Depletion of IRS Enforcement Is Undermining the Tax Code

Testimony of Chye-Ching Huang, Senior Director for Economic Policy, CBPP*

Before the House Ways and Means Committee

Chairman Neal, Ranking Member Brady, and distinguished members of the Committee, thank you for the opportunity to testify today.

My testimony will explain how underfunding Internal Revenue Service (IRS) enforcement empowers tax avoiders and evaders, including certain large corporations and businesses, while hurting honest tax filers. This inequity mirrors the 2017 tax law and many of its regulations. The law gave profitable corporations and wealthy households large tax cuts and new ways to game the tax code, while largely leaving low- and moderate-income Americans behind.

There is, however, promising bipartisan recognition that IRS enforcement funding is too low, and that the revenue gains from added enforcement funding would more than offset the cost. Lawmakers can build on this to restore adequate funding for the core government function of collecting taxes owed under law. Lawmakers should also pursue meaningful tax reform that strengthens the integrity of the tax code, raises revenue, and boosts workers’ and families’ incomes.

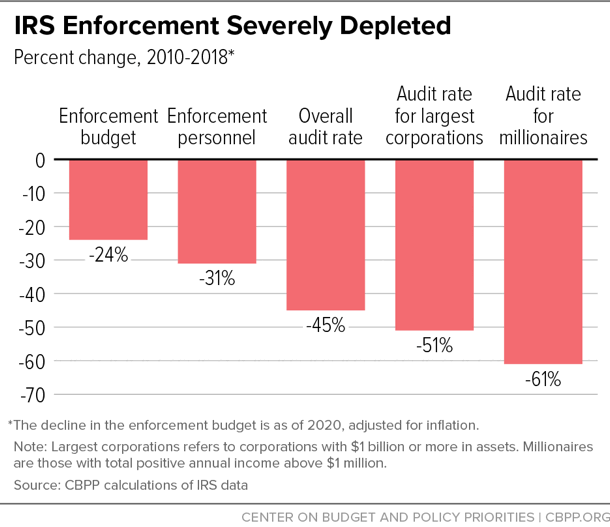

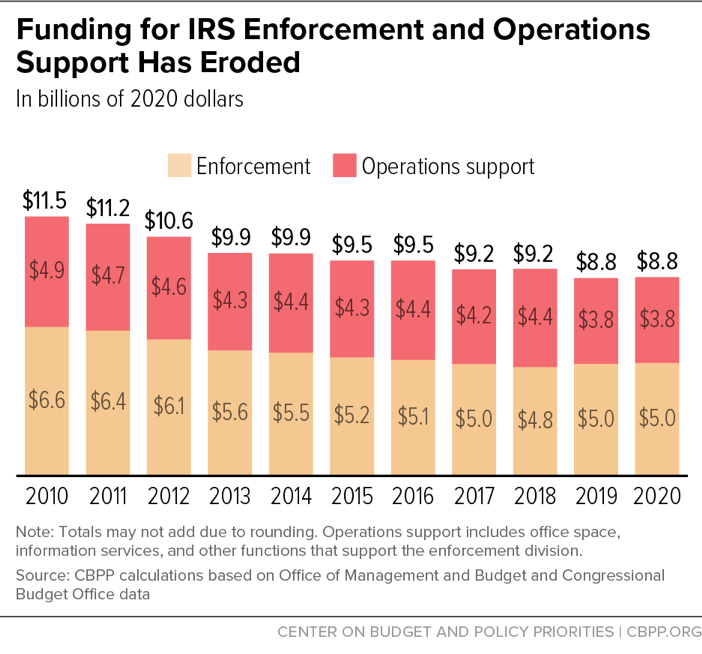

Figure 1 summarizes the impact of the deep cuts to IRS funding since 2010:[1]

- IRS funding overall has been cut by 21 percent in inflation-adjusted terms.

- IRS enforcement funding has been cut by 24 percent in inflation-adjusted terms, even as the number of tax returns has grown by about 9 percent.[2]

- The number of operations staff has fallen by 31 percent, and the number of revenue agents with the expertise to conduct audits of complex returns has fallen by 35 percent.

- The audit rate overall has fallen by 45 percent, from 0.9 percent to 0.5 percent.[3]

- The audit rate for corporations with more than $1 billion in assets is down 51 percent.

- The audit rate for filers with more than $1 million[4] in annual income is down 61 percent.

These trends have significant implications for efforts to address the tax gap. Each year an estimated $441 billion in federal taxes owed is not paid voluntarily and on time. Underreporting of tax liability accounts for 80 percent of this gross tax gap; the other 20 percent reflects failure to file a return or failure to pay the tax reported on returns on time and in full.[5] The IRS recovers about 14 percent of the gross tax gap through enforcement efforts and other late payments, leaving a net tax gap of $381 billion.

The steep decline in audits for high-income individuals stemming from IRS underfunding means that low- and moderate-income households claiming the Earned Income Tax Credit (EITC) are now audited at roughly the same rate as the top 1 percent of filers, even though the former are responsible for less than 10 percent of the tax gap due to underreporting while the latter may account for as much as 70 percent.[6]

The 2017 tax law and its regulations, too, reflect skewed priorities. While the tax law delivered large tax cuts and new gaming opportunities to corporations and wealthy households, it not only failed to expand the EITC — a proven tool for raising incomes and reducing poverty among working families — but also left 26 million children in low- and moderate-income families out of its full increase in the Child Tax Credit, even while expanding eligibility for the credit to families with incomes up to $400,000. Policymakers should fundamentally restructure the law to raise revenues in ways that reduce inequality, boost the incomes of struggling workers and families, and reduce tax avoidance.

Weakening Enforcement Empowers Tax Cheating and Gaming

Cutting IRS enforcement amounts to what former IRS Commissioner John Koskinen called “tax cuts for tax cheats.”[7] Large corporations, pass-through businesses (S corporations, partnerships, and sole proprietorships), and high-income individuals that do not pay the taxes they owe are the biggest winners when the IRS doesn’t receive the resources it needs to collect taxes owed.

Audits of large businesses and high-income individuals are complex. Large corporations can use myriad accounting games, entities, and transactions across countries to avoid or evade taxes. Pass-through businesses — whose income is taxed at their owners’ individual tax rates and flows disproportionately to wealthy households[8] — can have complex, opaque ownership arrangements. High-income and high-wealth households often have complex finances across generations, entities, and countries.

To audit such complex returns, the IRS uses expert Revenue Agents with at least two to three years of on-the-job training to conduct on-site audits. But funding cuts have cost the IRS much of its most experienced staff: the number of Revenue Agents fell by 35 percent between 2010 and 2018, to the lowest number since 1954.[9] As a result, audit rates for large corporations, most pass-through entities, and very high-income individuals (those with annual incomes surpassing $1 million) have plummeted, even though they all are large sources of the $441 billion annual gross tax gap.[10]

The most well-resourced filers can afford creative tax advisors, litigators, and lobbyists to aggressively push the boundary between lawful tax avoidance and unlawful tax evasion, including when they are audited, recent reporting starkly illustrates.[11] An IRS that lacks the resources to defend that boundary may have to give way, surrendering revenue that should be owed under the best interpretation of the tax law, and setting a precedent for other filers.

Funding cuts have also reduced the IRS’ ability to detect and prosecute tax evasion and corruption. Cases brought by the IRS’ criminal division have dropped by about a quarter since 2010.[12] As ProPublica notes, recent high-profile prosecutions for tax evasion, including of Paul Manafort, Michael Cohen, and Michael Avenatti, occurred because they attracted the attention of federal investigators for other reasons.[13] Such trends may, in turn, hurt anti-corruption efforts more generally: as an OECD-World Bank report notes, “[while] viewed as distinct crimes, tax crime and corruption are often intrinsically linked.”[14]

Funding cuts that hobble IRS enforcement and empower the well-resourced to game the tax code not only shrink federal revenue, but also undermine honest filers’ confidence in the integrity of the tax system. This is a serious threat to a system that relies on voluntary compliance.

Audits of Large Corporations Halved

As the IRS has hemorrhaged experienced Revenue Agents, the audit rate for large corporations (those with $1 billion or more in assets) has fallen by half over the last ten years. So has the audit rate for corporate giants (those with more than $20 billion in assets), with these corporations going from near certainty of being audited to a coin-toss chance.[15]

Auditing “smarter” cannot make up for such deep losses of expert staff. The IRS is improving its data analytics to try to better select for audits the large corporations that are most likely to be non-compliant,[16] but staff are needed to follow up on audit leads. Take this example from a ProPublica report on the audit of Facebook:[17]

Although billions of dollars were at stake in the Facebook audit, the IRS had no funds to hire an expert. The audit team had to wait for three months, until the new fiscal year began in October 2015, to even begin looking. Then, because of a lengthy contracting process, it took six more months for the $800,000 contract to go through. The expert, an economist who specializes in analyzing these intra-company deals, finally went to work in March 2016.

Large corporations can pour resources into tax planning, litigation, and lobbying to try to shift the boundary between permissible tax avoidance and unlawful tax evasion — and to stretch out their cases as long as they can — but budget cuts have hampered the IRS’ ability to match them. It appears that the IRS has therefore become more willing not to pursue some filers, or to settle with them for much smaller amounts than it believes they owe. For example, the percent of audited returns of “corporate giants” that has resulted in no change in taxes paid whatsoever has quadrupled since 2010, and additional tax assessed on audit for corporations has been halved since 2010.[18]

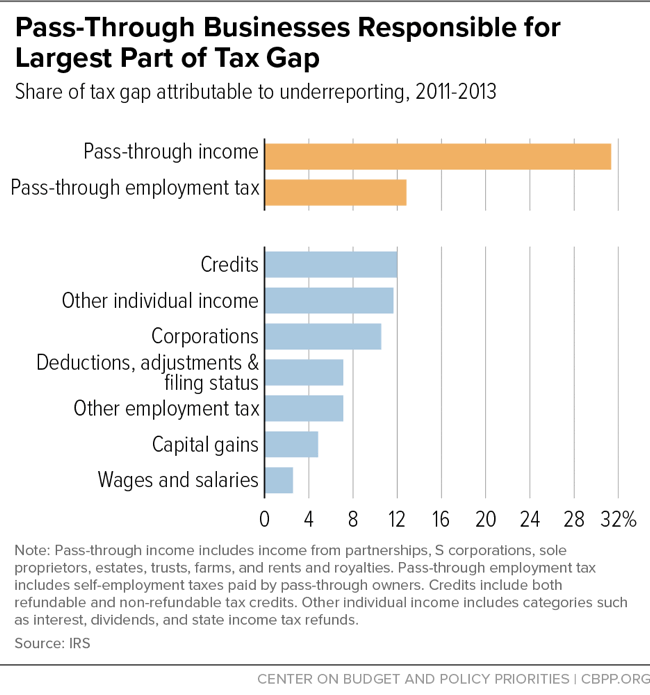

Audits of Pass-Throughs Cut by Two-Fifths

Underreporting of pass-through income and self-employment taxes accounts for 44 percent of the gross tax gap due to underreporting, more than any other source.[19] (See Figure 2.) While this income is supposed to show up on owners’ individual tax returns, a study using IRS data found that:[20]

Our inability to unambiguously trace 30% of partnership income to either the ultimate owner or the originating partnership underscores the concern that the current U.S. tax code encourages firms to organize opaquely in partnership form in order to minimize tax burdens.

The audit rates for both S Corporation and partnership returns have fallen by more than 40 percent since 2010, to just 0.2 percent.

Among both pass-throughs and corporations, audits and the recovery of amounts owed by businesses that fail to file returns to pay employment taxes — which is a crime — have cratered due to lack of resources. The IRS had an effective and efficient program to collect these amounts, but the process for identifying and pursuing cases of employment tax non-filing “has been declining since FY 2011 and virtually stopped in October 2016 due to significant reductions in staffing.”[21]

Audits of High-Income Filers Cut by Three-Fifths

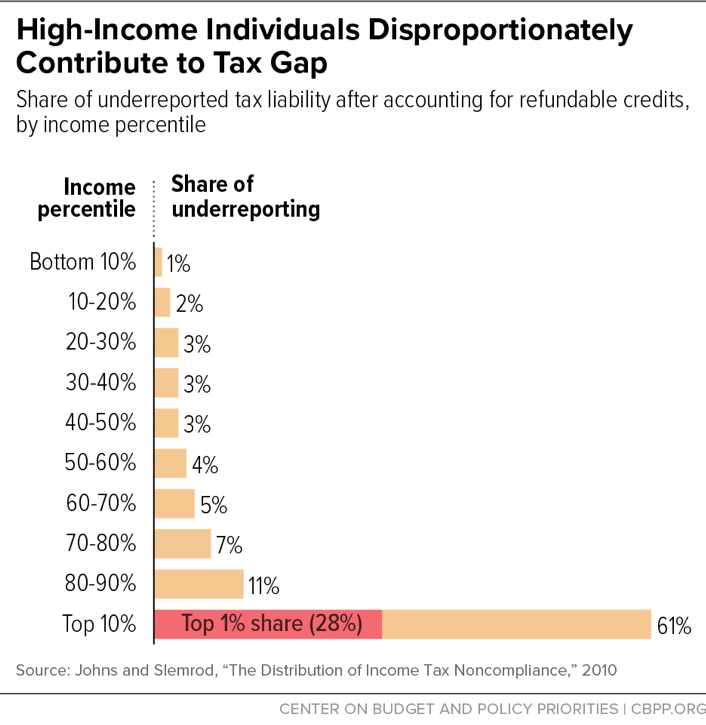

The audit rate for the highest-income individuals has plummeted as well, down 67 percent for those in roughly the top 1 percent. These same individuals are disproportionately the owners of corporations and pass-through businesses, where audit rates have also dropped. Filers in the top 1 percent account for roughly 30 percent of the tax gap due to income underreporting (see Figure 3), according to a 2010 study primarily using data from 2001.[22] A more recent study that attempts to incorporate new research on tax non-compliance estimates that the figure could be as high as roughly 70 percent.[23]

Attrition of expert IRS personnel and other resources has also damaged the agency’s ability to conduct tax enforcement among the very highest-income households within the top 1 percent. The IRS’ Global High Wealth Industry Group, created to audit the complex returns of these very wealthy filers, did not receive the resources it had planned for, hampering its efforts.[24]

The IRS’ ability to pursue high-income people who simply don’t file their taxes has also taken a big hit. Over 2014 to 2016, almost 880,000 high-income households owing more than $45 billion failed to file; the IRS is unlikely to collect these tax dollars owed due to lack of resources.[25]

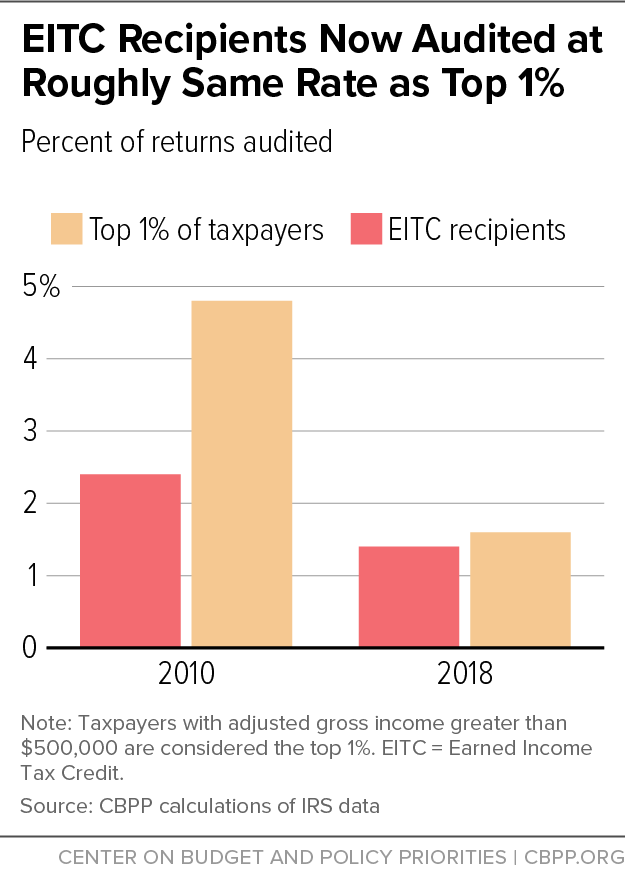

EITC Recipients Now Audited at Same Rate as Top 1 Percent

Because of the steep drop in audit rates for high-income individuals, households claiming the EITC for low- and moderate-income workers and their families are now audited at about the same rate as filers in the top 1 percent (see Figure 4), even though underreporting in the EITC accounts for less than 10 percent of the gross tax gap[26] while filers in the top 1 percent may be responsible for 70 percent of it. Audits of high-income individuals and corporations also yield larger average collections than audits of lower-income taxpayers.[27] EITC audits were 39 percent of audits in 2018.

While EITC audit rates have fallen in the face of IRS budget cuts, they have been far less affected by the loss of experienced Revenue Agents than audits of large businesses and high-income individuals. IRS examinations of low-income filers’ returns often occur by mail, so they are cheaper and require less expertise to administer, as Commissioner Rettig has noted.[28]Also, while high-income filers and large businesses can hire lawyers, accountants, and lobbyists to challenge an audit,[29] the vast majority of EITC filers audited aren’t represented by a lawyer or other tax professional.[30]

The disconnect between the steep cuts to audit rates of large businesses and high-income individuals and their outsized contribution to the tax gap also creates stark geographic and racial patterns. Estimates by a former IRS economist and researcher suggests that the most highly audited areas of the country are now rural, Southern counties that are predominantly African American.[31]

2017 Tax Law Provisions Further Encourage Tax Gaming

Recent changes in tax law add insult to injury by further complicating the IRS’ enforcement challenge. The 2017 tax law’s pass-through deduction is a prime example.

While pass-throughs are the largest source of the tax gap, audit rates for S corporations and partnerships are far lower than for EITC filers. Instead of addressing pass-through tax non-compliance, the 2017 tax law created a costly, complex new deduction for pass-throughs. The top 1 percent of households will get 61 percent of the benefit from the new deduction for pass-through income, while the bottom two-thirds of households will get just 4 percent, according to the Joint Committee on Taxation.[32] The deduction cuts the top rate on pass-through income below the top rate on wages and salaries, thereby increasing the incentive to use pass-throughs for tax avoidance. As one tax advisor told a conference of personal financial advisors:

This is, without a doubt, one of the biggest areas of planning that we can have under the new law. This is why, in large part, they should have just renamed the [2017 tax law] the tax professional, lawyer and financial advisor job security act of 2017.

The [pass-through] deduction leaves a gaping hole in the tax code, and the goal by the end of the presentation today is to make you guys the bus drivers, or the truck drivers, to drive right through that hole with your clients. [33]

Similarly, the 2017 tax law’s corporate tax cuts create opportunities for more tax gaming. By slashing the corporate rate from 35 percent to 21 percent, it opened a wide gap between the top individual tax rate and the corporate rate, inviting wealthy filers to shelter income in corporations.[34]

While there is a difference between lawful tax avoidance and unlawful tax evasion, complex and lucrative provisions like the pass-through deduction create an incentive for well-resourced taxpayers to push that boundary, and the depletion of the IRS gives them more leeway to do so.

High-Income Role in Tax Gap Likely Even Greater Than Understood

Tax gap estimates are based on a sample of audit data, but limitations in these data may understate the contribution of large businesses and wealthy households to the tax gap in a few ways:

- The “precipitous decline in both the number and thoroughness of large corporation audits means that estimates of the ‘tax gap’ attributable them may be an understatement,” a former IRS Office of Research economist and Taxpayer Advocate Service researcher has warned.[35]

- The most recent tax gap estimates use data from 2011 to 2013 — when audit rates were higher and so may have better deterred tax non-compliance. In addition, the ability of well-resourced filers to push the boundary between tax evasion and avoidance when audited may lead to underestimates of the size of the tax gap.

- Also, estimates of the amount of the tax gap that’s attributable to the top 1 percent of filers are based on audit and tax return data, which may understate tax misreporting because many sources of income of wealthy filers do not have to be reported in tax returns or may be hidden by the well-resourced, even in an audit.[36]

- The difficulty of tracing ownership of pass-throughs, specifically partnerships, even with IRS data may mean that their contribution to the tax gap is understated.[37]

Further, the regularity and depth of reporting on different parts of the tax gap is uneven. There are annual, detailed reports on the sources of EITC errors, as required by statute and regulation. But IRS reporting on the tax gap is part of its voluntary research program, with stretches of four or six years between reports, and these reports give far less detail about large sources of the tax gap. The last tax gap report, for example, uses data from 2011 to 2013, so it does not address recent compliance concerns such as cryptocurrency. Nor does it address the extent to which foreign tax evasion, such as Americans’ sheltering of their income in foreign bank accounts, contributes to the tax gap. As the Government Accountability Office recently reported, the “IRS does not have an estimate of the revenue loss due to offshore noncompliance. However, international tax policy experts believe that the losses are in the billions of dollars annually.”[38]

The Fiscal Absurdity of Underfunding Enforcement

The Congressional Budget Office estimates that adding $20 billion to the IRS enforcement budget over ten years would generate more than $55 billion in revenue, so the net savings would exceed $35 billion.[39] And, as the Treasury Department notes, such estimates include only the revenue that the IRS would directly recover. There would likely be large added savings because more enforcement would deter some non-compliance.[40]

Unfortunately, the 2020 appropriations level for the IRS as a whole did not even keep pace with inflation. For just enforcement funding, there was an inflation-adjusted increase, but it was less than 1 percent (see Figure 5). So, the budget agreement left on the table billions of dollars of federal revenue that additional enforcement dollars could secure.

Building on Bipartisan Support for Restoring Adequate Enforcement

As a reasonable initial goal, lawmakers should at least return the IRS budget to its funding levels of 2010, adjusted for inflation, because that’s when the deep cuts in IRS funding began.[41] But IRS enforcement is now so depleted, with 31 percent fewer staff than in 2010, that there are practical limits to how much restored funding and staff the IRS can absorb immediately. Existing staff will likely need to take time away from auditing and other duties to help hire and train new staff. The accelerated loss of senior enforcement staff due to retirement has further weakened IRS capacity, so building staff numbers back up to 2010 levels will come on top of the need to replace greater numbers of retiring staff.

This means that IRS funding will need to be restored gradually over a number of years. Such rebuilding requires a multi-year funding commitment because the IRS must hire and train a significant number of auditors and other staff, which requires time and some funding certainty. This is particularly important for addressing plummeting audit rates among the highest-income individuals and the most complex returns because, as noted above, experienced Revenue Agents must conduct those audits. As Commissioner Rettig noted, “in the longer-term, Congress must fund and the IRS must hire and train appropriate numbers of [Revenue Agents] to have appropriately balanced [audit] coverage across all income levels.”[42] To plan for and implement an orderly rebuilding, the IRS will also need confidence that lawmakers will sustain the added funding.

Promisingly, there is some bipartisan recognition that more IRS enforcement funding is needed, that it should involve a multi-year commitment, and that a special budget mechanism could help provide both. Last year the Trump Administration and the House both proposed multi-year increases in IRS enforcement funding under a special budget mechanism that would have helped protect the funding from competition with other discretionary funding priorities.[43] The final budget deal did not include these proposals, but lawmakers can nevertheless build on them and pursue other budget mechanisms that recognize the special nature of IRS enforcement funding (namely, the fact that it generates budget savings). Further, the President and Congress came together last year on a bipartisan basis to enact the Taxpayer First Act of 2019, which aimed to modernize and improve the IRS, which may increase lawmakers’ confidence in funding rebuilding of the IRS.

As the IRS National Taxpayer Advocate has noted, increased funding for operations support and customer services (such as handling taxpayer calls and correspondence) is a necessary complement to restoring enforcement funding, since increased enforcement would place greater demands service and operations budgets that are already stretched. For example, in fiscal year 2019, telephone assistors answered only about 29 percent of phone calls to the IRS.[44]

Lawmakers and the IRS can also take a number of steps to rebalance compliance activity. Restored IRS funding should go first to restoring compliance activity where it has fallen off most steeply and to addressing the largest sources of the tax gap. For example, one study found that an efficient use of restored enforcement funding would be to hold audit rates fixed for filers making less than $200,000 while focusing new resources on enforcement among high-income and high-wealth individuals and corporations.[45] The largest sources of the tax gap, such as underreported pass-through income, should also receive proportionately large research attention. Lawmakers and the IRS should prioritize improving the regularity, depth, and quality of tax gap estimates and associated research into the largest sources of tax non-compliance.

As for addressing EITC errors, Congress should focus on the causes of those errors, such as by requiring paid preparers to meet basic standards of competency and oversight as Presidents Trump and Obama have both proposed,[46] rather than simply allowing EITC filers to become a greater and greater share of audits.[47]

National Needs Require Tax Policy That Raises Revenue, Boosts Workers’ and Families’ Incomes, and Safeguards the Integrity of the Tax System

My testimony, together with that of Professors Furman and Kysar, shows that the 2017 tax law, its implementing regulations, and a decade of damage to the IRS are combining to deliver large tax cuts to profitable corporations, large pass-throughs, and the already well-to-do, including tax avoiders and evaders. This combination is problematic not only for low- and moderate-income workers and their families but for the nation as a whole.

As a share of the economy, federal revenue is now at its lowest level in half a century (other than immediately after a recession), even as more baby boomers retire and become eligible for Social Security, Medicare, and Medicaid. Climate change demands attention, and a raft of needs for investment in physical infrastructure and human capital remains unmet.[48]

There is also little broadly shared benefit to show for the 2017 law. It has not substantially reduced profit shifting offshore or other forms of tax avoidance, as Professor Kysar’s testimony notes. Instead, it has created a raft of new tax gaming opportunities through provisions like the pass-through deduction and through generous regulations.[49] Workers and families saw far less from the law than the well-off: it will boost the after-tax incomes of households in the top 1 percent by 2.9 percent by 2025, roughly three times the 1.0 percent gain for households in the bottom 60 percent, the Tax Policy Center estimates.[50] Promises that provisions like the corporate tax cuts would provide indirect, trickle-down benefits to low- and moderate-income households are little comfort, given the evidence set out in Professor Furman’s testimony.

To meet the nation’s most pressing needs, tax policy going forward should instead:

- Raise revenue, especially by scaling back or eliminating tax breaks that let large amounts of income from highly profitable corporations, large pass-throughs, and well-off individuals face little or no tax.[51]

- Strengthen the integrity of the tax code and tax administration to reduce tax gaming, collect taxes owed, and make the tax system fairer for honest tax filers; and

- Directly boost the incomes of low- and moderate-income workers and families who were largely left behind by the 2017 tax law, by enacting proposals to strengthen the EITC and Child Tax Credit such as those that Chairman Neal and other members of the Committee have advanced.[52]

Thank you for the opportunity to testify today. I welcome any questions you might have.

End Notes

* This testimony draws heavily on prior work by the author and CBPP, cited below.

[1] Internal Revenue Service, “SOI Tax Stats – IRS Data Book,” Table 9a, updated December 19, 2019, https://www.irs.gov/statistics/soi-tax-stats-irs-data-book.

[2] Taxpayer Advocate Service, “Annual Report to Congress,” 2019, p. 23, https://taxpayeradvocate.irs.gov/2019AnnualReport.

[3] More recent IRS data show that the individual audit rate has continued falling, reaching 0.45 percent in 2019. However, comparable data for income groups and corporations are not yet available. Internal Revenue Service, “IRS Progress Update FY2019,” 2019, p. 25, https://www.irs.gov/pub/irs-pdf/p5382.pdf.

[4] Total positive income.

[5] Internal Revenue Service, “Federal Tax Compliance Research: Tax Gap Estimates for Tax Years 2011–2013,” https://www.irs.gov/pub/irs-pdf/p1415.pdf.

[6] Natasha Sarin, Lawrence H. Summers, and Joe Kupferberg, “Tax Reform for Progressivity: A Pragmatic Approach,” Hamilton Project, https://www.hamiltonproject.org/assets/files/SarinSummers_LO_FINAL.pdf.

[7] John A. Koskinen, “Prepared Remarks of John A. Koskinen,” Tax Policy Center, April 8, 2015, p. 2, https://www.urban.org/sites/default/files/publication/49026/2000180-prepared-remarks-of-irs-commissioner-before-tpc.pdf.

[8] Samantha Jacoby, “Policymakers Should Ensure Pass-Throughs Pay More of Taxes They Owe,” Center on Budget and Policy Priorities, November 22, 2019, https://www.cbpp.org/blog/policymakers-should-ensure-pass-throughs-pay-more-of-taxes-they-owe.

[9] Letter from Charles P. Rettig to Senator Ron Wyden, September 6, 2019, pp. 4-5, footnote 1, https://www.documentcloud.org/documents/6430680-Document-2019-9-6-Treasury-Letter-to-Wyden-RE.html. Also see Internal Revenue Service, “SOI Tax Stats – IRS Data Book,” Table 9a, updated December 19, 2019, https://www.irs.gov/statistics/soi-tax-stats-irs-data-book. The 2019 Taxpayer Advocate Service report to congress suggests that Revenue Agent staffing has continued to fall, with a 39 percent decline between 2010 and 2019. Taxpayer Advocate Service, “IRS FUNDING: The IRS Does Not Have Sufficient Resources to Provide Quality Service,” 2019, p. 27 https://taxpayeradvocate.irs.gov/Media/Default/Documents/2019-ARC/ARC19_Volume1_MSP_03_IRSFUNDING.pdf. The number of Revenue Officers, who collect money owed, dropped by 50.4 percent over the same period.

[10] Internal Revenue Service, “SOI Tax Stats – IRS Data Book,” Table 9a, op. cit.

[11] See, for example: Paul Kiel, “The IRS Decided to Get Tough Against Microsoft. Microsoft Got Tougher.” ProPublica, January 22, 2020, https://www.propublica.org/article/the-irs-decided-to-get-tough-against-microsoft-microsoft-got-tougher; Paul Kiel, “Who’s Afraid of the IRS? Not Facebook,” ProPublica, January 23, 2020, https://www.propublica.org/article/whos-afraid-of-the-irs-not-facebook.

[12] Jesse Eisinger and Paul Kiel, “After Budget Cuts, the IRS’ Work Against Tax Cheats Is Facing ‘Collapse,’” ProPublica, October 1, 2018, https://www.propublica.org/article/after-budget-cuts-the-irs-work-against-tax-cheats-is-facing-collapse.

[13] Jesse Eisinger and Paul Kiel, “You Can’t Tax the Rich Without the IRS,” ProPublica, May 3, 2019, https://www.propublica.org/article/you-cant-tax-the-rich-without-the-irs-internal-revenue-service.

[14] OECD and The World Bank, “Improving Co-operation between Tax Authorities and Anti-Corruption Authorities in Combating Tax Crime and Corruption,” 2018, https://www.oecd.org/tax/crime/improving-co-operation-between-tax-authorities-and-anti-corruption-authorities-in-combating-tax-crime-and-corruption.pdf.

[15] Currently there are 631 such corporations.

[16] IRS, “LB&I Announces Large Corporate Compliance Program,” May 16, 2019, https://www.irs.gov/newsroom/lbi-announces-large-corporate-compliance-program.

[17] Kiel, “Who’s Afraid of the IRS? Not Facebook.”

[18] Internal Revenue Service, “SOI Tax Stats – IRS Data Book,” Table 9a, op. cit.

[19] Internal Revenue Service, “Federal Tax Compliance Research: Tax Gap Estimates for Tax Years 2011–2013,” op. cit.

[20] Michael Cooper et al., “Business in the United States: Who Owns It and How Much Tax Do They Pay,” Office of Tax Analysis, October 2015, https://www.treasury.gov/resource-center/tax-policy/tax-analysis/Documents/WP-104.pdf.

[21] Treasury Inspector General for Tax Administration, “Billions of Dollars of Nonfiler Employment Taxes Went Unassessed in the Automated 6020(b) Program Due Primarily to Resource Limitations,” September 16, 2019, https://www.treasury.gov/tigta/auditreports/2019reports/201930069_oa_highlights.html.

[22] Andrew Johns and Joel Slemrod, “The Distribution of Income Tax Noncompliance,” National Tax Journal, Vol. 63, No. 3, September 2010, https://assets.documentcloud.org/documents/5219189/The-Distribution-of-Tax-Noncompliance.pdf.

[23] Sarin, Summers, and Kupferberg, p.330, op. cit.

[24] Jesse Eisinger and Paul Kiel, “The IRS Tried to Take on the Ultrawealthy. It Didn’t Go Well.” ProPublica, April 5, 2019, https://www.propublica.org/article/ultrawealthy-taxes-irs-internal-revenue-service-global-high-wealth-audits.

[25] “Testimony of The Honorable J. Russell George Treasury Inspector General for Tax Administration before the Committee on Appropriations, Subcommittee on Financial Services and General Government,” U.S. House of Representatives, September 26, 2019, https://www.treasury.gov/tigta/congress/congress_09262019.pdf.

[26] Internal Revenue Service, “Federal Tax Compliance Research: Tax Gap Estimates for Tax Years 2011–2013,” op. cit. The EITC contribution to the gross tax gap over 2011-2013 was $27 billion annually, which is 6 percent of the $441 billion gross tax gap and 8 percent of the $352 billion underreporting tax gap (the latter figure is most comparable to the top 1 percent share, which is calculated as a share of the underreporting tax gap).

[27] Congressional Budget Office, “Options for Reducing the Deficit: 2019-2028,” December 2018, p. 307, https://www.cbo.gov/system/files/2019-06/54667-budgetoptions-2.pdf.

[28] Rettig, p. 1, op. cit. A correspondence examination costs the IRS approximately $150.

[29] See, for example: Kiel, “The IRS Decided to Get Tough Against Microsoft. Microsoft Got Tougher;” Kiel, “Who’s Afraid of the IRS? Not Facebook.”.

[30] Taxpayer Advocate Service, “Annual Report to Congress,” February 2018, Vol. 1, https://taxpayeradvocate.irs.gov/Media/Default/Documents/2018-ARC/ARC18_Volume1.pdf.

[31] Paul Kiel and Hannah Fresques, “Where in The U.S. Are You Most Likely to Be Audited by the IRS?” ProPublica, April 1, 2019,” https://projects.propublica.org/graphics/eitc-audit. Presenting estimates from Kim M. Bloomquist, “Regional Bias in IRS Audit Selection,” Tax Notes Federal, March 19, 2019. For further discussion of geographic and racial implications of these audit rate trends, see Chye-Ching Huang and Roderick Taylor, “How the Federal Tax Code Can Better Advance Racial Equity,” Center on Budget and Policy Priorities, July, 25, 2019, https://www.cbpp.org/research/federal-tax/how-the-federal-tax-code-can-better-advance-racial-equity.

[32] See Chuck Marr, “JCT Highlights Pass-Through Deduction’s Tilt Toward the Top,” Center on Budget and Policy Priorities, April 24, 2018, https://www.cbpp.org/blog/jct-highlights-pass-through-deductions-tilt-toward-the-top.

[33] Emily Horton, “Tax Planner: Drive Wealthy Clients Through ‘Gaping Hole’ in Tax Code,” Center on Budget and Policy Priorities, May 31, 2018, https://www.cbpp.org/blog/tax-planner-drive-wealthy-clients-through-gaping-hole-in-tax-code.

[34] For a further of the ways that the 2017 tax law encourages tax gaming, see Chuck Marr, Brendan Duke, Chye-Ching Huang, “New Tax Law Is Fundamentally Flawed and Will Require Basic Restructuring,” Center on Budget and Policy Priorities, August 14, 2018, https://www.cbpp.org/federal-tax/fundamentally-flawed-2017-tax-law-largely-leaves-low-and-moderate-income-americans; and David Kamin et al., “The Games They Will Play: An Update on the Conference Committee Tax Bill,” December 18, 2017, https://ssrn.com/abstract=3089423.

[35] Kim M. Bloomquist, “The Tax Gap: Holding Steady or Missing in Action?” Tax Notes Federal, October 28, 2019, https://www.taxnotes.com/tax-notes-federal/information-reporting/tax-gap-holding-steady-or-missing-action/2019/10/28/2b1p7.

[36] Sarin, Summers, and Kupferberg, p.330, op. cit.

[37] Michael Cooper et al., op. cit.

[38] Government Accountability Office, “Foreign Asset Reporting: Actions Needed to Enhance Compliance Efforts, Eliminate Overlapping Requirements, and Mitigate Burdens on U.S. Persons Abroad,” GAO-19-180, April 2019, https://www.gao.gov/assets/700/698133.pdf.

[39] Congressional Budget Office, op. cit.

[40] Office of Management and Budget, “The Appendix, Budget of the United States Government, Fiscal Year 2017: Department of the Treasury,” p. 1047, https://obamawhitehouse.archives.gov/sites/default/files/omb/budget/fy2017/assets/tre.pdf.

[41] This should be only an initial goal. Since 2010 the number of returns filed has grown 9 percent, and the IRS has been asked to implement and enforce new regimes including under the Foreign Account Tax Compliance Act, the Affordable Care act, and the 2017 tax law.

[42] Rettig, p. 4, op. cit.

[43] Specifically, both proposed discretionary cap adjustments. See Chuck Marr, “Senate Should Pave Way for Rebuilding IRS Enforcement,” Center on Budget and Policy Priorities, August 1, 2019, https://www.cbpp.org/blog/senate-should-pave-way-for-rebuilding-irs-enforcement.

[44] Taxpayer Advocate Service (2019), op. cit.

[45] Sarin, Summers, and Kupferberg, p.330, op. cit.

[46] Robert Greenstein, John Wancheck, and Chuck Marr, “Reducing Overpayments in the Earned Income Tax Credit,” Center on Budget and Policy Priorities, January 31, 2019, https://www.cbpp.org/research/federal-tax/reducing-overpayments-in-the-earned-income-tax-credit.

[47] Ibid.

[48] Paul N. Van de Water, “2017 Tax Law Heightens Need for More Revenues,” Center on Budget and Policy Priorities, November 15, 2018, https://www.cbpp.org/research/federal-tax/2017-tax-law-heightens-need-for-more-revenues.

[49] Samantha Jacoby, “Corporation-Friendly Treasury Regulations Reducing Federal Revenues,” Center on Budget and Policy Priorities, February 6, 2020, https://www.cbpp.org/research/federal-tax/corporation-friendly-treasury-regulations-reducing-federal-revenues; Samantha Jacoby, “Pass-Through Deduction Regulations Reflect Industry Lobbying,” Center on Budget and Policy Priorities, January 30, 2019, https://www.cbpp.org/blog/pass-through-deduction-regulations-reflect-industry-lobbying; Samantha Jacoby, “Final Opportunity Zone Rules Could Raise the Tax Break’s Cost,” Center on Budget and Policy Priorities, February 3, 2020, https://www.cbpp.org/blog/final-opportunity-zone-rules-could-raise-tax-breaks-cost.

[50] TPC Table T17-0314. The year 2025 is when the law will be fully phased in but before many of its provisions are scheduled to expire. The distribution is roughly similar in Tax Policy Center tables for 2018. The law is even more tilted to the top in 2027, when most of the individual provisions have expired.

[51] Chuck Marr, Samantha Jacoby, and Kathleen Bryant, “Substantial Income of Wealthy Households Escapes Annual Taxation Or Enjoys Special Tax Breaks,” Center on Budget and Policy Priorities, November 13, 2019, https://www.cbpp.org/research/federal-tax/substantial-income-of-wealthy-households-escapes-annual-taxation-or-enjoys.

[52] Chuck Marr et al., “Working Families Tax Relief Act Would Raise Incomes of 46 Million Households, Reduce Child Poverty,” CBPP, April 10, 2019, https://www.cbpp.org/research/federal-tax/working-families-tax-relief-act-would-raise-incomes-of-46-million-households; and Chuck Marr, Yixuan Huang, and Vincent Palacio, ”House Ways and Means Committee Legislation Would Expand EITC and Child Tax Credit,” CBPP, updated July 2, 2019, https://www.cbpp.org/research/federal-tax/house-ways-and-means-committee-legislation-would-expand-eitc-and-child-tax.

More from the Authors