BEYOND THE NUMBERS

Raising Social Security’s Retirement Age Cuts Benefits for All Retirees

Some policymakers, including prominent presidential candidates, have endorsed raising Social Security’s full retirement age to improve the program’s long-term solvency. Raising the retirement age cuts benefits for all retirees, the cuts could be deep, and they would fall hardest on lower- and middle-income Americans — who rely heavily on their hard-earned Social Security and have not shared equally in recent life expectancy gains.

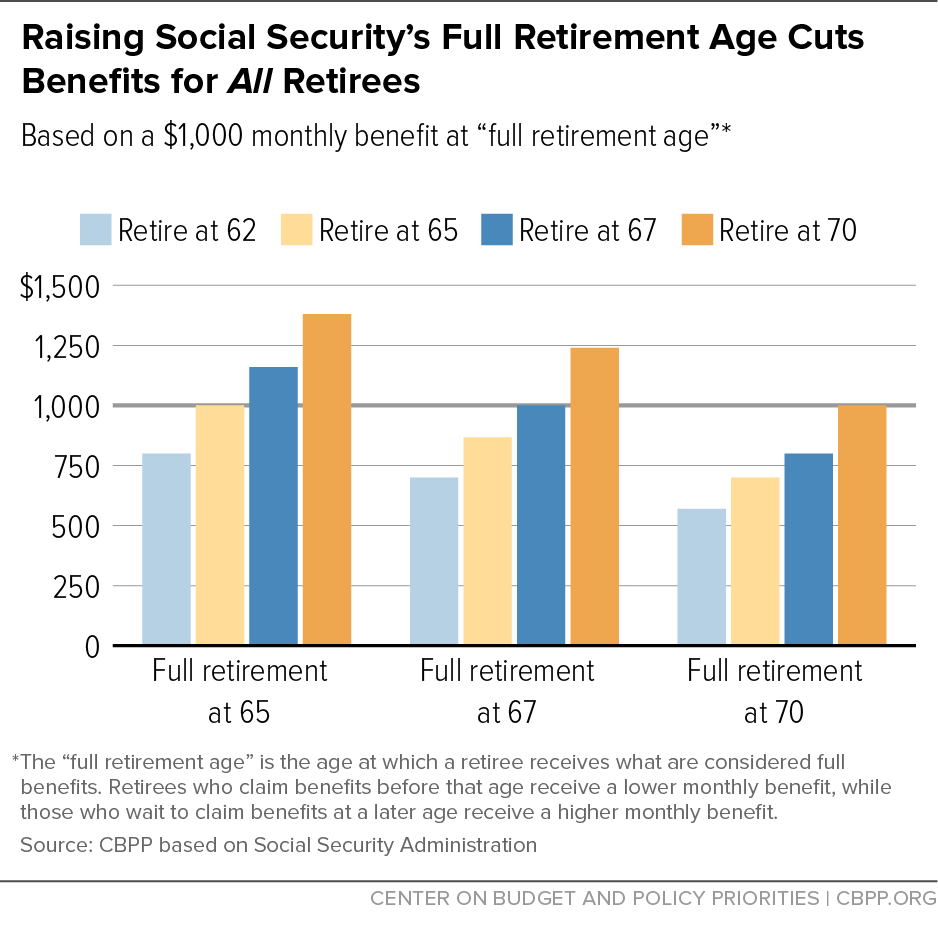

The full retirement age is the age at which retirees can receive full Social Security benefits. If you claim benefits before full retirement age, you receive permanently reduced monthly benefits; if you claim them after, you get a permanent increase. The full retirement age was 65 for most of Social Security’s history. The last major Social Security overhaul, in 1983, gradually raised it to 66 (where it stands now) and will eventually raise it to 67, a change that effectively cuts benefits by 13 percent. There’s talk of moving the age further to 68, 69, or 70. Such a change would have significant effects.

- Raising the retirement age means cutting benefits — no matter when you file. A higher retirement age means that an early retiree gets a deeper reduction and a delayed retiree gets a smaller bonus. If the age rose from 67 to 68, monthly benefits would fall by about 7 percent, for all new retirees. If it rose to 70, the cuts would be nearly 20 percent. (See graph. For more information, see the box, “Why Does Raising the Retirement Age Reduce Benefits?” here.)

- Most people claim early, which means they could receive as little as half their full benefit. Nearly half of retirement beneficiaries claim benefits at age 62. Some of these beneficiaries — especially those with lower earnings — are in poor health but don’t meet the stringent criteria for disability benefits. If the retirement age were 70, a retiree at age 62 would receive only 57 percent of his or her full monthly benefit.

- Low-income people don’t live as long as high-income people — and the gap is widening. Supporters of retirement age increases often point to increasing longevity. And that’s true — for some people. Average life expectancies are rising, but the gains are mostly among higher-income Americans. Life expectancy for the bottom half of earners has barely changed over the past 30 years.

- Retirement age increases hit the pocketbooks of workers with low and moderate incomes hardest. Though raising the retirement age cuts everyone’s benefits roughly equally, it affects incomes unequally. That’s because Social Security benefits make up a greater share of income for low- to middle-income retirees, as well as for minorities.

{kind=link}

{kind=link}