BEYOND THE NUMBERS

Housing Vouchers Work: Providing Stable Housing to Low-Wage Workers

This is the next post in our “Housing Vouchers Work” blog series, which provides the latest facts and figures about the Housing Choice Voucher program, the largest rental assistance program to help families with children, working people, seniors, and people with disabilities afford decent, stable housing.

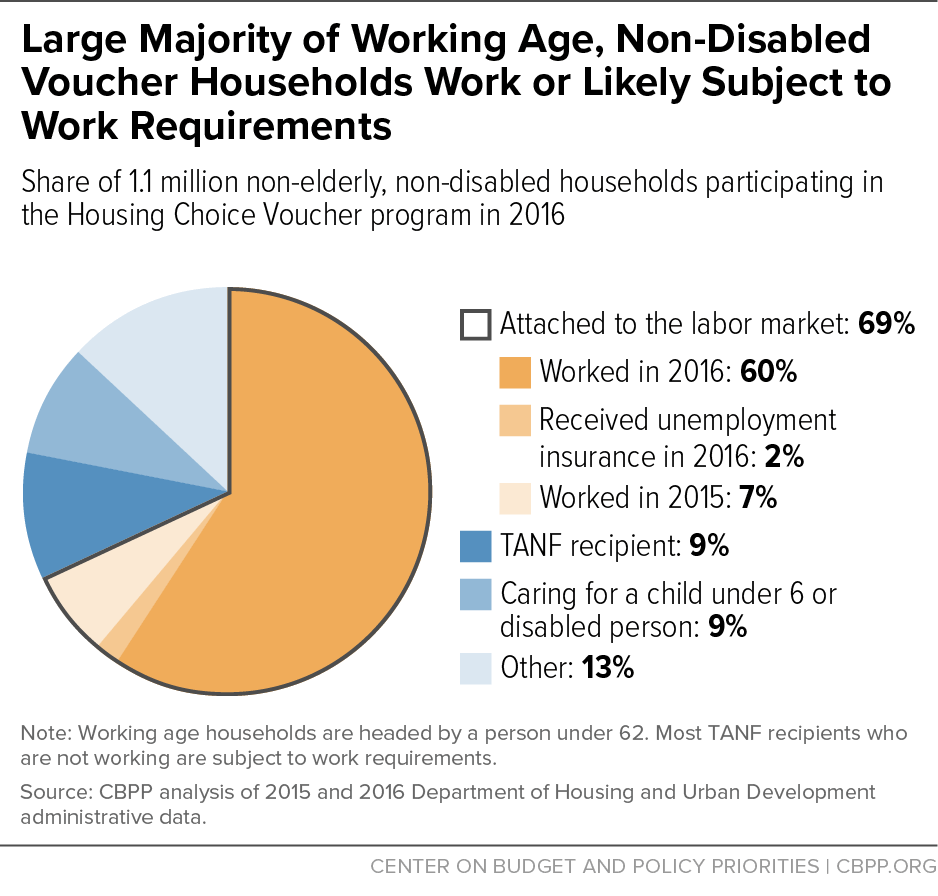

Vouchers help over 760,000 working households make ends meet. Most participants in the Housing Choice Voucher program who can reasonably be expected to work do so. In 2016, nearly 70 percent of non-disabled, working-age voucher households had at least one member who was working or had worked recently (see chart). Another 9 percent of households using vouchers were likely subject to a work requirement under the Temporary Assistance for Needy Families program.

Three-quarters of these working households are families with children. The typical working family with a voucher is headed by a 39-year-old woman with two school-age children. She earns roughly $17,000 annually or about $8.50 per hour for full-time work. (The Department of Housing and Urban Development does not collect data on hours worked.) That means she can only afford to pay about $400 per month for rent and utilities and still have enough money available to get to work and meet other essential costs. Without her voucher, she wouldn’t able to afford the market rent for a modest two-bedroom apartment anywhere in the country without paying over 30 percent of her monthly income (the federal standard for affordability).

Vouchers, like other federal rental assistance, support work by enabling families to live in stable homes and freeing up income to meet the additional costs of working, such as transportation. Uniquely, vouchers give households the flexibility to move to communities with access to better job opportunities. This may be why a larger share of voucher households work compared to their non-elderly, working-age counterparts in other housing programs.

Rents have been rising faster than incomes, making it increasingly difficult for low-income working families to keep a roof over their heads. More than 5 million low-income working households paid over half their income for housing in 2015. When housing costs consume such a great share of household income, low-income families are at greater risk of housing instability, getting evicted, or becoming homeless.

Despite rising numbers of low-income families struggling to pay rent and make ends meet, funding limitations leave 3 in 4 eligible households unable to receive federal rental assistance. Fully funding existing housing vouchers and raising the caps on non-defense discretionary spending (in which voucher funding is included) in 2018 would enable more working families to have a stable, affordable home.