Tax Returns: A Comprehensive Assessment of the Bush Administration's Record on Cutting Taxes

Letting High-Income Tax Cuts Expire Is Proper Response to Nation’s Short- and Long-Term Challenges

July 26, 2010

Executive Summary

The Bush Administration has stood in favor of tax cuts through thick and thin. In the midst of a booming economy and large projected budget surpluses, President Bush’s top economic policy initiative — both as a candidate in 2000 and upon taking office — was to cut taxes. When the economy slowed, the Bush Administration’s response also was dominated by tax cuts. Now, in the face of yawning deficits and its own pledge to reduce them, the Administration has again put forward large, permanent tax cuts as part of its most recent budget.

This analysis offers a comprehensive review of the Bush Administration’s tax cuts. It assesses their costs, benefits to different income groups, and economic effects to date, as well as down the road. It both synthesizes previous findings about the individual tax measures and includes new findings about their combined effects, using new distributional analyses by the

- The Bush tax cuts have contributed to revenues dropping in 2004 to the lowest level as a share of the economy since 1950, and have been a major contributor to the dramatic shift from large projected budget surpluses to projected deficits as far as the eye can see.

- The tax cuts have conferred the most benefits, by far, on the highest-income households — those least in need of additional resources — at a time when income already is exceptionally concentrated at the top of the income spectrum.

- The design of these tax cuts was ill-conceived, resulting in significantly less economic stimulus than could have been accomplished for the same budgetary cost. In part because the tax cuts were not as effective as alternative measures would have been, job creation during this recovery has been notably worse than in any other recovery since the end of World War II.

If the Administration’s latest tax proposals — which would make permanent most of the tax cuts enacted in 2001 and 2003 and establish new tax cuts on top of that — are enacted, the long-term results are likely to be even more troubling. Over the next 10 years, total tax-cut costs will equal $3.9 trillion, reaching nearly $600 billion or 3.3 percent of the economy in 2014 alone. (These calculations include the effects of the higher interest payments caused by the tax cuts.) The resulting higher deficits will slow future economic growth, saddle future generations with sizable interest payments, and leave the nation ill-prepared not only for the retirement of baby boomers but also for responding to potential future crises — from security matters to natural or environmental disasters — the particulars of which are unknown today.

Pressure to reduce these deficits will mount. Because the tax cuts are so tilted toward the highest-income households — and become even more so over time, as some of the upper-income tax cuts phase-in — the burden of financing these lopsided tax cuts ultimately is likely to be borne disproportionately by households who gain only modestly from the tax cuts. This will be the case unless offsetting spending cuts or tax increases are enacted that reduce benefits or raise taxes primarily on high-income households. As a result, over the long term most Americans may well be net losers from the tax cuts.

Cost of Tax Cuts

The Tally So Far

The three rounds of tax-cut legislation (in 2001, 2002, and 2003) account for a substantial share of the nation’s current deficit.

- The tax cuts would reduce revenues by $276 billion in 2004, according to Joint Committee on

Tax ation estimates. Further, the interest costs associated with the enacted tax cuts would equal $20 billion, using CongressionalBudget Office assumptions. The total cost would therefore be $297 billion, or 2.6 percent of the economy (or GDP). - Using these estimates, the cost of the tax cuts account for more than half of the 2004 deficit, which CBO estimates to be $477 billion or 4.2 percent of GDP. Based on these estimates, the deficit would have been 1.6 percent of GDP without the tax cuts.

- These calculations, however, do not take into account the economic effects of the tax cuts. Most economic analyses suggest that the tax cuts have had some positive effect on the economy in the short run — at issue is the extent of this positive effect given their cost. These positive effects would make the short-run revenue losses associated with tax cuts somewhat smaller, and estimates of the deficit without the tax cuts somewhat higher. Nevertheless, even using the Administration’s assumptions about the economic effects of its tax cuts, the tax cuts would still account for 45 percent of the 2004 deficit.

| Table 1: | |

|

| As Percent of GDP |

| 2004 deficit with tax cuts | 4.2% |

| Cost of tax cuts | 2.6% |

| 2004 deficit without tax cuts | 1.6% |

| Source: CBPP calculations based on data from the Joint Committee on Taxation and the Congressional Budget Office | |

Indeed, the contribution of the tax cuts to the current deficit exceeds the contributions attributable to other factors, such as the economic downturn. A new CBO study finds that the direct effects of the business cycle account for only six percent of the 2004 deficit. Furthermore, when the cost of all legislation enacted since 2001 is considered, the tax cuts are found to cost more than all program increases combined, including increases in military expenditures, homeland security, and education spending. Domestic discretionary spending (which is funded on an annual basis) is now being singled out by the President and Congress for reductions. The cost of the tax cuts, however, is 18 times the cost of the increases in domestic discretionary spending.

| Table 2: | ||

|

| As Percent of GDP | |

|

| Average, 1980-2003 | 2004 |

| Spending | 21.1% | 20.0% |

| Revenue | 18.5% | 15.8% |

| Deficit | 2.6% | 4.2% |

| Source: Congressional Budget Office | ||

In 2004, CBO estimates that federal revenues will fall to their lowest level as a share of GDP — 15.8 percent — since 1950. The revenue base will be smaller, as a share of the economy, than it was before programs such as Medicare, Medicaid, and the interstate highway system existed. In contrast, total federal spending in 2004 is not estimated to be at particularly high levels as a share of the economy. CBO projects that federal spending will equal 20.0 percent of GDP in 2004, a level that is lower than in the 22 years from 1975 to 1996.

Unprecedented Use of Gimmicks

Research by Brookings Institution economists

Gale and Orszag, citing CBO data, show that at the start of 2001 the cost ten years down the road of extending all tax-cut measures in law that had a temporary status was $22 billion. By contrast, if the temporary tax-cut provisions in place today are all extended, their cost in ten years (i.e., in 2014) will be $431 billion.

The Administration has engaged in ongoing efforts to obscure the ultimate costs of its tax cuts. These efforts are reflected in the Administration’s current budget, released in February 2004. The budget shows deficit figures only over the next five years, which obscures the likely growth of the deficit in the second half of the coming decade under the Administration’s proposals, with the large deficits driven in significant part by its proposal to make the tax cuts permanent.

In addition, in its current budget, the Administration proposes new tax-advantaged savings and investment accounts that feature striking timing gimmicks. As a result, this proposal raises revenue over the first five years. But the proposal would cause increasingly large revenue losses after that. The proposal ultimately is likely to cost the equivalent of $35 billion a year.[1]

In a final, particularly audacious gimmick, in legislation sent to Congress on April 2, the Administration proposes a budget rule that would, for official purposes, make the cost of extending the 2001 and 2003 tax cuts disappear. If this change were enacted, the CBO would be required to show legislative proposals to make the tax cuts permanent as having zero cost.

The Long-Term Costs

If the tax cuts the Administration wants to make permanent are made permanent, current relief from the swelling Alternative Minimum

- Over the 10-year period from 2005 through 2014, the direct costs of the enacted and proposed tax cuts would total $2.8 trillion. The cost would equal 2.1 percent of the economy in 2014.

- From 2005 through 2014, the increased interest payments on the debt that result from the tax cuts would amount to $1.1 trillion. The interest payments would grow steadily with each passing year and in 2014 would equal $218 billion — or 1.2 percent of the economy. This amount alone is as large a share of the economy as the government now spends on all programs and activities under the Departments of Education, Homeland Security, Interior, Justice, and State combined.

- Considering both the direct costs of the tax cuts and the associated increase in interest payments, the tax cuts would increase deficits by nearly $4 trillion between 2005 and 2014.

- Over the next 75 years, the cost of these tax cuts — assuming they are made permanent — would be more than the combined shortfall in the Social Security and Medicare Hospital Insurance trust funds.

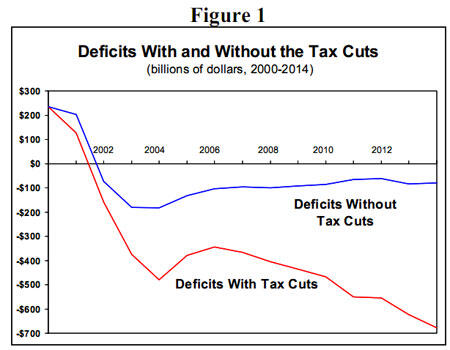

In the absence of the tax cuts, the deficit picture over the coming decade would look very different. Without the tax cuts, the deficit would be under $100 billion in most years. With the tax cuts, the deficit is projected to grow to more than $675 billion by the end of the decade.[2] If the tax cuts are extended, revenues over this period will remain at quite low levels by recent historical standards. Over the next decade, average revenues as a share of GDP would be lower than the average levels of revenues in the 1960s, 1970s, 1980s, and 1990s.

Distribution of Tax-Cut Benefits

The benefits that the tax cuts provide to different groups vary dramatically. New data from the

- The one-fifth of households in the middle of the income spectrum will receive an average tax cut of $647.

- The top one percent of households will receive tax cuts averaging almost $35,000 — or 54 times as much as that received on average by those in the middle of the income spectrum.

- Households with incomes above $1 million will receive tax cuts averaging about $123,600. The tax cuts for millionaires will cause their after-tax income to jump by 6.4 percent, nearly three times the percentage increase received by the middle fifth.

The overall shares of the tax cuts that are going to different households also are illuminating. The

- In 2004, the middle 20 percent of households will receive 8.9 percent of the tax cuts.

- By contrast, millionaires — totaling just 0.2 percent of

U.S. - The tax cuts will confer more than $30 billion on the nation’s 257,000 millionaires in 2004 alone.

| Table 3: | |||

| Income Class | Average tax cut | % increase in after-tax income | % share of tax cut |

| Middle 20 percent | $647 | 2.3% | 8.9% |

| Top one percent | $34,992 | 5.3% | 24.2% |

| Over $1 million | $123,592 | 6.4% | 15.3% |

| Source: Urban-Brookings Tax Policy Center | |||

As uneven as the distribution of the tax cuts is in 2004, their distribution will become still more uneven over time. This is because the tax cuts of most benefit to the middle class are already fully in place while some of the tax cuts of most benefit to high-income households — such as the eventual elimination of the estate tax — are only partly in effect now or have yet to take effect at all. If the tax cuts were fully in place today, the middle fifth of households would receive essentially the same tax cut that they are scheduled to receive under 2004 law, while the top one percent would receive tax cuts substantially larger than under 2004 law.[4]

Three “Middle-Class Provisions” Compared With Other Tax-Cut Provisions

In assessing the tax cuts and their distribution across different income groups, it is interesting to distinguish between three so-called “middle-class provisions” and all of the other tax-cut provisions enacted over the past few years. These “middle-class provisions” — which established the 10 percent tax bracket, expanded the child tax credit, and provided tax relief to married couples — were first enacted in 2001 and became fully effective in 2003, when their implementation was accelerated as part of the 2003 tax-cut package. This acceleration expires at the end of 2004, at which time the provisions return to their original phase-in path. These “middle-class provisions” have generally received broad bipartisan support, in contrast to many of the other tax-cut provisions, which are dominated by the more contentious upper-bracket rate reductions, dividend and capital gains rate cuts, and the elimination of the estate tax.

These three “middle-class provisions” provide substantial help to the broad middle class, although it is sometimes overlooked that they provide significant tax benefits to high-income households as well. The middle fifth of households will receive an average tax cut of $547 in 2004 from these provisions. The top one percent of households will receive an average tax cut of $1,320 from these measures.

| Table 4: | |||

| Income Class | Three “Middle-Class” Provisions | All Other Tax-Cut Provisions | |

| Middle 20 percent | $547 | $100 | |

| Top one percent | $1,320 | $33,672 | |

| Source: Urban-Brookings Tax Policy Center | |||

The distribution of these “middle-class provisions” stands in stark contrast, however, to the distribution of tax benefits under the remaining tax-cut provisions. The top one percent of the income spectrum will receive an average tax cut of almost $33,700 from all of the other tax-cut provisions in 2004, while the middle fifth of households will receive an average tax cut of just $100. The other tax cuts provide those at the top of the income scale with average tax benefits more than 300 times larger than the benefits that those in the middle of the income spectrum are receiving. This gap will widen even further over time.

Of particular note, these three “middle-class provisions” account for just one-third of the cost of the tax cuts over time. In other words, the vast majority of the tax cuts that benefit the middle class could have occurred at about one-third of the cost of the tax cuts that have been enacted or that the Administration is now proposing.

The Administration’s Hesitant Support of Provisions That Help Lower-Income Households

The Administration has worked hard to create the impression that its tax cuts benefit all families, including those of modest means. In most cases, however, the Administration has accepted tax cuts for lower-income families only under pressure. When it has had the opportunity to initiate such tax cuts, it has consistently rejected them.

For example, when promoting his 2001 tax-cut plan in his first months in office, President Bush emphasized the benefits for low-income families with children by using an example of a waitress earning $25,000. As it turned out, the waitress he mentioned would have received no tax cut (or a small tax cut if she had significant child care costs) because the President’s proposal provided no relief to families that owed no income tax but paid significant amounts of payroll tax. The Administration received substantial criticism in early 2001 on this score, and it ultimately agreed to Congressional changes to its child tax credit proposal that provided significant aid to the waitress in the President’s example and to millions of other low- and moderate- income working families with children.

A similar story played out in 2003. The President proposed accelerating most of the income tax cuts enacted in 2001 that were scheduled to phase in over time, but he rejected accelerating the child tax credit provision enacted in 2001 that is of benefit to low- and modest-income working families. A front-page story in The New York Times called attention to this omission the day after the 2003 tax bill was signed into law, generating a torrent of criticism. The Administration shifted positions in the face of this criticism, voicing support for accelerating the provision in question. But the Administration expended little effort on this score, and the acceleration has not been enacted.

The Very Well-Off: Big Winners on Two Fronts

The very well-off have been big winners on two fronts. They secured enormous gains in income in the 1980s and 1990s. They now are receiving extremely large tax cuts as a result of the 2001 and 2003 tax-cut measures. The Congressional Budget Office provides the most comprehensive data available on recent changes in incomes and taxes for different income groups; these CBO data cover years from 1979 until 2001. Just-released CBO data show:

- The average after-tax income of the top one percent of the population more than doubled over this period, rising from $294,300 in 1979 to $703,100 in 2001, an increase of $408,800. (CBO adjusted these figures for inflation and expressed them in 2001 dollars.) This represents an increase of 139 percent.

- By contrast, the average after-tax income of the households that make up the middle fifth of the U.S. population rose $6,300, or 17 percent, during this period. And the average after-tax income of the poorest fifth of households rose $1,100, or only eight percent.

- In combination with data on before-tax income from a study issued by the National Bureau of Economic Research, these CBO data indicate that before-tax income was more concentrated at the top of the income scale in 2001 than at any time in the previous 65 years (i.e., back to 1936), except for the years from 1997-2000.

The pattern continues in 2004. The President’s budget proposes to make permanent every tax-cut provision enacted in 2001 and 2003 that predominately benefits people with high incomes. But the budget fails to extend — and thus would let die after 2006 — the provision of the 2001 tax-cut law that encourages greater retirement saving by working families with incomes under $50,000.

The Administration’s Story

Anyone who has learned most of what they know about the tax cuts from President Bush’s speeches and Administration press releases might find the foregoing discussion of the distribution of the tax cuts surprising. The Administration has consistently highlighted the tax benefits for the middle class and promoted its tax cuts as beneficial to a variety of sympathetic groups, such as small businesses. Unfortunately, much of the information it has put forward in this regard has been selective or misleading.

As one example, the Administration has consistently employed “averages” in a manner that falls far short of a reasonable use of statistics and overstates the benefits of the tax cuts to middle-income households. The Administration’s average tax-cut figures are skewed upward by the very large tax cuts that go to a small number of very high-income taxpayers. The large majority of

Similarly, the President has repeatedly invoked the benefits his tax cuts, and especially his proposal to reduce the top income tax rate, provide to small businesses. Yet, according to Treasury Department data, the top rate reduction benefits only two percent of small business owners. In other words, 98 percent of small business owners are not in the top tax bracket. In fact, many more such individuals receive the Earned Income Tax Credit for lower-income working families than are in the top bracket.

Furthermore, the Administration’s definition of “small business owner” includes anyone who earns even one dollar of income that is classified as business income under the tax code. Under this definition, one need not actually run or own a major share of a business to be classified a business owner. This definition includes wealthy individuals whose primary income does not come from small business ownership or operation but who do some consulting or invest in real estate on the side. Many of those in the top tax bracket are better characterized as very-high-income individuals, such as corporate executives, with some business investments.

Economic Effects of the Tax Cuts

From the outset, the Administration has argued that its tax cuts are good for the economy. Initially, the Administration touted the long-term benefits of its tax cuts. When the economy weakened, the Administration changed its tune and justified its tax-cutting agenda as a way to strengthen a struggling economy and create jobs. The tax cuts were poorly designed to provide short-term stimulus, however, and the results on the job-creation front have been disappointing. Further, the tax cuts, by adding significantly to mid-term and long-term deficits, are likely to be a drag on the economy over the long run.

Poor Bang for the Buck

An examination of President Bush’s 2003 tax-cut proposal demonstrates how ill-suited his proposals have been to providing short-term economic stimulus. Economy.com, an independent economics research firm whose analyses have been used widely in recent years, conducted a study in early 2003 that examined the various stimulus proposals then under consideration. The study measured the amount of increased economic “demand” that each dollar of lost tax revenue or increased program spending would generate in the year after the benefit has been provided. (One rule-of-thumb to keep in mind is that proposals that put more money in the hands of low- and middle-income people generally provide more short-term stimulus than proposals that put more money in the hands of high-income people, because low- and middle-income people are more likely than high-income people to spend quickly any additional income they might have.)

The Economy.com assessments indicate that only 19 percent of the President’s proposed 2003 stimulus package consisted of high “bang-for-the-buck” proposals — proposals that would yield more than one dollar of added short-term demand for each dollar of revenue loss. More than half of the Administration’s package consisted of its proposal to eliminate the taxation of corporate dividends. Economy.com estimated that proposal would generate less than a dime of short-term stimulus for each dollar of revenue lost.

Moreover, the tax cuts the Administration proposed in 2003 would have been spread out over ten years. For purposes of helping the economy in the short run, only tax cuts that take effect when the economy is weak are important. A mere 5.5 percent of the Administration’s proposed stimulus tax-cut package would have occurred in fiscal 2003 (that is, by the end of September 2003). Another 15.7 percent would have occurred in fiscal 2004. In combination, only about one-fifth of the proposed tax cuts would have been in effect by October 2004.

With only a small minority of the tax-cut proposals consisting of high “bang-for-the-buck” proposals and only a small percentage of the tax cuts taking effect by the end of fiscal 2004, the President’s 2003 stimulus proposal can fairly be characterized as highly inefficient at providing short-term stimulus. Only four percent of the President’s 2003 package consisted of high “bang-for-the-buck” tax cuts that would have been in effect by October 2004.[5]

| Table 5: | |

| Have high “bang for the buck” | 19% |

| Affect economy in the short run | 21% |

| Are effective stimulus | 4% |

The stimulus bill actually enacted in 2003 was modestly more efficient at providing short-term stimulus to the economy than the President’s original proposal, primarily because it included state fiscal relief. Even so, just 8 percent to 14 percent of the cost of stimulus legislation enacted in 2003 consisted of high “bang-for-the-buck” short-term stimulus proposals.

These data provide credence to a statement issued in February 2003 and signed by 10 Nobel Price-winning economists and 450 other economists, which stated in part: “Regardless of how one views the specifics of the [2003] Bush [tax cut] plan, there is wide agreement that its purpose is a permanent change in the tax structure and not the creation of jobs and growth in the near-term.”

Job Creation

A principal Administration justification for its tax cuts, particularly over the past year, has been their importance for job generation. The tax bills passed by Congress were somewhat less inefficient at stimulating the economy than the President’s original proposals. Even so, the results in this area have been poor.

- The Administration’s February 2004 Economic Report of the President itself noted that: “The performance of employment in this recovery has lagged that in the typical recovery and even that in the ‘jobless recovery’ of 1990-1991.”

- Employment remains substantially below its level at the start of the downturn, an unparalleled development this far into a post-World War II recovery. (Substantial job growth typically occurs by this point.) As of March 2004, there were still two million fewer jobs than when employment last peaked in March 2001.

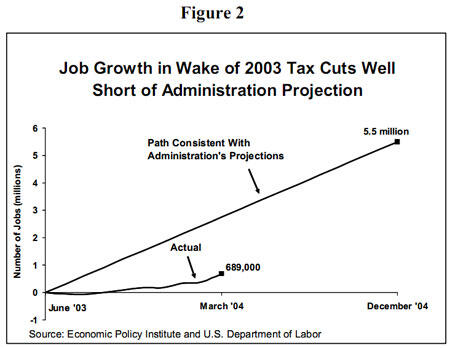

For three years, the Administration has been claiming its tax cuts would boost employment. But for three years, actual job growth has fallen far short of Administration expectations. For example, since the summer of 2003, the Economic Policy Institute has been comparing actual job growth to the amount of job growth the Administration predicted would occur with the passage of the 2003 tax-cut bill. The Administration predicted that with the passage of the tax-cut measure, 5.5 million jobs would be created in the 18 months from June 2003 through December 2004. In the first nine months of this 18-month period, a relatively modest 689,000 jobs were created, just 13 percent of the Administration’s projection.

President Bush and his Administration have highlighted a different labor market statistic — the relatively low unemployment rate of 5.7 percent (in March 2004). This level, however, is misleading. It does not reflect significant job growth and labor market strength; instead, it reflects an unusual decline in the number of people looking for a job. This decline is a sign of labor-market weakness, as it presumably indicates that people are dropping out of the labor force because they do not believe job prospects are promising. If labor force participation had been the same in March 2004 as in March 2001, when the downturn began, the unemployment rate in March 2004 would have equaled about 7.4 percent, rather than 5.7 percent.[6]

Job growth during this recovery might have lagged behind that of previous recoveries even if the recent economic policies had been better designed. Nonetheless, the exceptionally poor job growth of recent years suggests the Administration’s tax cuts have largely failed to accomplish one of its stated policy goals. The inefficiency of the tax cuts when it came to providing short-term stimulus makes this failure less surprising.

GDP Growth

Despite the 2001, 2002, and 2003 tax cuts, overall economic growth has been below par. The economy hit its low point during the last quarter of 2001. So far during the recovery period, the economy has grown at an average annual rate of 3.6 percent, after adjusting for inflation. This growth rate compares unfavorably with the growth rate in seven of the eight previous recoveries since the end of World War II.

This recession was “shallow” so perhaps one might expect the rebound to be less steep. To account for this, growth can be assessed from the point when the economy last peaked until now; this measure takes into account that the decline in the economy was not as great in this downturn as in some other downturns. Even by this measure, the current recovery rates poorly. The amount of economic growth over the period since the pre-recession peak lags behind the average amount of growth achieved at the comparable stage of other post-World War II recoveries.

Undermining Future Growth

Over time, the tax cuts will become even less effective at generating economic growth. In the medium term, the tax cuts are likely to have little effect on the size of the economy, despite costing hundreds of billions of dollars each year. Studies by both the CBO and the Joint Committee on

In the long-term, the tax cuts would have more pernicious effects on economic growth. Large, persistent deficits can gradually eat away at the nation’s economic foundation. The higher deficits to which the tax cuts significantly contribute will reduce national saving and thus over time result in less domestic investment (and more borrowing from overseas). The reduction in domestic investment and increased borrowing from abroad associated with budget deficits lowers the nation’s future standard of living from what it would otherwise have been. As the International Monetary Fund concluded in a January 2004 report:

Moreover, the same IMF report, as well as a study by former Treasury Secretary Robert Rubin, Wall Street economist

Plotting a Different Course

These findings suggest it is time to reconsider the tax cuts. The Administration disagrees. Its budget calls for making permanent nearly all of the tax cuts that were passed in 2001 and 2003, at an immense cost to the Treasury. It also proposes an array of new tax cuts and more budget gimmickry. For instance, it proposes a series of tax cuts related to savings that would, in all likelihood, diminish net national saving by substantially increasing the deficit. These proposals are designed to show increased tax revenues over the next five years but ultimately would cost approximately $35 billion a year.

These savings proposals continue two other undesirable patterns of the Administration’s tax-cut policies. First, the tax-cut benefits from the proposals would go overwhelmingly to the nation’s wealthiest individuals. Second, these tax cuts would harm already vulnerable state budgets. State income tax codes generally conform to the federal tax treatment of savings. As a result, if these savings-related tax cuts are enacted at the federal level, many states would experience revenue losses. Such revenue losses would be on top of the revenue losses many states are experiencing as a result of federal tax cuts enacted in 2001, 2002, and 2003.

A different policy course can be followed. Instead of pushing to make nearly all of the tax cuts permanent and institute new tax cuts on top, there should be an examination of which tax cuts should be extended, which should not be extended, and which should be scaled back or repealed. The tax code also needs reforms that would make it simpler and fairer, and doing so could raise needed revenues. Revenues could be raised by paring back or eliminating tax breaks that are ineffective or outmoded. Finally, revenue also could be raised by beefing up enforcement efforts aimed at corporations and households engaged in sophisticated schemes to hide their income from taxation.

End Notes

[1] This estimate is based on analyses by the

[2] For a discussion of the methodology underlying these budget projections, see

[3] The share of tax cuts received by those with very high-incomes is also greater than their shares of national income and of taxes paid. For example, the

[4] The estimate of tax law being fully in effect today reflects only the Administration’s proposal to extend most of the tax cuts enacted in 2001 and 2003, and does not include the effects of other tax-cut proposals in its fiscal 2005 budget.

[5] The President’s proposals to accelerate the expansion of the 10 percent tax bracket and the child tax credit increase were the only two provisions whose “bang for the buck” exceeded $1, according to Economy.com. According to Joint Committee on

[6] The 7.4 percent calculation assumes that the increased number of job seekers would not have affected the number of jobs.

More from the Authors