Tax Flight Is a Myth

Higher State Taxes Bring More Revenue, Not More Migration

Executive Summary

Attacks on sorely-needed increases in state tax revenues often include the unproven claim that tax hikes will drive large numbers of households — particularly the most affluent — to other states. The same claim also is used to justify new tax cuts. Compelling evidence shows that this claim is false. The effects of tax increases on migration are, at most, small — so small that states that raise income taxes on the most affluent households can be assured of a substantial net gain in revenue.

The basic facts, as this report explains, are as follows:

- Migration is not common. Most people have strong ties to their current state, such as job, home, family, friends, and community. On average, just 1.7 percent of U.S. residents moved from one state to another per year between 2001 and 2010, and only about 30 percent of those born in the United States change their state of residence over the course of their entire lifetime. And when people do relocate, a large body of scholarly evidence shows that they do so primarily for new jobs, cheaper housing, or a better climate. A person’s age, education, marital status, and a host of other factors also affect decisions about moving.

- The migration that’s occurring is much more likely to be driven by cheaper housing than by lower taxes. A family might be able to cut its taxes by a few percentage points by moving from one state to another, but housing costs are far more variable. The difference between housing costs in two different states is often many times greater than the difference in taxes. So what might look like migration in search of lower taxes is really often migration for cheaper housing.

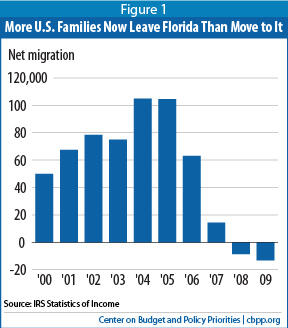

Consider Florida, often claimed as a state that attracts households because of its low taxes (Florida has no income tax). In the latter half of the 2000s, the previously rapid influx of U.S. migrants into Florida slowed and then reversed — Florida actually started losing population. The state enacted no tax policy change that can explain this reversal. What did change was housing prices. Previously, the state’s lower housing prices had enabled Northeastern homeowners to increase their personal wealth by selling their pricey houses and purchasing a comparable or better home in Florida at a lower price. But housing prices in Florida rose sharply during the mid-2000s, narrowing opportunities for Northeasterners to “trade up” on their expensive homes. And consider California: its loss of households to other Western states is often ascribed to tax differentials, but — as this report shows — housing-cost differentials are typically much, much larger.

- Recent research shows income tax increases cause little or no interstate migration. Perhaps the most carefully designed study to date on this issue concerned the potential migration impact of New Jersey’s 2004 tax increase on filers with incomes exceeding $500,000. It found that while the net out-migration rate of this income group accelerated after the tax increase went into effect, so did the net out-migration rate of filers with incomes between $200,000 and $500,000, and by virtually the same amount. At most, the authors estimated, 70 tax filers earning more than $500,000 might have left New Jersey between 2004 and 2007 because of the tax increase, costing the state an estimated $16.4 million in tax revenue. The revenue gain from the tax increase over those years was an estimated $3.77 billion, meaning that out-migration — if there was any at all — reduced the estimated revenue gain from the tax increase by a mere 0.4 percent.

- Low taxes can prevent a state from maintaining the kinds of high-quality public services that potential migrants value. Studies show that such amenities as cultural facilities, recreational opportunities, and good public services are powerful attractions for potential migrants. Many of those services are financed with tax dollars. Therefore, while low taxes decrease the cost of living, they might also prevent states from preserving or improving valued public services, which would discourage potential migrants.

Thus, while a few affluent households might leave a state because their income taxes are increased, the vast majority stay, and states gain a significant net increase in revenue to help support important services.

Against this evidence, anti-tax advocates, policymakers, and journalists continue to rely on a few deeply flawed studies and incomplete anecdotes to back up the taxation-migration myth. Among the most-often cited examples:

- A business-financed Oregon study received much attention for purporting to show that Portland residents were moving to Washington State to avoid Oregon’s higher income tax in general and a temporary increase in the county where Portland is located in particular. But the study failed to take key facts into account. For example, Oregon taxes the wages of people who work in the state even if they live elsewhere, so people who continued to work in Oregon could not avoid paying Oregon income tax on their wages by moving to Washington. In addition, a local economic boom in Portland and other factors were causing housing prices to rise faster on the Oregon side of the border than on the Washington side during the period the study covered. In all likelihood, whatever net migration was occurring reflected housing price differentials (as well as other potential factors) more than tax differentials — but the study didn’t adjust for that.

- High-profile critics of New Jersey’s above-mentioned tax increase — from the state’s governor to the Wall Street Journal — for years have pointed to a Chamber of Commerce-commissioned study showing that, starting in the same year the state enacted the measure, the total wealth of millionaires leaving the state began to exceed the total wealth of millionaires moving to the state. The study, however, was not designed to measure the potential impact of tax changes on those migration patterns; nor did it find a tax impact (its author acknowledges as much). Most of the people the study examined weren’t subject to the tax increase, since the study covered families with a net worth of $1 million or more, many of whom have less than $500,000 a year in taxable income. Nonetheless, the governor is still incorrectly claiming this study as evidence of a tax-migration effect.

- Critics of Maryland’s 2008 tax increase on income over $1 million point to the sharp decline that year in the number of filers in the state with taxable incomes exceeding $1 million as evidence that wealthy residents were fleeing the state. But an examination of actual tax return data shows that the vast majority of this decline occurred not because people moved out of the state, but because their incomes fell below the $1 million mark due to the recession and stock market crash; they remained on the tax rolls, but in a lower tax bracket.

It would not be credible to argue that no one ever moves to a new state because of the desire to live someplace where taxes are lower. But neither is it credible to say that taxes are a primary motivation, nor that migration has a large impact on the revenue impact of tax measures.

Extensive Research Documents Importance of Non-Tax Factors in Migration Decisions

To understand income taxes’ impact on migration, it is necessary to understand why Americans move — and why they don’t. Most people, rich and poor alike, are tied to their state of residence by job, family, friends, and community. Consequently, interstate moves are rare: on average, only 1.7 percent of U.S. residents moved from one state to another per year between 2001 and 2010, and only about 30 percent of those born in the United States change their state of residence over the course of their entire lifetime.[1] Moreover, some of these moves are across state lines within metropolitan areas — say, from New York City to its New Jersey or Connecticut suburbs. The focus of much of the rhetoric around taxes and migration, however, is around longer-distance migration trends — say, from New York to Florida.

Hundreds of academic studies in recent decades have documented myriad reasons why Americans might or might not migrate long distances. [2] These studies make clear that people move for many complicated, interrelated reasons. The research does not, by and large, study the impact of taxes themselves on a household’s decision to migrate, but the insights it provides can help explain why taxes likely are only a minor part of the equation.

For one thing, it takes a lot to get someone to move a long distance. The few households that do move are often driven by large economic motives, such as a new job or much cheaper housing.[3] And practically no matter where families might consider moving among the states, the potential savings from lower tax costs pale in comparison to the savings they would realize by moving to a state with cheaper housing.

Interstate tax differentials typically equal just a few percentage points of income, when all forms of taxation are taken into account. In 2007, the average tax on a middle-income family ranged from about 11 percent of income in states with higher taxes to about 6.7 percent in states with lower taxes, according to the Institute on Taxation and Economic Policy — a 4.3 percentage-point differential. The differential was 3.5 percent for higher-income taxpayers.[4] (Of course, if one looked only at one or two categories of tax, the differentials would be greater, for instance because states with higher income taxes tend to have lower sales and property taxes. But if taxpayers respond to interstate tax differences, logic dictates they should respond to the total tax level.)

In contrast to the small tax benefit from relocation, moving in search of cheaper housing can have a far bigger payoff — equal to as much as one-fourth or more of a household’s income.

California provides one example. A study by the Public Policy Institute of California found that Arizona from 2004 to 2007 was the leading destination for people moving out of California, both for low-income and high-income households.[5] But the median price of a three-bedroom house was more than twice as high in California as in neighboring Arizona in 2007, so by moving to Arizona an average middle-class or upper-middle-income family in California could reduce its annual mortgage costs by 24 percentage points and an upper-middle class family by 15. In some locations, the differentials could be even greater. (See Appendix I.) These differentials exceed, by a huge margin, any possible interstate tax differentials. In fact, according to the Institute on Taxation and Economic Policy, both middle- and upper-middle-income families that year faced slightly higher taxes in Arizona. (As noted below, the PPIC raised other reasons to be skeptical of any tax-migration connection.)

Another example is Florida, which many have held up as an example of a state whose low taxes attract large numbers of migrants, particularly from the Northeast. During the 1990s and most of the 2000s, the Northeast experienced both rapid appreciation in housing values and sluggish job growth while, in Florida, employment rose fast and land was relatively cheap. Northeastern homeowners could increase their personal disposable wealth by selling their pricey houses and purchasing a comparable or better home in Florida at a lower price.

Florida still lacks an income tax — and still has sunny weather and lots of sand and surf. What changed? Florida’s housing prices rose sharply during the mid-2000s, narrowing opportunities for Northeasterners to “trade up” on their expensive homes. Many decided either not to move or to move to states like Georgia or South Carolina, which have income taxes but also have cheaper housing and a mild climate. Then Florida’s economy collapsed in the severe recession, dispersing Floridians to other states in search of work.

As noted, housing and employment are not the only factors other than taxes that can influence families to move. People move to another state to attend college, to serve in the armed services, or to be closer to family members. The destruction wrought by natural disasters like Hurricane Katrina and Tropical Storm Rita can precipitate extensive interstate migration.[6] Any attempt to explain interstate migration must account for a range of economic, demographic, and personal considerations.

The academic literature yields another important insight for the debate about taxes and migration. Some have argued that high-income families are especially likely to move in response to changes in tax rates because they can afford the cost of moving to another state where the taxes are lower. But extensive research suggests that many of the factors deterring people from moving are most prevalent among households with higher-than-average incomes.[7] For instance:

- Family structure. Married couples generally have higher incomes than single people. Research shows that married couples are more likely to migrate to a location where both spouses can obtain a satisfactory job, but once they have found it, they tend to avoid long-distance moves because that would disrupt their working arrangements. In addition, parents — especially of teenagers — are less likely than others to move because they place a high priority on providing their children with a stable environment.

- Homeownership. People with higher incomes are more likely to own homes. This increases the costs of moving, as selling property is costly and time consuming. (There are exceptions; housing price differentials of the last decade created incentives for homeowners to sell, as discussed above.)

- Age. People with the highest propensity to migrate are between the ages of 18 and 24, an age group with below-average income because many, although having recently finished their education, have yet to obtain secure employment. They are also relatively mobile because many have yet to start a family.

- Employment status . Census data show that the unemployed, who are heavily concentrated at the low end of the income scale, have been four times more likely to move from one state to another over the past decade than the employed.[8]

This evidence suggests that the caricature of high-income households as likely to move quickly if hit with a tax hike should not be taken at face value. To be sure, some high-income families are relatively mobile and thus may be more likely to move because of a change in tax rates — those who are retired “empty nesters,” are wealthy enough to live off of income from their investments, or own second homes located in another state (which would enable them to change their official state of residence relatively easily). However, for the reasons described above, most high earners have strong ties to their state of the sort that might be expected to keep them there, even if their taxes are raised. Some own homes, or have high-paying jobs to which they are strongly attached. Many have working spouses who may have difficulty finding a satisfactory job at another location. Some have children, whose lives they don’t want to disrupt.

Moreover, low taxes are a double-edged sword when it comes to attracting mobile households. Studies show that such amenities as cultural facilities, recreational opportunities, and good public services are powerful attractions for potential migrants. (In addition, a study of migration into and out of the New England states found that spending on public services that lowers property crime, such as police protection, attracts residents of other states.[9]) Many of those services are financed with tax dollars. Therefore, while low taxes decrease the cost of living, they might also prevent states from preserving or improving valued public services, which would discourage potential migrants.

There are other reasons to doubt that high earners would necessarily move in response to tax increases. Many are prominent community leaders, some from families with a long history of local civic involvement. Some have strong ties to local medical professionals who have been caring for them for many years. Like most other people, the affluent have friends and family living close by — parents, children, grandchildren, and siblings — whom they don’t want to leave. And many might favor, or at least accept, tax increases as a means to preserve public services that would enhance communities in which they have already invested a great deal.

The limited propensity to move among high-income households was noted in the PPIC study of California out-migration described above. The PPIC study found that high-income families were actually less likely to move out of California than lower-income families. It noted further that this was true even of states that had lower taxes on the wealthy, such as states that had no income tax. (Income taxes tend to be paid more by higher-income families.) “Income taxes aren’t driving away the highest-income households,” PPIC reported.

None of this, of course, proves whether taxes lead individuals to migrate, much less the size of that effect if it exists. But it does give rise to skepticism about simplistic claims that tax increases cause households in general, or the rich in particular, to flee in large numbers. The research clearly indicates that tax-induced interstate migration is so rare that it should not deter policymakers from raising needed revenue, as the next section shows.

Recent Research Shows Income Tax Increases Cause Little or No Interstate Migration

Until recently, scholars in the United States have generally shied away from researching the question of whether state income taxes, specifically, cause interstate migration. To some extent researchers were thwarted by inadequate data, although it is also likely that — for the reasons described above — many simply assumed, correctly, that taxes would have little effect.

In the last 10 to 15 years, newly available data have enabled scholars to estimate whether and how state income taxes affect high-income households’ decision to move to another state. The new data come from individual state income tax returns, federal estate tax returns (from which state income tax liabilities can be estimated), and several decades worth of detailed Census-based data on individual households. [10] These data have made it possible, more than before, to evaluate the increasing number of assertions by policymakers and others that taxes make a significant difference.

Most studies that have approached the question in a rigorous and thoughtful manner have found little or no discernable tax effect. For example, using data from 1970-2000, economists Karen Conway of the University of New Hampshire and Jonathan Rork of Reed College found that differences in average income tax rates did not affect the interstate migration of high-income elderly households.[11] A study by Joel Slemrod of the University of Michigan and Jon Bakija of Williams College failed to find conclusive evidence that differences in state income taxes affect the location of the rich.[12]

Perhaps the most carefully designed study to date, conducted by Stanford University sociologists Cristobal Young and Charles Varner, estimated the migration effect of New Jersey’s 2004 tax increase on filers with incomes exceeding $500,000. They found that while the net out-migration rate of this income group accelerated after the tax increase went into effect, so did the net out-migration rate of filers with incomes between $200,000 and $500,000, and by virtually the same amount.[13] At most, the authors estimated, 70 filers earning more than $500,000 might have left New Jersey between 2004 and 2007 because of the tax increase, costing the state an estimated $16.4 million in tax revenue. The revenue gain from the tax increase over those years was an estimated $3.77 billion, meaning that out-migration — if there was any at all — reduced the estimated revenue gain by a mere 0.4 percent.[14]

Young’s and Varner’s findings shows how one can be misled when an extremely wealthy taxpayer – often one with a high public profile, e.g. a sports-team owner — announces that he or she is leaving a state to avoid a newly enacted tax. One might be tempted to conclude that such a person represents a larger cohort of silent but nonetheless footloose wealthy people. However, Young and Varner discovered that most of the revenue leakage was attributable to an extremely small number of high-income taxpayers. These departing “uber-rich” were so few in number that their out-migration barely affected the revenue gain resulting from the 2004 tax increase. Policymakers and members of the media should be cautious, therefore, in drawing conclusions from anecdotal evidence of tax-induced flight.[15]

The work of Conway and Rork, Slemrod and Bakija, and Young and Varner, as well as other independent academic research, stands in sharp contrast to a study undertaken in the late 1990s reporting evidence that raising state income taxes on affluent taxpayers would induce them to flee in large numbers. The evidence produced by the study is extremely circumstantial and has been called into serious doubt by other scholars. Published in 1998 by Harvard economists Martin Feldstein and Marian Wrobel, the study found that, when a state increased the progressivity of its tax system, pre-tax wages of the rich rose. Based on economic theory, they deduced that out-migration of high-income earners accounted for this upward wage adjustment. The authors reasoned that affluent families must have left the state in sufficient numbers to create a shortage of highly skilled workers, forcing their wages up even further.[16]

The two economists’ methodology is suspect for several reasons. First, as Young and Varner have pointed out, Feldstein and Wrobel may have spotted a tendency of states with widening inequality in pre-tax wages to enact progressive taxes, rather than a tendency of progressive taxes to cause the rich to flee.[17] Moreover, the economists didn’t observe actual migration flows; rather, they inferred them from their observations and economic theory. By contrast, Andrew Leigh, a Harvard-trained economist now at the Australian National University, conducted a separate study that found no link between tax progressivity and actual interstate migration rates in the United States. [18] Jeff Thompson of the University of Massachusetts, using a variant of Feldstein’s and Wrobel’s methods, found that the pre-tax wages of high-income workers increase only slightly in response to greater progressivity, implying at most a small uptick in out-migration.[19]

Claims of Tax-Induced Flight Are Fundamentally Flawed

As explained above, neither the broad body of research on interstate migration in general, nor more recent studies of migration by high-income households, support the assertion that “if you tax them, they will flee.” So why have many policymakers and journalists apparently accepted this argument? One reason is that those who perpetuate the migration myth fill a vacuum to some extent. Few policymakers or journalists are aware of the scholarly work showing the lack of relationship between income taxes and migration; the authors of these studies have not used it to influence tax policy debates but instead have generally presented it to academic audiences and often written it in a style not easily accessible to non-experts. [20]

Proponents of the migration myth frequently cite statistics and arguments that, although superficially convincing, suffer from one of the following fundamental flaws:

- Confusing correlation with causation. Before the onset of the Great Recession, a number of states with relatively low personal income taxes — such as Florida, discussed above — also enjoyed strong job growth, inexpensive housing, and a pleasant climate; such non-tax factors attracted migrants to these states. Meanwhile, weak labor markets, soaring housing costs, or unattractive climates plagued California and states in the Northeast and Midwest, some of which have comparatively high personal income taxes. One can easily produce statistics that would appear to demonstrate that tax differentials caused migration from higher-tax states to lower-tax ones, when in reality non-tax factors were the underlying drivers. Finding a correlation — two things happening at the same time — is not the same as proving that one of those things caused the other.

- Misrepresenting irrelevant findings. Some of the studies that tax opponents cite as demonstrating that tax increases drive affluent households out of a state don’t even address taxes. In at least one prominent case (discussed below), tax opponents have interpreted study findings so inaccurately that the study’s author felt compelled to warn the media against inferring tax effects from their findings.

- Improperly measuring migration. Some tax opponents have blamed declines in the number of very high-income tax filers in certain states on those states’ high-end tax increases, when the real reason was the recession. The recession in general, and the stock market collapse in particular, caused the number and percentage of federal income tax filers who reported incomes in excess of $1 million to fall sharply in 2008 (the first year of the recession). It stands to reason that if the number of households nationally that were above a particular income level declined, the same trend would be visible in individual states. The correct interpretation is that many of the extremely affluent moved down the income distribution, not out of the state to avoid the new taxes levied on their income.[21]

The case studies below illustrate each of these flaws in turn.

In and Out of Oregon

In 2009, Oregon raised income tax rates on married households with incomes over $250,000 ($125,000 for single filers), affecting the top 3 percent of the state’s households. Opponents sought to overturn the tax increase though a referendum, but voters affirmed the tax increase in January 2010. [22]

In that same year, the Oregon Business Council commissioned a study by ECONorthwest, a consulting firm, which provided “evidence” that the measure would drive a considerable number of affluent taxpayers out of Oregon. The study warned, “The data are clear. If the state raises the tax rate on affluent households, substantial numbers will move income out of Oregon.”[23] The Business Council and other powerful opponents of the tax increase used the study to support their position. Shortly before the referendum vote, Nike chair Phil Knight, arguably Oregon’s best-known businessman, wrote an op-ed in the state’s largest newspaper that harshly criticized the tax increase, claiming: “Reputable economists forecast” that “thousands of our most successful residents will leave the state” as a result of the tax increase. [24]

The ECONorthwest study cited three pieces of evidence to buttress its claim, none of which stands up under scrutiny.

The first is the fact that capital gains tend to be a larger fraction of the income of affluent households in states with relatively low income taxes (or no income tax) than in states with relatively high income taxes. The report claims this correlation “supports the hypothesis that some upper income households move to avoid capital gains taxes.” Although the study cautions against drawing policy conclusions from this simple correlation, it then states that “substantial numbers of affluent households will move income out of Oregon” if their income taxes are raised. But it presents no migration data to support this assertion; instead, it relies on indirect statistical inference.

The study ignores the fact that many of the states whose affluent taxpayers pay low income taxes and receive a relatively large share of their income in capital gains are also popular destinations for wealthy retirees, such as Florida, Nevada, and Wyoming. Since retirees have stopped working, they are much less likely than working people to receive wages and salaries and much more likely to rely heavily on other income sources, such as capital gains.

We recreated the study to account for the large share of wealthy retirees in these states, and found that it was their presence — not the lack of taxes — that generated high levels of capital gains in those states. (We also checked to see if the low taxes were correlated with high levels of wealthy retirees. They weren’t. See Appendix II.)

Second, the study argued that from 1992 to 2006, higher-income residents of the Portland metropolitan area moved to Washington because Oregon has an income tax and Washington doesn’t. Again, ECONorthwest failed to consider non-tax reasons for the migration — in this case, the fact that Portland was undergoing an economic boom during most of that period, driven by the start-up and growth of high-tech firms. Young tech workers moved into the city, pushing married couples into the suburbs, including Clark County, Washington, where developers were building subdivision after subdivision of large, relatively affordable houses. In 1990, average housing costs in Clark County were higher than for similar-sized homes in Multnomah County (Portland), but by 2000 they were lower, and the price differential was even greater in 2006. Economic development experts from both states agree that during that time period, Clark County offered a host of amenities to new residents, from larger house lots to a reputation for better schools and safer streets. Portland also developed a reputation for a quirky, youth-oriented culture, an environment in which some middle- and higher-income households did not want to raise their children.

Moreover, for the one-third of Clark County residents that still commuted into Oregon, there was little or no income-tax benefit from such a move, since Oregon taxes the Oregon wages of Washington residents.[25]

In any event, the migration into Clark County was hardly enormous. The $1.3 billion in household income that ECONorthwest claims Oregon allegedly lost to Clark County during that period due to migration would represent a tiny fraction — only 0.34 percent — of the $377 billion in income earned by tax filers from Portland’s Oregon suburbs in those years. Moreover, as noted, Oregon still collected income tax on commuters. So even if some portion of the migration were related to tax differentials, according to ECONorthwest’s estimates, it cost Oregon almost nothing.

The study’s third assertion relates to a 1.25 percent income tax that Multnomah County imposed from 2003 to 2005 to help finance its schools. [26] The share of the state’s wealthy residents that lived in Multnomah County fell from 24 percent in 2002 to 21 percent in 2003-05 before rebounding to 23 percent in 2006. ECONorthwest said the drop occurred because residents fled the county to avoid the tax and the rebound occurred because the tax expired. In fact, affluent families in the county simply became less affluent during that period relative to those in the rest of the state. Between 2003 and 2005, all of Oregon went through the last stages of a recession and the beginning of a recovery. But the recession was steeper and longer, and the recovery slower, in the county than in the rest of the state because the dot-com bust precipitated the downturn. (The county is home to more dot-com firms than almost any other Oregon county.) [27] As a result, the average income of affluent Multnomah families grew erratically, while the average income of the affluent in other parts of the state grew steadily and faster. In 2006, these trends reversed sharply, as the county’s recovery finally took hold.

In short, the ECONorthwest study wrongly blames taxes for a set of changes in residency and migration patterns that actually reflect other economic and demographic factors, such as retirements, housing price differentials, and differences in business cycles. (Some of these factors are discussed further in Appendix II.)

New Jersey: The Conclusion That Wasn’t There

If the Oregon study shows how researchers can manufacture a link between taxes and migration, the anti-tax efforts in New Jersey involved lobbyists, policymakers, and some in the news media who were determined to find a taxes-migration link in a study that doesn’t even contain the word “tax” in its findings.

In 2010, Boston College’s Center on Wealth and Philanthropy issued a report on the potential effect of changing demographics on charitable giving in New Jersey. It showed a sharp reversal in the flow of wealth into and out of New Jersey resulting from the migration of people with a net worth of $1 million or more.[28] Between 2004 and 2008, this migration produced a net loss of $70 billion of wealth for the state, the bulk of which reflected a drop in the number and wealth of millionaires migrating into the state. By contrast, between 2000 and 2003, millionaire migration had brought a net $82 billion of wealth into the state.[29]

What does that have to do with taxes? In 2004, the year in which the wealth of out-migrants began exceeding the wealth of in-migrants, New Jersey increased its personal income tax rates on income in excess of $500,000. The New Jersey Chamber of Commerce — which co-commissioned the report — opposed the tax, and the Chamber’s chair incorrectly asserted that the report made it “crystal clear that the state’s tax policies are resulting in a significant decline in the state’s wealth.”[30] Governor Chris Christie cited the report in a budget address to the legislature, stating, “Ladies and gentlemen, if you tax them, they will leave.”[31]

A Wall Street Journal editorial described the data as “striking” and noted that the reported change in wealth flows began the same year New Jersey increased taxes on top earners.[32]

Those assertions overlooked a key fact: most of the “millionaires” in the Boston College report weren’t subject to that tax increase. The report studied families with a net worth of $1 million or more — not a net annual income of $1 million. In fact, the report states that in 2006 the average income of these migrants was only $159,000, far below the threshold at which the tax increase became effective. [33] Moreover, while the millionaire households moving into New Jersey during 2004-06 may have had less wealth than the millionaires moving out of the state, they actually had more income — $6.2 billion for the in-migrants, opposed to $5.3 billion for the out-migrants.[34] If it said anything about migration and income taxes, then, the report suggested that high-income households flocked to New Jersey after the tax went up.

John Havens, the report’s author and a Boston College professor, went out of his way to caution against concluding that the new tax was draining New Jersey of money. “Taxes are just one possibility,” he said in an interview. “I think the data could support a series of conclusions.”[35] But Governor Christie is still citing the report as proof that taxation causes migration. [36]

Confusing “Down” with “Out” in Maryland

A final example shows that even a preliminary shard of data can make its way into the news media and into policymakers’ debates as “proof” of a taxes-migration connection. In 2008, Maryland raised its income tax rate on incomes over $1 million; the rate stayed in effect through 2010. [37] Opponents of the increase pounced on the fact that in 2008, the number of state income tax filers with taxable incomes exceeding $1 million fell precipitously. At one point in 2009, even though the state comptroller said it was too early to know whether a significant number of millionaires had actually left the state, a Washington Examiner headline proclaimed, “Millionaires flee Maryland taxes.”[38] Similarly, in March 2010 a Wall Street Journal editorial pushed the migration myth with the headline, “Maryland’s Mobile Millionaires” and the subhead, “Income tax rates go up, rich taxpayers vanish.” [39] The fallacy continues to make the rounds.[40]

A recent report from the Institute of Taxation and Economic Policy (ITEP) presented actual tax return data that set the record straight. [41] The data reveal two key facts undermining the argument that tax-induced out-migration had much to do with the recent decline in million-dollar filers:

- Between 2007 and 2008, 3,404 Maryland taxpayers fell out of the million-dollar ranks because their incomes declined; they remained on the tax rolls, but in a lower tax bracket. By comparison, only 448 filers with million-dollar incomes in 2007 left the state or died, thereby disappearing from the rolls in 2008. (The income tax data do not show which filers moved and which died.)

- The great majority of these 448 “departed” filers did not flee over tax increases. We know this because hundreds of million-dollar filers have left the state every year for a long time. Between 2001 and 2006, an average of 5.7 percent of the state’s million-dollar filers in a given year disappeared from the state’s tax rolls the following year. Only if this rate of out-migration rose significantly in 2008 and 2009 would there be credible evidence that the millionaire’s tax affected out-migration at all.

In 2008, the out-migration rate of million-dollar filers was 6.2 percent. This deviation from the 5.7 percent trend of 0.5 percentage points implies that, in that year, 36 of the million-dollar filers might have left the state because of the new tax. (The comparable estimate for 2009 is 84 filers.) [42] But, as this report has shown, people move (or don’t move) for a host of reasons, none of which the journalists or policymakers who latched on to the statistic took into account. In any event, the figure certainly suggests that such impacts — if they exist — must be very small.

Even if the increase in out-migration was due solely to the tax rise, the total estimated impact — 120 filers leaving over two years — would be less than 2 percent of the total number of high-earning filers in 2007, the year before the tax went into effect. [43]

Conclusion

Critics of tax increases (and advocates of tax cuts) have sounded their alarm so loudly and often that their unproven assertion, “if you tax them, they will flee,” has gained credibility among some policymakers and journalists. But, thanks in part to wider access to actual tax return data, independent analysts have shown that the alarmists are wrong. More careful, thorough studies have assembled compelling evidence that the effects of tax increases on migration are, at most, small. In other words: raising taxes won’t spark a large wave of out-migration, and cutting taxes won’t spark a large wave of in-migration.

Policymakers need this sort of honest and accurate information about the implications of tax increases and tax cuts in order to help them address the very challenging fiscal and economic circumstances that most states continue to face. In the face of a weak economic recovery, continuing state budget shortfalls, and likely cuts in aid to states by the federal government, tax increases can allow states to avert deep cuts in public services such as education and health care. Tax cuts make those spending reductions more severe. Given this difficult scenario, state policymakers should not let false claims about taxes and migration shapes their decisions.

APPENDIX I

Methodology for Estimating the Financial Impact of Owning a Median-Priced, Three-Bedroom Home in California and Arizona For Average Middle-Class and Upper-Middle-Class Families

The body of this report points out the very large differential facing families in California and Arizona in the mid-2000s and suggests that this is a likely explanation for at least some of the state-to-state migration. This Appendix describes the source of that calculation.

Consider an average middle-class family in California wishing to buy a three-bedroom home there. In May 2007 such a home sold for $486,000. Let’s assume that the family attempted to qualify for a conventional mortgage — 30-year fixed rate, 20 percent down — at an interest rate of 5 percent. After making a down payment of $97,200, the family’s mortgage payments would be $25,000 per year, or 54 percent of its $46,000 income, an amount far beyond its reach. Even an average upper-middle-class family in California, with an income of around $76,000, would have to pay 33 percent of its income for its mortgage.

Now suppose that both the middle-class and upper-middle-class families considered moving to Arizona and purchasing a median-priced three-bedroom home there. Such a home sold for only $238,000 in May 2007, less than half its cost in California. After a down payment of $47,600, the middle-class family’s annual mortgage would total only $12,300, or 30 percent of the family’s income. Similarly, the average upper-middle-class family’s annual mortgage would be a very affordable 18.5 percent of income.

By contrast, neither family would have had a tax incentive to move to Arizona. In fact, their taxes would have been less if they had stayed in California. According to the Institute on Taxation and Economic Policy (ITEP), in 2007 the average middle-class family in Arizona paid 9.4 percent of its income in state and local taxes, compared to 8.3 percent in California. For the average upper-middle-class family, the increase in tax costs in Arizona would have been 0.1 percentage points.

Housing Cost Methodology

The Zillow Company provides estimates online going back 10 years for the median selling price of homes with selected characteristics for several, but not all, of the 50 states (www.zillow.com.). As noted in the text, we assumed that the family seeking to buy a three-bedroom home selling at the median price planned to finance its purchase with a conventional mortgage. In such a mortgage, the lender requires a down payment equal to 20 percent of the selling price, and the remainder is financed with a 30-year fixed rate mortgage. We assumed an interest rate of 5 percent. We did not take property taxes and property insurance into account. Based on these assumptions, we estimated the monthly mortgage payment with a mortgage payment calculator available at www.mortgagecalculator.org.

The average middle class family in each state is defined as a household with the average income of the non-elderly households in the middle quintile of the income distribution of all non-elderly households in the state, as reported by the Institute of Taxation and Economic Policy, ( www.itepnet.org/whopays3.pdf). The average upper-income family in each state is defined as the household with the average income of the non-elderly households in the second to highest quintile of all non-elderly households in the state, as reported in the aforementioned ITEP report.

The computation of the estimated housing costs and ratios of housing costs to income for the average middle-income and upper middle-income families for California and Arizona is presented in Table A-1.

| TABLE A-1: Housing Costs and Burdens for Median Priced Three Bedroom Home, California vs. Arizona, May 2007 |

||

| California | Arizona | |

| Median selling price of three-bedroom home, May 2007 | $486,000 | $238,000 |

| Down payment on a conventional mortgage (20 percent of row 1) | $97,200 | $47,600 |

| Principal to be financed (row 2 – row 1) | $388,800 | $190,400 |

| Monthly mortgage payment, 30-year, fixed rate, 5 percent | $2,083 | $1,022 |

| Annual mortgage payment (row 4 x 12) | $24,996 | $12,264 |

| Income of average middle-class family | $46,000 | $40,600 |

| Mortgage payment as percent of income [(row 5/row 6) x 100] | 54.3% | 30.0% |

| Income of average upper middle-income family | $75,700 | $66,300 |

| Mortgage payment as a percentage of income [(row 5/row 8) x 100] | 33.0% | 18.5% |

APPENDIX II

Further Analysis Refuting Evidence Presented by ECONorthwest, Inc. Allegedly Showing That Raising Income Tax Rates on Affluent Taxpayers Would Cause Many to Flee the State and Potential Affluent In-Migrants to Shun Oregon and Settle Elsewhere

As explained in the body of this report, ECONorthwest, Inc., a consulting firm, claimed in its report, An Analysis of Marginal and Average Tax Rates in Oregon and the Impact on Household Migration, (June 2009), that affluent taxpayers avoid states with high personal income taxes. The consulting firm presented three pieces of empirical evidence, each of which is flawed. The flaws are described briefly in the body of this report; the first two of them are presented here in greater detail.

Asserted Relationship Between State Tax Treatment of Capital Gains and Income Does Not Withstand Scrutiny

The consulting firm presented a regression equation allegedly showing that the higher the personal income taxes that a state imposes on affluent taxpayers, the smaller the percentage of their income is accounted for by capital gains. In this equation, the dependent variable is the percentage of the total income of a state’s affluent taxpayers accounted for by capital gains. The explanatory variable is the amount of state and local income tax deductions claimed by affluent taxpayers as a percentage of their income. The consultant defines affluent taxpayers as those with federal adjusted gross incomes equal to or greater than $200,000, as reported by the Internal Revenue Service. The consulting firm assumed that, if an affluent taxpayer has a high concentration of capital gains in his or her income, he or she is relatively mobile geographically and, therefore, responsive to interstate differences in taxes. Equation 1, below, shows the estimation of the equation with 2006 data.

| EQUATION 1: (net capital gains/income) = a +b*(personal income tax deductions/income) |

|

| Value of b | -0.787 |

| Standard Error | 0.340 |

| Statistically Significant? (p-value) | Yes 0.025 |

We tested whether the real factor driving net capital gains/income is not income tax levels but, rather, the concentration of retirees. For each state, we measured this concentration by computing the percentage of affluent tax filers claiming Social Security benefits. We also tested the possibility that the ratio of capital gains to total income of the affluent might be affected by climate (that is, better climate attracts more geographically mobile affluent people). So, we included as another explanatory variable the number of days per year that are partly cloudy or cloudy (as measured by the National Weather Service). When we included these variables, the significance of the coefficient on the ratio personal income taxes to income disappears and the absolute value of this coefficient shrinks considerably. The impact of the concentration of rich retirees among the affluent is much larger than the impact of the tax variable and is highly statistically significant. The results, also using 2006 data, are reported in Equation 2.

| EQUATION 2: (capital gains/income) = a + b(personal income tax)/income + c (cloudiness index)+ d(number claiming social security/total number of filers) |

|||

| B tax/income |

C cloudiness |

D concentration of retirees |

|

| Value of coefficient | -.455 | -.082 | .853 |

| Standard error | -.301 | -.071 | .203 |

| p. value | .137 | .302 | 0001 |

| Statistically significant? | No | No | Yes |

It is theoretically possible, however, that a low income tax attracts affluent retirees. If so, raising income taxes could induce retirees to leave a state or potential in-migrants to shun it. To test this possibility, we estimated another regression equation (Equation 3), in which the dependent variable is the concentration of retirees among the affluent, and the explanatory variables are the ratio of personal income taxes to income and cloudiness.

| EQUATION 3: (number claiming social security/total number of filers) = a + b(personal income tax/income) +c (cloudiness index) |

||

| B tax/income |

C cloudiness |

|

| Value of coefficient | -.367 | -.045 |

| Standard error | -.207 | -.056 |

| p value | .082 | .421 |

| Statistically significant? | No | No |

Although the coefficient on the tax variable is negative, it is not statistically significant from 0.

Therefore, these equations provide evidence that the estimated impact of the personal income tax/income ratio in ECONorthwest’s equation is biased. When the concentration of retirees among the affluent is included in the equation, evidence that high costs drive away capital gains income disappears.

Analysis of Migration Patterns Within Portland Metropolitan Area Is Biased

The consulting firm drew some arbitrary conclusions about the causes of migration patterns within the Portland metropolitan area, which includes Clark County, Washington. It found that from 1992 through 2006, taxpayers who moved from the Oregon portion of the metropolitan area to the Washington portion had a higher average annual income than that of taxpayers who migrated in the opposite direction. ECONorthwest arbitrarily concluded that relatively prosperous families originally living on the Oregon side were moving to Washington primarily to avoid Oregon’s income tax. [44]

The firm identified the number of families migrating from Oregon to Clark County, and their average income (in the year after they moved) in each of the 15 years it examined. By multiplying the number of migrants by their average income each year and summing over all 15 years, the firm estimated the total amount of income flowing out of the three Oregon counties into Clark County. ECONorthwest conducted the same exercise for families moving from Clark County to Oregon. It found that the income flowing from Oregon to Washington exceeded the amount flowing the other way by $1.3 billion. This amount, the consulting firm concluded, was the economic loss to Oregon, and the corresponding gain to Washington, of tax-induced migration in the first year after the movers changed their residence. The firm implied that if Oregon were to raise its income tax rate on high income households even further, its economic losses from cross-border flight would be even greater.[45]

ECONorthwest’s argument is flawed for at least three reasons:

First, workers who moved their families to Clark County but still worked in Oregon continued to pay income tax to Oregon on their wages, salaries, and business profits. According to the Census Bureau, 32 percent of workers living in Clark County commuted to an Oregon work site in 2000, almost identical to the 33 percent who did so in 1990.[46] Oregon lost taxes on only the unearned income of these commuters — interest, dividends, capital gains, etc.

Second, families with higher-than-average incomes in Oregon had reasons other than taxes to move to Clark County during the 15 years. For one thing, housing prices grew more slowly in Clark County than in Oregon. In 1990, the median price per room of an owner-occupied home in Multnomah was actually less than in Clark. Thomas Potiowsky, the State Economist of Oregon, explained that a booming Portland economy, fueled by the success of Nike, Intel, and a variety of other dot-com companies, drove up home prices throughout the Portland metro area. Clark County’s houses remained relatively affordable because the county had a large supply of undeveloped land, and regulations on land development were less stringent there than in the three Oregon Counties. Meanwhile, many Oregonian homeowners had a big incentive to sell their high-valued homes, move to Clark County, buy “more house” for their money (or the same sized house surrounded by more land). Real estate developers responded to the increase in demand for housing by constructing subdivisions consisting of new houses on relatively large land plots in Washington.[47]

Other perceived attributes besides relatively cheap housing also attracted families with higher-than-average incomes to Clark County, especially from Multnomah County.

The City of Portland was perceived by some of its residents as very “liberal” politically, aggressive in enforcing stringent environmental regulations that affected residents and businesses alike, and tolerant of people with perceived “alternative lifestyles.” Many of these residents cringed at the phrase found on many bumper stickers, tee shirts, and signs in Portland saying “Keep Portland Weird!” [48] Schools and public safety were perceived to have deteriorated in the city. By contrast, Clark County was perceived as “family friendly.” Schools were viewed as newer and better funded than in Multnomah County, and streets safer. Clark County had more open space. Houses had larger yards in which kids could play. There was less exposure to people who engaged in lifestyles perceived by some to be undesirable.[49]

Married people with children comprised a significant share of people moving from Oregon to Clark County. [50] This might have been another reason that migrants from Oregon to Clark County had higher incomes than those migrating the other way, since married people, especially with children, have higher family incomes than people with no children, regardless of their marital status.[51]

Migrants from Clark County to Oregon had lower incomes than those migrating the other way because they were younger and more likely to be single, not because rich families were fleeing to avoid Oregon’s income tax. Many were in their 20s and 30s and wanted to live in or near areas with plentiful work opportunities (such as downtown Portland or technology centers in Washington County). They also were attracted to the social life of Portland and its immediate environs.[52]

The third reason to question the analysis is that when put into perspective, $1.3 billion over that extended period in “income leakage” is not so much. Over the course of 1992-2006, Oregonians living in Clackamas, Multnomah, and Washington Counties reported $377 billion in adjusted gross income. That means only 0.34 percent [that is, $1.3 billion/($377 billion + $1.3 billion)] of income earned on the Oregon side “leaked out.” So even if the author’s income estimates are taken at face value, they suggest that Oregon’s recently-enacted tax increases will not unleash a flood of out-migration into Washington. While tax increases might cause some affluent Oregonians to cross the state line, this effect will not significantly shrink Oregon’s overall income tax base. The affluent Oregonians who stay put will pay higher taxes that will dwarf any revenue lost if a few leave.

End Notes

[*] Dylan Grundman, Anna Kawar, Eleni Orphinades, and Ashali Singham contributed to this report.

[1] Raven Molloy, Christopher L. Smith, and Abigail Wozniak, “Internal Migration in the United States,” Journal of Economic Perspectives, forthcoming, Table 2, p.12.

[2] Prominent surveys of the literature include Michael J. Greenwood, “Research on Internal Migration in the United States: a Survey,”Journal of Economic Literature, January 1975; Michael J. Greenwood, “Human Migration: Theories, Models, and Empirical Studies,” Journal of Regional Science, October 1985; George I. Treyz, Dan S. Rickman, Gary L. Hunt, and Michael J. Greenwood, “The Dynamics of U.S. Internal Migration,” The Review of Economics and Statistics, May 1993; Michael J. Greenwood, “Internal Migration in Developed Countries,” in M.R. Rosenzweig and O. Stark, eds., Handbook of Population and Family Economics (Amsterdam: Elsevier, 1997); William F. Frey, “Internal Migration,” in Paul Demeny and Geoffrey McNicoll, eds., International Encyclopedia of Population, New York: Macmillan, 2003; and William F. Frey, “Migration to Hot Housing Markets Cools Off,” Web-ed, Brookings Institution, December 2008.

[3] Alicia Sasser Modestino, “Voting with Their Feet: Local Economic Conditions and State Migration Patterns,” Regional Science and Urban Economics, May 2010. For an analysis of the impact of these housing differentials on migration, see Jeffery Zabel, The Role of the Housing Market in Migration Responses to Employment Shocks, Working Paper 09-02, New England Public Policy Center, Federal Reserve Bank of Boston, 2009.

[4] Specifically, these data compare the fifth-highest and fifth-lowest taxing states. See “Who Pays?” www.itepnet.org/whopays3.pdf.

[5] Public Policy Institute of California, “Are the Rich Leaving California?” June 2009, http://www.ppic.org/content/pubs/jtf/JTF_LeavingCAJTF.pdf.

[6] According to one analysis of U.S. Census data, as many as 379,000, or 9.3 percent of Louisiana’s population, fled the state because of Katrina and Rita in 2005 alone; see http://geography.about.com/od/obtainpopulationdata/a/postkatrina.htm.

[7] Internal Migration in the United States , Table 2, p. 12.

[8] People with a at least a college education, who tend to have relatively high incomes, tend to be more geographically mobile because their skills are marketable over a wider area. See Joshua Rosenbloom and William Sundstrom, The Decline and Rise of Interstate Migration in the United States: Evidence from the IPUMS, 1850–1990. Working Paper #9857, Cambridge, MA: National Bureau of Economic Research. July 2003. However, education level is but one trait that links higher income with a higher propensity to migrate across state lines, against several other traits, noted above, that cut the other way.

[9] Jeff Thompson, The Impact of Taxes on Migration in New England, Political and Economy and Research Institute, University of Massachusetts, Amherst, April 2011, pp. 14-15.

[10] While the Census-based data may have been available since 1970, scholars have needed to collect several decades worth of such data to evaluate how changes in state income tax provisions have affected the migration patterns of high-income households. See, Karen Conway and Jonathan Rork, “No Country for Old Men (or Women): Do State Tax Policies Drive Away the Elderly?” unpublished manuscript, March 2011.

[11] “No Country for Old Men (or Women)”, March 2011, Table 7, p. 46.

[12] This contrasts with their findings on estate and inheritance taxes, which we are only alluding to here since we are focusing on the impact of income taxes. See Joel Slemrod and John Bakija, Do the Rich Flee from High Tax States? Evidence from Federal Estate Tax Returns, Working Paper 10645, National Bureau of Economic Research, July 2004.

[13] Cristobal Young and Charles Varner, “Millionaire Migration and State Taxation of Top Incomes: Evidence from a Natural Experiment,” National Tax Journal, June 2011.

[14] Authors’ estimate from Millionaire Migration and State Taxation, Table 4, p. 31, and Table 5, p. 32. The authors provided estimates from the revenue gains for New Jersey only for years 2004 through 2006, but estimated the revenue losses from tax-induced out-migration, from 2004 through 2007. We attempted to estimate the revenue gain for 2007. The revenue gains from the tax increase grew each year, from 2004-2006. In 2006, the estimated revenue gains were $1.08 billion. We conservatively assumed that the revenue gains from the tax increase in 2007 were identical to those in 2006--$1.08 billion. In this manner, We arrived at an estimate of the revenue gains for the whole 2004-2007 period--$3.77 billion, $16.4 million is .4 percent of $3.77 billion.

In 2008, Young and Varner, then at Princeton University, and a colleague, Douglas S. Massey, undertook a study, similar to their recent work, on the impact of the tax increase on migration. There were three major differences: 1) The sociologists did not create a control group. They assumed that the 2004 tax increase caused the acceleration in the migration rate of tax filers. As a result, their estimates of the tax increase’s impact are greatly overstated. 2) In addition to estimating the tax increase’s effect on millionaire out-migration, they attempted to estimate the number of households deterred from migrating to New Jersey because of the tax increase and the impact of their behavior on income tax revenues. 3) They estimated the impact of the tax increase only from 2004 through 2006, since data for 2007 was not yet available. They found that from 2004 through 2006, 1,064 households either left New Jersey because of the tax increase or were deterred from moving into New Jersey because of it. The revenue consequence was a loss of $113 million on a total revenue gain (in the absence of tax related migration) of nearly $2.8 billion. The estimated percentage revenue leakage was 4 percent ($113 million/$2.8 billion). However, keep in mind that this estimate is severely upwardly biased, as the authors did not control for factors other than the tax increase that might have contributed to the change in migration behavior from 2004-2006. See Cristobal Young, Charles Varner, and Douglas S. Massey, Trends in New Jersey Migration: Housing, Employment, and Taxation, Woodrow Wilson School of Public Affairs, Policy Research Institute for the Region, September 2008.

[15] Young and Varner found that three-quarters of the revenue leakage was attributable to 18 taxpayers in the top 0.1 percent of the income distribution. Most of these received only investment income. Millionaire Migration, Table 5, p. 31.

[16] Martin Feldstein and Marian Wrobel, Can State Taxes Redistribute Money? Journal of Public Economics, June 1998.

[17] Millionaire Migration , p. 4.

[18] Andrew Leigh, Do Redistributive Taxes Reduce Inequality? National Tax Journal, June 2008.

[19] Jeff Thompson, Costly Migration and the Incidence of State and Local Taxes, University of Massachusetts-Amherst, Political Economy Research Institute, February 2011. Thompson did find circumstantial evidence that tax increases reduce the pre-tax wages of young middle-income workers, suggesting that their propensity to migrate in response to tax changes is high.

[20] For further discussion, see Jon Shure, “Many Wealthy Moving Down, Not Out” Center on Budget and Policy Priorities, December 22, 2011, http://www.offthechartsblog.org/many-wealthy-moving-down-not-out/ .

[21] For further discussion, see Jon Shure, “Many Wealthy Moving Down, Not Out” Center on Budget and Policy Priorities, December 22, 2011, http://www.offthechartsblog.org/many-wealthy-moving-down-not-out/ .

[22] See Chuck Marr and Michael Leachman, “Oregon Voters Approval of Tax Increase Noteworthy as Federal Tax Debate Opens,” Center on Budget and Policy Priorities, February 16, 2010.

[23] Robert Whelan, An Analysis of Marginal and Average Income Tax Rates in Oregon and the Effect on Household Location, ECONorthwest, Inc., June 2009. : http://www.oregonbusinessplan.org/LinkClick.aspx?fileticket=EbUBv-ZJFKw%3D&tabid=102 .

[24] “Nike Chairman: Anti-business Climate Nurtures 66, 67,” The Oregonian, January 17, 2010.

[25] http://www.blueoregon.com/2010/09/many-clark-county-residents-work-and-pay-income-taxes-oregon/ . However, these migrants to Clark County would escape taxation on their non-wage income, such as interest, dividends, and capital gains.

[26] See http://web.multco.us/finance/itax.

[27] In the county, the recession lasted four years (from 2000 to 2004). The average annual percentage drop in employment during the period was 1.6 percent, and in 2005, the county’s employment grew by only 0.4 percent. By contrast, the statewide recession lasted for three years (2000 to 2003). The average annual decline in employment during this period was only 0.3 percent.

[28] John Havens, “Migration of Wealth in New Jersey and the Impact on Wealth and Philanthropy,” Center on Wealth and Philanthropy, Boston College, Boston, MA, January 22, 2010. http://www.cfnj.org/news/Wealth-Migration-Study-February-2010.pdf .

[29] “Migration of Wealth in New Jersey,” Table 1.

[30] Leslie Kwoh, “New Jersey Loses $70B in Wealth During Five Years as Residents Depart,” Star Ledger, February 4, 2010. http://www.nj.com/business/index.ssf/2010/02/nj_loses_70b_in_wealth_over_fo.html .

[31] “Text of Gov. Chris Christie Budget Speech to Legislature,” March 16, 2010, http://www.nj.com/politics/index.ssf/2010/03/text_of_gov_chris_christie_bud.html.

[32] “A New Study Shows That Wealth Flees After Taxes Rise,” Wall Street Journal, February 13, 2010, http://online.wsj.com/article/SB10001424052748703630404575053324236600444.html .

[33] How could the net migration of the wealthy increase the state’s income but diminish its wealth? The character of in-migrants and out-migrants differ markedly. “The heads of wealthy households entering New Jersey are younger, earn higher incomes, and are more frequently employed….Heads of wealthy households leaving New Jersey tend to be older, more likely to be retired or widowed, and have more wealth.” “Migration of Wealth in New Jersey,” p. 11.

[34] “Migration of wealth in New Jersey,” Table 4.

[35] Tom Moran, “Can't blame taxes for flight of the wealthy from New Jersey,” The Star Ledger, February 7, 2010, http://blog.nj.com/njv_tom_moran/2010/02/cant_blame_taxes_for_flight_of.html .

[36] “Gov. Chris Christie blames Democratic tax, fee hikes for $70 billion in wealth leaving New Jersey,” http://www.politifact.com/new-jersey/statements/2011/jun/17/chris-christie/gov-chris-christie-blames-democratic-tax-fee-hikes/.

[37] The state created a new tax bracket on income in excess of $1 million with a tax rate of 6.25 percent. Under prior law, the highest bracket started at 5 percent and applied to all incomes in excess of $500,000; see http://individuals.marylandtaxes.com/taxforms/default.asp.

[38] “Millionaires flee Maryland taxes,” The Examiner, March 26, 2009, http://washingtonexaminer.com/education/2009/05/millionaires-flee-maryland-taxes .

[39] “Maryland’s Mobile Millionaires,” The Wall Street Journal, March 12, 2010, http://online.wsj.com/article/SB10001424052748703976804575114241782001262.html .

[40] See for instance Arthur B. Laffer, Stephen Moore, and Jonathan Williams, Rich States, Poor States, American Legislative Exchange Council, June 2011, p. 15.

[41] Institute on Taxation and Economic Policy, “Five Reasons to Reinstate Maryland’s Millionaire Tax,” Washington, D.C., March 9, 2011. http://www.itepnet.org/pdf/md_5millionaires_0311.pdf.

[42] According to ITEP’s analysis, in 2007 there were 7,192 million-dollar filers in 2007. One half of one percent of 7,192 equals 36 filers. In 2009, 364 million dollar filers dropped off Maryland’s income tax rolls--7.4 percent of the 4,932 million-dollar filers in 2008. This 7.4 percent rate of out-migration was 1.7 percentage points above the 2001-2007 trends of 5.7 percent. According to ITEP, in 2009, there were 4,134 million-dollar filers, 1.7 percent of which equals 84 filers. The estimated total number of filers leaving the state in 2008 and 2009 combined because of the tax increase was therefore 36 + 84, or 120 filers, 1.7 percent of the 7,192 million dollar filers in 2007.

[43] The state comptroller also released data on the number of million dollar filers in a given year who were not million-dollar filers in the previous year. This number was 1,592 and 1,526 in 2008 and 2009, respectively. These numbers are down sharply from the 3,207 such million-dollar filers in 2007. The mostly likely reason for this sharp decline is a large drop in native Marylanders climbing up into the million-dollar ranks from lower income brackets. It is possible that some of the drop was attributable to potential million-dollar in-migrants who chose not to come to Maryland because of the new tax.

[44] An Analysis of Marginal and Average Tax Rates in Oregon, p. 2.

[45] An Analysis of Marginal and Average Income Tax Rates in Oregon, p. 7.

[46] US Census Bureau, Journey to Work and Place of Work, http://www.census.gov/population/www/socdemo/journey.html

[47] Telephone interview by Robert Tannenwald with Thomas Potiowsky, State Economist of Oregon, June 2, 2011. We could not find data comparing the average size of a residential land plot among the four metro counties.

[48] The phrase was part of a campaign to promote local businesses in Portland. See www.keepportlandwierd.com.

[49] Telephone interview of Richard H. Carson by Robert Tannenwald, on June 13, 2011, and e-mail correspondence between Dr. Tannenwald and Mr. Carson on June 9, 2011. .Mr. Carson served as the Director of Clark County’s Community Development Department between 1999 to 2007. He also served as the Director of Planning and Management for METRO, Portland's regional elected government between 1988 to 1992. See www.richcarson.org for more on Mr. Carson’s credentials and background. He is currently the City Administrator of Cascade Locks, Oregon.

[50] Evidence that families migrating from Oregon to Clark County were larger than those migrating the other way can be gleaned from migration data collected by the Internal Revenue Service. Between 1992 and 2006, the average number of exemptions per return of federal income tax filers in the former group was 2.0, compared to 1.7 exemptions per return in the latter group. Authors’ calculations from data provided at www.irs.gov.

[51] For example, in Oregon, 2010 median income (in 2009 inflation-adjusted dollars) for a four-person family headed by a married couple was $71,593. The comparable figure for a married couple with no children under 18 years of age was $51,793. The comparable income for a non-family person was $29,606. Source: U.S. Census Bureau.

[52] Telephone Interview of Dr. Jason Jurjevich by Robert Tannenwald, on June 11, 2011. Dr. Jurevich is the Assistant Director of the Center for Population Studies, Portland State University, Portland, Oregon.

More from the Authors

Areas of Expertise

Areas of Expertise