Social Security beneficiaries with higher incomes pay income tax on part of their benefits. Those with incomes below $25,000 ($32,000 for couples) pay no tax on benefits, while those with the highest incomes pay tax on as much as 85 percent of their benefits. This arrangement is sound for several reasons:

- The substantial proceeds from taxing Social Security benefits are credited to the Social Security and Medicare trust funds, strengthening the programs’ financing.

- The taxation of benefits is broadly progressive, since people with low incomes (about half of all beneficiaries) pay nothing and the tax rate on benefits increases with income.

- As an earned benefit, Social Security should be subject to tax, like other earned benefits, such as employer pensions.

- Social Security’s tax treatment is more favorable than that of private defined-benefit pensions, primarily because of the protections for low-income beneficiaries.

Scaling back the taxation of Social Security benefits, as some lawmakers in both parties have proposed, would be unwise.Scaling back the taxation of Social Security benefits, as some lawmakers in both parties have proposed, would be unwise. Social Security faces a long-run financial shortfall estimated at 2.78 percent of payroll subject to the Social Security payroll tax, or roughly 1 percent of gross domestic product. Unless changes are made, the program’s trust funds will be depleted in 2035, at which time revenues will cover only about three-quarters of scheduled benefits.[1] Reducing the taxation of benefits would require raising Social Security payroll taxes or cutting Social Security benefits more than would otherwise be necessary to ensure adequate financing. These benefit cuts or tax increases would likely fall in part on low- and moderate-income beneficiaries. Moreover, making a smaller portion of benefits subject to tax would primarily help higher-income beneficiaries, making the Social Security program less progressive.

How Social Security Benefits Are Taxed

Social Security beneficiaries must pay federal income tax on a portion of their benefits if their income exceeds certain thresholds; the portion of benefits that is taxable rises with income. Income for this purpose equals a taxpayer’s adjusted gross income (AGI) plus tax-exempt interest, certain other tax-exempt income, and half of Social Security benefits (whether or not they are taxable); this is referred to as “modified AGI.” A three-part formula applies:

- For individuals with modified AGI below $25,000 and couples with modified AGI below $32,000, no Social Security benefits are taxable.

- For individuals with modified AGI between $25,000 and $34,000 and couples with modified AGI between $32,000 and $44,000, up to 50 percent of benefits are taxable. (The amount that’s taxable equals the lesser of 50 percent of benefits or 50 percent of the amount by which modified AGI exceeds the lower threshold.)

- For individuals with modified AGI over $34,000 and couples with modified AGI over $44,000, up to 85 percent of benefits are taxable.

For a detailed explanation of the tax calculation, see Appendix Table 1.

Taxes on Benefits Support Social Security and Medicare

The proceeds from taxing Social Security benefits provide an increasingly important source of income for both Social Security and Medicare.

- The revenue from taxing up to 50 percent of Social Security benefits is devoted to the two Social Security trust funds. In 2019, this will provide an estimated $36.9 billion in income to the Old-Age and Survivors and Disability Insurance trust funds, or about 3.5 percent of their total income. Since the income thresholds are not indexed for inflation, taxes on benefits will grow to 7.4 percent of Social Security income by 2028.[2]

- The revenue from taxing 50 to 85 percent of Social Security benefits is devoted to Medicare’s Hospital Insurance (HI) trust fund. This will represent $24.1 billion, or 7.4 percent, of HI income in 2019 and 12.4 percent of income by 2028.[3]

The taxation of benefits will provide almost $1 trillion to the Social Security and Medicare trust funds over the next ten years. Without this income, the programs would face greater funding shortfalls and earlier reserve depletion dates.

Taxation of Benefits Is Progressive

Taxes on Social Security benefits fall more heavily on high-income than low-income taxpayers. That’s both because a larger share of benefits is taxable for high-income taxpayers and because they face higher marginal income tax rates.

About half of Social Security beneficiaries pay no tax on their benefits because their incomes are below $25,000 ($32,000 for couples), according to the Congressional Budget Office (CBO). At the other end of the income spectrum, a small number of high-income taxpayers pay as much as 31 percent of their benefits in taxes. That’s equal to the top marginal income tax rate of 37 percent applied to 85 percent of their benefits. (The top rate applies to single tax filers with incomes over $510,300 in 2019 and couples with incomes over $612,350.)

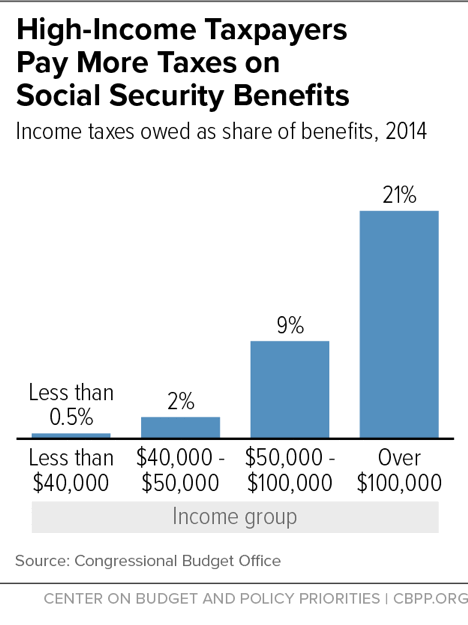

On average, beneficiaries pay about 7 percent of their benefits in income taxes. Beneficiaries with incomes below $40,000 owe less than 0.5 percent of their benefits in taxes, CBO estimates. In contrast, beneficiaries with incomes over $100,000 owe about 21 percent (see Figure 1).[4]

History and Rationale for Taxing Social Security Benefits

For more than four decades, Social Security benefits were not subject to income tax. The Treasury Department’s “rationale for not taxing Social Security benefits was that the benefits under the [Social Security] Act could be considered as ‘gratuities,’ and since gifts or gratuities were not generally taxable, Social Security benefits were not taxable.”[5]

Former Social Security Commissioner Robert M. Ball long argued that, since Social Security is an earned benefit, it should be taxed like other earned benefits, such as employer pensions. Workers pay income tax on private pensions to the full extent that their benefits exceed their contributions, with no income thresholds.

As a leading member of the Greenspan commission on Social Security in 1982-83, Ball had an opportunity to promote this idea.[6] The subsequent Social Security Amendments of 1983 provided that up to 50 percent of benefits would be taxable for beneficiaries with incomes above certain levels. A decade later, the Omnibus Budget Reconciliation Act of 1993 provided for the taxation of up to 85 percent of benefits for individuals with modified AGI above somewhat higher thresholds. The provision has since remained unchanged.

Lawmakers chose the 85-percent figure because actuaries estimated that no Social Security beneficiary had paid (through withholding from his or her paychecks) for more than 15 percent of his or her own benefits. The rest represents employer contributions and imputed return on both worker and employer contributions. Most beneficiaries contribute much less than 15 percent of their own benefits, so the 85-percent limit was considered generous.[7] In addition, the income thresholds shield low-income beneficiaries from tax.

Social Security Is Taxed More Favorably Than Private Pensions

The income tax treatment of Social Security benefits is considerably more favorable than that of private defined-benefit pensions, which are otherwise similar to Social Security. Because of the income thresholds and the 50- and 85-percent limits, only about 30 percent of Social Security benefits are currently subject to income taxation. In contrast, defined-benefit pensions are fully taxable except for the typically small portion representing the employee’s own after-tax contributions.

CBO and the Joint Committee on Taxation estimate that taxing Social Security and Railroad Retirement benefits in exactly the same way as private pensions would raise $411 billion in additional revenues over ten years. (Under this approach, the Social Security Administration would compute the taxable amount of benefits and report that information annually to each beneficiary.[8]) Stated another way, the current tax treatment of Social Security provides beneficiaries with a $411 billion tax reduction, relative to the tax treatment that private pensions face.

Proposals to Reduce the Taxation of Benefits

Despite the strong rationale for taxing a portion of Social Security benefits, some members of Congress from both sides of the aisle have proposed scaling it back. These proposed changes would reduce Social Security revenues, worsening the program’s long-run financial shortfall and requiring additional tax increases or benefit cuts to restore long-run solvency. In addition, they would make the system of Social Security benefits and taxes less progressive.

Former Rep. Sam Johnson, who chaired the Social Security Subcommittee when Republicans controlled the House, proposed scaling back the taxation of benefits as part of a bill to restore Social Security solvency by cutting scheduled benefits.[9] Johnson’s bill would have phased out (from 2045 through 2054) the portion of the taxation of benefits that is credited to the Social Security trust funds. (It would not have affected the income tax revenues credited to the HI trust fund.) That provision would have increased Social Security’s 75-year shortfall by 17 percent (0.47 percent of taxable payroll), according to the Social Security actuary.[10]

Social Security Subcommittee Chair John Larson has offered a different proposal to scale back the taxation of benefits as part of a comprehensive bill to expand Social Security benefits, raise payroll taxes, and assure long-run solvency.[11] The Larson bill would replace the existing pair of income thresholds with a single set of thresholds ($50,000 for individuals and $100,000 for couples), above which up to 85 percent of benefits would be taxable. As under current law, the thresholds would not be indexed. The amount of income tax revenue allocated to Medicare would not change compared to current law, and the remaining revenue from the taxation of benefits would be allocated to Social Security. While less costly than the Johnson provision, the Larson provision would still reduce Social Security revenues by an amount equal to 0.14 percent of payroll.[12] If the Larson bill did not scale back the taxation of benefits, it would not need to raise payroll taxes as much, thereby leaving more room to raise revenues for other pressing needs, such as strengthening the financing of Medicare and moving to universal health coverage.

| APPENDIX TABLE 1 | |

|---|---|

| Taxable Portion of Social Security Benefits | |

| Modified Adjusted Gross Income (AGI) | Taxable Portion of Benefits |

| Single Individual | |

| Less than $25,000 | None |

| $25,000 - $34,000 | Lesser of

|

| More than $34,000 | Lesser of

|

| Married Couple Filing Jointly | |

| Less than $32,000 | None |

| $32,000 - $44,000 | Lesser of

|

| More than $44,000 | Lesser of

|

End Notes

[1] Kathleen Romig, What the 2019 Trustees’ Report Shows About Social Security, Center on Budget and Policy Priorities, June 5, 2019, https://www.cbpp.org/research/social-security/what-the-2019-trustees-report-shows-about-social-security.

[2] 2019 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, Table IV.A3, https://www.ssa.gov/oact/TR/2019/tr2019.pdf.

[3] 2019 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds, Table III.B4, https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2019.pdf.

[4] Congressional Budget Office, The Taxation of Social Security Benefits, February 12, 2015, https://www.cbo.gov/publication/49948. These figures are for 2014; the numbers would be slightly different today because of the 2017 tax law and other factors.

[5] Larry DeWitt, Taxation of Social Security Benefits, , Office of the Social Security Administration Historian, Research Note #12, February 2001, https://www.ssa.gov/history/taxationofbenefits.html.

[6] Robert M. Ball, The Greenspan Commission: What Really Happened, Century Foundation, 2010, pp. 44-46.

[7] Wayne Liou and Julie Whittaker, Social Security: Calculation and History of Taxing Benefits, Congressional Research Service, October 27, 2016, p. 12, https://fas.org/sgp/crs/misc/RL32552.pdf. Note that this calculation is distinct from estimates of an individual’s “rate of return” on his or her Social Security contributions.

[8] Congressional Budget Office, Options for Reducing the Deficit: 2019-2028, December 2018, pp. 242-43, https://www.cbo.gov/system/files/2019-06/54667-budgetoptions-2.pdf.

[9] Social Security Reform Act of 2016, H.R. 6489, 114th Congress, https://www.congress.gov/bill/114th-congress/house-bill/6489.

[10] Social Security Administration, Office of the Chief Actuary (OACT), Letter to the Honorable Sam Johnson, December 8, 2016, https://www.ssa.gov/oact/solvency/SJohnson_20161208.pdf; OACT, Provisions Affecting Taxation of Benefits, Proposed Provision H6, June 25, 2019, https://www.ssa.gov/oact/solvency/provisions/charts/chart_run099.html.

[11] Social Security 2100 Act, H.R. 860, 116th Congress, https://www.congress.gov/bill/116th-congress/house-bill/860.

[12] OACT, Letter to the Honorable John Larson, Richard Blumenthal, and Chris Van Hollen, January 30, 2019, https://www.ssa.gov/oact/solvency/LarsonBlumenthalVanHollen_20190130.pdf; OACT, Provisions Affecting Taxation of Benefits, Proposed Provision H7, June 25, 2019, https://www.ssa.gov/oact/solvency/provisions/charts/chart_run223.html.

More from the Authors