Extend CARES Act Eviction Moratorium, Combine With Rental Assistance to Promote Housing Stability

Without new relief measures to help more struggling families afford rent and avoid eviction, millions of households could face housing instability, homelessness, and greater overall hardship in the coming months. To prevent this crisis and protect families, the next relief package should include short-term emergency rental assistance to help prevent evictions for households behind on their rent, emergency housing vouchers to help those at greatest risk of prolonged homelessness upon eviction, and extensions of both income assistance and the federal ban on evictions to provide additional security and keep people from falling through the cracks.

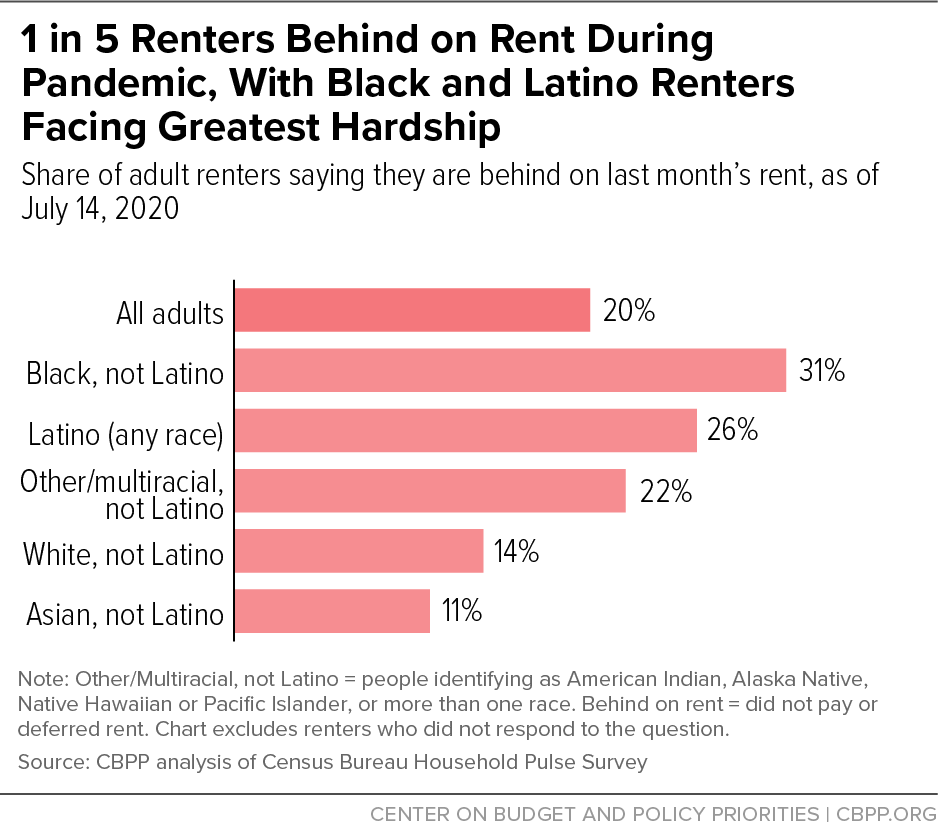

Emerging data show that the COVID-19 crisis is having especially severe impacts on low-income households.[1] Job losses have been heavily concentrated in industries that pay low average wages, and households with high housing costs and low incomes often have little financial cushion. Recent Census data show that 13.8 million adults in rental housing — 1 in 5 renters — report being behind on rent, with households of color reporting far higher rates of missed payments compared to the national average.[2] Because of sharp inequities in education, employment, housing, and health care stemming in large part from systemic racism, Black, Latino, Indigenous, and immigrant households have been particularly hard hit.

Congress included a limited ban on evictions in the Coronavirus Aid, Relief, and Economic Security (CARES) Act of March, but this moratorium expired on July 24. The federal eviction ban paused evictions in most federally subsidized housing and covered between 12.3 million and 19.9 million households, or 28.1 to 45.6 percent of all renter households, preventing them from being evicted if they were unable to pay their rent.[3]

Although the federal eviction ban — paired with various state and local protections — has helped households avoid eviction, it does not prevent people from accruing housing-related debt. People still owe rent payments even when they cannot be evicted for non-payment, so they are still at risk of eviction when any federal, state, or local moratoriums end if they are unable to pay their current rent or make up the past-due amounts.

Evictions can lead to long-term housing instability for households. The forced moves that result from evictions are particularly harmful for children and can disrupt their social, physical, and academic development. For people with low incomes, rent is typically their largest monthly expense, so help meeting this need can make a substantial difference in the family’s ability to afford other necessities and remain stably housed during the crisis.[4]

"Averting an eviction crisis in the coming months will require a multi-faceted approach that includes a continued pause on evictions."Averting an eviction crisis in the coming months will require a multi-faceted approach that includes a continued pause on evictions. Robust rental assistance and relief measures that shore up income — like expanded unemployment benefits — are critical for ensuring struggling households can afford to stay in their homes. To prevent evictions, and not just delay them, any eviction moratorium must be paired with rental assistance.

Current Eviction Protections and Their Limitations

The CARES Act included a 120-day federal eviction moratorium for renters who participate in federal housing assistance programs or live in a property with a federally backed mortgage.[5] The moratorium prohibited owners of the defined properties from both filing new evictions against tenants for not paying rent and charging additional fees because of non-payment. This ban expired on July 24, allowing landlords to issue 30 days’ notice for tenants to vacate properties.

The CARES Act moratorium covered tenants who receive assistance through most federal housing programs, including public housing, the Housing Choice Voucher program, Low Income Housing Tax Credit properties, and rural housing programs administered through the U.S. Department of Agriculture (USDA). Also included in the protections were renters in homes with mortgages owned, securitized, or insured by Fannie Mae, Freddie Mac, the Department of Housing and Urban Development (HUD), USDA, or other federal agencies. The federal moratorium also paused foreclosures for homeowners struggling to make payments on federally backed mortgages, and landlords of federally backed multifamily properties may request up to 90 days of forbearance, during which they could not evict any tenants in their property for non-payment.

Less than half of all 43.7 million renter households are estimated to have been covered by the CARES Act moratorium. According to the Federal Reserve Bank of Atlanta, the federal ban covered between 12.3 million and 19.9 million households (28.1 to 45.6 percent of all renter households), meaning that the federal moratorium didn’t cover as many as 31.4 million renter households.[6] (Separately, the Federal Housing Finance Agency [FHFA] has implemented a mortgage and eviction moratorium on single-family homes with mortgages through Fannie Mae or Freddie Mac. This applies to both homeowners and renters. FHFA recently extended this moratorium to August 31.[7])

Some renters are covered by state and local bans, but many others have no protection at all. As states shut down in March, courts closed in many places, which by default delayed eviction hearings; however, in places without specific bans, landlords could still begin the process while housing courts found a socially distant alternative.

The states and localities with eviction moratoriums provide varying levels of protection but typically extend to all renters, not just those living in the federally subsidized homes covered under the CARES Act.[8] Some of these measures have already expired, others are set to end soon, and some have been extended. Tracking evictions in a few cities has shown that local and state moratoriums have had at least some success in keeping renters safely in their homes.[9] After the statewide eviction ban in Wisconsin expired on May 27, eviction filings in the first two weeks of June increased 42 percent compared to the same time period in 2019, with a slightly greater increase (44 percent) reported in Milwaukee County.[10] In Shelby County, Tennessee, which includes the city of Memphis, about 9,000 eviction cases were pending when hearings resumed in mid-June.[11] In other places where evictions are still paused, filings have fallen sharply. In Boston, where the local moratorium extends through mid-August, only eight eviction filings were processed from late June to early July (a 99 percent decrease from the same period in 2019).[12]

The federal, state, and local bans have given many renters an important short-term reprieve but are insufficient by themselves. Although renters generally cannot be evicted for non-payment while a moratorium is in place, they still accrue debt if they are unable to pay their rent in full each month. When an eviction ban lifts, a previously protected tenant who missed a rent payment (or several) may still be unable to pay in the future, let alone address any back rent due.

Moreover, landlords, who may be coping with their own unemployment or additional expenses related to the pandemic, rely on rental income to cover maintenance and other property-related expenses, including property taxes. Smaller landlords spend at least half of their rental income on mortgage payments, property taxes, and insurance for their properties.[13] Significant decreases in rental income could lead to declines in property upkeep and foreclosures, which in turn can lead to more evictions and loss of affordable rental housing. In fact, a study of evictions in Milwaukee from 2009 to 2011 found that nearly 1 in 4 evictions was due to landlord foreclosure.[14] Local governments rely on property taxes from owners to fund essential services, such as health care, education, nutrition services, and housing programs. Many municipalities are already struggling to cover increased need during the pandemic, and decreases in property tax and other revenue from rental housing could lead them to be less prepared to deal with increased homelessness or other impacts of mass evictions.

Eviction and Homelessness Incur Costs for Renters, Landlords, and Cities

Failing to expand and extend eviction moratoriums or provide rental assistance could lead to millions of evictions over the next several months. One in five adults in rental housing reported that they were behind on rent in a Census Bureau Household Pulse Survey conducted in early July. That includes 12.5 million adults who had not paid rent and another 1.3 million whose rent had been deferred.[15]

The data also show wide racial and ethnic disparities in the share of renters behind on rent. Structural racism and discrimination create the circumstances that have contributed to Black and Latino households being more likely to be renters and to have lower incomes and fewer assets, which puts them at higher risk of missing rent payments and being evicted. The pandemic has impacted renters of all racial and ethnic backgrounds, but mass evictions would deepen existing disparities, many of which stem from explicitly and implicitly racist housing policies.20 (See Figure 1.)

Evictions may force families into more crowded housing conditions, like doubled up with other families or at a homeless shelter, putting them at higher risk of contracting COVID-19. Families that end up in the homelessness system, which is under considerable strain from the pandemic, will likely have to eat, sleep, and bathe with many other people. An April Centers for Disease Control and Prevention study of shelters in Boston, San Francisco, Atlanta, and Seattle found that 25 percent of shelter residents and 11 percent of staff had contracted COVID-19.[16] Other evicted households that become homeless but are unable or decide not to go to a shelter may struggle to access basic amenities like bathrooms due to restaurant and store closures.[17] Homelessness has lasting impacts, and among children, it is associated with increased likelihood of cognitive and mental health problems,[18] physical health problems such as asthma,[19] physical assaults,[20] accidental injuries,[21] and poor school performance.[22]

People often assume that homelessness is the only outcome of evictions, but while many people who are evicted from their homes enter homeless shelters, not all do.[23] Families with low incomes are resilient and often find ways to avoid homelessness, but evidence shows evictions are also harmful in the short and long term.

Displacement through eviction often results in households moving to housing with substandard living conditions in neighborhoods with higher rates of crime and poverty, which may lead to health and safety problems.[24] Landlords often reject potential tenants with a recent eviction, limiting renters’ choices when moving. Evictions can have especially severe consequences for children. Evictions often lead to children changing schools, and such disruptions are associated with students falling behind by almost half a year of school or more. Frequently moving between the ages of 6 and 10 is associated with lower incomes later in life for any child, and the more frequent the moves, the greater the impact.[25] If displaced from their previous neighborhood, adults must navigate losing social ties, finding new child care, changing jobs or losing income, and the other logistical and financial aspects of moving with little time to prepare.[26]

In addition to the human costs, evictions are expensive for tenants, landlords, and municipalities. When evicted, renters must bear the cost of moving or replacing their possessions in addition to the hurdle of paying a deposit for a new rental unit. Workers who are evicted may miss work to attend hearings or move, pay more in commuting costs from their new home, or lose their job entirely. Landlords and tenants both often have to pay court fees, and most landlords also incur attorney fees. Landlords may also lose rental income while waiting for a new tenant to move in. Meanwhile, municipalities must pay the costs of staffing courts and enforcing and supervising evictions. Evictions may also increase the need for homeless shelters and other social services, again increasing costs for local governments.

Mass evictions during the pandemic would be particularly harmful. Even if families are not forced into more crowded housing situations, going through the eviction process could put households at increased risk of contracting COVID-19 as they attend housing court and move their belongings. While some courts are conducting virtual hearings, others still require people to come in person. In one such example, the housing court denied a request for a virtual hearing from a woman in Louisiana with high risk of serious consequences if infected with COVID-19 due to her disability.[27]

Unemployment is expected to remain high well into 2021,[28] and evictions could make it even harder for affected individuals to find and maintain work. Evictions can sever a family’s social ties, exacerbating the social isolation and disruptions in education that children faced during spring school closures and may continue to experience as schools adjust for the new school year. Many systems that help struggling families are already over-burdened and would likely be unable to meet the rising need that such an increase in evictions would likely cause.

More Rental Assistance Funding Needed to Avoid Rise in Evictions, Homelessness

Although the CARES Act eviction moratorium and mortgage protections were limited to certain federally supported properties, they have been critical for keeping some people in their homes during the pandemic. The House-passed Heroes Act would extend and expand these renter and homeowner protections for up to a year. Extending and expanding the federal eviction and mortgage foreclosure bans are short-term solutions that would continue to protect people living in the specified properties but still lead to people accruing housing-related debt.

In addition to proposals targeted to people who need mortgage assistance (including landlords), Congress must provide assistance specifically for renters to enable families to pay past and future rent costs. This would ensure that families avoid accruing debt due to an inability to afford rent and possible eviction when the federal moratorium expires. Rental assistance also helps landlords pay their mortgage, property taxes, and other bills.

Specifically, the next relief package should include:

- Short-term emergency rental assistance. For most people, evictions can be mitigated with short- or medium-term help paying their rent.[29] The next relief package must include significant emergency rental assistance that helps people pay both current and past-due housing-related costs (including utilities). These resources should prioritize those facing the most severe housing challenges, including those experiencing or at high risk of homelessness. Emergency rental assistance is also critical for helping landlords cover their costs.

-

Emergency housing vouchers. For people who are homeless or renters who are at the greatest risk of eviction and homelessness, long-term rental assistance such as a housing voucher is much more likely than short-term rental assistance to provide the long-term stability that can be essential to reducing hardship and helping people get back on their feet. For renters, unpredictable factors such as illness or job losses can trigger eviction and homelessness, but underlying factors can significantly increase their chances of ending up in an emergency shelter or on the street. These factors include a history of poverty and housing instability (including prior episodes of homelessness), living doubled up with other families due to economic hardship, having high levels of debt or rent arrears, having already received an eviction notice, being pregnant or having young children, or attempting to flee domestic violence.[30] In addition, over 40 percent of people living in homeless shelters have a disability;[31] people with disabilities face higher unemployment rates than the general population and may experience discrimination or health-related barriers to work and accessing housing.[32]

Congress should provide $26 billion[33] for new Housing Choice Vouchers targeted to people who are homeless; at risk of homelessness; or fleeing or attempting to flee domestic violence, dating violence, sexual assault, or stalking.[34] These groups are facing some of the most urgent housing needs during the COVID-19 crisis and are most likely to need assistance the longest. This level of investment would help approximately 500,000 households access a safe, stable, and accessible home.

Long-term rental assistance like Housing Choice Vouchers reduces housing instability, homelessness, and poverty while improving outcomes for children and adults, research shows.[35] Despite such success, about 75 percent of households likely eligible for rental assistance do not have it due to funding constraints.[36] Vouchers are especially vital to reducing the racial inequities exacerbated by the pandemic. Seventy percent of households currently receiving vouchers are people of color,[37] and vouchers have a record of reaching low-income Black renters in need of assistance.[38] Long-term rental assistance will be critical to helping many of the hardest-hit families find or keep a home and to preventing further entrenchment of racial and economic disparities.

- Extend income assistance. Households will need more than just rental assistance to make up for lost income and stay stably housed, but additional support provided in the CARES Act that may help tenants is also set to expire soon. For example, many people who lost their jobs due to the pandemic have relied on expanded unemployment benefits, which both expanded who is eligible for jobless benefits and increased the amount they receive by $600 per week. The $600-per-week benefit increase is slated to expire at the end of July, while the eligibility expansions and additional weeks of jobless benefits are set to expire at the end of the year. Congress should extend these unemployment benefit expansions and provide other forms of support targeted on struggling households, such as temporary increases in SNAP benefits, the Child Tax Credit, and the Earned Income Tax Credit. These forms of support bolster income and can help families pay the rent.

End Notes

[1] Sharon Parrott et al., “More Relief Needed to Alleviate Hardship: Households Struggle to Afford Food, Pay Rent, Emerging Data Show,” Center on Budget and Policy Priorities, July 21, 2020, https://www.cbpp.org/research/poverty-and-inequality/more-relief-needed-to-alleviate-hardship.

[2] Census Bureau Household Pulse Survey data, Housing Table 1b. Last Month’s Payment Status for Renter-Occupied Housing Units, by Select Characteristics: United States, for data collected July 9-14, 2020, https://www.census.gov/data/tables/2020/demo/hhp/hhp11.html.

[3] Sarah Stein and Nisha Sutaria, “Housing Policy Impact: Federal Eviction Protection Coverage and the Need for Better Data,” Federal Reserve Bank of Atlanta, https://www.frbatlanta.org/community-development/publications/partners-update/2020/covid-19-publications/200616-housing-policy-impact-federal-eviction-protection-coverage-and-the-need-for-better-data.aspx.

[4] Debby Mayne, “Ten Biggest Expenses of the American Family,” PocketSense, October 31, 2018, https://pocketsense.com/ten-biggest-expenses-of-the-american-family-5646654.html.

[5] The legislation differentiates between mortgages for single-family properties, which have 1-4 units, and multifamily properties, which have 5 or more units, but tenants have the same protections regardless of the building’s size.

[6] Stein and Sutaria, op. cit; Harvard Joint Center for Housing Studies, “America’s Rental Housing 2020,” January 31, 2020, https://www.jchs.harvard.edu/sites/default/files/Harvard_JCHS_Americas_Rental_Housing_2020.pdf.

[7] Federal Housing Finance Agency, Press Release, June 17, 2020, https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Extends-Foreclosure-and-Eviction-Moratorium-6172020.aspx#.

[8] For more information on state eviction moratoriums, Eviction Lab has created a detailed scorecard for each state: https://evictionlab.org/covid-policy-scorecard/.

[9] See Eviction Lab’s eviction tracking at https://evictionlab.org/eviction-tracking/.

[10] Cary Spivak, “Predicted surge comes true: Eviction filing jump over 40% in Milwaukee County and state,” Milwaukee Journal Sentinel, June 15, 2020, https://www.jsonline.com/story/news/investigations/reports/2020/06/15/evictions-milwaukee-and-wisconsin-jump-over-40/3177897001/.

[11] Micaela Watts, “9,000 eviction hearings stalled by coronavirus resume Monday. Advocates say it’s the beginning of a crisis,” Memphis Commercial Appeal, June 14, 2020, https://www.commercialappeal.com/story/news/2020/06/14/evictions-stalled-coronavirus-resume-monday-memphis/5328897002/.

[12] Eviction Lab, “Eviction Tracking,” updated July 11, 2020, https://evictionlab.org/eviction-tracking/.

[13] Jenny Schuetz, “Halting evictions during the coronavirus crisis isn’t as good as it sounds,” Brookings Institution, March 25, 2020, https://www.brookings.edu/blog/the-avenue/2020/03/25/halting-evictions-during-the-coronavirus-crisis-isnt-as-good-as-it-sounds/.

[14] Matthew Desmond, “Unaffordable America: Poverty, housing, and eviction,” Institute for Research on Poverty at University of Wisconsin-Madison, March 2015, https://www.irp.wisc.edu/publications/fastfocus/pdfs/FF22-2015.pdf.

[15] Census Bureau Household Pulse Survey data, Housing Table 1b. Last Month’s Payment Status for Renter-Occupied Housing Units, by Select Characteristics: United States, for data collected July 9-14, 2020, https://www.census.gov/data/tables/2020/demo/hhp/hhp11.html.

[16] “Assessment of SARS-CoV-2 Infection Prevalence in Homeless Shelters — Four U.S. Cities, March 27-April 15, 2020,” Morbidity and Mortality Weekly Report, Centers for Disease Control and Prevention, May 1, 2020, https://www.cdc.gov/mmwr/volumes/69/wr/mm6917e1.htm?s_cid=mm6917e1_w.

[17] Carey L. Biron, “Closed bathrooms afflict U.S. homeless in coronavirus lockdown,” Reuters, May 26, 2020, https://www.reuters.com/article/us-health-coronavirus-usa-homelessness-f/closed-bathrooms-afflict-u-s-homeless-in-coronavirus-lockdown-idUSKBN2321FX.

[18] Marybeth Shinn et al., “Long-Term Associations of Homelessness with Children’s Well-Being,” American Behavioral Scientist, Vol. 51, No. 6, February 2008; Linda C. Berti et al., “Comparison of Health Status of Children Using a School-Based Health Center for Comprehensive Care,” Journal of Pediatric Health Care, Vol. 15, September/October 2001.

[19] Berti et al., op. cit.

[20] Stanley K. Frencher et al., “A Comparative Analysis of Serious Injury and Illness among Homeless and Housed Low Income Residents of New York City,” Trauma, Vol. 69, No. 4, October 2010.

[21] Ibid.

[22] Jelena Obradovic et al., “Academic Achievement of Homeless and Highly Mobile Children in an Urban School District,” Development and Psychopathology, 2009.

[23] Natasha Menon, “A Comparative Analysis of Urban Eviction Prevention Policies in New York City, Philadelphia, and San Francisco,” University of Pennsylvania, April 27, 2020, https://repository.upenn.edu/cgi/viewcontent.cgi?article=1039&context=ppe_honors.

[24] Desmond, op. cit.

[25] Kathleen Ziol-Guest and Ariel Kalil, “Frequent Moves in Childhood Can Affect Later Earnings, Work, and Education,” MacArthur Foundation, March 2014, https://housingmatters.urban.org/sites/default/files/wp-content/uploads/2014/09/How-Housing-Matters-Policy-Research-Brief-Frequent-Moves-in-Childhood-Can-Affect-Later-Earnings-Work-and-Education.pdf.

[26] Ibid.

[27] Order of Reversal (https://www.nhlp.org/wp-content/uploads/2020-CW-0531-Notice-Judgment-and-Disposition.pdf), Application (https://www.nhlp.org/wp-content/uploads/1st-Circuit-Writ-ADA.pdf), and Amicus Brief (https://www.nhlp.org/wp-content/uploads/2020.6.23-Amicus-BQ.pdf) litigation materials from Louisiana concerning a trial court’s denial of a woman’s request to hear an eviction case remotely due to a disability, which rendered her unable to attend an in-person hearing due to a higher risk of serious consequences as a result of possible COVID-19 infection. The justice of the peace court denied to order a remote hearing, and the tenant filed an application for review in the Louisiana Court of Appeals, granted in the order above. NHLP, “COVID-19 Litigation Resources,” July 8, 2020, https://www.nhlp.org/campaign/protecting-renter-and-homeowner-rights-during-our-national-health-crisis-2/.

[28] Congressional Budget Office, “Interim Economic Projections for 2020 and 2021,” May 19, 2020, https://www.cbo.gov/publication/56351.

[29] Some states and cities have realized this and utilized existing state-funded rental or housing assistance programs or federal fiscal relief to provide limited rental and mortgage assistance, but the resources have gone quickly and left many people without any help. See: David Roeder, “Citing huge need, city officials start issuing $1,000 grants for housing costs,” Chicago Sun Times, April 7, 2020, https://chicago.suntimes.com/coronavirus/2020/4/7/21212348/chicago-rent-mortgage-relief-housing-assistance-grants; Liz Navratil, “Minneapolis receives more than 7,800 requests for rental assistance,” Star Tribune, April 27, 2020, https://www.startribune.com/minneapolis-receives-more-than-7-800-requests-for-rental-assistance/569991162/; Tony Gorman, “DSHA halts renters relief program after being swamped with applications,” Delaware Public Media, April 27, 2020, https://www.delawarepublic.org/post/dsha-halts-renters-relief-program-after-being-swamped-applications; Marisa Kendall, “Three days after launch $11 million Santa Clara County coronavirus relief fund runs out of money,” Mercury News, March 27, 2020, https://www.mercurynews.com/2020/03/27/three-days-after-launch-11-million-coronavirus-relief-fund-runs-out-of-money/.

[30] Center for Evidence-based Solutions to Homelessness, “Homelessness Prevention: A Review of the Literature,” January 2019, http://www.evidenceonhomelessness.com/wp-content/uploads/2019/02/Homelessness_Prevention_Literature_Synthesis.pdf.

[31] U.S. Department of Housing and Urban Development, “The 2016 Annual Homeless Assessment Report to Congress,” December 2016, https://files.hudexchange.info/resources/documents/2016-AHAR-Part-2.pdf.

[32] U.S. Bureau of Labor Statistics, “Persons with a Disability: Labor Force Characteristics Summary,” U.S. Department of Labor, February 26, 2020, https://www.bls.gov/news.release/disabl.nr0.htm.

[33] This is the cost over five years. Representative Maxine Waters (D-CA) and Senator Sherrod Brown (D-OH) both introduced proposals (H.R. 7084 and S. 4164, respectively) to provide $10 billion for 200,000 new vouchers.

[34] Vouchers for people experiencing or at risk of homelessness may also be helpful for people transitioning from publicly funded institutional care settings — such as nursing homes — or from jail or prison and who were homeless prior to entering the facility or lack the resources needed to prevent becoming homeless upon returning to the community. See 24 CFR § 576.2.

[35] Will Fischer, Douglas Rice, and Alicia Mazzara, “Research Shows Rental Assistance Reduces Hardship and Provides Platform to Expand Opportunity for Low-Income Families,” Center on Budget and Policy Priorities, December 5, 2019, https://www.cbpp.org/research/housing/research-shows-rental-assistance-reduces-hardship-and-provides-platform-to-expand.

[36] Center on Budget and Policy Priorities, “Three Out of Four Low-Income At-Risk Renters Do Not Receive Federal Rental Assistance,” updated August 2017, https://www.cbpp.org/three-out-of-four-low-income-at-risk-renters-do-not-receive-federal-rental-assistance.

[37] Among households with a voucher, 48 percent are headed by a person identifying as Black, non-Hispanic, 18 percent by a Hispanic person of any race, 3 percent by someone non-Hispanic Asian or Pacific Islander, and 1 percent by someone Native American, non-Hispanic. See Department of Housing and Urban Development, “Picture of Subsidized Households,” 2019, https://www.huduser.gov/portal/datasets/assthsg.html.

[38] Roughly 38 percent of Black, non-Hispanic low-income renter households in need of federal rental assistance receive it, compared to 25 percent of all low-income renter households in need. Regardless of race, funding limitations prevent most renters in need of assistance from getting help. CBPP analysis of HUD custom tabulations of the 2017 American Housing Survey; 2017 HUD administrative data; FY2018 McKinney-Vento Permanent Supportive Housing bed counts; 2017-2018 Housing Opportunities for Persons with AIDS grantee performance profiles; and the USDA FY2018 Multi-Family Fair Housing Occupancy Report.

More from the Authors

Areas of Expertise