Testimony of Will Fischer, Senior Policy Analyst, Before the Senate Banking Subcommittee on Housing, Transportation, and Community Development

Thank you for the opportunity to testify. I am Will Fischer, Senior Policy Analyst at the Center on Budget and Policy Priorities. The Center is an independent, nonprofit policy institute that conducts research and analysis on a range of federal and state policy issues affecting low- and moderate-income families. The Center’s housing work focuses on improving the effectiveness of federal low-income housing programs, and particularly the Section 8 housing voucher program.

It is commendable that the subcommittee is holding a hearing on streamlining and strengthening rental assistance. The proposed Affordable Housing and Self-Sufficiency Improvement Act (AHSSIA), Section 8 Savings Act (SESA), and Section 8 Voucher Reform Act (SEVRA) all contain important, timely measures to strengthen the voucher program and other major rental assistance programs. The reforms in these bills would sharply reduce administrative burdens for state and local housing agencies and private owners, establish voucher funding rules that would enable housing agencies to manage funds more efficiently, strengthen work supports, and generate large federal savings.

This testimony focuses on seven core reforms that should receive top priority for enactment. Each of these measures appears in some form in the version of AHSSIA circulated by the Financial Services Committee on April 13, 2012 and the version of SEVRA circulated by the Banking and Financial Services Committees on December 1, 2010.[1] These high-priority reforms would:

- Simplify rules for setting tenant rent payments, while continuing to cap rents at 30 percent of a tenant’s income;

- Streamline voucher housing quality inspections to encourage private owners to participate in the program;

- Establish a stable, fair voucher funding system to enable agencies to use funds more efficiently and better cope with shortfalls;

- Allow more working poor families to qualify for vouchers by modestly raising income targeting limits;

- Strengthen the Family Self-Sufficiency program, which offers housing assistance recipients job counseling and incentives to work and save;

- Provide added flexibility to “project-based” vouchers to support affordable housing development and preservation;

- Make the rental assistance admissions process fairer by limiting screening to criteria related to suitability as a tenant.

My testimony also discusses several other provisions that have been included in one or more of the reform bills.

Reform Would Build On Strengths of the Rental Assistance Programs

The nation’s rental assistance programs help more than four million low-income households afford decent housing. The great majority of these households are senior citizens, people with disabilities, and working poor families with children. As shown in the table attached to this testimony, rental assistance units are spread among the 50 states and across rural and urban areas.

Rigorous research has shown that rental assistance can sharply reduce the incidence of homelessness and housing instability — problems that have been shown to have serious harmful effects on children’s health and development.[2] Families that receive assistance to ease rent burdens also have more funds available for other basic needs, such as food, medication, child care, and transportation, and may be able to save or invest in education to help lift themselves out of poverty.[3]

Housing assistance produces positive indirect effects, as well. Studies suggest that work-promoting initiatives are more effective for families with affordable housing,[4] and a growing body of research suggests that stable, affordable housing may provide children with better opportunities for educational success.[5] Affordable housing combined with supportive services can help the elderly and people with disabilities retain their independence and avoid or delay entering more costly institutional care facilities.[6] The evidence of health care and other savings from providing affordable housing and services to homeless individuals with chronic health problems is particularly compelling.[7]

Research has found additional benefits when housing assistance enables low-income families to live in neighborhoods with lower poverty rates, including sharply fewer deaths from disease or accidents among girls and lower rates of obesity and diabetes.[8] Where housing policies have allowed low-income children to attend high-performing, economically integrated schools over the long term, their math and reading test scores are significantly better than comparable children who attended higher-poverty schools.[9]

The core reforms in SEVRA and AHSSIA would build on this record of success. Fourteen years have passed since the enactment of the Quality Housing and Work Responsibility Act (QHWRA) in 1998, the last major authorizing legislation affecting the voucher and public housing programs. As with any program, adjustments are needed over time to reflect changed circumstances and lessons learned.

Reforms that stretch limited dollars to assist more families or avoid painful cuts are especially urgent today, when budgets are tight but unemployment, poverty, and homelessness are high. The Congressional Budget Office (CBO) estimated that the December 2010 version of SEVRA would reduce the budget authority needed to fund the current level of housing assistance by more than $700 million over five years. Financial Services Committee staff have indicated that the April 2012 version of AHSSIA (which included additional cost saving measures) would save at least $1.5 billion. These estimates do not attempt to include administrative savings, which could lower funding needs by an added several hundred million dollars over five years.

Simplifying Rules for Determining Tenants’ Rent Payments

Tenants in HUD’s housing assistance programs generally must pay 30 percent of their income for rent, after certain deductions are applied. The rent streamlining provisions in AHSSIA and SEVRA maintain this rule, but would streamline determination of tenants’ incomes and deductions. As a result, the bills would reduce burdens on housing agencies, property owners, and tenants. The changes would also reduce the likelihood of errors in rent determinations and strengthen work incentives for tenants.

Most significantly, the bills would:

- Reduce the frequency of required income reviews. Currently, agencies and owners must review income annually for all tenants. AHSSIA and SEVRA would allow agencies and owners to limit reviews to once every three years for households that receive most or all of their income from fixed sources such as Social Security or SSI and consequently are unlikely to experience much income variation.[10]

Today agencies and owners also must adjust rents between annual reviews at the request of any tenant whose income drops. AHSSIA and SEVRA would require adjustments only when a family’s annual income drops by 10 percent or more, making such “interim” reviews less common but still providing adjustments when tenants would otherwise face serious hardship. The bills also would require interim adjustments for incomeincreases exceeding 10 percent, except that adjustments for earnings increases would be delayed until the next annual review to strengthen work incentives.

Together, these changes would sharply reduce the number of income reviews that agencies and owners must conduct. This would substantially lower administrative costs, since income reviews are among the most labor-intensive aspects of housing assistance administration. - Simplify deductions for the elderly and people with disabilities. Currently, if the household head (or his or her spouse) is elderly or has a disability, housing agencies and owners must deduct medical expenses and certain disability assistance expenses above 3 percent of the household’s income from income for purposes of determining the household’s rent. Agencies and owners report that this deduction is difficult to administer, since they must collect and verify receipts for all medical expenses. It also imposes significant burdens on elderly people and people with disabilities, who must compile and submit receipts that may contain highly personal information. Largely for these reasons, many households eligible for the deduction do not receive it. By contrast, a second deduction targeted to the same groups — a $400 annual standard deduction for each household where the head or spouse is elderly or has a disability — is quite simple to administer.

AHSSIA and SEVRA would increase the threshold for the medical and disability assistance deduction from 3 percent of annual income to 10 percent. This would reduce the number of people eligible for the deduction — and therefore the number of itemized deductions that would need to be determined and verified — while still providing some relief for tenants with extremely high medical or disability assistance expenses. At the same time, the bills would increase the easy-to-administer standard deduction for the elderly and people with disabilities, to $675 annually in SEVRA and $525 annually in AHSSIA, and index it for inflation.

In addition to reducing processing burdens for agencies, owners, elderly people, and people with disabilities, this change is likely to reduce payment errors substantially. HUD studies have found that the medical and disability expense deduction is one of the most error-prone components of the rent determination process, while errors in the standard deduction are rare.

The higher $625 standard deduction in SEVRA would be preferable, since it would come closer to fully offsetting rent increases (on average across all families) from the scaled back medical expense deduction (although it would also result in somewhat lower savings). Some individual households would see higher or lower monthly rents, but the changes would generally be modest. Congress could provide added protection for tenants who are adversely affected by allowing HUD to establish a hardship exemption policy (as AHSSIA would do) and delaying the effective date of the change to allow tenants to find other ways to cover out-of-pocket medical expenses. - Simplify deductions for families with children. AHSSIA and SEVRA would scale back an existing deduction for child care expenses — which evidence suggests is implemented inconsistently — by allowing deductions only of expenses above 5 percent of income (rather than all reasonable expenses). At the same time, it would increase from $480 to $525 a simple annual deduction that families receive for each child or other dependent, and index it for inflation. The dependent deduction recognizes the larger share of family income required to cover non-shelter expenses when a family has more children.

- Base rents on a tenant’s actual income in the previous year. Currently, rents are based on a tenant’s anticipated income in the period that the rent will cover, usually the coming 12 months. Except when a family first begins receiving housing assistance, AHSSIA and SEVRA would require agencies generally to base rents on actual income in the previous year. This would give tenants an incentive to increase their earnings, since such an increase would not affect their rent for as long as a year. It also would simplify administration, both by making it easier for agencies and owners to use tax forms and other year-end documentation to verify income and by reducing the need for mid-year rent adjustments for tenants whose earnings change during the year.

- Limit utility allowances based on family size and composition. AHSSIA contains a provision to limit utility allowances in the voucher program based on the number of bedrooms a family is eligible for given its composition, rather than the actual size of the unit. Today families are permitted to rent units larger than they are eligible for, but the cap on the total housing costs the voucher covers (that is, the payment standard) does not rise as a result. Adopting the AHSSIA limit on utility allowances would generate savings and avoid providing families incentives to rent larger units than they need.

- Allow housing agencies to use income data gathered by other programs. AHSSIA and SEVRA contain a provision that would allow state and local housing agencies and owners to rely on income determinations carried out under SNAP (formerly food stamps) and other federal means-tested programs, without separate verification. Currently, housing agencies and owners must determine and verify income independently, even though this duplicates work already being carried out by other agencies. Allowing housing agencies to rely on income determinations made by SNAP agencies would ease their administrative burdens considerably, since a large portion of housing assistance recipients also receive SNAP benefits.

AHSSIA, however, does not include a provision from the December 2010 version of SEVRA requiring state SNAP agencies to make available to housing agencies income data for families participating in both programs. It is important that Congress include this requirement, since without it many SNAP agencies may not provide the needed data.

Flat Rent Changes Offer Promising Way to Raise Revenues

To encourage a mixture of incomes among public housing residents, current law permits residents to elect to pay a “flat rent.” This policy benefits residents with the highest incomes (who pay less than 30 percent of their income for housing under the policy) but has been considered reasonable because HUD rules require that flat rents be set at the “estimated rent for which the [agency] could promptly lease the public housing unit” — that is, at the approximate market rent. Data suggest, however, that existing flat rents are well below market rents in some areas, which raises federal costs and can increase funding shortfalls for local agencies.

AHSSIA includes a statutory change proposed in the Administration’s 2012 budget to require agencies to set flat rents no lower than 80 percent of the HUD fair market rent for the area.[11] HUD estimates that the provision would reduce public housing operating subsidy needs by $150 million in the first year and by more than $400 million per year once the proposal is fully phased in.

As proposed by HUD, AHSSIA would require local agencies to implement the new policy no later than September 30, 2013, which would allow agencies some time to phase the policy in. In addition, the bill limits any increases in rental payments by affected households to 35 percent per year.

Minimum Rent Increase Would Harm the Poorest Tenants

The April version of AHSSIA contains a provision not included in SEVRA increasing to $69.45 a month the “minimum rents” that the lowest income housing assistance recipients can be required to pay, and indexing this amount for inflation. Under current law, housing agencies have the option of setting minimum rents for voucher holders and public housing residents up to $50. HUD also has authority to set minimum rents up to $50 in project-based Section 8 units, and currently has set that level at $25.

The April AHSSIA provision makes two significant improvements over the minimum rent proposal in the earlier version of AHSSIA that a House Financial Services subcommittee passed on February 7, 2012:

- The subcommittee-passed bill would have required all housing agencies and owners to charge minimum rents of $69.45, eliminating the discretion that exists under current law. By contrast the April AHSSIA provision would permit housing agencies and owners to set minimum rents below $69.45 for “good cause,” unless HUD disapproves the lower rent.

- The subcommittee-passed bill made no significant changes to existing protections for families that would face hardship if they were required to pay minimum rents. A 2010 HUD-sponsored study found that these protections help few families: 82 percent of agencies reported providing exemptions to less than 1 percent of families subject to minimum rents, and only 5 percent of agencies said they had exempted more than a tenth of affected families.[12] The April AHSSIA bill improves the hardship requirements to increase the chances that poor families facing hardship will be exempted.

Despite these improvements, the April AHSSIA provision is still likely to harm many of the nation’s most vulnerable families and individuals. As many as 500,000 households could be required to pay higher rents, including families with 725,000 children. While the improvements described above would protect some families, many are still likely to fall through the cracks, placing them at risk of severe hardship and even homelessness. Moreover, it is not clear what the rationale for the increase is. Congress should omit it in final rental assistance reform legislation.

Rent Demonstration Could Be Useful, but Restrictions Should Be Tightened

AHSSIA and SEVRA would authorize HUD to conduct a limited demonstration of alternative rent policies. Such a demonstration is potentially beneficial. Today’s rent rules generally work well, providing sufficient help to enable the neediest families to afford housing while not giving higher-income families more subsidy than they need. In addition, the current system maintains largely identical rules across programs and localities, making it easier for voucher holders to move from one community to another (for example to pursue a job opportunity), for private-sector owners and investors to participate in multiple programs and operate in multiple jurisdictions, and for HUD to provide effective oversight.

Most major changes — and particularly those that would result in sharply higher or lower subsidies for certain families — would carry substantial risks and tradeoffs. It is possible, however, that some substantial changes would have significant benefits that would justify enacting them on the federal level. For example, a policy of disregarding some percentage of earned income would carry added costs, but might encourage sufficient increases in earnings to offset a sizable share of the cost and justify the change. A demonstration could offer an opportunity to rigorously test policy alternatives to determine their costs and benefits relative to the current rules. HUD is already conducting a rent demonstration at a subset of MTW agencies, but would need additional statutory authority to extend it to other agencies.

However, the rent demonstration in AHSSIA and SEVRA should be strengthened in important ways. It should provide HUD broader flexibility to identify promising policies, limit the length of the demonstration to avoid allowing wasteful or harmful policies to remain in place indefinitely, explicitly require an experimental evaluation, and clarify that the “limited” number of families that can be subject to alternative policies should be no more than the number needed to yield statistically valid results.

Streamlining Inspections to Encourage Participation by Private Owners

The voucher program requires that vouchers be used only in houses or apartments that meet federal quality standards. AHSSIA and SEVRA would allow agencies to modestly change the inspection process used to ensure that units meet those standards. The changes would ease burdens on agencies and encourage landlords to rent apartments to voucher holders.

Most significantly, AHSSIA and SEVRA would allow agencies to inspect apartments every two years instead of annually. In addition, the bills would allow agencies to (1) rely on recent inspections performed for other federal housing programs, and (2) make initial subsidy payments to owners even if the unit does not pass the initial inspection, as long as the failure resulted from non-life-threatening conditions. Defects would have to be corrected within 30 days of initial occupancy for the payments to continue. These provisions would encourage owners to participate in the voucher program by minimizing any financial loss due to inspection delays. They also would enable voucher holders, who in some cases are homeless or experience other severe hardship, to move into the unit more quickly than under current rules.

Today, when an inspection of a unit occupied by a voucher holder finds a violation, the housing agency is permitted to temporarily halt subsidy payments if the owner fails to address the violation in a timely manner, and ultimately terminate the subsidy if the defects are not adequately repaired. AHSSIA and SEVRA would retain this authority and establish a series of requirements regarding the rights of tenants and other aspects of subsidy abatement and termination.

SEVRA also includes a beneficial requirement, which Congress should enact, for housing agencies to provide assistance to help tenants find a new unit and relocate if the subsidy to their unit is terminated because of an inspection violation. AHSSIA would make this assistance optional.

Stabilizing Voucher Funding Rules

One of the most important goals of authorizing legislation concerning the voucher program should be to establish a stable, fair, efficient policy for distributing funds to renew voucher subsidies to the approximately 2,400 state and local agencies that administer the program. This would enable those agencies to assist more families within the level of resources provided in annual appropriations bills than would otherwise be possible.

For the last nine years, appropriations acts have changed renewal funding policies every several years. Such instability creates uncertainty and makes many agencies reluctant to use the funds they have to serve the number of families Congress has authorized, out of fear that they will not receive sufficient renewal funding to maintain payments to landlords. As a result, only about 92 percent of authorized vouchers are in use, compared to about 97 percent before the changes in renewal funding policy began — a loss of assistance to about 100,000 families. The reform bills include a package of changes that would stabilize and strengthen renewal funding policy.

- Stable funding formula. AHSSIA and SEVRA would establish as a permanent part of authorizing law the policy in recent appropriations bills of basing each agency’s funding on the cost of the vouchers it used in the previous year, adjusted for inflation and certain other factors. This approach forces agencies to manage within a limited budget, while also ensuring that each agency’s funding level matches its actual needs.

- Stable reserve and offset policy. AHSSIA and SEVRA would assure state and local housing agencies that they can maintain a funding reserve of at least 6 percent of the renewal funding for which they are eligible, but permit HUD to “offset” (that is, deduct from the agency’s funding) reserves above that level. AHSSIA improves on the SEVRA offset policy by extending it to cover MTW agencies in addition to non-MTW agencies; this avoids unfairly disadvantaging non-MTW agencies.

In the current funding environment, when agencies may fear that Congress will not provide sufficient new funding to support all vouchers in use, a predictable reserve level provides the cushion agencies need to reissue vouchers to needy applicants on the waiting list when families leave the program and be confident that they will have sufficient funds to sustain the vouchers. At the same time, making clear that HUD will have authority to offset reserves beyond the permitted amount provides a strong incentive for agencies to put excess funds to use assisting families. - Permitting agencies to assist as many families as possible with available funds. AHSSIA and SEVRA would encourage agencies to reduce the cost of voucher subsidies and stretch their voucher funds to serve as many families as possible by restoring flexibility that existed prior to 2003 to assist families beyond the agency’s “authorized voucher cap.” Under a policy adopted in annual appropriations acts since 2003, agencies are penalized if they use more than their authorized number of vouchers in a year, even if they can do so with available funds by reducing per-voucher costs. This policy has pushed many agencies to use substantially fewerthan their authorized number of vouchers, out of fear of exceeding the cap.

AHSSIA and SEVRA would remove this chilling effect and assure agencies that if they took steps to limit costs, they could use any savings to provide vouchers to more families even if this pushes them above their authorized voucher level. Vouchers above the authorized level that are supported by unused prior-year funds would not be counted for determining the agency’s future funding level, so this incentive would not increase program costs. - Efficient use of funds above renewal formula amounts. When Congress passes appropriations bills in a timely manner, it sets the voucher funding level before all the data needed to know the precise amount agencies will be eligible for under the renewal formula are available. In recent years, when funding has exceeded the amount needed HUD has been required to distribute the extra funds pro-rata to all agencies. HUD could use these funds more efficiently if it had authority to allocate them to meet unforeseen needs, reward high performance, or for other purposes. SEVRA provides HUD broad authority to make such allocations, while AHSSIA provides more limited discretion. The SEVRA provision would be preferable, but Congress should enact at least the AHSSIA provision.

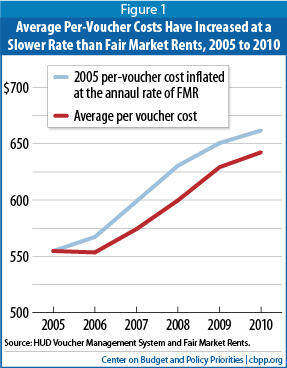

Per-Voucher Costs Have Risen More Slowly than Housing Costs in the Private Market

While AHSSIA and SEVRA would create important incentives to keep per-voucher costs low, it is important to note that this would build on the voucher program’s already successful record of restraining costs. Per-voucher costs have generally risen at a slower rate than housing costs in the private market. HUD-determined Fair Market Rents (FMRs), which are based in market rents for standard-quality unassisted units, increased by 19 percent from 2005 to 2010. As shown in figure 1, during that same period per-voucher costs increased by less than 16 percent.

A central reason for this is that housing agencies controlled voucher costs through their ability to set payment standards, which cap voucher subsidies and can be set anywhere from 90 to 110 percent of the FMR (and outside that range under some circumstances). This explanation receives support from HUD data showing that, on average, voucher payment standards declined in relation to FMRs from 2005 to 2010.

By incorporating an improved voucher renewal funding policy in permanent law, AHSSIA and SEVRA would provide agencies — as well as families with vouchers and private owners — with more confidence that renewal funding needs will be met in future years, which is particularly important to maintain program effectiveness in the current fiscal environment. This approach would not weaken Congress’s control over the cost of the program. Congress would still determine the amount of annual program funding, and if the funds appropriated in a given year were insufficient to fully fund the renewal formula, HUD would reduce each agency’s funding by the same percentage so funds would still be allocated based on agencies’ relative needs. The provisions in the bills would simply ensure that, for any given level of funding, more families would receive the important benefits that vouchers have been shown to provide.

Easing Income Targeting Rules to Help More Working-Poor Families

Currently, 75 percent of vouchers and 40 percent of project-based Section 8 and public housing units must be allocated to households with incomes at or below 30 percent of the median income in the local area at the time they enter the program. AHSSIA and SEVRA would adjust these criteria to require that those vouchers and units be allocated to households with incomes at or below 30 percent of local median income or the federal poverty line, whichever is higher. Neither this revised requirement nor current law restricts a family’s income after it is admitted.[13]

This change would give housing agencies greater flexibility to target working-poor families. Some agencies in low-income areas have expressed concern that the current targeting criteria prevent them from assisting these families. At the same time, the change would maintain the emphasis on assistance for the poor. CBO has estimated that the reduction in subsidy needs that would result from easing targeting rules would reduce funding needs by $1.14 billion over five years, making it the largest source of savings in the bills.

The only difference between the bills’ targeting provisions is that AHSSIA fixes language in SEVRA that could allow targeting in project-based Section 8 developments in Puerto Rico and other U.S. territories to be raised excessively. The federal poverty line is not designed to apply in U.S. territories, and using it to target housing assistance there would raise the targeting threshold far above 30 percent of the local median income and shift assistance away from the neediest families. For this reason, both AHSSIA and SEVRA seek to exempt the territories from the targeting change, but the SEVRA exemption applies only to “in the case of public housing agencies” located in a U.S. territory. This would allow sharp targeting increases in project-based Section 8 developments, which generally are not administered by public housing agencies. Congress should adopt the more complete AHSSIA exemption.

Strengthening the Family Self-Sufficiency Program

The Family Self-Sufficiency (FSS) program encourages work and saving among voucher holders and public housing residents through employment counseling and financial incentives. Both AHSSIA and SEVRA establish a stable formula to allocate funds to cover administrative costs of FSS programs. This formula would replace a competitive process that has made funding unpredictable and disrupted administration of local FSS programs.

Unfortunately, residents of units assisted through the project-based Section 8 program are ineligible for FSS today. AHSSIA (but not SEVRA) corrects this omission, enabling families receiving any type of Section 8 assistance as well as public housing residents to benefit from FSS. Offering participation in the FSS program to project-based Section 8 tenants would be optional for property owners. Generally, such tenants would participate in an FSS program operated by a public housing agency, if one is available that will admit the families. Owners of properties with project-based Section 8 contracts could also use funds in their HUD-required “residual receipts accounts” to operate an FSS program independently if it serves at least 25 participants.

AHSSIA also contains other beneficial FSS provisions, including a requirement that housing agencies with 500 or more voucher and public housing units offer or expand FSS programs if sufficient funds are available.

Facilitating Use of Project-Based Vouchers

Both AHSSIA and SEVRA would make it easier for a housing agency to enter into agreements with owners for a share of its vouchers to be used at a particular housing development. Through such “project-basing,” agencies can, for example, partner with social service agencies to provide supportive housing to formerly homeless people or support development of mixed-income housing in low-poverty neighborhoods with strong educational or employment opportunities.

Residents of units with project-based voucher assistance have the right to move with a voucher after one year, using the next voucher that becomes available when another family leaves the program. (When this occurs, a voucher remains attached to the housing development; the family moving out of the development receives a separate voucher.) This “resident choice” feature and other policies make the project-based voucher option significantly different from earlier programs that provided project-based assistance.

AHSSIA and SEVRA increase the percentage of an agency’s voucher assistance that can be project-based from 20 percent to 25 percent, if the added 5 percent is used in areas where vouchers are difficult to use, to house homeless families or individuals, or to provide supportive housing to people with disabilities. AHSSIA adds units that house veterans or the elderly to the categories that qualify for this added authority. In SEVRA, agencies would be permitted to project-base the higher of 25 percent of their authorized vouchers or 25 percent of their voucher funding, giving greater flexibility to housing agencies that are able to keep project-based voucher costs low. AHSSIA would base the limit strictly on the percentage of the agency’s authorized vouchers.

In addition, the bills would permit housing agencies to commit to project-based voucher contracts with a term of 20 years (the term HUD permits for contracts under the separate project-based Section 8 program), rather than the 15-year maximum permitted today. The bills would also permit owners to establish and maintain site-based waiting lists subject to civil rights and other requirements, allow agencies to provide project-based vouchers in the greater of 25 percent of units or 25 units in a project, and permit 40 percentof the units in a project to have project-based vouchers in areas where vouchers are difficult to use or the poverty rate is 20 percent or less.[14] These policy changes would help agencies increase the effectiveness of the voucher program in rural and suburban areas, where rentals are frequently scarce and properties tend to be small, and in low-poverty areas in all types of locations.

Protection Against Arbitrary Screening of Housing Assistance Recipients

Housing agencies and owners must screen housing assistance applicants based on several federally required criteria, and can opt to establish additional screening criteria. AHSSIA and SEVRA would make several changes to the screening process for the housing voucher program, including limiting optional screening criteria to those directly related to the family’s ability to meet the obligations of the lease and requiring housing agencies to consider mitigating factors before denying assistance. These important improvements would prevent, for example, denial of assistance to a family with a good record of paying rent on time but (like many poor families) a weak credit history for other reasons, and would make it easier to provide housing vouchers to homeless people and others with an urgent need for assistance who today might be denied help for arbitrary reasons.

Unfortunately, the current AHSSIA draft drops a provision of some versions of SEVRA that would have made similar (and equally important) changes in the public housing and project-based Section 8 programs. Congress could extend the changes to those programs by restoring the omitted provisions or simply by giving HUD authority to establish common requirements for all rental assistance programs.

Both AHSSIA and SEVRA also would add an important protection for families being shifted from assistance under the public housing or HUD multifamily programs to housing vouchers due to the elimination of the existing assistance for the properties in which they reside. The bills recognize that such families are not new to HUD assistance and should be considered continuing participants rather than new applicants subject to initial screening. In addition to protecting families, these changes also would reduce administrative burdens for housing agencies.

Other Provisions

In addition to these seven core reforms, a series of other provisions appear in SEVRA, AHSSIA, or both. Several of these provisions are discussed below:

- Local flexibility to adjust voucher payments to accommodate the special needs of people with disabilities. Housing agencies today can allow people with disabilities to use vouchers to rent more expensive units than is permitted for other families, if this is necessary to accommodate their disability. If this requires a payment standard above 110 percent of the FMR, however, the agency must obtain special approval from HUD. This can create delays that make it much more difficult for people with disabilities to use vouchers. Accessible units are often more costly than a typical unit in an area, either because few such units exist or because they require added investments by owners.

SEVRA and AHSSIA would allow agencies to provide exceptions up to 120 percent of the FMR for this purpose without approval from HUD. Because these exceptions would be needed for only a small share of vouchers, this important provision’s cost would be minimal. - Use of vouchers in manufactured housing. AHSSIA drops a beneficial SEVRA provision that would allow vouchers to be used to cover loan payments, insurance payments, and other periodic costs of buying a manufactured home, in addition to the cost of renting a space on which to place the home. The combined payments would, however, be subject to the same subsidy limits that apply to other vouchers.

Currently, vouchers can be used to cover the full range of periodic homeownership costs for the purchase of a traditional home or a manufactured home set on land also purchased by the family. But if a family rents the space for a manufactured home, which is common in some states, the voucher subsidy is limited to about 40 percent of the assistance it could otherwise provide, and can only cover the space rental costs and not the costs of purchasing the home. The SEVRA provision would allow vouchers to be used effectively in a segment of the housing market that in some areas is the most readily available source of affordable housing — and that for many families offers the most realistic avenue to homeownership. - Fair Market Rents. AHSSIA and SEVRA contain identical provisions that would make modest improvements to the process for setting FMRs by streamlining HUD’s FMR determination process and giving housing agencies added authority to protect families from rent increases stemming from FMR reductions.

- Rental Assistance Demonstration. AHSSIA would authorize $150 million for a five-year Rental Assistance Demonstration (RAD) testing the conversion of public housing and Section 8 moderate rehabilitation units to project-based vouchers or Section 8 project-based rental assistance, and $50 million for similar conversions of units from the Rent Supplement program or Rental Assistance Program to Section 8 project-based rental assistance.

RAD offers a promising approach to preservation of needed subsidized housing. HUD has just issued a final notice to implement a version of RAD approved the 2012 HUD appropriations act. The AHSSIA RAD provision’s most important improvement over the existing version of RAD is that it would permit public housing units to receive subsidy levels capped under regular Section 8 rules rather than limiting subsidies to the amount the units received through public housing prior to conversion. This would make RAD a more effective and flexible tool, but only if appropriators provided the needed funds — a step they were unwilling to take in the 2012 act. - Economic Security Demonstration. AHSSIA contains a provision not included in SEVRA directing HUD to carry out a demonstration to rigorously evaluate options for helping to increase the economic security of housing assistance recipients, including financial incentives, work requirements, and other interventions, and authorizes $25 million for this purpose. Such a demonstration could generate important information about the effectiveness of policies to promote economic security. If Congress enacts it, however, it should specify that new policies may remain in place only during the demonstration or until otherwise allowed by Congress, to avoid leaving harmful policies in place indefinitely.

- Moving-to-Work. The version of AHSSIA passed by a House Financial Services Subcommittee in February 2012 contained a harmful provision permitting an unlimited expansion of the Moving to Work (MTW) demonstration, which currently exempts 35 housing agencies from nearly all federal housing laws and regulations. This would risk deep cuts to housing assistance over time (due to the block grant funding formula used in MTW) and harmful policy changes, such as sharp rent increases on vulnerable families or time limits on assistance even for working poor families who cannot afford to stay in their homes without help. Moreover, the sweeping scale of the expansion would make it impossible to address a key shortcoming of the existing MTW demonstration — that it has permitted risky policy changes without carefully evaluating them to determine their true impact.[15]

The April version of AHSSIA also contains a large-scale MTW expansion, but the expanded program would be subject to significant limitations. These include prohibitions on waivers of some key tenant protections and requirements for rigorous evaluation of the riskiest policies. If Congress enacts an MTW expansion as part of reform legislation, it is essential that it be subject to the limitations in the April AHSSIA bill.

It should be noted however, that even with these limitations MTW expansion would still pose serious risks. Most importantly, the April AHSSIA bill would allow large (though capped) shifts of funds from the voucher program to other purposes, raising the risk that the expansion would result in many fewer needy families receiving housing assistance than would be assisted under regular program rules. Moreover, the goals of MTW, such as testing alternative policies and streamlining program administration, can be pursued effectively through other, less risky approaches. Consequently, even the more limited MTW expansion in the April AHSSIA bill can be justified only if it is critical to the enactment of comprehensive legislation containing most or all of the important reforms discussed earlier in this testimony.

Conclusion

The core provisions of AHSSIA and SEVRA would build on the voucher program’s many strengths through a series of measured, targeted improvements that, taken together, would deliver important benefits to housing agencies, private owners, and low-income families. Moreover, because several of the bills’ provisions extend beyond the voucher program, they also would improve the public housing and project-based Section 8 programs.

It is important that Congress expeditiously enact rental assistance reform legislation with these key provisions. The need for housing assistance is unusually high today, with elevated levels of homelessness and poverty and widespread foreclosures. Yet Congress appears unlikely to expand resources for housing assistance substantially, and is likely to consider substantial cuts — on top of the sharp reductions enacted in recent years to voucher administrative fees, public housing capital grants, and other housing programs.

At this time, the nation needs its housing assistance programs to be as efficient and effective as possible, and the measures in AHSSIA and SEVRA would take major steps toward that goal. The bills’ core provisions have been fully vetted through deliberations in the past four congressional sessions, and it is urgent that Congress enact them this year so that the large federal savings they would generate — as well as their many other benefits — can begin to be realized.

HUD Rental Assistance in Rural and Urban Areas

February 13, 2012

The federal government’s three largest rental assistance programs — Section 8 Housing Choice Vouchers, Public Housing, and Multifamily Assisted units — provide over 4.4 million units of assisted housing, 633,000, or 14 percent, of which are located outside of metropolitan areas. In addition to these programs administered by the Department of Housing and Urban Development (HUD), the U.S. Department of Agriculture’s Rural Housing Service provides rental assistance to 265,000 households.a

According to HUD’s most recent report, 84 percent of renters with “worst-case” housing needs live in central cities or suburbs, while 16 percent live in non-metropolitan areas.b While the number of federally-assisted affordable rental units is only sufficient to serve about one in four eligible families,c their distribution across metropolitan and non-metropolitan areas is in close proportion to relative need.

| HUD-Funded Rental Assistance | ||||||

| State | Housing Choice Vouchers | Public Housing Units | Multifamily Assisted Housing Unitsd | |||

| Non-Metro | Metro | Non-Metro | Metro | Non-Metro | Metro | |

| Total | 228,304 | 1,783,180 | 188,151 | 869,305 | 216,557 | 1,154,853 |

| Percentage | 11% | 89% | 18% | 82% | 16% | 84% |

| Alaska | 953 | 3,362 | 351 | 770 | 372 | 1,578 |

| Alabama | 4,982 | 23,308 | 12,451 | 25,355 | 4,359 | 14,854 |

| Arkansas | 8,906 | 11,111 | 7,610 | 5,773 | 12,810 | 1,328 |

| Arizona | 817 | 19,521 | 281 | 6,308 | 569 | 8,806 |

| California | 3,861 | 283,552 | 327 | 39,256 | 2,635 | 112,705 |

| Colorado | 2,864 | 26,461 | 1,553 | 6,491 | 3,915 | 13,534 |

| Connecticut | 1,266 | 30,273 | 464 | 14,044 | 1,891 | 25,315 |

| District of Columbia | - | 8,797 | - | 8,067 | - | 13,437 |

| Delaware | - | 3,668 | 101 | 2,356 | 901 | 4,675 |

| Florida | 5,538 | 86,855 | 2,253 | 30,808 | 2,151 | 50,369 |

| Georgia | 4,971 | 47,235 | 14,168 | 27,981 | 5,963 | 23,801 |

| Hawaii | 2,873 | 4,421 | 1,130 | 4,142 | 1,355 | 3,213 |

| Iowa | 8,902 | 11,774 | 3,081 | 1,216 | 5,101 | 8,489 |

| Idaho | 1,332 | 5,221 | 322 | 427 | 1,531 | 2,769 |

| Illinois | 3,884 | 58,421 | 13,918 | 41,130 | 6,912 | 64,633 |

| Indiana | 5,323 | 28,971 | 2,253 | 13,726 | 6,694 | 29,436 |

| Kansas | 2,400 | 9,086 | 4,045 | 4,963 | 4,178 | 8,474 |

| Kentucky | 8,909 | 21,326 | 10,741 | 11,083 | 9,912 | 13,772 |

| Louisiana | 5,962 | 37,313 | 6,763 | 12,721 | 4,627 | 16,073 |

| Massachusetts | 18 | 71,999 | - | 31,772 | 133 | 67,447 |

| Maryland | 1,981 | 38,739 | 367 | 19,093 | 1,175 | 32,643 |

| Maine | 4,023 | 7,874 | 787 | 3,274 | 3,086 | 6,024 |

| Michigan | 7,254 | 45,358 | 4,886 | 17,625 | 7,928 | 55,281 |

| Minnesota | 5,137 | 25,152 | 5,349 | 15,668 | 9,461 | 26,417 |

| Missouri | 6,152 | 31,590 | 5,816 | 11,097 | 4,764 | 25,411 |

| Mississippi | 9,242 | 11,814 | 10,292 | 2,261 | 11,396 | 7,046 |

| Montana | 2,398 | 2,709 | 1,069 | 888 | 2,412 | 2,293 |

| North Carolina | 15,777 | 36,674 | 11,463 | 21,919 | 9,856 | 20,726 |

| North Dakota | 2,351 | 4,213 | 762 | 1,071 | 2,239 | 1,085 |

| Nebraska | 2,737 | 8,535 | 3,869 | 3,369 | 3,756 | 3,365 |

| New Hampshire | 2,686 | 6,167 | 875 | 3,193 | 3,632 | 3,381 |

| New Jersey | - | 60,107 | - | 37,154 | - | 49,621 |

| New Mexico | 3,143 | 7,884 | 1,854 | 1,916 | 2,783 | 4,312 |

| Nevada | 1,041 | 12,024 | - | 3,860 | 515 | 3,812 |

| New York | 11,127 | 200,486 | 4,966 | 204,372 | 6,641 | 126,913 |

| Ohio | 13,718 | 75,810 | 4,637 | 41,929 | 11,372 | 67,637 |

| Oklahoma | 4,084 | 19,722 | 5,062 | 7,059 | 5,291 | 9,573 |

| Oregon | 7,451 | 24,941 | 570 | 4,833 | 2,581 | 8,720 |

| Pennsylvania | 8,820 | 61,377 | 7,988 | 52,783 | 8,024 | 55,163 |

| Rhode Island | - | 8,577 | - | 9,284 | - | 16,347 |

| South Carolina | 4,248 | 19,621 | 3,683 | 9,376 | 5,496 | 15,210 |

| South Dakota | 2,168 | 3,133 | 903 | 645 | 3,540 | 2,686 |

| Tennessee | 4,324 | 29,083 | 10,790 | 24,069 | 7,300 | 27,660 |

| Texas | 13,775 | 127,479 | 10,733 | 38,543 | 7,656 | 56,204 |

| Utah | 571 | 9,798 | 147 | 1,630 | 402 | 4,472 |

| Virginia | 4,874 | 36,215 | 1,369 | 17,363 | 5,015 | 30,935 |

| Vermont | 2,981 | 3,005 | 1,247 | 581 | 2,409 | 1,566 |

| Washington | 3,325 | 41,505 | 1,262 | 13,013 | 2,188 | 17,490 |

| Wisconsin | 3,990 | 22,274 | 3,790 | 9,137 | 7,543 | 25,459 |

| West Virginia | 4,550 | 7,223 | 1,468 | 3,570 | 5,329 | 5,983 |

| Wyoming | 615 | 1,416 | 355 | 341 | 1,749 | 942 |

Notes

a This is the number of units receiving assistance under the USDA Section 521 rental assistance program; see the fact sheet at

.b “Worst Case Housing Needs 2009: A Report to Congress,” U.S. Department of Housing and Urban Development, Office of Policy Development and Research, February 2011. HUD defines households with “worst-case” needs as unassisted renters with incomes below 50 percent of the local area median income who paid more than one-half of their income for rent or lived in severely inadequate housing conditions.

c See Douglas Rice and Barbara Sard, “Decade of Neglect Has Weakened Federal Low-Income Housing Programs,” Center on Budget and Policy Priorities, February 2009, https://www.cbpp.org/cms/index.cfm?fa=view&id=2691 .

d Multifamily includes Section 8 New Construction or Substantial Rehabilitation (including 202/8 projects), and all other multifamily assisted projects with FHA insurance or HUD subsidy (including Section 8 Loan Management, Rental Assistance Program (RAP), Rent Supplement, Property Disposition, Section 202/811 capital advance and Preservation).

For additional explanation of the methodology used for these estimates, see .

End Notes

[1] My testimony focuses on these versions — the most recent public version of each bill — except where otherwise noted. Since SESA was circulated by the current leadership of the House Financial Services Committee earlier in this Congress, I generally focus on the committee’s later AHSSIA bill instead. A detailed side-by-side comparing AHSSIA, SEVRA, and current law is available at https://www.cbpp.org/sites/default/files/atoms/files/5-10-12-SEVRA-AHSSIA-CurrentLaw-Comparison.pdf.

[2] Diana Becker Cutts, MD, “US Housing Insecurity and the Health of Very Young Children,” American Journal of Public Health, August 2011, Vol. 101, No. 8, p. 1508; Michelle Wood, Jennifer Turnham and Gregory Mills, “Housing Affordability and Well-Being: Results from the Housing Voucher Evaluation,” Housing Policy Debate 19:367-412 (2008).

[3] Joint Center for Housing Studies of Harvard University, “America’s Rental Housing: Meeting Challenges, Building on Opportunities,” April, 2011, p. 5 and table A-9, http://www.jchs.harvard.edu/sites/jchs.harvard.edu/files/americasrentalhousing-2011.pdf.

[4] James A. Riccio, “Subsidized Housing and Employment: Building Evidence of What Works,” in Nicolas P. Retsinas and Eric S. Belsky, eds., Revisiting Rental Housing, Joint Center for Housing Studies and Brookings Institution Press, 2008.

[5] Maya Brennan, “The Impacts of Affordable Housing on Education: A Research Summary,” Center for Housing Policy, May 2011, http://www.nhc.org/media/files/Insights_HousingAndEducationBrief.pdf.

[6] Gretchen Locke, Ken Lam, Meghan Henry, Scott Brown, “End of Participation in Assisted Housing: What Can We Learn About Aging in Place?” Abt Associates Inc., February 2011, available at: http://www.huduser.org/publications/pdf/Locke_AgingInPlace_AssistedHousingRCR03.pdf.

[7] For summaries of findings and references, see U.S. Interagency Council on Homelessness, “Opening Doors: Federal Strategic Plan to Prevent and End Homelessness, 2010”, pp. 18-19, http://www.usich.gov/PDF/OpeningDoors_2010_FSPPreventEndHomeless.pdf; and Michael Nardone, Richard Cho and Kathy Moses, Medicaid-Financed Services in Supportive Housing for High-Need Homeless Beneficiaries: The Business Case,” Center for Health Care Strategies, Inc., June 2012, available at http://www.rwjf.org/files/research/74485.business.case.pdf.

[8] Jens Ludwig et al., “Neighborhoods, Obesity, and Diabetes — A Randomized Social Experiment,” New England Journal of Medicine, 365:16, October 2011, http://www.nejm.org/doi/full/10.1056/NEJMsa1103216;

Brian A. Jacob, Jens Ludwig, Douglas L. Miller, “The Effects of Housing and Neighborhood Conditions on Child Mortality,” NBER Work Paper No. 17369, National Bureau of Economic Research, August 2011, http://www.nber.org/papers/w17369.

[9] Heather Schwartz, “Housing Policy is School Policy,” The Century Foundation, 2010, http://tcf.org/publications/pdfs/housing-policy-is-school-policy-pdf/Schwartz.pdf.

[10] Many fixed-income benefits, such as Social Security and SSI, typically increase annually due to cost-of-living adjustments. To avoid a loss of revenue from this streamlined option, agencies would be required to assume that in the intervening two years these tenants’ incomes rose by a rate of inflation specified by HUD.

[11] The flat rent option was authorized by the Quality Housing and Work Responsibility Act of 1998 (QHWRA). The AHSSIA provision would also apply to "ceiling" rents, which were established prior to the enactment of QHWRA and are subject to somewhat different rules.

[12] Abt Associates et al, Study of Rents and Rent Flexibility, prepared for HUD Office of Public and Indian Housing, May 26, 2010, http://www.huduser.org/publications/pdf/Rent%20Study_Final%20Report_05-26-10.pdf.

[13] A separate provision of SEVRA (but not AHSSIA) would prohibit families from continuing to receive assistance if their income rises to a much higher level (generally above 80 percent of local median income). Currently, there is no income limitation after admission. Under SEVRA, owners and agencies could opt not to enforce this new policy in project-based Section 8 and public housing. And families with incomes above 80 percent of median in most areas no longer qualify for assistance under the voucher program because 30 percent of their adjusted income — their required contribution — exceeds the maximum rent a voucher can cover. Nonetheless, because the SEVRA policy would terminate assistance for some higher-income families (who would then typically be replaced by lower-income families who require larger subsidies), CBO estimated that it would cost $209 million over 5 years.

[14] Both today and under AHSSIA and SEVRA, agencies can place project-based vouchers in 100 percent of units in developments that assist the elderly or people with disabilities or provide supportive services to residents.

[15] For further discussion of the risks of posed by MTW expansion , see Douglas Rice and Will Fischer, Proposal to Greatly Expand “Moving to Work” Initiative Risks Deep Cuts in Housing Assistance Over Time, available at https://www.cbpp.org/sites/default/files/atoms/files/1-10-12hous.pdf, and Will Fischer, Expansion of HUD’s Moving to Work Demonstration is Not Justified, available at https://www.cbpp.org/cms/index.cfm?fa=view&id=3590 .

More from the Authors