Some States Much Better Prepared Than Others for Recession

As the widely expected recession sparked by the COVID-19 pandemic takes hold, the impact in some states will be unnecessarily harsh — especially if the recession is relatively deep — due to the state’s failure to adopt policies that support families and communities during a downturn, our review of state policies in four key areas finds. More specifically, people in states with inadequate budget reserves, weak unemployment insurance systems, relatively inaccessible Medicaid programs, and/or expensive higher education systems are particularly likely to struggle during the recession if they lose their jobs or enter the recession looking for work with few family resources to support them. Mississippi is the most poorly prepared. It’s the only state that ranks in the bottom ten across all four categories, while Florida, Louisiana, New Hampshire, and South Dakota rank among the worst in three categories. That said, every state likely will face significant budget gaps in the coming months, even those best prepared for the downturn, and will need aggressive help from the federal government.

"Every state could be better prepared for a recession; no state ranks in the nation’s top ten across all four policy areas."The pressures on state finances from the COVID-19 pandemic and resulting likely recession are mounting and will quickly become severe. Sales taxes, which make up a third of state revenues, are rapidly collapsing as restaurants and stores across the country close their doors and lay off their workers. Data are not yet available on the full scope of this collapse, but there is little doubt it is drastic, perhaps unprecedented. Income taxes, which make up another third of state revenues, also will decline sharply as mass layoffs rapidly push down people’s income and therefore their income taxes. Plus, the steep drop in the stock market means that wealthy people will soon begin reporting massive capital losses on their quarterly tax returns, further reducing state revenue.

Every state is likely to face serious fiscal challenges as the virus’s economic impact spreads, but state policies in place as the recession emerges will make an important difference in the experiences of people who are laid off or otherwise affected by the downturn. In states with relatively few reserves, relatively inaccessible Medicaid and unemployment programs, and relatively unaffordable colleges, people and communities will suffer unnecessarily. Conversely, in states with policies that are relatively strong in these areas, even the worst recession will cause considerably less harm than it would otherwise.

State policy choices also affect the length and depth of recessions for the entire country through their impact on residents’ income and spending, including spending at local businesses considering layoffs. State policy choices can sometimes have a lasting impact on families and communities as well, making them more or less productive and enhancing or diminishing our collective quality of life. Yet states vary significantly in how well they use public policy to protect their people — and their long-term economic health — from recessions. That’s especially true today, since some states seriously weakened their recession-preparation policies over the last decade, while others strengthened them.

To best weather recessions, states need:

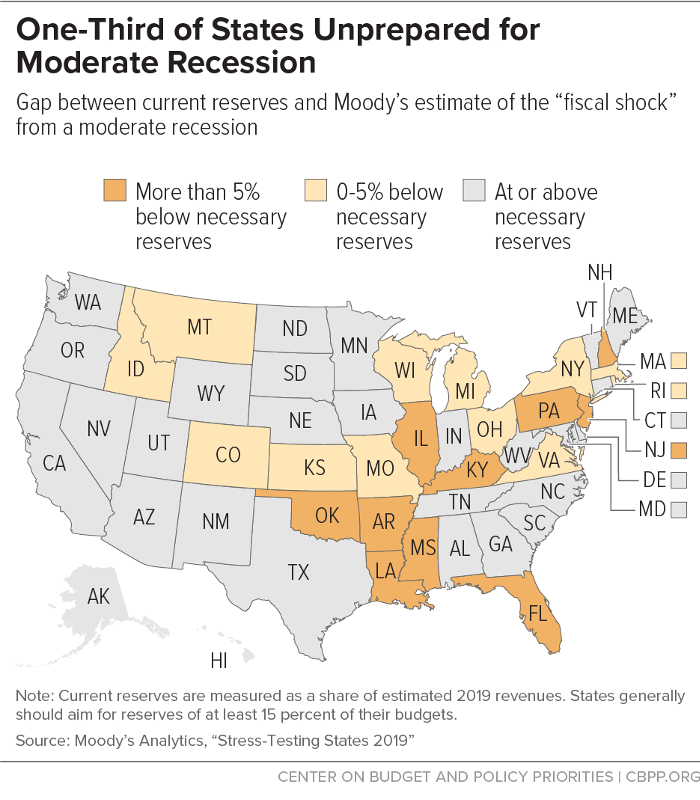

- Significant budget reserves and the flexibility to spend them when needed to limit the damage to state investments in people and infrastructure. When reserves are inadequate, states must either cut funding for schools, public health coverage programs, and other services during recessions, even as demand for these services is rising, or raise new revenue from people and businesses at a challenging time. Wyoming, with reserves exceeding 100 percent of the state’s budget, is best prepared for a downturn, according to a “stress testing” analysis by Moody’s Analytics. The least prepared states — some of which have reserves under 3 percent of the budget — include Louisiana, Oklahoma, Illinois, and New Jersey.

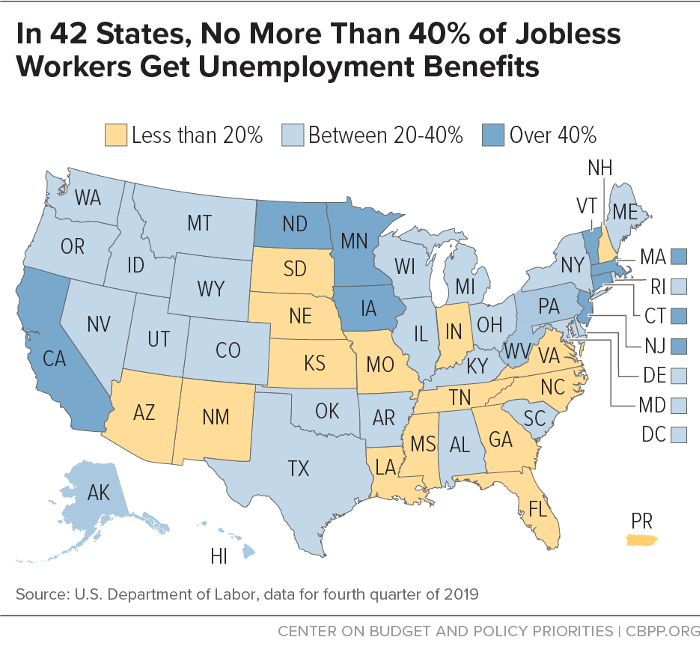

- Strong unemployment insurance systems. Unemployment insurance that reaches a significant share of jobless workers and provides benefits of adequate size and duration can help ensure that workers who lose their jobs still have some income to support their families and keep money flowing through local businesses, which otherwise might lay off even more people. In New Jersey and Massachusetts, 5 in 10 jobless workers receive unemployment benefits; in Mississippi, Nebraska, North Carolina, and South Carolina, fewer than 1 in 10 do.

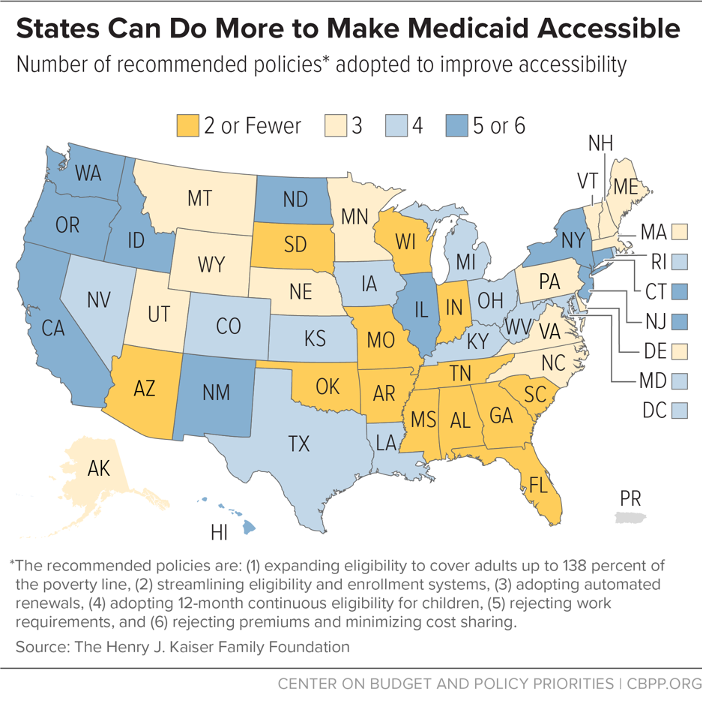

- Accessible Medicaid programs. States should ensure that people who lose health coverage because they are laid off or experience a drop in income, and people who can’t work because businesses aren’t hiring or for other reasons, can still get needed medical care, especially during a pandemic. State Medicaid rules also should ensure that people can keep coverage if they are already enrolled and remain eligible. New Mexico, Oregon, and Washington meet all six conditions we identified for promoting Medicaid accessibility, such as extending eligibility to low-income adults (by adopting the Affordable Care Act’s Medicaid expansion) and streamlining enrollment processes, while South Dakota meets just one of the conditions and Tennessee meets none.

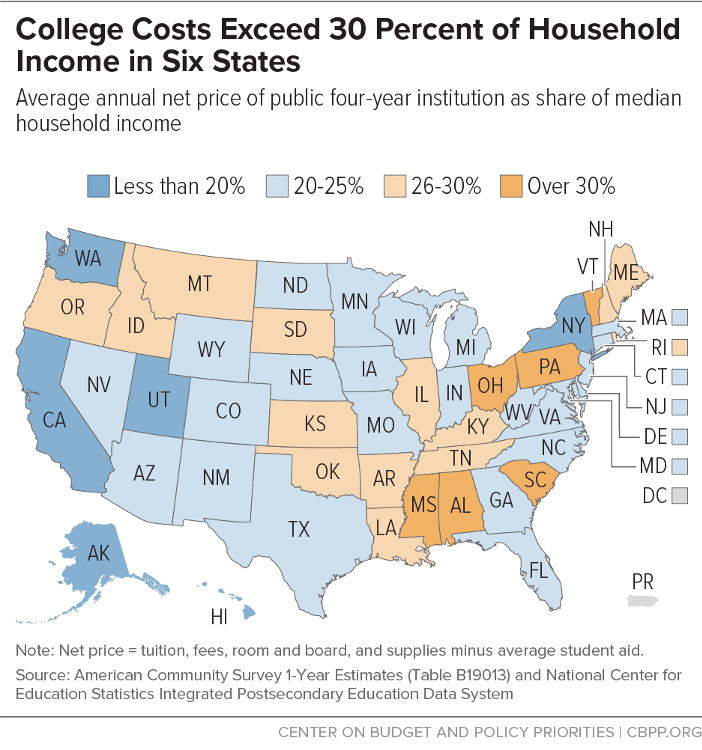

- Affordable public colleges and universities. Because jobless workers often seek additional training and education during economic downturns to expand their skills while the job market is weak, states need to ensure that college is affordable and accessible during downturns. The average net price of a public four-year institution ranges from 15 percent of median household income in Alaska to 36 percent in South Carolina.

While these policies are important for limiting a recession’s damage to a state’s economy, they are particularly vital to low-income families. Recessions disproportionately affect people with low incomes, who typically cannot meet their basic needs without public support such as access to health care, income for food, or housing assistance. People with low incomes also are especially affected by shifts in the labor market; during a downturn, they are more likely than other workers to lose their jobs.[1]

State policy decisions also have a particularly big impact on people of color. Historical racism and ongoing forms of discrimination and bias leave people of color, on average, with much less income and wealth than they would have otherwise, making them more likely to need public support, especially during a recession. Various state policies past and present have contributed to these inequities, so states have an obligation to make progress in reversing them, even during recessions.[2]

The federal government, unlike states, can spend more than it takes in during recessions to boost demand and thereby keep a recession from worsening. Emergency federal support for states and localities plays a crucial role in determining the depth and length of recessions by helping states sustain their spending, propping up the economy, and reducing the harm to families and communities. Emergency aid provided under the 2009 Recovery Act, which totaled more than $150 billion, closed about a quarter of the huge budget shortfalls that states faced after the last recession hit.[3] With states now beginning to face a lethal combination of rapidly rising costs and sharply declining revenues, federal policymakers should act aggressively to provide more substantial emergency financial aid to states.[4] The Families First Coronavirus Response Act is a good first step, providing about $36 billion of emergency aid in the form of an increase in the federal Medicaid matching rate. But it’s grossly inadequate to the fiscal crisis states will likely face in the weeks and months ahead. (See box, “Federal Aid to States Is Crucial During Recessions.”)

States, too, can take steps now — even with a recession looming — to limit the harm done. More specifically, they can take steps described in this paper to:

- Improve lawmakers’ flexibility to access reserve funds when needed and draw fully on reserves as the recession unfolds to limit harmful cuts to public services.

- Expand access to unemployment insurance to more jobless workers and make better use of workshare programs so more workers can keep their jobs.

- Expand Medicaid and improve access to the program in other ways, while suspending or eliminating work requirements and cost-sharing provisions.[5]

- Make colleges and universities more affordable, for instance by shifting tuition assistance from merit-based to need-based aid, reducing costs for low-income students and jobless workers, and offering in-state tuition to undocumented immigrants who attended a state’s K-12 schools.

Key Measures of State Preparedness

States vary greatly in how well prepared they are for a recession, based on an assessment of the following key policy areas. (See the Appendix for state-specific information.)

Adequate Reserves

States generally try to build up reserves in good times so they’re prepared for recessions and other fiscal emergencies and can avoid cutting public services during these difficult times. The amount of reserves a state needs depends on the potential volatility of its revenues and economy; states dependent on oil and other natural resources are particularly vulnerable because prices for these resources tend to fluctuate a lot. In general, states should aim for reserves equaling 15 percent or more of their budgets.

Fourteen states meet that standard today. Wyoming, whose economy depends heavily on natural resources, holds reserves that exceed its entire budget. Most of the other states with reserves equaling at least 15 percent of their budgets — Alaska, Idaho, Nebraska, Nevada, New Mexico, Texas, and West Virginia — also depend on oil or other natural resources. Some states, however, fall far below the 15-percent standard; in Arkansas, Illinois, Kentucky, and Pennsylvania, for example, total reserves are 3 percent of the budget or less.

Even accounting for the potential volatility of their revenue systems, Wyoming, Alaska, and North Dakota look well prepared for a downturn given their enormous reserves, according to a “stress testing” analysis by Moody’s Analytics.[6] Among states less reliant on resource extraction, Oregon stands out as particularly well-prepared. But a third of the states are unprepared for even a moderate recession, Moody’s found. (See Figure 1.) The least-prepared states include Louisiana and Oklahoma, whose economies are particularly vulnerable due to their heavy dependence on oil and other natural resources. Both states cut taxes deeply over the last 10-15 years, further weakening their revenue systems. Illinois, Kentucky, New Jersey, and Pennsylvania are also among the more poorly prepared; while their economies are not so volatile, they have exceptionally small reserves, partly because they failed for many years to adequately fund their public employee pension systems and now are struggling to restore those systems’ long-term health.

No matter how much a state holds in reserves, it won’t matter if policymakers do not or cannot access the reserves when needed. Yet some states severely constrain the use of reserves, such as by limiting how much can be withdrawn in a given year, requiring a supermajority vote in the legislature to approve withdrawals, or requiring replenishment of withdrawn reserves in a set amount of time, even if the economy has not yet recovered. Colorado and Missouri impose all three of these requirements, making their reserves particularly difficult to use when needed. Further, in states with large reserves based on natural resource extraction, such as Alaska, lawmakers cannot easily access most of the reserves, making the reserves less useful in a recession than might at first appear to be the case.

It is important to note that some states have built sizeable reserves by neglecting fundamental investments in their residents’ well-being and long-term prospects. North Carolina’s total reserves, for example, equaled 12.5 percent of the budget at the end of fiscal year 2019, leading Moody’s to find that the state is nearly prepared for a moderate recession. But over the last several years, North Carolina has sharply cut taxes, primarily for the wealthy and corporations, at the expense of schools and other basic public investments. Indeed, the state now operates one of the country’s most poorly funded school systems, with state and local funding per student more than $4,400 below the national average after adjusting for cost of living and other factors that affect state education costs, based on an analysis of 2017 data by the Education Law Center.[7] Thus, while North Carolina’s reserves may be nearly adequate to avoid substantial additional cuts if the looming recession is moderate, the cuts already imposed have weakened its future economic vitality. And if the recession is more severe, North Carolina may impose additional cuts on a school system that already is badly underfunded.

As of March 13, 2020, at least two states, Hawaii and Washington, have drawn on their reserves to respond to the COVID-19 public health crisis. Other states likely will soon follow suit. In the current environment, states should focus on addressing the health crisis and limiting the economic fallout from a recession, especially for the lowest-income families. That means drawing fully on their reserves as the recession develops. Now is not the time to build or hold on to reserves.

Strong Unemployment Insurance Systems

Unemployment insurance (UI), which provides some income for eligible workers who are laid off, is especially crucial during recessions, when many workers lose their jobs as employers scale back production. Income from UI helps workers maintain health insurance and access needed health care, mitigating the worst health effects of a layoff, which studies have linked to poorer health status and higher mortality.[8] UI also helps workers’ families remain relatively stable and avoid homelessness and hunger, ideally until the economy improves and more jobs are available. And it helps the broader economy at a crucial time by boosting demand. That is, because UI provides jobless workers with some income, they’re able to continue purchasing goods and services, which gives businesses a boost at a time when they might otherwise lay off more workers. As a result, the recession never gets as bad as it otherwise would have been.

While the federal government imposes certain minimum requirements on state UI systems, states have considerable discretion over benefit levels, eligibility rules, tax levels, and other aspects of their programs. States have used this discretion in very different ways, so state UI systems vary greatly in how prepared they are for the next recession.

For instance, from the 1960s until recent years, every state provided a maximum of 26 weeks of benefits, or more, for eligible jobless workers. (The median laid-off worker needed 25.2 weeks to find a new job in 2010, when the last recession’s impact on jobless workers reached its peak.[9]) That changed after the Great Recession, when nine states cut the maximum weeks allowed. The harshest rules are now in Florida and North Carolina, which offer no more than 12 weeks of benefits even in the worst recessions.

Other state UI eligibility rules also make a crucial difference during recessions. Most UI systems were built for the sort of economy in place decades ago and have never been updated for today’s workforce.[10] For instance, in many states workers laid off from part-time jobs — including parents caring for young children — must seek full-time employment to receive UI. Few states offer UI benefits for people who need to leave their jobs to care for a sick family member. And some states fail to count a worker’s most recent work history when determining eligibility, cutting off many low-income people employed in low-wage industries with volatile work hours. These antiquated rules particularly harm women and people of color, who are more likely to fall through these cracks in UI eligibility rules. For instance, women are much likelier than men to work in part-time jobs and to leave work to care for a family member. And African American workers are much likelier than white workers to experience discrimination in job hiring and treatment on the job, leaving them more often with spotty work histories and therefore less likely to qualify for UI.[11] (African Americans are also particularly likely to live in the South, where UI eligibility rules are generally more restrictive.)

The 2009 Recovery Act, adopted after the Great Recession struck, provided federally funded incentives to states to modernize their UI systems. Many states took advantage of these incentives to improve their programs. California, Maine, Nebraska, and the District of Columbia adopted all or nearly all of the reforms the Recovery Act encouraged, such as enabling people who leave work for compelling family reasons to qualify for UI. On the other hand, six states — Alabama, Florida, Kentucky, Mississippi, Missouri, and North Dakota — adopted none of the Recovery Act reforms, leaving federal money on the table.[12]

Since state eligibility rules vary so much, their UI systems reach widely varying shares of unemployed people. The UI systems in Mississippi, Nebraska, North Carolina, and South Dakota are barely functioning, reaching less than 10 percent of unemployed workers as of the fourth quarter of 2019. Sixteen states reach less than 20 percent of jobless workers. By contrast, only eight states — California, Connecticut, Iowa, Massachusetts, Minnesota, New Jersey, North Dakota, and Vermont — reach over 40 percent of eligible workers. (See Figure 2.)

The amount of benefits that eligible jobless workers receive also affects how well a state UI system assists families and communities (and the broader economy) during a recession. As with eligibility rules, benefit amounts vary greatly across the states. In five states plus the District of Columbia, the average weekly benefit is only a quarter or less of the average weekly wage. By contrast, Hawaii’s average weekly benefit is more than half the average weekly wage.[13]

States can also adopt work sharing programs that allow workers facing a potential layoff to share their hours with another employee and supplement their reduced income with UI.[14] This common-sense approach helps businesses retain talented, trained workers during difficult times so these workers can more easily return to full-time work as the economy improves. It also reduces costs for UI systems, which need only make partial payments to workers who otherwise would have no job at all. Yet 22 states lack work share programs, leaving workers and businesses without this option heading into the next recession.[15]

Federal Aid to States Is Crucial During Recessions

Nearly all states have to balance their budgets each year. During recessions, when revenues decline, states are forced to cut spending (including by laying off workers), raise new revenue, or both. By contrast, the federal government can spend more than it takes in. That’s a critical power during economic downturns, allowing the federal government to spend at a time when the private sector is scaling back, keeping the recession from getting worse.

A key way the federal government can support the economy during a downturn is by providing emergency federal support for states and localities. This support can limit both layoffs of teachers, health care workers, and others as well as damage to priority investments in the country’s future, such as schools and infrastructure.

During the Great Recession, the federal government provided two major forms of emergency aid to states and localities through the 2009 Recovery Act. The first was an across-the-board increase in federal matching rates for state Medicaid expenditures, with a trigger to deliver additional increases to states based on the condition of their economy. To qualify for the added funding, states were prohibited from cutting eligibility or enacting restrictions that would make it harder for eligible people to enroll and stay covered. The second major form of recession-related federal aid to states was primarily for education; states had to distribute much of it to local school districts using the formula they normally use for distributing state funds for K-12 education.

These crucial forms of emergency aid closed about a quarter of the combined $600 billion budget shortfall that states faced over the first five years after the Great Recession hit.a

Federal support for states and localities will again be critical in determining the recession that appears to be resulting from the COVID-19 pandemic. The newly enacted Families First Coronavirus Response Act is a good first step, providing about $36 billion to states through a 6.2 percentage point increase in the federal Medicaid matching rate (not including the Medicaid expansion population) as long as the public health emergency lasts.bbThis amount, however, is less than the 2009 Recovery Act provided, and likely far less than states will need to avoid laying off workers and cutting spending in other ways, deepening the recession. Federal policymakers should further enhance Medicaid matching rates, including an additional increase based on state economic conditions. They also should provide additional fiscal relief states can use to address the immediate health crisis and avoid layoffs and spending cuts that would worsen a recession and, in some cases, can cause lasting harm to families and communities.

a See Elizabeth McNichol, “Out of Balance,” CBPP, April 18, 2012, https://www.cbpp.org/research/out-of-balance.

b Jennifer Sullivan, “Medicaid Funding Boost for States Can’t Wait,” CBPP, March 12, 2020, https://www.cbpp.org/blog/medicaid-funding-boost-for-states-cant-wait.

Accessible Medicaid Programs

Recessions have a significant negative impact on physical and mental health, particularly for people of color, studies show.[16] Programs that help people meet health and social needs during a recession and its aftermath have been shown to mitigate these impacts. Medicaid and the Children’s Health Insurance Program (CHIP) provide low-income Americans with access to needed preventive health services and medical care, but state policies significantly affect who is eligible and whether eligible people can successfully navigate the enrollment and renewal processes.

During an economic decline, more people lose their jobs, which often means they lose job-based health coverage. Even people without job-based coverage going into a recession may experience an income decline that makes new coverage options available to them and their families. Some people might newly qualify for premium tax credits to purchase coverage on the health insurance marketplaces, and the lowest-income households could become eligible for Medicaid or (for children and youth) CHIP.

Medicaid is designed to respond to economic declines: when unemployment rises and incomes fall, enrollment increases. Medicaid and CHIP helped offset the loss of job-based coverage in previous recessions (see text box). To ensure that eligible people who need coverage can enroll, and to make the process as smooth as possible for both them and the state, states should adopt (or maintain) the following policies:

- Expanded Medicaid eligibility that covers non-elderly adults with incomes up to 138 percent of the poverty line (currently $17,236 for an individual or $35,535 for a family of four), as allowed under the Affordable Care Act (ACA). Adopting the ACA’s Medicaid expansion makes the program much more responsive to increased need during recessions, and the federal government pays 90 percent of the added costs.[17] Medicaid expansion has also been found to increase coverage rates and improve access to health care among unemployed workers.[18] This is one of the most important things states can do to prepare for the next recession. It is also among the highest-impact ways to cover more people at highest risk for complications related to COVID-19, including seniors not yet eligible for Medicare and people with chronic conditions.

- Streamlined eligibility and enrollment systems to allow individuals to (1) complete and submit applications using a mobile device, (2) scan and upload documents needed to make an eligibility determination, and (3) renew coverage online. Such systems enable individuals to get and maintain coverage even during otherwise complicated times.

- Automated renewals (sometimes called ex parte renewals), where the state uses existing data sources to automatically redetermine eligibility without requiring action from the individual or a caseworker.

- Twelve-month continuous eligibility for children in Medicaid and CHIP to ensure that enrolled children stay covered for a full 12 months, regardless of changes in circumstances such as income or household size. This is particularly important in recessions, which can expose children to adverse experiences such as food insecurity, lack of stable housing, family conflict, and child neglect and abuse.[19] Children with stable coverage during these volatile periods are likelier to have a usual source of care and to receive preventive health care, and their families are less likely to delay getting needed care for their children.[20] Notably, as a condition of receiving the increased federal matching dollars, the Families First Coronavirus Response Act prohibits states from terminating Medicaid coverage — for adults or children — for the duration of the public health emergency.[21]

States also should reject policies that make it harder for eligible people to enroll in and maintain coverage or obtain needed care. The Families First Coronavirus Response Act prohibits states from enacting these kinds of policies as a condition of receiving increased federal matching dollars. But in general, to be best prepared for a recession, states should:

- Reject policies that take Medicaid coverage away from people who do not meet work requirements. Such policies conflict with Medicaid’s central objective — namely, to provide affordable coverage to people who wouldn’t otherwise have it — and are the subject of ongoing legal action. They cause many people who are working or should be exempt to lose coverage because of the increased paperwork and red tape associated with burdensome reporting of work hours or work-related activities and the difficulty of obtaining an exemption.[22] During a recession, when unemployment is higher, work requirements would prevent even more people from obtaining and keeping coverage.

-

Reject premiums and minimize cost sharing, which create unnecessary barriers to maintaining coverage and accessing needed care. The barriers are even harder to clear during a recession, when household incomes are lower. Premiums lead fewer eligible low-income people to participate in Medicaid and CHIP, a large body of research shows.[23] Most of those who don’t enroll or lose coverage remain or become uninsured, so they face barriers to getting care and increased financial instability. Not surprisingly, premiums have the greatest adverse impact on people with the lowest incomes.

Cost sharing, even when the amount required is very small, can deter enrollees from accessing care and has been shown to have a negative effect on health outcomes.[24]

New Mexico, Oregon, and Washington meet all six of the conditions listed above for accessible Medicaid programs. Twenty-four states meet at least four of them, 14 states meet three of them, and 11 states meet two. South Dakota meets just one (automated renewals). Tennessee meets none of the six.

In addition to the six criteria listed here, states have many other ways to create simple, streamlined enrollment systems.[25] These include expanding the use of presumptive eligibility (that is, providing immediate, temporary Medicaid coverage to individuals who appear income-eligible while the state conducts a full eligibility determination), making real-time eligibility determinations, allowing enrollees to report changes to their household information online, allowing individuals to apply for more than one program at a time (like cash assistance, food assistance, and Medicaid), and adopting optimal policies for using electronic databases to verify eligibility. These kinds of enhancements are all the more important to expedite enrollment and reduce administrative burden on states during the public health emergency.

The Trump Administration has also allowed states to make changes that would harm enrollees or make it harder for eligible people to get coverage. The newest of these is an option to apply for a demonstration project converting the state’s Medicaid program for adults into a form of block grant.[26] Such demonstrations would likely worsen many enrollees’ health by taking away coverage and reducing access to care.[27] Moreover, by capping federal funding, the demonstrations would shift financial risk to states, with federal funding cuts most likely to occur when states can least absorb them. Particularly in this moment, when states face the dual threats of a public health emergency and an economic downturn, any actions to constrict rather than broaden Medicaid’s ability to respond are short-sighted and will harm people in greatest need of assistance.

Affordable Public Colleges and Universities

During recessions, when jobs are hard to find and layoffs increase, more people enroll in colleges and universities to boost their skills and training while the economy is weak. This choice benefits both them and state economies in the long term. Yet states vary considerably in how costly, and hence how difficult, they make this choice. The average net price of a public four-year institution — that is, published tuition and fees, room and board, and books and supplies minus the average aid received for a student — equaled at least 35 percent of median household income in Alabama and South Carolina in 2017, compared to 16 percent or less in Alaska, California, and Washington. (See Figure 4.)

The burden on households of color can be especially great, since they often face added barriers to employment and difficulty accessing better-paying jobs. In 17 states, the average net price of in-state tuition and fees in 2017 comprised 40 percent or more of the median household income for Black households. The average net price comprised 40 percent or more of the median household income for Latino households in seven states.

A major factor driving this variation is striking differences in how much each state spends on higher education apart from the tuition it collects. Some states push most of the costs of public colleges and universities on to students and their families, making higher education less affordable. In Vermont, New Hampshire, and Delaware, tuition finances at least 75 percent of state spending on higher education; in Pennsylvania, Colorado, and Michigan, tuition accounts for at least 70 percent. At the other end of the spectrum, tuition finances only 17 percent of state higher education spending in Wyoming and 20 percent in California.

States have shifted more college costs to students in recent decades, even as many families have had trouble absorbing additional expenses due to stagnant or declining incomes. From the 1970s through the mid-1980s, tuition and incomes both grew modestly faster than inflation. But by the late 1980s, tuition growth began outpacing income growth. Sharp tuition increases after the Great Recession hit exacerbated the longer-term trend. To make college more affordable and increase access to higher education, states need to reverse the long-term trend of disinvestment and increase funding for public two- and four-year colleges.

States can expand access and affordability further by improving immigrants’ access to public colleges and universities. Though federal immigration policy is in turmoil, states can take an inclusive approach to in-state tuition and financial aid that will benefit all residents regardless of immigration status.

Undocumented students are eligible for in-state tuition rates in 21 states plus the District of Columbia and have access to state financial aid in 12 states plus the District of Columbia.[28] State aid is essential because families that are undocumented have lower average incomes than other families, and a college education — even at in-state tuition rates — is out of reach for many without financial aid. Students who are undocumented don’t have access to Pell Grants and other federal assistance, which is by far the largest pool of need-based financial aid available to other students.

States already guarantee all children, no matter their immigration status, a place in K-12 schools to help them reach their potential and develop the educated workers of tomorrow. Giving the state’s high school graduates access to higher education at in-state tuition rates, with access to financial aid, builds on this investment.

Putting It All Together: Which States Stand Out?

States with adequate reserves and an effective safety net for people who lose their jobs or struggle to find work during a recession will fare better during the emerging recession than states that haven’t adequately prepared. With a recession now looming or already underway, states have little additional time to get ready. Policy decisions from past years will shape how their residents fare as the economy weakens.

In some states, those decisions may prove haunting. People who lose their jobs in Mississippi, for example, are especially likely to struggle, since that state scores among the most poorly prepared across the key policies[29] in all four categories considered in this paper. Mississippi ranks 44th in the adequacy of its reserves, 52nd (behind all states, the District of Columbia, and Puerto Rico) in the strength of its unemployment insurance system, and 47th in the affordability of its public universities, and has enacted only two of the six Medicaid provisions recommended for recession-preparedness.

Other states whose residents may suffer unnecessarily include Louisiana, New Hampshire, and South Dakota, which rank in the bottom ten across three of the four categories.[30] (Florida also ranks in the bottom ten across three categories, but ranks in the top ten in the fourth category — college affordability.) Five additional states — Arkansas, Kentucky, Oklahoma, Pennsylvania, and Tennessee — rank in the bottom ten on two of the four categories.

No state scores among the nation’s top ten in all four of the categories. California, North Dakota, and Oregon, though, score in the top ten in three categories.[31] (California falls somewhat short for adequate reserves, but ranks 15th in that category, while North Dakota and Oregon fall short on college affordability, ranking 15th and 36th, respectively.) Six states — Alaska, Connecticut, Hawaii, New Mexico, New York, and Washington — score in the top ten in two categories and the bottom ten in none.

The pressures on state finances from the COVID-19 outbreak are mounting and will quickly become severe. States face rising costs as they seek to contain the virus, and those costs will grow rapidly as businesses begin laying off workers and incomes decline, forcing large numbers of people to turn to Medicaid, unemployment insurance, and other forms of public assistance. At the same time, state revenue projections for the coming fiscal year will soon plummet, forcing state budgets out of balance. When that happens, states will start laying off teachers and other public employees, and start cutting back spending in other ways because states must balance their operating budgets annually, even in a recession. These layoffs and spending cuts will worsen the economy’s fall, and in some cases will inflict long-term harm on families and communities.

Federal aid should arrive before states begin implementing these cuts, since the goal is to minimize them. Federal policymakers must act aggressively now, on the cusp of a severe state fiscal crisis, to provide more substantial emergency financial aid to states.

States, too, can take steps now — even with a recession looming — to limit the harm done. More specifically, they can take steps described in this paper to:

- Improve lawmakers’ flexibility to access reserve funds when needed and draw fully on reserves as the recession unfolds, to limit harmful spending cuts to public services.

- Expand access to unemployment insurance to more jobless workers and make better use of workshare programs so more workers can keep their jobs.

- Expand Medicaid and improve access to the program in other ways, while suspending or eliminating work requirements and cost-sharing provisions.

- Make colleges and universities more affordable, for instance by shifting tuition assistance from merit-based to need-based aid, reducing costs for low-income students and jobless workers, and offering in-state tuition to undocumented immigrants who attended a state’s K-12 schools.

People in Puerto Rico Also Particularly Likely to Struggle in Next Recession

Puerto Rico is not included in this paper’s overall assessment above because comparable data are not available across all four policy categories. But there’s little question that Puerto Rico will likely struggle in the next recession. That’s especially true considering that the Commonwealth never emerged from the last recession and its economy has been contracting almost continuously since 2006.

- Reserves. Far from holding adequate reserves, Puerto Rico’s government is bankrupt and undergoing the largest public debt restructuring in U.S. history. The federally mandated oversight board steering that process is also responsible for restoring the island’s fiscal health. The devastation wrought by Hurricanes Irma and Maria, and the more recent string of powerful earthquakes, have only deepened Puerto Rico’s financial challenges. A national recession would make the situation much more difficult.

- Unemployment insurance. Only 16 percent of Puerto Rico’s eligible jobless workers receive UI, which ranks the Commonwealth 43rd among states and the District of Columbia. Further, Puerto Rico’s average weekly UI payment of $164 equals 30.9 percent of the island’s average weekly wage, which ranks Puerto Rico 37th among the states and D.C.

- Medicaid. Puerto Rico’s Medicaid program similarly needs restructuring. Unlike the states, whose federal funding covers a specified share of their Medicaid spending, Puerto Rico receives a fixed amount of federal funds each year as a capped block grant. And while each state’s matching rate is tied to its relative per capita income and can go as high as 83 percent, Puerto Rico’s matching rate is fixed at 55 percent, irrespective of need. (Last year, the federal government temporarily increased Puerto Rico’s Medicaid funding, including boosting its matching rate to 76 percent, but this increase lasts only through September 2021.)

- College affordability. Puerto Rico’s oversight board has prescribed deep cuts to the University of Puerto Rico (UPR), the island’s largest and only state-funded university. The central government subsidizes most of UPR’s operations, providing roughly $900 million annually as of 2017. The oversight board wants to cut those subsidies to approximately $400 million by 2024, claiming that more federal funding and other grants, as well as tuition hikes, will partly offset the cuts. The board also plans to cut the university’s operational expenses by some 10 percent, but most experts believe that the cuts will be much deeper.

| APPENDIX TABLE 1 | |||||||

|---|---|---|---|---|---|---|---|

| Measure #1: Adequate Reserves | |||||||

| State | Total Balances as a % of General Fund Expenditures FY20 | Rank | Moody’s “Stress Test”: (Total Surplus/ Shortfall) | Rank | Rainy Day Fund: No Replenishment Rule | Rainy Day Fund: No Limit on Use | Rainy Day Fund: No Supermajority Requirement |

| Alabama | 12% | 20 | 5% | 10 | 0 | 1 | 1 |

| Alaska | 53% | 2 | 81% | 2 | 0 | 1 | 0 |

| Arizona | 9% | 30 | 1% | 23 | 1 | 0 | 1 |

| Arkansas | 3% | 43 | -6% | 43 | 0 | 1 | 0 |

| California | 14% | 15 | 3% | 15 | 1 | 1 | 1 |

| Colorado | 8% | 35 | -2% | 33 | 0 | 0 | 0 |

| Connecticut | 15% | 14 | 3% | 18 | 1 | 1 | 1 |

| Delaware | 17% | 10 | 9% | 8 | 1 | 1 | 0 |

| District of Columbia | N/A | N/A | N/A | N/A | 0 | 0 | 1 |

| Florida | 8% | 34 | -6% | 41 | 0 | 1 | 1 |

| Georgia | 11% | 23 | 1% | 21 | 1 | 1 | 1 |

| Hawaii | 13% | 19 | 4% | 14 | 1 | 0 | 0 |

| Idaho | 14% | 16 | -1% | 30 | 1 | 0 | 1 |

| Illinois | 2% | 45 | -10% | 49 | 0 | 1 | 1 |

| Indiana | 14% | 18 | 4% | 13 | 1 | 1 | 1 |

| Iowa | 17% | 8 | 4% | 12 | 0 | 0 | 1* |

| Kansas | 9% | 32 | -2% | 34 | 1 | 1 | 1 |

| Kentucky | 3% | 44 | -9% | 48 | 1 | 1 | 1 |

| Louisiana | 4% | 41 | -15% | 50 | 1 | 0 | 0 |

| Maine | 11% | 26 | 0% | 24 | 1 | 1 | 1 |

| Maryland | 7% | 37 | 1% | 22 | 1 | 1 | 1 |

| Massachusetts | 12% | 21 | -4% | 36 | 1 | 1 | 1 |

| Michigan | 17%* | N/A | -3% | 35 | 1 | 0 | 1 |

| Minnesota | 11% | 24 | 5% | 11 | 0 | 1 | 1 |

| Mississippi | 10% | 28 | -7% | 44 | 0 | 0 | 1 |

| Missouri | 9% | 31 | -1% | 28 | 0 | 0 | 0 |

| Montana | 16% | 11 | -4% | 37 | 1 | 0 | 1 |

| Nebraska | 17% | 7 | 3% | 17 | 1 | 1 | 1 |

| Nevada | 17% | 9 | 12% | 7 | 1 | 1 | 1 |

| New Hampshire | 7% | 38 | -6% | 42 | 1 | 0 | 0 |

| New Jersey | 3% | 42 | -8% | 46 | 1 | 1 | 1 |

| New Mexico | 30% | 4 | 8% | 9 | 1 | 1 | 0 |

| New York | 8% | 33 | -1% | 31 | 0 | 1 | 1 |

| North Carolina | 13%* | N/A | -1% | 29 | 1 | 1 | 1 |

| North Dakota | 37% | 3 | 24% | 3 | 1 | 1 | 1 |

| Ohio | 10% | 29 | -2% | 32 | 1 | 1 | 1 |

| Oklahoma | 16%* | N/A | -8% | 47 | 1 | 0 | 0 |

| Oregon | 28% | 5 | 19% | 4 | 1 | 0 | 0 |

| Pennsylvania | 2% | 46 | -7% | 45 | 1 | 1 | 0 |

| Rhode Island | 5% | 40 | -5% | 39 | 0 | 1 | 1 |

| South Carolina | 16% | 12 | 2% | 19 | 0 | 1 | 1 |

| South Dakota | 11% | 25 | 3% | 16 | 1 | 1 | 0 |

| Tennessee | 7% | 36 | 0% | 25 | 1 | 0 | 1 |

| Texas | 16% | 13 | 16% | 5 | 1 | 1 | 0 |

| Utah | 12% | 22 | 2% | 20 | 0 | 1 | 1 |

| Vermont | 14% | 17 | 0% | 26 | 1 | 1 | 1 |

| Virginia | 6% | 39 | -4% | 38 | 1 | 0 | 1 |

| Washington | 10% | 27 | 0% | 27 | 1 | 1 | 1 |

| West Virginia | 26% | 6 | 14% | 6 | 0 | 1 | 1 |

| Wisconsin | 10%* | N/A | -5% | 40 | 1 | 1 | 1 |

| Wyoming | 109% | 1 | 130% | 1 | 1 | 1 | 1 |

| APPENDIX TABLE 2 | ||||||

|---|---|---|---|---|---|---|

| Measure #2: Strong Unemployment Insurance Systems | ||||||

| State | Recipiency Rate | Rank | Number of Modernization Policies Enacted* | Work Share Program | Average Weekly Benefit as Share of Average Weekly Wage | Rank |

| Alabama | 26% | 28 | 0/7 | 25% | 49 | |

| Alaska | 38% | 13 | 5/7 | 26% | 46 | |

| Arizona | 11% | 46 | 3/7 | ✓ | 23% | 51 |

| Arkansas | 22% | 33 | 5/7 | ✓ | 33% | 30 |

| California | 42% | 8 | 6/7 | ✓ | 25% | 49 |

| Colorado | 25% | 30 | 6/7 | ✓ | 40% | 17 |

| Connecticut | 46% | 4 | 5/7 | ✓ | 31% | 33 |

| Delaware | 26% | 25 | 5/7 | 27% | 44 | |

| District of Columbia | 32% | 18 | 7/7 | ✓ | 21% | 52 |

| Florida | 11% | 47 | 0/7 | ✓ | 26% | 45 |

| Georgia | 17% | 42 | 3/7 | 31% | 37 | |

| Hawaii | 39% | 12 | 5/7 | 55% | 1 | |

| Idaho | 23% | 32 | 3/7 | 42% | 12 | |

| Illinois | 39% | 11 | 5/7 | ✓ | 35% | 28 |

| Indiana | 18% | 40 | 2/7 | 33% | 31 | |

| Iowa | 43% | 6 | 4/7 | ✓ | 46% | 5 |

| Kansas | 19% | 39 | 5/7 | ✓ | 44% | 8 |

| Kentucky | 21% | 36 | 0/7 | 43% | 9 | |

| Louisiana | 11% | 48 | 1/7 | ✓ | 23% | 51 |

| Maine | 24% | 31 | 7/7 | ✓ | 40% | 16 |

| Maryland | 22% | 34 | 4/7 | ✓ | 31% | 35 |

| Massachusetts | 57% | 1 | 4/7 | ✓ | 39% | 19 |

| Michigan | 29% | 22 | 2/7 | ✓ | 32% | 32 |

| Minnesota | 45% | 5 | 5/7 | ✓ | 42% | 10 |

| Mississippi | 9% | 52 | 0/7 | 28% | 41 | |

| Missouri | 20% | 37 | 0/7 | ✓ | 29% | 40 |

| Montana | 38% | 14 | 4/7 | 46% | 3 | |

| Nebraska | 10% | 49 | 6/7 | ✓ | 40% | 18 |

| Nevada | 30% | 21 | 5/7 | 38% | 21 | |

| New Hampshire | 15% | 45 | 5/7 | ✓ | 31% | 34 |

| New Jersey | 55% | 2 | 4/7 | ✓ | 37% | 26 |

| New Mexico | 19% | 38 | 4/7 | 41% | 15 | |

| New York | 36% | 15 | 6/7 | ✓ | 27% | 43 |

| North Carolina | 10% | 50 | 5/7 | 28% | 42 | |

| North Dakota | 43% | 7 | 0/7 | 47% | 2 | |

| Ohio | 21% | 35 | 2/7 | ✓ | 39% | 20 |

| Oklahoma | 26% | 26 | 5/7 | ✓ | 45% | 6 |

| Oregon | 39% | 9 | 5/7 | ✓ | 42% | 13 |

| Pennsylvania | 35% | 16 | 3/7 | ✓ | 38% | 24 |

| Rhode Island | 39% | 10 | 5/7 | ✓ | 37% | 27 |

| South Carolina | 27% | 23 | 5/7 | 31% | 38 | |

| South Dakota | 10% | 51 | 4/7 | 41% | 14 | |

| Tennessee | 15% | 44 | 3/7 | 25% | 47 | |

| Texas | 26% | 27 | 2/7 | ✓ | 38% | 23 |

| Utah | 25% | 29 | 1/7 | 46% | 4 | |

| Vermont | 49% | 3 | 4/7 | ✓ | 42% | 11 |

| Virginia | 17% | 41 | 1/7 | ✓ | 29% | 39 |

| Washington | 31% | 19 | 5/7 | ✓ | 38% | 25 |

| West Virginia | 35% | 17 | 1/7 | 38% | 22 | |

| Wisconsin | 31% | 20 | 5/7 | ✓ | 35% | 29 |

| Wyoming | 27% | 24 | 2/7 | 44% | 7 | |

| APPENDIX TABLE 3 | |||||||

|---|---|---|---|---|---|---|---|

| Measure #3: Accessible Medicaid Programs | |||||||

| State | Medicaid Expansion | No Work Requirements1 | No Premiums or Cost Sharing for Non-Disabled Adults | 12 Months Continuous Eligibility for Kids in Medicaid and CHIP | Streamlined Eligibility and Enrollment System2 | State Processes Automated Renewals | Score |

| Alabama | ✓ | ✓ | 2/6 | ||||

| Alaska | ✓ | ✓ | ✓ | 3/6 | |||

| Arizona | ✓ | ✓ | 2/6 | ||||

| Arkansas | ✓ | ✓ | 2/6 | ||||

| California | ✓ | ✓ | ✓ | ✓ | ✓ | 5/6 | |

| Colorado | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Connecticut | ✓ | ✓ | ✓ | ✓ | ✓ | 5/6 | |

| Delaware | ✓ | ✓ | ✓ | 3/6 | |||

| District of Columbia | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Florida | ✓ | ✓ | 2/6 | ||||

| Georgia | ✓ | ✓ | 2/6 | ||||

| Hawaii | ✓ | ✓ | ✓ | ✓ | ✓ | 5/6 | |

| Idaho | ✓ | ✓ | ✓ | ✓ | ✓ | 5/6 | |

| Illinois | ✓ | ✓ | ✓ | ✓ | ✓ | 5/6 | |

| Indiana | ✓ | ✓ | 2/6 | ||||

| Iowa | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Kansas | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Kentucky | ✓ | ✓3 | ✓ | ✓ | 4/6 | ||

| Louisiana | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Maine | ✓ | ✓3 | ✓ | 3/6 | |||

| Maryland | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Massachusetts | ✓ | ✓ | ✓ | 3/6 | |||

| Michigan | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Minnesota | ✓ | ✓ | ✓ | 3/6 | |||

| Mississippi | ✓ | ✓ | 2/6 | ||||

| Missouri | ✓ | ✓ | 2/6 | ||||

| Montana | ✓ | ✓ | ✓ | 3/6 | |||

| Nebraska | ✓ | ✓ | ✓ | 3/6 | |||

| Nevada | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| New Hampshire | ✓ | ✓ | ✓ | 3/6 | |||

| New Jersey | ✓ | ✓ | ✓ | ✓ | ✓ | 5/6 | |

| New Mexico | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 6/6 |

| New York | ✓ | ✓ | ✓ | ✓ | ✓ | 5/6 | |

| North Carolina | ✓ | ✓ | ✓ | 3/6 | |||

| North Dakota | ✓ | ✓ | ✓ | ✓ | ✓ | 5/6 | |

| Ohio | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Oklahoma | ✓ | ✓ | 2/6 | ||||

| Oregon | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 6/6 |

| Pennsylvania | ✓ | ✓ | ✓ | 3/6 | |||

| Rhode Island | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| South Carolina | ✓ | ✓ | 2/6 | ||||

| South Dakota | ✓ | 1/6 | |||||

| Tennessee | 0/6 | ||||||

| Texas | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Utah | ✓ | ✓ | ✓ | 3/6 | |||

| Vermont | ✓ | ✓ | ✓ | 3/6 | |||

| Virginia | ✓ | ✓ | ✓ | 3/6 | |||

| Washington | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | 6/6 |

| West Virginia | ✓ | ✓ | ✓ | ✓ | 4/6 | ||

| Wisconsin | ✓ | ✓ | 2/6 | ||||

| Wyoming | ✓ | ✓ | ✓ | 3/6 | |||

| APPENDIX TABLE 4 | ||||||

|---|---|---|---|---|---|---|

| Measure #4: Affordable Public Colleges and Universities | ||||||

| State | Tuition Share of Public Higher Ed Appropriations, FY18 | Rank | Average Net Price as Share of Median Household Income, FY17 | Rank | In-state Tuition and Financial Aid Equity for Residents With Undocumented Status | In-state Tuition Equity for Residents With Undocumented Status |

| Alabama | 66% | 45 | 35% | 49 | ||

| Alaska | 28% | 5 | 15% | 1 | ||

| Arizona | 61% | 37 | 25% | 27 | ✓* | |

| Arkansas | 46% | 18 | 29% | 40 | ||

| California | 20% | 2 | 16% | 2 | ✓ | |

| Colorado | 71% | 47 | 24% | 24 | ✓ | |

| Connecticut | 56% | 33 | 22% | 16 | ✓ | |

| Delaware | 75% | 49 | 21% | 12 | ||

| District of Columbia | 50% | 23 | N/A | N/A | ✓ | |

| Florida | 28% | 6 | 20% | 7 | ✓ | |

| Georgia | 28% | 7 | 24% | 23 | ||

| Hawaii | 36% | 11 | 18% | 6 | ✓ | |

| Idaho | 27% | 4 | 26% | 31 | ||

| Illinois | 35% | 9 | 26% | 32 | ✓ | |

| Indiana | 61% | 39 | 21% | 11 | ||

| Iowa | 63% | 42 | 25% | 28 | ||

| Kansas | 52% | 27 | 28% | 37 | ✓ | |

| Kentucky | 50% | 24 | 30% | 42 | ✓ | |

| Louisiana | 48% | 20 | 30% | 41 | ||

| Maine | 56% | 32 | 27% | 35 | ||

| Maryland | 49% | 22 | 20% | 9 | ✓ | |

| Massachusetts | 47% | 19 | 23% | 19 | ||

| Michigan | 70% | 46 | 25% | 30 | ✓ | |

| Minnesota | 55% | 31 | 23% | 21 | ✓ | |

| Mississippi | 54% | 30 | 33% | 47 | ||

| Missouri | 48% | 21 | 25% | 26 | ||

| Montana | 54% | 28 | 26% | 33 | ||

| Nebraska | 42% | 14 | 25% | 25 | ✓ | |

| Nevada | 37% | 12 | 22% | 14 | ||

| New Hampshire | 79% | 50 | 30% | 44 | ||

| New Jersey | 60% | 36 | 20% | 10 | ✓ | |

| New Mexico | 26% | 3 | 23% | 17 | ✓ | |

| New York | 36% | 10 | 17% | 4 | ✓ | |

| North Carolina | 35% | 8 | 23% | 18 | ||

| North Dakota | 52% | 26 | 22% | 15 | ||

| Ohio | 59% | 35 | 31% | 45 | ||

| Oklahoma | 54% | 29 | 28% | 38 | ✓ | |

| Oregon | 57% | 34 | 27% | 36 | ✓ | |

| Pennsylvania | 73% | 48 | 34% | 48 | ||

| Rhode Island | 61% | 38 | 26% | 34 | ✓ | |

| South Carolina | 65% | 44 | 36% | 50 | ||

| South Dakota | 61% | 40 | 30% | 43 | ||

| Tennessee | 45% | 16 | 29% | 39 | ||

| Texas | 42% | 13 | 20% | 8 | ✓ | |

| Utah | 46% | 17 | 17% | 5 | ✓ | |

| Vermont | 84% | 51 | 32% | 46 | ||

| Virginia | 63% | 43 | 25% | 29 | ||

| Washington | 44% | 15 | 16% | 3 | ✓ | |

| West Virginia | 61% | 41 | 23% | 22 | ||

| Wisconsin | 51% | 25 | 23% | 20 | ||

| Wyoming | 17% | 1 | 22% | 13 | ||

| APPENDIX TABLE 5 | ||||||

|---|---|---|---|---|---|---|

| States in Top 10 and Bottom 10 on Key Measures | ||||||

| States | Moody's "Stress Test" | UI Recipiency | Accessible Medicaid Program | Net University Price/Income | Total Top 10s | Total Bottom 10s |

| Alabama | Top | Bottom | Bottom | 1 | 2 | |

| Alaska | Top | Top | 2 | 0 | ||

| Arizona | Bottom | 0 | 1 | |||

| Arkansas | Bottom | Bottom | 0 | 2 | ||

| California | Top | Top | Top | 3 | 0 | |

| Colorado | 0 | 0 | ||||

| Connecticut | Top | Top | 2 | 0 | ||

| Delaware | Top | 1 | 0 | |||

| District of Columbia | 0 | 0 | ||||

| Florida | Bottom | Bottom | Bottom | Top | 1 | 3 |

| Georgia | 0 | 0 | ||||

| Hawaii | Top | Top | 2 | 0 | ||

| Idaho | 0 | 0 | ||||

| Illinois | Bottom | Top | 1 | 1 | ||

| Indiana | Bottom | 0 | 1 | |||

| Iowa | Top | 1 | 0 | |||

| Kansas | 0 | 0 | ||||

| Kentucky | Bottom | Bottom | 0 | 2 | ||

| Louisiana | Bottom | Bottom | Bottom | 0 | 3 | |

| Maine | 0 | 0 | ||||

| Maryland | Top | 1 | 0 | |||

| Massachusetts | Top | 1 | 0 | |||

| Michigan | 0 | 0 | ||||

| Minnesota | Top | 1 | 0 | |||

| Mississippi | Bottom | Bottom | Bottom | Bottom | 0 | 4 |

| Missouri | Bottom | 0 | 1 | |||

| Montana | 0 | 0 | ||||

| Nebraska | Bottom | 0 | 1 | |||

| Nevada | Top | 1 | 0 | |||

| New Hampshire | Bottom | Bottom | Bottom | 0 | 3 | |

| New Jersey | Bottom | Top | Top | Top | 3 | 1 |

| New Mexico | Top | Top | 2 | 0 | ||

| New York | Top | Top | 2 | 0 | ||

| North Carolina | Bottom | 0 | 1 | |||

| North Dakota | Top | Top | Top | 3 | 0 | |

| Ohio | Bottom | 0 | 1 | |||

| Oklahoma | Bottom | Bottom | 0 | 2 | ||

| Oregon | Top | Top | Top | 3 | 0 | |

| Pennsylvania | Bottom | Bottom | 0 | 2 | ||

| Rhode Island | Top | 1 | 0 | |||

| South Carolina | Bottom | Bottom | 0 | 2 | ||

| South Dakota | Bottom | Bottom | Bottom | 0 | 3 | |

| Tennessee | Bottom | Bottom | 0 | 2 | ||

| Texas | Top | Top | 2 | 0 | ||

| Utah | Top | 1 | 0 | |||

| Vermont | Top | Bottom | 1 | 1 | ||

| Virginia | 0 | 0 | ||||

| Washington | Top | Top | 2 | 0 | ||

| West Virginia | Top | 1 | 0 | |||

| Wisconsin | Bottom | 0 | 1 | |||

| Wyoming | Top | 1 | 0 | |||

End Notes

[1] See Jared Bernstein and Keith Bentele, “Got Work? The Highly Responsive Labor Supply of Low-Income, Prime-Age Workers,” CBPP, updated December 13, 2019, https://www.cbpp.org/research/full-employment/got-work-the-highly-responsive-labor-supply-of-low-income-prime-age-workers.

[2] See Michael Leachman, Elizabeth McNichol, and Erica Williams, “States Can Make Progress Against Racial, Economic Inequities, Even in a Recession,” CBPP, forthcoming.

[3] See Elizabeth McNichol, “Out of Balance,” CBPP, April 18, 2012, https://www.cbpp.org/research/out-of-balance.

[4] Sharon Parrott et al., “Immediate and Robust Policy Response Needed in Face of Grave Risks to the Economy,” CBPP, March 19, 2020, https://www.cbpp.org/research/economy/immediate-and-robust-policy-response-needed-in-face-of-grave-risks-to-the-economy.

[5] As a condition of receiving the Families First Coronavirus Response Act’s increased federal matching rate, states may not cut Medicaid eligibility, implement policies that make it harder to enroll in or maintain Medicaid, terminate coverage (other than at the individual’s request or if the individual no longer resides in the state), or increase cost sharing or premiums above January 1, 2020 levels. This maintenance-of-effort requirement extends for the duration of the public health emergency.

[6] Moody’s Analytics, “Stress-Testing States, 2019,” October 2019, https://www.moodysanalytics.com/-/media/article/2019/stress-testing-states-2019.pdf.

[7] Danielle Farrie, Robert Kim, and David Sciarra, “Making the Grade 2019: How Fair Is School Funding in Your State?” Education Law Center, p. 4, https://edlawcenter.org/assets/Making-the-Grade/Making%20the%20Grade%202019.pdf.

[8] Elira Kuka, “Quantifying the Benefits of Social Insurance: Unemployment Insurance and Health,” National Bureau of Economic Research Working Paper 24766, June 2018, https://www.nber.org/papers/w24766.

[9] Drew DeSilver, “Four signs of the improving U.S. jobs situation,” Pew Research Center, February 6, 2015, https://www.pewresearch.org/fact-tank/2015/02/06/four-signs-of-the-improving-u-s-jobs-situation/#more-267072. How long a worker will be unemployed depends primarily on the state of the job market when they lose their job. See https://fivethirtyeight.com/features/the-biggest-predictor-of-how-long-youll-be-unemployed-is-when-you-lose-your-job/.

[10] For a good overview of the problems with UI systems, see Rachel West, “7 Steps to Make Sure Unemployment Insurance Is There When You Need It,” Talk Poverty, September 27, 2016, https://talkpoverty.org/2016/09/27/7-steps-make-sure-unemployment-insurance-need/.

[11] Austin Nichols and Margaret Simms, “Racial and Ethnic Differences in Receipt of Unemployment Insurance Benefits During the Great Recession,” Urban Institute, Unemployment and Recovery Project Brief #4, June 2012, https://www.urban.org/sites/default/files/publication/25541/412596-Racial-and-Ethnic-Differences-in-Receipt-of-Unemployment-Insurance-Benefits-During-the-Great-Recession.PDF.

[12] See Table 1 in National Employment Law Project, “Modernizing Unemployment Insurance: Federal Incentives Pave the Way for State Reforms,” May 2012, https://www.nelp.org/wp-content/uploads/2015/03/ARRA_UI_Modernization_Report.pdf?nocdn=1.

[13] CBPP calculations based on data from the U.S. Department of Labor’s quarterly reports on state UI systems available at https://oui.doleta.gov/unemploy/data_summary/DataSum.asp. See Appendix for data by state.

[14] For more on work sharing programs, see National Conference of State Legislatures, “Work Share Programs,” https://www.ncsl.org/research/labor-and-employment/work-share-programs.aspx. See also Dean Baker, “Can Work Sharing Bring the US Workplace into the 20th Century?” Center for Economic and Policy Research, June 21, 2018, https://cepr.net/can-work-sharing-bring-the-us-workplace-into-the-20th-century/.

[15] A list of states with current programs is available at NCSL, “Work Share Programs,” https://www.ncsl.org/research/labor-and-employment/work-share-programs.aspx.

[16] Claire Margerison-Zilko et al., “Health Impacts of the Great Recession: A Critical Review,” Current Epidemiology Reports, March 2016, https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4880023/.

[17] Paul D. Jacobs, Steven C. Hill, and Salam Abdus, “Adults Are More Likely To Become Eligible For Medicaid During Future Recessions If Their State Expanded Medicaid,” Health Affairs, Vol. 36, No. 1, January 2017, https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2016.1076. Medicaid expansion has also been shown to produce state budget savings by reducing, for example, hospitals’ uncompensated care costs, behavioral health costs, and corrections systems’ health care costs. See Jesse Cross-Call, “Medicaid Expansion Continues to Benefit State Budgets, Contrary to Critics’ Claims,” CBPP, October 9, 2018, https://www.cbpp.org/health/medicaid-expansion-continues-to-benefit-state-budgets-contrary-to-critics-claims.

[18] Thomas C. Buchmueller, Helen G. Levy, and Robert G. Valletta, “Medicaid Expansion and the Unemployed,” National Bureau of Economic Research Working Paper 26553, December 2019, https://www.nber.org/papers/w26553.

[19] Irwin Garfinkel, Sara McLanahan, and Christopher Wimer, eds., Children of the Great Recession, Russel Sage Foundation, August 2016, https://www.russellsage.org/publications/children-great-recession.

[20] Leighton Ku et al., “Improving Medicaid’s Continuity of Coverage and Quality of Care,” Association for Community Affiliated Plans, July 2009, https://www.communityplans.net/research/improving-medicaids-continuity-of-coverage-and-quality-of-care/.

[21] To be in compliance with the maintenance-of-effort provisions, states may only terminate coverage for individuals who no longer reside in the state, or for individuals who request their coverage be terminated.

[22] Jennifer Wagner and Jessica Schubel, “States’ Experiences Confirming Harmful Effects of Medicaid Work Requirements,” CBPP, updated October 22, 2019, https://www.cbpp.org/health/commentary-as-predicted-arkansas-medicaid-waiver-is-taking-coverage-away-from-eligible-people.

[23] Samantha Artiga, Petry Ubri, and Julia Zur, “The Effects of Premiums and Cost Sharing on Low-Income Populations: Updated Review of Research Findings,” Kaiser Family Foundation, June 1, 2017, https://www.kff.org/medicaid/issue-brief/the-effects-of-premiums-and-cost-sharing-on-low-income-populations-updated-review-of-research-findings/.

[24] Ibid.

[25] Jennifer Wagner, “Medicaid Agencies Should Prioritize New Applications, Continuity of Coverage During COVID-19 Emergency,” CBPP, March 19, 2020, https://www.cbpp.org/blog/medicaid-agencies-should-prioritize-new-applications-continuity-of-coverage-during-covid-19.

[26] State Medicaid Director Letter #20-001, RE: Healthy Adult Opportunity, Centers for Medicare & Medicaid Services, January 30, 2020, https://www.medicaid.gov/sites/default/files/Federal-Policy-Guidance/Downloads/smd20001.pdf.

[27] Jessica Schubel et al., “The Trump Administration’s Medicaid Block Grant Guidance: Frequently Asked Questions,” CBPP, February 6, 2020, https://www.cbpp.org/research/health/the-trump-administrations-medicaid-block-grant-guidance-frequently-asked-questions.

[28] These counts include Hawaii and Michigan, where access to in-state rates and aid — extended by Boards of Regents rather than state lawmakers — is limited to major state universities.

[29] The key policies used for these state rankings are the Moody’s “stress test,” the UI recipiency rate, the number of supportive Medicaid policies in place, and the net price of a four-year public university relative to median household income.

[30] Florida also scores in the bottom ten across three categories, but scores in the top ten for the fourth category: college affordability.

[31] New Jersey scores in the top ten across three categories, but scores in the bottom ten for the fourth category: adequate reserves.

More from the Authors

Areas of Expertise