Republican Leaders’ Tax Plan Would Deliver Large Tax Cuts to the Wealthiest Americans Even if It Doesn’t Cut the Top Rate

The Trump Administration and Republican congressional leaders have proposed a tax plan that includes cutting the top tax rate from 39.6 percent to 35 percent, but have left open the possibility of an additional top rate on the highest-income earners, purportedly to avoid “shift[ing] the tax burden from high-income to lower- and middle-income taxpayers.”[1] House Speaker Paul Ryan recently stated that the forthcoming version of the plan, expected to be unveiled on November 1, “will have that fourth bracket designed to make sure that we don’t have a big drop in income tax rates for high-income people.”[2]

The plan contains various other key provisions that would disproportionately benefit people at the top of the income spectrum.Yet the plan would still deliver a very large tax cut to the wealthiest households even if the top rate for very high-income individuals remained at its current 39.6 percent level, because the plan contains various other key provisions that would disproportionately benefit people at the top of the income spectrum and give many of them tax-cut windfalls.

Provisions like setting a special 25 percent rate for pass-through income (business income claimed on the owner’s individual income tax return), eviscerating the estate tax, and slashing the corporate tax rate from 35 to 20 percent all would mostly benefit the most well-off. Using Tax Policy Center (TPC) data, we provide a rough estimate of how the GOP tax plan would affect different income groups, even if the top tax rate remained at 39.6 percent applied at current-law thresholds.

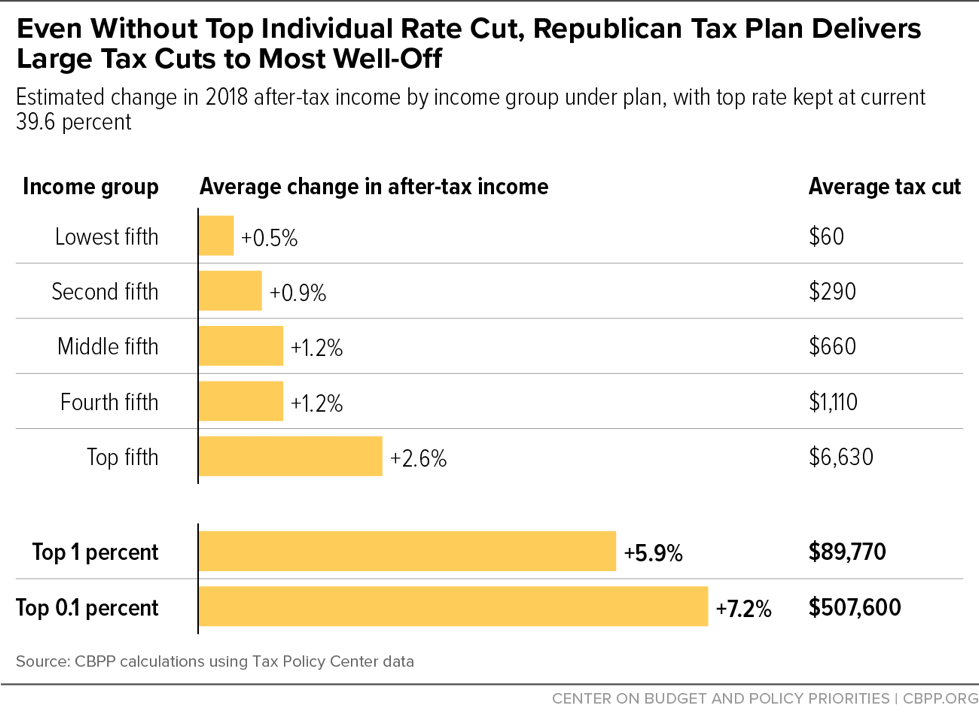

- The top 1 percent, who make above $733,000 annually, would see average tax cuts of $90,000 in 2018, increasing their after-tax incomes by 5.9 percent. (See Figure 1.) They would receive about 45 percent of the total net tax cut.[3]

- The top one-tenth of 1 percent of households — those with annual incomes exceeding $3.4 million — would receive average tax cuts of $507,000 apiece in 2018, raising their after-tax incomes by 7.2 percent in 2018.

- This 5.9 percent increase in after-tax income for the top 1 percent is five times larger than the 1.2 percent average increase in after-tax income for those in the middle fifth of the income spectrum, and more than ten times larger than the 0.5 percent income gain for the bottom fifth.

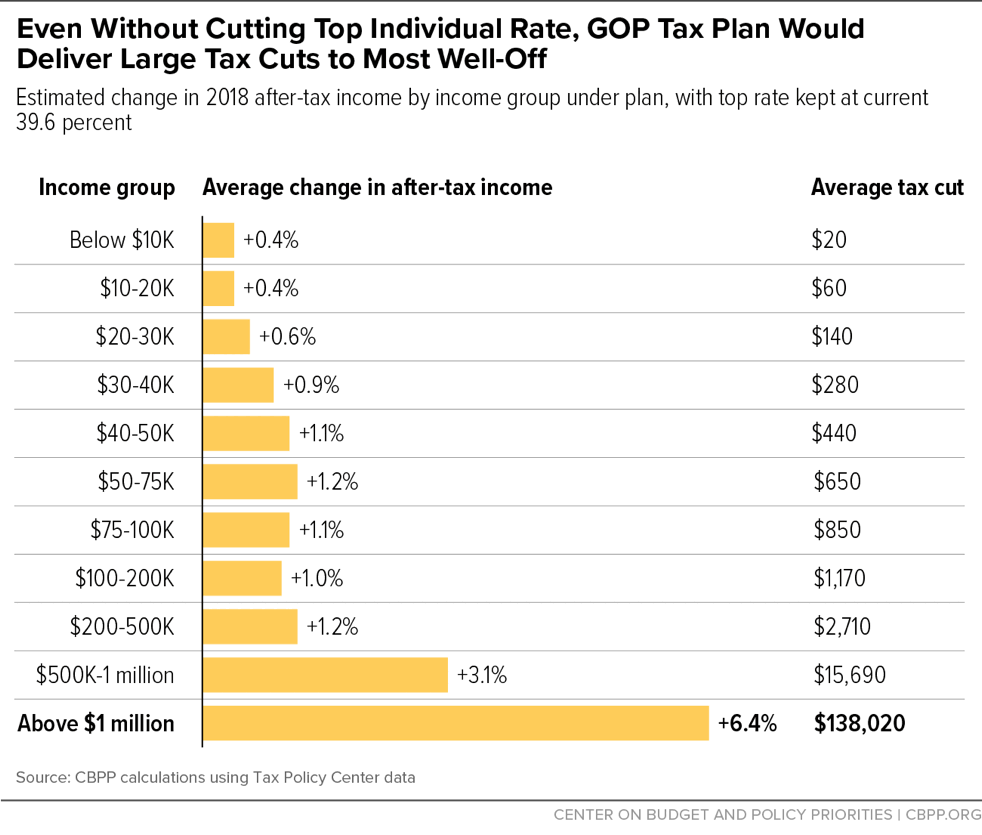

- People with annual incomes over $1 million would receive average tax cuts of $138,000 in 2018, compared to average tax cuts of $270 for households making below $75,000. Millionaires’ after-tax incomes would rise 6.4 percent in 2018, compared to a 0.9 percent increase for those making less than $75,000.

President Trump appears to recognize that those at the top of the income scale still would get large tax cuts even with a 39.6 percent top rate. An Administration official recently told a reporter that the President “basically thinks they [rich people] are fine and he believes they don’t care that much about the individual rate so long as they get all the other goodies like the corporate rate and expensing.”[4]

Only if the top rate were set significantly above the current level could it blunt the effects of the other provisions in the GOP tax plan that primarily or exclusively benefit the most well-off. But Speaker Ryan has ruled out raising the top rate above 39.6 percent.[5] And some Republican House members are reportedly considering applying the 39.6 percent rate only to income of above $1 million, more than double the current-law thresholds (whose continuation we assume in this analysis).[6] Such a proposal would do even less to reverse the GOP plan’s tilt to the top than the results we show here.

Many Tax Plan Provisions Benefit Wealthy, Not Just Top Rate Cut

The Trump Administration and GOP congressional leaders released their tax framework in September, proposing major changes to the tax code: a new rate structure with a top individual rate of 35 percent, a special rate for pass-through income, a higher standard deduction, the elimination of personal exemptions and many itemized deductions (including the deduction for state and local taxes), a cut in the corporate tax rate, and a transition to a so-called territorial system for taxing U.S. multinational corporations’ foreign profits.

The plan also left open the possibility of a fourth bracket with a rate above 35 percent, apparently in recognition that its benefits were likely skewed to high-income households. It stated: “An additional top rate may apply to the highest-income taxpayers to ensure that the reformed tax code is at least as progressive as the existing tax code and does not shift the tax burden from high-income to lower- and middle-income taxpayers.”[7]

The Tax Policy Center analyzed the plan, assuming a top tax rate of 35 percent. It concluded that the plan would disproportionately benefit households at the top of the income spectrum. The percentage increase in their after-tax incomes would be many times larger than that for low- and middle-income households.[8] For instance, in 2018, the top 1 percent would see an increase in their after-tax income of 8.5 percent, in contrast to a 1.2 percent increase for those in the middle 20 percent of the income spectrum and a 0.5 percent increase for those in the bottom quintile. The distribution of the tax cuts would grow even more skewed to the top by 2027.

Several of the GOP tax plan’s defenders said the findings that the plan favors the wealthy failed to account for pending decisions, such as on the top rate. The possible addition of a fourth, higher tax rate bracket has been a key defense that advocates of the plan have used to disparage the TPC analysis. The Wall Street Journal editorial page lambasted TPC for not assuming “a fourth tax-rate bracket for high earners that the tax plan left as an option.”[9] House Ways and Means Committee Chair Kevin Brady and Senate Finance Committee Chair Orrin Hatch have argued similarly.[10]

Claims of a potential top rate above 35 percent also seem aimed at confirming the Trump Administration’s oft-stated promise that its tax plan would not cut taxes for the rich. President Trump, for example, said in early September that “the rich will not be gaining at all with this plan,”[11] and Treasury Secretary Steven Mnuchin earlier promised that “there will be no absolute tax cut for the upper class.”[12]

But even if GOP tax-writers decide not to cut the top tax rate at all, leaving it at 39.6 percent, the modified plan would still disproportionately benefit the wealthy. The cut in the top rate is not the sole or even the primary driver of why the GOP leaders’ plan unveiled last month would deliver such large benefits to the most well-off. Rather, it’s the plan’s provisions that would:

- Create a special 25 percent rate for pass-through income. This is income from businesses such as partnerships, S corporations, and sole proprietorships that business owners claim on their individual tax returns. It is now taxed at the same rates as wages and salaries. This income is highly concentrated among those at the top of the income spectrum, and it represents a significant share of their income. [13] TPC finds that the top 1 percent would receive 88 percent of the benefit of a similar proposed 25 percent tax rate on pass-through income.[14] We also estimate that the 400 households in the country with the highest incomes would receive an average annual tax cut of $3.7 million apiece from this provision alone.[15]

- Eliminate the estate tax. The estate tax is the most progressive federal tax. Primarily because the first $11 million of a couple’s estate is exempt and goes untaxed, only the wealthiest 0.2 percent of estates pay any estate tax at all.[16] Repealing this tax thus would provide this very small fraction of estates with tax-cut windfalls averaging more than $3 million apiece. And the roughly 350 estates in a given year that are worth more than $50 million would get tax cuts from this measure averaging more than $20 million apiece.[17] Inheritances account for about 40 percent of all household wealth and are extremely concentrated at the top of the income scale.

-

Cut the corporate tax rate to 20 percent. The GOP tax plan includes a large cut in the corporate tax rate, from 35 percent to 20 percent. TPC estimates that more than one-third of the benefit of corporate rate cuts would flow to the top 1 percent of Americans, with 70 percent flowing to the top fifth of households.[18]

Treasury Secretary Mnuchin has repeatedly argued that the Administration’s “objective” for corporate tax cuts is boosting workers’ wages. Mnuchin has claimed that “many, many economic studies show that more than 70 percent of the burden of corporate taxes are passed on to the workers.”[19] But the evidence does not support this claim.

TPC estimates that about 20 percent of the value of corporate rate cuts flows to workers. Similarly, Congress’s official non-partisan scorekeepers — the Congressional Budget Office and Joint Committee on Taxation — as well as Treasury’s Office of Tax Analysis have all assessed the empirical research as showing that only about a quarter or less of corporate taxes fall on workers, meaning that they would receive a quarter or less of the benefit of corporate tax cuts.[20]

Further, even the modest part of a corporate rate cut that would flow to workers would likely do so in proportion to their share of total wage and salary income. With labor income concentrated among high earners such as executives and professionals, only a small benefit would ultimately flow to the workers hurt most by the slow wage growth of recent decades.[21]

Tax Plan Would Still Disproportionately Benefit Most Well-Off

If Top Rate Remains at 39.6 Percent

Using TPC data, we provide a rough estimate of the distribution of the GOP tax plan’s tax cuts, assuming the top tax rate would remain at 39.6 percent, with that rate applying to taxable income above $418,400 for singles and $470,700 for couples, as under current law.[22] Leaving the top rate unchanged would somewhat temper the sharp increase in the after-tax incomes of the highest-income households, but the plan would still be significantly skewed to the top. Instead of the after-tax incomes of the top 1 percent rising 8.5 percent in 2018, as under the original plan, their incomes would rise by roughly 5.9 percent if the top rate stayed at 39.6 percent. Similarly, for people with incomes above $3.4 million — which places them in the top one-tenth of 1 percent of the income spectrum — the original 10.2 percent increase in after-tax income would be shaved down to roughly 7.2 percent.

Nevertheless, a 5.9 percent increase for the top 1 percent and 7.2 percent for the top one-tenth of 1 percent would still dwarf the 1.2 percent income gain of the middle quintile and the 0.5 percent gain of the bottom quintile. This means that the tax plan with a 39.6 percent top rate would, like the original plan, exacerbate rising income inequality and do little to address the stagnant wages of low- and moderate-income workers.[23]

Under the original GOP tax plan, 54 percent of the net tax cuts would flow to the top 1 percent even though those earners are currently projected to pay 26 percent of federal taxes in 2018. If the GOP plan is modified to keep the top rate at 39.6 percent, 46 percent of the net tax cuts would still flow to the top 1 percent in 2018.

Similarly, millionaires still would get average tax cuts of $138,000 in 2018 under a top rate of 39.6 percent, compared to $200,000 with a top rate of 35 percent. By contrast, households making less than $75,000 would get average tax cuts of $270. Millionaires’ after-tax incomes would rise 6.4 percent, compared to 0.9 percent for households making below $75,000. (See Figure 2.)

These numbers may, in fact, underestimate the tax cuts for the most well-off, for two reasons. First, our methodology for reducing the tax cut in the GOP tax plan for high-income households by keeping the top rate at 39.6 percent does not take into account a portion of the pass-through tax cut, the reduction in the rate from 39.6 percent to 35 percent, and so our estimates only reflect the effects of reducing the top rate on pass-through income from 35 percent to 25 percent.[24] Yet the full pass-through tax cut would remain in place for high earners. Further, TPC estimates that a large gap between the top rate for ordinary income and the rate for pass-through income would create a strong incentive for tax avoidance, as many high-income households would recharacterize their income as pass-through income to take advantage of the lower rate. TPC’s estimates of the GOP tax plan’s pass-through provision reflect a 10-percentage-point gap between the plan’s top regular tax rate (35 percent) and its lower pass-through rate (25 percent). But that differential would grow to 14.6 percentage points if the top rate were held at 39.6 percent and the incentive for tax avoidance would expand, enlarging the tax cut for high-income households.

The second reason that these numbers may well understate the tax cut that would go to those at the top if the top tax rate remains at 39.6 percent is that the plan may retain the 39.6 percent rate only for income above a level such as $1 million a year. If all of the first $1 million of very wealthy households’ income is taxed at a rate below 39.6 percent, they will get larger tax cuts than we have estimated here.

These estimates show that to make the tax plan GOP leaders released in September meet its stated goal of being “at least as progressive as the existing tax code” will require far more dramatic changes than simply keeping the top individual income tax rate at 39.6 percent.

End Notes

[1] U.S. Department of the Treasury, “Unified Framework for Fixing Our Broken Tax Code,” September 27, 2017, https://www.treasury.gov/press-center/press-releases/Documents/Tax-Framework.pdf.

[2] Lindsey McPherson, “Tax Bill Will Include 4th Tax Bracket on High-Income Earners, Ryan Says,” Roll Call, October 20, 2017, https://www.rollcall.com/news/politics/tax-bill-will-include-4th-tax-bracket-on-high-income-earners-ryan-says/?utm_source=news-alert&utm_medium=email&utm_campaign=newsletters.

[3] The Tax Policy Center (TPC) estimated the effects of the Republican tax framework for 2018 and 2027. This analysis focuses on 2018 because the method for estimating the effects of the tax framework while holding the top rate at 39.6 percent relies on TPC data that are available for 2018 but not 2027 (see footnote 22 for details). It is important to note that TPC estimated that the GOP tax-cut plan with a 35 percent top rate would be significantly more tilted to the top in 2027 than in 2018: the top 1 percent would receive 53 percent of net tax cuts in 2018 compared to 80 percent in 2027. If the GOP framework plan is modified so the top tax rate remains unchanged, we would expect the share of benefits going to the wealthiest households to be higher in 2027 than the figures that we report here for 2018.

[4] Jonathan Swan, “Million dollar bracket in the works for GOP tax plan,” Axios, October 22, 2017, https://www.axios.com/million-dollar-bracket-in-the-works-for-gop-tax-plan-2499930587.html.

[5] In an interview with CNBC, Ryan stated that “we’re not talking about raising rates. It's already the top statutory rate, 39.6 percent. So, nobody’s talking about going up above that.” See CNBC, “CNBC Transcript: Speaker Paul Ryan on ‘Squawk Box’ Today,” September 28, 2017, https://www.cnbc.com/2017/09/28/cnbc-transcript-speaker-paul-ryan-on-squawk-box-today.html.

[6] Swan 2017. For an analysis of this proposal, see Steve Wamhoff, “GOP Tax Plan Will Mainly Benefit Millionaires Even If Top Rate Remains 39.6 Percent,” Institute on Taxation and Economic Policy (ITEP), October 24, 2017, https://itep.org/gop-tax-plan-will-mainly-benefit-millionaires-even-if-top-rate-remains-39-6-percent/. There are some differences between ITEP’s and TPC’s analyses of the original GOP plan for the dollar amount and share of tax cuts going to millionaires, though they are qualitatively similar.

[7] Ibid., U.S. Department of the Treasury.

[8] Tax Policy Center, “A Preliminary Analysis of the Unified Framework,” September 29, 2017, http://www.taxpolicycenter.org/publications/preliminary-analysis-unified-framework.

[9] Wall Street Journal Editorial Board, “Tax Policy Center Propaganda,” October 1, 2017, https://www.wsj.com/articles/tax-policy-center-propaganda-1506889612.

[10] Senate Committee on Finance, “Hatch Opening Statement at Finance Committee Hearing on International Tax Reform,” October 3, 2017, https://www.finance.senate.gov/imo/media/doc/10.3.17%20Hatch%20Opening%20Statement%20at%20Finance%20Committee%20Hearing%20on%20International%20Tax%20Reform.pdf; Emily Schillinger, September 29, 2017, https://twitter.com/ELSchillinger/status/913853036157693952.

[11] Nolan D. McCaskill, “Trump: Rich people won’t benefit ‘at all’ from tax plan,” Politico, September 13, 2017, www.politico.com/story/2017/09/13/trump-rich-people-tax-plan-242671.

[12] Elizabeth Gurdus, “EXCLUSIVE: Steve Mnuchin says there will be ‘no absolute tax cut for the upper class,’” CNBC, November 30, 2016, https://www.cnbc.com/2016/11/30/exclusive-steve-mnuchin-no-absolute-tax-cut-for-the-upper-class.html

[13] According to the Congressional Budget Office (CBO), pass-through income amounts to about a quarter (23 percent) of total income of the top 1 percent. See CBO, “The Distribution of Household Income and Federal Taxes, 2013,” June 8, 2016, https://www.cbo.gov/publication/51361.

[14] Tax Policy Center Table T17-0166.

[15] Note that the average annual tax cut for the top 400 households as a result of this provision would rise to $5.5 million if the top rate stayed at 39.6 percent because the value of the pass-through rate cut would rise. These estimates do not account for the increase in tax avoidance by high-income filers that would also occur. Chuck Marr, “Despite President’s Promise, Emerging Details Point to Large Tax Cut for Wealthiest,” CBPP, September 26, 2017, https://www.cbpp.org/blog/despite-presidents-promise-emerging-details-point-to-large-tax-cut-for-wealthiest.

[16] Chye-Ching Huang and Chloe Cho, “Ten Facts You Should Know About the Federal Estate Tax,” CBPP, updated May 5, 2017, https://www.cbpp.org/research/federal-tax/ten-facts-you-should-know-about-the-federal-estate-tax.

[17] Joint Committee on Taxation, “Revenue Estimate Request,” March 24, 2015, https://democrats-waysandmeans.house.gov/sites/democrats.waysandmeans.house.gov/files/documents/114-0191.pdf.

[18] Tax Policy Center Table T17-0180.

[19] Senate Budget Committee hearing, June 13, 2017. Mnuchin has made similar comments on many other occasions: House Appropriations Committee hearing, June 12, 2017; Senate Finance Committee hearing, May 25, 2017; House Ways & Means Committee hearing, May 24, 2017; CNBC interview, May 23, 2017, http://www.cnbc.com/2017/05/23/read-the-full-transcript-of-cnbcs-interview-with-treasury-secretary-steve-mnuchin.html; CBS News Interview, April 27, 2017, http://www.cbsnews.com/news/steven-mnuchin-trump-tax-plan-full-transcript/.

[20] Chye-Ching Huang and Brandon DeBot, “Corporate Tax Cuts Skew to Shareholders and CEOs, Not Workers as Administration Claims,” updated August 16, 2017, https://www.cbpp.org/research/federal-tax/corporate-tax-cuts-skew-to-shareholders-and-ceos-not-workers-as-administration.

[21] Ibid.

[22] Tax Policy Center Tables T17-0224, T17-0225, T17-058, and T17-0159. Tables T17-058 and T17-059 provide the 2018 distributional impact of reducing individual income-tax rates to 10, 25, and 35 percent without any other changes. To estimate the distributional impact of a GOP tax plan without a reduction in the top rate to 35 percent in the income percentile analysis, we subtract the average tax cut that households in the top 1 percent and the top 0.1 percent would receive as a result of the changes in individual tax rates from the tax cut they would receive under the entire GOP leaders’ tax plan (Table T17-0158)). For the income level analysis, we subtract the average tax cut for households making above $500,000 (Table T17-0159).

[23] Chuck Marr, Brandon DeBot, and Emily Horton, “How Tax Reform Can Raise Working-Class Incomes,” CBPP, updated October 13, 2017, https://www.cbpp.org/research/federal-tax/how-tax-reform-can-raise-working-class-incomes.

[24] In its analysis of rate reductions (TPC Tables T17-058, and T17-0159), TPC estimates of reducing the top rate from 39.6 percent to 35 percent includes the effects of this rate reduction on pass-through income. We used this estimate for backing out the effects of the top rate reduction in the GOP plan.

More from the Authors

Areas of Expertise

Areas of Expertise