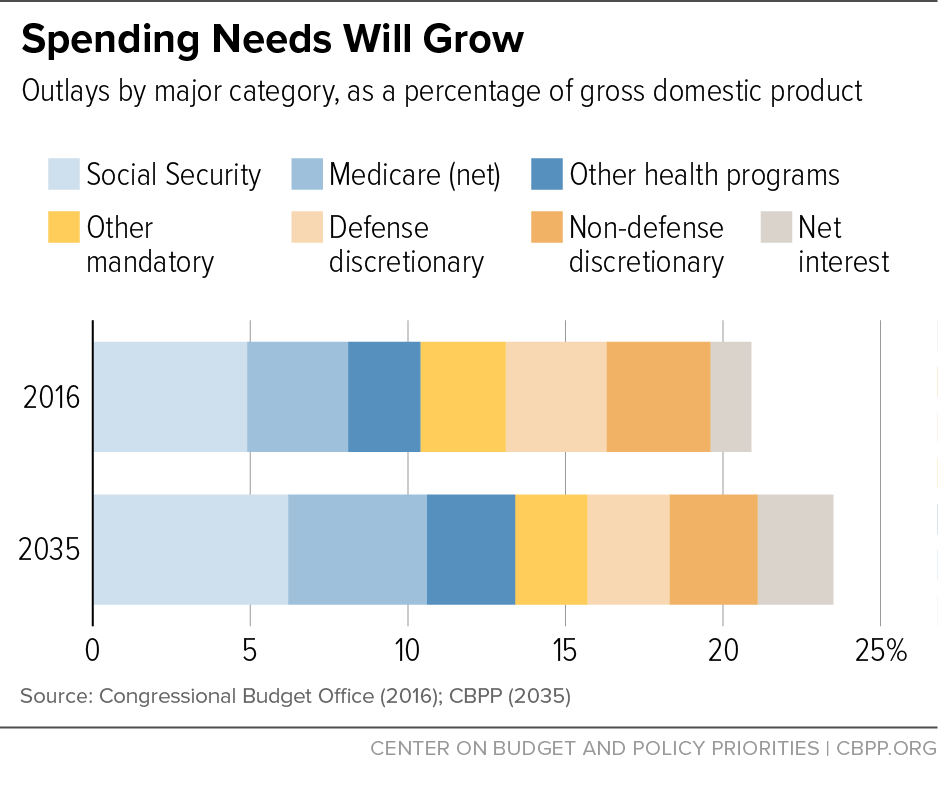

Although some policymakers seek to prevent the federal government from growing, or to shrink it, federal spending and taxes will have to grow significantly as a share of the economy in the coming decades. This is not a statement of political values; it’s a reflection of basic realities — the aging of America’s population, health care costs that rise faster than the economy grows (especially as medical advances continue), potential national security threats, and current and emerging domestic challenges such as large infrastructure needs that cannot be deferred indefinitely. Those factors, we estimate, will boost federal spending by about 2½ percent of gross domestic product (GDP) between now and 2035 — from 20.9 percent in 2016 to an estimated 23.5 percent in 2035 (see Figure 1). Revenues will need to rise at least as much to prevent the debt-to-GDP ratio from growing.

whether historical averages were ever appropriate fiscal benchmarks, they cannot be in the future.Since 1976, federal spending has averaged 20.5 percent of GDP, although its composition has changed substantially (see Box 1), while federal revenue has averaged 17.4 percent of GDP. Some policymakers have said these historical averages should serve as ceilings for fiscal policy for coming decades, and some have proposed constitutional or legal limits on spending or taxes at or below these averages.[1] But whether historical averages were ever appropriate fiscal benchmarks, they cannot be in the future due to these inescapable realities. And as spending grows, so too must revenue to finance it.

To reach our 23.5 percent of GDP by 2035, we estimate (as explained in the body of this analysis) that Social Security spending will rise from today’s 4.9 percent of GDP to 6.2 percent; Medicare, Medicaid, and other major health programs will rise from today’s 5.5 percent to 7.2 percent; interest on the national debt will rise from 1.3 percent to 2.4 percent; and other categories of spending will shrink slightly. To finance the overall increase in spending, revenues will have to grow from 17.8 percent of GDP in 2016 to at least 20.5 percent in 2035. At that point, the nation’s demographic shift will be largely complete — the entire baby-boom generation will have reached retirement age — and the pressures on the budget will abate. These projections are based on the Center on Budget and Policy Priorities’ long-run budget baseline, with certain policy and other adjustments specified below.[2]

To understand why government will have to grow, one must first recognize that federal spending is dominated by a handful of big-ticket items, and it’s primarily those items that will fuel the growth of federal spending overall. Those items, in turn, reflect longstanding public values and preferences about what the federal government should do at home and abroad. If those values and preferences extend into the future, then government spending and revenue will have to grow as a share of GDP to reflect them.

Specifically, Social Security amounts to nearly 5 percent of GDP today, while major health programs (primarily Medicare and Medicaid) amount to another 5.5 percent. The aging of America is making millions more people eligible for Social Security, which will rise in cost from 4.9 percent of GDP today to 6.2 percent by 2035. The aging of America also will make millions more people eligible for Medicare and Medicaid, which — combined with rising health care costs — will drive up health spending as a share of GDP from today’s 5.5 percent to 7.2 percent by 2035. Of particular note, the population of “old-old” Americans — those 85 and older — is growing very rapidly and, not surprisingly, they have much higher health care costs than the elderly in general.

Defense spending accounts for another 3.2 percent of GDP and, in recent decades, it has shrunk substantially as a share of GDP. Today, new threats to U.S. national security are emerging from terrorist groups as well as some nation-states. Many analysts argue that defense spending needs to grow faster than inflation for several years after half a dozen years of reductions. Our estimates assume that defense outlays will remain at or above 3.0 percent of GDP through 2021 and will decline gradually to 2.6 percent of GDP in 2035, although actual outlays could be higher if security challenges necessitate more funding.

Non-defense discretionary spending, which totals 3.3 percent of GDP, has borne the brunt of deficit-cutting efforts of recent years, along with defense. This category funds everything from law enforcement and homeland security, to education and research, to public health and veterans’ medical care, to parks and environmental protection. Rather than cut further, policymakers may need to change course due to such factors as: an aging infrastructure of roads and bridges that need serious repair (and whose deficiencies are hurting U.S. productivity); inadequate scientific and medical research, which could slow the pace of scientific discovery; deteriorating customer service at the Social Security Administration and the IRS; rising costs of health care and other services for veterans of America’s wars dating back to Vietnam; and needs for greater investment in areas such as child care. Our estimate assumes that this category of spending will remain roughly constant as a percentage of GDP for several years and decline to 2.8 percent of GDP in 2035.

While addressing the nation’s domestic and foreign challenges, policymakers should take steps in the coming years to restore its long-term fiscal health so that the debt doesn’t rise continually as a share of the economy (other than during periods when the economy is weak). Along with raising revenue and slowing the growth of health care costs, policymakers should find budget savings wherever they can by setting priorities, scrapping duplicative or outdated programs, investing in programs that work based on evidence, relying more on technology to achieve efficiencies and boost productivity, improving purchasing practices, and reducing errors and overpayments in federal programs. But while the major areas of federal spending discussed above will either grow or shrink only modestly as a share of GDP in the coming years, there are limits to how much policymakers can cut the rest of the budget, which includes net interest and key safety-net programs.

Box 1: Historical Trends in Federal Spending

Total federal spending has typically run about 20 to 21 percent of gross domestic product (GDP) in recent decades and is now just slightly above its 40-year average. It climbed above the average during both the years of Ronald Reagan’s presidency (marked by a deep recession in the early 1980s and a large defense build-up) and the Great Recession and its aftermath, but has since receded. In 2016, total federal spending amounted to 20.9 percent of GDP.

| Composition of Federal Spending as a Percentage of GDP, 1976-2016 | |||||

|---|---|---|---|---|---|

| Fiscal Year | 1976 | 1986 | 1996 | 2006 | 2016 |

| Social Security | 4.1 | 4.3 | 4.4 | 4.0 | 4.9 |

| Medicare (net) | 0.8 | 1.5 | 2.1 | 2.4 | 3.2 |

| Other major health programsa | 0.5 | 0.6 | 1.2 | 1.4 | 2.3 |

| Other mandatory programs | 4.1 | 2.8 | 2.2 | 2.6 | 2.7 |

| Defense discretionary | 5.0 | 6.0 | 3.3 | 3.8 | 3.2 |

| Non-defense discretionary | 4.8 | 3.6 | 3.3 | 3.6 | 3.3 |

| Net interest | 1.5 | 3.0 | 3.0 | 1.7 | 1.3 |

| Total | 20.8 | 21.8 | 19.6 | 19.4 | 20.9 |

Because of inflation and real economic growth, dollar numbers are hard to compare over long spans of time. Accordingly, in this paper, we put spending and revenues from different years in comparable terms by expressing them in relation to the size of the economy — that is, compared to GDP. Looking at spending and revenues as percentages of GDP is the standard measure that economists and budget analysts use to examine fiscal trends over time, make cross-national comparisons, and assess what a nation can afford.

Although the total level of federal spending in relation to the size of the economy is about the same today as it was four decades ago, the composition of federal spending has changed considerably. Social Security, Medicare, and other major health programs (primarily Medicaid) have each grown substantially as percentages of GDP. In total, those three program areas accounted for a quarter of federal spending in 1976 and close to half by 2016. Conversely, non-defense discretionary, defense, and other non-interest mandatory spending have all been on generally declining paths in relation to GDP. Net interest spending represents about the same percentage of GDP today as it did in 1976 but has reached substantially higher levels in some intervening years.

For starters, the federal government must pay interest on the debt, which now totals 1.3 percent of GDP but almost surely will rise. Although the debt has grown substantially in recent years, interest payments on it haven’t grown commensurately because, with moderate economic growth and little inflation, interest rates have remained at historically low levels. With unemployment falling, the Federal Reserve has begun to boost interest rates, which will increase the cost of interest payments. We estimate that net interest costs will reach 2.4 percent of GDP by 2035.

In addition, a sizeable share of the rest of federal spending consists of safety-net programs, such as SNAP (food stamps), Supplemental Security Income, unemployment insurance, and the refundable parts of the Earned Income Tax Credit and Child Tax Credit. These programs provide vital support for millions of struggling Americans, including the large population of working-poor and near-poor families. Moreover, with income inequality growing, policymakers should adhere to the principle, established by the Bowles-Simpson fiscal commission, that deficit-cutting efforts should not increase poverty or inequality. We estimate that, under current policies, this category of other mandatory spending will grow less rapidly than the economy, shrinking from 2.8 percent to 2.3 percent of GDP between now and 2035.

Box 2: Budget Plans Illustrate Need for Higher Spending and Revenues

Various bipartisan or conservative budget plans have recognized that federal spending and revenues will need to increase in relation to the size of the economy in future years.

National Academy of Sciences: The Committee on the Fiscal Future, a joint, bipartisan effort of the National Academy of Sciences and the National Academy of Public Administration, developed four budget paths to illustrate the range of policy choices for federal spending and revenues that would put the budget on a sustainable long-term path. One option was a low-spending path that eschewed revenue increases and accomplished its deficit reduction by making deep cuts in all program categories. At the other end of the spectrum was a path that accomplished most of its deficit reduction by raising taxes. Committee co-chair Rudolph Penner, a former CBO director (and moderate Republican), described both the low-spending and high-spending paths as “extreme.” Between these two extreme paths, the committee outlined two intermediate scenarios that blended substantial budget cuts and substantial revenue increases. Under the intermediate paths, federal spending and revenues would both significantly exceed recent average levels as percentages of GDP.a

Bipartisan Policy Center: Former CBO and OMB Director Alice Rivlin (a Democrat) and former Senate Budget Committee Chairman Pete Domenici (a Republican) chaired a task force of the Bipartisan Policy Center (BPC) that developed a budget plan. It proposed major program changes to reduce spending well below what it would be if policies remained unchanged but also acknowledged that total federal spending will have to surpass its historical average in the decades ahead, requiring significant revenue increases. Under an updated version of the Domenici-Rivlin plan that BPC issued in 2015, total spending would equal 22.5 percent of GDP in 2026 and 24.3 percent in 2040; revenues would equal 19.4 percent of GDP in 2026 and 21.3 percent in 2040.b

American Enterprise Institute: Four scholars at the American Enterprise Institute, a conservative think tank, released what they described as a plan “to achieve long-term fiscal sustainability and promote economic growth.” Even with significant cuts in Social Security, Medicare, and Medicaid, spending in the plan would reach more than 22 percent of GDP and revenues 21 percent of GDP by 2040.c

a National Research Council and National Academy of Public Administration, Choosing the Nation’s Fiscal Future (Washington: National Academies Press, 2010); Rudolph G. Penner, Statement before the Senate Budget Committee, February 11, 2010.

b Bipartisan Policy Center, A Bipartisan Approach to America’s Fiscal Future, May 2015. Because these projections are two years old, they are not strictly comparable to the estimates presented elsewhere in this paper.

c Joseph Antos, Andrew Biggs, Alex Brill, and Alan Viard, A Balanced Plan for Fiscal Stability and Economic Growth, American Enterprise Institute, May 2015.

That total federal spending and revenue will have to rise as a percentage of GDP is hardly a controversial notion. Budget plans from such diverse organizations as the National Academy of Sciences, the Bipartisan Policy Center, and the American Enterprise Institute have reached the same conclusion, finding that federal spending and revenues will have to rise and exceed their historical averages in coming decades even if policymakers make significant budget cuts. (See Box 2.)

In the pages that follow, we look more closely at:

- The aging of America, and its implications for Social Security, Medicare, and Medicaid;

- Rising health care costs, and their implications for health programs;

- Security challenges, and their implications for defense spending;

- Existing and emerging domestic needs, and their implications for non-defense discretionary spending;

- Interest costs and other remaining federal spending, and why policymakers cannot shrink it enough to prevent spending as a whole from rising markedly in the coming decades; and

- The resulting need for revenues to rise.

The Aging of America

The aging of the population will inevitably drive up costs for Social Security, Medicare, and Medicaid, which provide income and health security and long-term services and supports for older Americans. The share of the population that is 65 or older will grow from 15 percent to 21 percent over the next 20 years and inch up thereafter. This shift stems from the retirement of the large baby-boom generation, born from 1946 through 1964, and the drop in birth rates that followed the baby boom.

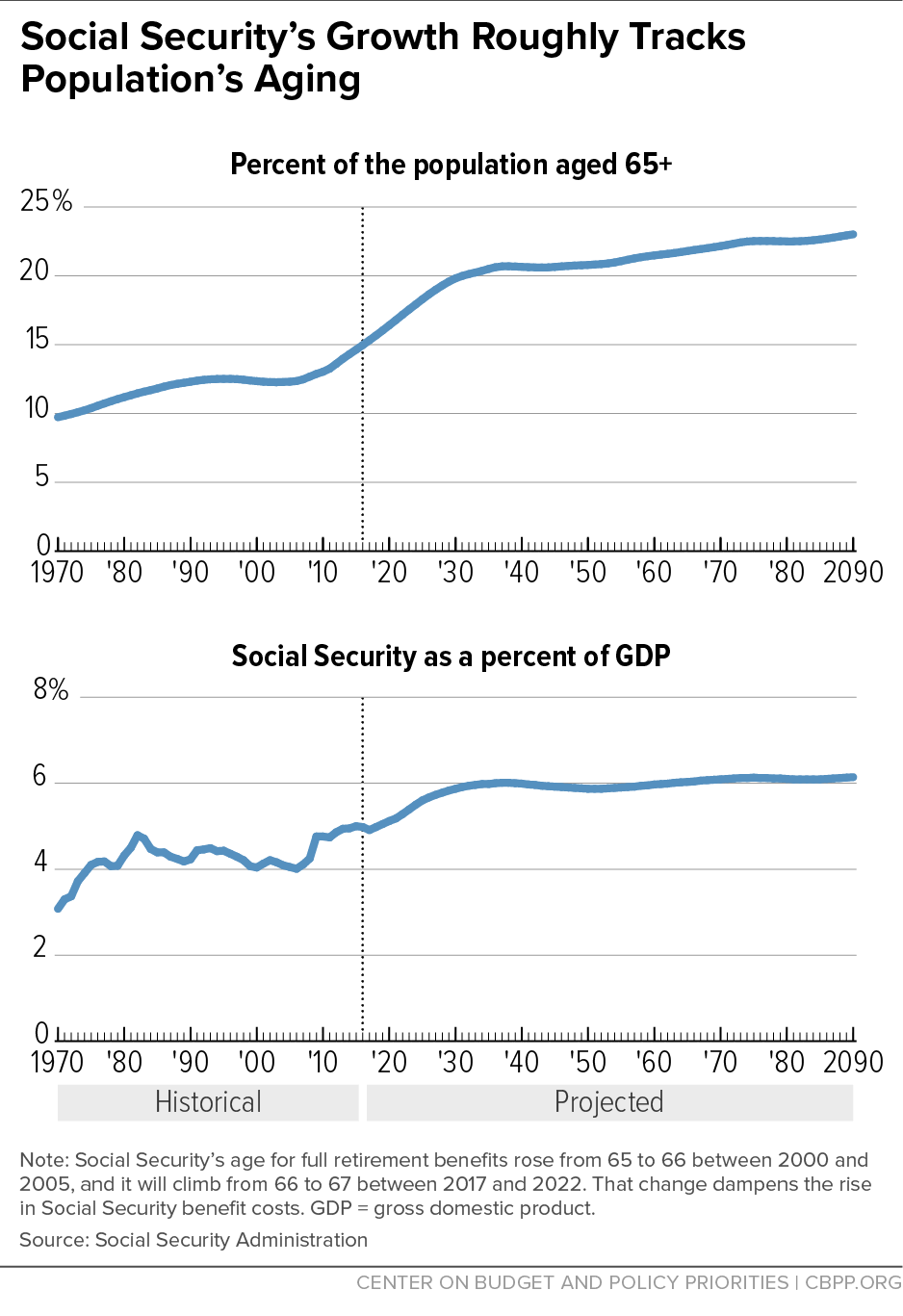

Although Social Security provides benefits to young survivors of deceased workers and working-age adults with serious disabilities, about three-quarters of its benefits go to people age 65 or older. Because of the aging population, its projected costs will rise from 4.9 percent of GDP today to just over 6 percent in the 2030s — an increase of a little over 1 percent of GDP. The rise in Social Security’s costs actually lags slightly behind the aging of the population (see Figure 2) due to already enacted increases in the age at which Social Security pays full retirement benefits (previously 65, now 66, and rising to 67 by 2022), which dampen the rise in benefit costs. (Each one-year increase in the age at which Social Security pays full retirement benefits results in a 7 percent across-the-board reduction in those benefits.) Thus, the projected growth in Social Security costs is fundamentally demographic, traceable to more beneficiaries and not to more generous benefits.[3]

The growth in the number of elderly people, along with increases in the cost and utilization of health care services, will also increase spending for the major federal health programs. Medicare is the primary source of health coverage for Americans over the age of 65. Medicaid provides additional acute-care coverage for low-income seniors and is the largest public payer for nursing home care and other long-term supports and services. Under current law, over 40 percent of the long-run growth in Medicare, Medicaid, and other major health programs is attributable to the aging of the population.[4] The aging of the population will increase the costs of these public programs not only because people who turn 65 become eligible for Medicare, but also because the share of the population that is very old, and hence in greater need of costly skilled nursing and long-term care, is projected to increase even more rapidly. Over the next 20 years, the portion of the population that is age 85 or over will grow from 1.9 percent to 3.1 percent.[5]

Due to these demographic pressures, Social Security is facing a long-run funding shortfall amounting to 1 percent of GDP. Under current law, the combined Social Security trust funds will be able to pay full benefits through 2034 but only three-quarters of scheduled benefits thereafter. Although any legislative package to restore Social Security solvency will likely include some benefit reductions, policymakers should not close the program’s shortfall entirely or primarily in that way, as explained below.

Because the benefits are modest and make up the principal source of income for most beneficiaries, the scope for achieving budgetary savings by cutting benefits is limited. Elderly retirees receive an average Social Security benefit of about $16,400 a year, and widows and disabled workers receive less. Benefits replace a smaller share of pre-retirement earnings than comparable programs in most other developed nations. The median income of individuals or couples age 65 or older receiving Social Security is only about $30,800, including their Social Security income.[6] Millions of beneficiaries have little or no income other than Social Security.

Benefits are already shrinking. Legislation enacted in 1983 increased Social Security’s full retirement age gradually from 65 to 67, which is the equivalent of a 14 percent across-the-board reduction in retirement benefits. Net Social Security checks also fail to keep pace with inflation because Medicare premiums, which tend to rise faster than overall inflation, are deducted from them.

Although gains in life expectancy have prompted calls for further increases in the retirement age, evidence is accumulating that the gains in life expectancy are concentrated among people with higher socioeconomic status.[7] This development argues for making Social Security’s benefit formula more progressive and focusing any benefit reductions on those with high lifetime average earnings. Yet doing so would yield relatively modest savings. Explicit means-testing of benefits for upper-income retirees would also save only very limited amounts.[8]

As a result of these considerations, any viable Social Security solvency package will need to include substantial additional revenues. While the package will likely include reductions in benefits, pressure is growing to expand Social Security, especially to improve the adequacy of benefits for low and medium earners. Our estimate assumes that, on balance, Social Security benefits will follow their currently scheduled path, rising from 4.9 percent of GDP in 2016 to 6.2 percent in 2035 because of the aging of the population.

Rising Health Care Costs and Other Relative Prices

Health care expenditures — in both the public and private sectors — have long grown at a faster pace than the economy and will likely continue to do so. This increase stems not only from rising health care prices (relative to prices generally) but also from more intensive utilization of health care services. New medical procedures, drugs, and treatments extend lifespans and reduce the burden of disease, but they come at a price, a large share of which is paid through Medicare, Medicaid, veterans’ medical care, and other public programs. In recent years, the pace of health care cost growth has slowed, but the extent to which the slowdown will persist is unknown.

Health care is the biggest but not the only area where increases in the relative price of what the federal government buys will put upward pressure on government spending. Many of the goods and services that the government purchases, such as education and scientific and health research, are labor-intensive and have limited opportunities for improved productivity, so their cost tends to rise at a higher-than-average rate. Since the early 1980s, for example, the costs of college tuition and hospital services have grown nearly seven-fold, while overall consumer prices have increased by just over two times.

The idea that the cost of labor-intensive services with slower-than-average productivity growth will rise at a rate greater than the economy’s overall rate of inflation has come to be called “Baumol’s cost disease,” after one of the economists who first identified the issue.[9] The late Senator Daniel Patrick Moynihan posited a corollary: Activities with Baumol’s disease tend to migrate to the public sector.[10] That may be because these activities generate increasing demands for taxpayer support as they become relatively more expensive and as the private sector tries to scale back the resources it devotes to them due to their rise in cost. Together, Baumol’s disease and Moynihan’s corollary pose a significant challenge to the federal budget. If the government is to continue providing the same level of services for a growing population in the face of rising relative prices, federal spending for those services will have to grow in relation to the size of the economy.

Still, the government’s health care programs will continue to present a fertile area for achieving significant budgetary savings. As the Institute of Medicine has written, “there is evidence that a substantial portion of health care expenditures is wasted, leading to little improvement in health or in the quality of care. Estimates vary on waste and excess health care costs, but they are large.”[11]

Policymakers will need to take significant further steps over the long term to slow the growth of health care costs in the private and public sectors alike. Achieving large additional savings over the near term will prove difficult, however, since the Affordable Care Act and the Medicare Access and CHIP Reauthorization Act (MACRA) have already put in place a wide range of policies for reducing excessive payments to providers and shifting to new payment models that seek to reward the quality rather than the volume of health services. And some analysts worry that it could prove difficult to sustain the slower rates of growth already built into Medicare’s formulas for paying health care providers.

There also is limited room to make Medicare more progressive. Medicare beneficiaries, most of whom receive Social Security, have a median income of only about $26,200 a year.[12] Most Medicare benefits go to people who are low or middle income by any standard. Moreover, affluent beneficiaries already pay substantially more for their Medicare benefits. Upper-income people pay higher premiums for both Supplementary Medical Insurance and prescription drug coverage, and MACRA further increased Medicare’s income-related premiums. Finally, the Hospital Insurance payroll tax is levied on all covered wages and self-employment income, without any income limit, and affluent individuals pay an additional Medicare contribution on both earnings and unearned income above $200,000 a year for an individual and $250,000 for a couple.[13]

Medicare’s benefits are not overly generous: they are less comprehensive than a typical employer-sponsored health plan, and beneficiaries must pay premiums, deductibles, and co-payments, with traditional Medicare placing no limit on the total amount of out-of-pocket expenditures that a beneficiary can incur each year. Traditional Medicare also doesn’t cover most hearing, dental, and vision care. On average, Medicare households spend a substantially larger share of their budgets on out-of-pocket health care costs than do non-Medicare households — 15 percent versus 7 percent.[14]

In Medicaid, the opportunity for efficiency gains is limited even more. Medicaid already expends much less than private insurance to cover people of similar health status. This is due primarily to Medicaid’s much lower payment rates to providers and lower administrative costs. Most proposals that would secure more than very modest federal savings from Medicaid — such as proposals to convert the program to a block grant or impose a per capita cap on federal Medicaid reimbursements to states — would do so by shifting substantial costs to states. If that occurs, states will very likely cut eligibility, benefits, or provider payments and hence reduce low-income beneficiaries’ access to care — and thereby widen health disparities.[15]

To be clear: Policymakers should pursue opportunities to reduce cost growth in Medicare and Medicaid; but, they should do so in ways that don’t place burdens on people of modest means that they would have difficulty affording and don’t reduce access to health care or compromise the quality of care. Even with a vigorous effort to control costs, however, spending on the federal government’s major health programs is bound to rise significantly as a percentage of GDP, and consequently so will federal spending overall.

Our estimate for Medicare assumes that policymakers will achieve additional net savings of about $280 billion over the next ten years — the amount proposed in President Obama’s final budget — and that the savings will grow proportionately thereafter.[16] Under that assumption, Medicare spending (net of premiums) will increase from 3.2 percent of GDP today to 4.4 percent in 2035. Other major health programs encompass Medicaid, the Children’s Health Insurance Program (CHIP), and premium and cost-sharing subsidies in the health insurance marketplaces. Because these programs’ benefits are focused on low- and moderate-income people, room for achieving savings is limited, and our estimate assumes a continuation of current policies. We estimate that spending for these programs will rise from 2.3 percent to 2.8 percent of GDP between now and 2035.

Security Challenges

At 3.2 percent of GDP, defense spending is significantly below its 4.8 percent average over the past 40 years and is near the low of 2.9 percent of 1999 through 2001, before the attacks of September 11. The size of the armed forces is about 40 percent smaller than it was under President Reagan. In the Congressional Budget Office (CBO) baseline, defense declines to 2.7 percent of GDP over the next ten years, which would represent the lowest level of defense as a share of GDP in the post-World War II era.[17] Thus, defense does not appear a likely candidate to contribute more to deficit-reduction efforts in the coming years. Furthermore, President Trump and leading congressional Republicans are proposing substantial increases in defense funding.

Recent events indicate that terrorism will likely remain a threat to the United States and its allies for some time to come, and new threats from hostile nations such as cyber warfare are emerging. Like civilian infrastructure, some defense weapons systems are aging and may need modernization or replacement. The new systems should be more capable than the old ones but can also be more costly. In addition, domestic political considerations often prove an obstacle to needed structural reforms in defense — such as retiring older weapons systems, closing unneeded bases, and reforming and modernizing military retirement systems — that would make it easier for the Defense Department to meet its evolving challenges within the constraints of tight budgets. These factors offer little reassurance that the Pentagon’s budget will fall as markedly as a share of GDP as the CBO baseline projects.

Last fall the Center for Strategic and Budgetary Assessments invited expert teams from five think tanks to develop their preferred defense strategy, identify the forces needed to carry it out, and estimate the strategy’s cost. Four out of the five teams recommended defense spending paths that exceeded the amounts allowed under the caps established in the Budget Control Act, as reduced by sequestration.[18]

Our estimate assumes modest near-term growth in the defense budget above baseline levels, along the lines suggested by Brookings Institution defense analyst Michael O’Hanlon.[19] We assume that defense spending, which amounted to 3.2 percent of GDP in 2016, stabilizes at 3.0 percent of GDP through 2021 and grows with prices and population thereafter. Under this assumption, defense shrinks slowly relative to GDP, reaching 2.6 percent of GDP by 2035. If the security situation grew significantly worse, of course, higher levels of defense spending would likely be required.

Existing and Emerging Domestic Needs

Recent efforts to reduce federal spending have focused disproportionately on the parts of the budget controlled by the annual appropriations process: non-defense discretionary (NDD) programs and defense. This has squeezed spending for NDD activities to levels that are or will soon become too low to sustain without risking damage to areas important to long-term economic growth, such as infrastructure, research, and education. NDD programs encompass most of the basic operations of government, including law enforcement, homeland security, veterans’ medical care, scientific and medical research, public health, education and training, child care, national parks, environmental protection, and transportation. These programs are now in the seventh year of an austerity drive. Even with the 2015 bipartisan budget deal, which slightly relaxed the limits on funding for these programs for fiscal years 2016 and 2017, NDD spending in 2017 will be about 13 percent below the comparable 2010 level after adjusting for inflation (nearly $100 billion lower in 2017 dollars). At 3.3 percent of GDP in 2016, NDD spending is already below the 40-year average of 3.7 percent. On its current course, NDD spending will decline still further in the years ahead.[20]

The harmful consequences of this ongoing squeeze are wide-ranging. Our nation’s roads, bridges, and other infrastructure are in serious need of repair and modernization, which is inflicting a significant cost in economic output that will grow larger over time if not addressed. In some cases, as with the water crisis in Flint, Michigan, failing infrastructure puts public health and safety at risk. The American Society of Civil Engineers (ASCE) periodically assesses 16 major sectors of infrastructure to evaluate their current condition and the amount of money needed to put them in good operating condition. Its latest report card issues an overall grade of D+, with most sectors — including roads, schools, dams, aviation, public transit, drinking water, wastewater management, and energy distribution — rated in poor shape. ASCE estimates that currently available funding will fall short of what’s needed by about $200 billion a year over the next several years.[21]

Cuts in scientific and biomedical research have similarly slowed the pace of scientific advances, as creative young researchers are increasingly unable to obtain research grants.[22] And reduced funding for federal statistical programs threatens to undermine the quality of the economic and demographic data that help shape many business and government decisions, including the 2020 census.[23] In addition, due to budget cuts, customer service at the Social Security Administration, IRS, and other federal agencies has deteriorated along many dimensions.[24] The fraction of tax returns that are audited has declined, and there is evidence of growing tax noncompliance.[25]

New spending needs are emerging as well. For example, policymakers will need to accommodate the rising costs of health care and other services for veterans, including those wounded in ongoing conflicts and aging survivors of the Vietnam War. Making federal assets and cultural resources like the national parks less vulnerable to climate-related extreme weather events is likely to entail additional investments.

The widely discussed growth in income inequality also calls for increased government activity in certain areas. The years from the end of World War II into the 1970s were ones of substantial economic growth and broadly shared prosperity. Beginning in the 1970s, however, not only did economic growth slow, but the income gap also widened.[26] Globalization has been a factor, reducing the demand for labor in import-competing industries and their suppliers. The declining bargaining power of labor, growing industrial concentration, frequent periods of less-than-full employment, and many other developments have also played important parts.

Some ways of responding to these developments, such as increasing the minimum wage and expanding overtime pay, would have little budgetary effect, but others would add to federal expenditures. One approach, for example, is to undertake efforts to raise market incomes through increasing the human capital stock. MIT economist David Autor has written, “Human capital investment must be at the heart of any long-term strategy for producing skills that are complemented rather than substituted by technology.”[27] This investment could take the form of expanding early childhood education, making higher education more affordable, providing more apprenticeships and other forms of job training, and the like. Government could also increase wage income by creating subsidized jobs or direct public employment and ensuring that working families with low or modest incomes can afford child care.

A complementary approach is to expand supports that help offset market-generated inequalities and assure that low- and moderate-income families have decent incomes, health care, and retirement. For example, many progressives and conservatives alike support increasing and expanding the Earned Income Tax Credit and Child Tax Credit, which would increase the rewards to work and support children’s development.[28] Policymakers also could take steps to strengthen certain other safety-net programs.

In the face of the pressures outlined here, further reductions in NDD spending as a percentage of GDP, as called for by the existing statutory caps (including sequestration, which is scheduled to return in full in 2018), would prove painful and difficult to achieve and would exacerbate many of the problems just described. Reversing the deferred maintenance of public infrastructure, conducting adequate scientific research, restoring the quality of basic government services, and responding to growing economic inequality will very likely require stabilizing or increasing this category of spending in relation to GDP.

Our estimate assumes that NDD spending will receive increases above the post-sequestration levels that reach $100 billion a year in 2020 and 2021 and will keep pace with inflation and population growth thereafter. An increase of this size would bring NDD spending back roughly to its level in 2010 in inflation-adjusted terms. It would provide about $1 trillion over ten years that could finance additional infrastructure and meet some other domestic shortfalls. Even under this assumption, NDD spending would simply remain at about 3.3 percent of GDP through 2021 and then drop slowly to 2.8 percent of GDP by 2035, which would be the lowest level on record (with data back to 1962).

Interest Costs and Other Federal Spending

The rest of the federal budget comprises mandatory spending programs other than Social Security and the major health programs. The largest of these is interest. Although federal debt held by the public has increased substantially as a result of the Great Recession and policies to address it, federal interest costs as a percent of GDP have plunged because interest rates have dropped to historically low levels. The Federal Reserve has begun gradually raising rates, however, and most economic forecasters expect a rise in federal borrowing costs over the next few years.

CBO projects that the interest rate on ten-year Treasury notes will climb from 1.8 percent in 2016 to 2.8 percent in 2018 and 3.7 percent over the 2021-2027 period. That would represent an inflation-adjusted, long-term interest rate of 1.3 percent, which is well above the current real interest rate, though more than a percentage point below the average before the recession.[29] The projected rise in interest rates will increase federal spending on net interest payments from 1.3 percent of GDP in 2016 to 2.4 percent in 2035, assuming that the debt-to-GDP ratio remains roughly constant.

Spending on the remaining mandatory programs is already low in historical terms and is projected to fall still further. This diverse category includes programs such as veterans’ compensation and pensions, SNAP, the Earned Income Tax Credit and Child Tax Credit, Supplemental Security Income for the aged and disabled poor, federal employee retirement benefits, unemployment compensation, and farm price supports. Under current law, spending on mandatory programs outside Social Security, health care, and net interest is already slated to decline from 2.8 percent of GDP in 2016 to 2.4 percent by 2035 — which is below its average of 2.8 percent of GDP for the 1976-2016 period. This decline, however, will offset only a portion of the projected increase in interest costs.

In the face of the forces pushing federal expenditures higher, policymakers should pursue avenues for achieving budgetary savings. They need to set priorities, eliminate duplicative and outdated programs, and make spending decisions based on evidence about what works. Such savings, however, will not nearly offset the factors that will lead to the higher overall spending detailed above.

Greater reliance on technology can achieve efficiencies and increase productivity in some federal functions. But much of the budget comprises cash or in-kind benefit payments, and achieving significant cost reductions in these programs would require scaling back the benefits provided. Although automating paper processes can reduce some administrative costs, many low-income and elderly citizens face financial or cognitive barriers to online access and will continue to depend on personal contact, either by phone or face-to-face.[30] Moreover, some complicated problems cannot be resolved without human assistance.

Policymakers and program administrators should also take further steps to improve purchasing practices and payment accuracy and assure that benefits reach only those for whom they are intended. Increased funding for program integrity activities can sometimes save taxpayers money in the long run.[31] But the savings that can be achieved in this way are often overstated, and periodic efforts to root out fraud, waste, and abuse in the federal budget typically produce only limited savings.

Savings opportunities are also limited by the need to avoid increasing poverty and hardship. In their plan of late 2010, the co-chairs of the President’s fiscal commission, Erskine Bowles and Alan Simpson, established a guiding principle that deficit-reduction efforts should not increase poverty or inequality. Policymakers should adhere to this principle in future deficit-reduction efforts. In fact, previous major deficit-reduction actions — including the bipartisan deficit-reduction packages of 1990 and 1997 and the 1993 deficit-reduction package — took steps to reduce poverty or increase access to health care even as they reduced deficits. In contrast, the 2018 budget resolution that the House Budget Committee recently adopted concentrates roughly half of its non-defense spending cuts on programs that assist people of limited means.[32] Ruling out increases in revenues, as the House plan does, virtually ensures that a heavy share of the deficit-reduction burden will fall on those least able to bear it.

Box 3: The Appropriate Budget Target

The period when the U.S. economy was operating below its potential, with slack remaining in the labor market and interest rates near zero, was not the time for shrinking the budget deficit. When the economy is at or near potential, however, policymakers should generally aim to keep the debt from growing faster than the economy or possibly to reduce it gradually.

Deficits that lead to a perpetually rising debt-to-GDP ratio are unsustainable because they leave less and less saving available for private investment. Generally, the debt-to-GDP ratio should rise during periods of economic slack or major emergencies and then decline during good times. When the economy slows, federal revenues automatically decline or grow more slowly, and spending on unemployment insurance and other social programs increases, keeping the downturn from becoming longer and deeper, but causing deficits to rise. Stabilizing or reducing the debt ratio when the economy is strong allows these automatic stabilizers to work and provides policymakers with the flexibility to enact temporary program increases and tax cuts to boost demand and alleviate hardship when the economy is weak.

Stabilizing or reducing the debt-to-GDP ratio does not require balancing the budget or running surpluses, as long as the debt grows no faster than the economy. For example, from 1946 through 1979, the nation ran balanced budgets or surpluses in only eight years. Yet over those 34 years, the debt fell from 106 percent of GDP to 25 percent because the economy grew faster than the debt. Making budget balance the preeminent fiscal policy goal is neither necessary nor desirable, and such a goal is especially damaging if revenue increases are taken off the table.a

Some have suggested that certain debt-to-GDP ratios have a particular significance in terms of their effect on the economy. In reality, there are no absolute thresholds. Researchers at the International Monetary Fund have written, “Our results do not identify any clear debt threshold above which medium-term growth prospects are dramatically compromised.”b Moreover, today’s very low real (inflation-adjusted) interest rates justify a higher debt-to-GDP ratio than was appropriate when the government faced much higher borrowing costs.

a Robert Greenstein and Joel Friedman, Balancing the Budget in Ten Years and No New Revenue Are Flawed Budget Goals, CBPP, March 15, 2015.

b Andrea Pescatori, Damiano Sandri, and John Simon, Debt and Growth: Is There a Magic Threshold?, International Monetary Fund WP/14/34, February 2014, p. 4.

Revenues Will Need to Rise

The pressures for higher spending mean that revenues, too, will need to rise. Although balancing the budget each year isn’t necessary, policymakers should generally aim to keep federal debt held by the public from growing faster than the economy once the economy is healthy. (See Box 3.) That, in turn, will require limiting budget deficits to an average of no more than about 3 percent of GDP under CBO’s current economic assumptions.

Federal revenues averaged 17.4 percent over the 1976-2016 period. With spending averaging 20.5 percent of GDP over those years, that level of revenues would have been sufficient to keep the debt-to-GDP ratio about the same at the end of this period as at its beginning, had it not been for the Great Recession. The debt-to-GDP ratio in 2007 (35 percent) was not much higher than in 1976 (27 percent). During and after the recession, however, it swelled to about 75 percent of GDP.

Under current law, federal revenues are projected to edge up gradually from the 2016 level of 17.8 percent of GDP, as increases in real income push taxpayers into higher income tax brackets. Even if federal expenditures continue to adhere to current budget restrictions, including sequestration, and defense and NDD spending thus continue to shrink markedly as a share of GDP, current-law revenues would fail to keep the debt from growing more rapidly than the economy.[33] And if, as a result of the factors we have described here, it proves impossible (and unwise) to maintain the existing limits on discretionary spending, historical or current-law levels of revenues will be still more inadequate.

Under the spending assumptions presented here, federal revenues would need to grow to 20.5 percent of GDP by 2035 in order to stabilize the debt-to-GDP ratio. Even more revenues would be required to reduce the debt ratio.

Fortunately, there is considerable room for increasing revenues in sound, efficient ways that would not injure the economy and that, by financing investments important for long-term economic growth, should ultimately help the economy grow.

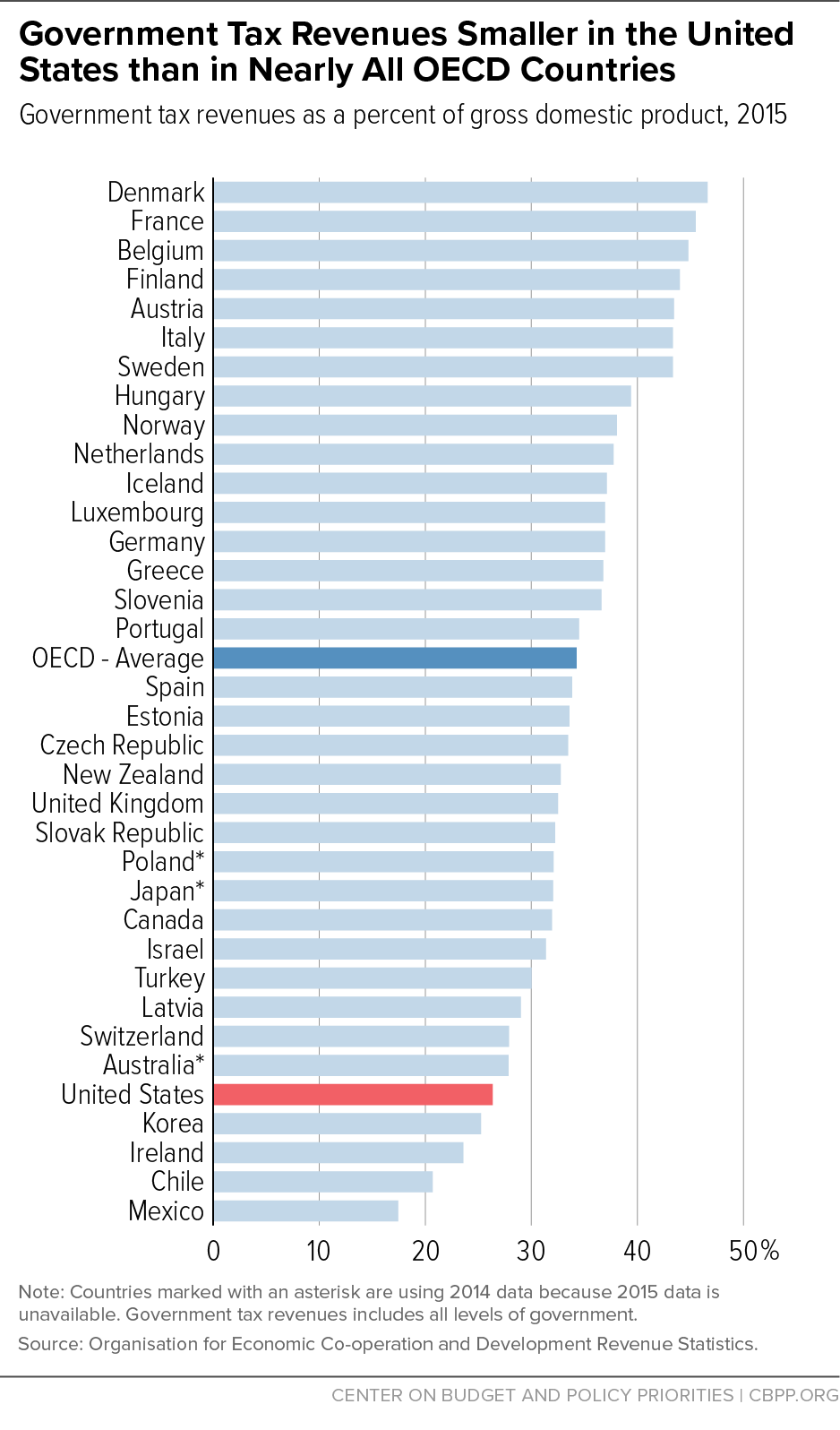

The United States collects less in total federal, state, and local tax revenues than nearly any other developed country when measured as a share of the economy, according to the Organisation for Economic Co-operation and Development (OECD). (See Box 4.) The U.S. share — 26 percent of GDP — is 8 percentage points below the average for OECD member countries. By this standard, the United States has considerable room to raise more revenue.

Box 4: The United States Is a Low-Tax Country

The United States collects less in total government tax revenues than nearly any other developed country when measured as a share of the economy. Total government receipts in the United States are not only well below other industrialized countries; they’re also lower than in countries that are far less wealthy than the United States. (See figure.) The U.S. share — 26 percent of GDP — is 8 percent of GDP below the average for members of the Organisation for Economic Co-operation and Development (OECD). These figures include tax collections by all levels of government; in the United States, that means federal, state, and local governments. They exclude charges for public services and other items that the OECD classifies as non-tax receipts.

On a related note, federal tax expenditures — effectively, spending delivered through the tax system as tax deductions, exclusions, and other targeted tax breaks, which former Federal Reserve Chairman Alan Greenspan has termed “tax entitlements” — reduce federal revenues by over $1 trillion annually. Many tax expenditures are poorly designed to achieve their desired policy goals, so reforming or eliminating them could not only raise revenue but also could help ensure these policies achieve their aims more effectively and encourage investment resources to flow to where they will be used most productively (rather than to where the after-tax return is greatest, irrespective of an investment’s economic merits).[34]

Further, various taxes designed to correct for market failures could both raise revenue and increase the strength of the economy. For example, well-designed energy taxes could ease the use of fossil fuels and thereby reduce the risk of serious long-term damage to the economy as a result of global warming. Taxes designed to reduce certain financial-sector practices that encourage speculation could make the economy more stable.

Conclusion

Demographic, economic, and other factors will increase the demand for many of the goods and services that the federal government can produce most effectively and efficiently, such as Social Security, health insurance coverage, long-term investments in education and infrastructure, and basic scientific research and development. Federal spending and revenues will consequently need to be larger in relation to the size of the economy in coming decades than they have been in the past.

Spending of 20 to 21 percent of GDP and revenues of 17 to 18 percent of GDP — the averages of the past several decades — will not be sufficient to support government functions that the public widely supports or that are important for long-term economic growth. In fact, budget plans from both bipartisan and conservative organizations — including a National Academy of Sciences expert panel, the Bipartisan Policy Center, and the American Enterprise Institute — all have recognized that spending and revenues will need to exceed historical levels, even as these plans have proposed substantial cuts in various programs.

How spending and revenues are increased matters greatly, of course. Higher taxes and spending need not be a barrier to economic growth, as past U.S. experience — for example, following the tax increases enacted in the early 1990s and at the end of 2012 — and that of other countries show. Policymakers should structure tax increases to promote economic efficiency and other important social objectives, such as by putting a price on greenhouse gas emissions and curbing inefficient tax expenditures. Higher taxes can also be growth-promoting if they are used to finance investments in public education, infrastructure, public health, and other forms of physical and human capital. The bottom line is that under the circumstances our country now faces, a larger, appropriately designed public sector is not to be avoided, but welcomed.

End Notes

[1] The leading House proposal for a constitutional balanced budget amendment (H.J.Res. 1) would limit federal spending to 20 percent of GDP. The leading Senate proposal (S.J.Res. 24) would limit spending to 18 percent of GDP.

[2] Richard Kogan, Paul N. Van de Water, and Chloe Cho, Long-Term Budget Outlook Has Improved Significantly Since 2010 But Remains Challenging, Center on Budget and Policy Priories (CBPP), August 2016, https://www.cbpp.org/research/federal-budget/long-term-budget-outlook-has-improved-significantly-since-2010-but-remains.

[3] Kathleen Romig, What the 2017 Trustees Report Shows About Social Security, CBPP, July 24, 2017, https://www.cbpp.org/research/social-security/what-the-2017-trustees-report-shows-about-social-security.

[4] Congressional Budget Office, The 2017 Long-Term Budget Outlook, March 30, 2017, p. 16, https://www.cbo.gov/publication/52480.

[5] U.S. Social Security Administration, Office of the Chief Actuary, Population Estimates, https://www.ssa.gov/oact/HistEst/Population/2017/Population2017.html.

[6] U.S. Social Security Administration, Income of the Population 55 or Older: 2014, April 2016, Table 3.A2, https://www.ssa.gov/policy/docs/statcomps/income_pop55/2014/sect03.html#table3.a2.

[7] Hilary Waldron, “Trends in Mortality Differentials and Life Expectancy for Male Social Security-Covered Workers, by Average Relative Earnings,” Social Security Bulletin, 67:3, April 2008; National Academy of Sciences, The Growing Gap in Life Expectancy by Income: Implications for Federal Programs and Policy Responses, 2015, http://www.nap.edu/catalog/19015/the-growing-gap-in-life-expectancy-by-income-implications-for.

[8] Kathy Ruffing, Means-Testing No Answer for Social Security, CBPP, March 10, 2011, https://www.cbpp.org/blog/means-testing-no-answer-for-social-security.

[9] William J. Baumol, The Cost Disease (New Haven: Yale University Press, 2012).

[10] Daniel Patrick Moynihan, Miles to Go: A Personal History of Social Policy (Cambridge: Harvard University Press, 1996), p. 17.

[11] Committee on the Learning Health Care System in America, Best Care at Lower Cost: The Path to Continuously Learning Health Care in America (Washington: National Academies Press, 2012), p. 101.

[12] Gretchen Jacobson et al., Income and Assets of Medicare Beneficiaries, 2016-2035, Kaiser Family Foundation, April 2017, http://www.kff.org/medicare/issue-brief/income-and-assets-of-medicare-beneficiaries-2016-2035/.

[13] Paul N. Van de Water, Medicare Is Already Means-Tested, CBPP, May 19, 2011, https://www.cbpp.org/blog/medicare-is-already-means-tested. Repealing the two Medicare taxes on high-income filers, as congressional Republicans are considering, would widen the long-term fiscal gap and make Medicare less progressive.

[14] Kaiser Family Foundation, The Latest Trends in Income, Assets, and Personal Health Care Spending Among People on Medicare, November 2015, Exhibit 29, http://kff.org/slideshow/the-latest-trends-in-income-assets-and-personal-health-care-spending-among-people-on-medicare/.

[15] Edwin Park, Medicaid Per Capita Cap Would Shift Costs and Risks to States and Harm Million of Beneficiaries, CBPP, February 27, 2017, https://www.cbpp.org/research/health/medicaid-per-capita-cap-would-shift-costs-and-risks-to-states-and-harm-millions-of; CBPP, Senate Health Care Bill Ends Medicaid as We Know It, July 6, 2017, https://www.cbpp.org/research/health/senate-health-care-bill-ends-medicaid-as-we-know-it-with-even-bigger-cuts-than-house.

[16] CBO, Proposals for Health Care Programs — CBO’s Estimate of the Fiscal Year 2017 Budget, March 29, 2016, https://www.cbo.gov/publication/51431. The Obama budget proposed $376 billion in gross reductions in Medicare spending, partly offset by the cost of repealing sequestration.

[17] CBO, An Update to the Budget and Economic Outlook: 2017 to 2027, June 2017, https://www.cbo.gov/publication/52801.

[18] Jacob Cohn and Ryan Boone, How Much is Enough? Alternative Defense Strategies, Center for Strategic and Budgetary Assessments, November 2016, http://csbaonline.org/uploads/documents/CSBA6218_%28How_Much_is_Enough%29Final4-web.pdf.

[19] Michael E. O’Hanlon, The $650 Billion Bargain: The Case for Modest Growth in the Defense Budget (Brookings Institution Press, August 2016).

[20] CBO, An Update to the Budget and Economic Outlook: 2017 to 2027, and historical budget data.

[21] American Society of Civil Engineers, 2017 Infrastructure Report Card — Economic Impact, http://www.infrastructurereportcard.org/the-impact/economic-impact/.

[22] Ronald J. Daniels, “A generation at risk: Young investigators and the future of the biomedical workforce,” Proceedings of the National Academy of Sciences, January 13, 2015, http://www.pnas.org/content/112/2/313.abstract.

[23] Arloc Sherman, Census Funding in Crisis, CBPP, June 28, 2017, https://www.cbpp.org/blog/census-funding-in-crisis.

[24] Kathleen Romig, Cuts Weakening Social Security Administration Services, CBPP, March 15, 2017, https://www.cbpp.org/research/social-security/cuts-weakening-social-security-administration-services.

[25] Brandon DeBot, Emily Horton, and Chuck Marr, Trump Budget Continues Multi-Year Assault on IRS Funding Despite Mnuchin’s Call for More Resources, CBPP, March 16, 2017, https://www.cbpp.org/research/federal-budget/trump-budget-continues-multi-year-assault-on-irs-funding-despite-mnuchins.

[26] Chad Stone et al., A Guide to Statistics on Historical Trends in Income Inequality, CBPP, November 7, 2016, https://www.cbpp.org/research/poverty-and-inequality/a-guide-to-statistics-on-historical-trends-in-income-inequality.

[27] David Autor, “Polanyi’s Paradox and the Shape of Employment Growth,” September 3, 2014, http://economics.mit.edu/files/9835.

[28] Chuck Marr et al., EITC and Child Tax Credit Promote Work, Reduce Poverty, and Support Children’s Development, Research Finds, CBPP, October 1, 2015, https://www.cbpp.org/research/federal-tax/eitc-and-child-tax-credit-promote-work-reduce-poverty-and-support-childrens.

[29] CBO, An Update to the Budget and Economic Outlook: 2017 to 2027, p. 21.

[30] United States Senate, Special Committee on Aging, Reduction in Face-to-Face Services at the Social Security Administration, March 2014, https://www.aging.senate.gov/imo/media/doc/SSA%20Hearing%20Staff%20Memo1.pdf.

[31] Kathy Ruffing, Making Social Security Disability Programs More Efficient, CBPP, February 5, 2015, https://www.cbpp.org/blog/making-social-security-disability-programs-more-efficient.

[32] Isaac Shapiro, Richard Kogan, and Chloe Cho, House GOP Budget Plan Cuts Programs Aiding Low- and Moderate-Income People by $2.9 Trillion Over Decade, CBPP, August 3, 2017, https://www.cbpp.org/research/federal-budget/house-gop-budget-cuts-programs-aiding-low-and-moderate-income-people-by-29.

[33] CBO, An Update to the Budget and Economic Outlook: 2017 to 2027, Table 1.

[34] For example, see Chuck Marr, Nathaniel Frentz, and Chye-Ching Huang, Retirement Tax Incentives Are Ripe for Reform, CBPP, December 13, 2013, https://www.cbpp.org/blog/tax-incentives-for-retirement-savings-are-ripe-for-reform, and Will Fischer and Chye-Ching Huang, Mortgage Interest Deduction Is Ripe for Reform, CBPP, June 25, 2013, https://www.cbpp.org/research/mortgage-interest-deduction-is-ripe-for-reform.

More from the Authors