IRS Budget Needs to Be Restored and Supplemented to Implement and Enforce the New Tax Law

Multi-Year Challenges Will Require Multi-Year Funding Commitment

The implementation and enforcement of the recently enacted federal tax legislation pose a once-in-a-generation, multi-dimensional challenge for the Internal Revenue Service (IRS). The new law will affect virtually every taxpayer and business in the country. It eliminates ingrained features of the income tax, such as the personal exemption and many deductions, introduces a new tax treatment of certain types of income, and adopts a completely new international corporate tax regime. It is certain to spark questions from the public and businesses, who will look to the IRS for answers. Of particular concern, given some of the law’s features and the hasty way in which it was put together, it will also likely lead to an aggressive effort by some businesses and wealthy individuals to push against the law’s outer boundaries — and possibly over them — to minimize their taxes.

This challenge is magnified by the IRS’s shrunken budget and depleted workforce.

As a result, the IRS will need to provide extensive guidance to taxpayers, update its systems and forms, undertake significant public education, expand customer service, and, importantly, strengthen enforcement in the years to come. This challenge is magnified by the IRS’s shrunken budget and depleted workforce. Its budget was cut by $2.4 billion, or 18 percent, between 2010 and 2017, after adjusting for inflation, and the agency has lost 18,000 employees (nearly one-fifth of its workforce), with enforcement personnel accounting for roughly four-fifths of this reduction.

In the weeks and months ahead, the Trump Administration and Congress should take two essential actions:

- Provide a substantial funding boost for the IRS in 2018. The IRS was allocated $12 billion in 2017. It will need a substantial boost across the organization for the current fiscal year in order both to address ongoing funding shortfalls and to gear up for the regulatory (with Treasury), customer service, and enforcement challenges the new law poses. Providing additional funding for the IRS should be a top priority for the Administration and Congress as they negotiate 2018 funding levels.

- Make the necessary multi-year commitment to the IRS in the 2019 budget. The Trump Administration’s 2019 budget, expected to be released in early February, needs to include a robust commitment to the IRS, laying out a multi-year funding path sufficient to implement and enforce the new law’s fundamental changes to the tax code. Funding for 2019 will cover the crucial first filing season under the new law, and the IRS’s customer service budget needs to reflect the increased workload that will entail. Moreover, because the IRS enforcement budget has been disproportionately cut and the risk of new forms of tax gaming is high, the Trump 2019 budget should make a multi-year commitment to rebuild and bolster the IRS’s enforcement capabilities.

After years of targeting the IRS’s budget for deep cuts, some GOP taxwriters have indicated in recent weeks that more IRS funding is needed.[1] Reportedly, the IRS estimates that it will need roughly $500 million in 2018 and 2019 for implementation of the new law.[2] Any funding increase should start from last year’s levels, not from the lower levels in the House and Senate appropriations bills. Those bills were drafted before the tax law’s enactment and merely continued the same misguided policy of undermining the IRS’s ability to perform its core functions of collecting taxes, providing service to taxpayers, and enforcing the nation’s tax laws.

Policymakers should heed the example of how Congress and the IRS responded to major tax reform legislation in 1986. After that reform was enacted, the IRS significantly expanded taxpayer service efforts, hiring an additional 1,300 staff.[3] At the same time, the agency was in the midst of a major effort to recover unpaid taxes, and so was actively strengthening its enforcement capabilities. And these staff increases occurred at a time when the IRS already had about one-fifth more staff that it does today.

The IRS plays a fundamental role in our system of government by helping taxpayers comply with the tax code and ensuring that the nation’s tax laws are enforced fairly and credibly, as well as by collecting nearly all of the revenue that funds federal programs from national defense and health care to investments in highways, science research, and education. In the face of deep budget cuts and personnel reductions, the IRS has struggled to keep up with its basic core functions. Implementation of the new tax law will add substantially to the strain. It is incumbent on Congress and the Trump Administration to provide the resources the IRS will need over the coming years to meet the customer service and enforcement challenges the new tax law creates.

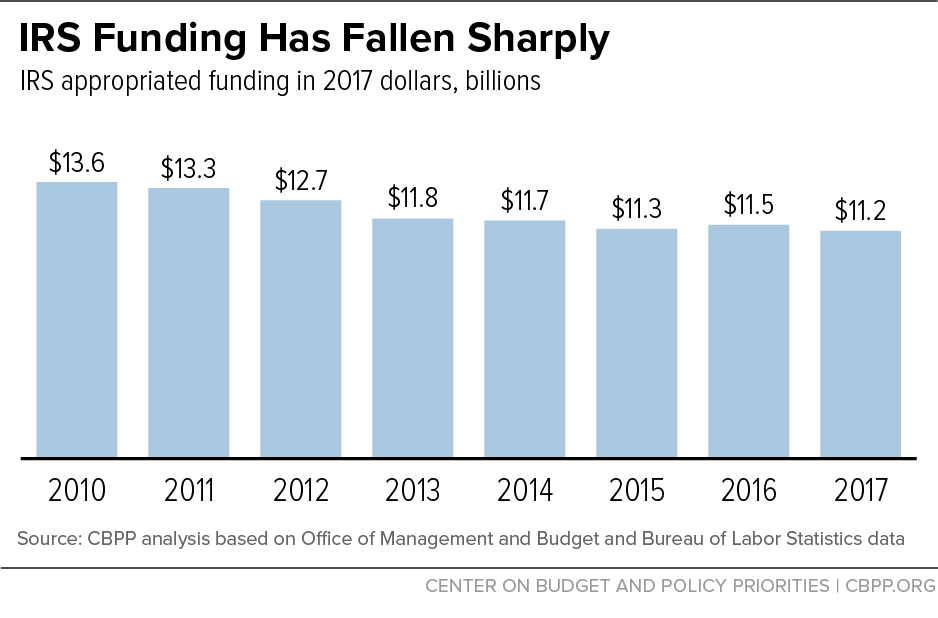

IRS Funding Has Fallen Sharply Since 2010

The IRS has been targeted for sharp funding cuts since 2010. Its 2017 appropriation was $2.4 billion below the 2010 level after adjusting for inflation, amounting to an 18 percent cut. (See Figure 1.) As most IRS funding goes to staffing, the cuts have forced the IRS to reduce its workforce dramatically; the agency lost roughly 18,000 employees — around 19 percent of its workforce — between 2010 and 2017.[4]

These damaging cuts have weakened the agency’s ability to perform its core functions of collecting taxes and enforcing the nation’s tax laws. As seven former IRS commissioners from both Republican and Democratic administrations have written: “Over the last fifty years, none of us has ever witnessed anything like what has happened to the IRS appropriations over the last five years and the impact these appropriations reductions are having on our tax system.”[5]

Even as congressional Republican leaders and the Trump Administration announced their intention to overhaul the tax code last year, they continued to propose still deeper cuts to the IRS budget for 2018. The House and Senate appropriations bills would cut the IRS budget by $149 million and $124 million below its 2017 level, respectively. Both bills would shrink the IRS budget to fully 20 percent below its 2010 level, adjusted for inflation.

As the tax bill moved closer to its eventual enactment, however, some key GOP lawmakers acknowledged that the IRS would need additional funding to implement it. House Ways and Means Oversight Subcommittee Chairman Rep. Vern Buchanan said he “envisioned $500 million in funding. . . to design new tax forms, write new guidance publications and train customer service staff to implement a rewritten tax code,” Government Executive reported.[6] And Senate Finance Committee Chairman Orrin Hatch, according to his spokesperson, “will work closely with the IRS to make sure they can implement [the new law].”[7]

According to the National Taxpayer Advocate, the IRS has estimated that it will need $495 million in 2018 and 2019 to implement the new tax law. Any funding increase should start from last year’s levels, not from the lower levels in the House and Senate appropriations bills. The additional funds would be used for bolstering customer service, producing new tax forms and publications, revising regulations, and issuing guidance as well as training IRS employees on the new law’s provisions. The IRS will also need to update its systems to reflect the new law’s changes. For instance, it has identified 131 filing season systems that will need updates to address changes to individual and business tax rates, inflation indexing, various tax threshold levels, and the like, as well as to align fraud detection filters with the new provisions.[8]

Customer Service, Shortchanged Since 2010, Likely to See Rise in Demand

The tax legislation received significant media and paid-advertising attention as it moved rapidly through Congress. As a result, many Americans are likely aware there has been a major tax change, but may be unclear on many of the details of the changes, such as the end of the personal exemption, the elimination or modification of a number of longstanding deductions, and the complex new definitions of who is eligible for certain favorable tax treatments, particularly the new tax break for “pass-though” business income (that is, income from businesses such as partnerships, S corporations, and sole proprietorships that is passed through to the firms’ owners and claimed on their individual tax returns). While it’s hard to predict how many taxpayers will seek to contact the IRS with questions, these combined factors could well lead to a substantial increase in customer-service demand.

The 1986 tax reform sparked a 14 percent increase in call volume. More recent tax policy changes also have generated a significant increase in questions from taxpayers. Following the enactment of the Affordable Care Act in 2010, calls and correspondence rose 8 percent the next year and 18 percent the year after that. Call volume more than doubled after the stimulus tax cuts of 2008, even though the changes were relatively straightforward.[9]

The IRS is currently ill-prepared for a surge in taxpayer inquiries. The budget cuts since 2010 have significantly weakened taxpayer services, making it more difficult for taxpayers to reach IRS representatives for assistance filing their returns and paying their tax bills.

The tax filing season in 2015 was particularly “abysmal,” according to then-IRS Commissioner John Koskinen. During that filing season, nearly two-thirds of calls were not answered at all, and callers that did get through waited an average of 23 minutes.[10] The dismal state of taxpayer services helped convince Congress to boost IRS funding modestly for 2016 and 2017, which was used to hire seasonal employees to provide phone and correspondence service.[11] This increase led to an improvement: for the 2017 filing season, 21 percent of calls to the IRS’s main taxpayer services line went unanswered, and taxpayers waited an average of 7 minutes to speak to an IRS representative.[12] But with other new demands on the IRS as a result of the tax law, such improvements can’t be maintained for the 2018 filing season absent a funding increase.

Outside of tax season, customer service is even weaker. For instance, the IRS no longer answers any tax law questions outside of tax season. The National Taxpayer Advocate has criticized that policy, stating “the IRS’s continued unwillingness to help taxpayers by answering such a broad range of tax law questions represents a breathtaking abdication of a core function of tax administration.”[13] While this practice is objectionable even in the absence of large tax policy changes, it seems especially untenable for the years ahead, as taxpayers focus on how their taxes will change as they head into filing their first returns under the new law in 2019.

The IRS will need more people to answer phone inquiries, and they will need to be trained on the provisions of the new tax law so they can provide correct answers. Even with the modest funding boost for the IRS in 2017, staffing for taxpayer services in 2017 was still 10 percent (roughly 3,000 employees) below its 2010 level.[14] (See Figure 2.) Further, employee training resources have been cut to the bone. To live within shrunken appropriations, the IRS has had to reduce its employee training budget by two-thirds since 2009, and it spent less than $500 per employee on training in 2017.[15]

In response to the 1986 tax reform, the IRS added 1,300 staff and increased phone capacity by 30 percent.[16] (And in the year before the 1986 tax reform bill was passed, the IRS had roughly 15,000 more employees than it does today.) Following a full review in late 1988, the General Accounting Office concluded that the:

IRS did a good job implementing the Tax Reform Act and preparing for the increased work load it expected during the 1988 filing season. IRS mounted an extensive media campaign to inform taxpayers about tax law changes and to encourage them to file early. It hired and trained additional staff to answer taxpayer questions and process tax returns, extensively tested tax forms before distributing them to the public, and tested service center readiness before the filing season began.[17]

The President, Congress, and IRS should strive for a similar result for the 2019 filing season, though the job will not end in a single year, as discussed below.

Implementation Should Include Restoring and Significantly Bolstering Enforcement

Given the expected spike in taxpayer questions and the risk of backlash if inquiries are not answered, it is understandable that the initial attention of policymakers and the media seems to be on customer service. And successful customer service is critical.

But IRS enforcement must be strengthened, as well, which will pose a dual challenge. First, budget cuts have disproportionately targeted funding for enforcement, and the IRS’s capability to perform this function adequately must be restored. Second, the new tax law’s design will invite taxpayers, particularly affluent ones and corporations with means to hire high-priced accountants and lawyers, to re-characterize their financial affairs strictly for tax purposes, aggressively pushing against the boundaries of the new law. IRS enforcement must be able to identify those who step over the boundaries.

The new tax law will tax various types of income — labor, pass-through, domestic corporate, and international corporate income — at different tax rates. It will also tax pass-through income from some sectors at a different rate than pass-through income from other sectors. Certain deductions can be taken against certain types of income but not others (e.g., pass-throughs generally will be able to deduct more interest expenses than corporations will). Meanwhile, the lines the new law draws within and around various types of “professional services” income are seemingly arbitrary (e.g., taxing a doctor or lawyer differently than an architect or an engineer) — and potentially porous.[18]

As a group of the nation’s top tax experts observed, for example, “the new pass-through deduction will likely result in a massive restructuring of employment and service management across many industries.”[19] As Tax Policy Center fellow and former Treasury Deputy Assistant Secretary of Tax Analysis Gene Steuerle has warned, “perhaps millions will change their form of ownership. Some taxpayers will also find it desirable to create multiple layers of corporations, partnerships, and other pass-through businesses.”[20]

Similarly, the new law adopts a new international corporate tax regime that will no longer subject foreign profits to U.S. tax, except for a minimum tax on certain extraordinary profits. This will create a greater incentive for large corporations to turn domestic profits into foreign profits.

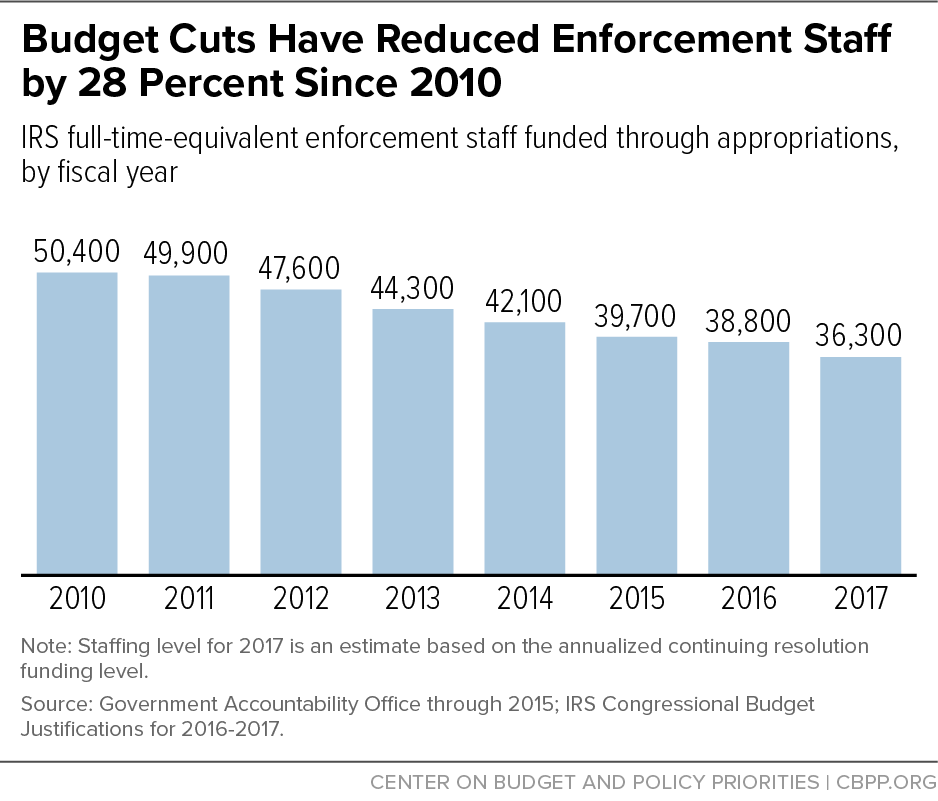

This drive to game the new law poses daunting challenges for the IRS to police and retain the integrity of the tax system. Yet as noted, IRS enforcement funding has been hit hard by funding and staffing reductions since 2010. In 2017, enforcement funding was 21 percent below its 2010 level in inflation-adjusted terms. The agency has lost roughly 14,000 enforcement employees — more than a quarter of its enforcement staff — since 2010.[21] (See Figure 3.)

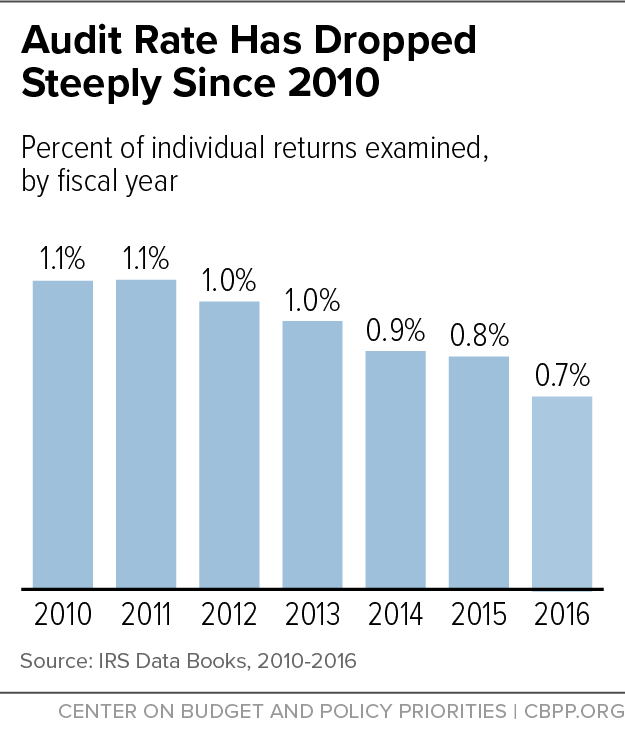

The decline in enforcement has reduced the IRS’s ability to go after tax evaders. The IRS audited just 1 of every 140 individual returns in 2016, down from 1 of 90 returns in 2010.[22] (See Figure 4.) Audit rates have fallen particularly sharply among high-income taxpayers. For instance, the audit rate for returns with incomes of over $1 million fell from its recent peak of 12.5 percent in 2011 to 5.8 percent in 2016.[23]

The IRS has designated high-income taxpayers as an enforcement priority due to their more complex finances and greater risk of noncompliance. Moreover, the return per audit hour is substantial. Among the highest-income returns, those with income above $1 million, the IRS identified over $2,000 in additional liability per audit hour, and for those with income above $5 million, it identified additional liability per audit hour of more than $4,500.[24]

Likewise, the audit rate for large corporations (defined by the IRS as those with assets greater than $10 million) fell from its recent peak of 17.8 percent in 2012 to just 9.5 percent in 2016. As a result, the IRS identified $12 billion less in additional tax liability through audits of large corporations in 2016 than it did in 2010, a decline of nearly 50 percent.[25]

Wealthy people trying to take advantage of the pass-through tax break, and multinationals trying to minimize tax under the new international regime, will not be one-year enforcement challenges. These challenges will last as long as these provisions remain in law.

Conclusion

The new tax law poses an immense challenge that the IRS is ill-prepared to handle, due to a dramatic reduction in its funding and workforce since 2010. Policymakers need to recognize the depth of the IRS’s budget and workforce depletion, as well as the multi-year and multi-dimensional nature of the response that will be urgently needed to implement and enforce the recently enacted tax changes. The Trump Administration and Congress should make the IRS a top priority in the negotiations of how to allocate funding for 2018, and should commit to sufficient multi-year funding for the IRS to implement and enforce the new tax law.

End Notes

[1] Angie Petty, “Will IRS Have The Resources to Implement Tax Reform?,” Deltek, January 2, 2018, https://www.deltek.com/en/learn/blogs/b2g-essentials/2018/01/will-irs-have-the-resources-to-implement-tax-reform.

[2] National Taxpayer Advocate, “2017 Annual Report to Congress: Executive Summary,” December 31, 2017, p. 5, https://taxpayeradvocate.irs.gov/Media/Default/Documents/2017-ARC/ARC17_ExecSummary.pdf.

[3] Ibid.

[4] Staffing level for 2017 is an estimate based on the annualized continuing resolution funding level. Government Accountability Office, “Internal Revenue Service: Observations on IRS’s Operations, Planning, and Resources,” February 27, 2015, p. 35, http://www.gao.gov/assets/670/668769.pdf; Internal Revenue Service, “Congressional Justification for Appropriations and Annual Performance Report and Plan,” 2017, https://www.treasury.gov/about/budget-performance/CJ18/05.%20%20IRS%20-%20FY%202018%20CJ.pdf.

[5] Former IRS Commissioners Mortimer M. Caplan, Sheldon S. Cohen, Lawrence B. Gibbs, Fred T. Goldberg, Jr., Shirley D. Peterson, Margaret M. Richardson, and Charles O. Rossotti, “Letter to the Honorable Thad Cochran, the Honorable Barbara A. Mikulski, the Honorable Harold Rogers, and the Honorable Nita M. Lowey: IRS Appropriations for Fiscal Year 2016,” November 9, 2015, http://taxprof.typepad.com/files/former-irs-commissioners-letter-on-agency-budget.pdf.

[6] Charles S. Clark, “House Subcommittee Mulls IRS Funding to Implement Tax Reform,” Government Executive, December 13, 2017, http://www.govexec.com/management/2017/12/house-subcommittee-mulls-irs-funding-implement-tax-reform/144540/.

[7] Charles S. Clark, “Could a Resource-Strapped IRS Handle Tax Reform?,” Government Executive, November 30, 2017, http://www.govexec.com/management/2017/11/could-resource-strapped-irs-handle-tax-reform/144193/.

[8] National Taxpayer Advocate, “2017 Annual Report to Congress: Executive Summary,” December 31, 2017, p. 5, https://taxpayeradvocate.irs.gov/Media/Default/Documents/2017-ARC/ARC17_ExecSummary.pdf.

[9] Ibid, p. 5.

[10] National Taxpayer Advocate, “FY 2016 Objectives Report to Congress: Review of the 2015 Filing Season,” June 30, 2017, p. 9, http://www.taxpayeradvocate.irs.gov/Media/Default/Documents/2016-JRC/2015_Filing_season_review.pdf.

[11] IRS, 2018 Congressional Justification.

[12] National Taxpayer Advocate, “FY 2018 Objectives Report to Congress: Review of the 2017 Filing Season,” June 28, 2017, p. 6, https://taxpayeradvocate.irs.gov/Media/Default/Documents/2018-JRC/JRC18_Volume1_2017Review.pdf.

[13] Ibid, p. 7.

[14] Staffing level for 2017 is an estimate based on the annualized continuing resolution funding level. Government Accountability Office, 2015 and IRS 2018 Congressional Justification.

[15] National Taxpayer Advocate, “Annual Report to Congress 2017: Executive Summary,” p. 4, https://taxpayeradvocate.irs.gov/Media/Default/Documents/2017-ARC/ARC17_ExecSummary.pdf.

[16] Ibid, p.5.

[17] General Accounting Office, “Internal Revenue Service: Effective Implementation of the Tax Reform Act Led to Uneventful 1988 Filing Season,” November 1988, p. 2, https://www.gao.gov/assets/150/147107.pdf.

[18] For more information on pass-throughs, see Reuven Avi-Yonah et al., “The Games They Will Play: An Update on the Conference Committee Tax Bill,” revised December 22, 2017, https://ssrn.com/abstract=3089423.

[19] Ibid.

[20] C. Eugene Steuerle, “The TCJA Will Create More Complexity For Taxpayers Than It Claims,” Tax Policy Center, January 5, 2018, http://www.taxpolicycenter.org/taxvox/tcja-will-create-more-complexity-taxpayers-it-claims.

[21] Staffing level for 2017 is an estimate based on the annualized continuing resolution funding level. Government Accountability Office, 2015 and IRS 2018 Congressional Justification.

[22] Internal Revenue Service, “2016 Data Book,” https://www.irs.gov/pub/irs-soi/16databk.pdf and Internal Revenue Service, “2010 Data Book,” https://www.irs.gov/pub/irs-soi/10databk.pdf.

[23] IRS data books, 2011-2016.

[24] IRS defines high-income returns as those with total positive income over $200,000. Treasury Inspector General for Tax Administration, “Improvements Are Needed in Resource Allocation and Management Controls for Audits of High-Income Taxpayers,” September 18, 2015, https://www.treasury.gov/tigta/auditreports/2015reports/201530078fr.pdf.

[25] IRS data books, 2010-2016.