumptions, total federal outlays (including interest payments) grow from 21.5 percent of GDP in 2013 to 22.9 percent in 2023 and 25.2 percent in 2040. Primary outlays — outlays other than interest payments — fall from 20.2 percent of GDP today to 19.3 percent in the early 2020s and then rise again to 20.6 percent by 2040, slightly above today’s level. Medicare, Medicaid, and other mandatory health programs more than account for the growth in primary outlays from the early 2020s to 2040. Social Security also rises as a share of GDP, but much more modestly. Outlays for other programs decline; much of that reduction comes in the first decade, as the economy recovers and spending consequently falls for programs like unemployment insurance, and as the BCA caps on discretionary funding continue to tighten (relative to GDP). Revenues grow substantially for the next few years, reflecting an economy recovering from the deep recession, and creep up slowly thereafter, reaching 20.6 percent of GDP in 2040 — close to the level in the final Clinton years, the last time the federal budget was in surplus.

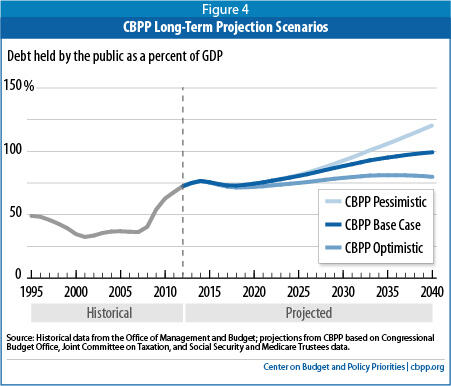

Since budget projections are highly uncertain, particularly for the long run, we also prepared two illustrative alternative paths — one with more pessimistic assumptions, the other with more optimistic assumptions.

In our optimistic path, the debt plateaus at about 80 percent of GDP in the late 2030s. This path assumes that policymakers replace sequestration for 2014 through 2021 with measures that yield equal policy savings over the next ten years and somewhat greater savings beyond that. This path also assumes slower growth in Medicare costs.

In our pessimistic path, the debt ratio rises more rapidly and reaches 120 percent of GDP by 2040. This path assumes higher rates of spending after 2023 for all programs except Social Security. These assumptions do not reflect the full range of uncertainty. Another severe recession or a catastrophic disaster, for example, could cause the debt to shoot up rapidly.

Difficult Policy Changes Still Needed to Ensure Long-Term Stability

Although the long-term budget problem appears significantly more manageable than in previous projections, policymakers still face difficult choices to put the budget on a more sustainable path for the long term. We have long maintained that stabilizing the debt-to-GDP ratio over the coming decade (with deficit reduction measures phased in after the economy has recovered more fully) is a minimum appropriate budget course.[7] Deficits are not a problem when the economy is operating well below its potential, as it has been since 2008. But a persistently rising debt-to-GDP ratio in good times and bad alike reflects an unsustainable budget policy that ultimately poses threats to financial stability and long-term growth.[8] That’s why the debt ratio should not rise when the economy is at or near full employment. In addition, a falling debt-to-GDP ratio would give policymakers more flexibility to address future economic or financial crises.

Projected debt-to-GDP ratios should be reduced through carefully designed policies that strengthen (rather than weaken) the slow economic recovery and job creation in the near term, while putting in place fair and balanced deficit reduction that grows in size over time. (Job creation is essential; it has little chance of passing either house of Congress, however, unless it is part of a broader fiscal policy package.) Replacing sequestration with a more sensible set of savings measures that end the immediate austerity which sequestration is imposing and replace it with larger savings later in the decade could both benefit the economy in the short term and produce somewhat lower debt ratios in the long term. That echoes the recent recommendations of the International Monetary Fund, which called the automatic spending cuts “indiscriminate” and instead urged U.S. lawmakers to “[repeal] the sequester and [adopt] a more balanced and gradual pace of fiscal consolidation in the short term; expeditiously [raise] the debt ceiling to avoid a severe shock to the U.S. and the global economy; and [implement] a comprehensive and back-loaded set of measures to restore long-run fiscal sustainability.”[9]

Based on CBO’s February 2013 projections, CBPP previously estimated that $1.5 trillion in additional deficit reduction (including interest savings) would stabilize the debt at 73 percent of GDP over the coming decade (relative to a baseline that, as noted, makes a different assumption about certain expiring tax cuts).[10] Because CBO’s May baseline projections reduced projected deficits by more than $800 billion through 2023, the deficit reduction required to stabilize the debt will now be somewhat less. In a future paper, we will analyze how various deficit-reduction paths, including paths that combine some near-term, temporary measures to accelerate job creation with permanent deficit-reduction measures that kick in after the economy has fully recovered, would affect the debt-to-GDP ratio.

Even if the President and Congress agreed on enough deficit reduction to stabilize the debt over the coming decade, the debt-to-GDP ratio would still very likely rise somewhat for a number of years after 2023 (before slowing down) and remain well above the level of the previous 60 years. In particular, the aging of America’s population and projected increases in per-capita health care costs will continue to put considerable pressure on federal health and retirement programs and on the budget as a whole. Stabilizing the debt ratio over the coming decade — while not sufficient to solve our long-term fiscal problems — would give policymakers time to identify, by later in the decade, further steps needed to keep the debt ratio from rising again in future decades and make more progress on these long-run budget challenges.

As we have written, going further and enacting more significant deficit reduction now that puts the debt ratio on a modest downward path after the economy has recovered would bring additional advantages (see box below) — if policymakers can achieve it without slowing the recovery, shortchanging important investments for the future, increasing poverty and inequality, or sacrificing health care quality. Unfortunately, this seems a tall order in the current political environment.[11]

There are major unknowns in the health care arena, and policymakers should approach this area with appropriate caution. The growth of both public and private health costs has slowed appreciably in the past few years, but experts do not agree on how much of this slowdown is likely to continue over the long term. As our pessimistic and optimistic paths demonstrate, the answer affects the size of the long-term fiscal problem and the magnitude of the measures that will be needed to further slow health-care cost growth (beyond modest steps that can be taken now). More fundamentally, we currently lack needed information on how to slow health cost growth substantially without reducing health care quality or impeding access to necessary care. Demonstration projects and other experiments to find ways to do so are now starting and should generate important lessons. By later in the decade, we will know more about what works and what doesn’t, and whether we can build upon and spread the changes already starting to occur to slow health cost growth.

Is There An Appropriate Debt-to-GDP Ratio?

When examining our nation’s debt, this analysis focuses on debt held by the public, which is the amount the government has borrowed in credit markets to cover its cash needs. Gross federal debt — and its close cousin, debt subject to limit — comprise debt held by the public plus debt that one part of the federal government owes another part.

Economists have long said that debt held by the public, not gross debt, is the economically meaningful debt measure. The debt held by the public is what affects the economy. The borrowing associated with that debt competes for capital with investment needs in the private sector (for factories, equipment, housing, and so forth) and can affect interest rates. In contrast, when the Treasury issues bonds to Social Security and other federal trust funds, that intragovernmental transaction does not affect credit markets. As the Congressional Budget Office has stated: “Long-term projections of federal debt held by the public (measured relative to the size of the economy) provide useful yardsticks for assessing the sustainability of fiscal policies.” In contrast, gross debt “is not useful for assessing how the Treasury’s operations affect the economy.”a

A stable debt-to-GDP ratio is a key test of fiscal sustainability.b Increases in the dollar amount of debt are not a serious concern as long as the economy is growing at least as fast. Between 1946 and 1974, for example, debt held by the public grew significantly in dollar terms but — thanks to economic growth — plummeted as a percentage of GDP, from 109 percent to 24 percent.

Some suggest that certain debt-to-GDP ratios have a particular meaning in terms of their effect on the economy. In reality, there are no absolute thresholds. Until recently, for instance, many pointed to a 2010 analysis by economists Carmen Reinhart and Kenneth Rogoff suggesting that debt-to-GDP ratios of 90 percent or more are associated with significantly slower economic growth. But the authors have acknowledged computational errors in their original work and clarified that there is no “magic threshold” for the debt ratio above which countries pay a marked penalty in terms of slower economic growth. To the extent that countries with higher levels of debt experience slower growth, there is little evidence that the high debt caused the slow growth; the reverse is just as likely to be true — that the slow growth caused the high debt — or some combination of the two effects.

Similarly, some analysts call for a debt ratio of 60 percent of GDP or less, a goal that the European Union and the International Monetary Fund adopted some years ago. No economic evidence, however, supports this or any other specific target, and IMF staff have made clear that the 60 percent criterion is arbitrary and should not guide near-term fiscal policy in the wake of the recent financial crisis, which drove up government debt worldwide.

All else being equal, a lower debt-to-GDP ratio is preferred because of the additional flexibility it provides policymakers facing economic or financial crises. But, all else is never equal. Lowering the debt ratio comes at a cost, requiring larger spending cuts, higher revenues, or both. That is why we have emphasized the importance of not only the quantity but also the quality of deficit reduction, which should not hinder the economic recovery or cut spending in areas that can boost future productivity or harm vulnerable members of society.

a Congressional Budget Office, The Long-Term Budget Outlook, December 2007, p. 12.

b Ideally, policymakers would focus on the amount of debt held by the public net of financial assets (such as securities and loans) that the government owns.

Overview of the Long-Term Budget Projection

Like other fiscal policy organizations, CBPP examines the long-run budget outlook by focusing on a limited set of revenue and spending categories. This streamlined approach captures the main dynamics of future spending and revenues without getting bogged down in the kind of detail that’s important for annual congressional deliberations but can be a distraction when looking decades ahead.

Between 2013 and 2040, we project that total revenues under current policies will rise from the current low level of 17.5 percent of GDP to 20.6 percent. Program or primary outlays — that is, federal spending excluding interest — will fall from 20.2 percent of GDP today to 19.3 percent in the early 2020s, before climbing to 20.6 percent in 2040. As Figure 2 shows, revenues will soon come close to covering non-interest outlays throughout our projection period.

Analysts and policymakers who use federal outlays to describe the size of government should focus on program or primary outlays, because such spending reflects explicit policy decisions. The remaining category of spending — interest — is determined by the size of the federal debt and the level of interest rates. Total outlays, which include interest, represent 21.5 percent of GDP today and rise to 25.2 percent by 2040. (See Figure 2.)

The Outlook for Revenues

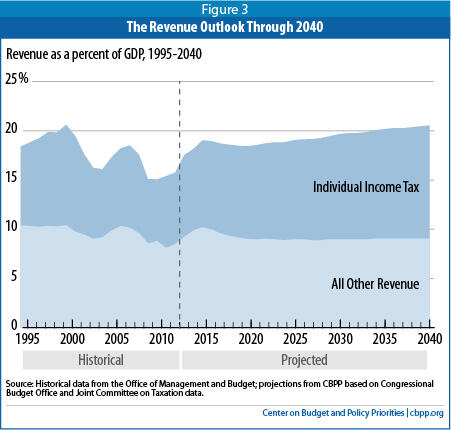

Federal revenues are projected to rise under current policies from 17.5 percent of GDP in 2013 to 18.8 percent in 2023, due in significant part to the economic recovery. Revenues are then projected to rise gradually over the ensuing 17 years by slightly less than 2 percent of GDP. They reach 20.6 percent of GDP in 2040, which is close to the levels in the final years of the second Clinton Administration, when the nation last ran budget surpluses.

Our revenue projection departs from current tax law in just two respects. First, it assumes that expansions in certain tax credits (the Earned Income Tax Credit, the Child Tax Credit, and the American Opportunity Tax Credit for college students) that policymakers enacted in 2009 and extended in 2010 and 2013 will continue after 2017, their current expiration date. Second, it assumes that a set of temporary tax cuts primarily benefiting businesses that are colloquially known as “the extenders” (because policymakers regularly extend them) will also continue. Many budget analysts make such assumptions because they give a more realistic picture of what it means to follow current tax policies.

No significant changes in tax law are scheduled to take effect after the end of the ten-year projections in 2023. Revenues creep up gradually as a share of GDP between then and 2040 for two major reasons. First, rising real incomes push people into higher tax brackets, a trend commonly labeled “real bracket creep.” (Although the income tax brackets are indexed to keep pace with inflation, income is projected to grow at a slightly faster rate, so more income becomes taxed at higher rates over time, even as statutory income tax rates remain unchanged.) Second, an aging population will withdraw growing amounts from retirement accounts, and most of those withdrawals are taxable. In contrast, while funds remain in these accounts, they enjoy tax-favored treatment.

Those factors cause individual income tax receipts to rise slowly but steadily as a percentage of GDP. (See Figure 3.) All other revenues — which include social insurance taxes such as those for Social Security and Medicare, corporate income taxes, estate, excise and other taxes — are projected to remain near today’s level (about 9 percent of GDP) in the long run, after briefly climbing in the next few years as the economy recovers.

The Outlook for Spending

The major categories of federal spending will exhibit markedly different patterns between now and 2040.

Social Security. Benefits under the Old-Age, Survivors, and Disability Insurance programs (together known as Social Security) will rise slowly but steadily in the next two decades — from 5.0 percent of GDP today to 6.1 percent in the 2030s — and then stabilize. That pattern largely reflects the aging of the population. The share of Americans who are 65 or older will climb from 14 percent today to just over 20 percent in the mid-2030s before leveling off.[12] (Three-fourths of Social Security benefits go to people 65 or older; most of the rest go to early retirees over age 62 and disabled workers over age 50.) The scheduled rise in the program’s full retirement age — which is now 66 (up from 65 before 2000) and will climb to 67 between 2017 and 2022 — dampens the growth in Social Security costs. Each year’s rise in the full retirement age trims benefits across the board for future retirees by about 7 percent, regardless of whether they claim benefits early or work until the full retirement age (or beyond).[13]

Medicare. Net outlays for Medicare benefits — that is, total payments minus the premiums paid by enrollees — are expected to rise from 3.1 percent of GDP today to 4.8 percent in 2040. Medicare fundamentally faces the same demographic pressures as Social Security. (People aged 65 or older who are insured for Social Security benefits through their own work or a spouse’s — as well as disabled Social Security beneficiaries under age 65 who have served a two-year wait — are eligible for Medicare.)

Unlike Social Security, Medicare faces an extra source of cost pressure: the tendency of medical costs, fueled by technological advances and increased utilization, to outpace the growth of GDP. The ACA’s cost controls and delivery system reforms, plus other developments in health care delivery, are expected to curb (though not erase) that pressure. Our projections assume that policymakers will not undo the ACA’s cost-control provisions.[14]

Like most other organizations’ long-term projections, CBPP’s assume that full benefits to Social Security and Medicare Hospital Insurance (HI) recipients will continue even after those trust funds are exhausted. Participants count on those benefits to continue, and policymakers have long adopted that assumption as their benchmark when weighing proposals. Nevertheless, the programs technically lack legal authority to pay full benefits once their trust funds are exhausted. Their trustees project that the HI fund will be exhausted in 2026 and the combined Social Security funds in 2033.[15] In those years, incoming revenues would still support 87 percent of Medicare hospital insurance benefits and about three-quarters of Social Security benefits.[16] Policymakers have always acted to stave off trust fund depletion whenever it loomed. For an alternative in which we assume that policymakers trim benefits, raise revenues, or some combination to ensure continued trust fund solvency after that point, see “Illustrative Alternative Projections” below.

Medicaid, CHIP, and health insurance subsidies. Medicaid — a joint federal and state program — provides health coverage to eligible low-income people, while the Children’s Health Insurance Program (CHIP) covers many low-income children through capped grants to states. The ACA expanded the reach of Medicaid, and about half of the states thus far have decided to offer the expansion, with more expected to do so over time. Also under the ACA, new state-based exchanges will enable millions of people without other coverage to buy health insurance at reasonable prices and without exclusions for pre-existing conditions or other restrictions that have often made individual or small-group coverage unaffordable. The Medicaid expansion and exchanges will get underway in 2014.

The combination of health-cost growth and the ACA expansions will push up spending for Medicaid, CHIP, and the exchanges by a full percentage point of GDP in the coming decade — from 1.7 percent now to 2.7 percent in 2023, with most of that growth occurring by 2017. After 2023, following CBO estimates, the growth in this category of health spending slows, reaching 3.3 percent of GDP in 2040; most of that increase occurs in Medicaid which — like Medicare — will face demographic pressures from an aging population. (Medicaid pays for over half of all long-term care costs.)

Other program spending. This category includes hundreds of programs that Congress appropriates annually — known as defense and nondefense discretionary programs — as well as entitlement or mandatory programs other than Social Security, Medicare, Medicaid, CHIP, and health insurance subsidies.

- Defense discretionary spending covers the budgets of the Pentagon and certain related agencies (such as the intelligence community and the nuclear-weapons programs of the Department of Energy).

- Nondefense discretionary spending encompasses federal spending for transportation; space and science; biomedical research; environmental protection; early-childhood, elementary, and secondary education; subsidized housing; veterans’ medical care; international aid and diplomacy; justice, law enforcement, and general government; and many other national priorities.

- Other mandatory spending includes pensions for federal civilian and military retirees; veterans’ pensions, compensation, and education benefits; the Supplemental Nutrition Assistance Program (SNAP, formerly known as food stamps); the refundable portions of the EITC, Child Tax Credit, and American Opportunity Tax Credit; Supplemental Security Income (SSI) for poor elderly and disabled people; unemployment insurance; Temporary Assistance for Needy Families (TANF); farm price supports; and many smaller programs.

Over the next ten years, this catchall category of “other spending” will fall substantially as a percentage of GDP — from 10.3 percent today to 7.9 percent in 2023. (We base our projections on CBO’s, adjusted to phase down operations in Afghanistan, remove the assumed extension of Hurricane Sandy funding, and continue certain expansions of refundable credits that are slated to expire in 2017, as detailed in Appendix 1.) Most of this drop occurs in discretionary spending, which falls as the BCA’s discretionary caps squeeze defense and nondefense programs alike and as the Afghanistan war continues to wind down. Such programs will be squeezed even more tightly if the BCA sequestration continues for 2014 through 2021 as scheduled. Our baseline assumes that policymakers end sequestration after 2013 and do not offset the resulting costs.

Other mandatory spending declines, though less precipitously. Unlike Social Security and the major health programs, most of the programs in this category do not face particular demographic or cost pressures; some — such as unemployment insurance and SNAP — will shrink automatically as the economy recovers and unemployment declines.[17]

In the long run, neither CBO nor other forecasters attempt to project this category of “other spending” on a program-by-program basis, an impractical task given its widely varied composition. Instead, they project aggregate spending using stylized assumptions about its future growth. We assume that discretionary spending after 2021 (the last year of the BCA caps) — and the “other program spending” category as a whole after 2023 (including other mandatory spending) — will grow in step with inflation plus population growth. In other words, we assume that such spending will remain steady per person in real terms. This implies that such spending will edge down as a percentage of GDP, from 7.9 percent in 2023 to 6.5 percent in 2040.

Our approach to projecting “other spending” is consistent with both historical experience and the factors driving those programs in the future. Many large mandatory programs in this category — notably federal military and civilian retirement and Supplemental Security Income — are projected to shrink significantly as a percentage of GDP for decades to come. And while some discretionary programs face rising demand from a growing population, others may not. The historical record indicates that, over the long run, “other spending” tends to rise more in line with inflation and population growth than with GDP. For example, total spending for programs other than Social Security and mandatory health programs is projected to be virtually identical in the second half of the coming ten-year period, after the economy has recovered — from 2019 through 2023 — to its average level for 1976-2012, adjusted for inflation plus population. (See Appendix 2.)

Of course, a richer country may choose to invest more in education, infrastructure, research, and the various other programs in this category. Such a choice — which could push other spending somewhat above 10 percent of GDP, its average over the 1992-2012 period — is reflected in CBO’s alternative fiscal scenario. But such an assumption would mark a significant increase in real spending per American and is not consistent with historical trends. In the case of other mandatory spending, it would require enacting increases in benefit amounts or expansions in eligibility. Although an increase in this category of spending might be desirable, it does not reflect either the current path or historical experience and should not be depicted as a continuation of current policy.

Interest. Unlike every other spending category, net interest does not reflect explicit funding decisions by policymakers. Instead, it is jointly determined by (1) the amount of borrowing that’s necessitated by policymakers’ other spending and revenue decisions and (2) the interest rates set in financial markets.

Today, federal net interest costs represent just 1.4 percent of GDP, almost matching the low figures recorded in the 1950s through early 1970s and again in the early 2000s, when our debt was far smaller as a share of GDP. But today’s low interest rates, which are holding down borrowing costs, are not expected to last forever. By 2023, net interest costs — at 3.4 percent of GDP — are expected to be about two and a half times today’s level, although the debt itself will barely climb (from 75 percent to 78 percent of GDP) during that same period.

In the long run, CBPP assumes — following CBO — that the real interest rate on the flagship ten-year Treasury note will be 3.0 percent, compared to less than 1 percent today. With an inflation rate (as measured by the Consumer Price Index for Urban Consumers, or CPI-U) that levels off at 2.5 percent, that implies a nominal ten-year rate of 5.6 percent. The effective interest rate on federal debt is somewhat lower because the government borrows in a range of maturities from three months to 30 years, with an average maturity of about five years. In addition, the government collects some interest income — such as interest on student loans — that partly offsets the interest it owes on borrowing. By 2040, we estimate that under current policies, debt will reach 99 percent of GDP and net interest costs will equal 4.6 percent of GDP.

Illustrative Alternative Projections

In the optimistic path, the debt-to-GDP ratio grows slowly and levels off at 80 percent in the late 2030s — 19 percentage points below our baseline projection. (See Figure 4.) Two differences in assumptions lead to this more favorable outcome. First, under this path, we assume that policymakers, instead of ending sequestration after 2013 and not offsetting the cost, will replace it after 2013 with other deficit-reduction measures, generating policy savings (not counting interest) of about $940 billion over the 2014-2023 period relative to our base case. This assumption is responsible for four-fifths of the improvement between the base case and the optimistic alternative. Second, the optimistic path assumes that most of the recent slowdown in health-care cost growth will continue and the rate of Medicare “excess cost growth” (the percentage by which the growth of health care costs per beneficiary exceeds the growth of GDP per person) after 2023 will average 0.5 percent a year, or about 0.6 percentage points a year less than in the base case.

In the pessimistic case, debt climbs more rapidly than in the baseline and reaches 120 percent of GDP by 2040. This result stems from assumptions of higher spending in two categories. First, spending for programs other than Social Security, health entitlements, and interest is assumed to grow at the same rate as GDP after 2023, rather than keeping pace with inflation and population growth. This assumption accounts for three-fourths of the deterioration between the base case and the pessimistic alternative. Second, health care spending grows at the more rapid rate in CBO’s alternative fiscal scenario, which assumes that Congress will discontinue some of the ACA’s cost-saving provisions after ten years.

Since other unforeseen factors could also drive up spending or reduce revenues (or vice versa) the actual budget outcome could turn out to be even worse than our pessimistic alternative or even better than our optimistic scenario.

The projected insolvency of the Social Security and Medicare Hospital Insurance trust fund represents another source of uncertainty for the long-run budget projections. The programs’ trustees project that the HI trust fund will be exhausted in 2026 and that Social Security’s combined Old-Age and Survivors Insurance and Disability Insurance trust funds will become insolvent in 2033.[18] Our long-run projections assume, as do most other budget projections, that Medicare and Social Security benefits will continue to be paid in full even after these dates. Under law, however, benefit payments are not allowed to exceed the resources available in the respective trust funds; therefore, after the trust funds are exhausted, benefits could be paid only to the extent that dedicated taxes are collected in each year.

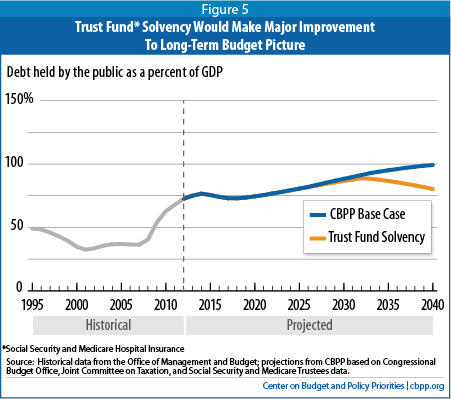

Bringing the HI and Social Security trust funds into financial balance — through tax increases, benefit cuts, or some combination of the two — would make a major contribution to improving the long-run budget picture. If Social Security and HI expenditures equaled these programs’ revenues each year after their projected insolvency, federal debt would peak at 89 percent of GDP in 2032 and decline to 80 percent of GDP by 2040. (See Figure 5.)

Comparison with CBO and Other Projections

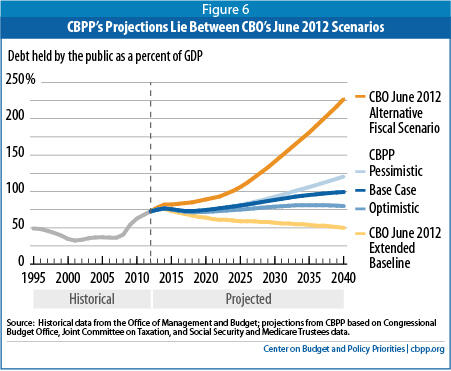

CBPP’s new projections fall between the two projections in CBO’s last long-term report, issued in June 2012.[19] (See Figure 6.) Neither of those two CBO projections, however, offers a realistic representation of today’s budgetary policies.

CBO’s alternative fiscal scenario assumed that revenues and spending will diverge from current budgetary policies in three major ways. First, it assumed that once revenues reach 18.5 percent of GDP, they will remain there over the long run. But Congress would have to cut taxes continually in order to bring this about, since rising real incomes will move taxpayers into higher income tax brackets, and since certain other tax provisions — for example, withdrawals from tax-favored retirement accounts — will have a growing impact over time as more baby boomers retire.

Second, the CBO alternative scenario assumed that the ACA provisions to restrain the growth of Medicare costs will not be in effect beyond ten years. This outcome would require Congress to change the Medicare law substantially.

Third, the CBO alternative scenario assumed that spending for programs other than the major entitlements (Social Security, Medicare, Medicaid, and other health programs) will revert to its average share of GDP over the past 20 years and then grow with GDP. Once again, this higher level of spending could come about only if Congress enacted increases in this category of spending, setting it on a very different course that reverses the budget cuts of recent years and greatly expands real spending per person. (See Appendix 2.)

For all these reasons, CBO’s 2012 alternative fiscal scenario substantially overstates the trajectory of federal deficits and debt and should not be viewed as a projection of current budgetary policies.

The long-term “realistic baseline” of the Committee for a Responsible Federal Budget is similar to our base projection. In CRFB’s latest update, the debt-to-GDP ratio reaches 108 percent in 2040, compared to 99 percent in our base case. Most of the difference in the projections stems from different assumptions about the growth of discretionary and other mandatory spending (that is, other than Social Security and the major health programs). As explained above, we assume that these categories of spending will grow at the rate of inflation plus population growth in the long run; CRFB assumes they grow at the rate of growth of GDP. A smaller portion of the difference in the projections is due to different assumptions about the rate of increase in health spending. Even so, CRFB’s “realistic baseline” entails much lower debt levels than our pessimistic alternative. (Note: CRFB’s baseline was issued before the Medicare and Social Security trustees issued their latest reports on May 31. Our baseline incorporates the trustees’ revised, modestly more optimistic Medicare cost projections. The trustees’ latest Social Security projections are essentially unchanged from those in the trustees’ previous report.)

Appendix 1

Assumptions Underlying the Projections

The first ten years of our estimates are based on CBO’s ten-year baseline budget projections published in May 2013.[20] We adjust CBO’s baseline to reflect current tax and spending policies more realistically, as explained below. For subsequent years, we project spending and revenues using growth rates from CBO’s last long-term projections, published in June 2012, and the Medicare and Social Security trustees’ most recent annual reports, published on May 31, 2013.[21]

Budget projections necessarily reflect a great deal of uncertainty. We therefore find it inadvisable to place much confidence in estimates that extend beyond 30 years. We outline below the assumptions that underlie our projections, which run through 2040, and discuss the outcomes that would result from more pessimistic and optimistic assumptions. Of course, we cannot know what policymakers will decide or what voters will desire in future years — variables with enormous implications for spending and revenues. What we can do, however, is show where the current trajectory leads. Our projections provide a benchmark for understanding the long-term fiscal implications of the major choices that policymakers face.

Projections Through 2023

We base our expenditure and revenue projections through 2023 on CBO’s May 2013 baseline budget projections, adjusted by CBO’s estimated effects of certain alternative policy scenarios. CBO’s ten-year projections follow budget baseline rules that call for assuming that current laws will remain unchanged — an assumption that is sometimes unrealistic. In certain areas, current laws differ from current policies. For this reason, we and many other budget-watchers regularly adjust the CBO baseline.

We diverge from CBO’s ten-year baseline in assuming the following (see Table 1):

- A collection of business and individual tax deductions and credits, known as “Normal Tax Extenders,” will not expire on schedule, but rather will continue without being paid for.[22]

- The improvements to refundable tax credits (the Child Tax Credit, Earned Income Tax Credit, and American Opportunity Tax Credit) in the 2009 Recovery Act — which policymakers have extended twice — will not expire in 2017 but will be permanently extended.

- Congress will continue to defer the scheduled sustainable growth rate (SGR) cuts in Medicare physician payments, as it routinely has in recent years, and instead freeze payment rates. (CBO’s baseline assumes that the SGR cuts will take effect.)

- War expenditures will decline due to a reduction in total troop levels in Afghanistan to 45,000 by 2015.

- The automatic, across-the-board cuts (sequestration) that the 2011 Budget Control Act (BCA) specifies for 2014 through 2021 will not take effect. (These cuts are scheduled because of the failure of the Joint Select Committee on Deficit Reduction [the “supercommittee”] to reach an agreement.)

- The increased disaster funding necessitated by Hurricane Sandy, to the extent that it exceeds the historical average for disaster funding, is a one-time expense. (CBO is required by law to assume that the increased funding will continue every year for the next ten years.)

- Discretionary spending will grow with population and inflation, instead of just inflation, after the expiration in 2021 of the BCA’s budget caps.

Expenditure Projections After 2023

Our long-term projections use the 2023 levels of spending and revenues described above. We then apply what we believe are appropriate growth rates to the various categories of spending and revenues. We project the growth of Social Security costs after 2023 at the same rate as the Social Security trustees’ intermediate long-term projections.[23] For Medicare, we project cost growth according to the Medicare trustees’ “alternative physician projection,” which is the same as their intermediate projection except that it assumes that the SGR cuts will not take place and that Medicare physician spending growth will gradually return to the same rate as overall health spending per person.[24] We project Medicaid, CHIP, and health exchange subsidy costs to grow at the rate in CBO’s June 2012 extended baseline, which assumes current law for the three programs.

| Table 1 CBPP Adjustments to CBO's May 2013 Ten-Year Baseline Projections (Increase or decrease in projected deficits by fiscal year ($ billions); totals may not add due to rounding) | ||||||||||||

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | ‘14-‘23 | |

| CBO baseline deficits | 642 | 560 | 378 | 432 | 482 | 542 | 648 | 733 | 782 | 889 | 895 | 6,340 |

| Continue most expiring tax provisions: | ||||||||||||

| Recovery Act credit improvements | 0 | 0 | 0 | 0 | 0 | 2 | 28 | 28 | 28 | 28 | 27 | 140 |

| All other extenders (except bonus depreciation) | 0 | 21 | 42 | 43 | 46 | 49 | 52 | 58 | 63 | 68 | 75 | 517 |

| Phasedown in Afghanistan | 0 | -15 | -34 | -46 | -54 | -57 | -61 | -62 | -64 | -66 | -67 | -526 |

| Freeze Medicare's Payment Rates for Physicians | 0 | 9 | 13 | 13 | 13 | 13 | 14 | 15 | 16 | 17 | 17 | 139 |

| Assume sequestration does not take effect: | ||||||||||||

| Defense discretionary | 0 | 28 | 43 | 49 | 51 | 53 | 53 | 53 | 53 | 54 | 55 | 491 |

| Nondefense discretionary | 0 | 21 | 31 | 34 | 35 | 36 | 36 | 35 | 34 | 34 | 34 | 329 |

| Medicare (net) | 0 | 3 | 8 | 8 | 8 | 9 | 10 | 10 | 11 | 5 | 0 | 72 |

| Other mandatory (including defense mandatory) | 0 | 7 | 7 | 6 | 6 | 5 | 5 | 6 | 5 | 0 | 0 | 48 |

| Assume Sandy “emergency” funding is one-time expense | 0 | -2 | -10 | -18 | -26 | -31 | -36 | -39 | -41 | -43 | -45 | -291 |

| Assume discretionary grows with population and inflation after 2021 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 6 | 20 | 26 |

| Subtotal of adjustments | 0 | 71 | 99 | 89 | 79 | 78 | 101 | 102 | 104 | 102 | 118 | 945 |

| Debt service | 0 | 0 | 2 | 4 | 9 | 14 | 20 | 26 | 32 | 39 | 46 | 192 |

| Total adjustments | 0 | 72 | 101 | 93 | 88 | 93 | 121 | 128 | 136 | 141 | 164 | 1,137 |

| CBPP baseline deficits | 642 | 632 | 479 | 525 | 570 | 634 | 770 | 861 | 918 | 1,029 | 1,059 | 7,478 |

| Outlays, Revenues, and Deficits as a Percent of GDP Under CBPP Projections | ||||||||||||

| Outlays | 21.5% | 21.9% | 21.8% | 21.8% | 21.6% | 21.6% | 22.0% | 22.2% | 22.4% | 22.9% | 22.9% | 22.1% |

| Revenues | 17.5% | 18.1% | 19.0% | 19.0% | 18.7% | 18.6% | 18.5% | 18.4% | 18.6% | 18.7% | 18.8% | 18.6% |

| Deficits | 4.0% | 3.8% | 2.7% | 2.8% | 2.9% | 3.0% | 3.5% | 3.8% | 3.9% | 4.1% | 4.1% | 3.5% |

| Source: CBPP calculations based on data from the Congressional Budget Office. | ||||||||||||

We also assume that spending for discretionary and other mandatory programs (a category that excludes Social Security, Medicare, Medicaid, CHIP, and health insurance subsidies) grows with the rates of population growth and inflation. This approach essentially assumes that these programs will continue providing the same real level of per-person services in the future as they do in 2023. Appendix 2 provides a detailed discussion of our reasoning.

Revenue Projections After 2023

The American Taxpayer Relief Act of 2012 permanently extended most of the 2001 and 2003 tax cuts, which are now part of current law. ATRA also permanently continued relief from the alternative minimum tax (AMT), indexing the exemption to inflation. In both cases, Congress ended a series of short-run extensions and patches that had led analysts to draw a sharp distinction between current law and current policy. With ATRA’s enactment, that distinction has diminished.

We project individual income tax revenues using the growth rates after 2023 in Variant 2 of the extended baseline in CBO’s June 2012 report.[25] Although the report was published before ATRA, Variant 2 of CBO’s individual income tax revenue projections assumed extension of all of the 2001 and 2003 tax cuts and AMT relief, which is close to what Congress actually enacted and therefore provides a reasonable proxy for long-term growth in this category of revenues. It also assumed real bracket creep, which leads to growing revenues over time as rising real incomes slowly push more income into higher tax brackets. Our resulting revenues from individual income taxes are about 0.5 percent of GDP higher than in CBO’s Variant 2 — the consequence of ATRA’s tax increase on a subset of upper-income taxpayers.

For all other revenues, which include corporate income and payroll taxes and other taxes and fees, we project growth with CBO’s June 2012 extended baseline projections for “all other revenue,” with the exception of risk adjustment receipts. The ACA requires each state (or the federal government on a state’s behalf) to assess a charge on certain individual and small-group health insurance plans if the actuarial risk of a plan’s enrollees in a given year is less than the average actuarial risk of all enrollees in all such plans in the state, and to use those proceeds to compensate plans that serve higher-risk enrollees. [26] The budget will record the risk-adjustment charges as receipts and the payments as outlays, but the two will offset each other and have virtually no net effect on the deficit. Because the payments are included with other program spending, we take care to assess the same amount of offsetting revenues.

Projection Results

Table 2 below shows our projections for each major category of the budget as a share of GDP between 2000 and 2040. Debt as a share of GDP jumped between 2005 and 2010, reflecting the effects of the Great Recession and actions taken to mitigate its impact. Debt shrinks relative to GDP in the middle of the coming decade and then starts growing again near the end of the decade, ultimately reaching 99 percent of GDP in 2040.

| Table 2 Outlays, Revenues, Deficits, and Debt as a Share of GDP Through 2040 | |||||||||

| Social Security | Medicare | Medicaid, CHIP, and exchanges | Other program outlays | Total program outlays | Net interest | Revenues | Surplus(+)/ deficit(-) | Debt held by the public | |

| 2000 | 4.1% | 2.0% | 1.2% | 8.6% | 15.9% | 2.3% | 20.6% | 2.4% | 35% |

| 2005 | 4.2% | 2.4% | 1.5% | 10.4% | 18.4% | 1.5% | 17.3% | -2.6% | 37% |

| 2010 | 4.9% | 3.1% | 2.0% | 12.8% | 22.7% | 1.4% | 15.1% | -9.0% | 63% |

| 2012 | 4.9% | 3.0% | 1.7% | 11.7% | 21.3% | 1.4% | 15.8% | -7.0% | 73% |

| 2013 | 5.0% | 3.1% | 1.7% | 10.3% | 20.2% | 1.4% | 17.5% | -4.0% | 75% |

| 2015 | 5.1% | 3.1% | 2.2% | 9.9% | 20.2% | 1.5% | 19.0% | -2.7% | 76% |

| 2020 | 5.2% | 3.2% | 2.6% | 8.3% | 19.3% | 2.9% | 18.4% | -3.8% | 74% |

| 2023 | 5.5% | 3.5% | 2.7% | 7.9% | 19.6% | 3.4% | 18.8% | -4.1% | 78% |

| 2025 | 5.6% | 3.7% | 2.8% | 7.7% | 19.9% | 3.5% | 19.0% | -4.4% | 81% |

| 2030 | 5.9% | 4.2% | 3.0% | 7.4% | 20.5% | 4.1% | 19.7% | -4.9% | 88% |

| 2035 | 6.1% | 4.6% | 3.1% | 6.9% | 20.7% | 4.4% | 20.2% | -4.9% | 95% |

| 2040 | 6.1% | 4.8% | 3.3% | 6.5% | 20.6% | 4.6% | 20.6% | -4.6% | 99% |

| Source: CBPP calculations based on Congressional Budget Office data. | |||||||||

Alternative Projections

In addition to projecting a base case that continues current policies, we have also prepared pessimistic and optimistic scenarios that illustrate the effects of plausible alternative outcomes.

Optimistic alternative. In our optimistic case, we make two assumptions that slow the growth of debt in the long run:

- The recent slowdown in health cost growth continues, so that cost growth per beneficiary in Medicare that exceeds the growth of GDP per person (called “excess cost growth”) averages 0.5 percent per year after the end of the ten-year budget window.

- Congress enacts permanent deficit reduction legislation to replace the supercommittee sequestration cuts for 2014 through 2021. Compared to the base case, which assumes that sequestration is cancelled but not paid for, this entails about $940 billion in policy savings (primarily increases in revenues and reductions in non-interest mandatory spending) over ten years and $1.1 trillion in total deficit reduction (including interest savings). Since revenues and mandatory spending are assumed to grow more rapidly than discretionary spending, which bears the brunt of sequestration, this policy produces somewhat more deficit reduction in the long run than simply allowing sequestration to remain in effect.

Combining these two favorable assumptions, our optimistic case projects the debt ratio to rise more slowly, reaching 80 percent of GDP by 2040. Moreover, non-interest spending falls below revenues by 2030, so a primary budget surplus (that is, a surplus excluding interest) emerges and grows each year through 2040. As a result, the debt ratio begins to decline in the late 2030s.

Pessimistic alternative. In our pessimistic alternative, we make two assumptions that cause the long-term debt trajectory to be more problematic:

- The ACA’s health cost control measures are not in effect after 2023. Thereafter, costs grow at the rate described in the alternative fiscal scenario in CBO’s June 2012 long-term budget outlook.

- Other non-interest spending (which excludes Social Security and mandatory health spending) grows with GDP after the ten-year budget window instead of growing with population and inflation (in which case it would decline modestly as a share of GDP).

| Table 3 Debt Ratios Under Alternative CBPP Scenarios | ||||

| Base case | Pessimistic | Optimistic | Trust fund solvency | |

| 2013 | 75% | 75% | 75% | 75% |

| 2015 | 76% | 76% | 75% | 76% |

| 2020 | 74% | 74% | 72% | 74% |

| 2023 | 78% | 78% | 74% | 78% |

| 2025 | 81% | 81% | 75% | 81% |

| 2030 | 88% | 93% | 79% | 87% |

| 2035 | 95% | 106% | 81% | 87% |

| 2040 | 99% | 120% | 80% | 80% |

| Source: CBPP calculations based on Congressional Budget Office and Social Security and Medicare Trustees data. | ||||

Combining these two negative assumptions, our pessimistic case projects the debt ratio to reach 120 percent of GDP by 2040.

Trust fund solvency alternative. In our trust fund solvency alternative, we assume that after the Hospital Insurance trust fund and the combined Old-Age, Survivors, and Disability Insurance (OASDI) trust funds are exhausted, Congress bring these programs’ revenues and spending into annual balance through tax increases or benefit cuts or a combination of the two.

These steps would reduce deficits by an amount equal to the projected HI and OASDI trust-fund shortfalls in each year after their respective trust-fund exhaustions. By 2040, addressing trust-fund solvency in this way results in substantially lower deficits and a debt-to-GDP ratio of 80 percent.

Appendix 2

Projecting Spending for Programs Other than Major Entitlements

As explained in Appendix 1, we assume that Social Security, Medicare, Medicaid, and other health entitlement programs will grow after 2023 at rates used by the Social Security and Medicare trustees and by CBO, respectively. The question is how to project the aggregate costs of all other spending programs (“other spending”) after 2023.

Other organizations sometimes assume that these programs will track GDP, which normally grows faster than prices and population; CBO adopted this assumption in its June 2012 extended baseline. CBO went further in its alternative fiscal scenario (AFS), which assumed that this category would grow rapidly for five years to return to its 1992-2011 average as a percentage of GDP and then stay there.

We believe that our approach makes more sense. To see why, let’s examine the actual patterns of such spending in 1976-2012 and the current projections through 2023.[28]

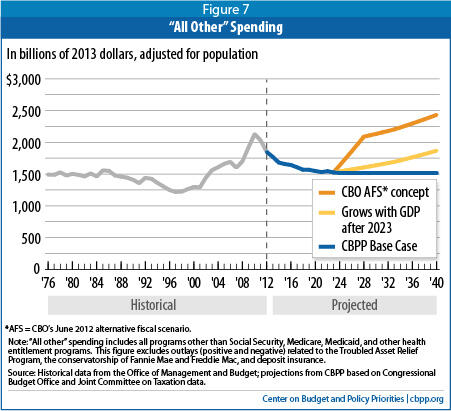

“Other spending” will total about $1.65 trillion in 2013. Adjusted for prices and population, that is only slightly higher than its average over the 1976-2012 period (see Figure 7). This category has already receded from its record levels in recent years, which were fueled by the Iraq and Afghanistan wars, the 2009 Recovery Act, and automatic increases in unemployment insurance and costs for certain anti-poverty programs such as SNAP during the very deep recession. Those factors are temporary. By 2019 through 2023 — the last half of the standard ten-year window for budget projections — this category (adjusted for prices and population) will be back at $1.5 trillion, identical to its average over the 1976-2012 period. We continue that level through 2040.

Mimicking the basic approach used in CBO’s AFS would cause annual outlays for these programs to shoot up to the equivalent of over $2.4 trillion, in today’s terms, in 2040.[29] Even assuming that this category tracks GDP, as CBO’s extended baseline does, would cause this category to rise to $1.9 trillion by 2040. In short, we conclude that the methods used by CBO and some other analysts imply a sharply rising, rather than constant, amount of “other spending” per person.

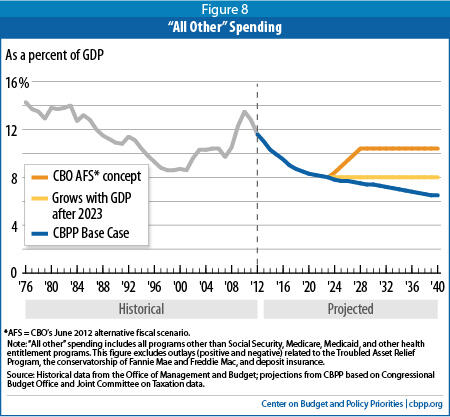

Our assumption that “other spending” will keep pace with prices and population translates into a gently declining path when expressed as a percentage of GDP (see Figure 8). The approach used in CBO’s AFS, by contrast, would have such spending rise quickly by over 2 percentage points of GDP and stay there. Although our approach differs from CBO’s, we think it is a more reasonable depiction of what “current policy” means for this category in the long run.

A few other points are also worth noting:

- We assume spending grows with both population growth and inflation. For discretionary programs (which make up over two-thirds of the “other spending” category), normal baseline methodology adjusts only for inflation. And while some discretionary programs — such as infrastructure, education grants, and law enforcement — clearly face rising demand from a growing population, others (such as defense, scientific and biomedical research, and the weather service) may not.

- Many mandatory programs in this category will shrink significantly as a percentage of GDP for decades to come. The single biggest set of mandatory programs in this category is federal retirement. Both the federal civilian and military workforces have declined for a half century as a share of the U.S. population. Furthermore, federal civilian employees hired after 1983 are not in the Civil Service Retirement System but in the less generous Federal Employees Retirement System; the older system will gradually wither. As a result, federal civilian and military retirement benefits will decline as a percentage of GDP for many decades. In fact, their actuaries project that spending for military retirement will grow no faster than prices and population, and that spending for civilian retirement will rise more slowly than that.[30] Similarly, the Social Security actuaries project that Supplemental Security Income (SSI), another program in this category, will gradually decline as a percentage of GDP through 2037.[31] In general, mandatory programs other than Social Security, Medicare, Medicaid, and health insurance premium credits do not face significant demographic or cost pressures over the long run.

- Historically, this category of spending has grown less rapidly than GDP and only barely faster than prices and population, as Figure 7 shows, even though a sizable number of new programs or major program increases were enacted since 1976.[32] Without new programs or major expansions, this category may naturally grow more slowly than we are projecting.

Writing for the Brookings Institution, William Gale and Alan Auerbach — who (unlike us) keep other spending constant as a share of GDP in their long-run projections — are nevertheless explicit that such an assumption reflects a change in policy: “Our forecast assumes that a richer society will want to spend more on discretionary spending, going beyond the current services provided by government.”[33] We, however, believe that for projections that are meant to serve as a neutral extension of current policy, a constant level of real spending per person is a better benchmark.

Although using historical averages as a percent of GDP to project “other spending” (as well as revenues) over the long run may seem to be a bland, technical choice, it unintentionally has harmful effects on the budget debate. Michael Linden of the Center for American Progress summarized this point in a recent report:

[J]ust as [CBO’s] long-term projections assumed unpaid-for tax cuts beginning 10 years out, they also assumed unpaid-for spending increases. It is no surprise that budget projections built on assumptions of future massive, but unspecified, deficit-increasing policies would show enormous amounts of debt. Those projections may be useful as a warning to future Congresses not to dramatically cut taxes and increase spending without paying for any of it, but they are not particularly useful for determining the fiscal outcome of our current budget path.[34]

Moreover, if revenues and “other spending” are fated to return to their historical averages, then Congress can do little to alter their projected long-run path. That puts the entire onus of deficit reduction on the remaining categories: Social Security, Medicare, Medicaid, and related programs. Our approach, in contrast, more accurately captures the future dynamics of the budget and allows policymakers to weigh the long-run effects of their proposals.

End Notes

[1] The authors acknowledge the extensive assistance of William Chen, Kelsey Merrick, and Joel Friedman.

[2] Kathy Ruffing, Kris Cox, and James Horney, The Right Target: Stabilize the Debt, Center on Budget and Policy Priorities, January 12, 2010, https://www.cbpp.org/cms/index.cfm?fa=view&id=3049.

[3] Committee for a Responsible Federal Budget, Our Debt Problems Are Still Far from Solved, May 15, 2013, Figure 4.

[4] Michael Linden, It’s Time to Hit the Reset Button on the Fiscal Debate, Center for American Progress, June 6, 2013, http://www.americanprogress.org/issues/budget/report/2013/06/06/65497/its-time-to-hit-the-reset-button-on-the-fiscal-debate/.

[5] Like our long-term baseline, the ten-year baseline that we and CRFB use assumes that sequestration will end after 2013 and the Medicare physician cuts will be cancelled, without offsets. However, that baseline assumes that the “tax extenders” either will expire as scheduled or that the costs of continuing these tax breaks will be offset.

[6] Congressional Budget Office, The Long-Term Budget Outlook, June 2012.

[7] Ruffing, Cox, and Horney.

[8] Chad Stone, From a Deficit to a Surplus and Back Again, U.S. News, April 25, 2013, http://www.usnews.com/opinion/blogs/economic-intelligence/2013/04/25/debt-economic-growth-relationship.

[9] International Monetary Fund, Concluding Statement of the 2013 Article IV Mission to The United States of America, June 14, 2013, http://www.imf.org/external/np/ms/2013/061413.htm.

[10] Richard Kogan, $1.5 Trillion in Deficit Savings Would Stabilize the Debt Over the Coming Decade, Center on Budget and Policy Priorities, February 11, 2013, https://www.cbpp.org/cms/index.cfm?fa=view&id=3900.

[11] Kogan, $1.5 Trillion in Deficit Savings Would Stabilize the Debt, p. 4.

[12] Based on the intermediate assumptions of the 2013 Social Security trustees’ report; see http://www.ssa.gov/OACT/TR/2013/lr5a2.html.

[13] See “Why Does Raising the Retirement Age Reduce Benefits?” in Kathy A. Ruffing and Paul N. Van de Water, Social Security Benefits are Modest, Center on Budget and Policy Priorities, January 11, 2011, https://www.cbpp.org/cms/?fa=view&id=3368.

[14] Our projections do, however, assume that legislators will avoid the deep reductions in physician payment rates — including a 25 percent cut in January 2014 — that would be required under Medicare’s “sustainable growth rate” (SGR) formula, and will instead freeze physician fees at today’s rates for the next ten years. Congress has routinely overridden the scheduled SGR cuts since 2003. See Appendix 1.

[15] The separate Disability Insurance trust fund is expected to be exhausted in 2016, the much larger Old-Age and Survivors Insurance fund in 2035. Combined, the two funds could pay full benefits until 2033.

[16] Social Security and Medicare Boards of Trustees, Status of the Social Security and Medicare Programs, A Summary of the 2013 Annual Reports, May 31, 2013.

[17] Robert Greenstein, President, Center on Budget and Policy Priorities, Testimony before the Senate Committee on Finance, February 26, 2013, https://www.cbpp.org/cms/?fa=view&id=3908, p. 6.

[18] 2013 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds; 2013 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds.

[19] CBO, The 2012 Long-Term Budget Outlook.

[20] Congressional Budget Office, Updated Budget Projections: Fiscal Years 2013 to 2023, May 2013.

[21] CBO, The Long-Term Budget Outlook, June 2012; Trustees Reports, May 2013.

[22] Congress has enacted numerous tax provisions — including the corporate research and experimentation tax credit, the deductibility of local and state taxes, and the deductibility of expenses for classroom teachers — as “temporary measures” scheduled to expire after one or two years but then regularly extended them.

[23] Like CBO, we assume that Social Security and Medicare will pay benefits even after their trust funds are exhausted. In their latest annual reports, the programs’ trustees project that the Medicare Hospital Insurance trust fund will be exhausted in 2026, and that the combined Old-Age, Survivors, and Disability Insurance trust funds — the formal name of Social Security — will be exhausted in 2033.

[24] Medicare Trustees, 2013 Annual Report, p. 209.

[25] CBO, The 2012 Long-Term Budget Outlook, p. 82. Variant 2 of CBO’s individual income tax projections is distinct from its “extended baseline” and “alternative fiscal scenario.”

[26] Edwin Park, Ensuring Effective Risk Adjustment, Center on Budget and Policy Priorities, May 18, 2011, https://www.cbpp.org/cms/?fa=view&id=3497.

[27] More precisely, we assume that discretionary spending will grow with prices and population after 2021, when the BCA’s discretionary caps expire, and that other mandatory programs will grow with prices and population after 2023, the last year for which CBO estimates the costs of each such program in its published baselines.

[28] We chose 1976 as a starting point because the Congressional Budget Act, with its new procedural constraints on program expansions, took effect in that year; the Vietnam War had ended; the 1973-1975 recession had ended; and the Johnson and Nixon Administrations — with their plethora of new programs and expansions — had ended.

[29] We mimic CBO’s approach by using the 1992-2012 average as a percent of GDP, since final 2012 data are now available.

[30] For historical information on federal employment, see http://www.opm.gov/policy-data-oversight/data-analysis-documentation/federal-employment-reports/historical-tables/total-government-employment-since-1962/ (and for a comparison to population, see Chart 10-1 in “Improving the Federal Workforce,” Analytical Perspectives, Budget of the U.S. Government, Fiscal Year 2014). For an analysis of the long-run outlooks for the civil service and military retirement trust funds, see Katelin P. Isaacs, Federal Employees’ Retirement System: Budget and Trust Fund Issues, Congressional Research Service, January 10, 2013, http://www.fas.org/sgp/crs/misc/RL30023.pdf and Military Retirement Fund, Audited Financial Report, November 6, 2012, http://comptroller.defense.gov/cfs/fy2012/13_Military_Retirement_Fund/Fiscal_Year_2012_Military_Retirement_Fund_Financial_Statements_and_Notes.pdf.

[31] Social Security Administration, Annual Report of the Supplemental Security Income Program, June 20, 2013, http://www.ssa.gov/OACT/ssir/SSI13/ssi2013.pdf.

[32] Examples of programs created or significantly expanded since 1976 include the EITC and Child Tax Credit (whose refundable portions count as spending), Pell Grants, special education for people with disabilities, the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC), child care assistance for low-income working families, mass transit capital and operating subsidies, renewable energy research and development, the Low Income Home Energy Assistance Program (LIHEAP), aviation security, the Webb veterans’ education program, the Universal Service Fund, and Build America Bonds. Against these many new programs or expansions is the elimination of the state and local revenue sharing program and the replacement of Aid to Families with Dependent Children with the Temporary Assistance for Needy Families block grant.

[33] Alan Auerbach and William Gale, Fiscal Fatigue: Tracking the Budget Outlook as Political Leaders Lurch from One Artificial Crisis to Another, February 28, 2013, http://www.brookings.edu/research/papers/2013/02/28-fiscal-fatigue-budget-outlook-gale.

[34] Michael Linden, It’s Time to Hit the Reset Button on the Fiscal Debate, Center for American Progress, June 6, 2013, http://www.americanprogress.org/issues/budget/report/2013/06/06/65497/its-time-to-hit-the-reset-button-on-the-fiscal-debate/.

More from the Authors

Areas of Expertise

Areas of Expertise