Corporate Tax Cuts Skew to Shareholders and CEOs, Not Workers as Administration Claims

Eventual Spending Cuts or Tax Increases to Pay for Corporate Rate Cuts Could Leave Most Workers Worse Off

To sell their tax policies as helping workers, Trump Administration officials claim that the bulk of the benefits from cutting the corporate tax rate by more than half, to 15 percent — a centerpiece of President Trump’s tax plan — would flow to workers and raise their wages.[2] In particular, Treasury Secretary Steven Mnuchin has repeatedly argued that the Administration’s “objective” for corporate tax cuts is boosting workers’ wages because “many, many economic studies show that more than 70 percent of the burden of corporate taxes are passed on to the workers.”[3] The evidence indicates that the bulk of the benefits from a corporate rate cut will go to those at the top.This claim is misleading, however, and the assertion that most of the benefits would go to workers is wide of the mark.

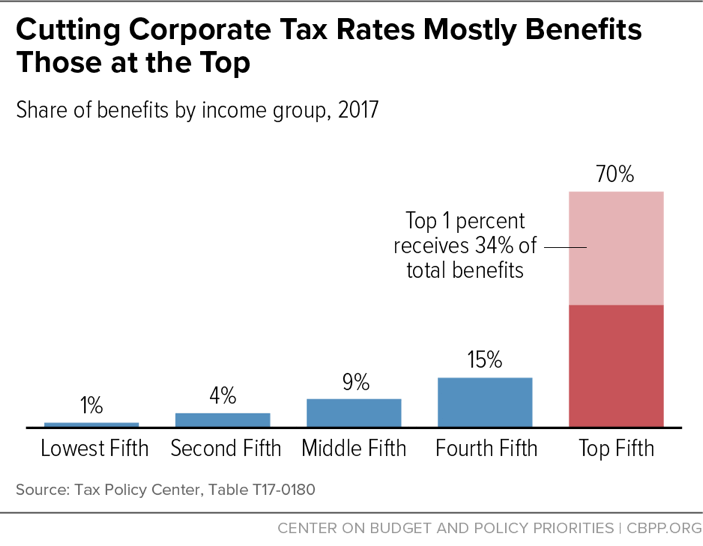

The evidence indicates that the bulk of the benefits from a corporate rate cut will go to those at the top, with only a small share flowing to low- and moderate-income working families. The Tax Policy Center (TPC) estimates about 70 percent of the benefit of a corporate rate cut will flow to the top fifth of households, with one-third flowing to the top 1 percent alone. (See Figure 1.) There are two main reasons why:

-

Only a modest share of corporate rate cuts flows to workers at any income level, including managers. TPC’s estimates incorporate a reasonable mainstream assumption that about 20 percent of the value of corporate rate cuts flows to workers. Similarly, Congress’s official non-partisan scorekeepers — the Congressional Budget Office (CBO) and Joint Committee on Taxation (JCT) — as well as Treasury’s Office of Tax Analysis all assess the empirical research as showing that only about a quarter or less of corporate taxes fall on workers, meaning that they would receive a quarter or less of the benefit of corporate tax cuts.

These estimates are far below the 70 percent figure Mnuchin claims. The 70 percent figure is supported most prominently by a study by President Trump’s Council of Economic Advisers Chair Kevin Hassett and American Enterprise Institute scholar Aparna Mathur, which other researchers have viewed with considerable skepticism due to its methodological weaknesses, and by another paper that sets out a model of how corporate taxes affect workers in different scenarios. In the latter paper, only the most generous assumptions support a 70 percent figure, and other research suggests that these assumptions are unrealistic.

- Even the modest part of a corporate rate cut that would flow to workers is skewed to high earners such as highly compensated executives and professionals. Whatever share of corporate rate cuts goes to workers likely does so in proportion to their share of total wage and salary income. Labor income is concentrated among high earners such as highly paid executives, lawyers and other professionals, and the like. Thus, only a small benefit would ultimately flow to struggling workers who have been hurt most by slow wage growth in recent decades.

Assumptions about who ultimately pays the corporate tax have a substantial impact on how the benefits of cutting the tax are estimated to be distributed across income groups. Mnuchin’s embrace of an abnormally large share flowing to labor — far more than the Treasury Department assumes, or assumed during the George W. Bush Administration[4] — means that a Trump Administration distributional analysis could show low- and middle-income workers receiving unrealistically large benefits. Indeed, there are signs that the Trump Administration may produce and tout distributional estimates of its tax plan that could use unconventional assumptions to paint the overall tax plan in a more favorable light. For example, Mnuchin has said, “[W]hen we come out with the tax plan, we will show the distribution, as you would expect, and [Congress] will see it,”[5] and Office of Management and Budget Director Mick Mulvaney has criticized Congress’s official scorekeepers.[6] Such estimates would be part of a troubling pattern of the Administration relying on unrealistic economic assumptions — like the economic growth assumptions it used in its budget,[7] which are rosier than those of the CBO to an unprecedented degree — and should be treated with caution.

Further, corporate rate cuts could ultimately hurt the majority of Americans, depending on how they are paid for. If, as in the Administration’s tax proposals, corporate rate cuts are not offset by spending cuts or increases in other taxes, any assumed increase in domestic investment — and therefore benefit for workers in the form of higher productivity and wages — won’t be sustained. The higher deficits would reduce national saving, meaning less capital would be available for investment in the economy and interest rates could rise. Higher interest rates, in turn, would reduce and ultimately reverse the increase in investment necessary for workers to gain (in the form of higher productivity and wages) from a corporate rate cut.

Mainstream distributional tables showing that corporate rate cuts provide some wage increases to workers through increased private investment implicitly assume that the tax cut would be paid for — but without displaying those offsets. Absent that implicit assumption, the same gains would not materialize. And under reasonable illustrative assumptions about how tax cuts could ultimately be financed, the bottom 80 percent of households would face average net tax increases or benefit reductions under Trump’s corporate rate cut proposal, while the top 1 percent would continue to receive large net tax cuts.

Tax reform — including corporate tax reform — should focus an important part on meaningfully boosting workers’ incomes, and there are ways to do so while raising revenues to meet national priorities or for deficit reduction. But the Trump plan would not meet these metrics, and it should not rely on distributional estimates outside the economic mainstream to claim otherwise.

How Cutting Corporate Taxes Could Benefit Workers, in Theory

A corporate rate cut increases after-tax corporate profits. In the short term, this would almost entirely benefit corporate shareholders. But eventually, the increase in returns to companies’ after-tax investments may spur an increase in investment flowing through corporations. In theory, the added investment should somewhat lower corporate investors’ after-tax returns, and therefore the extent to which they benefit from the rate cut. It should also raise workers’ productivity and possibly their wages, enabling them to share in the benefit of the rate cut. (Some of the rate cut may also benefit investors in other types of capital: as investment flows towards corporations, it reduces the supply of capital in the non-corporate sector, and thereby also increases returns to those investors.)

The extent to which cutting the U.S. corporate tax rate benefits U.S. workers depends on how mobile capital and workers are across international borders. If capital can flow very freely, investors worldwide can shift their investments into U.S. corporations when the U.S. corporate rate is cut. The added investment in the United States would reduce U.S. corporate investors’ after-tax returns — and their ability to benefit from the rate cut — but increase U.S. workers’ share of the benefit by boosting their productivity and wages.

However, any such benefits for workers do not take into account how corporate rate cuts are paid for. Once those offsets are considered, typical workers (and the majority of workers) could end up worse off, as this paper explains.

Only Modest Share of Corporate Rate Cuts Flows to Low- and Moderate-Income Workers

It is difficult to measure directly how much of the benefit of a corporate rate cut eventually reaches workers or non-corporate investors; many other things that affect the economy, investment, and wages could occur at the same time as corporate tax changes, and the effects of tax changes could take some time to become apparent. But various empirical studies have attempted to uncover the relationship by looking at changes in corporate rates across time and by comparing different states and countries. Credible mainstream organizations conducting rigorous policy analysis assess that evidence as showing that the bulk of corporate rate cuts goes to the owners of corporations and other types of capital, who are highly concentrated among high-income households. Only a modest share flows to workers, and even that benefit is concentrated among high earners. Thus, corporate rate cuts are heavily skewed to those at the top.

CBO[8] and JCT,[9] along with other mainstream estimators such as the career staff at the Treasury Office of Tax Analysis,[10] TPC,[11] and the Institute on Taxation and Economic Policy,[12] have reviewed the evidence about the distribution of corporate taxes and concluded that workers bear 25 percent or less of the corporate tax burden over the long term. (See Table 1.)

| TABLE 1 | ||

|---|---|---|

| Mainstream Consensus: Little of Corporate Taxes Falls on Workers | ||

| Organization | Labor’s share of tax | Highest income households’ share of tax |

| Treasury Office of Tax Analysis | 19% | 45% to top 1% |

| Tax Policy Center | 20% | 34% to top 1% |

| Joint Committee on Taxation | 25% | 31% to top 0.7% (income >$500,000) |

| Congressional Budget Office | 25% | 47% to top 1% |

| Tax Foundation | ~70% | Not Available |

Mnuchin’s claim that 70 percent of the corporate tax flows to workers is used only by the Tax Foundation, and is an outlier from the mainstream consensus.[13] The most prominent empirical estimate that might support this claim is a study (written up in a series of papers) by Hassett and Mathur.[14] Examining data from a cross-section of countries, they conclude that a 1 percent increase in the corporate tax rate reduces wages by nearly 1 percent. Other researchers, however, have viewed this report quite skeptically.[15]

For example, a report by economists Jane Gravelle and Thomas Hungerford for the non-partisan Congressional Research Service notes that the Hassett-Mathur finding implies that a $1 increase in the corporate tax would decrease annual wages by $22 to $26 — a result “that no model could ever come close to predicting.”[16] Further, as Gravelle and Hungerford point out, the paper has a number of significant statistical problems, such that even if only small adjustments are made to the Hassett-Mathur approach, its model would find “no evidence that changes in the top corporate tax rate affect wage rates in manufacturing.” Although Hassett and Mathur have revised their paper to include additional assumptions, these updates do not correct the methodological issues that Gravelle and Hungerford have pointed out.

The Treasury Department under Mnuchin has also cited a study by Céline Azémar and Glenn Hubbard that says 60 percent of the corporate tax falls on workers, ignoring the estimates of its own Office of Tax Analysis.[17] The Azémar-Hubbard estimate assumes that corporate profits are split between employers and workers based on their negotiating power. Even under that assumption, it finds that workers would get a large share of corporate rate cuts only when union membership is high and the country is small — but the U.S. is a large country with low union membership.

A CBO working paper by William C. Randolph sets out a model that finds that workers bear about 70 percent of the corporate tax — but only under the most generous possible assumption that investment can flow completely freely across international borders.[18] CBO, JCT, Treasury, and TPC all consider the Randolph paper and adjustments by other researchers in setting their estimates, and all conclude that the burden on workers is dramatically lower than in Randolph’s model and assumptions.

One reason why the 70 percent figure is implausible is that research suggests that at least 60 percent of the corporate tax falls on corporate investors — because 60 percent of the tax applies to unusual corporate profits that benefit them alone. These studies find that a large and growing share of corporate profits consists of “excess returns,” or uniquely high returns to a particular investment that other investors could not make and that flow from factors like special skill, market power (e.g. patents or a monopoly), and luck. If corporate investors are making uniquely high returns, taxing some of those returns will still leave them with positive “excess” returns; they will have no reason to reduce their investment, because they couldn’t find those excess returns elsewhere. And if taxes on excess returns don’t lower corporate investment, they will not be passed on to workers because they won’t affect workers’ productivity or wages. If 60 percent or more of corporate returns are excess returns, then shareholders bear 60 percent or more of the corporate tax. That leaves at most 40 percent of the tax that can be borne by workers.[19]

Further, whatever share of a corporate rate cut eventually flows to workers, even it will be skewed to high earners such as executives and other professionals like high-paid lawyers, accountants, and consultants. Mainstream models assume that any part of a corporate tax cut that flows to workers will be shared among them in proportion to their share of labor income — i.e., income from salaries, wages, and other forms of compensation for work.[20] Although labor income is less concentrated at the top of the income distribution than income from investments (such as capital gains, interest, and dividends), it is still skewed to the top. For example, TPC estimates that in 2015, about 48 percent of labor income went to the top 20 percent of the income distribution, and more than 10 percent of labor income went to the top 1 percent.[21]

Taking these two effects into account — workers receive only a modest share of the value of corporate rate cuts and that portion is skewed to high earners — mainstream estimates conclude that overall, more than one-third of the value of corporate rate cuts flows to the top 1 percent of households, and at least 70 percent flows to the top fifth of households.

Corporate Rate Cuts Could Ultimately Leave Most Americans Worse Off

If corporate tax cuts are not offset by tax increases or spending cuts, the resulting increased deficits would reduce national saving, meaning less capital would be available for investment in the economy and interest rates would consequently rise. This would ultimately reverse any increase in investment caused by the rate cut, preventing productivity and workers’ wages from rising.[22] For corporate tax cuts to produce sustained wage gains for workers by increasing their productivity, the tax cuts must be offset.

How those offsets are designed, however, could have a large impact on the distributional effects. The offsets could reduce workers’ incomes by more than their increase in wages.[23]

Mainstream distributional tables showing workers receiving a modest share of the benefits from corporate rate cuts effectively assume these tax cuts would be paid for sooner or later. But the offsetting spending cuts or tax increases are not reflected in the distributional tables, because the estimators have no way of knowing what the specific offsets will be. As a result, distributional tables almost certainly produce an overly positive effect of the impact of corporate rate cuts on ordinary workers. [24] Once offsets were taken into account, such workers would be less well off — and likely worse off on net — unless the corporate rate cuts were financed largely or entirely through tax increases on high-income households.

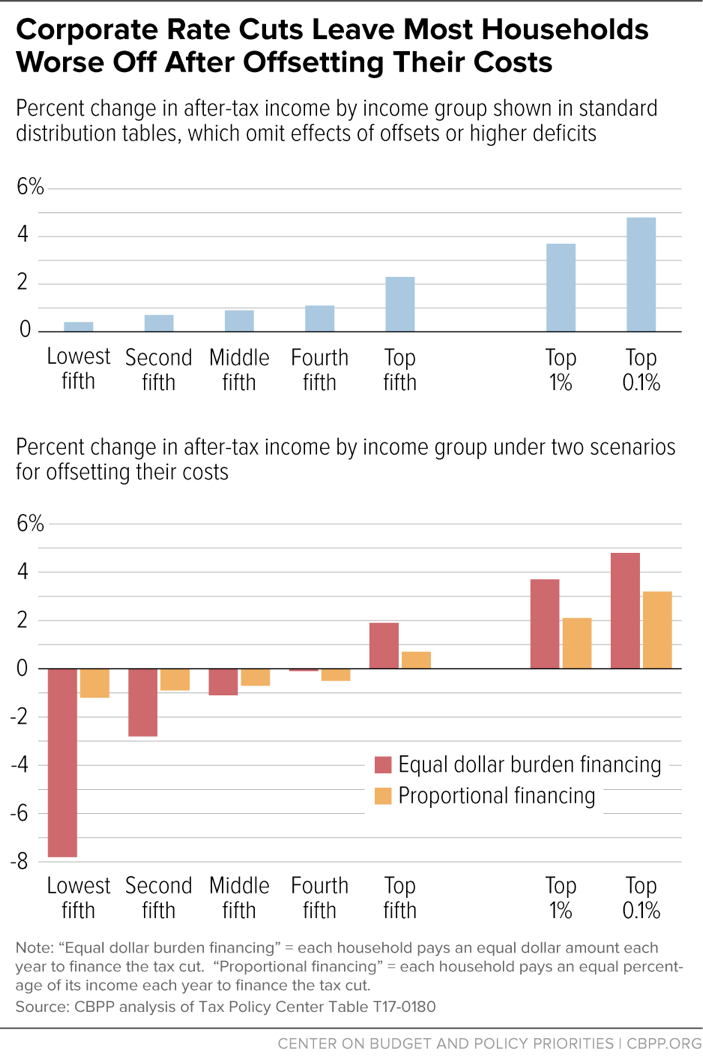

For example, the Administration’s proposal to cut the corporate tax rate from 35 percent to 15 percent would cost more than $2 trillion over ten years, and the Administration has proposed no policies that could plausibly offset the cost. These corporate tax cuts would flow largely to the top, while providing little benefit to most workers. And if one assumes that the tax cuts must be fully offset eventually by some combination of reductions in government benefits and increases in other taxes, it’s clear that most workers would be worse off under the proposal.[25] Consider the two following simple financing scenarios for a corporate rate cut costing $200 billion a year, also shown in Table 2 and Figure 2:[26]

- Each household pays an equal dollar amount each year to finance the tax cuts. Under this scenario, each household, on average, receives a tax benefit from the corporate rate cut, but in the long run it also “pays” $1,145 per year to finance the tax cuts. Something close to this scenario could occur if the tax cuts were financed largely or entirely through spending cuts to programs that affect most Americans. We refer to this as the “equal dollar burden” scenario.

- Each household pays an equal percentage of income each year to finance the tax cuts. Under this scenario, each household, on average, receives a tax benefit from the corporate rate cut, but it also pays 1.6 percent of its income each year to finance the tax cuts. Something close to this scenario could occur if the tax cuts were financed through a combination of spending cuts and progressive tax increases. We refer to this as the “proportional burden” scenario.

Under both scenarios, most Americans — at least the bottom 80 percent — would be net losers. For example, an average household in the bottom 20 percent would receive roughly $60 a year from the corporate rate cut. But under the equal dollar burden financing scenario, the household would lose $1,140 a year from the spending cuts to offset the cost; under the proportional financing scenario, it would lose $220 a year. Therefore, they would be left $1,080 or $160 worse off, respectively. Meanwhile, the top 1 percent of households would receive tax cuts averaging $59,000 a year and would be big winners even after the offsets are taken into account. On balance, they would be at least $34,000 (more than 2 percent of their after-tax income) better off, on average. The results are even more striking for the top 0.1 percent of households, who would be at least $240,000 (more than 3 percent of their after-tax income) better off even after financing is considered.

| TABLE 2 | ||||||

|---|---|---|---|---|---|---|

| Corporate Rate Cuts Make Most Americans Worse Off After Accounting for Financing Net effect of $200 billion annual corporate tax cut, based on Tax Policy Center analysis of long-run change in corporate tax burden from rate cut in 2017 |

||||||

| As shown in standard distribution tables* | With equal dollar burden financing |

With proportional financing |

||||

| Income Group | Dollars | Change in after-tax Income | Dollars | Change in after-tax Income | Dollars | Change in after-tax Income |

| Lowest Fifth | $60 | 0.4% | -$1,080 | -7.8% | -$160 | -1.2% |

| Second Fifth | $220 | 0.7% | -$920 | -2.8% | -$310 | -0.9% |

| Middle Fifth | $500 | 0.9% | -$640 | -1.1% | -$400 | -0.7% |

| Fourth Fifth | $1,040 | 1.1% | -$110 | -0.1% | -$430 | -0.5% |

| Top Fifth | $5,840 | 2.3% | $4,700 | 1.9% | $1,810 | 0.7% |

| Top 1% | $59,400 | 3.7% | $58,250 | 3.7% | $34,100 | 2.1% |

| Top 0.1% | $361,330 | 4.8% | $360,190 | 4.8% | $242,060 | 3.2% |

Overall, the net effect would be to transfer tens of billions of dollars from the bottom 80 percent of households to higher-income Americans.

Moreover, these scenarios could understate the harm to low- and moderate-income families from corporate rate cuts because the measures adopted to finance them could disproportionately target programs that help those people. The Trump Administration’s budget, for example, targets roughly three-fifths of its severe budget cuts on programs that help low- and moderate-income families afford the basics or improve their upward mobility, cutting these programs by $2.5 trillion over ten years.[27] Along the same lines, House Budget Committee Chairman Black’s budget plan also proposes tax cuts paired with cuts to safety net programs.[28]

If corporate rate cuts were offset — either immediately or in the future — primarily by cuts to programs serving low- and moderate-income people, then the net effects would be even more regressive than the scenarios presented in this analysis. The resulting fiscal squeeze also likely would eventually mean fewer resources for investments in areas like infrastructure and education that could broadly benefit the economy, jobs, and wages over time.

End Notes

[1] Ted Lee provided valuable research assistance.

[2] The Trump Administration is reportedly considering a higher corporate tax rate, but no specific new rate has been reported and its public proposal remains 15 percent.

[3] Senate Budget Committee hearing, June 13, 2017. He has made similar comments on many other occasions: House Appropriations Committee hearing, June 12, 2017; Senate Finance Committee hearing, May 25, 2017; House Ways & Means Committee hearing, May 24, 2017; CNBC interview, May 23, 2017, http://www.cnbc.com/2017/05/23/read-the-full-transcript-of-cnbcs-interview-with-treasury-secretary-steve-mnuchin.html; CBS News Interview, April 27, 2017, http://www.cbsnews.com/news/steven-mnuchin-trump-tax-plan-full-transcript/.

[4] In 2008, the Bush Administration’s Office of Tax Analysis (OTA) in the Treasury Department changed its estimate of the share of the tax falling on labor from 0 percent to 24 percent. In 2012, OTA updated its estimate to 18 percent to better reflect new empirical evidence, and the latest OTA estimate, from 2017, is 19 percent. Julie Anne Cronin et al., “Distributing the Corporate Income Tax: Revised U.S. Treasury Methodology,” Technical Paper 5, May 2012, https://www.treasury.gov/resource-center/tax-policy/tax-analysis/Documents/TP-5.pdf.

[5] House Ways and Means Hearing, May 24, 2017. Mnuchin made similar statements in a Senate Banking Committee hearing, May 18, 2017, and a Senate Finance Committee hearing, May 25, 2017.

[6] Philip Klein, “Mick Mulvaney: The day of the CBO ‘has probably come and gone,’” Washington Examiner, May 31, 2017, http://www.washingtonexaminer.com/mick-mulvaney-the-day-of-the-cbo-has-probably-come-and-gone/article/2624609.

[7] Chad Stone, “Gap Between Trump, CBO Predictions on Economic Growth the Largest on Record,” Center on Budget and Policy Priorities, May 22, 2017, https://www.cbpp.org/research/federal-budget/gap-between-trump-cbo-predictions-on-economic-growth-the-largest-on-record.

[8] Congressional Budget Office, “The Distribution of Household Income and Federal Taxes, 2008 and 2009,” July 2012, https://www.cbo.gov/publication/43373; Congressional Budget Office, “The Distribution of Household Income and Federal Taxes, 2013,” June 2016, https://www.cbo.gov/publication/51361.

[9] Joint Committee on Taxation, “Modeling the Distribution of Taxes on Business Income,” JCX-14-13, October 16, 2013, https://www.jct.gov/publications.html?func=startdown&id=4528.

[10] U.S. Department of the Treasury, Office of Tax Analysis, “Treasury’s Distribution Methodology and Results,” November, 12, 2015, https://www.treasury.gov/resource-center/tax-policy/tax-analysis/Documents/Summary-of-Treasurys-Distribution-Analysis.pdf, and Distribution of the Tax Burden, Current Law, 2018, from https://www.treasury.gov/resource-center/tax-policy/Pages/Tax-Analysis-and-Research.aspx.

[11] James R. Nunns, “How TPC Distributes the Corporate Tax,” September 13, 2012, http://www.taxpolicycenter.org/publications/how-tpc-distributes-corporate-income-tax; TPC tables T17-0179 and T17-0180, http://www.taxpolicycenter.org/simulations/distribution-change-corporate-tax-burden-june-2017.

[12] ITEP follows Treasury’s distribution of the corporate tax burden: Citizens for Tax Justice, “Bruce Bartlett Is Wrong: New Conclusions on the Corporate Income Tax Change Nothing,” Tax Justice Blog, October 30, 2013, http://www.ctj.org/taxjusticedigest/archive/2013/10/bruce_bartlett_is_wrong_new_co.php#.WUGBWlXyuot.

[13] The Tax Foundation’s dynamic analysis appears to assume that labor’s share of corporate taxes is proportional to its share of national income, an approach that no other organization uses. Kyle Pomerleau, “Details and Analysis of the 2016 House Republican Tax Reform Plan,” Tax Foundation, July 5, 2016, https://taxfoundation.org/details-and-analysis-2016-house-republican-tax-reform-plan/.

[14] Kevin A. Hassett and Aparna Mathur, “Taxes and Wages,” American Enterprise Institute Working Paper No. 128, June 2006; Kevin A. Hassett and Aparna Mathur, “A Spatial Model of Corporate Tax Incidence,” American Enterprise Institute Working Paper, December 1, 2010; “A Spatial Model of Corporate Tax Incidence,” Applied Economics 47(13): 1350-1365 (2015).

[15] For example, see: Jennifer C. Gravelle, “Corporate Tax Incidence: A Review of Empirical Estimates and Analysis,” CBO Working Paper Series 2011-01, June 2011, https://www.cbo.gov/sites/default/files/cbofiles/ftpdocs/122xx/doc12239/06-14-2011-corporatetaxincidence.pdf. For an overview of issues with the Hassett and Mathur study, see: Aviva Aron-Dine, “Well-Designed, Fiscally Responsible Corporate Tax Reform Could Benefit the Economy,” Center on Budget and Policy Priorities, June 4, 2008, https://www.cbpp.org/research/well-designed-fiscally-responsible-corporate-tax-reform-could-benefit-the-economy-unpaid.

[16] Jane G. Gravelle and Thomas L. Hungerford, “Corporate Tax Reform: Issues for Congress,” Congressional Research Service, December 26, 2012, https://www.cfr.org/content/publications/attachments/corporate_tax_reform.pdf.

[17] Richard Rubin, “Who Ultimately Pays for Corporate Taxes? The Answer May Color the Republican Overhaul,” Wall Street Journal, August 8, 2017, https://www.wsj.com/articles/who-ultimately-pays-for-corporate-taxes-the-answer-may-color-the-republican-overhaul-1502184603?mg=prod/accounts-wsj; Céline Azémar and R. Glenn Hubbard, “Country characteristics and the incidence of capital income taxation on wages: An empirical assessment,” Canadian Journal of Economics, 48 (5) (2015): 1762-1802.

[18] William C. Randolph, “International Burdens of the Corporate Income Tax,” CBO Working Paper Series 2006-09, August 2006, https://cbo.gov/sites/default/files/cbofiles/ftpdocs/75xx/doc7503/2006-09.pdf. This “base case” also assumes that labor is completely immobile, that foreign and domestic goods can be perfectly substituted for each other, and that other countries don’t change their taxes in response to U.S. tax changes.

[19] See Laura Power Nunns and Austin Frerick, “Have Excess Returns to Corporations Been Increasing Over Time?” Treasury Office of Tax Analysis Working Paper 111, November 2016 https://www.treasury.gov/resource-center/tax-policy/tax-analysis/Documents/WP-111.pdf; Eric Toder, and Kim Rueben, “Should We Eliminate Taxation of Capital Income?” in Henry J. Aaron, Leonard Burman, and C. Eugene Steuerle (eds.), Taxing Capital Income, 2007.

[20] The standard assumption is that workers can freely move between businesses that pay the corporate tax and those that do not, so if corporations invest more and pay higher wages, workers will move from non-corporate jobs into corporate jobs until wages equalize between the two types of businesses.

[21] James R. Nunns, “How TPC Distributes the Corporate Tax,” September 13, 2012, http://www.taxpolicycenter.org/publications/how-tpc-distributes-corporate-income-tax; TPC tables T17-0179 and T17-0180, http://www.taxpolicycenter.org/simulations/distribution-change-corporate-tax-burden-june-2017.

[22] For example, a 2005 JCT analysis of a hypothetical $500 billion corporate tax cut that is not paid for found that over time “[g]rowth effects eventually become negative without offsetting fiscal policy for each of the proposals, because accumulating Federal government debt crowds out private investment.” Long-run impacts on employment were similarly either close to zero or negative, depending on assumptions about how the Federal Reserve set monetary policy. JCT, “Macroeconomic Analysis of Various Proposals to Provide $500 Billion in Tax Relief,” JCX-4-05, March 1 2005, p.8, http://www.jct.gov/x-4-05.pdf.

[23] Economists typically analyze where the corporate tax burden ultimately falls using models that assume offsetting fiscal policies; estimates based on such models underlie the distributional assumptions used by Congress’s official non-partisan scorekeepers as well as Treasury’s Office of Tax Analysis. For example, see Randolph, Table 3.

[24] For a general discussion of distributional analyses of tax cuts incorporating consistent financing assumptions, see Jason Furman, “A Short Guide to Dynamic Scoring,” Center on Budget and Policy Priorities, revised August 24, 2006, https://www.cbpp.org/research/a-short-guide-to-dynamic-scoring.

[25] For this analysis, we use TPC’s long-run distribution of the corporate tax from rate cuts for 2017, and a conservative estimate for a $200 billion annual tax cut.

[26] For more on these assumptions, see: William G. Gale, Peter R. Orszag, and Isaac Shapiro, “The Ultimate Burden of The Tax Cuts,” Center on Budget and Policy Priorities and Tax Policy Center, June 2, 2004, https://www.cbpp.org/archives/6-2-04tax.htm.

[27] Isaac Shapiro, Richard Kogan, and Chloe Cho, “Trump Budget Gets Three-Fifths of Its Cuts From Programs for Low- and Moderate-Income People,” Center on Budget and Policy Priorities, May 30, 2017, https://www.cbpp.org/research/federal-budget/trump-budget-gets-three-fifths-of-its-cuts-from-programs-for-low-and.

[28] Robert Greenstein, “Commentary: Harsh House GOP Budget Resolution Asks Most from Those Who Have Least” Center on Budget and Policy Priorities, July 18, 2017, https://www.cbpp.org/press/statements/greenstein-harsh-house-gop-budget-resolution-asks-most-from-those-who-have-least.

More from the Authors