Commentary: Senate Tax Bill Revisions Make Its Fundamental Tradeoffs — Big Tax Cuts for the Top, Little Gain for Low- and Moderate-Income Families — Even Harsher

The revised tax bill[1] from Senate Finance Committee Chairman Orrin Hatch takes his original bill[2] — which already provided large tax cuts to the wealthy and profitable corporations, raised taxes on millions of households, and did little if anything for millions more — and makes it even worse in very basic ways.

proposals meant to benefit middle-class families — such as expanding the standard deduction, expanding the Child Tax Credit (CTC), and lowering tax rates —would expire after eight years.To finance a permanent cut in the corporate tax rate, the revised bill permanently repeals the Affordable Care Act’s individual mandate — the requirement that people get health insurance or pay a penalty — which would leave 13 million more people uninsured, raise premiums for millions more, and create uncertainty across the health insurance market.[3] In addition, it proposes a permanent change in the tax code that would raises taxes on many low- and middle-income individuals who would get little or nothing from the permanent corporate rate cuts. While all those measures would be permanent, other proposals meant to benefit middle-class families — such as expanding the standard deduction, expanding the Child Tax Credit (CTC), and lowering tax rates —would expire after eight years. And even though the revised bill provides a larger increase in the CTC than Chairman Hatch’s original bill, it continues to provide only a token increase ($75 or less) to 10 million children low-income working families.

The Chairman’s revisions to his original bill reflect the fundamental trade-off at the core of every Republican tax plan of recent weeks: large, permanent tax cuts for profitable corporations, along with tax changes that don’t help or even hurt low- and moderate-income families. Hatch’s changes come to a bill that already provided large benefits to the wealthy, including a significant cut in the estate tax that only the top two out of every 1,000 estates face to begin with; a tax cut for “pass-through” income that the owners of such businesses as partnerships, S corporations, and sole proprietorships claim on their individual tax returns and that’s taxed at the same rates as wages and salaries; a repeal of the Alternative Minimum Tax that’s designed to ensure that the wealthiest households pay at least some minimum level of tax; and a cut in the top individual income tax rate — all while providing little if anything for millions of low- and middle-income families.[4]

13 Million More Uninsured, Along With Premium Increases

The new bill repeals the individual mandate, which would increase the number of Americans without health insurance by 13 million by 2027, the Congressional Budget Office (CBO) estimates. Millions more would face increases in their premiums: the cost of buying coverage in the Affordable Care Act’s marketplace would rise by about 10 percent in most years, CBO estimates, or by hundreds of dollars per year for about 7 million mostly middle-income consumers and by over $1,000 per year for many older people.[5]

Senate Majority Leader Mitch McConnell said that Republicans added this measure to Hatch’s original bill in large part to help pay for permanent corporate tax rate cuts.[6] Repealing the mandate generates federal savings due to reduced health coverage: the government would spend less on premium tax credits to help low- and moderate-income households pay for marketplace coverage as fewer people sign up for it, less on Medicaid as fewer people enroll, and less on the tax exclusion for employer-sponsored health insurance as fewer employees get coverage from their employers.

By generating $53 billion in savings in 2027, the mandate repeal pays for about one-third (about 4.7 percentage points) of the overall corporate tax cut that would reduce the current 35 percent corporate rate to 20 percent. We estimate, based on Tax Policy Center estimates,[7] that by 2027 a 4.7-percentage-point corporate rate cut would provide annual tax cuts worth an average of $14,890 for households with incomes over $1 million and $94,540 for households in the top 0.1 percent (with incomes over $3.1 million in 2017). That’s because corporate rate cuts largely benefit corporate CEOs and wealthy investors.

Thus, these proposals amount to a trade-off that provides corporate tax cuts that overwhelmingly benefit the wealthy, at the cost of health coverage for 13 million people and premium increases for millions more.

Permanent Corporate Tax Cuts, With Tax Increases for Everyone Else

To further ensure that the bill not does increase the deficit beyond the first ten years, as required under budget rules, Chairman Hatch proposed two additional changes to it.

First, it makes permanent a change to the inflation measure used to adjust tax brackets and other tax parameters every year — using the “chained Consumer Price Index,” which grows more slowly than the current inflation measure. In practice, that means that taxpayers across the board will pay slightly more each year, with the impact growing over time. As New York University professor David Kamin demonstrates,[8] this provision represents a trade-off between a tax increase for every income group except the top 1 percent and a three-percentage-point drop in the corporate tax rate that this provision finances.

Second, the revised bill makes the other provisions related to individual income taxes, including those that provide tax relief to middle-class families, expire after eight years. The expiration of such provisions as the larger CTC, the increased standard deduction, and the cut in individual income tax rates means that many millions more families would face a tax increase beginning in 2026. Even if lawmakers made these provisions permanent, however, the added benefits for many low- and moderate-income families would not be large enough to outweigh the harm they would suffer from the mandate repeal and a chained CPI, along with other individual tax provisions such as the repeal of personal exemptions. Indeed, that’s why tens of millions of families are direct losers from the bill even within the first decade of its implementation.

The Republican tax bill’s supporters already object to such an analysis, arguing that policymakers over the next decade surely will extend the individual tax provisions that would otherwise expire. That’s far from certain, however. Whether due to concerns over the deficit or political gridlock, there is simply no guarantee that the President and Congress will act. But if, policymakers do extend the individual tax provisions in the coming years without offsetting the cost of doing so, the actual costs of this tax bill will far exceed the $1.5 trillion over the first ten years that’s allowed under this year’s budget reconciliation process. As we’ve previously noted,[9] the likely result of unpaid-for tax cuts, and the higher deficits they will fuel, is more pressure on policymakers down the road to cut programs that provide basic assistance for struggling families; health care to children, seniors, people with disabilities and adults with low earnings; and basic public services that benefit the country and economy as a whole, like education, job training, environmental protection, scientific research, and infrastructure. President Trump’s 2018 budget and the 2018 congressional budget resolution already propose cuts that disproportionately affect low- and moderate-income people. In other words, under Chairman Hatch’s revised tax bill, low- and middle-class people will foot the bill for a permanent corporate tax cut either because they pay higher taxes to cover the cost now or they face spending cuts down the road to offset the higher deficits.

A Child Tax Credit Increase That Provides Only Token Help to Millions Who Most Need It

Finally, the revised bill expands the CTC, raising its cost by about $13 billion (or 22 percent) per year but does almost nothing for the millions of low- and moderate-income working families that would get only token help under the prior proposal.

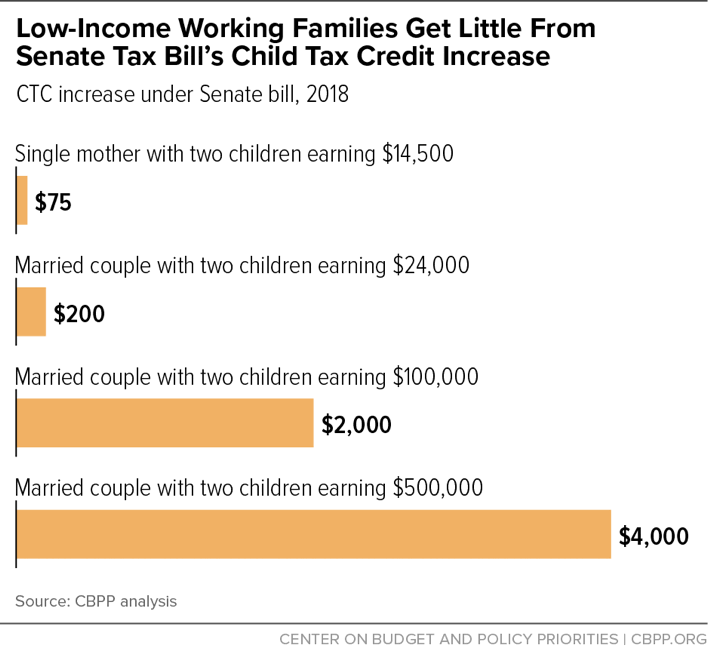

Under the revised proposal, a single mother with two children working full time at the minimum wage would still get just a $75 increase in her credit, as under the prior proposal, while a family with two children and $500,000 in earnings would get a $4,000 credit — up from $3,300 under the prior proposal (see Figure 1) and from $0 under current law. Some 10 million children in working families would get a $75 increase or less. And even this meager increase would be temporary, because the entire CTC increase — as well as the bill’s other individual income tax cuts — would end after 2025.

The revised Senate bill raises the maximum CTC to $2,000 per child, compared to $1,650 under the prior bill. Like the prior bill, it also extends the credit to 17-year-olds, who are currently ineligible. The new bill, however, still severely limits the increase to millions of children in working families because a family must have earnings high enough to owe substantial federal income taxes to benefit from the full $1,000-per-child increase. As we have explained, [10] this means that:

- 1 in 7 children in working families — about 10 million children under age 17 — whose parents work at low-paying jobs would get just $75 per family (even if the family has more than one child), or less; and

- About 16 million additional children under age 17 in low-income working families would get more than $75 but less than the full $1,000-per-child increase — in most cases, much less.

Altogether, 1 in 3 children in working families would receive a token or partial increase. And while severely limiting the CTC increase for many children who need it most, the bill provides the credit to many high-income families for the first time. It raises the income level at which the credit begins phasing out from $110,000 per couple all the way to $500,000. (The prior proposal raised the threshold even higher, to $1 million per couple.)

Conclusion

Chairman Hatch’s revised tax bill takes a bill that would already harm low- and moderate-income families and makes it worse. As noted above, it retains key provisions of his original bill, including a deep cut in the estate tax, a tax cut for “pass-through” businesses, and an end to the Alternative Minimum Tax, that skewed the benefits of this bill heavily to the wealthy. And to achieve the top priority of making corporate tax rate cuts permanent, it includes changes that will cause millions of low- and middle-income people to face a tax increase, add 13 million people to the ranks of the uninsured, and force millions more to pay higher premiums.

End Notes

[1] Joint Committee on Taxation, Description of The Chairman’s Modification to the Chairman’s Mark of the ‘Tax Cuts And Jobs Act,’” November 14, 2017, https://www.finance.senate.gov/imo/media/doc/11.14.17%20Chairman's%20Modified%20Mark.pdf.

[2] Joint Committee on Taxation, “Description of The Chairman’s Mark of the ‘Tax Cuts And Jobs Act,’” November 9, 2017, https://www.finance.senate.gov/imo/media/doc/11.9.17%20Chairman's%20Mark.pdf.

[3] Aviva Aron-Dine, “Senate Tax Bill Would Add 13 Million to Uninsured to Pay for Tax Cuts of Nearly $100,000 Per Year for the Top 0.1 Percent,” Center on Budget and Policy Priorities, November 15, 2017, https://www.cbpp.org/blog/senate-tax-bill-would-add-13-million-to-uninsured-to-pay-for-tax-cuts-of-nearly-100000-per-year.

[4] Sharon Parrott, “Senate Tax Bill Has Same Basic Flaws as House Bill,” Center on Budget and Policy Priorities, November 14, 2017, https://www.cbpp.org/research/federal-tax/senate-tax-bill-has-same-basic-flaws-as-house-bill.

[5] Aron-Dine.

[6] Phil Mattingly, “McConnell on the rationale for adding the individual mandate repeal to the tax plan, from the WSJ CEO Council event (via the great @ColinCNN),” Twitter, November 14, 2017, https://twitter.com/Phil_Mattingly/status/930539733947645953.

[7] Tax Policy Center table T17-0015.

[8] David Kamin, “Trade-Offs Made Clear in the Senate Bill,” Medium, November 15, 2017, https://medium.com/whatever-source-derived/trade-offs-made-real-in-the-senate-bill-b5176fff01aa.

[9] Sharon Parrott, “Congress Moves Toward Costly Tax Cuts, Setting Stage for Deep Budget Cuts,” Center on Budget and Policy Priorities, October 26, 2017, https://www.cbpp.org/blog/congress-moves-toward-costly-tax-cuts-setting-stage-for-deep-budget-cuts.

[10] Chuck Marr, “New Senate Child Credit Proposal Still Doesn’t Prioritize Families That Most Need It,” Center on Budget and Policy Priorities, November 15, 2017, https://www.cbpp.org/blog/new-senate-child-credit-proposal-still-doesnt-prioritize-families-that-most-need-it.

More from the Authors

Areas of Expertise