The Current Services Baseline: A Tool for Understanding Budget Choices

Introduction

When governors and legislative bodies put forward state budget proposals, they almost always recommend changes in state policies, such as increases or reductions in the number of people eligible for state services, alterations in formulas used to fund schools and local governments, changes in staffing levels, and so on. To understand the potential fiscal impact of these policy changes, policymakers and the public need to know how they — and the dollar amounts budgeted for them — compare to the state's current practices. Without a published current services baseline, such a comparison is next-to-impossible. Yet only 22 states (plus the District of Columbia) produce a current services baseline to make such a comparison possible.

A current services baseline is a reality check in the budget process. It indicates what the state would have to spend on a given program, such as health care for poor children, property tax reductions for senior citizens, or economic development assistance to businesses, in order to maintain the program at its current level, in the absence of any policy changes. It reflects the impact of factors that cause year-to-year variations in the cost of providing a given service and the number of people who use it, such as inflation, changing wage levels, population growth, and economic and demographic shifts, as well as enacted policy changes that have yet to take effect.

A current services baseline deliberately excludes the impact of proposed policy changes, such as changes in per-pupil school funding or Medicaid eligibility. This approach allows policymakers and the public to compare the baseline to a proposed or enacted budget allotment to see whether the budget reflects either a spending cut or a spending increase. Such clarity is especially important at times when states are struggling to maintain a balance between revenues and spending levels, as they are expected to do for at least the next several years.

Current services baselines are essential for budget transparency and accountability because they let the public see what the budget really does and then hold their elected officials accountable for those changes. But unlike the federal government, which has included information on the cost of maintaining current services in the President's annual budget proposal since the mid-1970s, most states do not follow this practice. This report explains how a current services baseline improves the state budget process, summarizes states' current practices in this area, and suggests ways that states without current services baselines could design them.

A Current Services Baseline Provides a Reality Check in Budget Process

A current services baseline projection (sometimes called a "current services budget") measures how much it will cost a state in an upcoming budget period to deliver the same quantity and quality of services to residents it is delivering in the current budget period, [1] taking into account the impact of factors such as:

- Inflation and other changes in the per-person cost of providing the programs and service. (General inflation is not always the appropriate measure of these cost changes. In health programs, for example, medical cost growth would be more appropriate.)

- Any expected changes in the number of people utilizing those services and benefits due to population growth or other factors.

- Any previously enacted rule changes that have not yet phased in, ongoing formula-based adjustments (such as a school funding formula based in part on population growth), and other factors that would require statutory changes to undo.

A current services baseline does not commit lawmakers to any particular action; rather, it provides a neutral benchmark against which to compare budget proposals or an enacted budget. For instance, proposed budgets typically (1) indicate the amount spent on each program in at least one past year, (2) estimate the amount being spent in the current year, and (3) recommend a level of spending for the next year (or biennium). Without a baseline, legislators and the public are likely to compare the spending recommendations to the current-year estimate or the prior-year actual figure; this is often a woefully inaccurate comparison, since circumstances may have greatly changed.

To provide a simple example, consider a Department of Motor Vehicles in a state where automobile ownership is on the rise and where there is no excess staff capacity. A current services baseline would show what the DMV would need to spend to keep up with increased demand for drivers' licenses and auto titles as well as other increasing costs. This information is useful because if the governor proposes funding below the baseline, legislators and the public can see at a glance that the agency cannot make ends meet without changing policies (e.g., slower processing times or improved technology) and so can demand details on the real-world impact of the funding change. If the governor proposes funding above the baseline, legislators and the public should expect details on what additional services the DMV would provide with the extra funding.

Current services baselines are neither a radical nor a new idea. At the federal level, current services baselines have been an important part of the budget process for three decades. They serve as a common basis for "scoring" (determining the cost or savings of) changes to existing programs. Having an agreed-upon baseline is an important element of the current debate over future federal deficits and how to address them; the full extent of the problem and the impact of proposals to reduce spending or raise revenues would not be known without the information that current services projections provide.

They are common at the state level also. Twenty-two states plus the District of Columbia regularly prepare some form of current services baseline, although their comprehensiveness varies significantly. The examples below from two such states, Connecticut and North Carolina, illustrate the kind of information such a baseline can provide.

Example 1: Connecticut

The Connecticut governor's proposed budget includes an estimate of the cost of continuing programs at current-law levels. The table below shows selected columns from the table for the Department of Public Health in the governor's FY 2011-2013 budget proposal. (Connecticut has a biennial budget and prepares current services estimates for both years of the budget. We show only the first year.)

| Agency Programs by Total Funds (net of reimbursements) |

2010-2011 Estimated |

2011-2012 Current Services |

2011-2012 Recommended |

| Health Initiatives | 163,249,013 | 164,095,232 | 156,965,352 |

| Regulatory Services | 20,371,606 | 17,734,158 | 17,458,302 |

| Commissioner's Programs | 7,796,061 | 7,616,922 | 7,483,054 |

| Laboratory Services | 10,994,973 | 14,253,591 | 12,188,805 |

| Healthcare Systems | 17,327,215 | 18,315,153 | 18,158,611 |

| Agency Management Services | 8,198,355 | 10,687,238 | 9,898,357 |

| Other Public Health | 29,785,881 | 32,010,664 | 31,886,389 |

| Total – Gross | 257,723,104 | 264,712,958 | 254,038,870 |

| Less turnover | 0 | -1,200,000 | -1,200,000 |

| Total – Net | 257,723,104 | 263,512,958 | 252,838,870 |

Connecticut's practice of providing a program-level summary of significant changes to the current services level allows policymakers and the public to easily identify policy changes by noting the difference between the current services level and the recommended funding amounts. For example, this table shows that recommended funding for Laboratory Services for FY 2011-12 ($12,188.805) is more than the amount spent in FY 2010-11 ($10,994,973) but less than the amount required to maintain current-law service levels ($14,253,591).

In Connecticut's case, these estimates are not as useful as they could be because the budget does not always explain the methodology used to estimate the current services level. Nevertheless, they provide a clear starting point for anyone concerned about the impact of the proposed budget on the state's ability to provide these services.

Source: FY2011-2013 Governor's Biennium Budget, Part 2, Budget-in-Detail, p. 273.

A Current Services Baseline Improve a State Budget in Numerous Ways

There are at least five specific ways that a current services baseline improves state budgeting.

- It provides an honest assessment of the state's overall fiscal health compared to the current year. Before debate begins on a spending plan for the upcoming fiscal year, policymakers should know what the state's basic fiscal situation is. Will the state likely have enough resources to expand or maintain services at current levels, or must it cut programs or raise revenues to balance its budget?

States already know what the revenue side of the budget looks like from their baseline revenue forecasts, as noted above. But revenues alone can paint a misleading picture of a state's budgetary position. When revenue is growing strongly, as it did in the late 1990s, a current services baseline provides a clear picture of how much surplus revenue is likely to exist after the state meets its current spending needs. During an economic downturn, as in recent years, a current services baseline allows an honest evaluation of the size of the budget shortfall. It can also provide warning of future problems, either for the budget as a whole or for a particular program.[2]Example 2: North Carolina

The North Carolina governor's budget proposal includes a "continuation" or "base" budget, which estimates the cost of continuing existing programs and is used as the baseline for measuring the impact of budget proposals. The table below shows the continuation budget for the major education programs compared to spending in recent budgets.

Program 2010-2011 2011-2012 Base Budget 2011-2012 Recommended Public Education 7,085,588,912 7,923,543,951 7,572,712,912 Community Colleges 1,055,135,961 1,102,475,214 1,016,629,522 University System 2,666,935,206 2,887,492,464 2,657,835,835 The governor's budget for 2011-2012 provides more state funding for Public Education (K-12 schools) than in the prior budget but less than the amount needed to maintain existing support for these schools.

This table is an example of why a current services budget can be helpful. It allows observers to sort out the effects of a decrease in temporary funding — in this case, the expiration of emergency federal stimulus aid — from changes in the state's longer-term funding for a program. The base budget figure for Public Education (that is, the cost of maintaining current services) is $7.9 billion, or considerably higher than the $7.1 billion the state spent in 2010-2011. One of the main reasons is that the federal government was paying a much larger-than-usual share of North Carolina's education costs in 2010-2011. Thus, less state money was required in 2010-2011.

Because the emergency federal aid ended before state revenues recovered from the recession, fully funding support for Public Education would have required significant cuts in other areas or tax increases. In this case, the governor recommended a funding level of $7.6 billion, enough to only partially fill the gap left by the expiration of federal assistance. A current services baseline makes these kinds of trade-offs much more transparent.

Source: Governor's Recommended Budget FY2011-2013; historical spending (FY2011): Appendix Table 10

- It helps legislators and the public understand a proposed budget's likely consequences for a specific service or program. If a governor's budget includes more dollars for Medicaid, those added dollars may simply be needed to maintain the current program in the face of higher medical costs or an increase in the caseload; without a baseline, the public will not be able to judge whether the proposed "increase" represents an expansion of the program. But if the budget proposes a higher or lower level of spending for a given service than the amount in the current services baseline, communities and individuals can expect to receive higher or lower levels of services.

- It provides a neutral, consistent way to evaluate policy changes across agencies and functions. It can be difficult to understand how much of a particular service a proposed funding level would actually provide. In some states, there is little consistency among programs in the way budget information is presented, and various agencies may or may not publish information on how much spending would be needed to continue current policies.

- It can improve government efficiency. A regular, thorough examination of each program's costs and caseload can help policymakers and the public identify inefficiencies and programs that are no longer needed. And it can help "right-size" programs, avoiding over- or under-funding them.

- It can allow for the implementation of sensible budget controls such as PAYGO. Today in most states, it is impossible for policymakers to know whether demands for program increases or tax cuts are affordable over the longer term. This impedes optimal decision-making and leaves states vulnerable to serious long-term budget problems. To address a similar problem, the federal government uses a method known as PAYGO (pay-as-you-go) that requires Congress to offset the cost of legislated spending increases or revenue reductions compared to a baseline through other revenue increases or spending reductions.

PAYGO is superior to the draconian, inflexible limitations on revenues or expenditures that some have promoted in states. It imposes budget discipline while recognizing the need to adapt to changing circumstances in a responsible manner. And, unlike many rigid tax or expenditure limitations, PAYGO maintains legislative prerogatives over the budget and allows lawmakers to expand programs or reduce taxes when it is affordable. Regularly preparing a current services baseline would be an important step towards implementing PAYGO if desired.[3]

A current services baseline is useful at many points in the budget process. In the budget preparation process, which begins months prior to the governor's formal submission of a recommended budget, when state agencies prepare their budget requests for the coming year and executive budget staff evaluate these requests. Current services budgeting builds a regular examination of each program's costs and efficiencies into the budget process from the start.

As legislative committees consider the impact of the budget on the state's ability to deliver services, a current services baseline can make it much easier for them to review the proposed policy changes. Using the baseline, they can quickly determine which funding changes result from economic and demographic changes and which result from decisions to provide more or fewer services.

During the public debate over the budget, a current services baseline is of particular importance to citizens, reporters, and nonprofit organizations (such as budget and fiscal watchdog groups or advocates for particular services or benefits). These groups need to know what policy changes are included in a budget proposal, but unlike legislative or agency staff, they often do not have the time or information to prepare their own estimates of the cost of continuing current services to serve as a point of comparison.

States Already Have Information Needed for Current Services Baselines

Almost any state should be able to produce a current services baseline using information that individual agencies already prepare as part of the regular budget process. (States that do not already prepare this information ought to be doing so, in order to make sound decisions.) There are two steps to calculating the baseline.

The first step is to determine the current full-year cost of each program. For most programs, this equals the amount of spending in the current year, but in some cases it will be more or less than that amount. For example, if a program expansion started in the middle of the current year, spending for this expansion must be adjusted to reflect its full-year cost. Similarly, any unusual costs in the current year, such as one-time costs relating to an emergency, should be removed. Finally, if a program is scheduled to end after the start of the current year, the program and its related costs also should be removed.

The second step is to factor in changes in the program's cost by determining the number of recipients and the cost per recipient in the current year and then estimating the cost for the coming year by factoring in expected changes in per-recipient costs and the number of recipients. In addition, if a previously approved expansion (such as the opening of a new prison or a phased-in expansion of Medicaid eligibility) is scheduled to start in the coming year, this must be taken into account.

When estimating costs as part of preparing a budget, some states distinguish between "mandatory" and "discretionary" programs. Some programs are established by law to provide a benefit to any entity (such as a person, local government, or nonprofit organization) that meets certain eligibility criteria. For example, individuals with incomes below a specific level are eligible for medical assistance; if the number of people with incomes below that level increases, the state is required to provide that assistance. Spending changes like this, which the program's statutory provisions require, are considered "mandatory" unless law or policy is changed.

In contrast, other programs are considered "discretionary," which means their funding level is set each year as part of the budget process. Possible examples include grants to local schools for staff training programs for a direct service such as running the Department of Motor Vehicles.

Most states that prepare a current services baseline factor in price increases and population or caseload changes for mandatory programs, but for discretionary programs they apply a standard inflation adjustment (such as the Consumer Price Index or the U.S. Bureau of Economic Analysis' price deflator for state and local government purchases) or simply assume that funding will remain at the same level as in the current budget. This is similar to the federal current services baseline, in which baseline funding estimates for discretionary programs are adjusted only for the overall inflation rate while funding for mandatory programs takes into account expected changes in prices, number of recipients, and sometimes utilization patterns.

The most accurate current services baselines reflect the fact that the rate at which the cost of a given service changes can depend in part on the service — the costs of providing health care and education, for example, may grow at very different rates. Changes in the number of recipients of services often differ by program as well. To generate accurate results, therefore, states often need to use an estimate of changes in the subpopulation that the program serves, rather than an estimate of changes in total population, in preparing their baseline.

Since most states already prepare forecasts of future costs and changes in the state population and many subpopulations as a part of their budget process, they are well prepared to calculate a current services baseline. There may be disagreements about particular aspects of these forecasts, but as long as the projections on which the baseline is founded are stated explicitly and published along with the baseline, analysts can assess the impact of specific projections on the baseline.

A current services baseline is most useful to budget analysts if it is very detailed. For example, an estimate of the cost of continuing each element of a state's public health programs is more helpful than an estimate of the cost of continuing the state health agency as a whole.

Also, a current services baseline is best for long-term planning if it covers more than just the coming year. Current services spending projections for two to five years, when paired with revenue projections for this same period, allow a state to assess its future fiscal health.

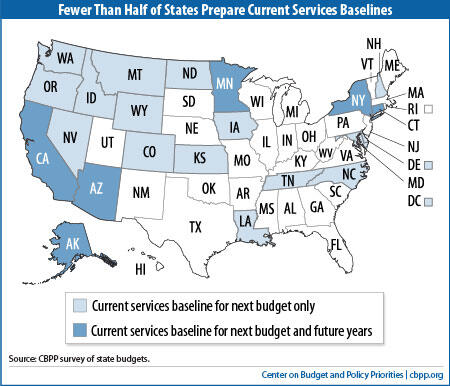

Twenty-Two States Plus DC Prepare Current Services Baselines

| TABLE 1: States that Prepare Detailed Current Services Baselines |

|

| State | Length of Projection |

| Alaska | 10 years |

| Arizona | 2 years |

| California | 5 years |

| Colorado | Next Budget |

| Connecticut* (B) | 5 years |

| Delaware* | Next Budget** |

| District of Columbia | Next Budget |

| Idaho | Next Budget |

| Iowa | Next Budget |

| Kansas* | Next Budget |

| Louisiana | Next Budget |

| Maryland | Next Budget** |

| Minnesota (B) | 4 years |

| Montana (B) | Next Budget |

| Nevada (B) | Next Budget |

| New Hampshire (B) | Next Budget |

| New York | 4 years |

| North Carolina (B) | Next Budget |

| North Dakota (B) | Next Budget |

| Oregon (B) | Next Budget |

| Tennessee | Next Budget |

| Washington (B) | Next Budget |

| Wyoming (B) | Next Budget |

| Number of states: 23 (including DC) | |

| Source: CBPP survey of executive budget documents. (B) means state has a biennial budget. *State Notes: Connecticut officially adopts a biennial budget but annually prepares an updated budget. Delaware suspended preparation of a current services analysis for fiscal year 2012. Kansas projects some agencies on a biennial basis. ** Some states, including Delaware, Florida, Georgia, Maryland, Pennsylvania, and West Virginia prepare multi-year expenditure projections that are similar to current services projections. These projections are not current services projections, however, because they incorporate policy changes by using the Governor's recommended spending for the next budget as the starting point rather than the current year's spending. Delaware and Maryland prepare current services estimates for the next budget but project later years based on their governors' recommendations. |

|

Twenty-two states and the District of Columbia prepare current services baselines, according to our survey of state budgets. [4] (See Table 1.) Six of these states — Alaska, Arizona, California, Connecticut, Minnesota, and New York — project beyond the next budget year. The remaining 16 states[5] and the District of Columbia prepare a current services baseline for just the next annual or biennial budget.

The methodologies used for calculating a current services baseline vary across the states but contain many common elements:

- Program changes. All the states include in their current services estimates any previously approved program changes that have not yet taken effect during the base year. In addition, some states include other factors in their current services baseline projection besides those already noted. For example, Connecticut adjusts the baseline projection to include costs mandated by statute or court order.

- Inflation. Most states that prepare current services baselines adjust for changing prices throughout the budget, typically using a broad-based measure such as the Consumer Price Index for most of the budget. [6] Several use both a general price index and one or more other indices that are relevant to specific programs so as to incorporate program-specific cost drivers that the general inflation rate might not reflect, such as health care or energy costs. For example, Connecticut and New York use a medical inflation rate for Medicaid.

- Population and caseload changes. All these states include the effect of population or caseload changes on program costs. Most states go beyond projected changes in the general population, instead using projected changes in the population that the specific programs serve. For example, a number of states project the number of residents expected to be eligible for Medicaid in order to estimate the program's future cost. And many states use forecasts of the number of school-age children in order to estimate the current-services cost of school aid.

- Employee costs. State employee salaries make up a significant share of state budgets. A number of states estimate future costs by factoring in salary increases included in collective bargaining agreements where applicable. Others assume that salaries will increase by the amount of inflation. Some states estimate growth in state employee benefits using projections of health care costs that exceed general inflation.

An ideal current services baseline would include the following features:

- It would adjust prior-year spending to reflect program-specific inflation, caseload or population changes, and enacted policy changes that haven't taken effect.

- It would be published as part of the regular budget document.

- Its underlying assumptions would be clear and published in the budget document.

- It would provide estimates at a detailed level, not just for whole agencies.

- Its projections would extend beyond the budget year for two to five years.

Conclusion

States often already have the information available to calculate current services baselines, but fewer than half of them do so on a regular basis. By preparing and publishing these baselines, states can help involve a broad segment of their residents in decisions about how their tax dollars are spent, as well as provide policymakers with important information to help them evaluate policy proposals.

End Notes

[1] The specific name of current services-type analyses can differ by state. These analyses are also called continuation budgets or maintenance budgets, among other things.

[2] It could be problematic to establish a current services baseline right after a recession, when current expenditures are well below the level required to adequately serve residents. As an alternative, a state could use the same methodology that is used to construct a current services baseline to compare current levels of spending with the cost of providing a pre-recession level of services. Alongside its current services baseline, a state could provide a "pre-recession services baseline" to further inform decision-making about how best to manage its economic recovery.

[3] For more information on state PAYGO see Iris J. Lav, "PAYGO: Improving State Budget Discipline While Retaining Flexibility," Center on Budget and Policy Priorities, September 22, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3587.

[4] Additional states incorporate some elements of current services baselines for some programs but do not prepare comprehensive reports. For the purposes of this report, a state is classified as preparing a current services baseline if it estimates the current services cost of all major programs with at least agency-level detail.

[5] These states are Colorado, Delaware, Idaho, Iowa, Kansas, Louisiana, Maryland, Montana, Nevada, New Hampshire, North Carolina, North Dakota, Oregon, Tennessee, Washington, and Wyoming.

[6] Kansas, Maine, Minnesota and North Dakota are examples of states with current services baselines that generally do not adjust for inflation throughout the budget. In specific instances, such as medical inflation associated with Medicaid, Arizona does factor in inflation. Similarly, while Virginia does not factor in inflation for all programs, it does apply inflation for a number of major expenditure items, including Medicaid, school aid, and some state employee benefits.

More from the Authors