Commentary: ACA “Alternatives” Don’t Protect People With Pre-Existing Conditions

“If the ACA were overturned, it would leave people who have pre-existing conditions vulnerable once again to many of the health and financial risks that existed before the ACA.” With the Affordable Care Act (ACA) again at risk through the suit to strike down the law that is before the Supreme Court, some of its detractors are backing proposals they say would restore popular protections for people with pre-existing conditions if the law is overturned. But maintaining affordable coverage for people with pre-existing conditions would then require a complete set of rules for insurers and standards for benefits — plus financial assistance to make plans affordable for sick and healthy people alike and avoid the risk of an insurance market “death spiral.”

None of the supposed alternatives to the ACA offered by the Trump Administration or congressional Republicans have these features. Some bar insurers from excluding pre-existing conditions from coverage but allow them to design plans that lack the very benefits people with pre-existing conditions need. One would prohibit insurers from charging higher premiums based on health status but allow insurers to deny coverage outright to people who are sick.[1] If the ACA were overturned, such piecemeal approaches would leave people who have pre-existing conditions vulnerable once again to many of the health and financial risks that existed before the ACA, across the individual, small-group, and large-group insurance markets.

Despite Claims, Trump Order, Congressional Proposals Lack Consumer Protections

In late September, President Trump issued an executive order declaring that the “policy” of the United States is to “ensure that Americans with pre-existing conditions can obtain the insurance of their choice at affordable rates.”[2] As has been widely reported, this statement is meaningless and has no legal effect.[3] The same document reiterates the Trump Administration’s true policy: its endorsement of the ACA repeal lawsuit that seeks to overturn the ACA, including its pre-existing condition protections, which is scheduled to be argued before the Supreme Court in November.[4] The Administration also has a four-year track record of trying to dismantle the ACA’s pre-existing condition protections.[5]

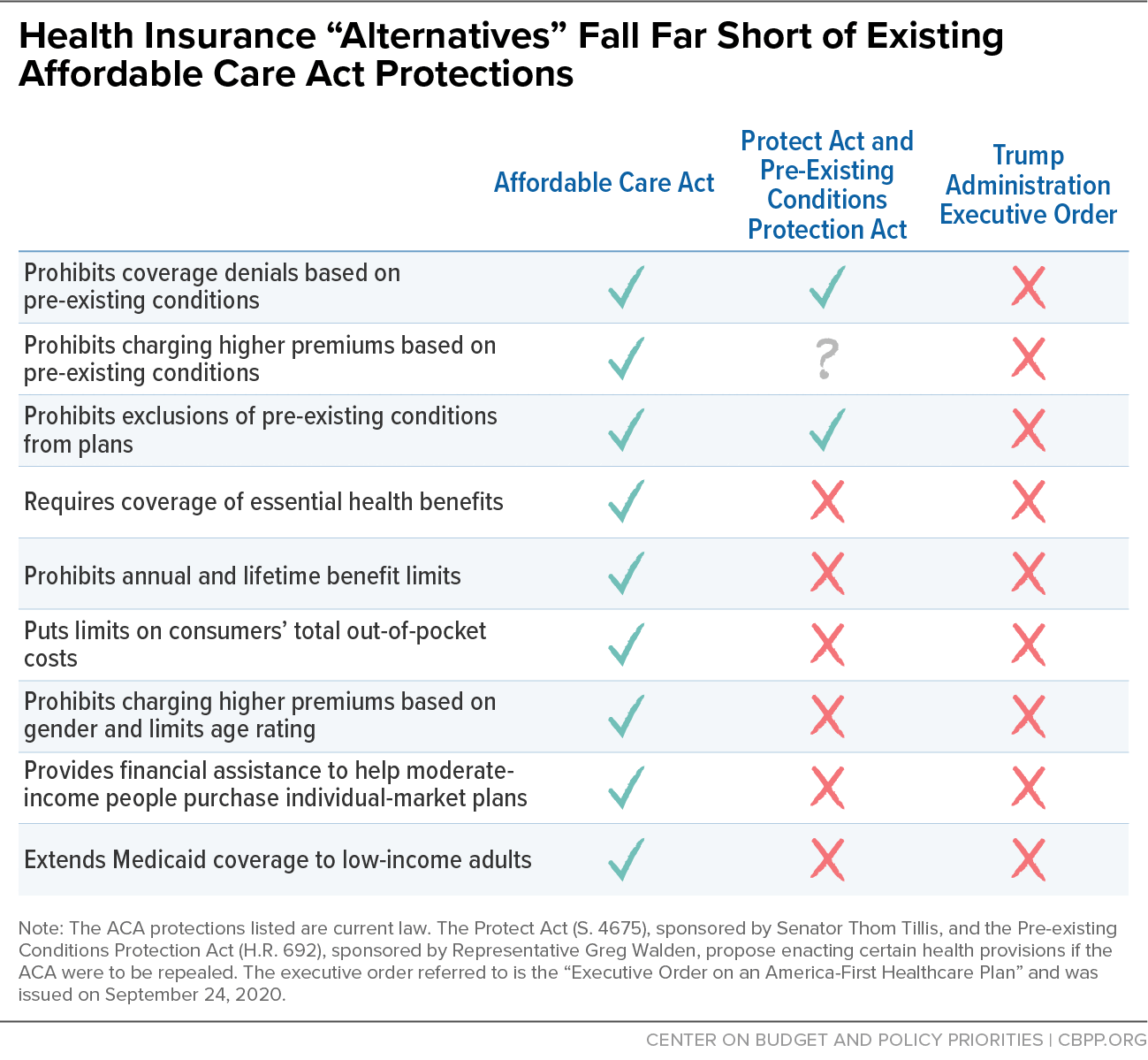

The Senate recently considered the Protect Act,[6] sponsored by Senator Thom Tillis, which would reinstate two ACA pre-existing condition protections but leave many others on the cutting room floor. Rep. Greg Walden introduced a similar bill, the Pre-Existing Conditions Protection Act,[7] in the House last year. (See Figure 1.)

The Protect Act, which failed to advance in the Senate, would reinstate ACA pre-existing conditions protections that prohibit insurers from denying applicants based on pre-existing conditions and from excluding pre-existing conditions from coverage. The bill language is unclear on a third protection, the ACA’s prohibition on charging higher premiums due to a person’s health status.[8] The bill’s sponsors did not adopt the ACA’s unambiguous approach, which spells out a limited set of factors that insurers can use to set premiums and bars the use of any other factors. Instead, the Protect Act would let insurers charge higher premiums based on age and gender (which the ACA limits and prohibits, respectively) and might let them set prices based on other proxies for health status as well.

Meanwhile, the Protect Act lacks many other ACA protections and would let insurers:

- exclude coverage of essential health benefits — such as maternity coverage, mental health care, and substance use treatment — as many plans did before the ACA;[9]

- impose annual and lifetime limits on how much they will pay out (in large employer plans as well as individual-market and small business coverage); and

- sell plans with no limit on how much enrollees could owe in out-of-pocket costs if they got sick (another change that would affect large employer plans as well as the individual and small-group markets).

So insurers couldn’t refuse a plan to someone with pre-existing conditions or carve out their pre-existing conditions from coverage. But they could sell plans that exclude high-cost drugs, cancer treatment, or maternity coverage. And they could impose annual limits on what plans will pay out — whether on all health services or health services for specific conditions — that would make them useless to people with expensive health conditions.

Under this approach, a person who has cancer technically could buy a plan that does not exclude coverage of cancer. However, their benefits could run out because the insurer imposes an annual or lifetime limit, or the plan might not cover the prescription medicines that treat the cancer. Likewise, someone with a substance use disorder would be eligible to buy a plan, and the plan could not exclude the pre-existing condition outright. But insurers would not have to cover substance use disorder treatment or any other essential health benefit a person might need.

Once the door is opened to a resurgence of pre-ACA tactics, it would drive a race to the bottom among insurers. That’s because, once exclusions for pre-existing conditions, annual benefit limits, or benefit carveouts are allowed, the economic logic driving insurers to adopt these tactics would be overwhelming. For example, suppose an insurer was considering covering HIV medications. With no requirement for insurers to cover these medications, it would fear being the only company to do so and attracting all applicants in that area who have HIV. Insurers would choose not to cover these drugs, to impose sharp limits on them, or to cover them only through an expensive add-on “rider” that would be priced based on the assumption that everyone who would buy it needs the medications. Prior to the ACA, this occurred in the individual market for many benefits, including maternity coverage and mental health services.[10]

Overturning the ACA would most directly affect individual and small-group coverage. (States could put in place pre-existing condition provisions for these markets, but before the ACA, almost none put in place comprehensive protections; moreover, states would not have the authority or the resources to fully address all the gaps.[11]) But striking down the law would impact people with large employer plans too. The ACA barred employer plans from imposing waiting periods for benefits that last longer than three months and required these plans to cap the yearly amount enrollees must pay in out-of-pocket costs, including deductibles.[12] Prior to 2010, tens of millions of people had large-group health plans with lifetime or annual limits, and almost 20 percent of workers with large-group plans didn’t have a cap on total out-of-pocket costs.[13]

Proposals Pose Other Risks to People With Pre-Existing Conditions

Apart from the holes these bills leave in the ACA’s insurance consumer protections, they pose other significant problems for people with pre-existing conditions.

First, none of them would replace the ACA’s premium tax credits, which would disappear if the law were struck down. Eliminating the ACA’s financial assistance would put coverage out of reach for millions of low- and moderate-income consumers, including many with pre-existing conditions. It also would create severe adverse selection in state insurance markets, since it would remove a major financial incentive for healthy people to enroll in plans that pool risk across people with and without serious health needs.

The Congressional Budget Office (CBO) predicted that trying to maintain the ACA’s consumer protections while eliminating its subsidies for individual-market coverage would cause the individual market to collapse in much of the country and cause premiums to spike sharply elsewhere.[14] CBO based its projections partly on the pre-ACA experiences of states that prohibited discrimination based on pre-existing conditions but did not provide financial assistance. These states often had very high individual-market premiums, which put coverage out of reach for most of their residents.[15]

Second, these bills would not replace the ACA’s Medicaid expansion for low-income adults. While Medicaid expansion isn’t usually listed among the bill’s protections for people with pre-existing conditions, it should be. In a Michigan survey of adults enrolled through expansion, about 70 percent had a pre-existing condition, such as diabetes, hypertension, or depression.[16] With 13 million people covered through expansion, that suggests millions of people with pre-existing conditions would become uninsured if the ACA were thrown out. Research shows that expansion has been especially important for people with serious health needs, enabling them to obtain regular care,[17] giving them access to medications for their conditions,[18] and saving lives.[19]

It’s not surprising that the bills purporting to reinstate pre-existing condition protections have lots of holes. Before the ACA lawsuit put the law at risk, congressional Republicans — backed by the Trump Administration — repeatedly proposed legislation that would gut the ACA’s protections for people with pre-existing conditions. This includes the American Health Care Act, a repeal bill[20] the House passed in 2017, and a bill proposed by Senators Bill Cassidy and Lindsay Graham (“Cassidy-Graham”) that would have let states opt out of most pre-existing condition protections.[21] The Better Care Reconciliation Act, another 2017 repeal bill[22] that was narrowly blocked in the Senate, would have let states opt out of benefit standards. All of these bills would also have decimated the ACA’s Medicaid expansion and financial assistance. The Administration also incorporated the Cassidy-Graham approach in its fiscal year 2019 and 2020 budgets.

The good news is that the ACA remains the law of the land, and the arguments in favor of overturning it are extremely weak.[23] People with pre-existing conditions, as well as people who are healthy now but get sick in the future, can obtain a plan with comprehensive benefits and strong financial protections regardless of their health status. Let’s hope it stays that way.

End Notes

[1] Julie Appleby, “Cory Gardner’s Bill Has As Much to Do with Politics as Pre-Existing Conditions,” Kaiser Health News and PolitiFact HealthCheck, September 18, 2020, https://khn.org/news/cory-gardners-bill-has-as-much-to-do-with-politics-as-preexisting-conditions/.

[2] United States, Executive Office of the President [Donald Trump], “Executive Order on an America-First Healthcare Plan,” September 24, 2020, https://www.whitehouse.gov/presidential-actions/executive-order-america-first-healthcare-plan/.

[3] Susannah Luthi and Rachel Roubein, “Trump makes fresh health care push, saying he’ll protect sick Americans,” Politico, September 24, 2020, https://www.politico.com/news/2020/09/24/trump-health-executive-orders-billing-421383; and Caitlin Owens, “Trump’s latest empty health care rhetoric on pre-existing conditions,” Axios, September 25, 2020, https://www.axios.com/trump-pre-existing-conditions-executive-order-45e86c69-a620-42d4-a3d6-e952d9040e4d.html.

[4] The executive order states, “I have agreed with the States challenging the ACA, who have won in the Federal district court and court of appeals, that the ACA, as amended, exceeds the power of the Congress. The ACA was flawed from its inception and should be struck down.” For more, see “Suit Challenging ACA Legally Suspect But Threatens Loss of Coverage for Millions,” CBPP, updated August 21, 2020, https://www.cbpp.org/research/health/suit-challenging-aca-legally-suspect-but-threatens-loss-of-coverage-for-tens-of.

[5] Aviva Aron-Dine, “Trump’s Health Care Plan Would Do Much the Same Damage as His Effort to Repeal ACA Through the Courts,” CBPP, July 8, 2019, https://www.cbpp.org/blog/trumps-health-care-plan-would-do-much-the-same-damage-as-his-effort-to-repeal-the-aca-through; and “Trump Administration’s Repeal Suit Stance Is In Line With Its Health Care Agenda,” CBPP, updated February 21, 2020, https://www.cbpp.org/research/health/trump-administrations-aca-repeal-suit-stance-is-in-line-with-its-health-care-agenda.

[6] Protect Act, S. 4675, https://www.congress.gov/bill/116th-congress/senate-bill/4675/text.

[7] Pre-existing Conditions Protection Act of 2019, H.R.692, https://www.congress.gov/bill/116th-congress/house-bill/692/text.

[8] Katie Keith, “What It Means to Cover Preexisting Conditions,” Health Affairs, September 11, 2020, https://www.healthaffairs.org/do/10.1377/hblog20200910.609967/full/.

[9] Kaiser Family Foundation, “Analysis: Before ACA Benefits Rules, Care for Maternity, Mental Health, Substance Abuse Most Often Uncovered by Non-Group Health Plans,” June 14, 2017, https://www.kff.org/health-reform/press-release/analysis-before-aca-benefits-rules-care-for-maternity-mental-health-substance-abuse-most-often-uncovered-by-non-group-health-plans/.

[10] Ibid.

[11] Aviva Aron-Dine, “States Can’t Protect Themselves From Harmful Effects of ACA Repeal,” CBPP, January 10, 2020, https://www.cbpp.org/blog/states-cant-protect-themselves-from-harmful-effects-of-aca-repeal.

[12] Kaiser Family Foundation, “Potential Impact of California v. Texas Decision on Key Provisions of the Affordable Care Act,” September 22, 2020, https://www.kff.org/health-reform/issue-brief/potential-impact-of-california-v-texas-decision-on-key-provisions-of-the-affordable-care-act/#grouphealthplans.

[13] Thomas D. Musco and Benjamin D. Sommers, “Under the Affordable Care Act, 105 Million Americans No Longer Face Lifetime Limits On Health Benefits,” ASPE, March 2012, https://aspe.hhs.gov/basic-report/under-affordable-care-act-105-million-americans-no-longer-face-lifetime-limits-health-benefits; and Loren Adler and Paul Ginsburg, “Health Insurance as Assurance: the Importance of Keeping the ACA’s Limits on Enrollee Health Costs,” Brookings Institution, January 17, 2017, https://www.brookings.edu/blog/usc-brookings-schaeffer-on-health-policy/2017/01/17/health-insurance-as-assurance-the-importance-of-keeping-the-acas-limits-on-enrollee-health-costs/.

[14] Congressional Budget Office, “How Repealing Portions of the Affordable Care Act Would Affect Health Insurance Coverage and Premiums,” January 2017, https://www.cbo.gov/sites/default/files/115th-congress-2017-2018/reports/52371-coverageandpremiums.pdf.

[15] Price Waterhouse Coopers, LLC, “Challenges of partial reform – Lessons from State Efforts to Reform the Individual and Small Group Market Before the Affordable Care Act,” February 2017, https://www.chcf.org/wp-content/uploads/2017/12/PDF-ChallengesStateReformBeforeACA.pdf; Harris Meyer, “ACA repeal without replacement could spur insurer exodus,” Modern Healthcare, November 19, 2016, https://www.modernhealthcare.com/article/20161119/MAGAZINE/161119891/aca-repeal-without-replacement-could-spur-insurer-exodus; and Christopher Koller, “Why Republican health reform ideas are likely to fail,” Politico, December 7, 2016, https://www.politico.com/agenda/story/2016/12/republican-health-reform-ideas-obamacare-unlikely-work-000252/.

[16] Jesse Cross-Call, “Michigan Medicaid Proposal Would Lead to Large Coverage Losses, Harm Low-Income Workers,” CBPP, April 19, 2018, https://www.cbpp.org/research/health/michigan-medicaid-proposal-would-lead-to-large-coverage-losses-harm-low-income.

[17] Benjamin D. Sommers et al., “Three-Year Impacts Of The Affordable Care Act: Improved Medical Care And Health Among Low-Income Adults,” Health Affairs, Vol. 36, No. 6, June 2017, https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2017.0293.

[18] Ausmita Ghosh, Kosali Simon, and Benjamin D. Sommers, “The Effect of Health Insurance on Prescription Drug Use Among Low-Income Adults: Evidence from Recent Medicaid Expansions,” Journal of Health Economics, Vol. 63, November 6, 2018, https://www.sciencedirect.com/science/article/abs/pii/S0167629617300206.

[19] Sarah Miller, Norman Johnson, and Laura R. Wherry, “Medicaid and Mortality: New Evidence from Linked Survey and Administrative Data,” National Bureau of Economic Research Working Paper No. 26081, updated August 2020, https://www.nber.org/papers/w26081?sy=081.

[20] Jacob Leibenluft, “CBO Analysis Refutes Ryan Claims that House Health Bill Maintains Protections for Pre-Existing Conditions,” CBPP, May 26, 2017, https://www.cbpp.org/research/health/cbo-analysis-refutes-ryan-claims-that-house-health-bill-maintains-protections-for.

[21] Aviva Aron-Dine, “Cassidy-Graham’s Waiver Authority Would Gut Protections for People with Pre-Existing Conditions,” CBPP, September 15, 2017, https://www.cbpp.org/blog/cassidy-grahams-waiver-authority-would-gut-protections-for-people-with-pre-existing-conditions.

[22] Edwin Park, “New CBO Estimate: Still 22 Million More Uninsured Under Revised Senate Republican Health Bill,” CBPP, July 20, 2017, https://www.cbpp.org/research/health/new-cbo-estimate-still-22-million-more-uninsured-under-revised-senate-republican.

[23] Tara Straw and Aviva Aron-Dine, “ACA Repeal Even More Dangerous During Pandemic and Economic Crisis,” CBPP, October 5, 2020, https://www.cbpp.org/health/commentary-aca-repeal-even-more-dangerous-during-pandemic-and-economic-crisis.

More from the Authors