BEYOND THE NUMBERS

Roundup: Administration Efforts to Sabotage the Affordable Care Act

The House, which last week voted to block Trump Administration guidance weakening standards for state Affordable Care Act (ACA) waivers, is expected to vote today on a bill reversing the Administration’s expansions of substandard health plans and cuts to outreach and enrollment assistance. Here are our recent pieces on some of the major issues involved.

Expanding Skimpy Short-Term Health Plans

-

Blocking Trump Rule on Short-Term Health Plans Would Benefit Consumers

“The House will vote this week on a bill curbing so-called “short-term” health plans, which are exempt from the ACA’s consumer protections. Some argue that the bill would hurt consumers, citing a Congressional Budget Office (CBO) estimate that it would cause some people to become uninsured. But in reality, CBO’s analysis underscores the dangers of short-term plans. It confirms that short-term plans have large coverage gaps that expose consumers to catastrophic costs and that a Trump Administration rule expanding the availability of these plans will raise costs for people with pre-existing conditions. By blocking the rule and making other changes, the House bill would increase the number of people with comprehensive health coverage. . . .”

-

CBO: Administration’s Short-Term Plans Rule Means a Return to Pre-ACA Practices

“The House Energy and Commerce Health Subcommittee will consider legislation tomorrow to curb so-called ‘short-term’ health plans, which are exempt from the ACA’s consumer protections. Some argue, wrongly, that these plans are less harmful than they appear, and they have cited a recent Congressional Budget Office (CBO) report to make their case. That report, however, confirms that the Trump Administration’s expansion of short-term plans will leave people who buy these plans with large gaps in coverage and will raise costs for people with pre-existing health conditions. . . .”

-

Key Flaws of Short-Term Plans Pose Risks for Consumers

“Federal rule changes to short-term health plans are set to take effect on October 2, newly allowing insurers to offer them to consumers for up to one year (instead of three months) and renew or extend them even longer. . . . [I]n most states, short-term plans are exempt from pre-existing-condition protections and benefit standards that individual-market plans must meet. This new parallel market for skimpy plans will expose consumers buying these plans to new risks and raise premiums for those seeking comprehensive coverage, especially middle-income consumers with pre-existing conditions. . . .”

-

More States Protecting Residents Against Skimpy Short-Term Health Plans

“Since the Trump Administration issued new rules last year expanding short-term health plans, which are exempt from the ACA’s protections for people with pre-existing conditions and benefit standards, nearly a dozen states have set their own limits and consumer protections for short-term plans. Others should follow suit. . . .”

Letting States Waive Key ACA Provisions Without Protecting Consumers

-

“Trump Administration guidance changed how the federal government will evaluate so-called 1332 waiver proposals from states in ways that would weaken protections for people with pre-existing conditions and other vulnerable groups. The House is expected to vote today on a bill to roll back the Administration’s changes. . . . The Administration has insisted that its 1332 guidance doesn’t affect ACA pre-existing condition protections, and in fact, certain of those provisions are not waivable under section 1332. However, the guidance and discussion paper promote waivers that would weaken protections and benefits that people with pre-existing health conditions need the most, by encouraging states to promote plans that lack ACA pre-existing condition protections; reduce the benefits that plans cover; increase net premiums, deductibles, and other cost-sharing charges; and rescind protections for vulnerable populations. . . .”

-

Commentary: Trump Administration Rules on Health Waivers Weaken Pre-Existing Condition Protections

“The ACA has helped millions of people with pre-existing health conditions enroll in affordable, comprehensive health coverage, including by barring insurers from denying them coverage and establishing new standards for premium rating and benefits. But now, the Trump Administration is using an ACA provision to let states weaken or eliminate protections for this same group. . . .”

Cutting Marketplace Outreach and Consumer Assistance

-

In Latest ACA Sabotage, Administration Nearly Eliminates Marketplace Enrollment Assistance Funds

“The Trump Administration this week slashed funding for consumer enrollment assistance and outreach through the ACA navigator program. The funding cuts, and other changes to the program, will reduce access to crucial assistance that helps consumers make informed decisions about their insurance and sign up for and maintain comprehensive coverage — yet another in the Administration’s efforts to weaken the ACA. . . .”

-

Navigator Funding Cuts Will Leave Many Marketplace Consumers on Their Own

“The Department of Health and Human Services (HHS) announced yesterday which groups will receive navigator funds in the 34 states where the federal government runs the ACA marketplace. But the Trump Administration’s sharp cuts in overall navigator funding in the last two years mean that many consumers who buy insurance through HealthCare.gov will be on their own to complete the complex application and enrollment process to get affordable health coverage. . . .”

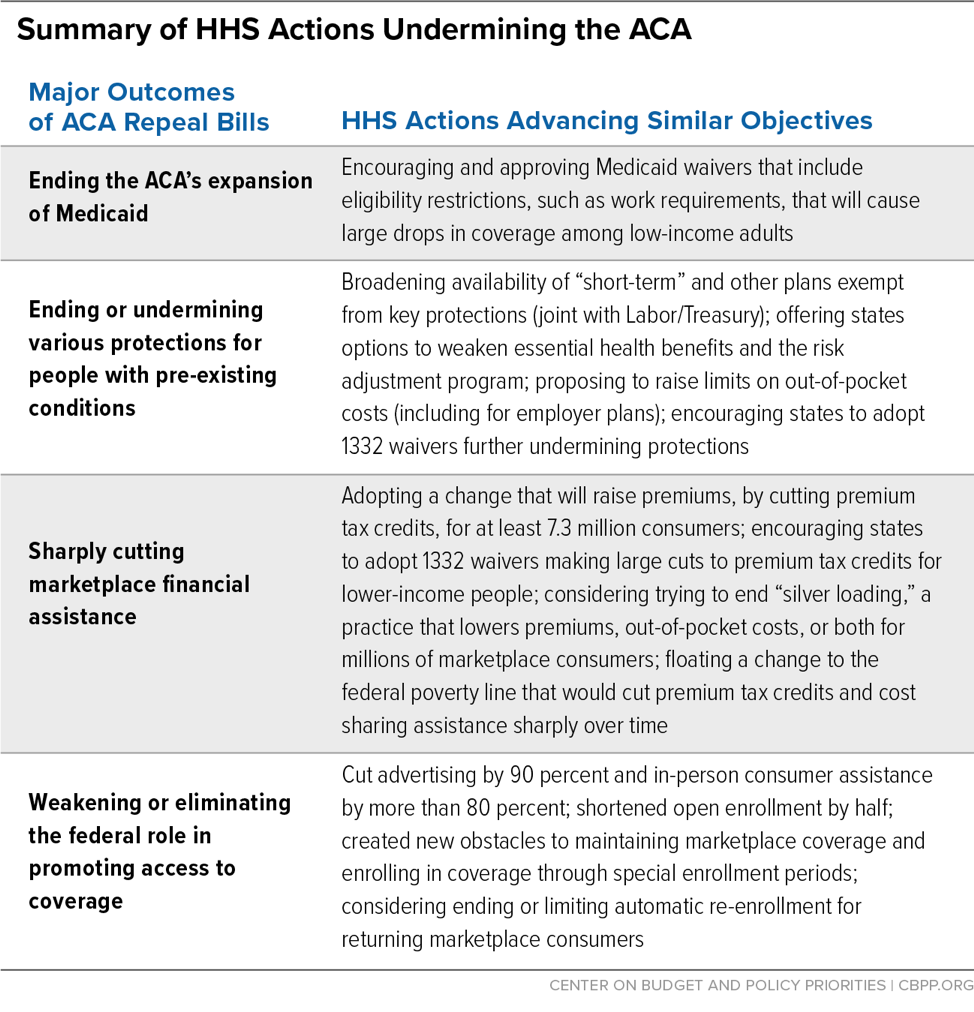

For more information, see our Sabotage Watch timeline of Administration actions that would sabotage the ACA. The table below shows how with a legislative repeal of the ACA off the table for now, the Administration has continued to pursue some of the major policy objectives of the repeal bills that Congress rejected in 2017 through rulemaking and other administrative actions.