Alaskans Could Suffer the Most Harm Under the House Republican Health Plan

The House Republican health care plan would impose on Alaska the nation’s largest cut in premium tax credits, a five-fold increase in state costs for new enrollees if Alaska wanted to maintain its Medicaid expansion, and the elimination of key health benefits for Alaska Natives. While the plan would seriously harm all states, Alaska would face a “perfect storm” of detrimental effects that would gut its Medicaid program, destabilize its individual health insurance market, and widen disparities in health coverage. In short, Alaskans would likely lose more under the House plan than residents of any other state.

Harmful Effects Would Ripple Across Alaska’s Insurance Market

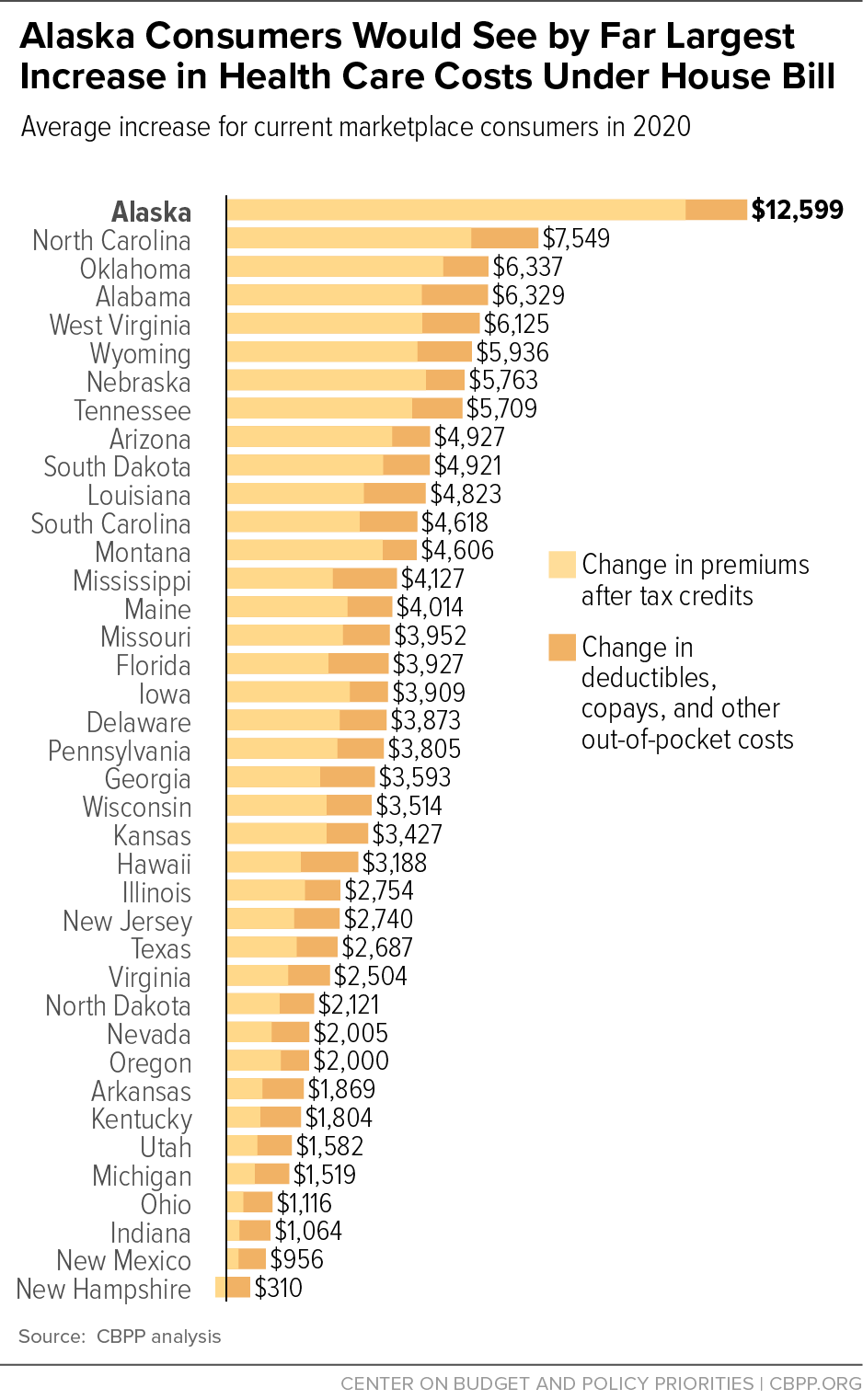

Alaskans would face by far the largest cut in tax credits — and largest increase in total out-of-pocket health care costs — in the nation. The House bill sharply reduces tax credits that help people pay individual-market premiums. Alaska would see by far the nation’s largest reduction in tax credits, averaging $10,500 (nearly 80 percent) for current marketplace consumers in 2020.

These large cuts reflect the fact that the House bill’s tax credits, unlike the Affordable Care Act’s (ACA) premium tax credits that Alaskans receive today, do not adjust for geographic variation in premiums. Alaska has by far the highest individual (as well as employer) market premiums of any state, so it benefits disproportionately from the ACA’s geographic adjustment. As a result, Alaskans would lose almost twice as much from the House plan’s changes to tax credits as people in any other state — or almost five times the nationwide average for HealthCare.gov consumers.

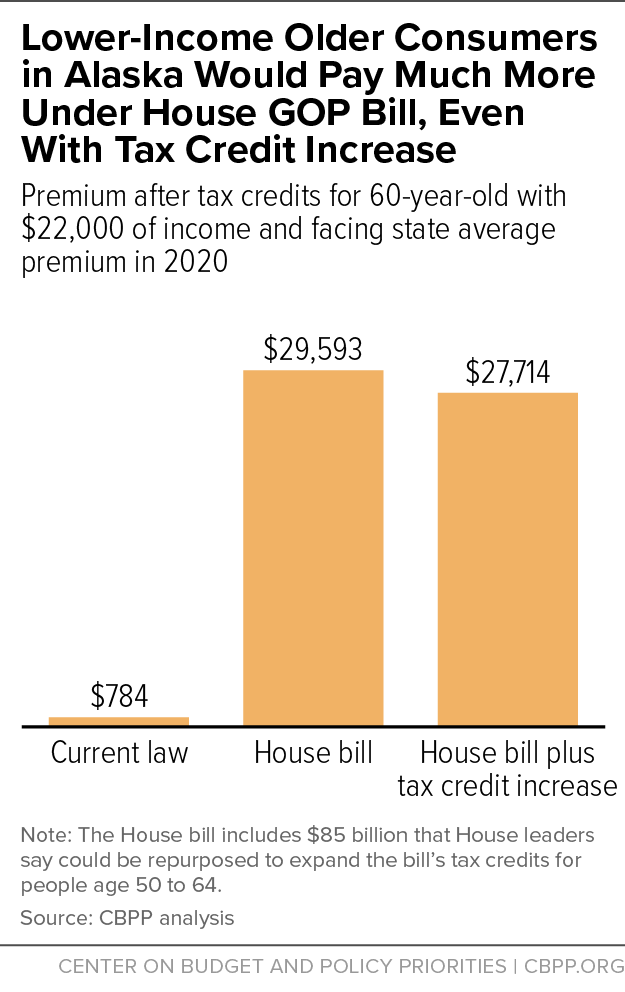

The cuts to tax credits, along with other changes in the House bill, would be even harsher for lower-income and older Alaskans. For example, a 60-year-old Alaska consumer with income of $22,000 would see her tax credit fall by $23,100. Her premiums (before accounting for her tax credit) would rise significantly, primarily because the House bill would let insurers charge older consumers much higher premiums than they can today. As a result, her net premium — that is, her premium after her tax credit — would skyrocket from roughly $800 today (4 percent of income) to $29,600, or far above her total income.

The House bill would also increase out-of-pocket costs for Alaska consumers. It repeals and does not replace the ACA’s cost-sharing reductions, which reduce or eliminate deductibles and other out-of-pocket costs for people with low and moderate incomes. In addition, the Congressional Budget Office (CBO) projects that the bill would lead to increases in deductibles and other out-of-pocket costs across the board, because it would effectively allow insurers to stop offering lower-deductible plans.[1] These changes would increase out-of-pocket costs by an average of about $1,500 for Alaska marketplace consumers. Total costs for Alaska marketplace consumers — taking into account tax credits, out-of-pocket costs, and CBO’s estimates of changes in pre-tax-credit premiums under the House bill — would increase by $12,600, on average. [2] (See Figure 1.)

While House Republican leaders have suggested they would be open to modestly increasing tax credits for older people, the changes under discussion would barely reduce the bill’s cost increases for Alaska consumers. When they modified their legislation March 20, House Republicans added a provision costing roughly $85 billion and suggested those resources could be repurposed for larger tax credits for older consumers. But even if the $85 billion were repurposed to pay for higher tax credits for people age 50 and older, total costs for Alaska marketplace consumers would still increase by an average of $12,000, or 95 percent as much as without the tax credit increase. And the 60-year-old Alaskan cited above would still see her net premiums jump to $27,700, more than her total income. (See Figure 2.)

The individual health insurance market would be destabilized. Given these enormous cuts, and the resulting cost to consumers of maintaining coverage, Alaska’s individual market would almost certainly see large coverage losses, even before taking into account the bill’s destabilizing impact on the market. And that impact could be severe.

CBO concluded that the House bill’s subsidies and its new Patient and State Stability Fund would keep the individual market stable in “most areas.” But that may not be true in Alaska. Instead, large cuts in tax credits and the elimination of cost-sharing subsidies, coupled with repeal of the individual mandate, threaten to destabilize Alaska’s already fragile individual market.

CBO predicted that an ACA repeal bill that President Obama vetoed last year, which eliminated the ACA’s tax credits with no replacement, would cause the individual market to disappear in three-quarters of the country: with neither a mandate nor subsidies to draw healthy people into the risk pool, markets in most of the country would fall into a “death spiral” of ever-rising premiums and falling enrollment. But for Alaska, the House bill isn’t very different than that earlier bill. It cuts subsidies for current marketplace participants by four-fifths in 2020 and even more over time. And it repeals the individual mandate immediately, damaging the individual-market risk pool. That would put substantial upward pressure on premiums next year and discourage insurers from participating in Alaska’s market.

The House bill would also prevent Alaska from receiving federal matching funds for its reinsurance program after 2019. Last year, recognizing the unique challenges facing their state, Alaska policymakers created a two-year reinsurance program to lower premiums in the individual market by having the state pick up part of the costs of covering high-cost patients. The reinsurance funds are a main reason why Premera, the only insurer participating in Alaska’s marketplace, lowered its expected premium increase for 2017 in Alaska, and the program would likely encourage insurers to participate in Alaska’s market going forward.

Under the ACA, Alaska’s reinsurance program could qualify for federal matching funds through a so-called “1332 waiver.”[3] That’s because, by lowering premiums, it is projected to lower the cost of federal premium tax credits, saving the federal government roughly $55 million in 2020 under current law, according to Alaska’s waiver application.[4] Those savings could offset the federal matching funds, fulfilling the requirement that 1332 waivers not increase the federal deficit. In December 2016, Alaska submitted a 1332 waiver proposal seeking federal matching funds beginning in 2018 in order to sustain its reinsurance program.[5] In February the Trump Administration indicated to Alaska policymakers that it will look favorably upon the application.[6] And Secretary of Health and Human Services Tom Price cited Alaska’s reinsurance program in a recent letter to governors as a model for how states can use 1332 waivers.[7]

But even if the application is approved, it would not be possible to continue the arrangement in 2020 or beyond under the House Republican plan. That’s because the bill delinks tax credits from local premiums: lowering premiums would no longer lower federal costs because tax credits would be the same whether premiums were higher or lower. Alaska would get some funding from the House Bill’s Patient and State Stability Fund that it could use for reinsurance (though less than its 1332 waiver application is seeking for years after 2019).[8] But it couldn’t leverage its state-funded program to secure additional federal help to address its unique needs and counteract the premium increases and destabilization to its market resulting from the House bill.[9]

Medicaid Cuts Would Undermine Expansion, Force Other Program Cuts

Under the House plan, states would continue to get the enhanced federal matching rate of 90 percent for people enrolled in Medicaid expansion coverage before 2020, but would get the regular match rate — which for Alaska is 50 percent — for each new person who joins the program starting in 2020. This means each new enrollee would cost Alaska five times as much as people enrolled before 2020. Because most adult Medicaid enrollees use the program for relatively short periods, the lower matching rate would apply to most expansion enrollees within a few years. This would soon make the expansion prohibitively expensive for Alaska to maintain, especially when coupled with other Medicaid cuts in the House bill.

Taking into account both the reduced match for expansion and the cap on per-beneficiary federal Medicaid funding (discussed below), the House plan would shift $1 billion in Medicaid costs to Alaska over ten years, the Urban Institute estimates. Federal Medicaid dollars coming into the state would shrink by 11 percent, compared to current law.[10] Given Alaska’s persistent budget difficulties in the face of declining oil revenues — the state faces a nearly $3 billion deficit for next fiscal year and the legislature is contemplating using some of the earnings from its Permanent Fund to fund government — it’s highly unlikely that Alaska could find the state dollars necessary to offset the large federal cut.

Thus, the state very likely would have to eliminate the expansion, which provides coverage to 30,000 Alaskans[11] and is a key reason why Alaska’s uninsured rate among adults dropped from 18.9 percent in 2013 to 11.7 percent in 2016.[12]

In addition to cutting Medicaid expansion funding, the House bill would place a per-person cap on federal funding for Medicaid as a whole. The cap would apply to all Alaskans on Medicaid, including the 10,000 seniors, 74,000 children, and 17,000 people with disabilities enrolled today. The proposal is designed to substantially cut federal Medicaid spending, with the cuts growing each year, by increasing the per-beneficiary cap at a lower rate each year than currently projected growth in per-enrollee costs. These cuts would be deepest precisely when need is greatest, since federal Medicaid funding would no longer increase automatically when public health emergencies like opioids or a natural disaster increase state costs.

Alaska Natives Would Be Especially Hard Hit

In 2014, before Alaska implemented the Medicaid expansion, 37 percent of non-elderly Alaska Natives were uninsured, second only to South Dakota for the highest uninsured rate among American Indians and Alaska Natives.[13] The ACA’s Medicaid expansion has enabled Alaska to provide many more Alaska Natives with coverage. Today, while Alaska Natives make up 15 percent of the state’s residents, they constitute nearly 40 percent of its Medicaid enrollees.[14]

Alaska Natives with Medicaid can use their coverage to get care at Indian Health Services (IHS) and tribal operated facilities or with other providers who take Medicaid. Medicaid also pays the full cost for travel to such facilities, which is a critical benefit for rural Alaskans. The millions of new federal dollars brought into Alaska through the Medicaid expansion have helped tribal facilities improve care and offer more services. Ending the expansion, as the House bill would almost certainly force Alaska to do, would disproportionately harm Alaska Natives.

The House bill would harm Alaska Natives who get coverage through the marketplace as well. Not only would it dramatically reduce the size of the tax credits people receive, but its repeal of the ACA cost-sharing reductions would be especially burdensome for Alaska Natives because they qualify for more assistance than other consumers with similar incomes. (In particular, many Alaska Natives qualify for cost-sharing reductions that reduce their deductibles and other out-of-pocket costs to zero.) Alaska is second only to Oklahoma in the percentage of its marketplace enrollees who are American Indian or Alaska Native and qualify for this enhanced assistance. Further, Alaska Natives receive the largest average annual cost-sharing reduction in the country among American Indians and Alaskan Natives: $426 per month, or almost twice as large as those in the next state, Wyoming.[15] Under the House bill, they would lose this assistance and instead face deductibles of thousands of dollars.[16]

End Notes

[1] Congressional Budget Office, “American Health Care Act,” March 9, 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/americanhealthcareact.pdf.

[2] For a description of the methodology behind these estimates, see Aviva Aron-Dine and Tara Straw, “House GOP Health Bill Still Cuts Tax Credits, Raises Costs by Thousands of Dollars for Millions of People,” Center on Budget and Policy Priorities, March 22, 2017, https://www.cbpp.org/research/health/house-gop-health-bill-still-cuts-tax-credits-raises-costs-by-thousands-of-dollars.

[3] For more information about Section 1332 waivers, see Jessica Schubel and Sarah Lueck, “Understanding the Affordable Care Act’s State Innovation (‘1332’) Waivers,” Center on Budget and Policy Priorities, February 5, 2015, https://www.cbpp.org/research/understanding-the-affordable-care-acts-state-innovation-1332-waivers.

[4] “Alaska 1332 Waiver Application,” State of Alaska, Department of Commerce, Community, and Economic Development, Division of Insurance, December 30, 2016, https://www.commerce.alaska.gov/web/Portals/11/Pub/Alaska-1332-Waiver-Application-with-Attachments-Appendices.pdf?ver=2017-01-05-112938-193.

[5] Alaska proposed a five-year waiver from 2018 through 2022, with an option to renew for an additional five years.

[6] Andrew Kitchenman, “Alaska sees positive federal signals on individual insurance market,” Alaska Public Radio Network, February 23, 2017, http://www.alaskapublic.org/2017/02/23/alaska-sees-positive-federal-signals-on-individual-insurance-market/.

[7] “Offering states flexibility to increase market stability and affordable choices,” U.S. Department of Health and Human Services, March 13, 2017, https://www.hhs.gov/about/news/2017/03/13/offering-states-flexibility-increase-market-stability-and-affordable-choices.html.

[8] Alaska’s waiver application estimates federal savings of about $180 million for 2020 to 2022 (see Table 8). Oliver Wyman’s estimates that Alaska’s allocation from the Patient and State Stability Fund would be $53 million in 2018, and total national funding for the fund would fall to roughly $35 million starting in 2020 because the House bill’s allocation for Patient and State Stability Fund Grants falls by a third after 2019.by a third after 2019. The Oliver Wyman estimates are available at http://health.oliverwyman.com/content/dam/oliver-wyman/blog/hls/featured-images/March2017/StatbyStateTable.pdf.

[9] Even taking into account the House Bill’s Patient and State Stability Fund, CBO’s estimates imply that premiums for current marketplace consumers would rise nationwide under the House bill; increases would if anything be larger in Alaska, for the reasons discussed in the main text. See Matthew Fiedler and Loren Adler, “How will the House GOP health care bill affect individual market premiums?,” The Brookings Institution, March 16, 2017, https://www.brookings.edu/blog/up-front/2017/03/16/how-will-the-house-gop-health-care-bill-affect-individual-market-premiums/.

[10] John Holahan et al., “The Impact of Per Capita Caps on Federal and State Medicaid Spending,” Urban Institute, March 21, 2017, http://www.rwjf.org/content/dam/farm/reports/issue_briefs/2017/rwjf436077.

[11] Alaska Department of Health and Social Services, http://dhss.alaska.gov/HealthyAlaska/Pages/dashboard.aspx. Data as of February 28, 2017.

[12] “Kentucky, Arkansas Post Largest Drops in Uninsured Rates,” Gallup-Healthways Well-Being Index, February 8, 2017, http://www.gallup.com/poll/203501/kentucky-arkansas-post-largest-drops-uninsured-rates.aspx.

[13] Samantha Artiga and Anthony Damico, “Medicaid and American Indiana and Alaska Natives,” Kaiser Family Foundation, March 2016, http://files.kff.org/attachment/issue-brief-medicaid-and-american-indians-and-alaska-natives.

[14] Alaska Department of Health and Social Services, http://dhss.alaska.gov/Commissioner/Pages/TribalHealth/medicaid.aspx.

[15] “Health Insurance Marketplace Cost Sharing Reduction Subsidies by Zip Code and County 2016,” US Department of Health and Human Services, https://aspe.hhs.gov/health-insurance-marketplace-cost-sharing-reduction-subsidies-zip-code-and-county-2016.

[16] For more information on what is at stake for Alaska Natives in the House bill, see “How the House Repeal Bill Would Harm Alaska Natives,” Families USA, March 14, 2017, http://familiesusa.org/product/how-house-repeal-bill-would-harm-alaska-natives.

More from the Authors

Areas of Expertise