BEYOND THE NUMBERS

Policymakers must replenish Social Security’s disability fund by late 2016 to prevent a one-fifth cut in benefits. A proposal from Rep. Xavier Becerra, the top Democrat on the House Ways and Means Subcommittee on Social Security, would obviate the need by folding the Disability Insurance (DI) Trust Fund into the much larger Old-Age and Survivors Insurance (OASI) fund. Merging the trust funds is a reasonable idea that's been around for years, and lawmakers should seriously consider it.

A separate DI trust fund wasn’t fiscally necessary. The Senate insisted on it when designing the disability program as part of Social Security’s 1956 Amendments, and the House acquiesced. Lawmakers have enacted other benefit expansions — such as dependent and survivor benefits, which weren’t part of the original 1935 Social Security Act but were added in 1939; early-retirement benefits, added in 1956; and benefits for disabled widows and widowers over age 50, added in 1967 — without creating a separate fund.

The government can pay disabled-worker benefits from a single, commingled trust fund while continuing to track those costs separately. That’s what the trustees’ report does, for example, with benefits for disabled widow(er)s and disabled adult children — two groups whose benefits are paid (mostly) from the OASI fund.

Having two separate trust funds means that policymakers occasionally need to reallocate taxes between them. That’s a traditional act that Congress has taken 11 times, in six separate measures — and in both directions. Policymakers wouldn’t need to, however, if there were a single fund.

This isn’t a new idea. The 1979 Advisory Council on Social Security, for example, unanimously recommended merging the two trust funds but retaining separate cost analyses.

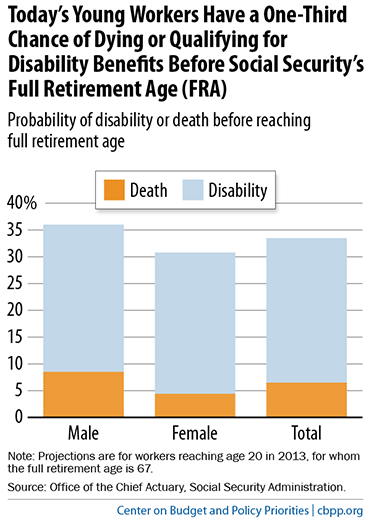

Disability benefits are an essential part of Social Security — today’s young workers have roughly a one-third chance of becoming disabled or dying before they reach full retirement age — and are closely integrated with the retirement program. Both funds face fairly similar long-run shortfalls, and key features — including the tax base, the work history required to become insured for benefits, the benefit formula, and cost-of-living adjustments — are similar or identical. And there’s overlap in the people they serve; most DI recipients are close to or even past Social Security’s early-retirement age.

Policymakers should strengthen both the disability and retirement programs by addressing overall Social Security solvency. Breaking down the artificial distinction between two separate trust funds would help them focus on that goal.

{kind=link}