Six Reasons Why Supermajority Requirements to Raise Taxes Are a Bad Idea

A few states are considering amending their constitutions to make it even harder to close tax loopholes and otherwise change the tax code to raise more revenue. The proposed amendments would require that revenue-positive tax changes win support from supermajorities of each house of the legislature plus the governor’s signature, rather than the normal simple majority required for all other legislation.

Only a few states have such requirements, and their experience fails to prove that supermajorities actually lead to lower taxes or sounder tax policy. On average, states with strict supermajority requirements levy taxes at a nearly identical level as other states. That’s because most states avoid tax increases most of the time, without supermajority requirements.

More worrisome, supermajority rules can cause significant damage to a state’s capacity to properly handle its finances. Here are six reasons why these rules are a bad idea.

- Supermajority rules reduce accountability by protecting special interest tax breaks. Supermajority requirements make it even more difficult to get rid of ineffective and unfair tax breaks than it already is. In many cases, repealing a tax break is considered a tax increase subject to the higher vote thresholds. This means that costly deductions, credits, and other tax expenditures that often benefit only a handful of corporations or individuals have more protection than other types of spending, which can be cut by a simple majority vote. Lobbyists have a far easier time shielding narrow tax benefits from cuts since opponents have to muster an inordinate number of votes. Conversely, enacting new tax breaks requires only a simple majority vote.

- Supermajority rules shift costs from some state residents to others. With tax increases and the repeal of tax breaks subject to supermajority requirements, lawmakers are more likely to raise fees, tuition, and other levies not subject to the requirements, and to reduce support for local governments, who may need to raise property taxes as a result. This shifts the cost of government from some taxpayers to others — students, Medicaid recipients, and local property owners, for example.

- Supermajority rules may raise state spending or dissuade states from making capital investments by increasing interest rates. Research shows that investors are less willing to buy bonds from states with supermajority tax requirements. This is because such rules reduce states’ flexibility to raise revenue, making them (in the eyes of investors and bond rating agencies) less trustworthy borrowers. Supermajority states thus are more likely to have lower bond ratings, forcing them to make higher interest payments to investors and pushing up the cost of new roads, public buildings and other bond-financed projects.

- Supermajority rules make it harder to finance transportation investments. Investments in transportation infrastructure are particularly threatened by a supermajority requirement because of the structure of gasoline taxes. Most highway and other transportation projects are funded by state gasoline taxes that are not indexed for inflation. To keep up with rising highway-construction costs, gasoline tax rates must be periodically increased, but supermajority rules make that more difficult. Five of the seven strict supermajority states have not raised gas taxes in over 15 years, while most other states have increased them at least once in the last decade.

- Supermajority rules limit budget options available to legislators and increase the chances that recessions will be deeper and longer. The best available approach to combating recession-induced budget gaps is often a balanced one that includes both revenue increases and targeted spending cuts. By making it harder to raise taxes, supermajority rules encourage states to cut spending deeper. By removing demand from the economy, this approach makes recovery more difficult. Supermajority states have fared worse during the recession than other states.

- Supermajority rules increase the power of extremists and special interests. In supermajority states, a small minority of legislators and special-interest lobbyists can thwart the will of a majority. Small groups of lawmakers can hold even the most popular legislation hostage, demanding narrow concessions or the inclusion of expensive pet projects.

Most States Avoid Tax Increases Most of the Time, Without Supermajority Requirements

The amendments under consideration in Minnesota (House File 1598 and Senate File 1384) and New Hampshire (CACR 6), and similar proposals considered recently in states like Texas, would place those states outside the mainstream. Most states’ legislatures can send tax bills to the governor with a simple majority vote in each house, the same margin required to enact most other bills. Two-thirds of states — 33 of 50 — and the District of Columbia allow a tax measure to pass with a simple majority in each house of the legislature.

Just seven states have a constitutional supermajority requirement that applies to all tax increases: Delaware, Mississippi, and Oregon each require a three-fifths vote of each house, and Arizona, California, Nevada, and Louisiana each require a two-thirds vote of each house. A few other states require supermajorities to approve some but not all tax increases, require voter approval for tax increases, or establish a supermajority requirement in statute, where the legislature can override it when necessary; see Appendix for details.

The reason these rules have remained rare is simple: States don’t need supermajority requirements to ensure that taxes will remain manageable, that major tax increases will be rare, and that legislators will think very carefully before increasing taxes.

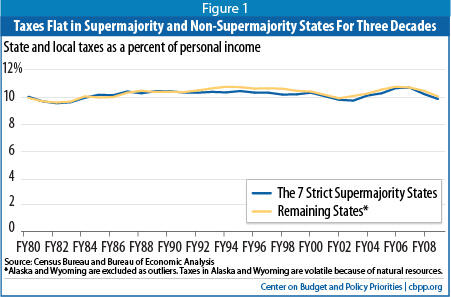

- Taxes have been flat as a share of personal income in non-supermajority states for thirty years. In the average state with no broad constitutional supermajority requirement, taxes as a share of personal income have hovered in a narrow range — between 9.7 percent and 10.9 percent — since 1980.[1] That’s almost identical to the average range for the seven strict supermajority states — 9.7 percent to 10.8 percent (see box on page 4).

- Major tax increases are rare, usually occurring in the aftermath of recessions, when revenues have fallen short of the cost of maintaining core public services such as education and health care, and generally accompanied by deep spending cuts. Before the 2007-09 recession hit, the average state had not increased taxes by more than two percent of total revenues in over 9 years, prior to the previous recession.[2] Moreover, recession-driven tax increases are almost always offset by tax cuts in good economic times. For example, states in total raised personal and corporate income taxes in 1993 and 1994, following a recession, but then cut these same taxes for eight straight years, from 1995 through 2002, after which the next recession took hold.[3]

- There are already significant barriers to raising taxes. One barrier to raising taxes is the checks-and-balances of American democracy: It is not easy for a piece of legislation to win majority approval, separately, in each house of the legislature and also to get the signature of the governor. Another barrier is politics: Any elected official who votes to raise taxes is well aware of the potential political fallout. In other words, voters already have a tool available to them to hold elected officials accountable for raising taxes if they choose, which is that they can vote them out of office.

Supermajority Rules Reduce Accountability by Protecting Special Interest Tax Breaks

Supermajority rules protect tax loopholes and other narrowly targeted tax breaks. This is because eliminating a tax deduction, credit, exemption, or other special rule is typically governed by supermajority rules, on the grounds that it raises taxes on at least one corporation or individual.[4] State tax codes are riddled with such tax breaks, some of which are effective and some of which are not.[5] Often, tax breaks make state tax systems less level and more imbalanced. Narrowly tailored tax breaks are part of the reason why the average profitable Fortune 500 Corporation pays less than half the statutory state tax rate and many profitable corporations pay nothing at all.[6]

Supermajority Rules Don't Necessarily Lower Taxes

An argument often heard in debates over supermajorities is that state taxes should be lower. But there is little evidence that states with such requirements actually have lower taxes. The average state with a constitutional supermajority rule covering all tax increases has tax levels that are nearly identical to the tax levels in the average other state.* Taxes have been flat as a share of personal income in both supermajority and non-supermajority states for the last three decades.

Some academic studies find that, after controlling for other factors, supermajority rules do lower taxes compared to their level without the rule.** On the other hand, at least one study finds that these rules do not affect the total revenue — taxes, fees, and other forms of revenue — that states collect. Supermajority states may raise fees and other revenue to compensate for the restrictions on taxes.***

*See footnote 1.

**See, for example, Brian G. Knight, "Supermajority voting requirements for tax increases: evidence from the states," Journal of Public Economics, 76 (2000), pp. 41-67.

***Meagan M. Jordan and Kim U. Hoffman, "The Revenue Impact of States Legislative Supermajority Voting Requirements," Midsouth Political Science Review, 2009, Vol. 10, p.

This means that tax breaks are getting a special legislative protection that is not afforded other types of legislation. Tax breaks are sometimes referred to as "tax expenditures,” because they often function much like a direct expenditure program albeit typically with less accountability. But if the legislature in a state with a supermajority rule decides it wants to stop spending money on a direct expenditure program, it can do so with simple majority votes. If it wants to get rid of a wasteful corporate tax loophole, the legislature needs to meet the higher threshold.

Thus, for a state with a supermajority requirement seeking to balance its budget, it is legislatively easier to repeal a Meals on Wheels program, lay off state troopers or kindergarten teachers, cut health care services for seniors, or cut college financial aid than to close a corporate tax loophole.

To be sure, tax breaks can be difficult to eliminate even under simple majority rules. But given the power and influence that lobbyists for large corporations often wield in state capitols, meeting the supermajority threshold to repeal a tax break can be particularly difficult. For lobbyists wishing to protect a tax loophole, supermajority requirements make their job significantly easier by reducing the number of legislators that need convincing. Even if a majority of legislators oppose the lobbyist’s efforts and want to get rid of an ineffective corporate tax break, the lobbyist can still prevail. This is why one legal scholar called a supermajority tax restriction proposed at the federal level the "Tax Loophole Preservation Amendment to the Constitution.”[7]

California’s experience with a constitutional supermajority requirement for raising taxes bears out these concerns. The California Citizens Budget Commission, a distinguished bipartisan panel of business and community leaders formed in 1993 to study the state’s budget problems, reported that the state’s supermajority requirement "makes it relatively easy to enact tax breaks but difficult to repeal them.” The Commission recommended the state Constitution be changed to allow the legislature to narrow or eliminate tax breaks by a simple majority vote, so that it would be as easy to eliminate tax breaks as to create them.[8]

Under a supermajority requirement, it is much easier to enact a tax break than to get rid of it. This is a particular problem when a state enacts a tax break that turns out to be far more expensive than originally thought. Such an error is uncommon but far from unheard-of; in recent years, states as diverse as Arizona and Maryland have made headlines by enacting tax credits that turned out to be far easier to claim — and therefore had far greater impact on the state treasury — than was originally intended when the credit was enacted. (In Arizona’s case, it was a tax credit for low-emission vehicles; in Maryland’s case, it was a tax credit for historic preservation.) Under a supermajority requirement, reversing or tightening up the rules for the credit would be harder to pass in the legislature than it was to enact the credit in the first place.

Supermajority requirements also make it harder for a state to control how changes in federal tax policy affect the state. Many state personal and corporate income tax systems are tied automatically to the federal definitions of adjusted gross income or taxable income. This means that when Congress enacts a measure that reduces the federal income tax base, it affects the state tax base too, and automatically flows through to reduce revenues in these states. States can "decouple” from the federal tax code so that a specific federal provision is disregarded in state tax calculations, but in a state with a supermajority requirement, getting such a federal tax break out of its own tax code may be considered a "tax increase” and thus subject to the supermajority rule.

A recent federal tax break cost states with supermajority requirements more money than other states. The federal government recently decided to try to stimulate the national economy by giving corporations a special tax break for equipment purchases. Most states declined to incorporate this tax break into their own codes. But three of the seven states with strict supermajority rules — Delaware, Louisiana, and Oregon — allowed this tax break to cost them revenue.[9]

Supermajority Rules Shift Costs from Some State Residents to Others

Supermajority requirements restrict states from some kinds of revenue increases — closing loopholes and raising taxes — but not others. Lawmakers in supermajority states can still raise various fees, such as the fees charged to Medicaid recipients or college tuition, by simple majority vote. They can also cut funding to local governments by simple majority vote, which may lead local governments to raise property taxes.

In this way, supermajority rules make it more likely that some people — Medicaid recipients, college students, or local property owners, for example — will see their costs increase. Effectively, the rules encourage state lawmakers to shift costs from some taxpayers to others.

Supermajority Rules May Raise State Spending or Dissuade States from Making Capital Investments by Increasing Interest Rates

States that enact supermajority requirements may be likely to have lower bond ratings and pay more to finance infrastructure projects than they otherwise would. This is because states and localities routinely sell bonds to finance construction projects, like roads, schools and hospitals. A primary consideration for potential investors in those projects is the likely ability of a state to repay those bonds. By reducing a state’s flexibility to raise needed revenue, supermajority requirements send a message to investors that a state is a less trustworthy borrower.

Credit rating agencies inform investors about the security of investing in bonds and other investment products. If the rating agencies rank poorly a state’s creditworthiness, investors are likely to demand higher interest payments when the state floats a bond to pay for an infrastructure project — a new road, community college, or convention center, for example — making these projects more expensive.

States with Supermajority Restrictions Have Suffered More in this Recession than Other States

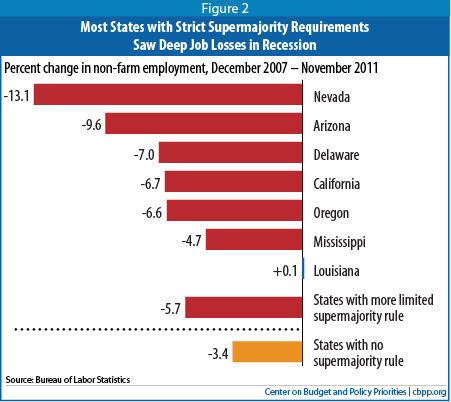

Some proponents of supermajority restrictions claim they improve a state’s economy and create jobs. For instance, a legislator who voted to enact a statutory supermajority requirement in Wisconsin last year claimed the requirement would help “jumpstart Wisconsin’s economy” and “create a positive, job-creating business environment.”* There is no credible evidence that it will. In fact, a cursory glance at recent economic data actually shows that the economies of states with supermajority requirements are in worse shape than their neighbors’. This is almost certainly a coincidence, but the experiences of states during the recent recession makes clear that supermajority restrictions have not produced the vibrant economies sometimes envisioned by proponents.

Since the recession started:

- The seven states with broad, constitutional supermajority restrictions have lost 6.7 percent of their jobs, while states with no supermajority restrictions have lost 3.4 percent.

- Six of the seven states with strict supermajority requirements have experienced above-average job declines.

- The two states with the deepest job losses — Arizona and Nevada — both have broad, constitutional supermajority restrictions. Nevada has lost 13 percent of its jobs since the recession started and Arizona has lost nearly 10 percent.**

*State Representative Evan Wynn, “Rep. Wynn Supports More Proposals to Jumpstart WI Economy,” press release issued January 28, 2011. http://legis.wisconsin.gov/assembly/wynn/pressreleases/Pages/Rep Wynn Supports More Proposals to Jumpstart.aspx

** The recession started in December 2007. These figures measure job losses through November 2011, using statistics from the Bureau of Labor Statistics.

The major rating agencies have said, explicitly, that supermajority restrictions can reduce a state’s creditworthiness. One of the criteria used by Standard & Poor’s in establishing a state’s credit rating, for instance, is state flexibility to raise revenue when necessary. States receive the highest score for this criterion if:

The state has autonomy to raise taxes and other revenues (rate and base); in addition, there is no constitutional constraint or extraordinary legislative threshold for approval (a simple majority requirement for approval of new taxes, for example) and state policymakers have, in our view, a proven track record of implementing tax increases as one of the alternatives to address budget imbalances.[10] [emphasis added]

Another major rating agency, Moody’s Investors Service, specifically cited the supermajority restrictions in Nevada and Arizona as reasons for downgrading those two states in recent years.[11] In Nevada’s case, Moody’s noted that “the supermajority requirement to raise taxes presents a hurdle to achieving balance on an ongoing basis going forward.” Moody’s also recently expressed concern about the supermajority requirement in Oklahoma, citing the rule as a reason for declining to improve that state’s credit rating.[12]

Supermajority requirements concern the rating agencies, and the investors who rely upon them, because they believe that the limit inevitably will constrain the state’s revenue stream, forcing interest payments to compete with other state funding obligations for an increasingly limited stream of funds. From the perspective of a potential investor, this creates the specter — however remote — that the state could default on its debt.

The costs to states of worrying investors in this way can be significant. An extensive study of state revenue limits and borrowing costs conducted for the Public Policy Institute of California by James Poterba, now a professor at the Massachusetts Institute of Technology, and Kim Rueben of the Urban-Brookings Tax Policy Center found that “states with supermajority provisions face higher borrowing costs than states without such requirements.”[13] They found that the impact is particularly strong during periods of fiscal stress: the authors found that a “$100 per capita deficit shock increases borrowing costs by 5.6 basis points,” compared to states without a supermajority requirement. That means an additional $560,000 in annual debt service for every $1 billion in new bond sales.

Some states might respond to such higher borrowing costs by issuing fewer bonds, which would mean less capital funds available to finance the construction and repair of roads, bridges, schools, universities, and other infrastructure investments. Investment in a state’s basic infrastructure is fundamental to its business climate, and supermajority restrictions can make these investments more expensive; in this way, the restrictions can make it harder for states to compete for business investment over time.

Supermajority Rules Make It Harder to Finance Transportation Investments

Investments in transportation infrastructure are particularly threatened by a supermajority requirement because of the structure of gasoline taxes. Most highway and other transportation projects are funded largely by state gasoline taxes. In most states, gasoline tax rates are not indexed for inflation, but highway-construction costs inevitably rise over time. As a result, gasoline tax rates must be periodically increased just to keep up with construction costs.

Broad supermajority requirements could make it substantially more difficult to finance road projects, even those with widespread support. A small number of legislators in either house of the legislature — for instance, a coalition of anti-tax conservatives and anti-highway environmentalists, drawn from the extremes of the political spectrum — could block measures that otherwise command wide support, damaging the state’s attractiveness to some businesses.

Indeed, among the seven states with strict supermajority requirements, five states — Arizona, Delaware, Louisiana, Mississippi, and Nevada — have gone more than 15 years without raising the gasoline tax (in the four other than Delaware, it has been over two decades). By contrast, most non-supermajority states raised their gasoline taxes at least once in the last decade.[14]

Supermajority Rules Limit Budget Options Available to Legislators and Increase the Chances that Recessions Will Be Deeper and Longer

Recessions often place states in a bind. To balance their budgets at a time when revenue is declining, states typically must either cut spending, raise revenue, or some combination of the two. In such circumstances, the best states can do is choose an approach that does the least possible harm to their damaged and fragile economies. Supermajority rules encourage states, instead, to choose options that can do more damage.

A particularly poor choice for states in such circumstances is to rely entirely on spending cuts to balance their budgets. This approach will make the recession even worse by reducing overall economic activity. When states cut spending, they lay off employees, cancel contracts with vendors, reduce payments to businesses and nonprofits that provide services, and cut benefit payments to individuals. All of these steps remove demand from the economy, further slowing the already weak economy.[15]

Raising taxes, particularly from wealthy people and multi-state corporations, is a less damaging approach during recessions. That’s because some people, especially those with high incomes, pay the new taxes without reducing their spending on goods and services. Corporations may pay the taxes out of retained earnings or spread the impact across other states. In this way, well-targeted tax increases do little damage to consumer spending during recessions while raising funds states can use to avoid further weakening the economy by laying off workers and otherwise reducing spending.

Typically states both raise revenue and cut spending during recessions. This balanced approach is better than spending cuts alone, particularly if the revenue increases are targeted to high-income people and the cuts are designed to both reduce spending and improve policy outcomes.[16] (States can also draw down reserves or seek assistance from the federal government, but usually these options on their own solve only part of the problem.)

Supermajority restrictions are designed to make it harder for states to raise revenue, even in recessions when a balanced approach that includes new revenue is usually the best way for states to limit the economic damage and support the recovery. These restrictions allow a minority of lawmakers to block a tax increase, forcing the legislative majority to enact spending cuts that they and their constituents do not want and that could cause unnecessary, additional damage to the state and national economy.

Supermajority Rules Increase the Power of Extremists and Special Interests

Supermajority restrictions can increase the power of special interest lobbyists and extreme factions of legislators willing to hold the majority hostage until their demands are met. In years in which a tax increase is necessary to balance the budget — for example, because of a recession, natural disaster, or other unforeseen circumstance — a small number of legislators could prevent the majority from enacting a balanced budget, using its veto power to extract special favors or projects.

To be sure, such vote-swapping can occur whether revenue-raising measures require a simple majority or a supermajority. But, as the bipartisan commission studying the effects of California’s supermajority requirement found, the degree of vote-swapping tends to intensify as the level of difficulty of obtaining the necessary votes to pass a budget increases. The level of difficulty is much greater when a supermajority is required.

The California commission found evidence that the state’s requirement for a two-thirds majority to pass budgets has led to enactment of substantial “pork-barrel” legislation that individual legislators have promoted.[17] Supermajority requirements present legislators with tempting opportunities to threaten to block revenue-raising measures that a majority favors unless the majority accepts various pet projects or programs these legislators are pushing. By making it easier to hold the budget process hostage, “supermajority” requirements actually grant “superpowers” to special interest lobbyists and small minorities of legislators with extreme agendas.

Appendix: State Supermajority Requirements

Limited Requirements

Four states — Arkansas, Florida, Kentucky, and Michigan — require a supermajority in limited circumstances. In Arkansas, it is required when increasing taxes that were in place when the rule was enacted in 1934; hence, the state’s sales tax and alcohol taxes can be raised by simple majority vote. In Florida, it’s required only for bills that increase corporate income tax rates above a certain threshold. In Kentucky, it’s required only in off-budget years. In Michigan, it covers only bills that increase the state property tax.

Limited Requirements to Avoid Votes of the People

Colorado requires a simple majority vote of the people to raise some or all taxes; the legislature can override the requirement with a supermajority vote only after a natural disaster. Similarly, Missouri requires a simple majority vote of the people for tax increases that exceed a certain threshold (about $70 million in 2008), but the legislature can avoid this in emergencies, for one year, with a two-thirds vote.

Broad Statutory Requirements

Washington and Wisconsin both require in statute a two-thirds vote of the legislature to enact increases in major taxes. In Washington, the restriction applies to all tax increases and includes reductions in tax breaks. In Wisconsin, the restriction applies only to rate increases, and so allows tax breaks to be reduced or eliminated by majority vote.

Broad Constitutional Restrictions

In the remaining nine states the constitution requires supermajority approval for the legislature to enact major tax increases. In two of these states, Oklahoma and South Dakota, the restriction does not apply to reducing or eliminating a tax break. In the other seven, it covers all tax increases, including reducing or eliminating tax breaks. Of these states, three — Delaware, Mississippi, and Oregon — require a three-fifths vote. Four — Arizona, California, Nevada, and Louisiana — require a two-thirds vote.

End Notes

[1] Based on tax revenue data from the U.S. Census Bureau and personal income data from the U.S. Bureau of Economic Analysis for the years 1980 through 2009, the latest year with data available. The average includes 41 states — all of the states that do not have a constitutional supermajority requirement for all tax increases, including eliminating tax breaks, with the exception of two outlier states, Alaska and Wyoming. Both of these states have taxes connected to natural resources that can cause tax revenue to be highly volatile.

[2] CBPP analysis of the National Council of State Legislature's State Tax Actions data and state revenue data from the U.S. Census Bureau. Based on total revenue in prior fiscal year.

[3] Sales taxes followed a similar pattern, with states in total increasing sales taxes in 1993, 1994, and 1995, followed by seven straight years of sales tax cuts from 1996-2002. Based on National Council of State Legislature's State Tax Actions data.

[4] In at least some states, such as Oregon, the legislature can repeal a tax break without triggering the supermajority requirement if the revenue is used to cut other taxes or reduce tax rates, such that no new revenue is realized by the state. Other supermajority requirements, including the one in California, have no such exemption.

[5] States often describe the many tax breaks they offer in a "tax expenditure report.” For a discussion of these reports and how they can be improved, see Michael Leachman, Dylan Grundman, and Nicholas Johnson, Promoting State Budget Accountability Through Tax Expenditure Reporting, Center on Budget and Policy Priorities, updated May 24, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3491.

[6] Citizens for Tax Justice and Institute on Taxation and Economic Policy, Corporate Tax Dodging in the Fifty States, 2008-2010, December 2011, at http://www.itepnet.org/pdf/CorporateTaxDodgers50StatesReport.pdf.

[7] Testimony of Samuel C. Thompson, then Dean of the University of Miami Law School, before the Subcommittee on the Constitution of the House Judiciary Committee on March 18, 1997.

[8] A 21st Century Budget Process for California: Recommendations of the California Citizens Budget Commission (Los Angeles, Center for Governmental Studies, 1998).

[9] Ashali Singham and Nicholas Johnson, "States Can Avert New Revenue Loss And Protect Their Economies by Decoupling From Federal Expensing Provision,” Center on Budget and Policy Priorities, April 14, 2011.

[10] Standard & Poor’s, U.S. State Ratings Methodology, Global Credit Portal, Ratings Direct, January 3, 2011, available at http://www.nasra.org/resources/StateRatingsMethodology.pdf.

[11] Moody’s Investor Services, Global Credit Research Press Release, “Moody’s Downgrades State of Nevada’s General Obligation Bonds to Aa2 from Aa1,” March 24, 2011. Moody’s Investor Services, Global Credit Research Press Release, “Moody’s Downgrades State of Arizona’s Issuer Rating to Aa3 from Aa2,” July 15, 2010.

[12] Moody's wrote that positive features of the state's outlook were “counterbalanced by constitutional constraints on the ability to raise revenue” and other factors. See Moody’s Investors Service, "Moody's Affirms Oklahoma's Aa2 General Obligation Rating and Stable Outlook," February 2, 2012. Oklahoma’s constitution requires a three-fourths vote to raise taxes (not including eliminating or reducing tax breaks).

[13] James M. Poterba and Kim S. Reuben, Fiscal Rules and State Borrowing Costs: Evidence from California and Other States, Public Policy Institute of California, 1999, http://www.ppic.org/content/pubs/report/R_1299JPR.pdf.

[14] Institute on Taxation and Economic Policy, “Building a Better Gas Tax,” December 2011. Note that some states index their gasoline taxes automatically to rising prices. Such automatic increases presumably would not be affected by a supermajority requirement.

[15] For a more detailed discussion, see “Budget Cuts or Tax Increases at the State Level: Which Is Preferable When the Economy Is Weak?” Center on Budget and Policy Priorities, April 28, 2010.

[16] For example, some states recently have found significant savings by reducing spending on prisons while still protecting public safety. See Michael Leachman, Inimai Chettiar, and Benjamin Geare, “Improving Budget Analysis of State Criminal Justice Reforms: A Strategy for Improving Outcomes and Saving Money,” Center on Budget and Policy Priorities and the American Civil Liberties Union, January 11, 2012.

[17] Reforming California’s Budget Process: Preliminary Report and Recommendations of the California Citizens Budget Commission, (Los Angeles: Center for Governmental Studies, 1995), pp.43-47. The requirement of a two-thirds supermajority of each house to pass a budget in California has since been repealed.

More from the Authors

Areas of Expertise