The Outlook for Marketplace Open Enrollment

Even taking into account these headwinds, there are also important factors that will sustain consumer demand for marketplace coverage.On November 1, 2017, HealthCare.gov and state marketplaces will start the Affordable Care Act (ACA)’s fifth open enrollment period, with consumers able to sign up for 2018 health coverage. This open enrollment will be the first under an Administration that has sought to undermine the ACA marketplaces, rather than strengthen them, and the Administration’s actions to date undoubtedly will depress enrollment. But even taking into account these headwinds, there are also important factors that will sustain consumer demand for marketplace coverage, although likely not at the levels seen during the last two open enrollment periods when over 12 million people signed up for plans.

Administration Actions Will Depress Enrollment

2018 Premiums Are Higher Because of the Administration’s Actions

The Trump Administration’s decision (and earlier threats) to stop making cost-sharing reduction (CSR) payments to insurers (payments reimbursing insurers for the cost-sharing assistance they are required to provide to lower-income enrollees), along with uncertainty about how and whether the Administration would administer other provisions of the ACA, have significantly increased 2018 marketplace premiums. Many insurers have raised premiums substantially due to concerns that the Administration would fail to enforce (or would work with Congress to repeal) the ACA’s individual mandate and due to broader uncertainty about the future of the ACA and how the Administration would administer it.[1] On top of that, insurers have increased silver plan premiums by an additional 7 to 38 percent this year to account for non-payment of CSRs.[2]

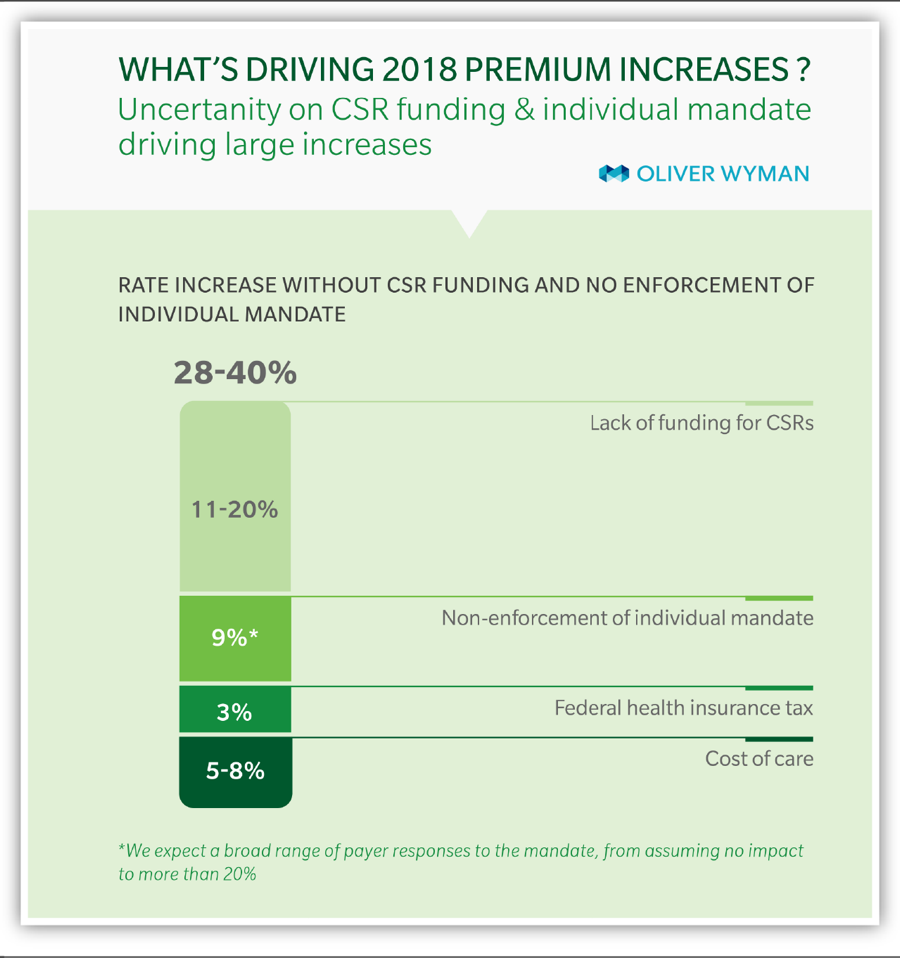

These increases are especially unfortunate given growing evidence that marketplace premium increases would have moderated this year, were it not for the Administration’s actions. Last year’s premium increases largely made up for insurers’ earlier underpricing, and 2018 premium increases would be under 10 percent in a stable policy environment, a Brookings Institution analysis concludes.[3] Similarly, an Oliver Wyman study published earlier this year forecast 2018 premium increases of 8 to 11 percent in a stable policy environment, compared to 28 to 40 percent with continued uncertainty about CSR payments and mandate enforcement.[4] (See Figure 1.) Actual premium increases for benchmark silver plans average 37 percent across the 39 states using the HealthCare.gov eligibility and enrollment platform (“HealthCare.gov states”), consistent with these projections.[5]

While tax credits will adjust to shield the large majority of marketplace consumers from premium increases (as discussed below), consumers with incomes too high to qualify for subsidies will face another year of steep premium increases, instead of more moderate premium growth. Some will likely drop coverage as a result.

Outreach Cuts Will Mean Greater Confusion, Lower Enrollment

The Administration’s large cuts to outreach and enrollment assistance make it less likely that new consumers will learn about the marketplace coverage and financial assistance available to them and harder for them to sign up if they do. The Centers for Medicare & Medicaid Services (CMS) is planning to spend 90 percent less this year on consumer outreach and education (budgeting just $10 million) and 40 percent less on navigator programs that offer enrollment help (budgeting $36 million) than it did for the 2017 open enrollment period.[6] CMS and the rest of the Administration are also reducing their outreach efforts in less quantifiable ways; for example, Department of Health and Human Services (HHS) staff will no longer participate in local enrollment events.[7]

Outreach remains critically important to enrollment. Two in five uninsured adults were unaware of the marketplaces as of earlier this year, and about half were unaware of marketplace financial assistance as of early 2016.[8] Marketing is effective at closing these information gaps. HHS research during the 2015 and 2016 open enrollment periods found that 20 to 37 percent of sign-ups by consumers new to the marketplace were attributable to outreach activities, such as television and digital advertisements.[9] Studies by California’s marketplace (Covered California) and outside experts confirm the effectiveness of advertising in reaching new consumers.[10]

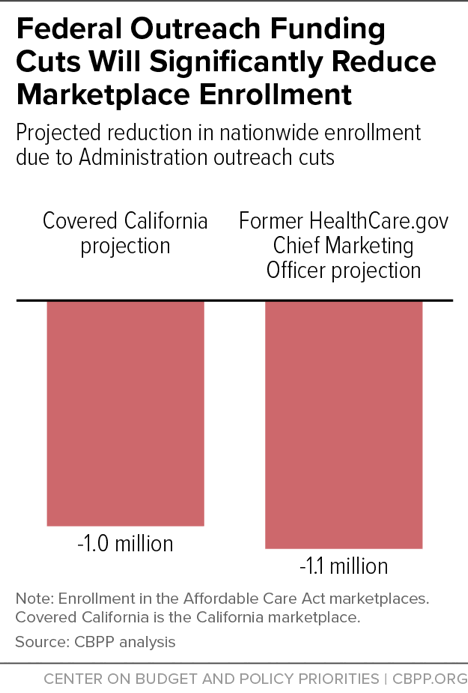

These studies indicate that the Administration’s outreach cuts will have large effects on enrollment. Covered California estimates that these cuts will lead at least 1 million fewer consumers to enroll in coverage nationwide, while HealthCare.gov’s former chief marketing officer projects at least a 1.1 million drop.[11] (See Figure 2.)

Halving the Open Enrollment Period Will Also Depress Sign-Ups

The Administration announced earlier this year that it would cut the 2018 open enrollment period in half for states using HealthCare.gov, with open enrollment running from November 1 through December 15, instead of through January 31. (Most states that run their own marketplace enrollment platforms are maintaining longer open enrollment periods.[12])

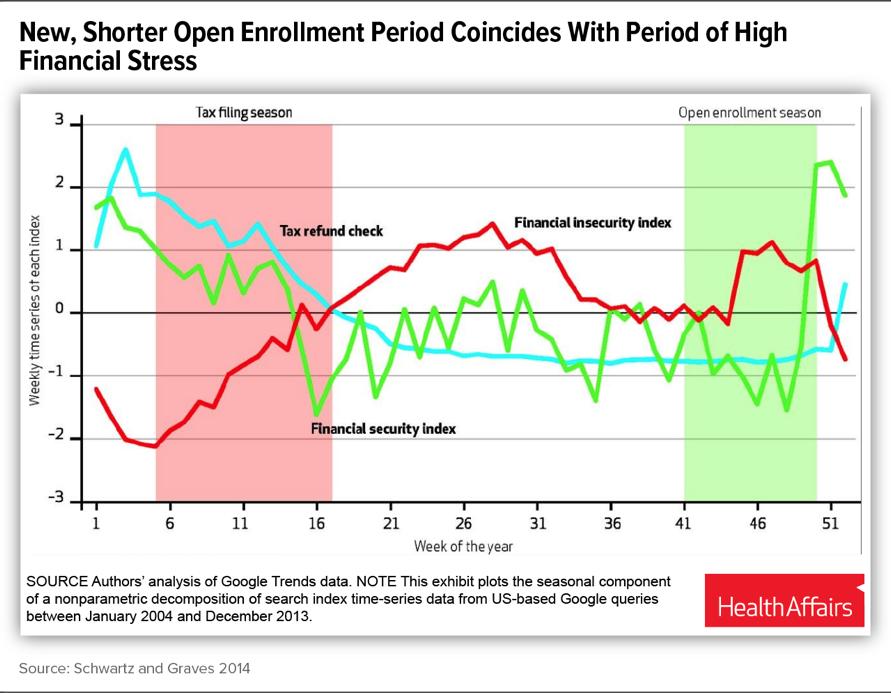

This change will likely depress enrollment in several ways. First, requiring all consumers to sign up by December 15 may overtax HealthCare.gov resources in the days leading up to the deadline, resulting in long website and call center wait times, or even website outages. Second, the shorter enrollment period means consumers will not have the option to wait out the holiday season and sign up for coverage in January. Low- and moderate-income families experience especially high levels of financial stress in December, which may discourage them from enrolling in coverage at that time of year, a study by Harvard and Vanderbilt University researchers found.[13] (See Figure 3.) Third, the shorter open enrollment means fewer opportunities for consumers to hear about HealthCare.gov and less time for them to visit, shop for plans, and get questions answered.

Even as consumers gain more experience with the marketplace, January has remained an important time for new consumer sign-ups. Last year, almost 1 million new HealthCare.gov consumers (30 percent) signed up after late December. January is typically a key month for enrollment of so-called “healthy procrastinators,” including many young people.[14] The shorter enrollment period also means that returning consumers will have less opportunity to switch plans after learning that they have been automatically re-enrolled.[15]

Nine-Month Effort to Repeal the ACA Has Left Consumers Confused

The Administration and Congress’s nine-month effort to repeal the ACA has resulted in confusion among consumers, with some mistakenly believing that the ACA has been repealed, and marketplace coverage is no longer available. In one early October survey, 39 percent of voters said that the ACA had already been fully or partially repealed; that belief was even more prevalent among young people.[16] A separate survey found that nearly a fifth of uninsured adults (mistakenly) believe the ACA’s individual mandate is no longer in effect, while nearly a quarter are unsure.[17]

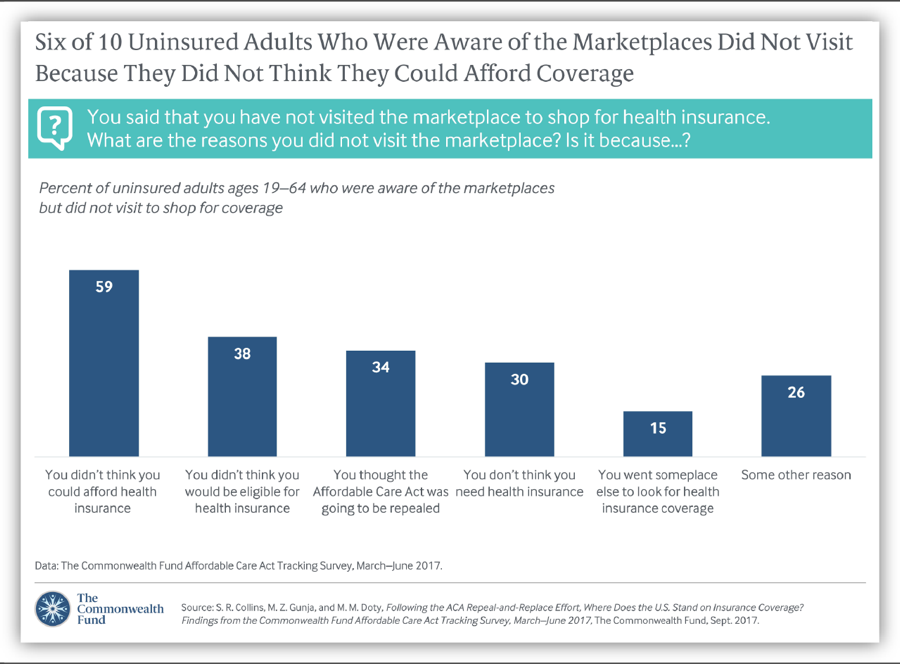

Unsurprisingly, people who believe that marketplace coverage has been or will soon be eliminated are less likely to sign up for a marketplace plan. Last year’s open enrollment coincided with the start of the repeal and replace debate in Congress and with a Trump Administration executive order widely seen as directing federal agencies to weaken the ACA. In a Commonwealth Fund survey, more than one-third of uninsured adults who knew about but did not visit the ACA marketplaces last year cited as one reason their belief that the ACA would soon be repealed.[18] (See Figure 4.)

Why Consumer Demand for Coverage May Stay Strong

Despite the headwinds described above, there are also important reasons marketplace coverage will remain attractive to consumers.

Most Marketplace Consumers Are Satisfied with Their Coverage

The starting point for open enrollment sign-ups are the roughly 10 million current marketplace consumers.[19] More than 80 percent of 2017 marketplace consumers are satisfied with their coverage, similar to previous years, surveys show.[20] (See Figure 5.) Consistent with that, 80 percent of individual market enrollees (on- and off-marketplace) plan to re-enroll in health insurance during the upcoming open enrollment period. [21] Re-enrollment is not appropriate for all consumers, since some obtain job-based coverage, experience income changes that make them eligible for Medicaid, or otherwise find a new source of coverage.

Nonetheless, in previous years, high satisfaction rates among marketplace consumers have indeed translated into high re-enrollment rates. Last year, for example, 5.3 million consumers — a majority of those enrolled — came back to HealthCare.gov or their state marketplace and actively selected a plan, in addition to the 2.8 million who were automatically re-enrolled.

Additionally, as the ACA marketplaces mature, a growing number of people have prior, often positive marketplace experience: they enrolled in the marketplace and then left, often because they obtained other coverage. This group may be more likely to return to the marketplace as “new” consumers if their circumstances change again.

Most Current and Potential Marketplace Consumers Are Protected from Rate Increases

Under the ACA, marketplace consumers with incomes below 400 percent of the poverty level (about $100,000 for a family of four) can purchase benchmark coverage for no more than a set fraction of their income, regardless of sticker price premiums. That means that these subsidy-eligible consumers are fully shielded from premium increases. For example, a family of four with income of $50,000 is guaranteed the option to purchase benchmark coverage for no more than about 6.5 percent of their income, or about $270 per month. Whether sticker price premiums increase to $1,000 or $2,000, the family’s net premium remains the same, with premium tax credits adjusting as needed to make up the difference.

The large majority of both current and potential marketplace enrollees are eligible for premium tax credits. Among 2017 marketplace enrollees, 84 percent qualify for tax credits.[22] Likewise, HHS estimated in 2016 that more than 80 percent of the marketplace-eligible uninsured had incomes below 400 percent of the poverty level, suggesting they could qualify for subsidies. Even taking into account people purchasing individual market coverage off-marketplace, HHS and independent analysts have estimated that a substantial majority of individual market consumers either receive premium tax credits or could qualify for them if they switched to purchasing marketplace coverage.[23]

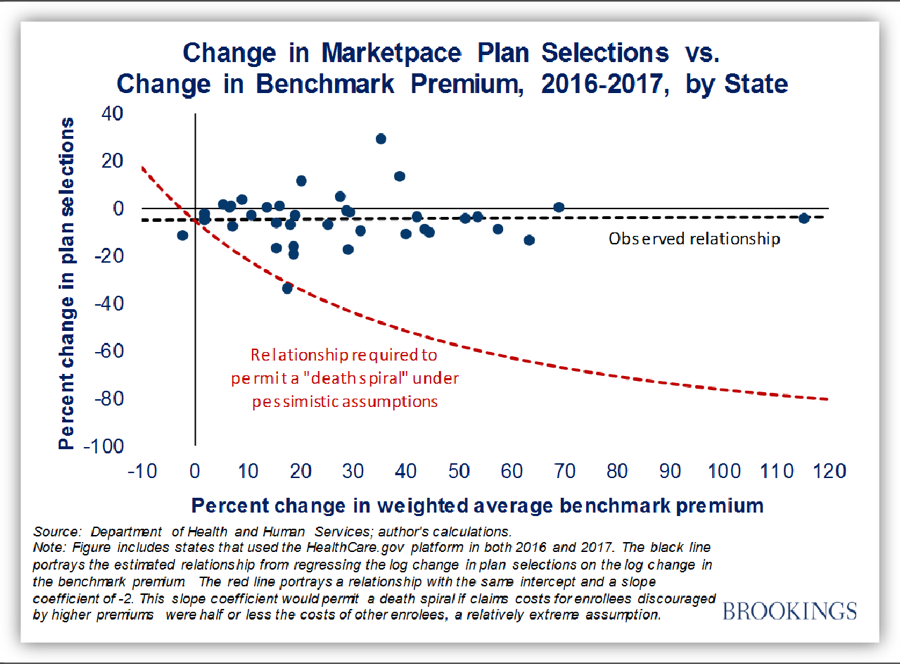

Last year, sticker price premiums for benchmark coverage increased by an average of 25 percent in HealthCare.gov states.[24] Nonetheless, average net premiums for the more than 80 percent of consumers qualifying for subsidies remained unchanged at $106 per month.[25] As would be expected given these figures, there’s no evidence that sticker price premium increases in 2017 significantly reduced marketplace enrollment. In fact, rate increases and enrollment changes were uncorrelated across states in 2017 (see Figure 6); the same was true in 2015 and 2016 as well.[26]

Many Subsidized Consumers Will Be Able to Find Lower-Cost Plans This Year

Not only will subsidy-eligible consumers be protected from premium increases, the nature of this year’s premium increases means that many subsidized consumers will be able to find better bargains than in previous years. As noted above, a large share of this year’s premium increases is due to the Trump Administration’s decision to stop CSR payments: payments reimbursing insurers for the cost-sharing assistance they are required to provide to lower-income enrollees. But this assistance is available only to consumers who enroll in marketplace silver plans. For that reason, insurers in most states have raised premiums for silver — but not for bronze, gold, or platinum — plans to account for the loss of CSRs.[27] Because premium tax credits increase to match increases in silver plan premiums, that means that tax credits in many places are increasing by much larger amounts than bronze or gold plan premiums are.[28]

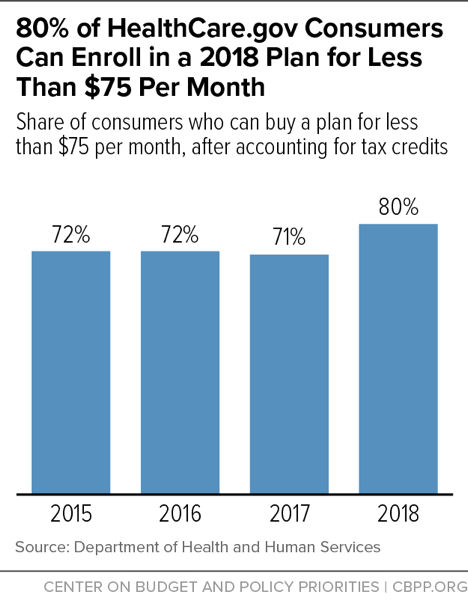

For many subsidized consumers, that will result in unusually low premiums (net of tax credits) for bronze and gold plans this year. For example, the Kaiser Family Foundation estimates that premiums for the lowest-price available bronze and gold plans will fall for subsidized consumers at most income levels in most of the country — in many cases by significant amounts. For a 40-year-old with income of $30,000 (about 250 percent of the poverty level), the cost of purchasing the lowest-price available bronze plans will fall by an average of 54 percent across HealthCare.gov states, while the cost of purchasing the lowest-price available gold plan will fall by an average of 16 percent. These decreases occur because silver plan premiums, and therefore tax credits, are increasing significantly more than bronze and gold plan premiums are.[29] Overall, HHS estimates that 80 percent of HealthCare.gov consumers will be able to find a 2018 plan with a premium of less than $75 per month after tax credits, a larger share than in any previous year (see Figure 7).[30]

Lower-income consumers who are eligible for generous cost-sharing assistance will usually still be best served by enrolling in silver plans.[31] But moderate-income consumers may be able to purchase plans with much lower deductibles for lower or similar prices and may have access to high-deductible plans with extremely low premiums. These unusual bargains could attract new enrollees who previously found marketplace coverage unaffordable (although unfortunately, fewer people will learn about them, due to the Administration’s cuts to marketplace outreach discussed above).

Unsubsidized Consumers May Also Find Better Deals Than Expected

Lower premium increases for gold and bronze plans compared to silver plans also mean that unsubsidized consumers may find better deals than they expect, although most will still face significant premium increases (in large part reflecting the Administration’s actions, as discussed above). The average premium increases reported by state regulators and in the press are heavily weighted toward silver plans, which enroll about three-quarters of HealthCare.gov consumers. But more than half of unsubsidized consumers are enrolled in bronze or gold plans. Many unsubsidized consumers may therefore see premium increases lower than reported averages even if they stick with a plan within their current coverage tier. Others may be able to secure smaller increases in total costs (premiums plus deductibles, copays, and coinsurance) if they shop around and consider bronze or gold plan options.[32]

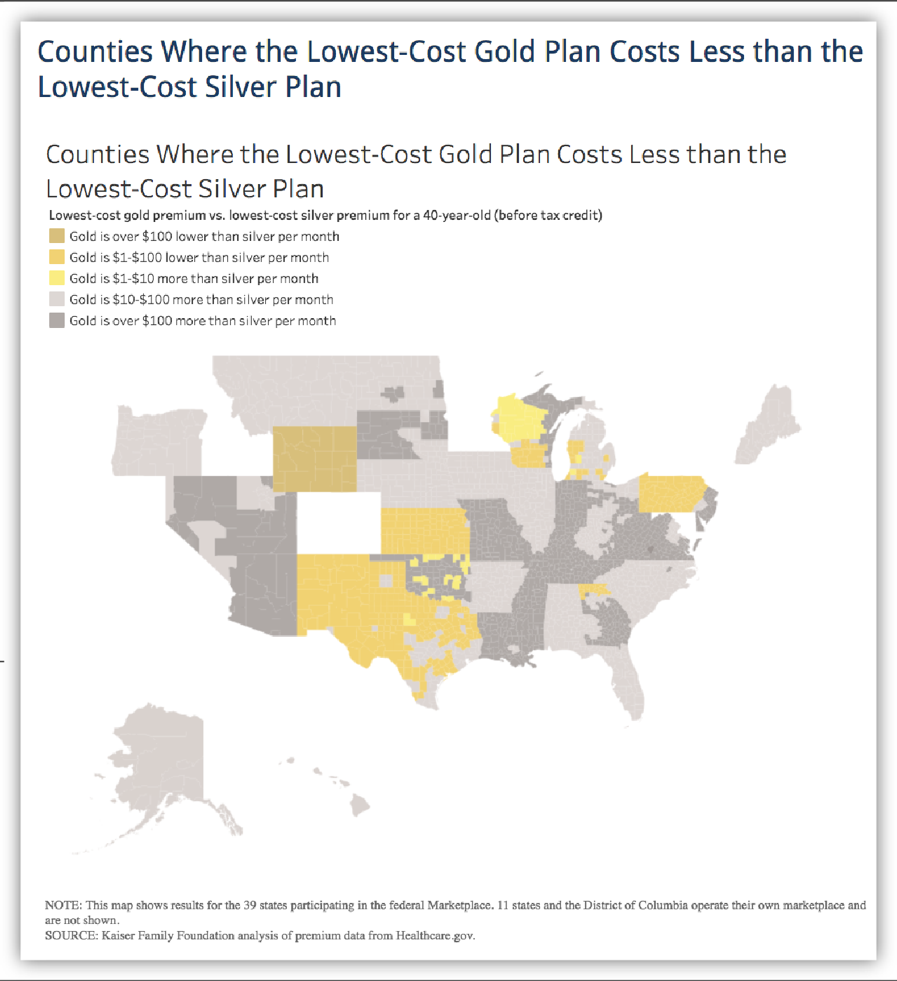

On average across HealthCare.gov states, premiums for the lowest-price available bronze and gold plans are increasing by only about half as much as lowest-cost silver plan premiums.[33] One result is that there are parts of the country where gold plans now cost about the same amount as, or less than, silver plans. (See Figure 8.) In some areas, therefore, unsubsidized consumers can both reduce their year-over-year premium increase and lower their deductibles by switching from silver to gold plans. Likewise, bronze plans may offer a better deal than silver plans, because, while they still have higher deductibles, the premium discount they offer is larger than normal this year. The lowest-price available bronze plan costs 29 percent less than the benchmark silver plan this year, on average across HealthCare.gov states, compared to 17 percent less last year.[34]

Projections for unsubsidized consumer attrition that are based on average silver plan premium increases — and ignore the better deals available for non-silver plans — are likely to overstate 2018 marketplace enrollment declines.

End Notes

[1] While there is no comprehensive survey of rate increases due to concerns about individual mandate enforcement, CareFirst, a major insurer in Maryland, Virginia, and Washington D.C., requested additional rate increases of 15 percent due to concerns about the individual mandate (https://www.vox.com/2017/5/8/15563448/trump-insurance-premiums-2018), and Pennsylvania’s insurance commissioner reported in June that insurers would request additional rate increases averaging 14.5 percent if concerns about mandate non-enforcement or repeal were not addressed (http://www.media.pa.gov/Pages/Insurance-Details.aspx?newsid=248). Insurers in a number of other states, including Alabama, Arizona, Indiana, Iowa, Louisiana, Oregon, and elsewhere, attributed a portion of their rate increases to concerns about mandate enforcement or to broader policy uncertainty.

[2] Rabah Kamal et al., “How the Loss of Cost Sharing Reduction Subsidy Payments Is Affecting 2018 Premiums,” Kaiser Family Foundation, October 27, 2017, https://www.kff.org/health-reform/issue-brief/how-the-loss-of-cost-sharing-subsidy-payments-is-affecting-2018-premiums/.

[3] Matthew Fiedler, “Taking Stock of Insurer Financial Performance in the Individual Health Insurance Market Through 2017,” USC-Brookings Schaeffer Initiative for Health Policy, October 27, 2017, https://www.brookings.edu/wp-content/uploads/2017/10/individualmarketprofitability.pdf.

[4] Kurt Giesa, “Analysis: Market Uncertainty Driving ACA Rate Increases,” Oliver Wyman, June 4, 2017, http://health.oliverwyman.com/transform-care/2017/06/analysis_market_unc.html.

[5] Assistant Secretary for Planning and Evaluation, “Health Plan Choice and Premiums in the 2018 Federal Health Insurance Exchange,” Department of Health and Human Services, October 30, 2017, https://aspe.hhs.gov/system/files/pdf/258456/Landscape_Master2018_1.pdf.

[6] For further discussion of the Administration’s outreach cuts, see Shelby Gonzales, “Trump Administration Slashing Funding for Marketplace Enrollment Assistance and Outreach,” Center on Budget and Policy Priorities, September 1, 2017, https://www.cbpp.org/blog/trump-administration-slashing-funding-for-marketplace-enrollment-assistance-and-outreach.

[7] Dylan Scott, “Trump Administration Abruptly Drops Out of Obamacare Events in Mississippi,” Vox, September 27, 2017, https://www.vox.com/policy-and-politics/2017/9/27/16374158/obamacare-mississippi-hhs-events.

[8] Sara R. Collins, Munira Z. Gunja, and Michelle M. Doty, “Following the ACA Repeal-and-Replace Effort, Where Does the U.S. Stand on Insurance Coverage?” Commonwealth Fund, September 7, 2017, http://www.commonwealthfund.org/publications/issue-briefs/2017/sep/post-aca-repeal-and-replace-health-insurance-coverage and Commonwealth Fund, “Affordable Care Act Tracking Survey,” http://acatracking.commonwealthfund.org/.

[9] Jonathan Cohn, “Trump Administration Says Obamacare Ads Don’t Work, but Federal Study Says They Do,” Huffington Post, September 20, 2017, https://www.huffingtonpost.com/entry/obamacare-ads-trump-health-human-services_us_59c1dc7de4b0186c2206bdd3.

[10] Peter V. Lee et al., “Marketing Matters: Lessons from California to Promote Stability and Lower Costs in National and State Individual Insurance Markets,” Covered California, September, 2017, http://hbex.coveredca.com/data-research/library/CoveredCA_Marketing_Matters_9-17.pdf and Pinar Karaca-Mandic et al., “The Volume of TV Advertisements During the ACA’s First Open Enrollment Period Was Associated with Increased Insurance Coverage,” Health Affairs, April 2017, http://www.healthaffairs.org/doi/10.1377/hlthaff.2016.1440.

[11] Joshua Peck, “Trump’s Ad Cuts Will Cost a Minimum of 1.1 Million Obamacare Enrollments,” Get America Covered, October 23, 2017, https://medium.com/get-america-covered/trumps-ad-cuts-will-cost-a-minimum-of-1-1-million-obamacare-enrollments-9334f35c1626 and Lee, op. cit.

[12] For a list of open enrollment deadlines in State-Based Marketplaces, see Louise Norris, “What’s the Deadline to Get Coverage During Obamacare’s Open Enrollment?” healthinsurance.org, October 2, 2017, https://www.healthinsurance.org/faqs/what-are-the-deadlines-for-obamacares-open-enrollment-period/.

[13] Katherine Swartz and John Graves, “Shifting the Open Enrollment Period for ACA Marketplaces Could Increase Enrollment and Improve Plan Choices,” Health Affairs, July 2014, http://www.healthaffairs.org/doi/10.1377/hlthaff.2014.0007#. Florida Blue, a major marketplace insurer, has also flagged this concern, noting in its comment letter on the HHS Notice of Benefit and Payment Parameters for 2018: “It is well established that creating an [open enrollment period] that peaks between Thanksgiving and Christmas forces consumers to make financial decisions when their debt is at its highest levels and their interest in their health is at the lowest. Allowing sales in January helps, as consumer debt levels for subsidy eligible individuals are often off-set by the earned income tax credit and people generally have a renewed focus on their health.”

[14] Centers for Medicare & Medicaid Services, “Strengthening the Marketplace by Covering Young Adults,” June 21, 2016, https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2016-Fact-sheets-items/2016-06-21.html.

[15] See Amy Goldstein, “ACA Enrollment Schedule May Lock Millions Into Unwanted Health Plans,” Washington Post, October 20, 2017, https://www.washingtonpost.com/national/health-science/aca-enrollment-schedule-may-lock-millions-into-unwanted-health-plans/2017/10/20/c2171008-b5ce-11e7-a908-a3470754bbb9_story.html?utm_term=.20478feb34cf.

[16] Morning Consult, National Tracking Poll #171011, October 19–23, 2017, https://morningconsult.com/wp-content/uploads/2017/10/171011_crosstabs_POLITICO_v1_AP-2.pdf.

[17] Ashley Kirzinger et al., “Kaiser Health Tracking Poll – October 2017: Experiences of the Non-Group Marketplace Enrollees,” Kaiser Family Foundation, October 28, 2017, https://www.kff.org/health-reform/poll-finding/kaiser-health-tracking-poll-october-2017-experiences-of-the-non-group-marketplace-enrollees/.

[18] Collins, Gunja, and Doty, op. cit.

[19] Centers for Medicare & Medicaid Services, “2017 Effectuated Enrollment Snapshot,” June 12, 2017, https://downloads.cms.gov/files/effectuated-enrollment-snapshot-report-06-12-17.pdf.

[20] Collins, Gunia, and Doty, op. cit.

[21] Ashley Kirzinger et al., op. cit.

[22] Centers for Medicare & Medicaid Services, “2017 Effectuated Enrollment Snapshot.”

[23] Assistant Secretary for Planning and Evaluation, “About 2.5 Million People Who Currently Buy Coverage Off-Marketplace May Be Eligible for ACA Subsidies,” Department of Health and Human Services, October 4, 2016, https://aspe.hhs.gov/system/files/pdf/208306/OffMarketplaceSubsidyeligible.pdf. In addition, McKinsey analysts estimated that about 70 percent of consumers across the entire individual market have incomes below 400 percent of the poverty level. McKinsey Center for U.S. Health Reform, “Exchanges Three Years In: Market Variations and Factors Affecting Performance,” May 2016, http://healthcare.mckinsey.com/sites/default/files/Intel%20Brief%20-%20Individual%20Market%20Performance%20and%20Outlook%20%28public%29_vF.pdf.

[24] Assistant Secretary for Planning and Evaluation, “Health Plan Choice and Premiums in the 2017 Health Insurance Marketplace,” Department of Health and Human Services, October 24, 2016, https://aspe.hhs.gov/system/files/pdf/212721/2017MarketplaceLandscapeBrief.pdf.

[25] Centers for Medicare & Medicaid Services, “Health Insurance Marketplaces 2017 Open Enrollment Period Final Open Enrollment Report,” March 15, 2017, https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2017-Fact-Sheet-items/2017-03-15.html.

[26] Matthew Fiedler, “New Data on Sign-Ups Through ACA’s Marketplaces Should Lay ‘Death Spiral’ Claims to Rest,” Brookings Institution, February 8, 2017, https://www.brookings.edu/blog/up-front/2017/02/08/new-data-on-sign-ups-through-the-acas-marketplaces-should-lay-death-spiral-claims-to-rest/; for analysis of earlier years, see Council of Economic Advisers, “Understanding Recent Developments in the Individual Market,” January 2017, https://obamawhitehouse.archives.gov/sites/default/files/page/files/201701_individual_health_insurance_market_cea_issue_brief.pdf.

[27] See https://public.tableau.com/profile/david3039#!/vizhome/StateSTrategiesforCSR2018/StateresponsestoCSRrisk.

[28] Marketplace plans are categorized into metal levels based on the share of total health care costs covered by the plan versus covered by the enrollee through deductibles, coinsurance, and copays. Bronze plans cover about 60 percent of total costs, on average, and had median deductibles of $6,300 in 2016. Silver plans cover about 70 percent of total costs, on average, and had median deductibles of $3,000 (though much lower for consumers eligible for cost-sharing assistance). Gold plans cover about 80 percent of total costs, on average, and had median deductibles of $1,000. (Platinum plans, which are significantly less common, cover 90 percent of total costs on average, with median deductibles of $250.) Centers for Medicare & Medicaid Services, “Data Brief: 2016 Median Marketplace Deductible $850, with Seven Services Covered Before the Deductible on Average,” July 12, 2016, https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2016-Fact-sheets-items/2016-07-12.html.

[29] Ashley Semanskee, Gary Claxton, and Larry Levitt, “How Premiums Are Changing in 2018,” Kaiser Family Foundation, October 30, 2017, https://www.kff.org/health-reform/issue-brief/how-premiums-are-changing-in-2018/.

[30] Assistant Secretary for Planning and Evaluation, “Health Plan Choice and Premiums in the 2018 Federal Health Insurance Exchange.”

[31] Consumers with incomes below 200 percent of the poverty level (about $25,000 for a single adult, or about $50,000 for a family of four) are eligible for cost-sharing subsidies that reduce their silver plan cost sharing to well below the levels they would face in a gold plan. But consumers with incomes between 200 and 400 percent of the poverty level may want to consider options other than silver plans.

[32] In addition, insurers in some states are imposing CSR-related increases only for on-marketplace silver plans, not for those offered exclusively off-marketplace. Unsubsidized consumers in these states may be able to obtain lower premiums for silver coverage by purchasing coverage off-marketplace.

[33] Semanskee, Claxton, and Levitt, op. cit.

[34] Assistant Secretary for Planning and Evaluation, “Health Plan Choice and Premiums in the 2018 Federal Health Insurance Exchange.”

More from the Authors

Areas of Expertise