Trapped by the Firewall: Policy Changes Are Needed to Improve Health Coverage for Low-Income Workers

The Affordable Care Act (ACA) expanded health coverage to more than 20 million people, principally by improving access to Medicaid and the individual insurance market. While the law put in place new protections for people with employer-sponsored health insurance, it did not dramatically change that market, the major source of health coverage for people under age 65. Employer-sponsored coverage often works well, allowing many people to enroll in comprehensive health benefits using employer contributions that make premiums affordable. But the picture can be quite different for low-income workers.[1]

Frequently, low-income workers get less employer help with their premiums, are offered less robust coverage, and must pay a greater share of their income toward health care costs compared to higher-income workers. And even if an employer’s offer of health coverage is not comprehensive or is unaffordable in practice, it may still disqualify low-income workers and their family members from getting a premium tax credit (PTC) for coverage in the marketplace. This is because the ACA included a “firewall” that makes people with employer-sponsored coverage offers ineligible for PTCs, provided that the employer coverage meets minimum federal standards for affordability and comprehensiveness.[2] But the standards are insufficient, barring many low-income people from enrolling in subsidized marketplace coverage that would be far more affordable and comprehensive.

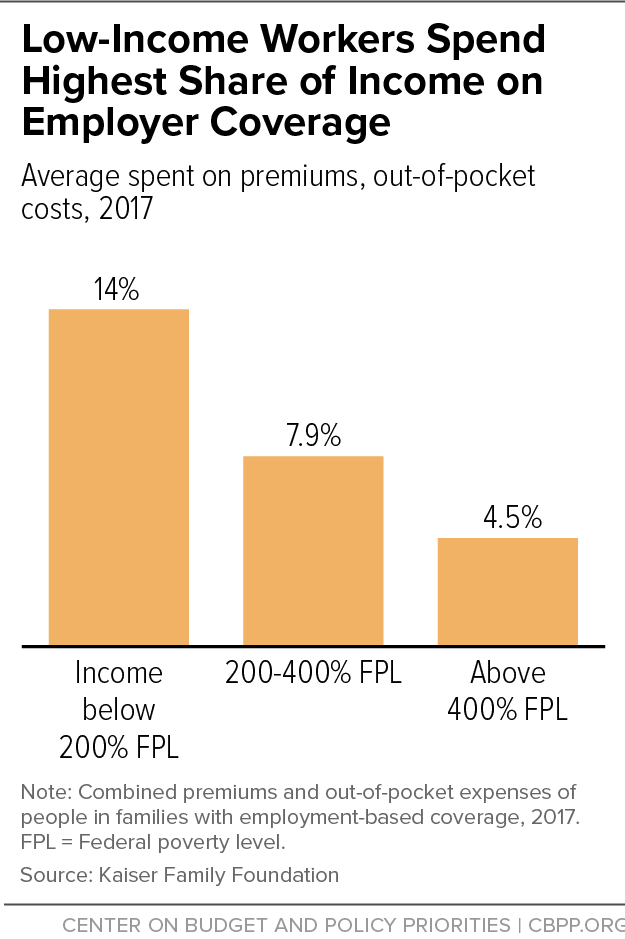

"Low-income workers deserve renewed attention from policymakers to further expand health coverage and make it more affordable for those who have it."Low-income workers deserve renewed attention from policymakers to further expand health coverage and make it more affordable for those who have it. Roughly 2.7 million uninsured people have incomes under 400 percent of the poverty line (the income cut-off for PTCs) but can’t claim the PTCs due to an offer of employer coverage.[3] Millions more enroll in employer plans but struggle to pay premiums or find they have inadequate protection against high out-of-pocket costs. On average, workers with employer coverage with incomes below 200 percent of the poverty line spend 14 percent of income on premiums and out-of-pocket costs, compared to 7.9 percent for those between 200 and 400 percent of the poverty line, and 4.5 percent for those above 400 percent of the poverty line.[4]

Eliminating the ACA firewall would let low-income workers choose their best coverage offer, whether it’s with their employer or at the marketplace with assistance from a PTC. That would reduce costs for workers and decrease the number of uninsured, but it would come at a high budgetary cost.

Short of eliminating the firewall, a range of policies could work around it to make coverage more affordable for workers by making more people eligible for PTCs and increasing awareness of the marketplace enrollment option:

- Fix the “family glitch.” Today an offer of affordable, adequate employee-only coverage disqualifies all family members from PTC eligibility, even when the family premium is very high as a share of income; this is referred to as the “family glitch.” One fix would be to measure family affordability based on the cost of family coverage, rather than the cost of an employee-only plan.

- Raise the standards for employer coverage offers. An employer coverage offer can be considered affordable and comprehensive under federal standards while still imposing high out-of-pocket expenses or covering a skimpy set of benefits. Raising these standards would improve employer coverage or, if the offer doesn’t meet the improved minimum requirements, free more workers to enroll in subsidized marketplace plans.

- Better equip PTC-eligible employees to enroll in marketplace coverage. Employers could do more to facilitate marketplace enrollment of employees who are ineligible for the workplace coverage. They could also be required to provide better upfront information about whether the employer offer is affordable and comprehensive or whether the worker can bypass the employer offer for subsidized coverage in the marketplace.

These options for making coverage more affordable for low-income workers could complement broader strategies for reducing health care costs and improving the quality of employer-sponsored insurance for all workers. Unfortunately, the Trump Administration is moving in the opposite direction, taking actions that will likely increase employees’ costs and exacerbate affordability struggles for those with low incomes.

Low-Income People Face High Costs Even in “Affordable” Employer Coverage

The cost of employer-sponsored insurance has increased steadily in the last several decades and has consistently outpaced workers’ earnings growth, even though premium growth has slowed notably since the ACA’s passage. Between 2000 and 2010, family premiums increased by 114 percent, compared to a 36 percent increase in earnings; between 2010 and 2019, family premiums increased by 49 percent compared to a 23 percent increase in earnings.[5]

Employee premiums for employer-sponsored coverage are particularly burdensome for low-income workers. Employees pay, on average, 18 percent of the premium for single coverage and 30 percent for family coverage.[6] Any given employee premium represents a higher share of income for low-income workers. For example, the average annual dollar amounts that covered workers contribute for family coverage is $6,015. That’s 6 percent of the annual income of someone making $100,000, but it’s 12 percent for someone making $50,000, and 30 percent of the income of someone making $20,000 a year.[7] Compounding this problem, employers with a large share of low-income workers tend to cover a smaller share of the total premium, especially for family coverage. Workers at these firms pay 41 percent of the cost of family coverage, compared to 30 percent at firms overall.[8]

High out-of-pocket costs also create hardships for low-income families.[9] Total out-of-pocket health spending increased by 54 percent and deductibles by 176 percent from 2006 to 2016, according to the Kaiser Family Foundation.[10] Among all firms, covered workers have an average annual deductible of $1,396 for single coverage and more than 1 in 10 workers have a deductible of $3,000 or more.[11] Deductibles are even higher for low-wage workers: $2,679 is more than two months’ earnings for a full-time, federal minimum wage worker. An increasing number of employees with high-deductible plans also have a savings option, such as a health savings account (HSA), to which they or their employer can make tax-deductible contributions, but these accounts are often poorly funded. Nearly half of workers still have an annual deductible greater than $1,000, after including employer contributions to accounts.[12] Front-loaded cost-sharing poses barriers for low-income workers. More than one-third of people with individual deductibles and half of people with family deductibles say they don’t have enough savings to meet their deductibles.[13] High out-of-pocket costs make people more likely to skip filling a prescription, receiving a medical test, or getting needed specialty care, according to the Commonwealth Fund.[14]

All told, low-income workers pay a substantial share of their income toward health costs. Among workers who enroll in employer coverage, people with income below 200 percent of the poverty line spend, on average, 14 percent of their income on premiums and out-of-pocket costs.[15] For comparison, people with income between 200 and 400 percent of poverty spend 7.9 percent of income, and people with income over 400 percent of the poverty line spend only 4.5 percent. (See Figure 1.)

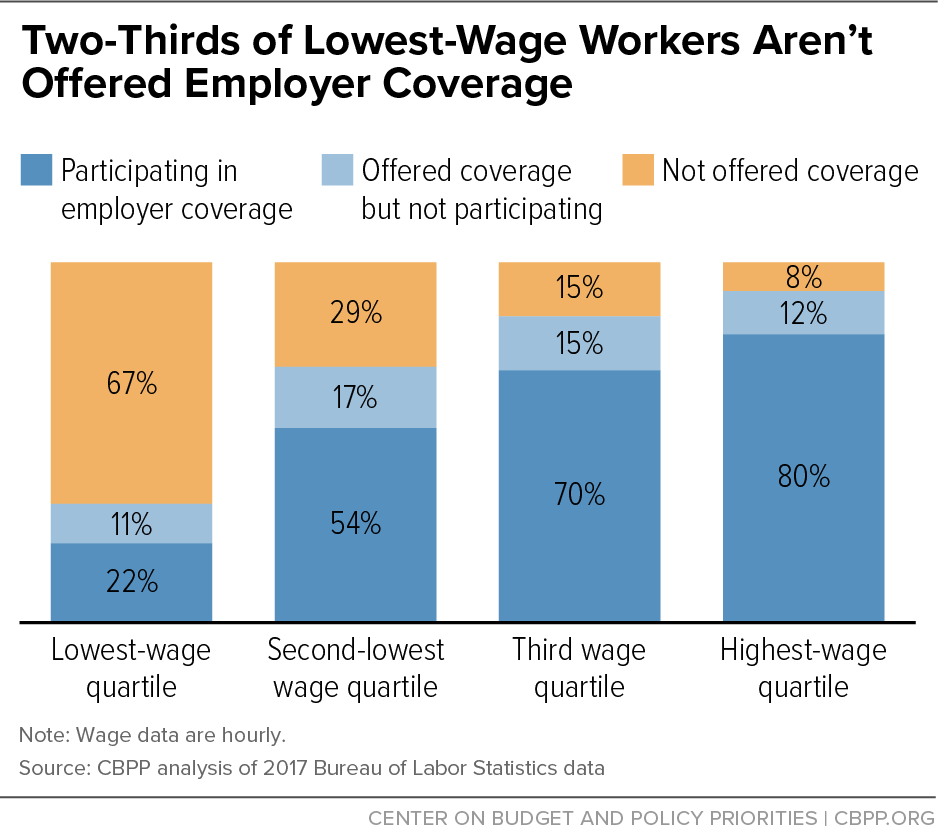

Low insurance offer and take-up rates contribute to striking disparities in employer-sponsored coverage enrollment by income and race. In the lowest quartile of the wage distribution, only about one-third of private sector workers are offered coverage, with 22 percent of them actually participating. This compares to 92 percent of workers in the top wage quartile being offered coverage and 80 percent participating.[16] (See Figure 2.)

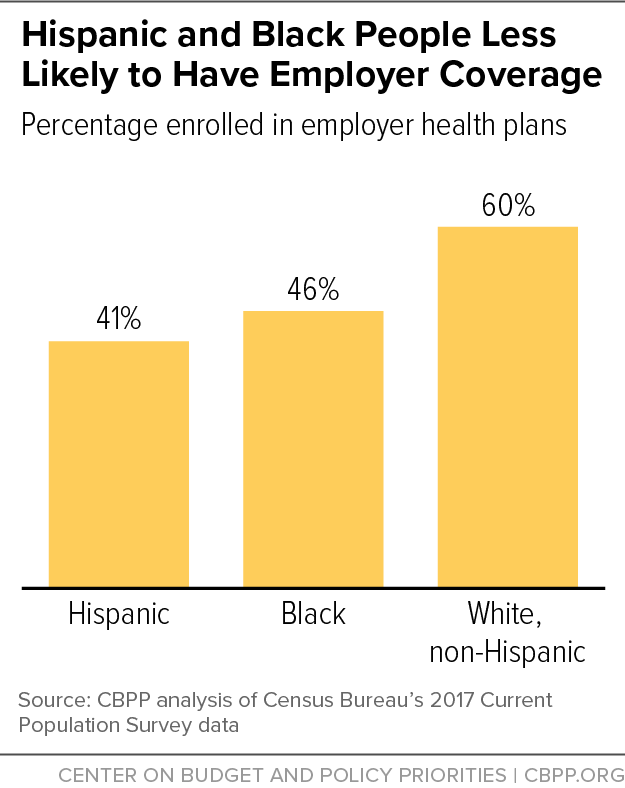

Employer-sponsored coverage is less common among Black and Hispanic people. About 60 percent of non-Hispanic white people have coverage through the workplace compared to 46 percent of Black people and 41 percent of Hispanic people.[17] These groups are less likely to have workplace coverage mainly because they are disproportionately likely to be in lower-income households where employer coverage is less available, but these disparities exist at nearly every income level. (See Figure 3.)

Inadequate Employer Offers Can Make Workers Worse Off

The ACA’s premium tax credits defray premium costs for low- and moderate-income families purchasing coverage in the marketplace, and cost-sharing reductions decrease out-of-pocket spending for people with income below 250 percent of the poverty line. Having an offer of employer-sponsored coverage makes someone ineligible for these subsidies, unless the offer is considered unaffordable or fails to meet a minimum value test. An offer is unaffordable if the lowest-cost plan covering only the employee costs more than about 10 percent of income (9.86 percent in 2019). A plan falls short of minimum value if its “actuarial value” is below 60 percent, meaning that it pays, on average, less than 60 percent of the cost of allowed benefits. If the employer offer is deemed affordable and meets minimum value, the employee is “firewalled” — that is, blocked from receiving marketplace subsidies.

Because of the firewall, having an offer of employer coverage can make a lower-income worker worse off compared to a worker with no offer of coverage at all. A major issue is that the affordability standard is set at a level that requires low-income workers to pay a far greater share of income for an employer plan than people with the same income are expected to pay toward marketplace coverage. A single person making $18,000 a year (about 150 percent of the federal poverty line) could be asked to pay nearly $1,800 toward premiums for an employer-sponsored plan, but in the marketplace, her expected contribution for benchmark coverage would be $750 (4.15 percent of income). This disparity is amplified for families, which often don’t qualify for assistance due to the so-called family glitch. Because of the glitch, if employee-only coverage is deemed affordable, no family member eligible for the employer plan is eligible for a PTC, even if family coverage costs much more than 10 percent of income.

In addition, minimum value is a relatively meager standard. Large employers (with 50 or more full-time workers) aren’t required to cover the package of essential health benefits that plans in the individual or small group markets must cover. Instead, employer plans can meet minimum value if they cover preventive services, physician visits, and hospital inpatient services and meet the 60 percent actuarial value standard. But this can leave some workers, particularly lower-wage ones, with skimpy benefit plans that may not cover needed care. Notably, 60 percent is far lower than the actuarial value of coverage that low-income marketplace enrollees can generally purchase in the marketplaces and translates to sizeable out-of-pocket costs, such as deductibles in excess of $6,000 for single coverage or $12,000 for a family.

These factors create disparities between families with and without employer coverage offers and show why some employees may be better off if they are free to shift to the marketplace. For example:

-

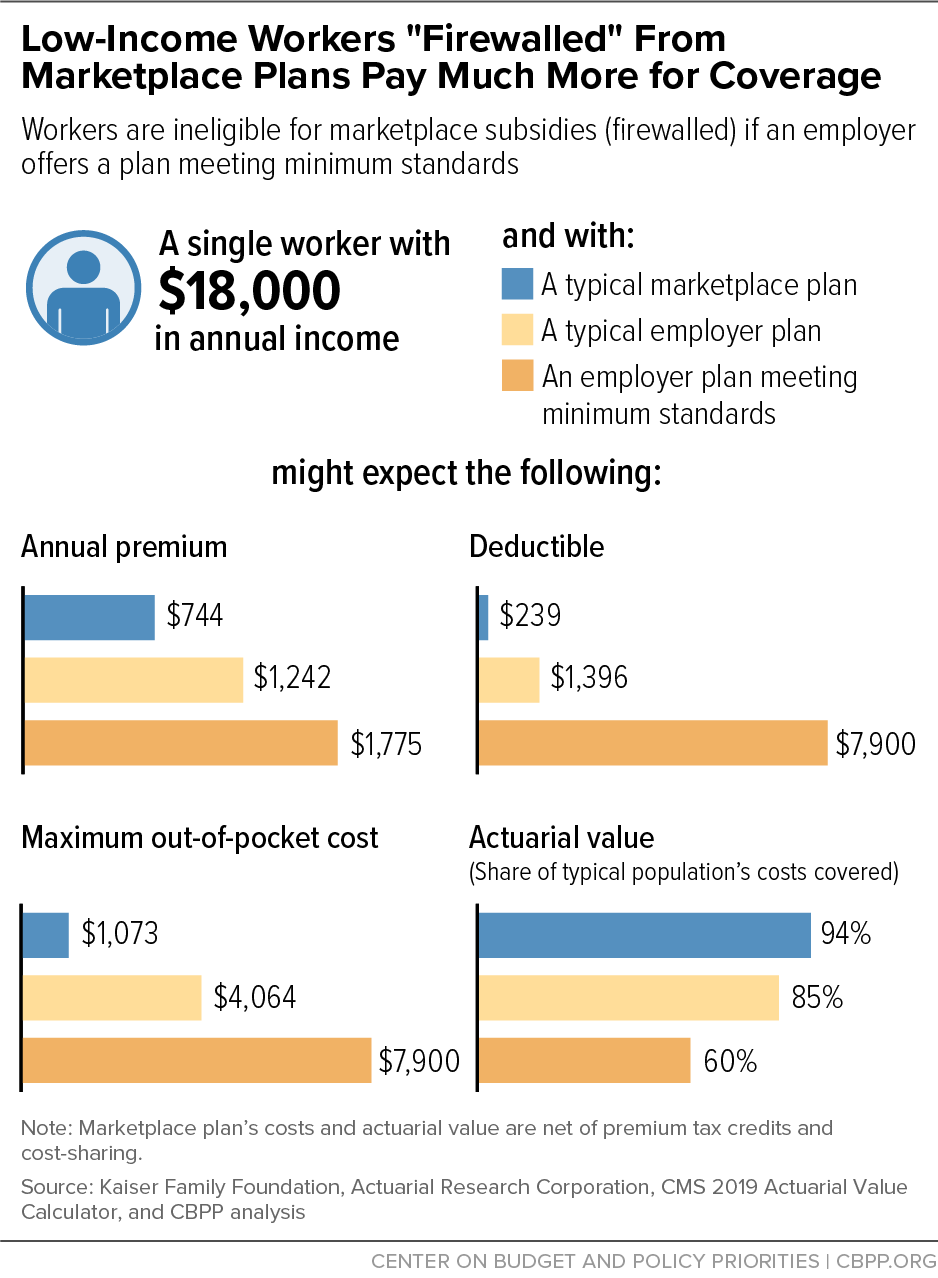

A single person with income of $18,000 (roughly 150 percent of the poverty line) has affordable employer-sponsored coverage if a plan costs less than about $150 per month, whereas in the marketplace, such an enrollee would pay only $62 per month, after a PTC, for benchmark coverage.

In the marketplace, a cost-sharing reduction would raise this consumer’s benchmark plan’s actuarial value to 94 percent. Deductibles for such plans average $239, and maximum out-of-pocket costs average $1,073.[18] That’s more generous than a typical employer plan, which has a lower actuarial value (85 percent),[19] higher average annual deductible ($1,396),[20] and higher maximum out-of-pocket cost ($4,064),[21] and it’s far more generous than a plan meeting the minimum standard of a 60 percent actuarial value. (See Figure 4.)

-

For a family of three with income of $42,000 (about 200 percent of the poverty line), an employer offer would make them ineligible for a PTC if the employee’s premium was less than about $345 per month (9.86 percent of income), even if family coverage cost three to four times that amount.[22] However, without an employer coverage offer, the whole family could get comprehensive benchmark coverage in the marketplace for only $229 per month (6.54 percent of income), net of the PTC.

They’d also be guaranteed a plan with an 87 percent actuarial value in the marketplace, in line with a typical employer plan but much more generous than the 60 percent minimum value requirement.

Eliminating Firewall Would Reduce Disparities But Is Costly

Eliminating the firewall that prevents most people with employer-sponsored coverage offers from PTC eligibility would make an estimated 2.7 million more people ― 9 percent of the total uninsured population ― eligible for affordable coverage.[23] Under this policy, employees would have a choice to enroll in their employer coverage or go to the marketplace. Many employees would likely choose to remain in employer-sponsored coverage, particularly middle- and higher-income workers whose income is too high for the PTC but who benefit substantially from the tax exclusion for employer-sponsored health insurance premiums. Workers who have less generous coverage offers or who are eligible for substantial PTCs would enter the marketplace.

Several groups ― the Center for American Progress, the Urban Institute, and Third Way ― have endorsed some version of eliminating the firewall as part of comprehensive health reform proposals.[24] The key advantage is improving equity across working families. It would give low-income workers access to the same marketplace premium and cost-sharing assistance available to people without employer offers. It could also improve equity across employers that may offer plans with vastly different coverage and out-of-pocket costs, since marketplace coverage would effectively become a new coverage floor.

The downside is cost. Many low- and moderate-income workers, particularly those with families, would move to the marketplace, generating increased federal costs for PTCs and cost-sharing assistance that would substantially exceed the federal savings from the tax exclusion for employer-sponsored coverage. Employers could also take certain measures that could further increase federal costs. First, some employers may encourage sicker or older workers to move to the marketplace, perhaps through design decisions that make their plans less attractive to people with serious health needs or through less subtle steering. Strong non-discrimination provisions would be necessary to prevent this. Second, employers would presumably be motivated to restructure their plans to maximize the benefits of both PTCs and the tax exclusion. That is, they’d probably have less incentive to keep premiums low for low-income workers (as long as they could avoid the penalty) since those workers could just go to the marketplace. Beyond further increasing federal costs, that could also mean that some middle-income people would see higher employee premiums (although employers could increase wages to compensate and employee dissatisfaction could mitigate premium increases).

“Shared Responsibility” Requirement Could Be Improved

The ACA’s “shared responsibility” provision requires large employers (those with more than 50 full-time workers) to offer health insurance coverage to full-time employees and their dependents. A penalty of $2,500 for each full-time worker (in 2019) is triggered if the firm doesn’t offer coverage and any employee gets a PTC in the marketplace. If it offers coverage but the employee-only premium is unaffordable or the plan doesn’t meet minimum value, the penalty is $3,750, but applies only to each full-time worker who receives a PTC. Employers are protected from the penalty by various safe harbors. For example, the employer’s offer is considered affordable if the lowest-cost plan would be affordable for workers with wages at the federal poverty line.

One way to improve the employer shared responsibility penalty would be to disconnect it from employees’ eligibility for PTCs. Under this policy, failure to offer coverage or offering subpar coverage would trigger the penalty, irrespective of workers’ enrollment in marketplace coverage with PTCs. Penalties could be assessed using existing employer reporting of offers and cost of coverage.

Separating the penalty from PTC enrollment would have several advantages. Most significantly, it would eliminate any employer incentive to discourage marketplace enrollment in order to avoid the penalty; indeed, employers could engage in outreach and enrollment without repercussions. Second, it would simplify administration using existing employer reporting versus the current multi-step process of cross-matching employer reporting with employee PTCs. This would also reduce uncertainty among employers about what penalties they will owe since penalties would not be contingent on an employee actions, and it would avoid a potentially lengthy appeals process contesting the eligibility of each specific employee who is awarded a PTC. Finally, disconnecting the penalty from PTC receipt would allow Congress to make decisions about changing the firewall separate from reconsideration of the nature and magnitude of the employer penalty. With this structure, an employer penalty could be maintained in some form while the firewall is eliminated or relaxed and more workers are freed to claim the PTC.

Another option is to eliminate the employer responsibility requirement altogether. But that would be very expensive and would likely come at the expense of much-needed improvements to PTCs and cost-sharing assistance.a It could also result in fewer employers offering coverage or employers offering worse coverage.

a For example, even retroactively suspending the employer mandate for its first four years (2015-2018) would cost $26 billion, according to the Congressional Budget Office. This doesn’t factor in the change in employer behavior that could result from lifting the penalty. “H.R. 4616, Employer Relief Act of 2018,” July 27, 2018, https://www.cbo.gov/system/files/2018-07/hr4616.pdf.

Other Ways to Improve Coverage for Workers

Short of eliminating the firewall, a range of policies could work around it to make coverage more affordable for workers by making more people eligible for the PTC. To the extent a policy change increases PTC eligibility, there would be some degree of crowd-out: a substitution of one type of coverage for another, instead of uninsured people becoming newly covered. But that is balanced by the desirability of giving more affordable coverage to currently insured workers, particularly low-income workers. In addition, one potential benefit of enrolling more people in marketplace coverage is a modest premium reduction in the marketplace, as a result of more healthier people who previously didn’t enroll in employer coverage due to cost joining the risk pool.

Fix the Family Glitch

More than 6 million people live in families that are ineligible for PTCs because they have an employer offer of single coverage that meets the federal affordability standard, even though the cost of family coverage from the employer exceeds the premium threshold, according to the Urban Institute.[25] Legislative or administrative action could allow families with unaffordable coverage offers to get financial help in the marketplace.[26]

One potential fix would allow family members with unaffordable coverage offers to be eligible for PTCs, while the employees themselves remain subject to the firewall. An estimated 3 million people would become eligible for tax credits under this proposal, according to the Urban Institute’s analysis.[27] More than 40 percent of those gaining PTC eligibility would be children. While the majority of people gaining eligibility would be those with income between 200 and 400 percent of poverty, people with income under 138 percent of the poverty line would experience the biggest premium reductions, with the mean family premium for people in this income range falling from 20 percent of income in employer-sponsored coverage to 5.5 percent in the marketplace.[28] People with incomes between 138 and 200 percent of the poverty line would see their premiums cut in half, from 17.6 percent to 8.2 percent of their income. An alternative proposal would be to allow the employee to claim a PTC in the marketplace if family coverage is unaffordable, even if the employee’s single offer is affordable. More than 6 million people would become eligible for PTCs under this option, according to the Urban Institute.

A second analysis concurred that fixing the family glitch would reduce families’ average total health care spending by thousands of dollars and drop their risk of spending at least 20 percent of income on health care by more than two-thirds.[29]

Raise the Standards for Employer Coverage Offers

As explained above, employer-sponsored coverage is considered unaffordable if the employee’s share of the premium for the lowest-cost plan exceeds roughly 10 percent of household income (9.86 percent in 2019). Reducing this threshold could prod more employers to improve coverage affordability or release more workers to seek subsidized marketplace plans if their employers did not meet the new standard. This could increase penalty collections, helping to finance the shift of workers to marketplace coverage with PTCs. Alternatively, Congress could de-link the affordability standard for employees’ PTC eligibility from the affordability standard for the employer penalty. (See box, “‘Shared Responsibility’ Requirement Could Be Improved.”) This would allow more workers (particularly those with low incomes) to enroll in subsidized marketplace plans without necessarily penalizing more employers.

Lowering the affordability threshold would primarily benefit low-income workers, who are more likely to have high premiums relative to income and would be eligible for the most substantial assistance if no longer firewalled. It would also complement congressional proposals to make PTCs more generous for marketplace consumers. For example, legislation by Representatives Richard Neal, Frank Pallone, and Bobby Scott — chairs of the three House committees with jurisdiction over major health care programs — would reduce the maximum share of income a family would pay for subsidized marketplace coverage from the current 9.86 percent to 8.5 percent.[30] The threshold for affordable employer coverage could be reduced to the same amount.

But even if the affordability threshold were reduced to 8.5 percent, a low-income person with an employer plan could pay considerably more for less coverage than someone with the same income who is eligible for a marketplace subsidy. For example, a person with income at 150 percent of the poverty line ($18,210 in 2019) would pay 4.15 percent of their income ($756) for individual or family coverage in the marketplace but up to 8.5 percent of income ($1,548) for single employer-sponsored insurance, which could offer less coverage. Congress could consider setting a lower affordability threshold for lower-income workers (for example, those with incomes below 200 percent of the poverty line), freeing those without truly affordable employer coverage to seek a better deal in the marketplace.

Another way to improve health care affordability for people with offers of job-based coverage would be to increase the share of anticipated health costs that the plan pays for. As explained above, a large-employer or self-insured group plan currently meets the minimum value standard if it covers at least 60 percent of the plan’s total allowed benefit cost, according to an online calculator that the Department of Health and Human Services (HHS) maintains. By contrast, “benchmark” marketplace coverage (the basis for calculating PTCs) covers 70 percent of expected costs, and people with incomes below 250 percent of the poverty line are eligible for cost-sharing assistance that further increases plans’ actuarial values.

One option would be to raise the minimum value standard from 60 percent to 70 percent to align with the marketplace benchmark. Raising the minimum value standard wouldn’t affect most employers since the average employer plan has an actuarial value of 85 percent.[31] While it could lead some employers to pass on premium increases to employees, the increase in the employee premium would be constrained by the affordability standard. Other employers offering low-value plans may drop coverage altogether but, to the extent that employees are eligible for PTCs, this might give more workers and their families access to more affordable and comprehensive coverage in the marketplace.

Another approach would be to define a more robust benefit standard. As noted, the benefit standard set for purposes of minimum value is less than what’s required in the individual or small group markets. When the ACA passed, the assumption was that employer-sponsored coverage at large firms was already sufficiently comprehensive. But as the employer coverage requirement was implemented, it became clear that a small minority of employers were not providing comprehensive coverage. That led the IRS to issue a warning that plans that did not include “substantial coverage” of inpatient hospitalization and physician services do not meet minimum value and employers can’t tell employees the coverage makes them ineligible for PTCs. However, it appears that the onus is on employees to bring non-compliance to the IRS’s attention.[32]

Improvements to the benefit requirements would help vulnerable workers who are offered the barest coverage today. For example, to qualify as minimum value coverage, large and self-insured employers’ health plans could be required to meet their state’s essential health benefit standard ― ten defined categories of items and services ― as individual and small-group coverage must do. An approach to avoid the complexity of employers having to meet a different standard in every state in which they operate is to either create a nationwide benefit standard based on the essential health benefit standard or allow employers to choose to follow one state’s standard, as they do to determine to which services the ACA’s annual and lifetime limits apply. The vast majority of large and self-insured plans exceed these minimum standards, but for employers with plans that don’t, their workers would no longer be firewalled into subpar coverage.

Help Eligible Workers Access Marketplace Subsidies

Some workers and their families aren’t firewalled but don’t realize it. One group often in this situation is workers who aren’t eligible for their employer’s coverage. Employers could be required to do more to connect those workers to the marketplace, and HHS could lower barriers to marketplace enrollment. Another group is workers who are eligible for employer-sponsored coverage but whose coverage is inadequate (i.e., doesn’t meet existing affordability or minimum value standards). Employees need help to determine whether their employer offer disqualifies them from marketplace subsidies or whether the offer falls short and leaves them eligible for more affordable, comprehensive coverage in the marketplace. Reaching out to these groups of PTC-eligible workers may reduce the number of uninsured.

One policy change that might help is to change the structure of the employer responsibility requirement. The current structure ― where an employee claiming the PTC potentially triggers a penalty for the employer ― discourages employers from connecting people to the marketplace. (See box, “‘Shared Responsibility’ Requirement Could Be Improved.”) Other approaches are discussed below.

Reaching Workers Ineligible for Employer-Sponsored Coverage

Even if an employer offers coverage, workers can still be ineligible for a variety of reasons. Large employers are only required to offer coverage of 95 percent of full-time workers, for example, and can exclude part-time employees or employees in certain locations or job classifications.[33] Employers may also establish waiting periods for enrollment in their coverage or use a “measurement period” to delay eligibility for up to a year for new workers who they contend don’t meet full-time status. Other people are eligible for coverage then lose eligibility. Job loss is the most common reason people lose employer coverage, but other workers can become ineligible despite still being employed, such as when their hours are reduced or their position or job location changes.

Employers are well-positioned to identify employees who have not been offered coverage, whose coverage has changed, or who are losing their coverage, and to help them find other sources of insurance. Regardless of an employee’s eligibility for employer-sponsored coverage, federal law requires employers to inform new employees about the marketplace and the PTC.[34] The law could be expanded to direct the Department of Labor (DOL) to require employers to provide this notice at other times, such as during the employer’s annual open enrollment. DOL could also improve the notice so that it provides more useful information. The DOL’s model notice requires an employer to note which classes of employees, if any, are eligible for coverage and to check a box indicating whether the coverage meets minimum value and is intended to be affordable, but questions that are specific to each employee are optional for employers. Employers could instead be required to answer all these questions so that an employee would know with certainty whether they are eligible for employer coverage, the actual cost of that coverage, and if any waiting period applies.

Employers are required to notify people who are losing their employer health benefits that they are eligible to continue with that coverage (typically by paying the full premium) under what’s known as “COBRA,” after the federal law that created it.[35] The DOL model notice for COBRA, which many employers use, contains language about the availability of the marketplace, but the information could be expanded to include: marketplace website and contact information, the availability of enrollment assistance, the availability of financial assistance, examples of how that financial assistance lowers premiums for a family, and the availability of a special enrollment period allowing people losing employer coverage to enroll outside the normal annual open enrollment period. Beyond adding information to the model notice, DOL could require this information in every COBRA notice.

COBRA notices are likely to reach a large portion of the 10 million uninsured people eligible for a special enrollment period due to job loss every year.[36] Providing workers with more information about financial assistance in the marketplace could help people avoid gaps in coverage during employment transitions or unnecessarily paying for COBRA coverage. Connecting people with in-person enrollment assistance could also help people bridge the gap when they lose job-based coverage.

Reaching Workers Who Are Offered Employer-Sponsored Coverage But Not Firewalled

Another group of workers who may be able to seek subsidized marketplace coverage are those who are eligible for employer-sponsored coverage that is unaffordable or fails to meet minimum value, but it’s often difficult for workers to determine on their own whether their employer’s health benefits meet those standards. To remedy this, employers could be required to tell an employee in advance if their coverage offer meets minimum value and how to calculate whether the premium for that plan is affordable. The information would need to be specific to the employee and account for the litany of exceptions and complications that employees are expected to navigate for themselves today.

Without requiring employers to provide such information, coverage offers can be hard for employees to parse. To start, an employee must know whether any plan is “eligible employer-sponsored coverage” — meaning it meets the ACA’s rules as a plan offer — versus a non-qualifying supplemental coverage option, such as fixed indemnity coverage, that offers scant benefits at a lower cost. Employers should have to be transparent about which plans qualify as eligible plans.

Once the employee knows which plan is an eligible employer-sponsored plan, determining whether it meets the minimum value and affordability requirements is similarly complicated. An employee would need to know the minimum value and calculate the affordability of each plan to know if any one plan meets both requirements to disqualify an employee from a PTC. Only then would an employee have the information to make an informed determination about whether the employer’s offer precludes PTC eligibility for themselves and their family.

Minimum value can’t be determined independently by employees; rather, it’s disclosed on an employer-provided summary of benefits and coverage (SBC). Employers are required to make the forms available to workers for each plan they offer, but in practice, many employees don’t know they are entitled to this form or have trouble getting it. Even if they have it, the form is lengthy and the minimum value designation is easily missed. The form also doesn’t spell out the consequences of having an offer that is not minimum value; for example, an employee whose plan’s minimum value is 58 percent isn’t told how to use that information.

The affordability standard requires that a plan cost less than 9.86 percent of income (in 2019), but special rules can make the calculation more than a function of just premium cost. Special tax provisions ― like for wellness plans, health reimbursement arrangements (HRAs), or cafeteria plans ― also affect whether a plan is considered affordable but are not transparent to even an employee who’s very knowledgeable about their benefits.

For example, one staffing company offers three medical plans: “Enhanced MEC,” “Fixed Indemnity,” and “Major Medical.”[37] The Enhanced MEC plan doesn’t cover hospitalization so doesn’t appear to meet the IRS definition of minimum value. The fixed indemnity plan is not eligible employer-sponsored coverage. Only the major medical plan, which is available only to full-time workers, might firewall a worker, so that plan’s minimum value and cost are what matters. The SBC for the major medical plan isn’t readily available so it’s unclear whether the plan meets minimum value. The website tells employees that if they qualify for the major medical plan, they are not eligible for a PTC, but with a premium of more than $1,500 per month, the plan may be unaffordable for many workers, allowing them to access PTCs.

No single required document available to employees at open enrollment captures all these variables, making it hard for employees to know whether they are firewalled or eligible for a marketplace subsidy. A form called the Employer Coverage Tool solicits key information ― including whether the offer has a waiting period, extends to family members, or meets minimum value, and the employee’s share of the premium ― but completing the form is optional for employers.[38] And, crucially, the form doesn’t tell employees how to use premium information to make an affordability determination. Because these forms aren’t required, they are often completed in one-off, and sometimes haphazard, ways. For example, two employees with identical positions going to the same human resources office may get different responses on the Employer Coverage Tool.

Requiring employers to provide reliable, comprehensive information about their health coverage offers in advance of the coverage year would make it possible for workers to determine whether they have an offer that bars them and their families from PTCs. This would help more employees gain access to subsidized coverage in the marketplace if they are eligible for it, while also preventing people from incorrectly claiming federal subsidies and later having to repay a credit they were not eligible to receive. Congressional proposals aimed at simplifying federal reporting requirements for employers include prospective reporting systems. But those proposals would only require general information to be shared with the employee ― information that is insufficient to accurately determine PTC eligibility for an individual employee.[39] Future proposals should instead seek to collect information from employers that is reliable and specific so that the employee can use it to understand whether they are eligible for marketplace subsidies instead. The Employer Coverage Tool could be a useful starting point, if employers were required to complete it and provide it to workers.

Administration Actions Threaten to Raise Costs, Reduce Benefits for Workers

Some low-income workers will likely face increased affordability challenges as a result of recent Trump Administration actions that will increase employees’ costs, reduce their benefits, or make it harder for them to access marketplace coverage when they lose employer coverage.

- Expanding the use of HRAs. A rule from the Departments of Treasury, Labor, and Health and Human Services permits employers to replace traditional group coverage for all or some workers with a dollar contribution that could be combined with individual market coverage. The rule could exacerbate the affordability challenges of low-income workers. If employers that don’t offer coverage begin to do so using an HRA, as the Administration expects, some low-income workers who currently get a PTC could become firewalled by their new coverage offer. Even if those workers use their new HRA offer in the marketplace to enroll in the exact same plan, they’d likely need to pay much more ― as much as 10 percent of income for single coverage versus a sliding-scale expected contribution for family coverage. Having more low-income workers with coverage offers could also exacerbate the problems caused by the family glitch.

- Increasing workers’ out-of-pocket costs. The Centers for Medicare and Medicaid Services finalized a rule that raises the limit on total out-of-pocket costs for many people with employer coverage, meaning families that experience costly illnesses or injuries would face an additional $400 a year in medical bills. The Administration finalized the policy even though, as the final rule itself notes, “all commenters on this topic expressed opposition to or concerns about the proposed change.”[40]

- Requiring verification of job loss to enroll in marketplace coverage. A person can enroll in marketplace coverage outside the annual open enrollment period if they lose qualifying coverage, often because of job loss or a reduction in work hours. The Administration made it more difficult to access this special enrollment period by requiring pre-enrollment verification. Documentation can be difficult for people to produce in a timely way given other urgent concerns people have when they leave a job or experience a significant reduction in income.

- Approving new association health plans (AHPs). The Administration opened a new gateway for employers to form private associations to provide health insurance that is exempt from some consumer protections found in the small group market. For example, AHPs could effectively discriminate based on health conditions by excluding certain essential health benefits required under other plans, like coverage of mental health treatment and prescription medications for costly conditions, since people who need those benefits would not sign up. In addition, an AHP could structure its membership rules and marketing tactics in ways more likely to attract healthier people and groups, while charging far more to others, such as small groups that are made up of women or older people, that work in professions deemed high risk, or that live in areas classified as higher cost. Portions of the rule were struck down in the U.S. District Court for the District of Columbia, but the Administration has appealed.

End Notes

[1] This paper focuses on low-income workers (generally, those with income below 200 percent of the poverty line), but moderate-income workers (those with income within the range for PTCs, up to 400 percent of the poverty line) often face challenges, especially in affording family coverage.

[2] An offer of employer-sponsored coverage does not preclude Medicaid eligibility.

[3] Linda Blumberg et al., “Characteristics of the Remaining Uninsured: An Update,” Urban Institute, July 2018, https://www.urban.org/sites/default/files/publication/98764/2001914-characteristics-of-the-remaining-uninsured-an-update_2.pdf.

[4] Gary Claxton, Bradley Sawyer, and Cynthia Cox, “How Affordability of Health Care Varies by Income Among People With Employer Coverage,” Kaiser Family Foundation, April 14, 2019, https://www.healthsystemtracker.org/brief/how-affordability-of-health-care-varies-by-income-among-people-with-employer-coverage/#item-start.

[5] Kaiser Family Foundation, “2019 Employer Health Benefits Survey,” September 25, 2019, https://www.kff.org/health-costs/report/2019-employer-health-benefits-survey/, and CBPP analysis of Bureau of Labor Statistics data.

[6] Ibid.

[7] Ibid.

[8] Ibid.

[9] Liz Hamel, Cailey Muñana, and Mollyann Brodie, “Kaiser Family Foundation/LA Times Survey Of Adults With Employer-Sponsored Health Insurance,” Kaiser Family Foundation, May 2, 2019, https://www.kff.org/private-insurance/report/kaiser-family-foundation-la-times-survey-of-adults-with-employer-sponsored-insurance/.

[10] Numbers are for people with large-employer coverage. Out-of-pocket expenses and deductibles grew faster than wages (up 29 percent) during this time period. Part of the growth in deductibles is due to employers’ shift away from co-payments, which dropped by 38 percent. Gary Claxton et al., “Increases in Cost-Sharing Payments Continue to Outpace Wage Growth,” Kaiser Family Foundation, June 15, 2018, https://www.healthsystemtracker.org/brief/increases-in-cost-sharing-payments-have-far-outpaced-wage-growth/#item-start.

[11] Kaiser Family Foundation, “2019 Employer Health Benefits Survey.”

[12] Ibid.

[13] PwC, “Medical Cost Trend: Behind the Numbers,” June 2019, https://www.pwc.com/us/en/industries/health-industries/assets/pwc-hri-behind-the-numbers-2020.pdf. In another study, 4 in 10 adults said they could not pay an unexpected expense over $400 with cash on hand. The number is higher for people with a high school degree or less. The numbers are also higher for Black and Hispanic adults at any education level compared to white adults. Federal Reserve, “Report on the Economic Well-Being of U.S. Households in 2018,” May 2019, https://www.federalreserve.gov/publications/files/2018-report-economic-well-being-us-households-201905.pdf.

[14] Sara R. Collins, Herman K. Bhupal, and Michelle M. Doty, “Health Insurance Coverage Eight Years After the ACA: Fewer Uninsured Americans and Shorter Coverage Gaps, But More Underinsured,” Commonwealth Fund, February 7, 2019, https://www.commonwealthfund.org/publications/issue-briefs/2019/feb/health-insurance-coverage-eight-years-after-aca.

[15] Claxton, Sawyer, and Cox.

[16] Bureau of Labor Statistics, “Healthcare Benefits: Access, Participation, and Take-Up Rates,” March 2017, https://www.bls.gov/ncs/ebs/benefits/2017/ownership/private/table09a.htm.

[17] CBPP analysis using the Census Bureau’s 2017 Current Population Survey.

[18] Kaiser Family Foundation, “Cost-Sharing for Plans Offered in the Federal Marketplace for 2019,” December 5, 2018, https://www.kff.org/health-reform/fact-sheet/cost-sharing-for-plans-offered-in-the-federal-marketplace-for-2019/.

[19] Actuarial Research Corporation, “Final Report: Analysis of Actuarial Values and Plan Funding Using Plans from the National Compensation Survey,” Compiled for Office of Policy Research, Employee Benefits Security Administration, Department of Labor, May 12, 2017, https://www.dol.gov/sites/default/files/ebsa/researchers/analysis/health-and-welfare/analysis-of-actuarial-values-and-plan-funding-using-plans-from-the-national-compensation-survey.pdf.

[20] Kaiser Family Foundation, “2019 Employer Health Benefits Survey.”

[21] Ibid.

[22] Figure based on the excess total average premium of $20,576 for employer-sponsored family coverage over the annual premium for coverage meeting the affordability threshold. Kaiser Family Foundation, “2018 Employer Health Benefits Survey.”

[23] Blumberg et al., “Characteristics of the Remaining Uninsured: An Update.”

[24] Center for American Progress, “Medicare Extra for All: A Plan to Guarantee Universal Health Coverage in the United States,” February 2018, https://www.americanprogress.org/issues/healthcare/reports/2018/02/22/447095/medicare-extra-for-all/; Linda J. Blumberg, John Holahan, and Stephen Zuckerman, “The Healthy America Program,” Urban Institute, May 14, 2018, https://www.urban.org/research/publication/healthy-america-program; David Kendall, Jim Kessler, and Gabe Horowitz, “Cost Caps and Coverage for All: How to Make Health Care Universally Affordable,” Third Way, February 19, 2019, https://www.thirdway.org/report/cost-caps-and-coverage-for-all-how-to-make-health-care-universally-affordable.

[25] Matthew Buettgens, Lisa Dubay, and Genevieve M. Kenney, “Marketplace Subsidies: Changing the ‘Family Glitch’ Reduces Family Health Spending But Increases Government Costs,” Health Affairs, July 2016, https://www.healthaffairs.org/doi/10.1377/hlthaff.2015.1491.

[26] While most attention has been paid to a legislative fix, the Trump Administration could address this problem under its existing statutory authority. The Treasury Department under the Obama Administration interpreted 26 U.S.C. 5000A to determine the employee’s “required contribution” for coverage in one way for the firewall (measuring the affordability of family coverage by the cost of individual coverage) but in a different way for determining whether an individual responsibility payment was owed (measuring the affordability of family coverage by the cost of family coverage). The latter interpretation is more reasonable and could be adopted by the current or future administrations.

[27] Ibid.

[28] Adults with income below 138 percent of poverty are eligible for Medicaid in states that expanded Medicaid under the ACA; a person with an offer of employer-sponsored coverage is not barred from Medicaid eligibility. The percentage of income includes the cost of employer-sponsored coverage, after accounting for the tax exclusion, plus the percentage of income the family would contribute toward marketplace coverage.

[29] Sarah A. Nowak, Evan Saltzman, and Amado Cordova, “Alternatives to the ACA’s Affordability Firewall,” RAND Corporation, 2015, https://www.rand.org/pubs/research_reports/RR1296.html.

[30] H.R. 1884, “Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019,” introduced March 26, 2019.

[31] Actuarial Research Corporation.

[32] Internal Revenue Service, “Group Health Plans that Fail to Cover In-Patient Hospitalization Services,” Notice 2014-69, https://www.irs.gov/pub/irs-drop/n-14-69.pdf. The Treasury Department (through the IRS) administers the minimum value rules, as they pertain to a determination of the adequacy of an employer coverage offer and employees’ eligibility for PTCs. This notice can be relied on, but the accompanying IRS regulation was never finalized. HHS did finalize its companion regulation on minimum value requiring “substantial coverage of inpatient hospital services and physician services.” 45 CFR 156.145.

[33] Self-insured plans are subject to IRS rules that prohibit discrimination in favor of highly compensated workers in eligibility or benefits, which somewhat constrains employers’ ability to differentiate between groups of workers. Fully insured plans are not subject to the same non-discrimination rules.

[34] See Model Notice, “New Health Insurance Marketplace Coverage Options and Your Health Coverage,” Department of Labor. For employers that offer coverage: https://www.dol.gov/sites/default/files/ebsa/laws-and-regulations/laws/affordable-care-act/for-employers-and-advisers/model-notice-for-employers-who-offer-a-health-plan-to-some-or-all-employees.pdf. For employers that do not offer coverage: https://www.dol.gov/sites/default/files/ebsa/laws-and-regulations/laws/affordable-care-act/for-employers-and-advisers/model-notice-for-employers-who-do-not-offer-a-health-plan.pdf.

[35] See “Model COBRA Continuation Coverage Election Notice,” Department of Labor, https://www.dol.gov/sites/dolgov/files/EBSA/laws-and-regulations/laws/cobra/model-election-notice.doc.

[36] Matthew Buettgens, Stan Dorn, and Hannah Recht, “More than 10 Million Uninsured Could Obtain Marketplace Coverage through Special Enrollment Periods,” Urban Institute, November 2015, https://www.urban.org/sites/default/files/publication/74561/2000522-More-than-10-Million-Uninsured-Could-Obtain-Marketplace-Coverage-through-Special-Enrollment-Periods.pdf.

[37] See Employer Solutions Staffing Group at www.essghealth.com. Accessed December 2, 2019.

[38] The Employer Coverage Tool can be found here: https://www.healthcare.gov/downloads/employer-coverage-tool.pdf.

[39] Senators Mark Warner and Rob Portman and Representatives Mike Thompson and Adrian Smith introduced S. 2366 and H.R. 4070, the Commonsense Reporting Act of 2019, to establish prospective employer reporting to the Data Services Hub that the marketplace could access at the time of enrollment.

[40] Aviva Aron-Dine and Matt Broaddus, “Changes to Insurance Payment Formulas Would Raise Costs for Millions With Marketplace or Employer Plans,” Center on Budget and Policy Priorities, updated April 26, 2019, https://www.cbpp.org/research/health/change-to-insurance-payment-formulas-would-raise-costs-for-millions-with-marketplace.

More from the Authors