Testimony of Jared Bernstein Before the House Committee on Education and the Workforce

Chairman Kline, Ranking Member Miller, and members of the Committee, I thank you for the opportunity to testify today and applaud you for holding this hearing on the issue that matters most to most Americans right now: opportunity, jobs, and the living standards of the broad middle class.

Introduction: Current Conditions and the American Middle Class

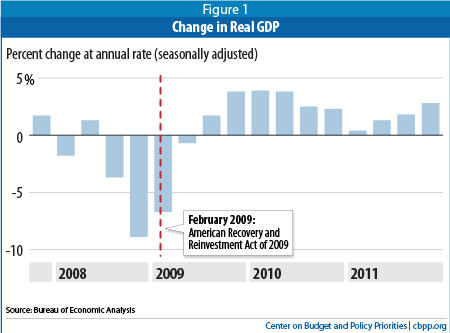

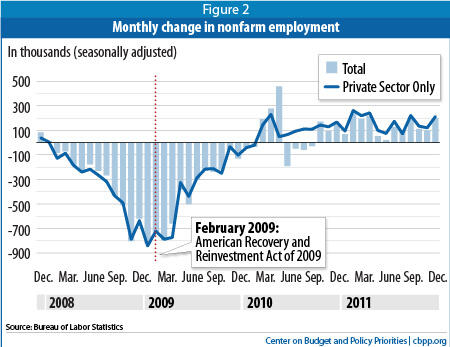

The current economy continues to expand in real GDP terms, as has been the case since the second half of 2009. Employment growth turned positive in March of 2010, and since then the private sector has added 3.2 million jobs on net; including the public sector, net job growth is 2.7 million. As the two figures below show, the rate of GDP contraction and job losses diminished shortly after the interventions of both the federal government through the Recovery Act, and the Federal Reserve, through monetary stimulus.

Moreover, nonpartisan research like that of the Congressional Budget Office has shown that government and Federal Reserve policies have played an integral role in this reversal.

Yet, while the economy is moving in the right direction, and has even developed some momentum in recent months—the unemployment rate fell by almost one percentage point last year, from 9.4 percent to 8.5 percent; the more comprehensive underemployment rate fell by 1.4 points, from 16.6 percent to 15.2 percent—the underlying growth rate of the expansion is still too slow to deliver middle-class families the economic opportunities they need to meet their family budgets, much less to get ahead.

As the President stressed in his State of the Union address, private sector employers have been adding net new jobs every month for close to two years, over three million so far. Of course, many more jobs were lost in the great recession, and I suspect that every policy maker in this room wants to see that growth rate accelerate.

Growth and the Middle Class: Necessary But Not Sufficient

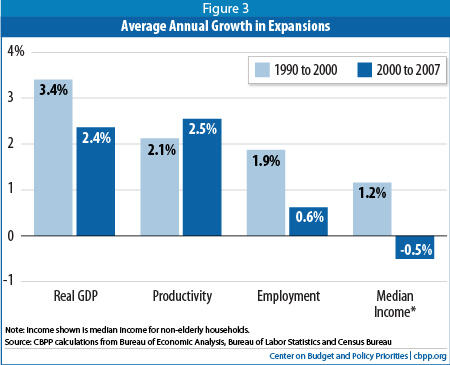

Yet, if we’re talking about middle-class economic prosperity, we must recognize that the growth is necessary yet not sufficient. GDP or productivity growth alone has not sufficiently lifted the incomes and living standards of the middle class (the next section explore the feedback loop between middle-class prosperity and a stronger economy). This is a long term problem, though it was especially evident in the business cycle expansion of the 2000s. Measuring from annual peak-to-peak years of the cycle—2000-2007—productivity grew 2.5 percent per year on average (19% overall) in those years and real GDP grew 2.4 percent per year (18% overall) but the real income of middle-class, working-age households fell half-a-percent per year, or 3.4 percent (see figure).

Middle-class income trends were much more favorable in the 1990s. Though the real income of working-aged households fell in the recession of 1990-91, it soon reversed course and grew 10 percent—an addition of about $5,600 dollars in today’s dollars—over the full cycle. Employers added 22.7 million jobs over the 1990s cycle, compared to 5.5 million over the 2000s cycle.[1]

I raise this comparison here to a few reasons. First, the national economic policy backdrop was very different over these two decades. In the 2000s, policy makers aggressively adapted supply-side,

trickle-down measures, characterized by large tax cuts favoring the wealthy, deregulation under the assumption that financial markets would self-monitor, and persistent budget deficits even during an expansion.

Fiscal and tax policies were especially different in the 1990s, as taxes were raised on the wealthiest and cut for the poorest among us, and the fiscal budget achieved multi-year surpluses for the first time since the 1950s.

Second, these observations are highly germane to the current national debates over jobs, oversight of financial markets, and tax policy. Supply-side, trickle down arguments are particularly resurgent, despite the evidence noted above. One is tempted to recall the admonition that those who forget the past are doomed to repeat it.

Third, these comparisons raise the critical question of what measures would be most advantageous for this committee to pursue in terms of reconnecting growth, productivity, and middle class prosperity. I will speak to this question in the last part of my testimony, but first, let us examine the other side of that question.

Middle Class Prosperity and the Health of the Economy

The trickle-down, deregulatory agenda—what I have called YOYO, or “you’re on your own” economics—presumes that the growth chain starts at the top of the wealth scale and “trickles down” to those at the middle and the bottom of that scale. But there is another theory, supported by evidence like that above, suggesting that a much better way to generate robust, lasting, and broadly shared growth is through an economically strengthened middle class.

At the most basic level, this growth model is a function of customers interacting with employers, business owners, and producers. A recent article by highly successful venture capitalist Nick Hanauer described this interaction as follows:

I’ve never been a “job creator.” I can start a business based on a great idea, and initially hire dozens or hundreds of people. But if no one can afford to buy what I have to sell, my business will soon fail and all those jobs will evaporate.

That’s why I can say with confidence that rich people don’t create jobs, nor do businesses, large or small. What does lead to more employment is the feedback loop between customers and businesses. And only consumers can set in motion a virtuous cycle that allows companies to survive and thrive and business owners to hire. An ordinary middle-class consumer is far more of a job creator than I ever have been or ever will be.

How does this dynamic interaction show up in the macroeconomy? Economist Alan Krueger, currently serving as Chair of the President’s Council of Economic Advisers summarized these findings in a recent speech, in a section on the consequences of economic inequality.

- Less robust (or debt-financed) consumption. Seventy percent of the US economy is accounted for by consumer spending, so if that part of GDP lags, economic growth slows. It is also the case that the propensity to consume out of current income is higher among lower-income households (i.e., compared to wealthier households, they’re more likely to spend than save their income).

Based on an estimate of these relative propensities and the large shift in the share of national income that accrued to the top 1 percent over the past few decades, Krueger calculates that aggregate consumption could be 5 percent higher in the absence of such large income shifts. Applying rules of thumb on the relationship between aggregate growth and jobs, and assuming both economic slack and that this income was not simply replacing demand elsewhere in the economy, this extra consumption growth could reduce unemployment by 1.75 percentage points, implying about 2.6 million more people with jobs.[2]

Krueger cites an important caveat about this type of calculation. In the face of stagnant earnings in the 2000s, many in the middle class borrowed to make up—or more than make up—the difference, in which case middle-class consumption did not fall as much as it would have absent this leverage. To point out that this method of improving middle class living standards is both unsustainable and extremely risky is an obvious understatement.

- Inequality and longer term growth. Krueger also points to recent research showing that “in a society where income inequality is greater, political decisions are likely to result in policies that lead to less growth.” Economist Mancur Olsen also hypothesized about this relationship decades ago.

As more income, wealth, and power is concentrated at the top of the income scale, narrow coalitions will form to influence policy decisions in ways less likely to promote overall, or middle-class, well-being, and more likely to favor those with disproportionate power and resources. In the current economics debate, we clearly see these dynamics in a tax code that bestows preferential treatment on those with large amounts of assets, like capital gains and stock dividends, relative to wage earners.

- Trickle-down economics, inequality, and incomes. Another piece of evidence with implications for rebuilding a strong middle class comes from new work by economists Emmanuel Saez et al. As shown in the figures from their paper (see Appendix), they use international evidence from a wide variety of advanced economies to examine two key links in the logic of the supply-side chain.

First, they look at the relationship between the top marginal income tax rate in these countries and the change in income inequality. They find a strong negative correlation: in countries like ours that cut the top marginal tax rate, income is a lot more skewed (and note that this refers to pretax income, so the result is not a direct function of the tax policy changes).

But the critical question for supply-side is whether these high-end marginal tax rate reductions lead to faster income growth (we’ve already seen that they lead to more income inequality). The bottom figure shows that they do not. Real per capita income growth across these countries is unrelated to the changes in tax rates.[3]

The above points emphasize an economic rationale for a growth model more favorable to the middle class. More broadly shared growth would not only score higher on a fairness criterion; it would provide a more reliable and durable structure for overall growth itself. It is no accident, in this regard, that the era of heightened inequality coincides with the arrival and persistence of what I’ve called “the shampoo economy:” bubble, bust, repeat.

But our emphasis on growth should not crowd out that of fairness, and in this regard, some of the most important recent work in this area has stressed the relationship between inequality and mobility, the latter being the extent to which individuals’ and families’ economic positions change over the life cycles. Again, I will briefly summarize the relevant findings.

- Economic mobility. Some policy makers, often in seeking to dismiss the inequality problem, argue that the US has enough income mobility to offset increased inequality. We may start out further apart, they argue, but we change places enough that it doesn’t matter. This argument fails, however, both in terms of logic and evidence. The existence of mobility cannot offset increased inequality; for that to occur, mobility itself must be accelerating. There is no evidence to support such acceleration and some new, high-quality work suggests a slight decline in the rate of mobility.

The US has considerably less income mobility than almost every other advanced economy. In particular, as stressed in a recent New York Times article, parental income is a stronger predictor of the success of grown children in the U.S. relative to other advanced nations—i.e., we have less intergenerational mobility than other nations.

Putting some of these themes together, I have hypothesized that there are causal linkages between inequality and immobility. To the extent that those who have lost income share in recent years suffer diminished access to the goods, services, and general living conditions that would enhance their mobility, we would expect to see economic results like those cited above.

Here, I’m thinking about everything from access to quality education, starting with pre-school (such early educational interventions have been shown to have lasting positive impacts), to public services, like decent libraries and parks, to health care, housing, and even the physical environment. The new research linking mobility and inequality may well find that as society grows ever more unequal, those falling behind are losing access to the ladders that used to help them climb over the mobility barriers they faced.

Policies Designed to Rebuild the Middle Class

It is widely maintained by some policy makers that it is up to the private sector to provide the middle class with the opportunities they need to get ahead. Given that most economic activity and jobs are not directly associated with government, this is of course true. But the idea that this implies no role for government is both wrong and dangerous, in the sense of ceding the playing field to our competitors who are not bound by such firm ideology. This insight is particularly germane given the trends presented above regarding job and income growth, inequality, and mobility.

In fact, government must enforce fair rules of the road, whether it comes to the selling of financial products or the rights of workers to collectively bargain with their employers. There is a role for government to ensure that basic needs, such as access to affordable health care and a secure retirement, are most efficiently met. Government must also offset market failures, including recessions, insufficient supply of skills in the workforce, and barriers to entry for potentially expanding industries. Finally, the system of funding government must be fair in the sense that middle class families do not face a proportionally larger tax federal tax burden—higher effective tax rates—than those with many more financial resources.

Every one of these policy areas provides policy makers like the members of this committee with the opportunity to help reconnect growth and middle class prosperity, restore some degree of income security, and push back on the inequality and immobility trends documented above.

The massive market failure of the great recession provides important lessons to policy makers, both regarding the lack of financial oversight that helped to inflate the housing bubble and the stimulus measures, most notably the Recovery Act, that helped to generate the historically large swings from negatives to positives in growth and jobs as shown in the first table above.

But more such measures are needed. While the economy is improving and unemployment is slowly coming down, at current growth rates, it will take many years to reach full employment. The following measures can help build on the momentum we have and accelerate the recovery:

- Extend the payroll tax holiday and unemployment insurance. Policy makers of both parties have widely agreed on the need to extend payroll relief through the end of the year ; failure to do so would add to the underlying fragility of the nascent expansion.

- Invest in infrastructure investment. As part of the American Jobs Act, the President proposed a national program to repair and modernize the nation’s public schools and community colleges. This plan is now a legislative initiative called FAST—Fix America’s Schools Today--soon to be introduced in both chambers. FAST addresses three big problems: 1) the backlog of maintenance repairs in strapped school districts across the nation, 2) the high unemployment among construction workers and other laborers who do this type of work, and 3) the energy inefficiency in many public schools where billions of taxpayer dollars are wasted through bad roofing, aging boilers, and poorly insulated windows. I urge legislators will give this idea a close look.

- Manufacturing policy: In his State of the Union address, the President presented some ideas, including tax incentives and trade enforcement measures, to help incentivize the insourcing of manufacturing work in America. In fact, manufacturers have added over 300,000 jobs over the past 21 months, and anecdotally, some producers say that perhaps they have overplayed the outsourcing idea and are interested in producing closer to where they sell (rising transportation costs and narrower international wage differentials may also be in play here).

In this regard, policy makers could help tap this development by closing international tax loopholes that incentivize multinationals to build factories abroad. The President’s most recent budget recommended to the so-called super committee in September, proposes $110 billion in loophole closures that would both level the playing field for domestic manufacturers and help relieve our fiscal situation.

Trade enforcement, including actions against countries that manage their currencies to artificially support their exports and block our imports, is another essential piece of this puzzle.

Note that these measures simply level the playing field and are in no sense protectionist—they do not provide unfair advantages to American firms nor do they block imports.

- Skills enhancement. This committee has a long history of interest in policies to ensure that the skills of American workers match those demanded by today’s employers. Ranking Member Miller’s Pathways Back to Work bill supports a subsidized employment program targeted at unemployed adults, modeled on a successful Recovery Act program that employed over 250,000 workers in 2009-10 (TANF Emergency Fund). This bill also provides work-based job-training for the long-term unemployed and summer jobs for younger workers.

President Obama also stressed the importance of workforce investment through what is typically called “sectoral employment strategies.” As opposed to generalized training that too often leaves participants unprepared for actual jobs, sectoral strategies link trainers, often through partnerships with community colleges, with local employers who provide granular information about future demand needs. Research by Georgetown University professor Harry Holzer shows these programs to be far more effective than traditional training programs that are too often detached from what’s happening in local labor markets.

- Improving workers’ bargaining power: As with international trade and taxation, the union organizing playing field is badly tilted against those who would like to exercise their right to collectively bargain. A recent rule change by the National Labor Relations Board will help workers who’ve petitioned to form a union to have a more timely election. In a climate where some employers who oppose unions can and do block elections with impunity, this new rule removes some of the above-noted-tilt.

Finally, it is important to note one area of public policy that has incorrectly been singled out in recent years as a factor holding back job growth and hurting the middle class: the regulatory climate. While onerous regulations should always be rigorously reviewed for proof of their net positive benefits, it is clear from the evidence that it is weak demand, not regulation, that’s preventing faster job creation.

Data from the BLS Survey of Layoff Events show low and declining shares of layoffs attributable to government regulations. A year ago (2010q3) less than half of one percent (0.44%) of layoffs were related to government regulations, according to employers. In the most recent quarter for which data are available, the share of layoff events attributable to government regulations fell to zero (technically, the number reported was too small to meet BLS sampling criteria), as did the shares of unemployment insurance claims and all other separations.[4]

Employers themselves, particularly small businesses, report in various surveys that poor sales (aka, weak demand) has been a much more important constraint then regulations. Recent analysis by the Treasury Department provides this summary:

- “In the September survey of small business owners by the National Federation of Independent Businesses, more than twice as many respondents cited poor sales (29.6 percent) as their largest problem than cite regulation (13.9 percent).

- In an August survey of economists by the National Association for Business Economics, 80 percent of respondents described the current regulatory environment as “good” for American businesses and the overall economy.

- [I]n a recent Wall Street Journal survey of economists, 65 percent of respondents concluded that a lack demand, not government policy, was the main impediment to increased hiring.”

Conclusion

This testimony has stressed that, even as the economy is improving and the American people are digging their way out of the Great Recession, unemployment is still high and economic growth still relatively slow. Compared to the massive losses in early 2009, we’re much improved. But compared to an economy that’s providing what I believe members of this Committee would recognize as gainful opportunities for middle class workers and their families, we’ve got a ways to go.

Importantly, that view does not suggest that GDP growth alone is sufficient, though it is of course necessary. As recently as the business cycle of the 2000s, we saw middle-class, working-age households lose ground in terms of their real income, even while productivity growth was relatively strong. My testimony amplifies a number of policy ideas currently under discussion that I believe will help to reconnect growth and middle class prosperity.

But arguments and evidence above also point to the importance of a strong middle class for growth itself, positing a feedback loop. Businesses cannot create jobs without customers, and in a climate of high levels of income concentration, the customer base becomes too narrow. In this regard, I present above a set of arguments connecting higher levels of income inequality with less satisfactory growth outcomes. Similarly, there is reason to believe that high levels of inequality negatively affect mobility, by both lengthening the distance disadvantaged families have to climb and shortening their ladders.

While more research clearly is needed to get a better handle on these interactions between broadly shared prosperity and better growth and mobility outcomes, the circumstantial evidence is quite strong. I urge the committee to take the policy steps to re-link the economic prosperity of the American middle class with the productivity and growth they themselves our helping to generate.

See

for AppendixEnd Notes

[2] As consumption is 70% of GDP, and each point of GDP above trend reduces unemployment by half a point, this calculation is .7*.5*5%, or 1.75%.

[3] Note that the income measure in their research is a broad average (real per-capita GDP growth); given that this measure is itself driven upwards by the growth of inequality, a median measure (insensitive to large accumulations at the top of the scale) would likely be even less correlated to tax changes, if not negatively correlated.

[4] A layoff is an event involving the filing of 50 or more initial UI claims by an employer during a 5-week period, with at least 50 workers separated from a job for more than 30 days. Separations include job losses from such an event, whether or not the worker claimed UI.