Health Proposals in President’s 2020 Budget Would Reduce Health Insurance Coverage and Access to Care

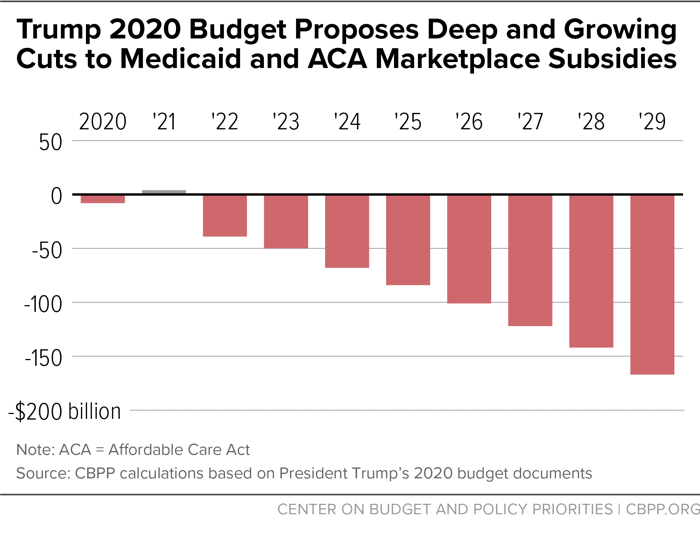

The health policies in the President’s fiscal year 2020 budget are a continuation of the Administration’s pursuit of deep cuts to core health care programs over the past two years.[1]The president’s budget reaffirms his support for an Affordable Care Act repeal plan that would cause millions of people to lose coverage.While the President is promising to enact health care legislation that would lower costs while protecting people with pre-existing conditions, his budget reaffirms his support for an Affordable Care Act (ACA) repeal plan that would cause millions of people to lose coverage, increase health care costs for millions more, end nationwide protections for people with pre-existing conditions, and cut Medicaid deeply. The budget also includes proposals designed to make it harder for low- and moderate-income people to enroll in or maintain Medicaid coverage — including taking Medicaid coverage away from people nationwide who don’t meet a work requirement — and proposals to cut premium tax credits and make it more difficult for people to maintain coverage in the ACA marketplaces. In total, the budget cuts Medicaid and ACA financial assistance by $777 billion over ten years, with the cuts growing steeply over time.

Repealing the Affordable Care Act and Overhauling Medicaid

The budget calls on Congress to enact legislation “modeled closely after” the ACA repeal-and-replace bill from Senators Bill Cassidy and Lindsey Graham, and then to cut coverage programs by hundreds of billions below the levels specified in that legislation over ten years.[2] (See Figure 1.) Specifically:

- The budget would eliminate the ACA’s Medicaid expansion, which has extended coverage to almost 13 million low-income adults, as well as its marketplace subsidies, which help about 9 million people afford coverage. The budget wipes out these programs and demands that states come up with alternatives. The result, according to the Congressional Budget Office (CBO), state insurance commissioners, and state Medicaid directors, would be massive disruption, given the scope of work, unrealistic timeline, and insufficient resources.[3]

-

The budget would replace the ACA’s major coverage expansions with a vastly inadequate block grant. After an initial increase, block grant funding levels would ultimately fall far below current-law funding for coverage programs, since the block grant would grow only with general inflation, with no adjustment for population growth or health care costs. Block grant funding also would not adjust from year to year for unexpected costs, leaving states on the hook for any and all such costs from recessions, natural disasters, public health emergencies, or prescription drug price spikes, making it even harder for states to use these funds to even partially replace ACA coverage programs.

In analyzing the Cassidy-Graham legislation, CBO concluded that its block grant would not enable states to establish coverage programs comparable to those in place under current law. Instead, states that did not expand Medicaid would use block grant funds in part to supplant state funding for existing programs, while Medicaid expansion states would struggle to maintain coverage for low-income adults and would generally not be able to replace the ACA subsidies that make marketplace coverage affordable for moderate-income consumers.[4] The block grant in the President’s budget provides hundreds of billions less in funding than the proposal CBO analyzed.

- The budget also would convert the rest of the Medicaid program, which covers seniors, people with disabilities, children, and pregnant women, to a per capita cap, limiting the amount of federal funding for each person enrolled in Medicaid regardless of need. The per capita cap amounts would increase only with general inflation, falling further and further below the cost of providing health care to vulnerable populations.

-

The Cassidy-Graham bill the budget endorses also gives states broad authority to eliminate or weaken many of the ACA’s protections for people with pre-existing conditions. Depending on how they used block grant dollars, states could permit insurers to charge higher premiums for people with pre-existing conditions or exclude key benefits from coverage for all individual market plans. As the CBO wrote in its preliminary analysis of the Cassidy-Graham plan, because the proposal would create such extreme disruption in insurance markets, states would face intense pressure to try to stabilize their markets by weakening these protections.

The budget claims to protect people with pre-existing conditions by requiring states to dedicate 10 percent of block grant funding to “high-cost” individuals. But virtually any use of block grant dollars would satisfy that requirement, simply because high-cost individuals account for most health care spending. Nothing in the budget prevents people with pre-existing conditions from being priced out of health care coverage.

These proposals would cause millions to lose coverage and millions more to have worse or less affordable coverage. Experts concluded that the Cassidy-Graham proposal for Medicaid and the ACA used as the framework for the budget would — in combination with the already enacted repeal of the individual mandate — likely lead to a total coverage loss of more than 20 million people, and the budget’s proposed cuts to coverage are much deeper.[5]

Additional Proposals Would Cut Medicaid and Marketplace Financial Assistance

ACA repeal and a Medicaid per capita cap are unlikely to be on the congressional agenda during 2019. But the Administration has moved forward with administrative actions that advance some of the same goals on a smaller scale — for example, Medicaid waivers that will make it harder for low-income adults to obtain and maintain coverage and actions that discourage marketplace enrollment and make marketplace plans more expensive.[6] Separate from its proposals to repeal the ACA, the budget puts forward a number of Medicaid and marketplace policies in that same spirit.

Proposed Medicaid Cuts Would Further Undermine Access to Care

Taking Medicaid Away From People Who Don’t Meet a Work Requirement

Expanding on the Trump Administration’s unprecedented approval of state work requirement policies, the President’s budget proposes to take coverage away from adults nationwide if they don’t meet a work requirement. In Arkansas, the first state to implement such a policy, almost 1 in 4 people subject to the work requirement lost their Medicaid coverage in the first seven months that it was in effect.[7]

The Administration estimates that the proposal would cut federal Medicaid spending by $130 billion over ten years. That would translate into about 1.7 million people losing Medicaid coverage starting in 2021, based on average federal Medicaid spending for an adult enrolled through the ACA’s Medicaid expansion. And the losses would likely be even higher: the Kaiser Family Foundation estimated that imposing Medicaid work requirements nationwide would cause 1.4 million to 4.0 million people to lose coverage, or between 6 and 17 percent of those subject to the work requirement.[8] If coverage loss rates were as high as in Arkansas, the number losing coverage would be even greater.

The vast majority of Medicaid beneficiaries are working or have significant barriers to work.[9] Taking coverage away from people who don’t meet a work requirement would cause many low-income adults to lose health coverage, including people who are working or can’t work due to mental illness, opioid or other substance use disorders, or serious chronic physical conditions, but who cannot overcome bureaucratic hurdles to document that they either meet work requirements or qualify for an exemption from them.

Moreover, Medicaid is a work support: access to health care makes it easier for many people with chronic health conditions such as diabetes or opioid use disorders to find work and keep their job. By proposing drastic cuts to Medicaid and taking coverage away from people who don’t meet a work requirement, the President’s budget would threaten access to care for millions of people and could make it harder for some of them to work.[10]

Increasing Red Tape for Medicaid Beneficiaries

The President’s budget includes language indicating that the Administration intends to undertake rulemaking to allow states to more frequently assess Medicaid beneficiaries’ eligibility. It estimates nearly $50 billion over ten years in savings from the intended regulatory change, indicating that it anticipates large coverage losses.

States are currently required to redetermine eligibility for most Medicaid beneficiaries at the end of a 12-month enrollment period. However, beneficiaries are required to report changes that may impact eligibility throughout the time they are covered under Medicaid, and states have the option to create systems and processes to check data sources periodically to see if beneficiaries remain eligible. If states find data that suggest consumers may no longer meet the eligibility requirements, they can request information from consumers and terminate coverage if they find a person no longer meets the eligibility requirements.

The Administration provides no evidence to support modifying the current regulations related to the frequency of Medicaid eligibility assessments. States already have flexibility to re-determine eligibility frequently based on information available through trusted third-party databases that they regularly use to inform all eligibility determinations, including renewals. Rather than the current policy that targets a subset of beneficiaries based on a data match finding of potential ineligibility, the proposal mentioned in the President’s budget would allow the state to require all beneficiaries complete an entire renewal process mid-enrollment year. Since renewals entail work for both the state staff and beneficiaries, requiring all beneficiaries to renew more than once yearly would be burdensome and significantly increase the chance that a beneficiary would miss a step, resulting in loss of coverage despite remaining eligible. For example, when Washington State increased frequency of renewals and created more related paperwork requirements, children’s enrollment in coverage programs plummeted. It rebounded once the state discontinued these burdensome processes.[11]

Requiring Documentation of Immigration Status Before Coverage Takes Effect

Many lawfully present immigrants, as well as all undocumented immigrants, are ineligible for Medicaid based on their immigration status, and states are required to verify that applicants are either citizens or have an eligible immigration status as part of determining eligibility for the program. States have tools to verify the citizenship or immigration status of the vast majority of applicants very quickly using data matching with other government agencies, but in some cases the process takes longer. In these cases, current law requires states to issue Medicaid benefits to people who have attested under penalty of perjury that they are citizens or have an eligible immigration status and who meet other eligibility factors such as income. This policy helps avoid what could otherwise be long delays while people obtain the documents they need and the state Medicaid agency processes them.

The budget proposes to eliminate this “reasonable opportunity” period and prohibit federal funding for Medicaid coverage until citizenship or immigration status has been verified. For some eligible people — including children, pregnant women, people with disabilities, and elderly individuals — this may result in significant delays in obtaining needed health care.

Ironically, past experience in Medicaid shows that U.S. citizens — rather than Medicaid-eligible immigrants — would likely experience the greatest harm.[12] Immigrants generally must have documents that prove their immigration status, so when data matching can’t immediately verify their status, they can more easily produce documents to satisfy the verification requirement. U.S. citizens are not required to carry documentation to prove their citizenship and often have a more difficult time producing documents like a birth certificate or record of birth abroad, and many U.S. citizens don’t have passports. Examples of U.S. citizens who may be delayed in getting Medicaid under this policy include:

- Newborns: obtaining a birth certificate can take up to six weeks, longer if parents do not apply for a Social Security number at the hospital (for example because they have not yet chosen a name).

- Adult citizen applicants born abroad, who are often not able to have their citizenship verified through data matching and may not have proof of citizenship readily available.

- People who have changed their names (such as people newly married).

- Anyone else who has an error in their Social Security record.

Allowing States to Reimpose Asset Tests

The budget would allow states to consider assets such as retirement savings accounts and some vehicles in determining Medicaid eligibility for children, parents, pregnant women, and other adults, undoing a major simplification achieved through the ACA, which eliminated these tests. Asset tests generally had little impact on Medicaid eligibility: most people with incomes below the Medicaid limit don’t have significant assets, so few people were found ineligible for Medicaid based on assets. But asset tests have a number of serious downsides.

First, having to document assets increases paperwork, deters some eligible people from applying for Medicaid, and leads to delays or even denials of coverage for eligible people — not because they have substantial assets but because they fail to provide all the paperwork proving they don’t.

Second and related, asset tests increase administrative costs and burdens for states. Even before the ACA, many states dropped asset tests because they were costly to implement and so few people were found to have assets over the limit.[13]

Third, imposing asset tests would have the perverse effect of making some very low-income people ineligible for both Medicaid and marketplace premium tax credits, the problem the ACA intended to avoid by eliminating asset tests. With an asset test, some people could be ineligible for Medicaid because their assets are above the state’s limit, but ineligible for premium tax credits because their income is too low.

Finally, asset tests can discourage low-income people from accumulating even modest savings (in some states, as little as $1,000) and punish them severely if they do.[14] Asset tests would be especially harmful for people who have contributed to retirement accounts but temporarily fall on hard times. These individuals would be forced to spend down their savings and incur associated penalties and fees in order to gain Medicaid eligibility for what may be a short window of time.

Making It Harder for Seniors and People With Disabilities to Qualify for Help

The President’s budget proposes to eliminate states’ existing flexibility to increase the amount of home equity seniors and people with disabilities may hold without losing eligibility for Medicaid. Current federal guidelines set a range: $585,000 to $878,000 in 2019.[15] A state using the minimum level, for example, would count home value exceeding $585,000 as an asset for purposes of determining Medicaid eligibility.[16] But a number of states, many of them states with higher-than-average home values, take advantage of the existing flexibility to set higher limits: California, Connecticut, the District of Columbia, Hawaii, Idaho, Maine, Massachusetts, New Jersey, New Mexico, New York, and Wisconsin.[17]

The President’s budget would require all states to use the lower $585,000 minimum home equity limit.[18] This change would make it harder for seniors and people with disabilities in states whose home value limit exceeds that minimum amount to qualify for Medicaid. It could force people in these states to sell their homes and cause a delay in their care until their house is sold.

Discouraging Medicaid Enrollees From Accessing Care

Under existing Medicaid state plan authority, states have considerable flexibility to establish cost-sharing amounts for beneficiaries, including imposing a maximum $8 co-payment for non-emergency use of the emergency department (ED). But to impose a co-payment that exceeds this $8 maximum, states need to obtain a special waiver under section 1916(f) of the Social Security Act. Only one state, Indiana, has ever received approval for such a waiver, which gave it the authority to impose a $25 co-payment for non-emergency use of the ED after a beneficiary’s first visit.

The President’s budget proposes to allow states to amend their Medicaid state plans and impose higher co-payments for non-emergency use of the ED. The Trump Administration claims that this will “encourage personal financial responsibility and proper use of health care resources.” But this hypothesis has already been tested in Indiana and turns out to be false. Indiana’s evaluation of its graduated co-payment shows no difference in use of the ED for non-emergency visits between Medicaid beneficiaries with an $8 co-payment and those with a $25 co-payment.[19] An earlier study also found that co-pays for non-emergency use of the ED didn’t change beneficiaries’ use of the ED or primary care.[20] In light of that evidence, there is no justification for weakening beneficiary protections and imposing co-payments that may deter appropriate use of the ED.

Allowing States to Drop Coverage of Non-Emergency Medical Transportation Benefit

One important benefit provided by Medicaid coverage is transportation to health care appointments, referred to as non-emergency medical transportation (NEMT). Studies find that lack of transportation is an important obstacle to getting needed care for low-income people, especially for elderly people and those with disabilities or chronic conditions.[21] In 2015, Medicaid NEMT was most commonly used to access behavioral health care and was also frequently used to access dialysis and preventive care.[22]

The President’s budget outlines the Administration’s plan to take regulatory action to make Medicaid’s NEMT benefit optional, despite evidence that eliminating NEMT worsens access to care.[23] To date, the federal Centers for Medicare & Medicaid Services (CMS) has granted waivers of NEMT for non-disabled adults to three states — Indiana, Iowa, and Kentucky. A 2016 evaluation[24] of Indiana’s waiver found that beneficiaries without access to NEMT were more likely to list transportation difficulties as a reason for missing an appointment than beneficiaries with access to the benefit. In addition, among beneficiaries without the NEMT benefit who missed an appointment, the proportion who identified transportation as a reason was nearly double among those with incomes below the poverty line compared to those with incomes above the poverty line.

Medicaid Formulary Pilot

The budget proposes to allow up to five states to limit access to prescription drugs in their Medicaid programs. This proposal risks causing harm to vulnerable Medicaid enrollees and would likely have a limited effect on Medicaid drug costs.

Under current law, CMS does not have the authority to allow states to refuse to cover specific drugs, an approach known as a closed drug formulary. Medicaid law requires states that include prescription drug coverage in their Medicaid programs — which all states do — to cover all FDA-approved drugs (with limited exceptions, defined in the law). However, states do have tools that allow them to negotiate better deals with drug manufacturers and to limit enrollees’ access to specialized, high-cost drugs in order to ensure they are used efficiently. They can require prior authorization in order to get a specialized medication or require Medicaid beneficiaries to try a lower-cost drug within a class before getting a high-cost one.

In return for covering all prescription drugs, Medicaid requires drug companies to provide substantial rebates, giving states a much lower price than typically offered to commercial health plans. These provisions of law — requiring coverage of all FDA-approved products and requiring drug manufacturers to provide states with rebates — reflect a carefully negotiated legislative compromise that has led to significant cost savings for state Medicaid agencies: the rebates allow the federal government and the states to achieve savings of about 50 percent, according to analysis from the HHS Office of Inspector General.[25]

The President’s budget proposes to change the law to give CMS authority to pilot closed formularies in up to five states, estimating that the pilots will save the federal government $410 million over a ten-year period. The goal of the proposal is to give the pilot states “more flexibility” in negotiating prices with manufacturers, “rather than participating… in the Medicaid Drug Rebate Program.” However, states already negotiate drug prices with drug companies today (in addition to participating in the federal rebate program). As noted, they are already able to give certain drugs preferred status in order to negotiate better deals. It’s unlikely that states could achieve substantially more in savings than they currently receive through the combination of the federal rebate program and supplemental rebates — and some may save significantly less.

Meanwhile, creating a closed formulary could prevent some Medicaid beneficiaries from getting the medications they need. While the proposal does include an appeals process to protect Medicaid beneficiaries’ access, this structure would impose a considerable burden on beneficiaries who need drugs that are not covered, which would very likely lead to some people going without needed care. Medicaid beneficiaries tend to be more frail than the general population, and barriers such as lengthy appeals processes could significantly reduce access to needed care.

Perhaps in recognition of these risks, the President’s budget does structure this proposal as a pilot program and requires a rigorous evaluation, which is critical when considering any new policy with the potential to harm beneficiaries. However, in this case, the likelihood of harm and the risk of disrupting the rebate program make this policy a poor candidate for a demonstration. Moreover, an evaluation might not capture the full effects of this proposal. In particular, a limited pilot program likely cannot evaluate the risk that closed formularies would undermine the drug rebate program. If that occurred, it could significantly increase Medicaid drug costs for states and the federal government over time.

In addition to the pilot program, the President’s budget also calls for several proposals that would close loopholes or reduce the cost of drugs in Medicaid. For example, the budget calls for lifting the cap on Medicaid prescription drug rebates from manufacturers. Currently, manufacturer rebates are capped at 100 percent of the average manufacturer price for the drug. By removing the cap, this proposal would require prescription drug manufacturers to pay higher rebates on drugs when the list price for the drug exceeds the rate of inflation, which would better protect states and the federal government from extremely high-cost drugs. The Medicaid and CHIP Payment and Access Commission reports that CBO estimates that this proposal would save $15-20 billion over ten years.[26]

Proposals Would Impede Access to Marketplace Coverage

Increasing Premiums for Many Low- and Moderate-Income Marketplace Enrollees

The Administration’s budget proposal would require all marketplace enrollees to pay out of pocket toward the cost of their health plans, even if they otherwise can enroll in zero-premium plans after accounting for premium tax credits.[27] Based on other estimates from the Administration, this would mean reducing tax credits and increasing premiums for about 1.6 million low- and moderate-income consumers.[28]

Part of the reason many people have access to zero-premium plans is an inadvertent consequence of the Trump Administration’s attempt to sabotage the ACA by ending reimbursement to insurers for the cost-sharing reductions (CSRs) they are required to provide lower-income consumers. Ending CSR reimbursements gave rise to “silver loading,” in which insurers build the cost of CSRs into marketplace silver plan premiums. Because premium tax credits are based on silver plan premiums, that approach effectively makes financial assistance more generous. Silver loading is reducing the number of uninsured by 500,000 to 1 million, CBO estimates.[29]

More generous financial assistance means the tax credit can cover the full premium of a low-cost plan for more consumers. For example, a 40-year-old with an income of $20,000 can enroll in the lowest-cost bronze marketplace plan with no net premium in most counties, according to the Kaiser Family Foundation.[30] In some counties, zero-premium bronze plans are available for people with somewhat higher incomes, and lower-deductible silver or gold premiums may also be available at zero net premium for low-income people.

The Administration’s argument for its proposal is that requiring everyone to pay a premium toward health insurance would increase “personal responsibility” — effectively, that health care is currently too affordable for low- and moderate-income consumers. But a zero-premium plan doesn’t mean the coverage is free. Zero-premium plans often have high deductibles and other out-of-pocket costs, although they still protect people against catastrophic costs and offer access to preventive care without cost sharing (and often to primary care and generic drugs with no or low cost sharing as well). Moreover, the enrollee is responsible for reconciling their tax credit and repaying any advance credit they weren’t entitled to receive.

Enrolling more of the estimated 4.2 million uninsured people with access to zero-premium plans[31] is a concept that has gained traction across the political spectrum. In 2018, Maryland legislators introduced a bill to automatically enroll eligible uninsured people in zero-premium plans, and scholars from the American Enterprise Institute have embraced a similar concept.[32] In addition to its direct effects on consumers, eliminating zero-premium plans would stymie these ideas.

Shortening Grace Periods That Help Marketplace Enrollees Stay Covered

Under current law, marketplace consumers who receive premium tax credits have three months to pay overdue premiums before insurers can end their coverage. The President’s budget proposes reducing the premium payment grace period from three months to one month, meaning people who fall behind on their marketplace premiums would lose coverage more quickly and might remain uninsured until the next enrollment period.[33]

As CBO explained in scoring a similar provision, the proposal’s savings would come not from those whose coverage is terminated due to their failure to pay their premiums, but rather from lost premium tax credits for people “who would have paid their delinquent premiums during the second or third month of their grace period [but] would instead have their coverage terminated.”[34] That’s because people who fail to pay premiums within 90 days already lose coverage and financial assistance for the second and third months of the grace period (the federal government doesn’t pay their premium tax credits, and insurers don’t have to pay their claims). The savings from the proposal would come from taking coverage and financial assistance away from people who would catch up on premiums within 90 days but can’t in just 30.

Based on state data on grace period use, we estimated that a similar congressional proposal would cause between 259,000 and 688,000 people per year to lose coverage.[35]

End Notes

[1] “A Budget for A Better America,” https://www.whitehouse.gov/wp-content/uploads/2019/03/budget-fy2020.pdf, and “FY 2020 President’s Budget for HHS,” https://www.hhs.gov/sites/default/files/fy-2020-budget-in-brief.pdf.

[2] For a discussion of the Cassidy-Graham legislation, see Jacob Leibenluft, Aviva Aron-Dine, and Edwin Park, “Revised Version of Cassidy-Graham Proposal Is More of the Same,” Center on Budget and Policy Priorities, September 25, 2017, https://www.cbpp.org/research/health/revised-version-of-cassidy-graham-proposal-is-more-of-the-same.

[3] See “Preliminary Analysis of Legislation That Would Replace Subsidies for Health Care with Block Grants,” Congressional Budget Office, September 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/53126-health.pdf; letter from current and former state insurance commissioners, September 25, 2017, http://www.insurance.ca.gov/0400-news/0100-press-releases/2017/upload/nr095-2017Cassidy-GrahamLtr.pdf; National Association of Medicaid Directors, “NAMD Statement on Graham-Cassidy,” September 21, 2017, http://medicaiddirectors.org/wp-content/uploads/2017/09/NAMD-Statement-on-Graham-Cassidy9_21_17.pdf.

[4] “Preliminary Analysis of Legislation That Would Replace Subsidies for Health Care with Block Grants,” Congressional Budget Office, September 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/53126-health.pdf.

[5] Matthew Fiedler and Loren Adler, “How will the Graham-Cassidy proposal affect the number of people with health insurance coverage?” Brookings Institution, September 22, 2017, https://www.brookings.edu/research/how-will-the-graham-cassidy-proposal-affect-the-number-of-people-with-health-insurance-coverage/.

[6] See Center on Budget and Policy Priorities, “Sabotage Watch: Tracking Efforts to Undermine the ACA,” https://www.cbpp.org/sabotage-watch-tracking-efforts-to-undermine-the-aca.

[7] On March 27, 2019, a district court vacated the Department of Health and Human Services’ (HHS) approval of Medicaid waivers in Arkansas and Kentucky that included work requirements. See also Jennifer Wagner, “Commentary: As Predicted, Arkansas’ Medicaid Waiver Is Taking Coverage Away From Eligible People,” Center on Budget and Policy Priorities, updated March 12, 2019, https://www.cbpp.org/health/commentary-as-predicted-arkansas-medicaid-waiver-is-taking-coverage-away-from-eligible-people.

[8] Rachel Garfield, Robin Rudowitz, and MaryBeth Musumeci, “Implications of a Medicaid Work Requirement: National Estimates of Potential Coverage Losses,” Kaiser Family Foundation, June 27, 2018, https://www.kff.org/medicaid/issue-brief/implications-of-a-medicaid-work-requirement-national-estimates-of-potential-coverage-losses/.

[9] Hannah Katch, Jennifer Wagner, and Aviva Aron-Dine, “Taking Medicaid Coverage Away From People Not Meeting Work Requirements Will Reduce Low-Income Families’ Access to Care and Worsen Health Outcomes,” Center on Budget and Policy Priorities, August 13, 2018, https://www.cbpp.org/research/health/taking-medicaid-coverage-away-from-people-not-meeting-work-requirements-will-reduce.

[10] Ibid.

[11] Laura Summer and Cindy Mann, “Instability of Public Health Insurance Coverage for Children and Their Families: Causes, Consequences, and Remedies,” Commonwealth Fund, June 2006, https://ccf.georgetown.edu/wp-content/uploads/2012/03/Uninsured_instability_pub_health_ins_children.pdf

[12] Donna Cohen Ross, “New Medicaid Citizenship Documentation Requirement Is Taking a Toll: States Report Enrollment Is Down and Administrative Costs Are Up,” Center on Budget and Policy Priorities, March 13, 2007, https://www.cbpp.org/research/new-medicaid-citizenship-documentation-requirement-is-taking-a-toll-states-report

[13] Vernon Smith, “Eliminating the Medicaid Asset Test for Families: A Review of State Experiences,” Kaiser Family Foundation, April 2001, https://kaiserfamilyfoundation.files.wordpress.com/2001/04/2239-eliminating-the-medicaid-asset-test.pdf.

[14] Kelly Isom, “Barriers to Savings: Asset Tests,” Bipartisan Policy Center, March 13, 2015, https://bipartisanpolicy.org/blog/barriers-to-savings-asset-tests/.

[15] Centers for Medicare & Medicaid Services, “2018 SSI and Spousal Impoverishment Standards,” https://www.medicaid.gov/federal-policy-guidance/downloads/cib120517.pdf.

[16] If an individual’s spouse or child under age 21 lives in the home, the home is not counted as an asset for purposes of determining Medicaid eligibility.

[17] Molly O’Malley Watts, Elizabeth Cornachione, and MaryBeth Musumeci, “Medicaid Financial Eligibility for Seniors and People with Disabilities in 2015,” March 2016, http://files.kff.org/attachment/report-medicaid-financial-eligibility-for-seniors-and-people-with-disabilities-in-2015.

[18] This limit would continue to be adjusted on an annual basis using the CPI-U.

[19] Lewin Group, “Healthy Indiana Plan 2.0: 2016 Emergency Room Co-Payment Assessment,” October 4, 2017, https://www.medicaid.gov/Medicaid-CHIP-Program-Information/By-Topics/Waivers/1115/downloads/in/Healthy-Indiana-Plan-2/in-healthy-indiana-plan-support-20-2016-emrgncy-room-copymt-assessment-rpt-10042017.pdf.

[20] Mona Siddiqui, Eric T. Roberts, and Craig E. Pollack, “The Effect of Emergency Department Co-payments for Medicaid Beneficiaries Following the Deficit Reduction Act of 2005,” JAMA Internal Medicine, January 26, 2015.

[21] MaryBeth Musumeci and Robin Rudowitz, “Medicaid Non-Emergency Medical Transportation: Overview and Key Issues in Medicaid Expansion Waivers,” Kaiser Family Foundation, February 24, 2016, https://www.kff.org/medicaid/issue-brief/medicaid-non-emergency-medical-transportation-overview-and-key-issues-in-medicaid-expansion-waivers/.

[22] Ibid.

[23] The President’s budget is unclear whether it intends to give states the option to not offer the NEMT benefit to non-elderly non-disabled adults only (as with the three states with waivers), or whether the benefit would be optional for all Medicaid beneficiaries, including children and people with disabilities.

[24] Lewin Group, “Indiana HIP 2.0: Evaluation of Non-Emergency Medical Transportation (NEMT) Waiver,” November 2, 2016, https://www.medicaid.gov/Medicaid-CHIP-Program-Information/By-Topics/Waivers/1115/downloads/in/Healthy-Indiana-Plan-2/in-healthy-indiana-plan-support-20-nemt-final-evl-rpt-11022016.pdf.

[25] Office of Inspector General, Department of Health and Human Services, “Medicaid Rebates for Brand-Name Drugs Exceeded Part D Rebates by a Substantial Margin,” April 2015, https://oig.hhs.gov/oei/reports/oei-03-13-00650.pdf.

[26] Medicaid and CHIP Payment and Access Commission, March 2019 meeting transcript, https://www.macpac.gov/wp-content/uploads/2018/03/March-2019-Meeting-Transcript.pdf.

[27] In 2020 and 2021 — before the President’s proposed ACA repeal would take effect — the provision would reduce spending by $345 million, in all.

[28] The most recent CMS data show 10.3 million people enrolled in marketplace coverage; in the 2020 Notice of Benefit and Payment Parameters, the Administration estimates that 16 percent of people enrolled in marketplace coverage have zero net premium. Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment, January 17, 2019, https://s3.amazonaws.com/public-inspection.federalregister.gov/2019-00077.pdf.

[29] Congressional Budget Office, “Appropriation of Cost-Sharing Reduction Subsidies,” March 19, 2018, https://www.cbo.gov/publication/53664.

[30] Rachel Fehr et al., “How ACA Marketplace Premiums Are Changing by County in 2019,” Kaiser Family Foundation, November 20, 2018, https://www.kff.org/health-costs/issue-brief/how-aca-marketplace-premiums-are-changing-by-county-in-2019/.

[31] Rachel Fehr et al., “How Many of the Uninsured Can Purchase a Marketplace Plan for Free?” Kaiser Family Foundation, December 11, 2018, https://www.kff.org/health-reform/issue-brief/how-many-of-the-uninsured-can-purchase-a-marketplace-plan-for-free/.

[32] Stan Dorn, James C. Capretta, and Lanhee J. Chen, “Making Health Insurance Enrollment As Automatic As Possible (Part 2),” Health Affairs Blog, May 3, 2018, https://www.healthaffairs.org/do/10.1377/hblog20180501.219130/full/.

[33] In 2020 and 2021 — before the President’s proposed ACA repeal would take effect — the provision reduces spending by a total of $78 million. CBO scored a similar provision as saving $4.9 billion over ten years.

[34] Congressional Budget Office, “Cost Estimate: H.R. 3922, CHAMPION Act of 2017,” October 19, 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/hr3922.pdf.

[35] Tara Straw, “Up to 688,000 Would Lose Insurance Under House Bill,” Center on Budget and Policy Priorities, October 31, 2017, https://www.cbpp.org/blog/up-to-688000-would-lose-insurance-under-house-bill.

More from the Authors

Areas of Expertise

Areas of Expertise

Areas of Expertise

Areas of Expertise