Promoting State Budget Accountability Through Tax Expenditure Reporting

Each year states spend tens, maybe hundreds, of billions of dollars through “tax expenditures.” Tax expenditures are tax credits, deductions, and exemptions that reduce state revenue. They can include everything from poverty-reducing tax credits, to middle-class benefits, to corporate subsidies. Tax expenditures cost state treasuries money in much the same way as direct spending for schools, health care, or road construction. And like direct spending, tax expenditures are a tool states can use to accomplish policy goals.

There is a key difference, however, between direct spending and tax expenditures. States typically require extensive documentation of how much direct spending they do each year, and their budget processes entail evaluation of each item. Tax expenditures usually receive far less scrutiny. For the most part, policymakers do not regularly examine tax expenditures, nor do states document their effectiveness the same way they do for on-budget expenditures.

This is a serious problem. Most tax expenditures are written into the tax code and thus will continue indefinitely — regardless of how costly they may become over time — unless the legislature acts to discontinue them. (Appropriated expenditures, by contrast, typically last only as long as the one- or two-year budget cycle.) Without information on a particular tax expenditure’s costs and benefits, lawmakers cannot make an informed decision on whether its continuation is in the state’s interest.

More broadly, if policymakers, the media, and the general public lack information about tax expenditures, they cannot fully participate in decisions about how to allocate state resources. In fact, in many states the policy debate encompasses little more than half of the state’s total expenditures because expenditures made through the tax code are not part of the conversation.

A state can address this lack of transparency by regularly publishing a tax expenditure report, also called a tax expenditure budget. A tax expenditure report lists the state’s tax breaks and how much each one costs, along with other relevant information that helps policymakers and others evaluate them.

If properly designed and produced, a tax expenditure report makes tax expenditures more transparent by telling policymakers and the public how the state is spending its money and what it is accomplishing through those expenditures. A tax expenditure report also encourages accountability by enabling policymakers and voters to evaluate individual tax expenditures and decide whether to continue them. In addition, a tax expenditure report saves money by enabling policymakers to monitor the costs of tax expenditures and rein in their cost if necessary.

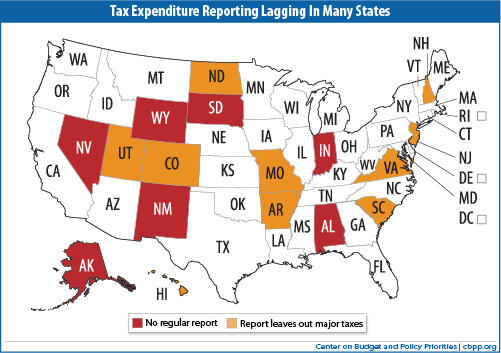

Forty-four states (counting the District of Columbia as a state) produce some form of tax expenditure report. [1] Unfortunately, many of these reports have significant shortcomings that limit their usefulness:

- Ten of the 44 states omit major taxes from their tax expenditure report, and six others fail to publish a report at least once every two years.

- Almost every state’s report omits some essential information, such as the law that mandates a given tax expenditure or the number of households or businesses that benefit. Some reports even omit the cost of many tax expenditures.

- Two states, Arkansas and New Hampshire, fail to make their report accessible to the public through means such as posting it on the Internet.

Some state tax expenditure reports are much better than others, but every state could improve its practices in this area. Oregon, Minnesota, and the District of Columbia publish relatively comprehensive and informative reports that could serve as a model for other states. Among the least useful reports are those issued by Arkansas, Colorado, and Utah, because they omit major taxes, fail to provide cost estimates and other key information for many tax expenditures, and/or are not available online.

Seven states produce no regular tax expenditure report, meaning that citizens have no way of knowing on an ongoing basis what the state is spending or what policies it is pursuing through the tax code. These states are: Alabama, Alaska, Indiana, Nevada, New Mexico, South Dakota, and Wyoming.

This report lays out best practices for tax expenditure reports — ways to make the reports maximally useful to policymakers and to the public. (For a list of the features a report should contain, see the box below.) It also describes other steps, beyond producing a tax expenditure report, states can take to better manage their tax-side spending. The goal is not to eliminate tax expenditures, which are neither good policy nor bad policy per se. Tax expenditures are one of a policymaker’s tools for achieving policy goals; like other tools, they can be put to good use or abused, and like other tools, their use should be transparent and accountable. A well-designed tax expenditure report can help accomplish that, especially when accompanied by other reforms that allow legislatures to regularly review and better manage tax-side spending.

Tax Expenditure Report Checklist

To achieve its goals of improving transparency, encouraging accountability, and saving money, a tax expenditure report should have the features listed below.

Accessibility. The report should be:

- Published regularly.

- Incorporated into the budget process.

- Available on the Web.

Scope. The report should include:

- Tax expenditures related to all taxes.

- All tax expenditures, including those with lower costs or those benefitting few taxpayers.

- Explicit and implicit tax expenditures.

- Tax expenditures enacted by the state that affect local government.

Detail. The report should include:

- The cost of the tax expenditure, using current data.

- The cost in future years, to allow comparison with other proposed expenditures.

- A description of the tax expenditure.

- The relevant legal citation and year of enactment.

- Detail on the taxpayers who benefit from the tax expenditure.

- Separate reporting for the state and local revenue losses, where applicable.

Analysis. The report should:

- Classify tax expenditures using the same categories as direct spending.

- State the purpose of each tax expenditure.

- Evaluate the extent to which that purpose has been accomplished.

- Analyze the distribution of benefits by income level and size of business.

To read the full report, click

.End Notes

End Note:

[1] All of the data in this report reflect tax expenditure documents released through March 2011.

More from the Authors

Areas of Expertise