Policymakers Often Overstate Marginal Tax Rates for Lower-Income Workers and Gloss Over Tough Trade-Offs in Reducing Them

“Our plan would … ensure that our tax code works together with the federal welfare system, so that low-income workers are able to climb into the middle class without having to overcome 80%-100% effective marginal tax rates,” Republican Senators Mike Lee and Marco Rubio wrote in a recent op-ed explaining the broad outlines of their tax reform proposal.[1] “Often when a worker gets a modest pay raise, higher taxes and lost benefits conspire to leave the person with little extra money in their pocket.”

As reflected in the Lee-Rubio op-ed, some in Washington are focusing more attention on the issue of how both tax-based and safety net program benefits for low- and moderate-income families phase down in response to higher earnings, how the phase-down translates into what are known as “marginal tax rates” (as explained below), and how those rates affect the work habits of beneficiaries. This issue surely deserves attention. However, some overstate the magnitude of these tax rates — as Senators Lee and Rubio did — and their impact on employment while overlooking the tough trade-offs involved in trying to reduce these rates.

The phase-down rate of program or tax benefits is often called a “marginal tax rate” because the reduction in benefits as earnings rise resembles a tax (with “marginal” referring to the effect on the next dollar of income). If, for example, a worker faces a marginal tax rate of 30 percent, that worker will lose 30 cents of each additional $1.00 he or she earns through a combination of reduced benefits and higher taxes. Many policymakers focus on marginal tax rates out of concern that workers who face higher rates are likelier to not work, to work less, or not to look for higher paying jobs than if they faced lower rates.

House Budget Committee Chairman Paul Ryan’s March 2014 report on the safety net (“The War on Poverty 50 Years Later”) illustrates how policymakers and others can oversimplify the marginal tax rate issue. The report argues that marginal tax rates for low-income people are very high and create a “poverty trap” in which families have little or no incentive to try to increase their earnings.[2] Unfortunately, the report overstates the marginal tax rates that most low-income people face. It also ignores work by leading researchers that finds that the safety net is responsible for lifting 40 million people out of poverty even after considering the impact of marginal tax rates on workers’ employment.

The marginal tax rates that low-income families face vary greatly based on their incomes, the number of people in their family, and the benefit programs in which they participate. Among low-income families, very poor families — those who are out of work or have earnings that leave them well below the poverty line — face the lowest marginal tax rates, while families with incomes modestly above the poverty line that receive more than one benefit that’s phasing down can face significantly higher rates.

Indeed, parents who are out of work or have very low earnings typically face a negative marginal tax rate — that is, if they can boost their earnings, their total income will rise by even more than their earnings rise because they’ll receive additional tax benefits that exceed the taxes they pay and the loss in other benefits. That’s because the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) increase as earnings rise above very low levels, effectively operating as wage supplements. That creates a strong incentive for parents to work rather than not work.

Some other low-income families, typically those with incomes modestly above the poverty line, can face marginal tax rates of around 65 percent over a relatively narrow income range, such as between about $18,000 and $25,000 for a family of three. (Their marginal rate can be higher if they receive benefits that go to only a modest minority of low-income households, such as housing assistance or child care assistance.)

For workers deciding whether to work more and by how much, however, their marginal tax rate may be less important than their average tax rate. While the former refers to taxes and benefit losses on the last dollar of income, the latter refers to taxes and benefit losses as a percentage of all pre-tax earnings. Thus, if a parent takes a $20,000 job and her income after taxes and benefits is $18,000, her average tax rate is 10 percent. While families with incomes modestly above the poverty line can face high marginal tax rates, they typically face very low or even negative average tax rates because they receive significant EITC and CTC benefits that often offset most or all of the lost benefits and higher taxes they face due to working. While the marginal tax rate may influence a worker’s decision about whether to try to increase her hours of work or seek a higher-paying job, the average tax rate is far likelier to affect her decision about whether to go to work in the first place.

Given this strong incentive to work rather than not work, we shouldn’t be surprised that research suggests the actual reduction in hours worked or wages earned due to marginal tax rates created by benefit phase-downs is modest. In addition, research suggests, the lack of a larger behavioral response also may reflect the fact that (1) many families don’t fully understand how benefits (particularly tax credits) adjust as earnings rise; (2) low-wage workers often have limited ability to control the number of hours they work or to find higher-paying jobs; and (3) many families that face high marginal tax rates do so for only relatively short periods of time.

Across the political and ideological spectrum, policymakers and opinion leaders share concerns about marginal tax rates and generally agree that, all else being equal, lower marginal tax rates are preferable to higher rates. The problem is that all else is not equal, and reducing marginal tax rates entails hard policy trade-offs.

Specifically, policymakers can reduce the marginal tax rate in a program in only three ways: (1) phase down its benefits more slowly, thereby extending benefits higher up the income scale and increasing program costs; (2) scale back assistance that poorer families receive so that benefits can phase down more gradually without raising costs, which would increase the extent and depth of poverty; and (3) eliminate assistance for needy individuals and families altogether.

And if policymakers consider options that would increase federal costs, they also must consider the impact of the program cuts and/or tax increases that would be used to offset the higher costs. For example, policymakers could pay for a proposal to lower the EITC’s phase-down rate in a number of ways, including by closing inefficient tax preferences that mainly benefit high-income people, by reducing other tax benefits for low-income families, or by cutting other programs. Those financing mechanisms have their own pros and cons.

Marginal tax rates from benefit phase-downs result from the interaction between two broadly agreed-upon policy goals: providing needed assistance to individuals and families who face difficulties making ends meet, and keeping costs down by not providing help to those whose income is more adequate. Any serious discussion of marginal tax rates must grapple with the fundamental tension between providing adequate help to those in need at a reasonable cost and avoiding high marginal rates.

Low-Income Households’ Marginal Tax Rates Are Often Overstated

SNAP (formerly food stamps), the EITC, Medicaid, and subsidies provided under health reform help low-income families pay rent, buy food, and obtain health care. These benefits phase down as family earnings rise, imposing a “tax” that reduces the family’s net gain from increased earnings. The marginal tax rate represents the total increase in taxes and/or loss of government benefits for each additional dollar of earnings. For example, a marginal tax rate of 30 percent means that each additional dollar of income will cause a loss of 30 cents through higher taxes and/or lower benefits. A family’s marginal tax rate depends on its income, size, number of children, benefits received, and the phase-down formula.

Some policymakers and analysts have expressed concern that high marginal tax rates may cause workers to choose not to work, to work less, or not to seek higher paying jobs. Some also are concerned that high marginal tax rates make it harder for families to move up the economic ladder when their earnings rise.

Unfortunately, discussions of these issues often overstate the marginal tax rates that most low-income families actually face. For example, the March 2014 report on the safety net from House Budget Committee Chairman Paul Ryan[3] highlights a statement in a Congressional Budget Office (CBO) analysis that “some low-income households face implicit marginal tax rates of nearly 100 percent,” but fails to mention data from the same CBO report showing that most low-income households’ marginal tax rates are substantially lower.[4] The CBO report shows, for example, that 75 percent of families with incomes between 100 and 150 percent of the poverty line faced marginal tax rates of less than 45 percent in 2012, and about 90 percent of these families faced marginal rates below 60 percent. Similarly, a 2013 report by the Brookings Institution’s Hamilton Project states that “[A] low-income, single parent can face a marginal tax rate as high as 95 percent”[5] without clarifying that most low- and moderate-income families do not face marginal rates that high.

To arrive at marginal tax rates in the 95-100 percent range, a family must participate simultaneously in multiple benefit programs — including those that assist only a small share of those eligible — and its income must be high enough that several of these benefit programs are phasing down at the same time but not so high that benefits have phased out. That combination of factors applies to only a small share of low-income families.

Less than one-third of families with children that are poor enough to qualify for Temporary Assistance for Needy Families (TANF) cash assistance receive it, for example. Just one-quarter of the low-income families eligible for housing assistance — and just one in six children in low-income working families eligible for child care assistance — receive help from those programs, largely because of their limited funding.

Among low-income families, marginal tax rates are typically lowest among poor families and highest among those with incomes somewhat above the poverty line. A key reason that most poor families do not face very high marginal tax rates is that at low income levels, the EITC and CTC rise with additional earnings, offsetting the marginal tax rates that phase-downs in other programs (such as SNAP) can create and providing a work incentive.

In fact, families in which a parent has very low earnings or is out of work — the very families whose employment rates policymakers are generally most concerned about — often face a negative marginal tax rate. As their earnings rise, their after-tax incomes rise by more than their earnings.

- Johns Hopkins University’s Robert A. Moffitt, a leading expert in this field, examined the marginal tax rates of low-income families that receive SNAP and found that among families with children that also receive other income supports and might theoretically face high marginal tax rates, “the vast majority have earnings so low that they face negative cumulative marginal tax rates.” That’s largely because most SNAP recipients’ incomes are in the range where EITC and CTC benefits are phasing in and because SNAP benefits do not start to phase down with the first dollar of earnings.[6] Moffitt also notes that while families receiving child care or housing benefits would face higher marginal tax rates, most low-income families don’t receive those benefits.

- Researchers Stephen Holt (of Holt Consulting and a long-time EITC expert) and the University of Washington’s Jennifer Romich examined tax and administrative records for about 2.5 million Wisconsin residents over the 2000-2002 period. They found that only 11 percent of poor single parents with children — and fewer than 10 percent of those with incomes between 100 percent and 250 percent of the poverty line — faced marginal tax rates that topped 50 percent in 2001 or 2002. [7] They also found that most families with marginal tax rates over 50 percent in one of those three years (2000-2002) had rates below 50 percent in the other two years.

- Urban Institute researchers measured the marginal tax rates that single-parent families with two children would face in each state if they received TANF, SNAP, and refundable tax credits (the EITC and CTC). They found that families raising their incomes from 100 percent to 150 percent of the poverty line could face marginal rates in the 40-60 percent range in most states.[8] However, Moffitt and other researchers who calculate marginal tax rates based on actual benefit receipt find that most families do not face rates this high because so few eligible low-income families receive TANF.

The high marginal tax rates that Chairman Ryan and others cite reflect themaximum rates only for the smallgroup of families that receive benefits from multiple programs simultaneously and have incomes within a relatively narrow range, typically starting near or modestly above the poverty line. And the data show that a substantial majority of workers with incomes near the poverty line ($19,790 for a family of three in 2014) already work at, near, or more than full time for all or most of the year. For example, 77 percent of adults who live in families with children and earn between $15,000 and $22,000 work at least 50 weeks during the year.[9] While a high marginal tax rate could affect a worker’s decision to seek higher pay or longer hours, it shouldn’t affect the worker’s decision of whether or not to work.

How Core Safety Net Programs Affect Marginal Tax Rates

The benefits with the biggest impact on low-income households’ marginal tax rates are refundable tax credits, SNAP, and health insurance (through Medicaid, the Children’s Health Insurance Program or CHIP, and health reform’s new insurance exchanges). They are the largest benefit programs for low-income working families and are available to all eligible families that apply.

A close look at these programs shows that the EITC and Child Tax Credit help ensure that the safety net overall rewards work over not working for families with children, and that health reform has significantly reduced work disincentives for many low-income parents. (We limit the discussion here to families with children because they are eligible for significantly more government benefits than able-bodied adults without children. Those without children do not face steep marginal tax rates because they do not receive much in the way of benefits that phase down.[10] Similarly, because they generally have access only to a very small EITC, they do not experience significant negative marginal tax rates if they take a job.)

EITC and Child Tax Credit Create Incentive to Work

An important fact often lost in discussions of marginal tax rates is that today’s safety net strongly rewards working over not working. Indeed, one of the major changes in social policy in recent decades has been the conversion of the safety net primarily into what analysts call a “work-based safety net.”[11]

Today’s safety net does relatively little for families in which able-bodied adults are not working. Basic cash assistance programs for families with children help only about one-third of families with children that meet the program’s eligibility criteria in their state — and an even smaller share of all poor families with children.[12] (Only 25 of every 100 poor families with children received TANF cash assistance in 2012, down sharply from 82 of every 100 such families in the 1979 and 68 out of every 100 in 1996 under the Aid to Families with Dependent Children, or AFDC, program, TANF’s predecessor.) Similarly, only about one-quarter of eligible low-income families with children receive housing assistance.

Most poor families with children in which a parent isn’t working can count only on SNAP, Medicaid, and child nutrition benefits (school meals or WIC, the Special Supplemental Nutrition Program for Women, Infants and Children). These benefits do not provide cash income and leave many families hard pressed to pay for basics such as rent.

If, however, the parent can get a job, the family receives not only earnings but also the EITC and CTC, which are available only to families with earnings. While SNAP benefits begin phasing out at fairly low earnings levels, the EITC and CTC typically more than make up for that loss.

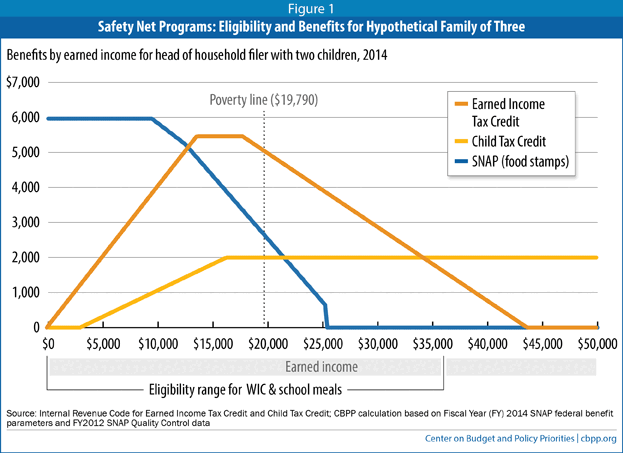

Figure 1 shows how the three income-support programs with the broadest reach among low-income families — SNAP, the EITC, and the CTC — phase in and out as earnings rise for a single parent with two children.[13] Families with earnings below $13,650 face a negative marginal tax rate as earnings rise because their combined EITC and CTC grows faster than their SNAP benefits fall and their payroll taxes rise. Then, between $13,650 and $17,830, SNAP benefits fall by about 24 to 36 cents for every dollar in added earnings — but the EITC remains steady and the CTC continues to rise as earnings climb (until earnings reach $16,330). In this income range, the marginal tax rate families face from the combined impact of SNAP, EITC, CTC, and the payroll tax is in the 17-to-44 percent range, with the higher part of the range affecting those with earnings above $16,330. [14]

Between $17,830 and about $25,000, both SNAP and the EITC phase down. As a result, over this narrow income range, marginal tax rates from these two programs and the payroll tax total about 65 percent. This is relatively high, although still well below the 95 percent or 100 percent rates sometimes cited. Figure 1 also indicates that this three-person family is eligible for the main child nutrition programs — WIC and school meal programs — at incomes up to roughly $36,000. The amount of WIC assistance remains the same over the entire eligibility range; school meal assistance falls modestly when income exceeds 133 percent of poverty ($26,320) but then remains fixed until income exceeds 185 percent of poverty.

As noted, families that also receive other benefits such as housing or child care assistance face higher marginal tax rates, as those benefits, too, phase down. That’s particularly true for families with earnings at 100-200 percent of poverty, where the EITC is phasing down as well. For parents with earnings well below the poverty line, in contrast, the phase-in of the EITC and CTC helps to counterbalance the phase-out of these other benefits, leaving most of these families with only modest marginal tax rates.

Moreover, while families with earnings in the $17,830 to $25,000 range often face a relatively high marginal tax rate (the rate on the next dollar earned), their average tax rate (the rate on all of their pre-tax income) remains low and, in some cases, negative. That’s because the EITC and CTC can cancel out some, all, or more than all of the cumulative loss in benefits and increase in other taxes that occur when a family’s earnings rise. This low average tax rate means that families are significantly better off financially if they take a job than if they don’t work, even if their earnings put them in a range where their marginal tax rate is high. The decision about whether to take a job at all rather than not to work is affected more heavily by a family’s average tax rate than the marginal tax rate on its next dollar of earnings.

In his recent book, We Are Better Than This, noted tax expert Edward Kleinbard, a former staff director of the Joint Congressional Committee on Taxation, explains how policymakers have used the EITC to create a strong work incentive. “Congress has wrestled with the problem of the high marginal costs of entering the job market,” Kleinbard notes. “This is the theory behind the Earned Income Tax Credit…which subsidizes low-income wage earners precisely to help with the twin problems of the out-of-pocket costs of holding a job and the forgone safety net benefits that follow when income rises above poverty levels.”[15] He explains that when evaluating the incentives facing an individual regarding whether to work, the question is not the tax rate the individual will face on the last dollar earned but the difference between an individual’s after-tax income and benefits if he or she works and if he or she does not work.

The EITC is highly effective as a work incentive and increases employment rates among low-income parents, a substantial body of research confirms. One notable study found that the positive work incentive provided by the EITC expansion enacted in the mid-1990s did more to induce people to go to work than did welfare reform policy changes such as time limits and work requirements.[16]

Work vs. No Work

To see how the safety net rewards work, consider an unemployed mother of two. Her children receive WIC or school meal assistance and the family is eligible for SNAP and Medicaid. She may receive housing assistance or TANF, but most families in her situation do not. Her family is very poor and she may have trouble keeping a roof over her head if faced with a long stretch of joblessness without another income source.

If this mother can get a job that pays $12,000, her family will receive a sizable EITC ($4,800) and CTC ($1,350) while losing only a modest part of her SNAP benefits ($612) and paying $918 in payroll taxes. The family will remain eligible for Medicaid. Overall, that $12,000 job leads to a $16,630 increase in income. Even if the family receives TANF while not working, the mother will be far better off taking this job than remaining out of work. Assuming the TANF benefits available in the median state, a family of three that goes from receiving TANF and SNAP to having a parent that works at a job for $12,000 will increase its disposable income (including SNAP and refundable tax credits) by almost $11,500. The family’s income will more than double by accepting the job.

To be sure, if the parent can find a job that pays more than $12,000, she will face a higher marginal tax rate. But the family will still be significantly better off financially if she takes the job than if she doesn’t work at all or works at a lower paying job.

That’s not to say that today’s safety net does an optimal job of encouraging work. For example, lack of affordable child care can stand in the way of a parent taking a job. If the parent has young or school-age children and lacks subsidized child care or low-cost care (including after-school care) from relatives, friends, or others, the cost of child care can outweigh the benefit to work. In this example, however, the obstacle to working is not a high marginal tax rate from tax and benefit programs, but insufficient funding for child care programs for low-income working parents.

Ironically, if child care subsidies were available on a sliding scale to all low-income working families that need it, many families’ marginal tax rates would rise, since those subsidies phase down over some income range. But parents with child care needs would have a stronger incentive — and be better able — to take a job, and their employment rates would likely rise.[17]

Medicaid and Exchange Subsidies

Some critics of the Affordable Care Act (ACA) complain that Medicaid and the ACA’s subsidies to buy private coverage in the new health insurance exchanges (also known as marketplaces) raise marginal tax rates. As with other income-tested programs, the impact on marginal tax rates is just one measure on which to judge the programs. These programs provide millions of Americans with access to affordable health care. Moreover, the marginal rate issue is far more complicated than it is often portrayed, especially by ACA opponents.

The ACA expands access to health coverage through public programs (mainly Medicaid) and subsidies to buy coverage in the exchanges. In states that adopt the ACA’s Medicaid expansion, Medicaid provides free or low-cost coverage to poor and low-income children and non-elderly adults with incomes up to 138 percent of the poverty line, or about $27,310 for a family of three.[18] Individuals and families that earn too much to qualify for Medicaid can receive subsidies for private coverage purchased through the exchanges.

Medicaid generally does not contribute to marginal tax rates over most of its income eligibility range because individuals remain eligible for full Medicaid coverage until their incomes reach the eligibility limit.[19] Thus, in states that have adopted the Medicaid expansion, Medicaid doesn’t raise marginal tax rates for people until their incomes get close to 138 percent of the poverty line. If their incomes exceed this level, they become eligible for exchange subsidies, which phase down gradually as income increases. [20] The exchange subsidies raise marginal tax rates modestly for families with incomes between about 138 and 400 percent of the poverty line, the upper eligibility limit for the subsidies. Over this range, premiums for coverage through the exchange are limited to between 3 and 6 percent of income.[21]

While this modest increase in marginal tax rates has received significant attention, the fact that the ACA sharply reduces work disincentives for poor parents with children in states that adopt the Medicaid expansion has received less attention. Before the ACA, parents in most states became ineligible for Medicaid at earnings levels far below the poverty line; the benefit cutoff was just 61 percent of the poverty line for working-poor parents in the typical (or median) state. As a result, working-poor parents risked losing Medicaid if they raised their earnings above this very low level, such as by moving from part-time to full-time work. Sixty-one percent of the poverty line is equivalent to just $1,005 per month for a family of three.

The situation is now very different in the 26 states and the District of Columbia that have adopted the Medicaid expansion. These states have raised Medicaid eligibility to 138 percent of the poverty line, and people who exceed this limit can receive subsidies to buy exchange coverage. As a result, parents no longer face the loss of insurance by raising their earnings, such as by taking a full-time job.

In states that do not adopt the Medicaid expansion, however, an abrupt eligibility cliff remains for parents with very low earnings. In the typical such state, working parents lose eligibility for Medicaid when their income reaches just 47 percent of the poverty line, or $9,300 a year for a family of three. They cannot qualify for exchange subsidies until their earnings more than double, to 100 percent of the poverty line. A parent who moves to a somewhat better job can lose Medicaid but earn too little to qualify for subsidies to purchase private coverage through the exchange. Policymakers in these states who want to reduce work disincentives for poor parents should reconsider their state’s position on the Medicaid expansion.

Research Suggests Marginal Tax Rates Have Only Modest Effects on People’s Work Choices

Many policymakers focus on marginal tax rates out of concern that higher rates will negatively affect an individual’s decisions about whether and how much to work. As economists have long noted, however, the effects of taxes and tax rates on work are not as clear-cut as many people assume, in part due to at least two competing forces:

- Substitution effect: By lowering the net benefit from working an additional hour, a higher marginal tax rate could lead someone to work less than he or she otherwise would. That’s known as the “substitution” effect, based on the idea that reducing the monetary benefits of work will lead people to substitute leisure for work.

- Income effect: On the other hand, someone facing a high marginal tax rate may work more hours in order to reach a particular after-tax income level, such as the level needed to afford rent and other basics. (Many low-wage workers work multiple jobs and long hours, despite low pay, to secure a more adequate income.) That’s known as the “income effect.”

A recent review of research on how various income-tested programs affect people’s choices about work, which Robert A. Moffitt co-authored, concluded that most low-income benefit programs have at most a modest impact in reducing work. Overall, the study found, programs’ work disincentives are sufficiently small as to have “almost no effect” in diminishing the safety net’s success in reducing poverty.[22] They found that, after accounting for these modest overall behavioral effects, the safety net lowers the poverty rate by about 14 percentage points, a very large amount. In other words, one of every seven non-poor Americans would be poor without the safety net. That translates into more than 40 million people.

Another study, by economists Hilary Hoynes and Diane Schanzenbach, found that the introduction of the Food Stamp Program (now called SNAP) in the 1960s and 1970s had modest negative effects on work, though somewhat larger effects than some other studies found.[23] The safety net has evolved significantly since then, however. Creation of the EITC and CTC, for example, helped counterbalance the phase-down of SNAP benefits as earnings rise (among other things), and changes to the SNAP benefit formula reduced marginal tax rates.[24] Moreover, Hoynes and Schanzenbach (along with co-author Douglas Almond) found that the Food Stamp Program had large positive effects on children’s educational outcomes and health as adults, underscoring that no one should evaluate safety net programs by marginal tax rates alone. [25]

In addition, research from the highly regarded Oregon Health Study found no statistically significant differences in employment rates between two randomly assigned groups of non-disabled, low-income childless adults: those who received Medicaid and those who remained on a waiting list.[26]

Why Aren’t the Work Effects Larger?

As discussed above, one reason that marginal tax rates may not have a large impact on employment among low-income families is that many such families do not, in fact, face very high marginal rates — and many who do face them only temporarily, not year after year.

Jennifer Romich and her colleagues suggest additional reasons why even relatively high marginal tax rates may have only modest impacts on the employment and earnings of low-income working families:

One explanation is that low-income workers have little discretion reducing their work hours. If workers cannot select the amount of time they work (hours, shifts, etc.), their only choice may be between working or not working at a given job. A larger issue is imperfect information or understanding. Marginal tax rates are difficult to calculate. When faced with intersecting programs in the welfare system, two knowledgeable observers note that “even economists have a hard time computing marginal tax rates.”… Evidence suggests that front-line caseworkers generally do not explain them … and peers are not a good source of information because individual situations are dependent on a large set of parameters which vary widely even among superficially similar families.[27]

Two studies based on interviews with low-income working families — one by Romich and the other by Laura Tach and Sarah Halpern-Meekin — support these explanations.[28] While the samples in these studies are small, their extensive interviews shed light on why relatively high marginal tax rates have only a modest impact on employment. The studies found the following.

- Low-income workers had only limited understanding of specific program rules. “[C]hanges in means-tested benefits are not obvious to the worker when he or she initially decides to accept a raise, take a second job, or work overtime hours,” the Romich study found. [29] It explains that because different programs adjust benefits on different schedules (some adjusting benefits immediately and others after an eligibility review, while tax-based benefits base eligibility on annual earnings reported at tax-filing time), workers don’t see the impact of an earnings change immediately in all benefits. The Tach study focused on the EITC and found that most respondents understood that they qualified because they worked and had low earnings, but “beyond these general understandings, they were unclear about specifics.”[30]

- Workers did not appear to turn down raises or promotions out of fear that raising their incomes would cost them too much in benefit losses. The Romich study found that “Over the three years of fieldwork, there were no reported instances in which workers directly declined a raise or promotion.”[31] The findings suggest that once in a job, workers generally do not turn down advancement opportunities based on marginal tax rates.[32]

Reducing Marginal Tax Rates Creates Difficult Policy Trade-Offs

All else being equal, policymakers and analysts of all political stripes appropriately prefer lower marginal tax rates. But, in public policy, all else is rarely equal.

There are three ways that policymakers can reduce the marginal tax rate associated with a program (such as SNAP or the EITC). All three involve difficult trade-offs:

- Significantly expand the program so that benefits phase down more gradually and extend higher up the income scale. That raises program costs significantly. Policymakers could offset those added costs by spending cuts or tax increases elsewhere in the budget, but if so, they must consider the pros and cons of both the expansion and the offsets.

- Phase down benefits more gradually and extend them to families higher up the income scale without raising costs by cutting the level of assistance to poorer families. That reduces the support for the families and children who most need help and can push them deeper into poverty.

- Eliminate all assistance to needy individuals and families. That would eliminate the phase-down but leave needy families destitute.

Policymakers also could offset some or all of the marginal tax rates created by one program or tax policy by changing other programs or parts of the tax code. But the basic calculus remains the same. Reducing marginal rates in a program or the tax code costs money; unless policymakers are willing to let budget deficits rise, they must offset that cost through tax increases or program cuts that necessarily involve policy trade-offs.[33]

Here’s an illustrative example. A single-parent family with two children is eligible for a maximum EITC of $5,460 in 2014. When its earnings rise above $17,830, the family’s EITC starts to decline, at a rate of about 21 cents per additional dollar earned. After its income reaches $43,756, it no longer qualifies for the EITC.

If one wants to reduce the EITC’s contribution to marginal tax rates, the credit must phase down more slowly. If the phase-down rate were reduced from 21 percent to 10 percent without any other changes to the EITC, a family would remain eligible for the EITC until its income exceeded $72,430. Even reducing the phase-down rate to 15 percent would enable families with incomes up to $54,230 to receive the EITC.

Reducing the EITC phase-down rate to 10 percent would cost an estimated $17 billion a year.[34] About $7 billion of it would come from extending the EITC to families with higher incomes. And, ironically, while this change would reduce marginal tax rates for families in the EITC’s current phase-down range, it would raise marginal tax rates for households who become newly eligible under the extended phase-down range. The latter group would still be better off than under current law because they’d receive a modest EITC benefit, but their marginal tax rate would be higher.

The only way to reduce the EITC phase-down rate without spending more money on the EITC is to cut assistance to lower-income workers in order to offset the cost of extending the credit to higher-income households. If policymakers did so by reducing the maximum credit, we estimate that they’d have to cut the maximum EITC by more than 20 percent to offset the cost of reducing the phase-out rate to 10 percent. Cuts of that magnitude would significantly weaken the EITC as an incentive for parents to take a low-wage job over not working. They also would make working-poor families poorer and push some families into poverty.

Consider, for example, how reducing the phase-down rate to 10 percent and cutting the maximum credit by 21.5 percent to offset the cost would affect families consisting of a single mother with two children:

- Families between $17,850 and $43,756 would have a lower marginal tax rate than under current law.

- However, many of those families — as well as many families at lower income levels — would be worse off than under current law. Families with incomes between $10,750 and $28,450 would receive a smaller EITCthan under current law and have less income to make ends meet. Families now eligible for the maximum credit would see their EITC cut by more than $1,100.

- Families at the higher income levels that would now receive the credit — those with incomes between $43,756 and $60,691 — would begin receiving a new tax benefit but would face highermarginal tax rates.

The trade-offs don’t stop there. By reducing the maximum EITC, the cost-neutral proposal reduces the incentive for some people to get a job or increase their earnings by limiting the maximum amount that the EITC will provide.

Similar trade-offs exist in other programs. SNAP provides larger monthly benefits to lower-income households, reflecting their greater difficulty in affording food. For most households, SNAP begins to phase down at incomes at or below 60 percent of the poverty line, though some households start losing benefits when their earnings rise above about 10 percent of the poverty line. SNAP benefits phase out at between 24 to 36 cents for every additional dollar earned.[35]

Reducing the rate at which SNAP phases down and thereby extending SNAP up the income scale would raise SNAP costs significantly. If policymakers offset those costs within SNAP, the effects would be highly problematic; SNAP benefits would be cut for very poor households in what would essentially be a shift in basic food aid from poorer households to those near or above the poverty line. Benefits to very poor households are hardly lavish — currently, a very poor household of four that receives the maximum SNAP benefit receives just $1.80 per person per meal. Various studies have found that many poor households already have difficulty securing adequate food to last through the month under the current SNAP benefit schedule, and an Institute of Medicine study last year raised questions about whether the current benefit schedule is adequate.

Conclusion

There is no painless way to reduce marginal tax rates. The structure of major means-tested programs reflects a balance among competing priorities: assisting families that need help, limiting program costs, and avoiding high marginal tax rates. Lowering marginal tax rates would be a positive change if it did not harm poor families, but it could deepen poverty and harm children if its costs were offset by cutting assistance to those already on the edge. In light of the growing evidence[36] that raising the incomes of poor children has important long-term health and education benefits, the substantial risk of causing long-term harm by making poor children still poorer would outweigh what the evidence suggests would likely be only modest benefits from reducing marginal tax rates.

End Notes

[1] Mike Lee and Marco Rubio, “A Pro-Family, Pro-Growth Tax Reform,” Wall Street Journal, September 22, 2014, http://online.wsj.com/articles/mike-lee-and-marco-rubio-a-pro-family-pro-growth-tax-reform-1411426189.

[2] House Budget Committee, “The War on Poverty: 50 Years Later,” March 2014, http://budget.house.gov/uploadedfiles/war_on_poverty.pdf.

[3] House Budget Committee, “War on Poverty: 50 Years Later,” March 2014.

[4] “Effective Marginal Tax Rates for Low and Moderate Income Workers,” Congressional Budget Office, November 2012. See, in particular, Figure 5 on p. 24.

[5] Melissa Kearney et al., “A Dozen Facts about America’s Struggling Lower-Middle Class,” Brookings Institution, December 2013.

[6] Robert A. Moffitt, “Multiple Program Participation and the SNAP Program,” Russell Sage Foundation, February 2014, http://www.russellsage.org/research/reports/multiple-program-participation-and-snap-program.

[7] Stephen D. Holt and Jennifer Romich, “Longitudinal Evidence on Combined Marginal Tax Rates Facing Low- and Moderate- Income Working Families,” 2009 working paper, cited with permission of the authors. A larger share of families between 100 and 150 percent of poverty likely faced marginal tax rates this high, since this is the income range in which several benefits phase down; the study doesn’t provide data on that.

[8] Elaine Maag et al., “How Marginal Tax Rates Affect Families at Various Levels of Poverty,” National Tax Journal, December 2012, http://www.urban.org/UploadedPDF/412722-How-marginal-Tax-Rates-Affect-Families.pdf. The researchers also measured marginal rates if Medicaid were considered, but the analysis was done before enactment of the Affordable Care Act, which provides subsidies to purchase private coverage in the exchanges. As this report explains, enactment of the exchange subsidies sharply loweredmarginal tax rates for parents with incomes near the prior Medicaid eligibility limit, while raising marginal rates more modestly for those who receive exchange subsidies because those subsidies phase down as earnings rise.

[9] CBPP analysis of the 2013 March Current Population Survey (which provides income and employment information for 2012). The analysis also showed that 75 percent of workers with earnings in this range who live in families with children worked 35 hours per week during the weeks they were employed. About two-thirds (63 percent) of these workers worked at least 1,750 hours (50 weeks at 35 hours per week) over the course of the year.

[10]Adults without children are generally ineligible for SNAP, except for three months out of three years, unless they are working (or in a work program, which few are) for at least 20 hours a week. Hence, taking a low-wage job can make them eligible for SNAP rather than cause a loss of benefits.

[11] While work incentives are stronger today than 20 years ago, the safety net is significantly weaker for families with children in which a parent is unsuccessful in the labor market, including families in which parents have substantial barriers to employment such as low skill levels, mental or physical impairments, addiction, or the need to care for family members who are ill or have disabilities.

[12] U.S. Department of Health and Human Services, Welfare Indicators and Risk Factors, Thirteenth Report to Congress, http://aspe.hhs.gov/hsp/14/indicators/rpt_indicators.pdf.

[13] SNAP, the EITC, and the CTC each reach at least 80 percent of families with children eligible for assistance, far more than housing, TANF, or child care. In the case of housing assistance and child care, the low participation rate reflects inadequate funding, rather than a failure of outreach. TANF is more complicated. States have a fixed allocation of funding and, since the 1996 welfare law, have increasingly used TANF funding for purposes other than basic income assistance for poor families. This funding shift took place as caseloads were plummeting in the late 1990s, in part due to state policy and program changes that made it more difficult to access TANF assistance and in part due to increases in employment stemming from improved work supports (such as the EITC), welfare reform, and an exceptionally strong economy. After the economy weakened in 2000 and again in 2008, TANF caseloads did not increase much in response.

[14] This figure reflects the employee share of payroll taxes. If the employer share is added, the effective marginal tax rate goes up, but the employee’s effective wage level goes up as well.

[15] Edward Kleinbard, We Are Better Than This: How Government Should Spend Our Money (Oxford University Press, 2014), p. 51.

[16] CBPP analysis of results from Jeffrey Grogger, “The Effects of Time Limits, the EITC, and Other Policy Changes on Welfare Use, Work, and Income among Female-Head Families,” Review of Economics and Statistics, May 2003 and data from the March 1999 Current Population Survey.

[17] See Hannah Matthews, “Child Care Assistance Helps Families Work: A Review of the Effects of Subsidy Receipt on Employment,” Center for Law and Social Policy, April 2006, http://www.clasp.org/resources-and-publications/publication-1/0287.pdf.

[18] CHIP, as well as Medicaid in some states, covers children at somewhat higher income levels.

[19] States can impose premiums and additional cost-sharing requirements (not over 5 percent of family income) on children enrolled in CHIP, so there can be a modest increase in marginal tax rates around the income level at which a child would become eligible for CHIP rather than Medicaid. In addition, states that serve children in Medicaid rather than CHIP can impose premiums and cost-sharing requirements on children whose families have incomes above 150 percent of the poverty line.

[20] More precisely, individuals see an increase in their marginal tax rate when their income is close to 138 percent of the poverty line because a modest rise in income will make them ineligible for Medicaid and eligible for subsidies to purchase private coverage. Because the shift from Medicaid to private coverage means that individuals must pay more for coverage (and the coverage itself may be less comprehensive), the increase in income results in a loss in benefits.

[21] The ACA’s premium subsidies limit out-of-pocket premium costs to 3 to 4 percent of income for people between 133 and 150 percent of poverty and to 4 to 6 percent of income for people between 150 and 200 percent of poverty.

[22] Yonatan Ben-Shalom, Robert A. Moffitt, and John Karl Scholz, “An Assessment of the Effectiveness of Anti-Poverty Programs in the United States,” prepared for the 2012 Oxford Handbook of the Economics of Poverty, Chapter 22. A version of this study is available at http://www.irp.wisc.edu/publications/dps/pdfs/dp139211.pdf.

[23] Hilary Williamson Hoynes and Diane Whitmore Schanzenbach, “Work Incentives and the Food Stamp Program,” NBER Working Paper No. 16198, July 2010, http://www.nber.org/papers/w16198.

[24] In 1977, Congress added an “earned income deduction” to the Food Stamp Program that deducted 20 percent of a household’s earnings before calculating the household’s benefit.

[25] Hilary Hoynes, Diane Whitmore Schanzenbach, and Douglas Almond, “Long Run Impacts of Childhood Access to the Safety Net,” NBER Working Paper 18535, November 2012.

[26] Matt Broaddus, “Medicaid Coverage Doesn’t Discourage Employment, New Study Shows,” Off the Charts blog, October 28, 2013, http://www.offthechartsblog.org/medicaid-coverage-doesnt-discourage-employment-new-study-shows/. A study of Tennessee’s Medicaid program found increases in employment among some adults after losing Medicaid, which might suggest that expanding Medicaid reduces work. But Urban Institute researcher Austin Nichols points out that the study does not have the same unbiased experimental evidence as the Oregon study, since the comparison group in the Tennessee study lived in different (neighboring) states. After examining the research literature, Nichols concluded: “The best guess is that Medicaid expansions have no effect on labor supply.” See Austin Nichols, “Newer Evidence is Not Always Better Evidence,” Urban Institute, February 5, 2014, http://blog.metrotrends.org/2014/02/urban-institute-experts-cbos-aca-report.

[27] Jennifer L. Romich et al., p. 424.

[28] Jennifer L. Romich, “Difficult Calculations: Low?Income Workers and Marginal Tax Rates,” Social Service Review, Vol. 80, No. 1 (March 2006), pp. 27-66; Laura Tach and Sarah Halpern-Meekin, “Tax Code Knowledge and Behavioral Responses among EITC Recipients: Policy Insights from Qualitative Data,” Journal of Policy Analysis and Management, Vol. 33, No. 2 (Spring 2014), pp. 413-439. The Romich study combined in-depth interviews of 40 Wisconsin families over a three-year period starting in 1997 with administrative data on benefit receipt and employment and earnings. The paper by Tach and Halpern-Meekin was based on a study in which a team of researchers conducted in-depth interviews with 115 families receiving the EITC in Boston in 2007.

[29] Romich, p. 49.

[30] Tach, pp. 10, 12.

[31] Romich, p. 57.

[32] While the behavioral responses to the phase-down of benefits may not be large, the Romich study found that families were frustrated that their circumstances did not improve to a larger extent when their earnings rose, though some expressed satisfaction that they had become more self-sufficient.

[33] For example, Melissa Kearney and Lesley Turner have proposed a “second earner tax deduction” to reduce marginal rates on second earners in married-couple families. (The proposal would not affect single-parent families.) A married couple filing a joint return would be eligible for a deduction equal to 20 percent of the lower-earning spouse’s first $60,000 in earnings; the deduction would begin phasing down once family income reached $110,000. The proposal is structured so that the deduction can be applied when determining a family’s EITC and, thus, it would increase the EITC for families in the credit’s phase-down range (and have no effect for families on the upslope or plateau). The proposal, which would reduce taxes for moderate- and middle-income families, would cost $8.2 billion per year, the authors estimate. They put forward one possible offset: cutting the personal exemption for a spouse by 75 percent, which means that middle- and high-income married couples in which only one spouse worked (or the second spouse had only very modest earnings) would pay higher taxes in order to offset the tax cut for married couples in which both spouses work. This may be a reasonable trade-off. Many policymakers, however, likely wouldn’t be willing to raise taxes on married couples with a stay-at-home spouse. Whatever one’s views on the proposal, it shows the importance of considering the impact of both a proposed cut in marginal tax rates and the proposed offset. For information on this proposal, see “Giving Secondary Earners a Tax Break: A Proposal to Help Low- and Middle-Income Families,” Brookings Institution, December 2013, http://www.hamiltonproject.org/files/downloads_and_links/THP_Kearney_DiscPaper_Final.pdf.

[34] CBPP calculation using the March 2013 Current Population Survey. The $17 billion figure reflects the cost in 2012 of lowering the EITC phase-down rate to 10 percent. The current phase-down rate for families with one child is just under 16 percent, so the marginal-rate reduction for those families would be smaller than for families with two or more children, for whom the current phase-down rate is about 21 percent.

[35] The SNAP benefit calculation assumes recipients can spend 30 percent of their net income (i.e., gross income minus a standard deduction, a deduction of 20 percent of earned income, and deductions for expenses such as high housing costs and child care) for food purchases. Households receive the maximum SNAP benefit for their household size if their net income after deductions is zero. Since all households receive the standard deduction and any working household deducts 20 percent of its earnings, the point at which a household stops receiving the maximum benefit depends on whether it has earnings and other deductible expenses and the amount of those expenses relative to its income. SNAP benefits can begin to decline for households without high housing costs when their income rises above a level as low as 10 percent of the poverty line. For working households whose housing costs are high enough in relation to their income that they can deduct the maximum amount allowable, SNAP benefits may not start to decline until earnings are close to 60 percent of the poverty line.

[36] See Arloc Sherman, Sharon Parrott, and Danilo Trisi, “Chart Book: The War on Poverty at 50, Section 3,” Center on Budget and Policy Priorities, January 7, 2014, https://www.cbpp.org/cms/index.cfm?fa=view&id=4073#Part5, and Arloc Sherman, Danilo Trisi, and Sharon Parrott, “Various Supports for Low-Income Families Reduce Poverty and Have Long-Term Positive Effects On Families and Children,” Center on Budget and Policy Priorities, July 30, 2013, https://www.cbpp.org/cms/index.cfm?fa=view&id=3997.

More from the Authors