Extracting Lessons for State Finances

What Other States Should Learn from Energy-Producing States’ Revenue Woes

Every state confronts unexpected revenue declines that lead to budget problems; states that rely heavily on revenues from oil, natural gas, and other fossil fuels know this particularly well. The fiscal actions that energy-producing states took — and things they didn’t do — provide lessons for lawmakers on preserving money for schools, health care, roads, and much more in bad times and good.

The fiscal actions that energy-producing states took — and things they didn’t do — provide lessons for other statesToday, despite the improving economy, many states are facing fiscal stress. In half the states revenue collections are below the amount expected to be collected when budgets were adopted.[1] And reports are beginning to come in of projected shortfalls next year.[2]

These budget difficulties are nothing new for the states that rely heavily on revenues from oil, natural gas, and other fossil fuels. Since oil prices dropped in 2014, these states — Alaska, Louisiana, New Mexico, North Dakota, Oklahoma, Texas, West Virginia, and Wyoming — have confronted financial crises that put at risk the public investments communities need to thrive.

The experiences of the energy-producing states demonstrate how better fiscal policy decisions would help lawmakers preserve and invest in the services that underpin their economies and quality of life. Extracting lessons from these states, others would be wise to:

- Avoid ineffective tax cuts and incentives that deplete revenues. Large tax cuts for wealthy people and profitable corporations, or tax breaks to incentivize business decisions, reduce dollars that states have to invest in thriving communities, and often for little or no payoff. In some states that draw heavily upon energy sector revenues, tax cuts pose as big of a problem, if not bigger, than falling energy prices. For example, the plunge in energy prices in states like Louisiana, Oklahoma, and West Virginia, would present a much less serious problem had lawmakers not made deep cuts to taxes or given out large tax breaks in recent years.

- Build up budget reserves to protect public investment and strengthen the economy. All state tax revenues have economic ups and downs but energy sector-reliant revenues are particularly volatile.[3] Energy states have found that adequate and accessible reserves are critical to surviving the boom and bust nature of the industry. During their energy sector boom times, many states have created trust funds, whose proceeds can be used to strengthen and diversify a state’s economy over the long run.[4] Other states don’t have this option available, but they can set aside tax revenues when their economies are growing to help sustain investments in slower times. Having reserves is particularly important for states that rely on taxation of capital gains, for example, which are subject to highs and lows.

- Diversify revenue sources to stabilize tax collections. A good mix of revenues helps to protect public investment in schools, roads, and other critical services by mediating the ups and downs of tax collections. For example, income and sales taxes are other revenue sources many states rely on. Alaska and Wyoming both lack an income tax — and Alaska also lacks a broad-based sales tax — leaving these states heavily reliant on energy-related revenues in a jam. Both saw steep declines in revenue in 2016 as a result of price drops. Oil prices, for example, are down 70 percent since June 2014. All states can benefit from a diverse revenue mix that includes sales and excise taxes and income taxes.

Energy Price Drops, Fiscal Policy Choices — Both Fuel State Woes

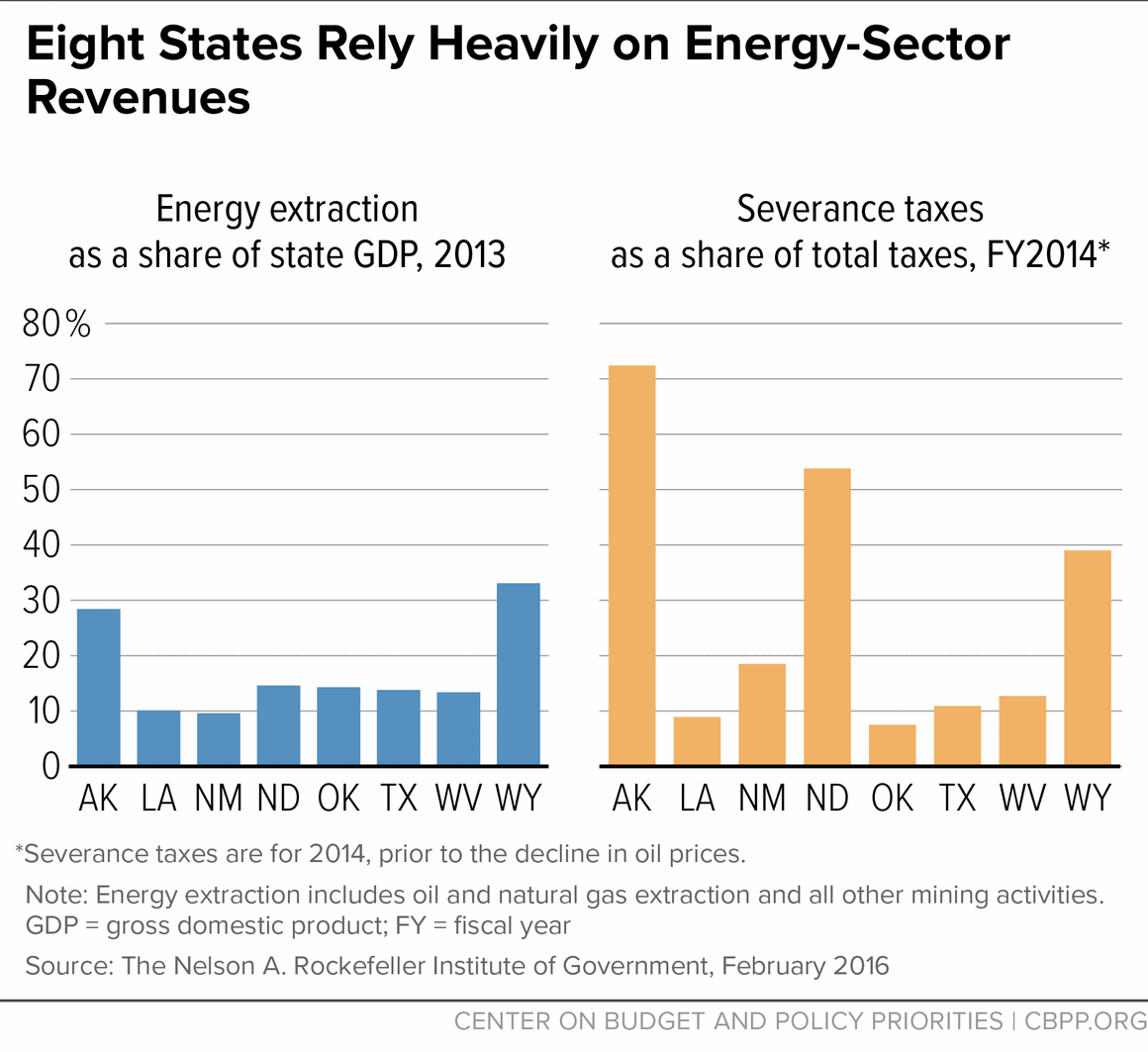

Alaska, Louisiana, New Mexico, North Dakota, Oklahoma, Texas, West Virginia, and Wyoming were the states most dependent on revenues from the taxation of the production, processing, and sale of oil, coal, and gas in 2014, before the full impact of falling oil prices hit.[5] These states tend to be heavily reliant on severance taxes — taxes levied on the extraction and use of natural products such as oil, natural gas, or coal. Severance taxes made up more, in some cases much more, than 7 percent of total taxes that year in these states. (See Figure 1.)

Severance taxes respond to factors outside of economic growth. That means they can add stability in bad economic times, but can create big drops in revenue in good economic times.

Six of these eight states — Alaska, Louisiana, North Dakota, Oklahoma, West Virginia, and Wyoming — grappled with large budget shortfalls during the 2016 legislative season when prices for oil, coal, natural gas, and other sources hit dramatic lows. While energy prices are no doubt having an impact on revenues in these six states, short-sighted fiscal policy decisions have exacerbated and sometimes directly fueled their woes. The remaining two energy states — New Mexico and Texas — also have seen severance tax revenues underperform, but with less severe results.

The states that rely heavily on severance tax revenue can take steps to ensure their long-term fiscal health, and, therefore, the health of public investments like schools, higher education, infrastructure, and more. And all states can learn from the energy-reliant states, and better prepare for the impact of future economic downturns by relying on diverse sources of revenue and using better budget practices.

Avoid Expensive but Ineffective Tax Cuts and Incentives

States’ economic development rhetoric often centers on tax cuts, despite growing evidence that they are a poor strategy for creating jobs and growth, and an even poorer strategy for creating broadly shared economic prosperity. Maintaining and improving schools, transportation networks, and other public services shown to boost the economy in the long term requires having reliable resources that grow as service costs increase. When states choose large, across-the-board tax cuts for higher-income households and profitable corporations, they end up skimping on public investment. This can set the state up for future budget problems.

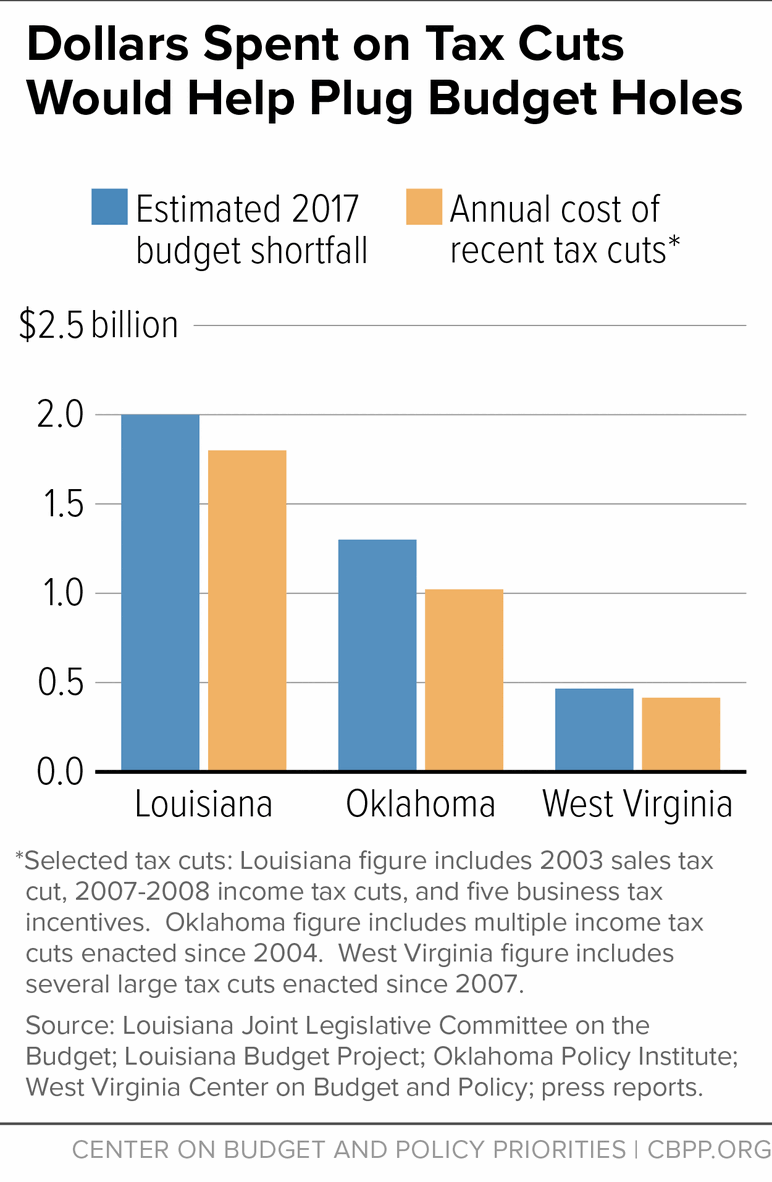

A cautionary tale has played out dramatically in fossil fuel-producing states. For example, in three states that rely heavily on severance tax revenues, large tax cuts and tax breaks nearly equal or exceed the budget shortfalls those states faced as the full impact of the energy price decline hit their revenues. (See Figure 2.) In other words, tax cuts — not energy prices — first fueled their fiscal woes. For example:

-

Louisiana lawmakers struggled to fill a budget shortfall that reached $2 billion, or over 20 percent of the general fund, as they crafted the 2017 budget.[6] Meeting in two special sessions plus a regular session, legislators addressed the gap with a mix of revenue increases and budget cuts. The biggest tax changes, including a 1-cent increase in the state sales tax, are temporary.[7] Lawmakers will be faced with tough choices about which of the state’s core responsibilities to fund in upcoming years. Already, Louisiana is facing a series of mid-year shortfalls. Last year, the state closed a $313 million shortfall that remained from the 2016 budget with a relatively small ($11.9 million) cut to higher education and by delaying payments to health care providers. The higher education cuts come on top of reductions in per-student higher education spending of 42 percent since 2008. These reductions caused in-state tuition to rise and are more severe than in all other states except Arizona and Illinois.[8]

The state’s continued reliance on short-term fixes simply kicks the can down the road. Louisiana now must address a projected $340 million shortfall in the 2017 budget as well as an estimated $1.5 billion gap when the temporary tax increases expire in 2018.[9] Closing these gaps solely with spending cuts would likely diminish the state’s future and cause harmful reductions in services to families. For example, if last year’s proposals resurface, there could be cuts to Louisiana’s primary college scholarship program that would result in 34,000 fewer students receiving aid.[10] Another proposal would close two medical schools and nine hospitals that care for the poor and uninsured, and terminate programs that serve people with disabilities.[11]

Louisiana made poor, avoidable fiscal policy decisions well before the recent energy bust. In 2007 and 2008, lawmakers repealed income tax increases they had enacted earlier in the decade to offset a sales tax cut that’s still in effect. The revenue impact of rolling back the income tax provisions now sets the state back about $800 million a year.[12] In addition, the state has pursued a wide range of tax incentives and tax breaks for energy companies and other businesses. The cost of several of these tax breaks has ballooned over time. For example, five tax subsidies — ones for the film industry, business inventory, fracking, solar and wind power, and the state enterprise zone — saw their combined cost rise from about $200 million in 2003 to over $1 billion in 2013.[13]

In addition, exempting new horizontal drilling wells from taxes for the first 24 months of operation — a period when the wells are particularly lucrative — cost the state over $1 billion from 2010 to 2014.[14]

-

Oklahoma faced a massive $1.3 billion shortfall for the 2017 fiscal year, about 20 percent of the budget.[15] This shortfall was closed by a combination of revenue increases and deep cuts in the state budget. The revenue increases totaled close to $900 million,[16] but about $560 million of that will not recur next year, leaving a large gap in the 2018 budget. In addition, some of the revenue came from slashing by more than 70 percent a tax credit that boosts the incomes of 330,000 working families, a decision that will likely diminish the future productivity of the children in those families.[17] The budget cuts were also painful. For example, the state reduced its support for higher education by nearly 16 percent.

Despite these difficult cuts and tax increases, Oklahoma’s budget problems continue. Production taxes on oil and gas are projected to come in $290 million lower in fiscal year 2017 than five years prior — equivalent to 68 percent. Falling energy prices are having an impact on income and sales tax collections as well. The state faces a projected $868 million shortfall in 2018.[18] The recent decline in oil and gas revenues is adding salt to these wounds. However, much like in Louisiana, years of short-sighted income tax cuts paved the way for the current crisis.[19] State lawmakers have cut the top income tax rate from 6.65 percent to 5.0 percent, which now costs the state over $1 billion annually.[20] At the same time, tax breaks adopted since the mid-2000s for the oil and gas industry cost the state $350 million in 2017.[21]

-

West Virginia’s projected shortfall for 2018 has reached $400 million, the equivalent of nearly 10 percent of the budget, according to the state’s revenue secretary.[22] Continuing to cut its way to a balanced budget as West Virginia has done in recent years will put pressure on education, public safety, and roads and bridges in the state. Universities, for example, could take a hit and be forced to raise tuition, which has gone up 42 percent since 2008.[23]

Again, energy prices are playing a role. Severance tax revenues from natural resource extraction came in almost 50 percent (or $245 million) lower than expected in 2017 and have not recovered yet. Still, the state would be in a much stronger financial position if it had not been cutting other taxes since the late 2000s. It phased out the business franchise tax, eliminated the grocery tax, cut corporate income taxes, and enacted new tax breaks for businesses — at a combined cost of $425 million a year, far more than the drop in severance tax collections.[24]

Each of these states can reverse course on recent tax cuts and tax breaks to raise the revenues needed to invest in services that build thriving communities. The real-life experience of states and the research show that tax cuts are a poor strategy for economic growth.[25] In contrast, raising revenues allows for economy-boosting investments without damaging jobs or the economy.[26]

The continuing budget problems of the energy states resulting from tax cuts should give other states pause. For example, Kansas, Mississippi, and North Carolina have deeply cut income taxes for individuals and businesses without replacing the lost revenues. This, over time, will force harmful cuts in services like schools, transportation, and public safety.

Build Up Reserves to Protect Public Investment and Strengthen the Economy

Severance taxes provide substantial revenues to states with oil, gas, coal, and other energy-related natural resources. But these revenues are as limited and as fluctuating as the finite, market-priced resources being taxed. To survive the boom and bust cycles, states need to have adequate and accessible reserves. These can boost efforts to strengthen and diversify a state’s economy for the long term.

Energy-producing states often maintain two types of reserves — “permanent” trusts and rainy day funds.

A permanent trust fund built with energy-related revenues, such as a share of the proceeds from taxing natural resources, will often support ongoing investments and promote economic development and diversification, even after natural resources dry up. Alaska, New Mexico, North Dakota, Texas, and Wyoming all have severance tax trusts of over $1 billion. Alaska’s Permanent Fund provides annual cash dividends to state residents, which help them address the state’s high cost of living (although lawmakers are considering changes to this system). Texas’ Permanent University Fund helps to finance higher education. A portion of Wyoming’s Permanent Fund pays for college scholarships. New Mexico diverts a certain percentage of its trust fund to its general fund each year.

The principal, as opposed to the interest generated from it, of these permanent funds is closely guarded. While spending the interest generated by the trust funds’ holding is governed by the regular appropriations process, there are stiff rules governing when the principal can be withdrawn. In most states with these types of trust funds, a vote of the people is required to draw down the principal. Establishing a permanent fund to hold big infusions of boom-time revenue or the initial proceeds from taxes or industry payments that result from mineral wealth serves another purpose as well: it prevents the state from building its ongoing budget on revenues that are one-time in nature.

While most states are unlikely to receive revenue bursts of the magnitude that boom times can bring to energy-producing states, many do experience significant ups and downs in tax collections. For example, the dot.com boom of the early 2000s and the run-up of the stock market in advance of the Great Recession brought large growth in income tax revenues to states that tax capital gains.

All states can extract lessons for their finances from energy- and technology-producing states that have experienced both booms and busts. A key takeaway: Reserve revenues from the high-growth times for new one-time investments or future economic downturns. For example, both Massachusetts and California deposit “extraordinary” capital gains revenue into a rainy day fund.

Rainy day funds are sensible tools to help states weather economic downturns and other shocks that lead to reduced resources for public investments. In addition to the permanent trust funds, the energy states, like the vast majority of states, attempt to maintain a sufficient balance in rainy day reserve funds, which are more easily accessible than trust fund balances.

In hard times, policymakers can tap rainy day funds to protect public services that residents rely on such as schools, higher education, and programs for the elderly and disabled. This shoring up of resources helps to maintain economic activity and prevent the destabilization of communities and families.

But not all rainy day funds are well-designed. The problems with the rainy day funds of energy states are common to many states. A number are too small — four of the eight states (Louisiana, North Dakota, Texas, and West Virginia) cap their rainy day fund’s size below 15 percent of their budget.[27] A rainy day fund of 15 percent would be adequate for the typical state to weather a relatively short and moderate recession without major tax increases or spending cuts.[28] In addition, six of the eight states only deposit year-end budget balances, when and if they’re available, rather than scheduling deposits of a specified amount at the start of the budget year when certain conditions are met.

-

North Dakota, a state which has both a rainy day fund and a trust fund, has room for improvement, for example. North Dakota’s rainy day fund is insufficient to help the state fully weather large revenue shocks, and its permanent trust fund is not well-designed. The rainy day fund relies on year-end balances and is capped at 9.5 percent of the state’s general fund budget. That means that lawmakers were restricted from maximizing the benefits of windfall revenue growth they experienced prior to the drop in energy prices.

When the boom cycle went bust in 2015, general fund revenues were $1.07 billion or nearly 20 percent short of the current biennial budget target. This was largely due to a $743 million dollar decline in sales tax collections, which make up over half of general fund revenues and are impacted substantially by changes in energy prices.[29] Lawmakers also recently adopted a series of personal and corporate income tax cuts as well as a buy down of local property tax rates that cost around $400 million, exacerbating the problem.[30] To resolve the massive shortfall, the governor ordered 4 percent cuts to all state agencies, drained the state’s ending balance, and drew down $500 million from the state’s rainy day fund (called the budget stabilization fund) to bring the budget into balance. This left the state with a projected rainy day fund balance of zero and vulnerable to a downturn in the immediate term.

There are a number of steps states including North Dakota can take to improve their rainy day funds. [31] They can remove the caps on their rainy day funds and build up reserves that equal 15 percent or more of the state budget. For example, states could instead make deposits when economic growth is expected to be above average in addition to when the budget ends in surplus — the current practice in most states. They also should avoid limits on how much of the fund can be withdrawn during a given year and allow lawmakers to approve withdrawals from the fund with a simple majority vote. Limits and supermajorities are barriers to using rainy day funds for their intended purposes — filling in when unexpected revenue shortfalls or spending increases develop mid-budget.

Diversify Revenue Sources to Improve Fiscal Security

Since oil prices have fallen, budgets in Alaska and Wyoming have bled red, providing a warning to other states to diversify revenue sources rather than rely too heavily on a single tax. These states’ near-exclusive reliance on severance tax revenues to pay for core services like schools and health care put both in jeopardy, even as the national economy was growing.

Levying different types of taxes can provide security when they have different responses to the ups and downs of an economy. Some taxes may react more slowly to the economy and either help delay a drop in revenues in an economic downturn or quicken recovery from a dip. And some rise or fall based on factors other than economic growth. For example, severance tax collections depend on oil prices, which can be a buffer to states if prices are high when the economy is declining. That means severance taxes can add stability in bad times. It also means that an overreliance on severance taxes can cause fiscal crises even as the national economy is growing. For example:

-

As recently as 2014, Alaska’s energy revenues accounted for 72 percent of all state revenues, a level of dependence driven in large part by the repeal of the state’s income tax in 1980 as well as the lack of a broad based sales tax. As oil prices plummeted, revenue from oil declined by 81 percent from 2012 to 2015[32] leaving the state in dire straits. The governor and legislature have failed to close the resulting budget gaps, which have grown to an estimated $2.65 billion in 2018. Last year, proposals to close the gap included deep cuts to state agencies.[33] The state considered eliminating two early education programs, hundreds of layoffs within the University of Alaska system, and a 20 percent reduction in a state nursing program that would have left some communities without a public health provider, among other things.[34]

To reduce cuts to state-supported health and education, the governor has proposed a dramatic plan that would change the way the state uses its severance tax revenues, reduce Permanent Fund dividend payments to Alaskans, and create a new, but modest state income tax in future years. On the whole, this plan would hit low-income households hardest, but it also would improve the state’s revenue diversity.[35] For now Alaska has relied on withdrawals from the state’s Constitutional Budget Reserve fund to balance the budget. Debate of the governor’s proposals will continue this year.

-

Wyoming does not levy an income tax, though the state does have a sales tax. While it may have a somewhat better mix of revenue sources than some other energy-producing states, it is still heavily reliant on revenues from energy sources. The drop in energy prices has weakened the state’s ability to fund core services. For example, falling energy sector revenues had a substantial impact on the state’s general fund budget, which are projected to drop by $550 million — a 14 percent decline — from the last budget cycle to the current one.[36] In addition, the state relies heavily on federal mineral royalties to fund its K-12 schools and due to the decline in energy prices, the state’s school fund (separate from the general fund) faces a $644 million shortfall in the current budget cycle, or about 30 percent of that fund.[37]

Even when a sector fuels much of the state economy — as it did for decades in Alaska and Wyoming — it shouldn’t be responsible for covering most of the state budget. Having income, sales, and severance taxes helps to mediate those fluctuations and stabilize revenue collections. All states can benefit from a diverse revenue mix that includes relatively stable sources such as sales and excise taxes as well as relatively fast-growing sources such as income taxes. Including an income tax in the mix of taxes is somewhat like having a balanced portfolio of investments. That portfolio would ordinarily include some riskier components that have the potential for more growth over the long term, such as stocks. Similarly, state personal income taxes are subject to wider swings up and down, but over the long term grow more than other state taxes.[38] The relatively strong growth of the income tax revenue allows states to deliver public services at a level adequate to meet the needs of state residents and the challenges of an ever-evolving economy, even as revenue from sales taxes and other sources grows more slowly than needed.

Conclusion

The long-run health of any state economy depends on its ability to maintain core investments in K-12 schools and higher education, roads and infrastructure, health, public safety, and other services that boost the well-being of residents. These investments require reliable revenues. States counting on volatile energy-sector revenues are particularly aware of how difficult this can be. They may sometimes benefit from an industry boom, but they also will feel the pain of the industry bust if they’re not fully prepared. That means better fiscal policy decisions are needed to ensure other revenue sources and reserves are available to cover short-term needs and allow for long-term economy-boosting investments. All states can extract lessons from energy-producing states’ revenue woes.

End Notes

[1] National Association of State Budget Officers, “Fiscal Survey of the States,” Fall 2016, http://www.nasbo.org/reports-data/fiscal-survey-of-states

[2] For example, Massachusetts is projecting an $800 million [?] budget gap for fiscal year 2018; Nebraska and Virginia are facing large gaps ($870 million and $1.5 billion, respectively) in their upcoming two-year budgets.

[3] Elizabeth C. McNichol, “Strategies to Address the State Tax Volatility Problem,” Center on Budget and Policy Priorities, April 18, 2013, https://www.cbpp.org/research/strategies-to-address-the-state-tax-volatility-problem.

[4] Devashree Saha and Mark Muro, “Permanent Trust Funds: Funding Economic Change with Fracking Revenues,” Metropolitan Policy Program at Brookings, April 2016, https://www.brookings.edu/wp-content/uploads/2016/07/Permanent-Trust-Funds-Saha-Muro-418-1.pdf.

[5] Alaska’s revenue was particularly hard hit by the decline in oil prices. By fiscal year 2015, severance taxes made up just 12 percent of tax revenues. (CBPP calculations of Census Government Finance data.) Fiscal year 2017 total general fund revenue was just 16 percent of the average for fiscal years2003–2013, Alaska Revenue and Expenditures FY07-FY17, Legislative Finance Division Informational Paper 17-1, July 2016.

[6] Louisiana Joint Legislative Committee on the Budget, “Executive Budget Presentation, Fiscal Year 2016-2017,” February 13, 2016, http://www.doa.la.gov/comm/presentations/JLCB%20Exec%20Budget%20Presentation%202-13-16.pdf.

[7] Associate Press, “See which Louisiana taxes are going up, and which aren’t,” The Times-Picayune, March 10, 2016, http://www.nola.com/politics/index.ssf/2016/03/see_how_louisiana_taxes_are_go.html; Julia O’Donoghue, “Louisiana House committee approves budget that funds TOPS, but not hospitals,” The Times-Picayune, May 10, 2016, http://www.nola.com/politics/index.ssf/2016/05/louisiana_house_budget_restore.html#incart_article_small.

[8] Michael Mitchell, Michael Leachman, and Kathleen Masterson, “Funding Down, Tuition Up,” Center on Budget and Policy Priorities, August 15, 2016, https://www.cbpp.org/research/state-budget-and-tax/funding-down-tuition-up.

[9] Elizabeth Crisp, “State revenue forecasting panel delays action on deficit until January,” The Advocate, December 13, 2016, http://www.theadvocate.com/baton_rouge/news/politics/article_8d72428c-c15a-11e6-9d6d-fbb5b68df450.html?sr_source=lift_amplify.

[10] Elizabeth Crisp, “Thousands of students could lose TOPS scholarship under latest ‘very nasty’ proposed budget cuts,” The Advocate, April 16, 2016, http://theadvocate.com/news/15467310-77/gov-john-bel-edwards-presents-750m-budget-cut-plan.

[11] Kevin Litten, “DHH secretary blasts Appropriations for ‘faux,’ ‘nonsensical’ budget proposal,” The Times-Picayune, May 12, 2016, http://www.nola.com/politics/index.ssf/2016/05/dhh_budget_cuts_hospitals.html.

[12] Julia O’Donoghue, “Louisiana’s budget is a hot mess: How we got here,” The Times-Picayune, February 19, 2016, http://www.nola.com/politics/index.ssf/2016/02/louisiana_is_in_a_budget_mess.html. The Institute for Taxation and Economic Policy has estimated the annual impact to be just slightly higher, but in the same ballpark.

[13] Steve Spires, “Louisiana’s $1.6 billion problem: How did we get here?” Louisiana Budget Project, February 24, 2016, http://www.labudget.org/lbp/2015/02/louisianas-1-6-billion-problem-how-did-we-get-here/.

[14] Louisiana Legislative Auditor, “Severance Tax Suspension for Horizontal Wells,” August 19, 2015, https://app.lla.state.la.us/PublicReports.nsf/65C7443D8D09105F86257EA6007174D9/$FILE/00009E0B.pdf; Louisiana Department of Revenue, “Tax Exemption Budget 2015-2016,” January 2016, http://revenue.louisiana.gov/Publications/TEB(2015-2016).pdf.

[15] Oklahoma Office of Management & Enterprise Services, “BOE approves $5.8B for appropriations, FY 2017 Budget Hole Projected at $1.3B,” February 16, 2016, http://content.govdelivery.com/accounts/OKOMES/bulletins/136b6c9; Oklahoma Policy Institute, “Budget Trends and Outlook – March 2016,” March 4, 2016, http://okpolicy.org/budget-trends-and-outlook-march-2016/.

[16] Oklahoma Policy Institute, “FY 2017 Budget Highlights,” June 7, 2016, http://okpolicy.org/fy-2017-budget-highlights/.

[17] Chuck Marr, et al., “EITC and Child Tax Credit Promote Work, Reduce Poverty, and Support Children’s Development, Research Finds,” Center on Budget and Policy Priorities, updated October 1, 2015, https://www.cbpp.org/research/federal-tax/eitc-and-child-tax-credit-promote-work-reduce-poverty-and-support-childrens?fa=view&id=3793.

[18] Barbara Hoberock, “With state facing $868 million budget hole, revenue will fall short of triggering income tax reduction,” Tulsa World, December 21, 2016, http://www.tulsaworld.com/news/capitol_report/with-state-facing-million-budget-hole-revenue-will-fall-short/article_cd4fb785-9f61-578f-859c-5ea9fc422fe0.html.

[19] Oklahoma Health Care Authority, “Press Release: OHCA to Propose Provider Rate Cuts,” March 29, 2016, http://www.okhca.org/about.aspx?id=18904.

[20] David Blatt, “The Cost of Tax Cuts in Oklahoma,” Oklahoma Policy Institute, January 12, 2016, http://okpolicy.org/the-cost-of-tax-cuts-in-oklahoma.

[21] David Blatt, “Even amid energy bust, Oklahoma’s oil and gas tax breaks exceed $400 million per year,” Oklahoma Policy Institute, May 5, 2016, http://okpolicy.org/even-amid-energy-bust-oklahomas-oil-gas-tax-breaks-exceed-400-million-per-year/.

[22] Ted Boettner and Sean O’Leary, “Confronting the Fiscal Gap,” West Virginia Center on Budget & Policy, February 16, 2016, http://www.wvpolicy.org/wp-content/uploads/2016/02/PDF-FY17-Gov-Budget-Brief-2.16.16-FINAL.pdf; Phil Kabler, “Report says tax cuts responsible for budget deficit,” Charleston Gazette-Mail, February 16, 2016, http://www.wvgazettemail.com/news/20160216/report-says-tax-cuts-responsible-for-budget-deficit; State News Service, “Governor Tomblin Issues Statement on Budget Following New Revenue Estimates for Fiscal Year 2017,” HighBeam Research, March 15, 2016. [link?]

[23] Phil Kabler, “WV agencies: Hypothetical budget cut could force layoffs, closures,” Charleston Gazette-Mail, February 18, 2016, http://www.wvgazettemail.com/news/20160218/wv-agencies-hypothetical-budget-cut-could-force-layoffs-closures and Mitchell, Leachman, and Masterson.

[24] Boettner and O’Leary.

[25] Michael Leachman, et al., “State Personal Income Tax Cuts: Still A Poor Strategy for Economic Growth,” Center on Budget and Policy Priorities, updated May 14, 2015, https://www.cbpp.org/research/state-budget-and-tax/state-personal-income-tax-cuts-still-a-poor-strategy-for-economic and Michael Mazerov, “Academic Research Lacks Consensus on the Impact of State Tax Cuts on Economic Growth,” Center on Budget and Policy Priorities, June 17, 2013, https://www.cbpp.org/cms/?fa=view&id=3975.

[26] Erica Williams, “A Fiscal Policy Agenda for Stronger State Economies,” Center on Budget and Policy Priorities, April 13, 2016, https://www.cbpp.org/research/state-budget-and-tax/a-fiscal-policy-agenda-for-stronger-state-economies.

[27] Elizabeth McNichol, “When and How States Should Strengthen their Rainy Day Funds,” Center on Budget and Policy Priorities, April 17, 2014, https://www.cbpp.org/research/state-budget-and-tax/when-and-how-states-should-strengthen-their-rainy-day-funds?fa=view&id=4129.

[28] Elizabeth McNichol and Kwame Boadi, “Why and How States Should Strengthen Their Rainy Day Funds,” Center on Budget and Policy Priorities, February 3, 2011, https://www.cbpp.org/research/why-and-how-states-should-strengthen-their-rainy-day-funds?fa=view&id=3387.

[29] North Dakota Office of Management and Budget, “North Dakota Rev-E-News,” February 2016, https://www.nd.gov/omb/sites/omb/files/documents/newsletters/201602news.pdf.

[30] Office of Management and Budget, “Legislative Appropriations 2015-2017 Biennium,” https://www.nd.gov/omb/sites/omb/files/documents/agency/financial/state-budgets/docs/budget/appropbook2015-17.pdf?ts=2016021812.

[31] McNichol, 2014.

[32] Alaska Office of Management & Budget, “Ten Minute Fiscal Overview Presentation,” 2015, http://gov.alaska.gov/Walker_media/documents/sustainable-alaska/10-min-fiscal-overview.pdf.

[33] Office of Management and Budget, “FY2017 10-Year Plan,” January 22, 2016, https://www.omb.alaska.gov/ombfiles/17_budget/PDFs/FY2017_10-year_plan_1_22_2016_FINAL.pdf.

[34] Becky Bohrer, “With deadline looming, a look at Alaska budget proposals,” Newsminer, May 12, 2016, http://www.newsminer.com/news/alaska_news/with-deadline-looming-a-look-at-alaska-budget-proposals/article_5963eef2-18a2-11e6-9ded-bb65d06bd838.html; Kirk Johnson, “Alaska’s Schools Face Cuts at Every Level Over Oil Collapse,” The New York Times, March 14, 2016, http://www.nytimes.com/2016/03/15/us/oil-collapse-drains-alaskas-wide-ranging-education-system.html?_r=0; Ed Schoenfeld, “Budget cuts could leave communities without health care,” Alaska Public Media, April 18, 2016, http://www.alaskapublic.org/2016/04/18/budget-cuts-could-leave-communities-without-health-care/; Rashah McChesney, “Budget Cuts Affect Alaska’s Food Safety Division,” Claims Journal, May 12, 2016, http://www.claimsjournal.com/news/west/2016/05/12/270747.htm .

[35] Aidan Russell Davis, Carl Davis, and Matthew Gardner, “Distributional Analyses of Revenue Options for Alaska,” Institute on Taxation & Economic Policy, April 2016, http://itep.org/itep_reports/pdf/AKrevenueoptions0416.pdf.

[36] Wyoming Legislative Service Office, “2017 Budget Fiscal Data Book,” December 2016, http://legisweb.state.wy.us/budget/2017databook.pdf.

[37] Wyoming Joint Education Committee, “Wyoming K-12 Education Funding Deficit White Paper,” December 28, 2016, http://legisweb.state.wy.us/lsoweb/WhitePaperEducation.pdf.

[38] Higher volatility does not automatically bring higher long-term growth for all state taxes. For example, the corporate income tax is more volatile than the personal income tax but also grows more slowly over the long term. See, for example, R. Alison Felix, “The Growth and Volatility of State Tax Revenue Sources in the Tenth District,” Federal Reserve Bank of Kansas City Economic Review, Third Quarter 2008, https://pdfs.semanticscholar.org/de6d/eeb4831daf425c2516ca352048005c9ba5b1.pdf.

More from the Authors

Areas of Expertise