Senate Health Bill Waivers Would Undermine Key Consumer Protections for People with Pre-Existing Conditions

Bill Would Cut Coverage, Raise Costs Even Without Cruz Amendment

With President Trump encouraging Senate Republicans to push forward with their plan to “repeal and replace” the Affordable Care Act (ACA), the Senate may again consider a revised version of the GOP bill, which includes the so-called “Cruz amendment” that would allow insurers to offer plans that could exclude people or charge them higher premiums if they have pre-existing medical conditions, or a version of the bill without that amendment.[1] While some Senate Republicans have claimed that the bill would protect people with pre-existing conditions even with the Cruz amendment included, health insurers, patient advocates, and other experts have debunked that assertion.[2] But even if the amendment is dropped or significantly modified, the Senate bill would still significantly scale back coverage and increase out-of-pocket costs for people with substantial medical needs.

The core Senate bill would let insurers exclude crucial services from their plans and dramatically raise deductibles and other out-of-pocket costs. That’s because the core Senate bill would let insurers exclude crucial services from their plans and dramatically raise deductibles and other out-of-pocket costs. It would do this by broadening an existing federal waiver option under the ACA to give states near-automatic approval to eliminate or weaken virtually all consumer protections and standards related to how health insurance plans are designed in the individual and small-group markets. These changes would also adversely affect people with large employer plans by allowing insurers to reinstitute annual and lifetime coverage limits for these plans.

Vice President Pence recently claimed, “The legislation ensures that every American with preexisting conditions has access to the coverage and care they need, no exceptions.”[3] Even without the Cruz amendment, the Senate Republican bill blatantly violates that standard, because:

- Many plans would exclude services that people with pre-existing conditions need. According to the Congressional Budget Office (CBO), about half of the U.S. population lives in states that would use the Senate bill’s waivers to weaken or eliminate the essential health benefits (EHB) standards that require plans in the individual and small-group insurance markets to cover a comprehensive set of health benefits.[4] CBO predicted that in states with essential health benefit waivers, mental health services, maternity care, and treatment for substance use disorders would be among the services most frequently excluded from coverage.[5] That alone would leave many people — especially those who have pre-existing conditions — without access to the benefits they need at an affordable price. (Notably, behavioral health conditions — including mental health conditions and substance use disorders — are among the most common pre-existing conditions.[6])

- People with pre-existing conditions could be on the hook for catastrophic out-of-pocket costs, even for the services their plan covers. In addition to allowing states to weaken or eliminate EHBs, the bill would let insurers charge people unlimited deductibles and other cost-sharing by eliminating the annual out-of-pocket limit of roughly $7,000 a year that’s in place today.

- The bill’s cuts to subsidies would also disproportionately affect people with costly pre-existing conditions. As a result of these cuts, typical deductibles would increase from less than $1,000 to more than $6,000 for lower-income marketplace consumers, and from about $3,000 to more than $6,000 for others. These changes are most costly for people with pre-existing conditions, who are more likely to have to spend the entire deductible amount year after year.

All told, the Senate bill would leave many individuals unable to find affordable, comprehensive coverage that meets their needs, thus effectively eliminating many of the ACA’s protections for people with pre-existing conditions.

Senate Bill Uses 1332 Waivers to Roll Back Benefit Design Requirements

The Senate bill would allow states to make sweeping plan design changes by broadening an existing waiver, known as a section 1332 or “state innovation waiver.” Established by the ACA, this waiver permits states to modify, with approval from the Department of Health and Human Services (HHS), a number of ACA provisions, including those related to the health insurance marketplaces, the premium tax credits people can obtain through the marketplaces, the essential health benefits, and protections against high out-of-pocket costs.

As part of the 1332 waiver process, states can also apply to receive federal “pass-through” funding — the funding the federal government would have spent in marketplace subsidies on the state’s residents in the absence of the waiver. For example, if the state uses a 1332 waiver in a way that reduces federal spending on premium tax credits, the state could recapture that funding and use it for other purposes, including activities unrelated to health care.

But under current law, the federal government is only allowed to approve a 1332 waiver if a state demonstrates that the waiver is expected to:

- Provide coverage that’s as comprehensive as what’s otherwise provided under marketplace plans;

- Provide coverage and cost-sharing protections that are as affordable as under the ACA;

- Provide coverage to at least a comparable number of people in the state; and

- Not increase the federal deficit.

These four guardrails help protect against drastic reductions in benefit standards through 1332 waivers or reductions in financial assistance for low-income people that would result in fewer people with health coverage.[7] For example, it wouldn’t be possible for a state to show under the current rules that coverage would be as comprehensive or as affordable under a 1332 waiver that removes a number of services from the EHB definition. The guardrails also help encourage states that get a waiver to use any pass-through funding to shore up coverage and affordability for their residents.

The Senate bill, however, would eliminate the first three guardrails, allowing waivers to be approved even if they reduce the comprehensiveness or affordability of coverage or increase the number of uninsured people in the state. The Senate bill would also require the HHS Secretary to approve any waiver a state proposes, as long as the waiver doesn’t add to the federal deficit. In addition, it would allow a state to use the pass-through funding it would receive under the waiver for purposes other than health care, which CBO confirmed would occur in some states. (Thus, the waivers would result in more uninsured people).[8]

All told, these changes would mean that if a state wanted to redefine or even eliminate the essential health benefits, it could do so, even if the result is coverage that’s less comprehensive for enrollees. Under the Senate bill as drafted, the federal government generally could not block such an effort, a staggering shift that would fail to ensure states are accountable for how they spend taxpayer dollars intended to make coverage more affordable and extend health coverage to the uninsured.[9]

Changes Proposed by Senator Ted Cruz Would Only Increase the Senate Bill’s Harm to People with Medical Conditions

Senator Ted Cruz has proposed modifying the Senate bill to allow any insurer that offers at least one plan that complies with the ACA’s market reforms and consumer protections to also sell other plans in the individual market that do not comply with these standards (“Consumer Freedom” plans). One of the primary effects of the Cruz amendment, relative to the Senate bill, would be to permit insurers to deny “Freedom” plan coverage to people with pre-existing medical conditions, to charge them a higher premium based on their health status, to exclude coverage of a pre-existing condition, or to impose a waiting period. This would segment the insurance market into separate healthy and unhealthy enrollee risk pools.

People who are healthier would enroll overwhelmingly in the “Freedom” plans — which would have lower premiums because the plans could deny coverage or charge much higher rates to people with medical conditions, plus exclude coverage for various costly services. This segmentation of the insurance market into separate healthy and unhealthy enrollee risk pools, a dynamic known as adverse selection, would have serious consequences for the ACA-compliant plans, driving up their premiums to levels that would likely be unaffordable for many people with pre-existing conditions. While people with pre-existing conditions technically would still be able to purchase such plans, in practice the cost would shut out many people with incomes above 350 percent of the poverty line, who wouldn’t be eligible for tax credits under the Senate bill.

And while people below that income level would receive tax-credit subsidies to help them afford their premiums for compliant plans, the Senate bill’s subsidies are tied to premium costs for bronze plans, which have deductibles of $6,000 or more. Someone who wanted to buy a plan with a more reasonable deductible would pay far more under the Cruz amendment. Particularly hurt by the Cruz amendment would be unsubsidized people in their 50s and 60s, most of whom have pre-existing medical conditions and who already would be paying far more in premiums under the Senate bill due to age-rating.

Many questions remain about the Cruz amendment, including whether some form of it will ultimately be included in the Senate Republican bill. Even if it isn’t, the underlying Senate bill would have serious harmful impacts on people with pre-existing medical conditions.

Margot Sanger-Katz, “Ted Cruz Has an Idea for How to Cover High-Risk Patients,” The Upshot, New York Times, July 5, 2017, https://www.nytimes.com/2017/07/05/upshot/ted-cruz-has-an-idea-for-how-to-cover-high-risk-patients.html. Lueck, op cit.

Senate Waivers Would Prompt Widespread Weakening of Plan Protections

Allowing states to waive EHBs and protections against high out-of-pocket costs might seem different from repealing these federal protections for people with pre-existing conditions altogether. But in fact, under the Senate Republican proposal, states would likely face heavy pressure to take such waivers, and many would do so.

Prior to the ACA, states were free to adopt ACA-like protections for people with health conditions, but few did. Robust protections for people with pre-existing conditions weren’t sustainable for states without the other key elements of the ACA structure: an individual mandate that people obtain health coverage or pay a penalty and robust subsidies that keep individual market premiums, deductibles, and other out-of-pocket costs affordable.

The Senate health care bill would eliminate the individual mandate, which would increase premiums by an estimated 20 percent in 2018. And starting in 2020, it also would sharply cut premium subsidies and repeal cost-sharing subsidies without providing any substitute, increasing total out-of-pocket costs (premiums, deductibles, copays, and coinsurance) by thousands of dollars for millions of people. Both would have the effect of discouraging enrollment among healthier people, which would make the individual market risk pool sicker, on average. This would put considerable pressure on states to eliminate the ACA’s protections for people with pre-existing conditions and allow insurers to reinstitute harmful practices from the past, as a way to lower premiums and entice more healthy people to return to the individual market.[10]

As a result, CBO estimated that about half the U.S. population would live in states subject to 1332 waivers if the Senate bill became law.[11] CBO also predicted significant cuts in financial assistance for individual market coverage: federal spending on premium tax credits for low- and moderate-income people would drop by about one-fifth by 2026 as a result of the waivers. States might use the pass-through funding to help stabilize their insurance markets, but, as noted, the bill wouldn’t require them to do so.

Waivers Would Lead Many States to Weaken or Eliminate EHB Standard

Several different federal standards guide what benefits plans must cover and the costs that people can be charged out of pocket: the essential health benefits, the requirement to limit annual out-of-pocket spending to no more than a set amount (the out-of-pocket limit), and the requirement to offer plans that fit within specified “metal” levels with certain actuarial values.

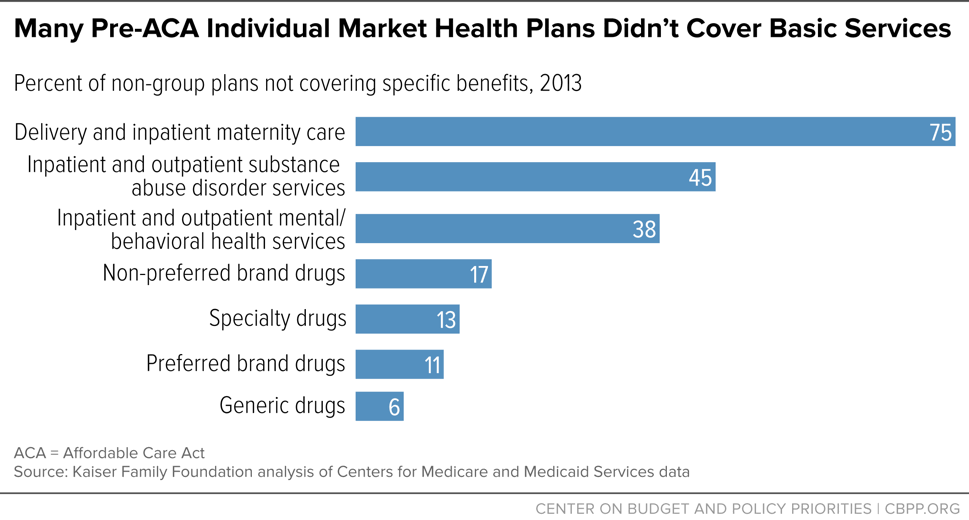

All individual and small-group health plans must cover ten EHBs: emergency services; hospitalizations; outpatient care; maternity and newborn care; mental health and substance use disorder treatment; prescription drugs; rehabilitation services; laboratory services; preventive services and chronic disease management; and pediatric care. Most people purchasing health insurance probably assume that it always covers these basic services. But before the ACA, it frequently didn’t. (See Figure 1.) In 2013, among plans in the individual market:

- 75 percent didn’t cover maternity care;

- 45 percent didn’t cover substance use treatment;

- 38 percent didn’t cover mental health services; and

- 13 percent didn’t cover specialty prescription drugs.[12]

People with Health Benefits from a Large Employer Could See Skimpier Plans Too

The elimination of federal EHB standards is also likely to harm people with large or self-insured employer plans. Under current rules and guidance, if just one state decides to waive EHBs, then large employer plans in every state could return to imposing lifetime and annual limits on coverage. As a Brookings analysis explains, that’s because the ACA’s ban on lifetime and annual limits only applies to essential health benefits, and large employers (even those that don’t have employees in multiple states) are free to decide which state’s EHB definition they want to adopt.[1] Before the ACA, 70 million people covered by large employers, including millions of children, faced lifetime limits on benefits, meaning that their health insurance coverage could end — for good — in the middle of a serious illness. Similarly, large employers are required to apply the ACA out-of-pocket limit only to benefits that are EHBs. Prior to the ACA, more than one-sixth of employer plans lacked limits on out-of-pocket spending.

Source: Matthew Fiedler, “Allowing states to define ‘essential health benefits’ could weaken ACA protections against catastrophic costs for people with employer coverage nationwide,” Brookings Institution, May 2, 2017, https://www.brookings.edu/2017/05/02/allowing-states-to-define-essential-health-benefits-could-weaken-aca-protections-against-catastrophic-costs-for-people-with-employer-coverage-nationwide/

As noted above, CBO estimates that close to half the U.S. population would be affected if states could waive or modify EHBs. A “large portion” of people would see plans “narrow the scope of the EHBs” by carving out certain services, thus making insurance plans that cover those services “extremely expensive.” If states modify EHBs to target services with high costs but relatively few users, “coverage for maternity care, mental health care, rehabilitate and habilitative treatment, and certain very expensive drugs could be at risk,” CBO wrote.[13]

Under such waivers, individual and small-group market plans in many places would likely revert to benefit packages much like what they offered before the ACA. Insurers would likely stop covering services that were no longer required as a way to discourage enrollment by sicker, costlier enrollees. Or, if plans did cover such costly treatments, they would charge exorbitant premiums because only those with pre-existing conditions would enroll in them.

For example, if insurers aren’t required to cover maternity benefits as an essential benefit, they would likely strip them out. They might then offer a “rider” so that someone could add the missing benefit. As CBO noted in its analysis of the House-passed health care bill, a maternity coverage rider could cost more than $1,000 per month, since insurers would price it with the expectation that people buying the benefit would use it. And even if insurers didn’t entirely remove a benefit, they could shift greater costs for that benefit onto the enrollees who need it, by imposing limits or higher charges under their plans, as explained below. The additional costs associated with having a pre-existing condition could be quite large, as Table 1 shows. They are higher than most individuals could pay on their own, which is why spreading the costs among a larger pool of people is important.

| TABLE 1 | ||

|---|---|---|

|

Waivers Would Leave People with Medical Conditions Bearing Higher Costs |

||

| ACA essential health benefit waived | Health condition | Extra cost |

| Maternity care | Pregnancy | $17,320 |

| Mental health and substance use disorder services | Drug dependence | $20,450 |

| Major depression | $8,490 | |

Even without waivers, the Senate bill would increase many people’s total out-of-pocket spending significantly, by increasing both their premiums and what they would have to spend on other out-of-pocket costs, including deductibles, in the individual market.[14] Premium credits in the Senate bill would be tied to a 58 percent “actuarial value” plan instead of a 70 percent plan, as is now the case. (Actuarial value is a measure of how comprehensive a plan is, and it is calculated based on how much it costs to provide the essential health benefits to a standard population. So, a 70 percent plan covers, on average, 70 percent of the cost of providing the essential benefits to a given population.) If a state stripped out certain benefits from EHB, then plans with a 58 percent actuarial value would be covering a much narrower set of costs — 58 percent of the more limited set of benefits. People in need of services that were stripped out would have to find a way to bear those costs on their own, or do without them entirely.

Weakened EHB Definition Means the Return of Annual and Lifetime Limits

Before the ACA, millions of people had health insurance that wouldn’t actually cover them if they got sick. Many plans had annual and lifetime dollar limits on coverage. The ACA fixed this by prohibiting annual and lifetime limits. But allowing states to waive the EHB standards would make these rules meaningless. That’s because the prohibition on annual and lifetime limits applies only to EHBs. So, if certain services are no longer considered EHBs, costs related to those services are not subject to the prohibition against annual and lifetime limits. That means insurers in waiver states could again cap the amount they would pay for certain services needed by a consumer with a high-cost or long-term health need such as cancer treatment. Just like before the ACA, people with health insurance would often be surprised, discovering too late that their health plan wouldn’t cover treatments they need, leaving them with staggering out-of-pocket costs — or forcing them into medical bankruptcy.

Waivers Could Be Used to Increase Enrollees’ Deductibles and Other Costs

Under the Senate bill, the other major way that insurers could pare down their plans in states with 1332 waivers would be through changes to enrollees’ out-of-pocket costs. Under 1332 waivers, states could eliminate or weaken a variety of financial protections that currently apply in the individual and small-group markets. If states chose to waive the relevant standards, plans could once again be allowed to:

- Remove or raise the cap on out-of-pocket costs, allowing plans to charge people exorbitant amounts in deductibles and other cost-sharing for the benefits that would still be covered. Today, each individual is protected from paying more than about $7,000 each year in deductibles, copayments, and other out-of-pocket costs for in-network care under their plan. Under the Senate bill, states could eliminate this requirement, or raise the cap far higher than it would otherwise be, shifting significant costs onto people who have costly illnesses. Moreover, the out-of-pocket cap (if it remained in place) wouldn’t apply to items and services that are no longer part of a state’s weakened EHB definition. In other words, an insurer could be allowed to impose a $20,000 annual out-of-pocket limit but many costly non-EHB services could be subject to unlimited deductibles and copayments. In 2013, before the ACA’s major coverage provisions took effect, more than one-third of plans offered in the individual market failed to include out-of-pocket caps that would have satisfied the ACA standard.[15]

- Eliminate the minimum standards for how comprehensive plans must be. Today, insurers can’t offer coverage in the individual or small-group market that’s less generous than “bronze” plans, which generally have deductibles of about $6,000 or more. Bronze plans (as with the other “metal” level requirements plans must satisfy under current law) are defined based on an estimate of how much of a standard population’s costs for covered health care services a given insurance plan will cover. Bronze plans cover about 60 percent of the cost of providing the EHBs, with the remaining 40 percent being covered by enrollees, in the form of deductibles, copayments, and other costs. Under the Senate bill’s version of a 1332 waiver, plans’ actuarial values could fall far below 60 percent. In other words, there would be no limit on how meager coverage would be. In 2010, more than half of individual market health plans failed to meet the minimum “bronze” standard of a 60 percent actuarial value. Many policies had AVs in the 35 to 50 percent range.[16]

- Eliminate the requirement that insurers offer lower-deductible, more comprehensive plans. Under the ACA, insurers that offer coverage through the marketplace must offer at least one “gold” plan with an 80 percent actuarial value and one “silver” plan with a 70 percent actuarial value. Without that requirement, many insurers would likely stop offering these more comprehensive plans. Or, if such plans were available, they would likely have very high, unaffordable premiums because only people with greater health care needs would be expected to purchase them. This would mean that people who have health conditions — especially chronic conditions that require ongoing checkups, regular medications, and periodic interventions — could end up spending large amounts out of pocket if they had individual or small-group coverage, assuming insurers still offer those plans at all.

Senate Bill Would Revive Pre-ACA-Style Plans — or Worse

In practice, even without the Cruz amendment, the Senate bill would likely cause plans in the individual and small-group markets to look much like they did prior to the ACA. Plans could even be somewhat less generous than what was on the market before 2014. That’s because at that time, in the vast majority of states, insurers were able to deny coverage to individuals based on health status and a number of other factors — and to charge enrollees they did accept higher premiums based on pre-existing medical conditions. Under the Senate bill as drafted, without the Cruz amendment, these practices wouldn’t be permitted. So insurers would likely design benefits to discourage enrollment by less-healthy people, to protect themselves from having to pay out very large claims, and to offer scaled-back, low-premium coverage that would attract healthier customers who cost less to cover. As a result, the Senate bill, even in the absence of the Cruz amendment, would gut existing protections for people with pre-existing conditions, leaving them without access to needed services or facing unaffordable out-of-pocket costs.

End Notes

[1] Sarah Lueck, “Cruz Amendment Would Worsen Already Harmful Senate Health Bill for People with Medical Conditions,” Center on Budget and Policy Priorities, July 12, 2017, https://www.cbpp.org/research/health/cruz-amendment-would-worsen-already-harmful-senate-health-bill-for-people-with.

[2] See, for example, https://www.scribd.com/document/353803476/Joint-AHIP-BCBSA-Consumer-Freedom-Option-Letter#fullscreen&from_embed; https://www.acscan.org/sites/default/files/National%20Documents/Groups%20letter%20on%20Cruz%20Amendment%20final%207.12.17.pdf; and Karen Politz and Anthony Damico, “Uneven Playing Field: Applying Different Rules to Competing Health Plans,” Kaiser Family Foundation, July 11, 2017, http://www.kff.org/health-reform/issue-brief/uneven-playing-field-applying-different-rules-to-competing-health-plans/.

[3] Noam N. Levey, “Obamacare Repeal Bills Could Put Coverage Out of Reach for Millions of Sick Americans,” Los Angeles Times, July 16, 2017, http://www.latimes.com/politics/la-na-pol-republicans-preexisting-conditions-20170716-story.html.

[4] Congressional Budget Office, “H.R. 1628: Better Care Reconciliation Act of 2017” June 26, 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/52849-hr1628senate.pdf.

[5] Congressional Budget Office, “H.R. 1628; American Health Care Act of 2017,” May 4, 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/hr1628aspassed.pdf.

[6] “Health Insurance Coverage for Americans with Pre-Existing Conditions: The Impact of the Affordable Care Act,” ASPE Issue Brief, January 5, 2017, https://aspe.hhs.gov/system/files/pdf/255396/Pre-ExistingConditions.pdf.

[7] Jessica Schubel and Sarah Lueck, “Understanding the Affordable Care Act’s State Innovation (“1332”) Waivers,” Center on Budget and Policy Priorities, February 5, 2015, https://www.cbpp.org/research/understanding-the-affordable-care-acts-state-innovation-1332-waivers.

[8] “Congressional Budget Office, June 26, 2017.

[9] Jason Levitis, “Changes to state innovation waivers in the Senate health bill undermine coverage and open the door to misuse of federal funds,” Brookings Institution, June 23, 2017, https://www.brookings.edu/blog/up-front/2017/06/23/changes-to-state-innovation-waivers-in-the-senate-health-bill-undermine-coverage-and-open-the-door-to-misuse-of-federal-funds/ and Nicholas Bagley, “Crazy waivers: the Senate bill invites states to gut important health insurance rules,” Vox, June 23, 2017, https://www.vox.com/the-big-idea/2017/6/23/15862268/waivers-federalism-senate-bill-essential-benefits.

[10] Aviva Aron-Dine and Tara Straw, “Senate Bill Still Cuts Tax Credits, Increases Premiums and Deductibles for Marketplace Consumers,” Center on Budget and Policy Priorities, revised June 25, 2017, https://www.cbpp.org/research/health/senate-bill-still-cuts-tax-credits-increases-premiums-and-deductibles-for.

[11] Congressional Budget Office, June 26, 2017.

[12] Gary Claxton et al., “Would States Eliminate Key Benefits If AHCA Waivers Are Enacted?” Kaiser Family Foundation, June 14, 2017, http://files.kff.org/attachment/Issue-Brief-Would-States-Eliminate-Key-Benefits-if-AHCA-Waivers-are-Enacted

[13] CBO, op cit.

[14] Aron-Dine and Straw, op cit.

[15] Julie Appleby, “Study: One-Third of Individual Plans Exceed Law’s Out-of-Pocket Cap,” Kaiser Health News, February 11, 2013, http://khn.org/news/study-one-third-of-individual-plans-exceed-laws-out-of-pocket-cap/. At that time, the out-of-pocket limit was set at about $6,300 per year.

[16] Jon R. Gabel et al., “More Than Half of Individual Health Plans Offer Coverage That Falls Short of What Can Be Sold Through Exchanges As Of 2014,” Health Affairs, originally published online May 23, 2012.

More from the Authors