New CBO Data Show Income Inequality Continues to Widen

After-Tax-Income for Top 1 Percent Rose by $146,000 in 2004

The Congressional Budget Office recently released extensive data on household incomes for 2004.[1]

CBO issues the most comprehensive and authoritative data available on the levels of and changes in incomes and taxes for different income groups, capturing trends at the very top of the income scale that are not shown in Census data.

The new CBO data document that income inequality continued to widen in 2004. The average after-tax income of the richest one percent of households rose from $722,000 in 2003 to $868,000 in 2004, after adjusting for inflation, a one-year increase of nearly $146,000, or 20 percent. This increase was the largest increase in 15 years, measured both in percentage terms and in real dollars.[2]

In contrast, the income of the middle fifth of the population rose $1,700, or 3.6 percent, to $48,400 in 2004. The income of the bottom fifth rose a scant $200 (or 1.4 percent) to $14,700.

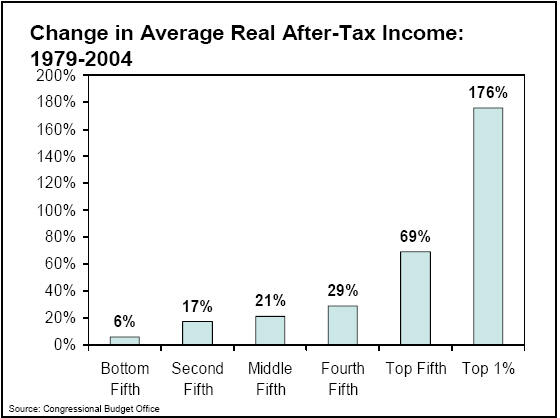

The new data also highlight the degree to which income gains over the past quarter-century have become increasingly concentrated at the top of the income scale. Since 1979 — the first year for which the CBO date are available — income gains among high-income households have dwarfed those of middle- and low-income households. Over this 25-year period:

-

The average after-tax income of the top one percent of the population nearly tripled, rising from $314,000 to nearly $868,000 — for a total increase of $554,000, or 176 percent. (Figures throughout this paper were adjusted by CBO for inflation and are presented in 2004 dollars.)

-

By contrast, the average after-tax income of the middle fifth of the population rose a relatively modest 21 percent, or $8,500, reaching $48,400 in 2004.

-

The average after-tax income of the poorest fifth of the population rose just 6 percent, or $800, over the past 25 years, reaching $14,700 in 2004.[3]

Because incomes grew much faster among the most affluent, this group’s share of the total national income also increased.

-

The top one percent of the population received 14.0 percent of the national after-tax income in 2004, nearly double its 7.5 percent share in 1979. (Each percentage point of after-tax income is equivalent to $71 billion in 2004 dollars.)

-

In contrast, the middle fifth of the population, which has 20 times more people in it, received 15.0 percent of the national after-tax income in 2004, down from 16.5 percent in 1979. The bottom fifth received 4.9 percent of the income in 2004, down from 6.8 percent in 1979.

Income is now more concentrated at the top of the income spectrum than in all but two years since the mid-1930s. This conclusion is reached by examining the CBO data in conjunction with data from a ground-breaking historical analysis of pre-tax income distribution trends published in a leading economics journal.[4] When viewed together, the studies indicate that the top one percent of households now receive a larger share of the national pre-tax income than at any time since 1937, except for the years 1999 and 2000.

| Table 1: | ||||

| Income Category | 1979 | 2004 | Percent Change | Dollar Change |

| Lowest fifth | $13,900 | $14,700 | 6% | $800 |

| Second fifth | 28,000 | 32,700 | 17% | 4,700 |

| Middle fifth | 39,900 | 48,400 | 21% | 8,500 |

| Fourth fifth | 52,300 | 67,600 | 29% | 15,300 |

| Top fifth | 92,100 | 155,200 | 69% | 63,100 |

| Top 1 Percent | 314,000 | 867,800 | 176% | 553,800 |

| Source: Congressional Budget Office, Effective Federal Tax Rates: 1979-2004, December 2006. | ||||

Income Gaps Widened in 2004

The CBO data show that gaps in income inequality widened significantly between 2003 and 2004. The share of after-tax income going to the top one percent rose from 12.2 percent in 2003 to 14.0 percent in 2004, an increase of 1.8 percentage points. As noted above, this amounts to $146,000 per household in the top one percent, equivalent to an additional $128 billion in income for the top one percent as a whole. This is the largest one-year increase in the share of income going to the top one percent in 15 years. The CBO data go back to 1979.[5], [6]

| Table 2: | ||

| Income Category | Dollar Change | Percent Change |

| Lowest fifth | $200 | +1.4% |

| Second fifth | 900 | +2.8% |

| Middle fifth | 1,700 | +3.6% |

| Fourth fifth | 2,000 | +3.0% |

| Top fifth | 11,600 | +8.1% |

| Top 1 Percent | 145,500 | +20.1% |

| Source: Congressional Budget Office, Effective Federal Tax Rates: 1979-2004, December 2006. | ||

The growing concentration of income at the top continues a long-term trend. Income concentration grew steadily during the latter half of the 1990s, and peaked in 2000, a year that the stock market hit a record high. From 2000 to 2002, income became less concentrated at the very top, partially due to the drop in the stock market; after-tax incomes fell from 2000 to 2002 for most income groups, but declined the most for the top one percent. In 2003 and 2004, however, the long-term trend toward growing income inequality returned.

Recent Federal Tax Policies Are Exacerbating Income Gaps

The CBO data also indicate that the growth in income disparities since 1979 largely reflects changes in before-tax income. That is, most of the divergence in income patterns among various income groups reflects diverging outcomes in the income that they received before taking changes in federal tax policies into account. Nonetheless, changes in federal taxes have had some influence over these patterns.

The direction in which the tax system influences inequality depends on the time period examined. Changes in federal tax policies exacerbated the growth in income disparities during the 1980s, when taxes were cut sharply for high-income individuals, but slowed the growth in income disparities during the 1990s, when tax rates for high-income households were raised and the Earned Income Tax Credit for low- and moderate-income working families was substantially expanded.

Legislation enacted since 2001 has provided taxpayers with about $1 trillion in tax cuts over the past six years. These large tax reductions have made the distribution of after-tax income more unequal. Because high-income households received by far the largest tax cuts, the tax cuts have increased the concentration of income at the top of the spectrum.

The CBO data provide additional evidence that the recent tax cuts have contributed to the widening income gaps. CBO provides data on effective federal income tax rates — that is, on the share of income that is paid in income taxes — for different groups of households. While all groups of households have seen declines in their effective federal income-tax rates since 2000, the declines have been much larger for the highest income taxpayers. For example, between 2000 and 2004, households in the top one percent of the income spectrum saw a drop in their effective federal income-tax rate of about 4.6 percentage points, more than twice the drop for households in the middle quintile (2.1 percentage points). This decline in the effective rate translated into an average income tax reduction of almost $58,000 for people in the top one percent, relative to what these households would have paid if their effective tax rate had remained unchanged.

These data do not provide a direct measure of the impact of tax policy changes because they reflect the impact not only of legislative changes but also of changes in household incomes and other factors that influence tax rates. Direct estimates by the Urban Institute-Brookings Institution Tax Policy Center that consider only the impact of the recent tax policy changes provide definitive evidence that the recent tax cuts have widened income inequality. The Tax Policy Center finds that as a result of the tax cuts enacted since 2001:[7]

-

In 2006, households in the bottom fifth of the income spectrum received tax cuts (averaging $20) that raised their after-tax incomes by an average of 0.3 percent.

-

Households in the middle fifth of the income spectrum received tax cuts (averaging $740) that raised their after-tax incomes an average of 2.5 percent.

-

But the top one percent of households received tax cuts in 2006 (averaging $44,200) that increased their after-tax income by an average of 5.4 percent.

-

Households with incomes exceeding $1 million received an average tax cut of $118,000 in 2006, which represented an increase of 6.0 percent in their after-tax income. That is more than double the percentage increase received by the middle fifth of households.

Finally, some of the tax cuts enacted in 2001 are still being phased in, and the tax cuts still phasing in are heavily tilted to people at the top of the income scale. These include the elimination of the tax on the nation’s largest estates and two income-tax cuts that started to take effect on January 1, 2006 and will go almost exclusively to high-income households.[8] As a result, the tax cuts ultimately will be even more skewed toward high-income households, and will increase income inequality to a still larger degree, than was the case in 2006.

End Notes

[1] Congressional Budget Office, Historical Effective Federal Tax Rates: 1979 to 2004, December 2006.

[2] Since 1979 (the first year for which CBO data are available), the after-tax income for the top one percent has increased by more than 20 percent only in 1986 and 1988. Analysts generally consider income data for the 1986-1988 period anomalous because a substantial amount of income "shifting" occurred during those years in response to the 1986 Tax Reform Act. For example, many high-income individuals chose to realize capital gains in 1986 in order to avoid paying the higher capital gains tax rates that took effect in 1987. For further discussion, see Joel Slemrod, "Income Creation or Income Shifting? Behavioral Responses to the Tax Reform Act of 1986," The American Economic Review, May 1995, pp. 175-180.

[3] In the CBO data, the income categories do not represent a fixed group of people from year to year but rather represent the people who fall into the various income categories in the year in question. As a result, the people in a given income category shift somewhat over time. This does not alter the conclusions of this paper but means that the trends shown in the data do not necessarily match the income trajectories of individual households.

[4] Thomas Piketty and Emmanuel Saez, “Income Inequality in the United States, 1913-1998,” Quarterly Journal of Economics, 118, 2003. Their tables have been updated through 2004 at http://emlab.berkeley.edu/users/saez/ The data presented by Piketty and Saez differ from those published by CBO for various reasons (e.g. Piketty and Saez present data for tax units, rather than households). The trends in the data, however, are the same. (The Piketty and Saez data are discussed in more detail in Aviva Aron-Dine and Isaac Shapiro, “New Data Show Extraordinary Jump in Income Concentration in 2004,” Center on Budget and Policy Priorities, revised October 13, 2006.)

[5] The income share of the top one percent grew faster in 1986 and 1988 than in 2004. The large 1986 and 1988 increases were the result of the previously-noted temporary income distortions related to the 1986 Tax Reform Act. (See footnote 2.)

[6] The CBO data show both before-tax incomes and after-tax incomes for the middle fifth of households rising between 2003 and 2004. Census data, relying on a different methodology, show the before-tax incomes of the middle fifth of households declining by 0.8 percent in 2004, a significant decline. The causes of the difference between the CBO and the Census data in this area are not clear. One reason may be the rising value of employer non-cash compensation, including employer-provided health benefits, which CBO counts as income and the Census figures do not. (A special analysis from the Census Bureau suggests that income and payroll taxes do not explain this trend; these Census estimates show that median household incomes declined in 2004 by 0.2 percent before taxes and 0.4 percent after taxes and government non-cash benefits, not a statistically different amount.)

Besides taxes and non-cash employee compensation, the CBO data differ from the before-tax Census figures in a number of other ways, including estimates of the value of Medicare and other public benefits. CBO also makes adjustments for household size when ranking households by income and assigning them to income categories.

[7] See Tax Policy Center tables T06-0273 and T06-0279 at www.taxpolicycenter.org.

[8] See "Two Tax Cuts Primarily Benefiting Millionaires Will Start Taking Effect January 1; Congress Declines to Rethink These Tax Cuts as It Proposes to Cut Aid to Low-Income Families," Center on Budget and Policy Priorities, December 28, 2005.

More from the Authors

Areas of Expertise