BEYOND THE NUMBERS

Top 10 Federal Tax Charts

These ten charts — previewed in our Countdown to Tax Day series — provide context for some important tax policy issues.

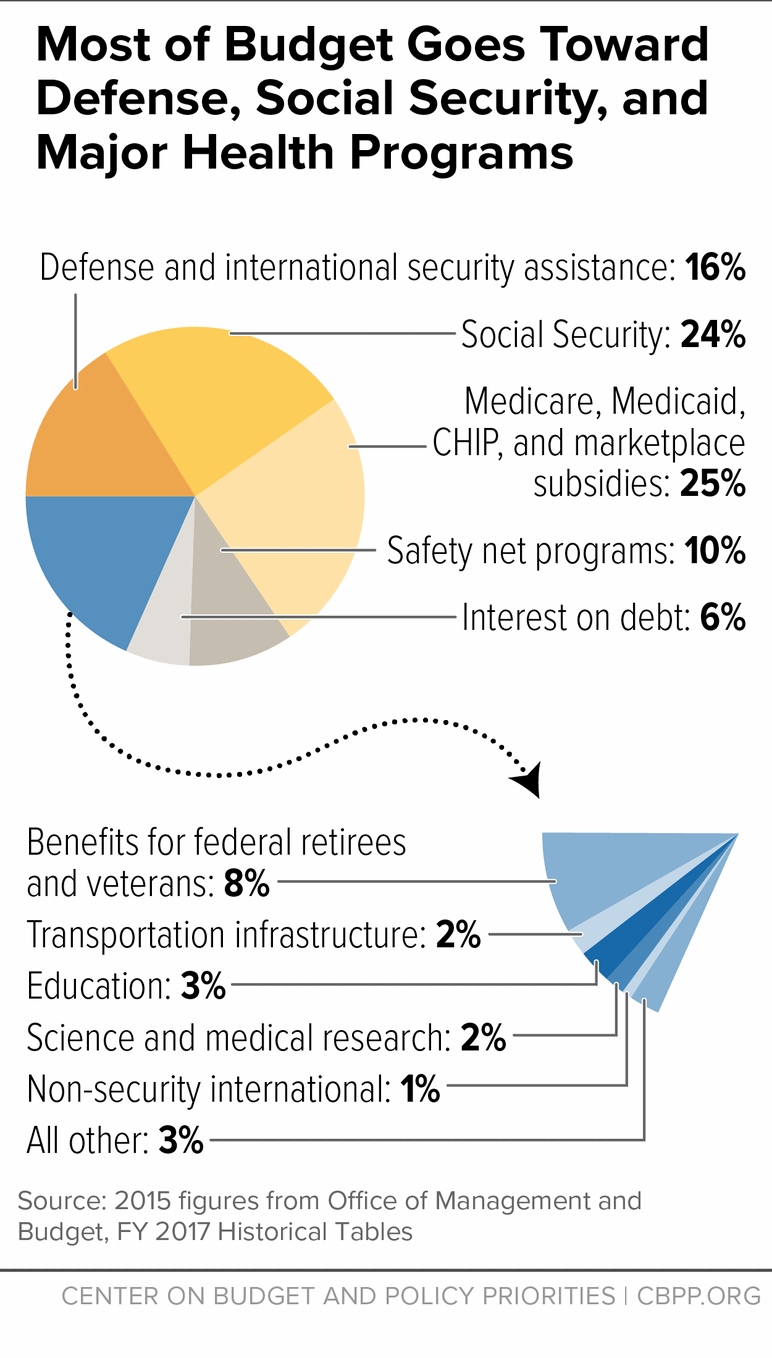

Our first chart reminds us why we pay taxes by showing where the money goes. Three large areas account for roughly two-thirds of the budget: health programs such as Medicare, Social Security, and defense and international security assistance. The safety net (including programs like SNAP and unemployment insurance) plus interest on the debt make up roughly another sixth.

The remainder — roughly 20 percent — is everything else, from infrastructure to science research, the FBI, education, veterans’ programs, and so on.

So, a part of almost every tax dollar goes to things like a safer highway bridge, a new hip for an elderly person, a soldier’s gear, or diabetes research.

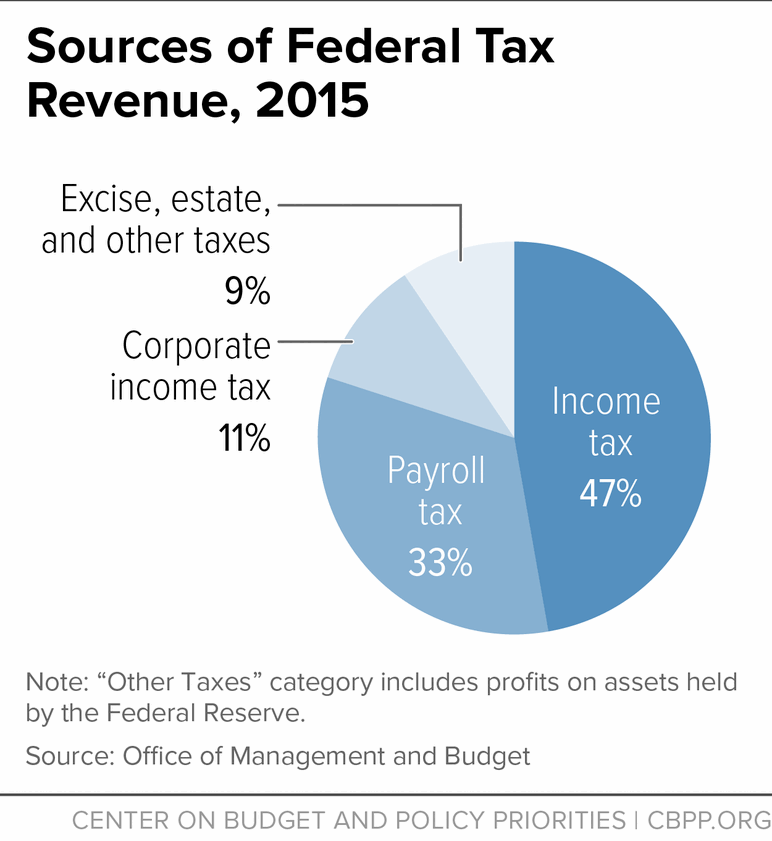

Our second chart shows where federal tax dollars come from.

The individual income tax is the largest federal tax, generating close to half of federal revenues. It’s progressive, meaning that tax rates generally rise as income rises.

The second largest category is payroll taxes to fund Social Security and Medicare, which account for a third of federal revenue. Payroll taxes as a whole are regressive: lower-income people pay a larger share of their incomes in tax than higher-income people do. (That’s because people pay Social Security tax only on their first $118,500 in wages.) Most lower- and middle-income people pay more in payroll taxes than federal income taxes.

But, while payroll taxes are regressive, Social Security and Medicare overall are progressive when you account for the benefits they provide as well as the taxes they collect.

Corporate taxes provide just 11 percent of federal revenue. The remaining 9 percent comes from various excise taxes on tobacco, alcohol, and other goods, as well as the estate tax on large inheritances. Despite growing evidence — and public awareness — of the high concentration of income and wealth at the top, policymakers have shrunk the estate tax dramatically since 2001. Consequently, only about 2 of every 1,000 estates have to pay any estate tax.

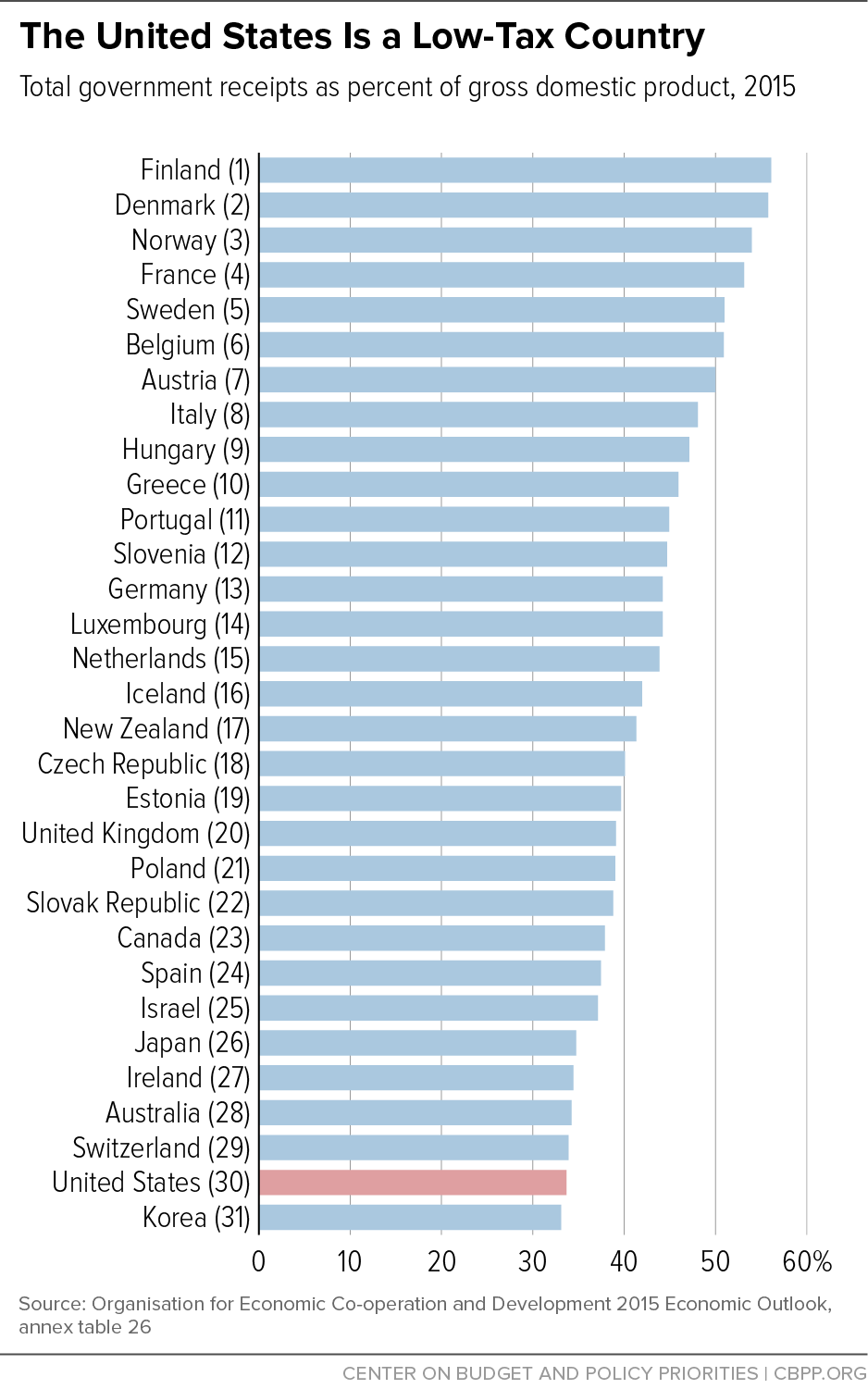

Our third chart shows that the United States is a low-tax country, contrary to claims like those from GOP presidential candidate Donald Trump. Among members of the Organisation for Economic Co-operation and Development, only South Korea has lower government receipts as a share of the economy than the United States.

Federal taxes are generally designed to ensure that federal income and payroll taxes don’t tax people into — or deeper into — poverty. The glaring exception is childless adults, roughly 7.5 million of whom are, in fact, taxed into or deeper into poverty.

That’s mostly because they’re largely excluded from the Earned Income Tax Credit (EITC), which, for them, is too small (or, for many of them, non-existent) to offset their income taxes and the employee share of their payroll taxes.

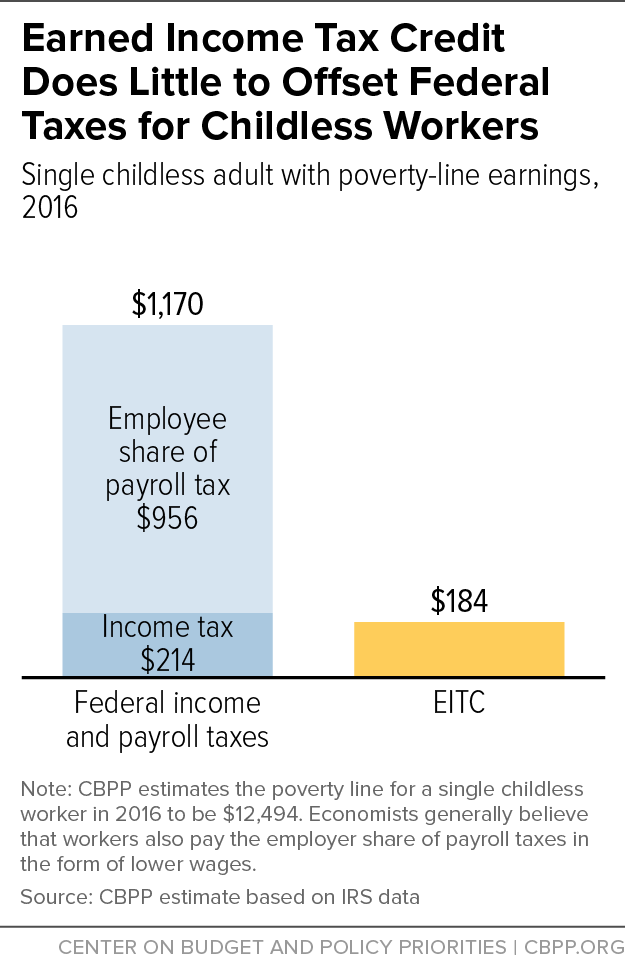

Our fourth chart highlights an example: a 25-year-old single woman making poverty-line wages in 2016 ($12,494) as a retail salesperson. Under current law, she’s taxed nearly $1,000 into poverty:

- She will have $956 (7.65 percent of her earnings) in Social Security and Medicare payroll taxes deducted from her paychecks.

- Her taxable income, after subtracting a $6,300 standard deduction and a $4,050 personal exemption, is $2,144. She’s in the 10 percent bracket, so she’ll have a $214 income tax liability.

- Together, her $214 in income tax liability and $956 in payroll taxes add up to $1,170.

- Yet, she’s eligible only for a small $184 EITC, so her federal tax liability will be $1,170 minus $184 — or $986.

Policymakers should make it a top priority to fix this glaring flaw in the tax code by strengthening the EITC for childless workers.

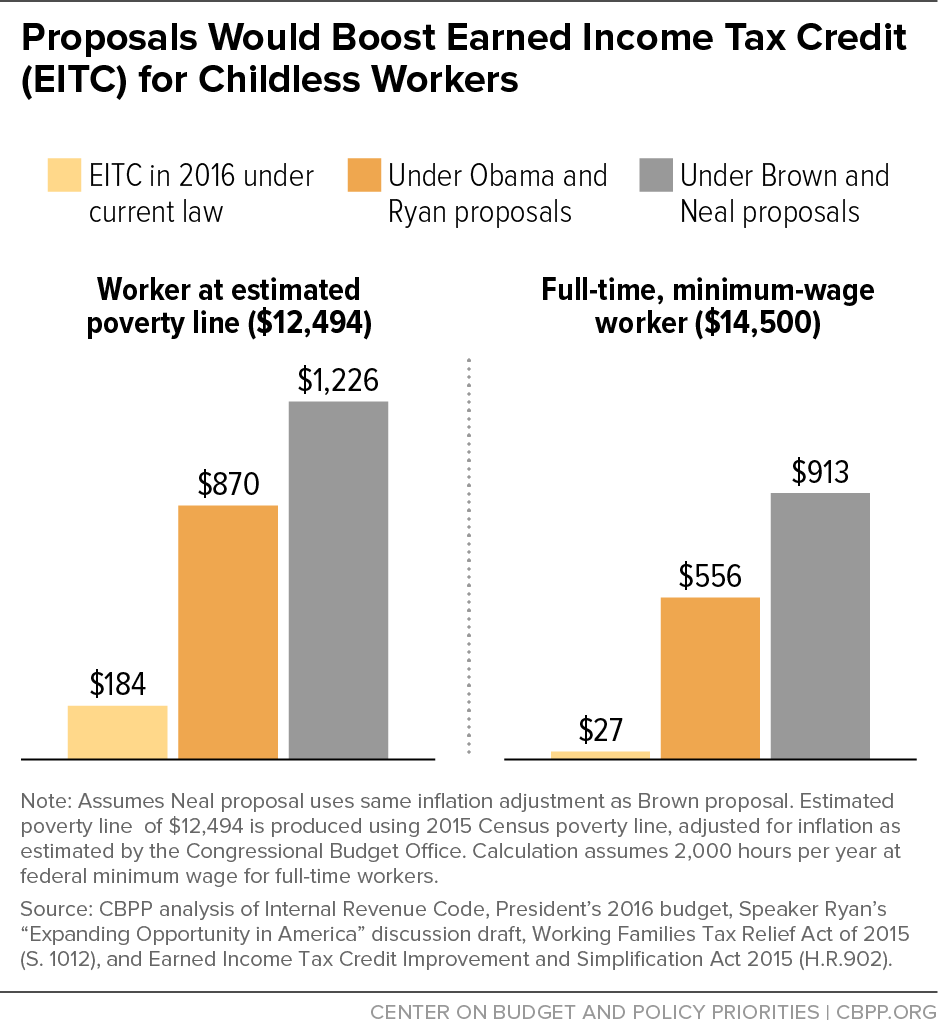

As our fifth chart shows, policymakers of both parties — including President Obama and House Speaker Paul Ryan, as well as Senate Finance Committee member Sherrod Brown and House Ways and Means Committee member Richard Neal — have proposed to increase the EITC for childless workers and to lower the eligibility age, which would move toward making a key principle universal: nobody should be taxed into poverty.

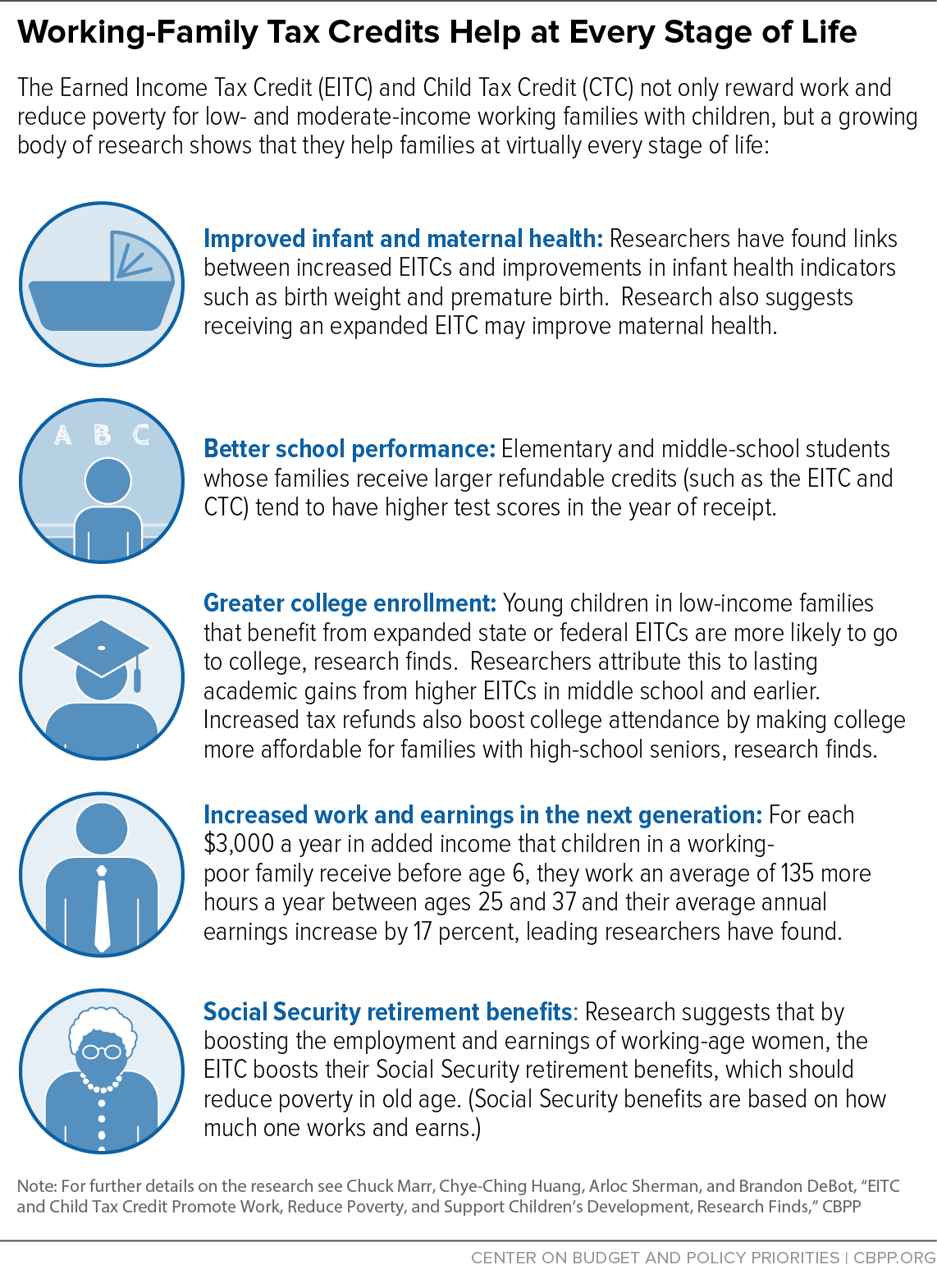

There’s understandable skepticism that lawmakers will act on that issue this year. But provisions in last year’s tax bill show the gains that are possible. The bipartisan tax bill that policymakers enacted in December included a major anti-poverty achievement in making permanent critical improvements in the Child Tax Credit (CTC) and Earned Income Tax Credit (EITC) that would have expired at the end of 2017. The improvements will continue to raise roughly 16 million people, including up to 8 million children, above or closer to the poverty line in 2018 and beyond.

The EITC and CTC encourage and reward work, and growing evidence suggests that income from these tax credits leads to better maternal and infant health, improved school performance, higher college enrollment, and increased work effort and earnings in adulthood, as our sixth chart shows.

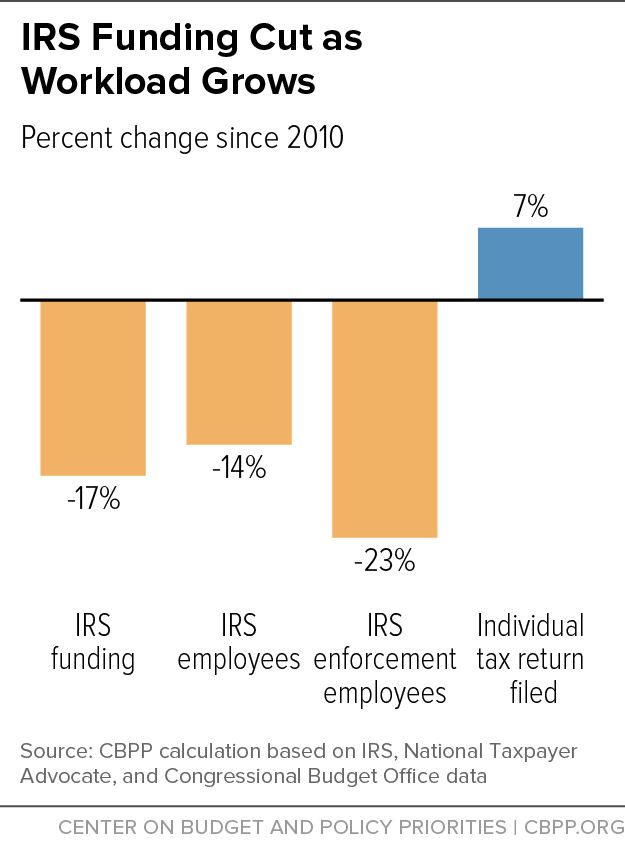

The Internal Revenue Service (IRS) plays a fundamental role in our system of government — helping taxpayers comply with the tax code, ensuring that the tax laws are enforced fairly and credibly, and collecting nearly all of the revenue that funds federal programs from defense to the safety net, roads, scientific research, and education. While policymakers should give the IRS the resources each year to do its job, they’ve fallen short in recent years.

In fact, since 2010, lawmakers have deliberately targeted the agency with severe budget cuts. Last year’s budget bill provided a modest — but far from adequate — funding increase. Yet even with it, IRS funding is still 17 percent below 2010 levels after accounting for inflation. In particular, policymakers have gutted enforcement funding, making it easier for tax cheats to escape audits. All of these cuts came in the context of a rising number of tax returns to process (as our seventh chart shows), new legislative mandates, and the growing threat of identity theft.

It’s essential that lawmakers take a more meaningful step this year to restore IRS funding.

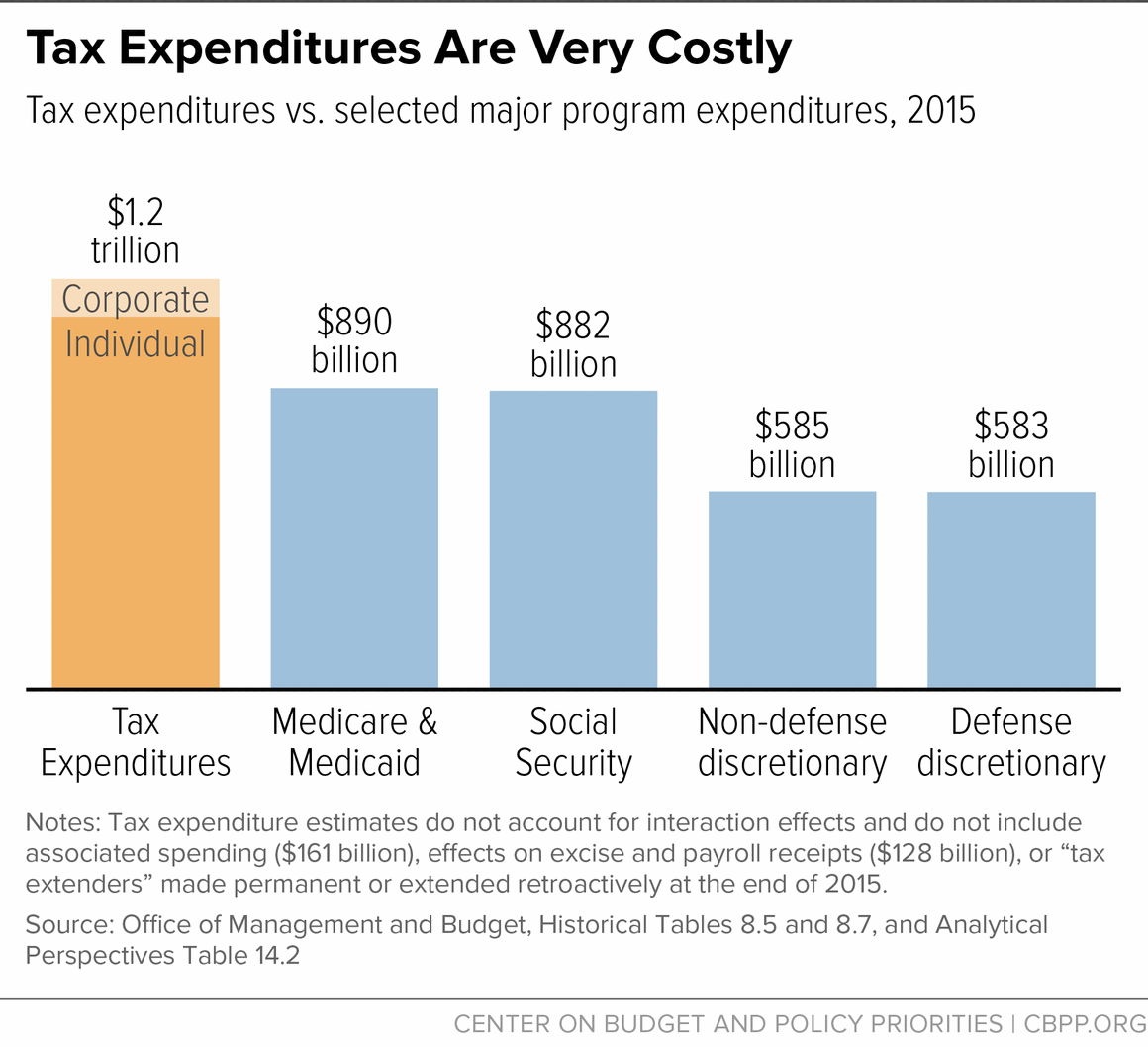

One area of the federal tax code that’s ripe for reform is “tax expenditures” — or subsidies delivered to individuals or businesses through deductions, exclusions, and other tax preferences.

In 2015, tax expenditures cut federal income tax revenue by over $1.2 trillion. As our eighth chart shows, that’s more than that year’s cost of Social Security, or the combined cost of Medicare and Medicaid, or non-defense or defense discretionary spending.

The biggest income tax expenditure for individuals in 2015 was the provision allowing households to exclude the value of employer-provided health insurance from their taxable income, Treasury estimates. Other prominent tax breaks include the deduction for home mortgage interest and the lower tax rates for capital gains than for earned income.

One of the largest corporate tax expenditures is the “deferral of income from controlled foreign corporations,” which allows multinational corporations to delay paying U.S. taxes on their foreign profits, sometimes indefinitely. Wage and salary earners, in contrast, have to pay taxes on their earnings in the year that they earn them.

Tax expenditures aren’t just costly; they often provide their largest subsidies to high-income people — the people least likely to need a financial incentive to do whatever the tax break is designed to encourage, such as buying a home or saving for retirement.

For these reasons, policymakers considering ways to address the nation’s long-term budget problems should consider reforming tax expenditures. As President Reagan’s former chief economic advisor, Harvard economist Martin Feldstein, has said, “cutting tax expenditures is really the best way to reduce government spending.”

Tax Day is a timely reminder that wage and salary earners, and small and domestic businesses, pay taxes on their income and profits each year to pay for the nation’s priorities. Yet many multinational corporations effectively get to choose each year whether and how much U.S. tax to pay on their foreign profits — and many choose to avoid those taxes indefinitely.

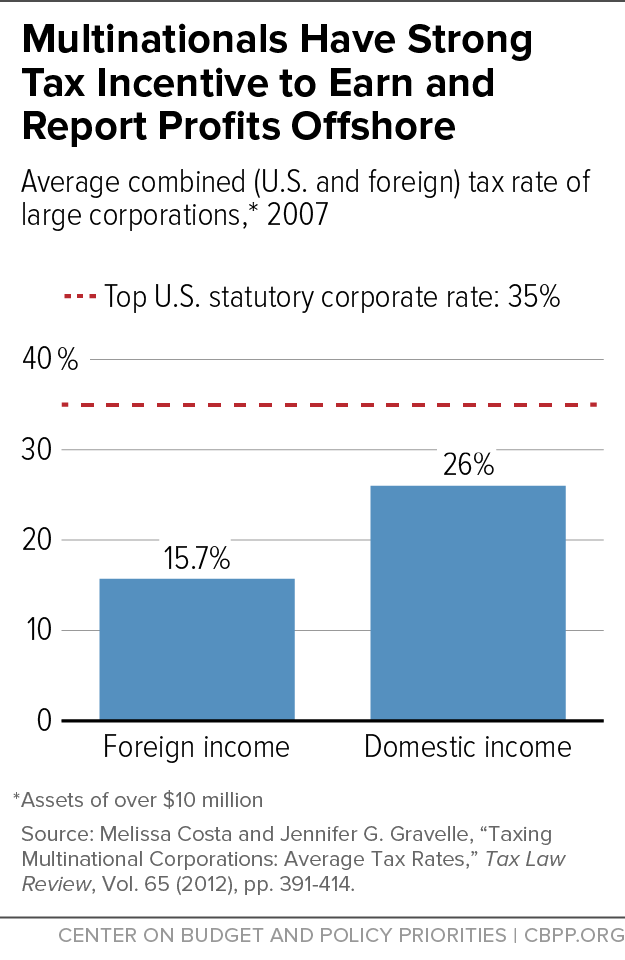

All countries face a basic question of how to tax profits that domestically based companies earn in other countries. A worldwide tax system taxes them the same as domestically generated profits, whereas a territorial system imposes no taxes on foreign profits. The United States has a hybrid system that taxes foreign and domestic profits at the same rate but only taxes foreign profits when they’re brought back to the United States, allowing companies to defer U.S. tax indefinitely.

This deferral feature is one of the costliest corporate tax expenditures, as we noted the other day. And it gives multinational corporations a powerful incentive to artificially shift U.S.-earned profits overseas.

Shifting a large amount of U.S.-earned profits to foreign tax havens is one way that multinationals achieve a much lower overall tax rate for their foreign income than their domestic income, as our ninth chart shows. (Various other tax breaks enable multinationals to pay a lower share of their domestic profits in tax than the top statutory corporate tax rate of 35 percent.) Reducing the tax code’s foreign tilt should be a core element of any future corporate tax reform.

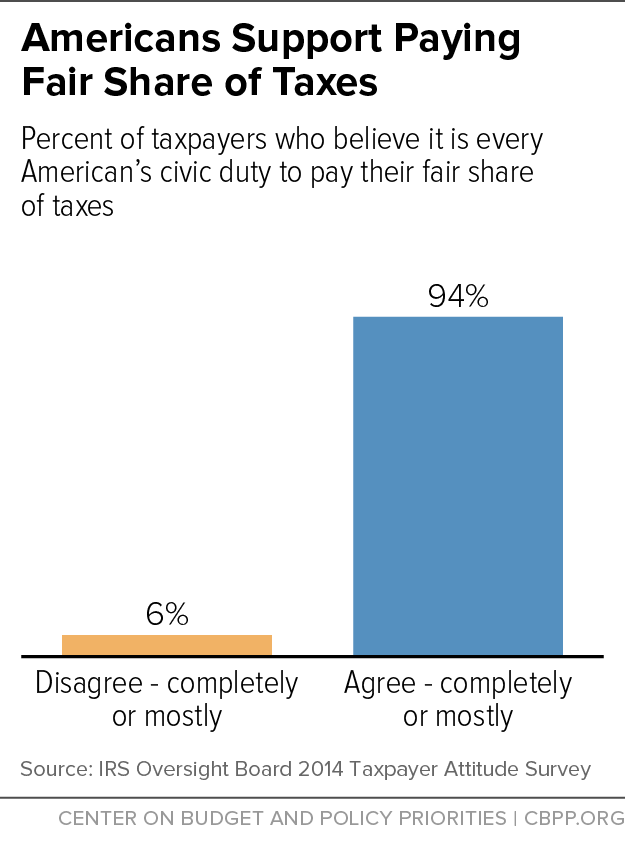

Our tenth chart shows that, contrary to the conventional wisdom, Americans overwhelmingly take pride in paying their taxes, as a 2014 survey by the IRS Oversight Board shows.

Our country’s tax system is based on voluntary compliance. Its proper functioning, therefore, depends on lots of civic duty and responsibility, and that’s exactly what exists. Some 94 percent of Americans believe it’s their civic duty to pay their fair share of taxes.

In The Atlantic last April, Vanessa Williamson highlighted some interview anecdotes that hint at the reasons behind these strong survey results:

- A 28-year-old from Utah: “It feels good to contribute.”

- A former Marine: “[It’s] the cost of being an American.”

- A woman from Kansas: “[T]he country has to be taken care of.”

Beyond the pride of fulfilling a fundamental civic obligation, Americans can take pride in where their tax dollars are going (see here for state tax dollars and here for federal). As one woman from Florida told Williamson, “maybe my little bit of money that I’m putting in is paying somebody else’s Social Security or Medicare.”