BEYOND THE NUMBERS

Many Marketplace Consumers Eligible for Zero-Premium Coverage

More than ever, low- and moderate-income consumers can find good deals for health coverage — and may have their premiums covered entirely by tax credits — if they sign up before open enrollment for the Affordable Care Act’s (ACA) marketplaces ends on December 15. Marketplace premiums fell slightly overall for 2019, and many people can find affordable options with various levels of cost-sharing (such as deductibles and co-pays).

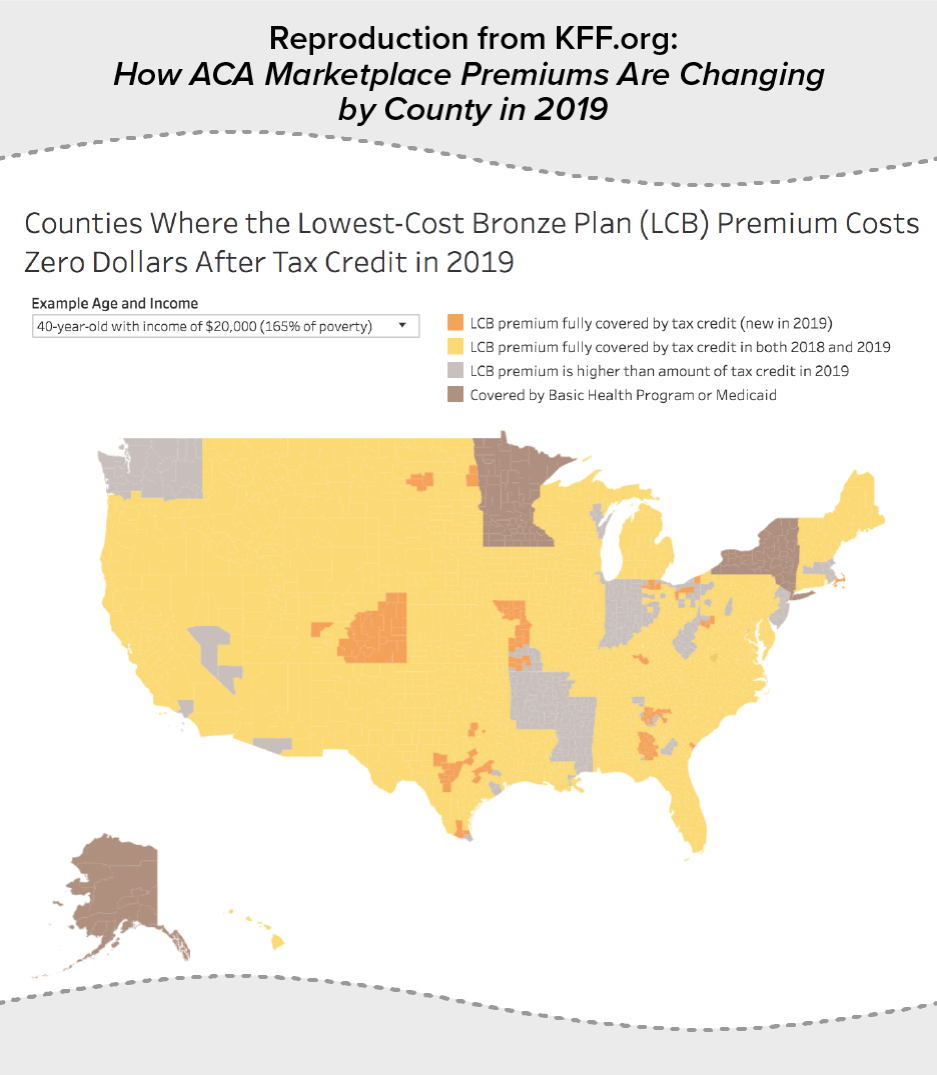

In most of the country — 2,532 of 3,142 counties — a 40-year-old with $20,000 in income can find a bronze plan with a premium that’s fully covered by the premium tax credit, according to the Kaiser Family Foundation. (See map.) At a $30,000 income, these plans that effectively carry no premiums are available in 659 counties.

There are trade-offs to enrolling in a bronze plan: deductibles are high and people with incomes below 250 percent of the federal poverty line miss out on cost-sharing assistance they’d get if they enrolled in a silver plan. On the other hand, more than half of bronze plans cover some services without requiring enrollees to pay the deductible first (for example, a handful of office visits with only a co-pay). And, for people who mostly want protection against catastrophic health costs, bronze plans may offer adequate protection.

Consumers in many counties also can enroll in gold plans — which typically have higher premiums but lower deductibles and other cost-sharing — for less than the cost of the lower-tiered silver plans. Unsubsidized premiums for gold plans are less than they are for silver plans in a quarter of counties (792 of 3,142 counties), meaning that a person without a subsidy can get a plan with lower cost-sharing obligations for less than they’d pay for a higher cost-sharing plan. Some subsidized consumers — in 411 counties, 40-year-olds with income of $20,000 — can get a zero-premium gold plan after accounting for premium tax credits.

These deals are largely an unintentional by-product of the Trump Administration’s decision in 2017 to end cost-sharing reduction payments, which reimburse insurers for the cost-sharing assistance that the ACA requires them to provide to lower-income enrollees in silver plans. This led insurers to “load” the cost of that federally mandated benefit into the silver plan premiums, raising them relative to the cost of other plan tiers. Higher silver plan premiums have meant higher premium tax credits, which then cover a greater share of the cost of lower-premium bronze plans or higher-premium gold plans.

Many consumers don’t know that the clock is ticking on these deals, due to the Administration’s cuts to advertising, consumer assistance, and navigator funding. A survey recently found that only one-quarter of people who buy their own insurance or are uninsured are aware of the December 15 open enrollment deadline.