BEYOND THE NUMBERS

Ahead of Social Security’s 80th birthday this Friday, we’ve updated our backgrounder listing our top ten facts about the program. The first three, summarized below, explain that Social Security provides a foundation on which workers can build for retirement as well as help for workers who become disabled and families whose breadwinner dies.

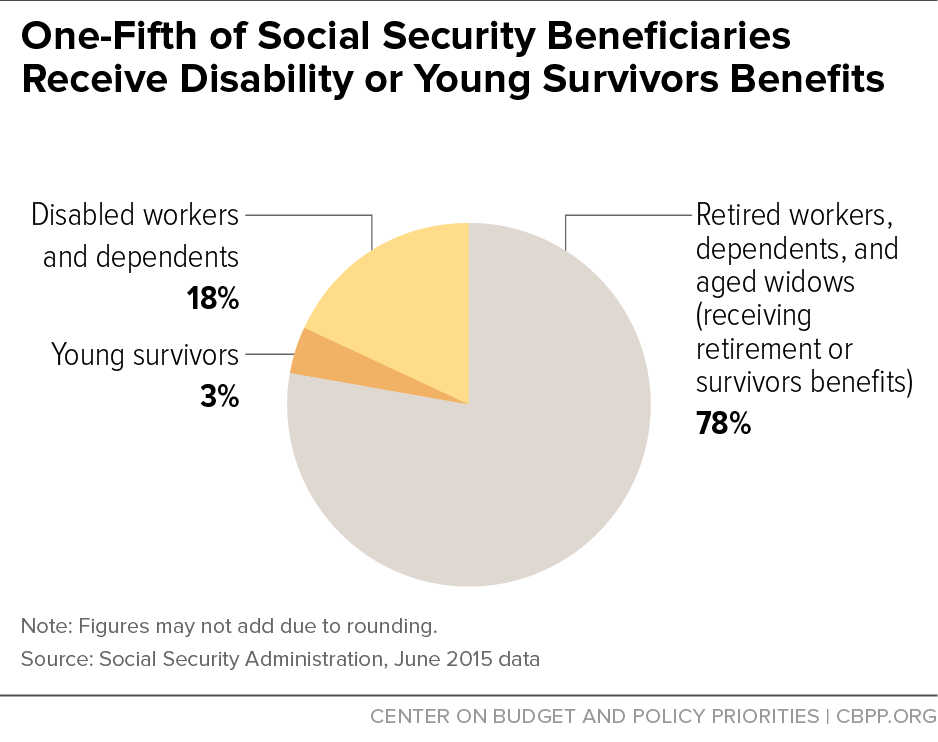

Fact #1: Social Security is more than just a retirement program. It provides important life insurance and disability insurance protection as well. Some 60 million people, or more than one in every six U.S. residents, collected Social Security benefits in June 2015. While three-quarters of them received benefits as retirees or elderly widow(er)s, 11 million (18 percent) received disability insurance benefits, and 2 million (3 percent) received benefits as young survivors of deceased workers.

The risk of disability or premature death is greater than many people realize. Of recent entrants to the labor force, about one-third (36 percent of men and 31 percent of women) will become disabled or die before reaching the full retirement age.

Fact #2: Social Security provides a guaranteed, progressive benefit that keeps up with increases in the cost of living.

Social Security benefits are based on the earnings on which you pay Social Security payroll taxes. The higher your earnings (up to a maximum taxable amount, currently $118,500), the higher your benefit.

Social Security benefits are progressive: they represent a higher proportion of a worker’s previous earnings for workers at lower earnings levels.

Once someone starts receiving Social Security, his or her benefits automatically increase to keep pace with inflation, helping to ensure that people do not fall into poverty as they age.

Fact #3: Social Security provides a foundation of retirement protection for nearly every American, and its benefits are not means-tested.

Almost all workers participate in Social Security by making payroll tax contributions, and almost all elderly people receive Social Security benefits. In fact, 97 percent of people aged 60-89 either receive Social Security or will receive it. The near-universality of Social Security brings many important advantages.

Social Security provides a foundation of retirement protection for people at all earnings levels. It encourages private pensions and personal saving because it isn’t means-tested — in other words, it doesn’t reduce or deny benefits to people whose current income or assets exceed a certain level. Social Security provides a higher annual payout than private retirement annuities per dollar contributed because its risk pool is not limited to those who expect to live a long time, no funds leak out in lump-sum payments or bequests, and its administrative costs are much lower.

Indeed, universal participation and the absence of means-testing make Social Security very efficient to administer. Administrative costs amount to only 0.7 percent of annual benefits, far below the percentages for private retirement annuities.

Finally, the universal nature of Social Security assures its continued popular and political support. Large majorities of Americans say that they don’t mind paying for Social Security because they value it for themselves, their families, and millions of others who rely on it.