How Tax Reform Could Become a Trap:

Tax Reform Holds Promise, But if Not Done Carefully, Could Increase the Deficit and Inequality and Harm the Economy

Policymakers are increasingly discussing the need for tax reform, with a number of them calling for large cuts in tax rates — to levels well below the Bush tax rates — as a core element of reform. They contend that sweeping but unspecified cuts in tax expenditures (credits, deductions, and other tax preferences) will offset the cost of deep cuts in tax rates and, depending on the proposal, possibly generate some revenue to reduce deficits. Many who favor this approach go a step further and call for policymakers to commit to specific cuts in tax rates before they agree on any specific tax expenditures to reduce.

Such approaches pose big risks. They could produce tax “reform” that increases both deficits and inequality because while cutting “tax expenditures” sounds appealing in the abstract, cutting specific tax expenditures enough to offset the costs of substantial new rate cuts and contribute meaningfully to deficit reduction would likely prove difficult, if not impossible, to achieve. Indeed, the difficulty of cutting popular tax expenditures — from the mortgage interest deduction to 401(k) tax preferences to the deduction for charitable contributions to the exclusion for employer-sponsored health insurance — is why those who urge policymakers to commit upfront to specific, large rate cuts rarely specify any tax expenditures to cut. In fact, they often highlight tax expenditures that they would refuse to touch, such as the preferential tax rate for capital gains.

The 1986 Tax Reform Act, which tax experts often laud, cut tax rates and broadened the tax base and, all else being equal, the “lower the rates and broaden the base” formula is economically sound. But all else is not equal today; the nation faces enormous long-term budget deficits that will require wrenching policy choices, and all parts of the budget — very much including revenues — must be on the table. Given our daunting long-term deficits, the single most important goal of tax reform should be to raise substantial revenue, in a progressive manner, as part of a balanced deficit-reduction policy.

In 1986, tax reform was “revenue neutral” — it was designed to neither increase nor reduce revenues compared to the pre-reform tax code. That was fine in 1986 but, today, revenue neutrality would be harmful. Politically, policymakers have two major opportunities to secure a substantial revenue contribution to deficit reduction (which they should pair with spending cuts). First, the current tax-rate structure expires at the end of 2012 and the higher, Clinton-era tax rates are scheduled to return on January 1. Preventing the Bush tax rates from expiring will require action by policymakers, and this presents an opportunity they shouldn’t squander to construct a tax structure that generates significantly more revenue than a continuation of current policies. Second, policymakers can curb tax expenditures, which Harvard economist and former Reagan economic advisor Martin Feldstein has called “the best way to reduce government spending.”

But, revenue-neutral tax reform — with a new permanent rate structure and most or all of the politically possible cuts in tax expenditures — eliminates both of these opportunities to secure a substantial revenue contribution for deficit reduction. Thus, tax reform that’s revenue neutral or provides only a small amount of new revenue will likely lead to either of two highly adverse outcomes: (1) a highly unbalanced and extreme approach to deficit reduction that relies solely on budget cuts and thereby increases inequality, produces significant hardship, and leads to underinvestment in areas like education, research, and infrastructure; or (2) continued failure by policymakers to reach a sizeable deficit-reduction agreement at all, as other policymakers (understandably) decline to agree to substantial budget cuts if they are not part of a balanced package that also includes significant revenue increases.

For these reasons, a tax reform process that begins by locking in lower tax rates would be highly ill-advised. It would set back deficit reduction efforts because, by locking in a permanent lower top rate while not specifying how to secure tax-expenditure savings, it would leave the crucial trade-offs shrouded in mystery. When policymakers later see the cuts they will have to make in the mortgage interest, charitable, retirement, health care, and other popular deductions and exclusions to finance the rate cuts and reach whatever revenue targets they had set, they will likely balk at the tax-expenditure cuts and, as a result, the revenue target will give way.

In other words, if policymakers set both a new lower top rate and a revenue target before writing the details of tax-reform legislation, the two targets will almost inevitably collide. And, with many conservative policymakers insisting they will oppose tax reform legislation unless Congress religiously adheres to the rate cuts specified in advance, the revenue target will likely fall by the wayside. That’s why a tax reform process should specify only one number in advance — the revenue target. Policymakers who want to cut tax rates would receive a clear message that how much they could lower the rates would depend upon how far they were willing to go in curbing tax expenditures.

Recent proposals from Senator Pat Toomey (R-PA), Governor Mitt Romney, and House Budget Committee Chairman Paul Ryan (R-WI) illustrate the dangers. Their proposals would cut tax rates far below current levels — extending all of the Bush tax cuts and adding large new tax rate cuts on top — while supposedly offsetting some or all of the cost through unspecified cuts in tax expenditures.[1] Various tax experts have concluded that policymakers would find it virtually impossible to enact enough tax expenditure cuts to come anywhere near offsetting the cost of the proposed big tax rate cuts of these plans.

Similarly, the Bowles-Simpson report recommended that the top rate not exceed 29 percent (although it said that should be conditioned on an end to lower rates on capital gains and dividends and the 29 percent top rate should not be adopted if those lower rates are retained.) Bowles-Simpson included an “illustrative” plan for curbing specific tax expenditures, which it estimated would offset the cost of its rate cuts and generate substantial new revenue for deficit reduction. But the tax expenditure cuts were merely “illustrative” for a reason — the commission members who voted for the report did not reach agreement on actual tax expenditure changes to recommend. Moreover, the illustrative plan would cut popular tax expenditures so severely that it almost certainly would die quickly in Congress.[2]

A tax reform approach that specifies rate cuts but not tax expenditure cuts in advance also would threaten the progressivity of the tax code. As explained below, across-the-board rate cuts are quite regressive, benefitting those at the top much more than anyone else. Policymakers who promote this approach often say their unspecified tax-expenditure changes will ensure that the tax code as a whole is no less progressive, even as (in most cases) they insist on retaining the preferential tax rate for capital gains and dividends. They make such claims about maintaining progressivity only in the abstract, however, without specifying how they would scale back tax expenditures to meet that goal. As discussed below, they would find it virtually impossible to honor that promise, especially if they cut tax rates deeply and maintained the current low rates on capital gains.

In essence, policymakers must not to let tax reform become a trap. The goal of lowering rates and broadening the base, if not pursued carefully and cautiously, could make it much harder, if not impossible, to achieve a balanced deficit-reduction plan. It also could lead to tax changes that reduce the progressivity of the tax code and thereby exacerbate income inequality, which is already very high.

Policymakers can avoid such a trap, and make tax reform an important positive force, by setting as the most important tax-reform goal the raising of substantial new revenue for deficit reduction and doing so in ways that maintain or improve the tax code’s progressivity. To pursue that path, policymakers should let the Bush tax cuts for households making over $250,000 expire on schedule, generating nearly $1 trillion for deficit reduction over ten years, and seek agreement on how much additional revenue to provide — alongside significant spending cuts — as part of a balanced deficit-reduction package. The revenue target should be the only numerical target they set up front. How low the rates are set should depend on how much policymakers will curb real tax expenditures, not be pre-ordained before they start making hard choices on tax expenditures. Policymakers should cut rates only if they can generate enough revenue from cutting tax preferences to meet their revenue target without gimmicks and in ways that will endure.

The Top Tax-Policy Priority: Raise Additional Revenue in a Progressive Manner to Help Address Deficits

Policymakers across the political spectrum recognize the need to reduce long-term deficits. As Federal Reserve Chairman Ben Bernanke has stated, “To achieve economic and financial stability, U.S. fiscal policy must be placed on a sustainable path that ensures that debt relative to national income is at least stable or, preferably, declining over time. Attaining this goal should be a top priority.”[3]

All major bipartisan deficit-reduction proposals, such as the Bowles-Simpson report, have acknowledged that spending cuts alone will not generate the needed savings and have embodied an approach that includes both spending cuts and tax increases. The bipartisan panels concluded that reducing deficits solely through spending cuts would impose unacceptably large sacrifices on vulnerable populations such as low-income families, the elderly, and the disabled and unwisely squeeze investment in education, infrastructure, and scientific research. They also recognized that rising costs throughout the U.S. health care system and the aging of the population will inexorably place upward pressure on federal spending as millions more Americans become eligible for Medicare and Social Security and, to some extent, Medicaid.

Moreover, spending cuts already are contributing significantly to deficit reduction. The 2011 Budget Control Act (BCA) created caps that will shrink discretionary spending to 5.6 percent of Gross Domestic Product (GDP) in 2021, well below the 8.7 percent average over the past 40 years. (Discretionary spending will shrink further, to 5.2 percent in 2021, if the automatic cuts — or “sequestration” — that the BCA calls for take effect starting in January.)

With unsustainable budget deficits on the horizon, policymakers should set as their top tax policy goal to raise significant revenue for deficit reduction. They also should agree to raise it in a progressive manner. After-tax income inequality worsened substantially over the 1979-2007 period, with average after-tax income rising just 18 percent for those in the bottom fifth of the income distribution and 38 percent for those in the middle three-fifths of the income distribution — while soaring by 277 percent for those in the top 1 percent, according to a recent Congressional Budget Office (CBO) analysis. Moreover, CBO found, the tax-policy changes of this period made the tax system less effective at helping to alleviate the growing inequality. “As a result,” CBO reported, “the increase in inequality of after-tax income was greater than the increase in inequality of before-tax income.”[4] Tax reform should not exacerbate these trends but, instead, should seek to restore some of the progressivity that the tax code has lost.

Cutting Tax Rates Across the Board Is Costly and Likely Regressive

Extending the Bush cuts in income tax rates would add $3.2 trillion to deficits over 2013-2022, not counting the cost of additional interest payments on the debt.[5] Some policymakers have proposed large rate cuts on top of the Bush tax cuts. Senator Toomey, for example, has proposed cutting all rates by 20 percent below the Bush levels — in essence, setting the top rate at 28 percent. That would reduce federal revenues by about $2.6 trillion over the next ten years, on top of the cost of extending the Bush tax cuts, according to the Urban Institute-Brookings Tax Policy Center. The additional interest payments on the debt would make the cost still higher.[6]

Analysts generally agree that policymakers must find more than $3 trillion in deficit reduction over ten years (measured against a baseline that assumes that current policies remain in place) to stabilize the debt in the coming decade so that it stops growing faster than the economy — a key fiscal policy goal. [7] (The BCA already locked in more than $1 trillion in cuts to defense and nondefense spending over the next decade relative to fiscal year 2010 levels adjusted for inflation, and produced additional savings in interest payments through its caps on discretionary funding. The more-than-$3 trillion still needed is in addition to that.) A 20 percent tax-rate cut would, by itself, nearly double the size of the remaining deficit-reduction task.

Proposals such as Senator Toomey’s, Chairman Ryan’s, and Governor Romney’s lock in the Bush tax cuts as a starting point, which themselves are not just very costly but regressive as well. In 2011, the Bush tax cuts increased after-tax incomes by an average of 6.2 percent — about $129,000 per household — for people with incomes exceeding $1 million, but by just 2.2 percent — about $830 per household — for those with incomes between $40,000 and $50,000, the Tax Policy Center reported.[8]

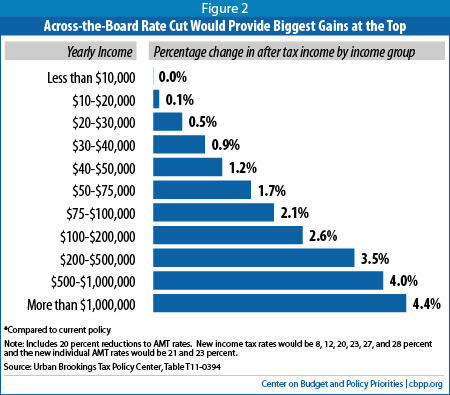

Proposals such as Senator Toomey’s, which would then cut tax rates across the board by 20 percent, may sound as though they would benefit all taxpayers equally. In fact, across-the-board rate cuts disproportionately benefit the nation’s wealthiest households and are quite regressive. To understand why, take a simple tax system with two tax rates: 20 percent and 40 percent. Say both tax rates are cut by half, so that the new bottom rate is 10 percent (instead of 20) and the new top rate is 20 percent (instead of 40). With these rate cuts, taxpayers will keep 90 cents — rather than 80 cents — of each dollar taxed at the bottom rate, generating a 12.5 percent increase in after-tax income. For each dollar taxed at the top rate, high-income households will keep 80 cents, rather than 60 cents, generating a 33 percent increase in after-tax income. Thus, even though both tax rates fall by the same percentage, the result is a regressive tax cut that benefits people in the top bracket the most, not only in dollars but in the percentage increase in their after-tax income (which many analysts regard as the best measure of whether a tax policy change is progressive or regressive).

The chart below illustrates the regressivity of a 20 percent across-the-board rate cut. After-tax incomes would grow by more than two and a half times as large a percentage for people making over $1 million as for people making between $50,000 and $75,000.

Broadening the Tax Base Dramatically Is Easy to Promise But Hard to Deliver

Tax expenditures cost the government more than $1 trillion per year in lost revenue, and scaling them back can make the tax code more efficient. Tax expenditures can reduce economic efficiency by favoring some forms of investment or economic activity over others. Often, they also provide the largest subsidies to certain activities — such as saving for retirement — to high-income families, even though such taxpayers are those who least need a financial incentive to engage in such activities (that is, they are the people most likely to undertake the activities even without a tax subsidy). That makes such tax incentives inefficient and wasteful.[9]

But curtailing tax expenditures, especially if that must produce deficit reduction and offset the cost of large and regressive reductions in tax rates, is far harder than many proponents suggest. First, there are immense political and other obstacles to raising very large amounts of revenue through tax-expenditure reform. Second, cutting tax rates reduces the revenue gains from base broadening. And third, it’s even harder to overhaul tax expenditures in a way that simultaneously offsets the cost of rate cuts, raises significant additional revenue for deficit reduction, and maintains or improves the progressivity of the tax code — especially if proponent insist on maintaining the preferential rate for capital gains.

Cutting Tax Expenditures Is Difficult

Recent estimates of the large cost of tax expenditures have “created unrealistic expectations about the potential revenue that could be raised through tax expenditure reform,” notes Professor John Buckley, former chief of staff for the Joint Committee on Taxation.[10] A recent Congressional Research Service (CRS) report similarly concludes:[11]

[T]here are impediments to base broadening by eliminating or reducing tax expenditures, because they are viewed as serving an important purpose, are important for distributional reasons, are technically difficult to change, or are broadly used by the public and quite popular. Given the barriers to eliminating or reducing most tax expenditures, it may prove difficult to gain more than $100 billion to $150 billion in additional tax revenues [in 2014] through base broadening.

CRS notes that base broadening in this range “would not allow for significant reductions in tax rates.” CRS explains that it would offset the cost of only “about a one or two percentage point reduction, thus reducing the top 39.6% rate to 37%.”

In other words, the base broadening that CRS considers politically realistic would fund only a small cut in tax rates below the Clinton-era rates that are set to take effect in 2013. It would fall well short of financing an extension of the current Bush-era rates, much less a rate cut of 20 percent below the Bush levels.

The evidence supports CRS’s conclusion about the political hurdles to major tax expenditure reform. Those hurdles are significant:

- Recent plans to “lower the rates and broaden the base” from policymakers such as Senator Pat Toomey and House Budget Committee Chairman Paul Ryan contain specific costly rate cuts but lack specific proposals to raise revenue from broadening the tax base. These plans also take one of the largest tax expenditures — the preferential tax rate for capital gains and dividends — off the table.

- Chairman Ryan has described tax expenditure reform as “getting rid of special-interest loopholes.” As the table below shows, however, the largest tax expenditures are items like the mortgage interest deduction, the tax exclusion of employer-sponsored health insurance, and the tax advantages for 401(k) plans and other retirement accounts, which benefit tens of millions of people. Most Americans would not consider them “special-interest loopholes.”

| Table 1 The Five Largest Individual Tax Expenditures, 2014 | ||

| Provision | Amount ($billions) | Share of All Tax Expenditures (%) |

| Exclusion of Employer Health Insurance | 164.2 | 13.2% |

| Exclusion of Employer Pensions | 162.7 | 13.1% |

| Mortgage Interest Deduction | 99.8 | 8.1% |

| Exclusion of Medicare | 76.2 | 6.1% |

| Capital Gains Rates | 71.4 | 5.8% |

| Note: Expiring provisions are extended Source: Jane G. Gravelle and Thomas L. Hungerford, “The Challenge of Individual Income Tax Reform: An Economic Analysis of Tax Base Broadening,” Congressional Research Service, March 22, 2012 | ||

- While the bipartisan 1986 Tax Reform Act was a notable accomplishment — cutting tax rates and broadening the tax base significantly (even eliminating the lower tax rate for capital gains, until policymakers restored it in later years) — a number of major tax expenditures survived that aggressive tax reform effort, such as the mortgage interest deduction and the exclusion for employer-sponsored health insurance.

- Recent efforts to reduce tax expenditures have produced relatively modest savings. For example, a Senate effort during the health reform debate to reduce the tax subsidy for employer-provided health insurance produced savings estimated by JCT at $19.8 billion in 2019, its first full fiscal year. By comparison, the underlying tax exclusion for employer contributions to health care will cost about $176 billion in 2015.

- Policymakers have rejected other proposed changes to tax expenditures out of hand. For example, Congress has repeatedly rejected President Obama’s proposal to cap the value of itemized deductions and various exclusions at 28 percent, thereby limiting the benefits that high-income households secure from various tax expenditures, such as the mortgage-interest deduction and the exclusion for employer-provided health insurance.[12] The proposal would raise $584 billion over ten years, enough to finance only a small part of the cost of the tax-rate cuts that various policymakers are now proposing. Yet the Obama proposal still was too ambitious for lawmakers in either party.

Tax expenditure reform faces significant technical and administrative challenges as well, as CRS notes, such as how to place a dollar value on various tax exclusions. In addition, and importantly, large-tax expenditure reform would likely require extensive transitional rules or relief (especially in areas like the mortgage interest deduction) that would substantially limit the savings for a number of years. As John Buckley has explained, “for more robust reform, more extensive transition relief will be required.”

Cutting Tax Rates Reduces Revenue Gains from Base Broadening

Compounding the difficulty of raising enough revenue from base broadening to both finance rate cuts and reduce deficits is an often overlooked fact: the more that income tax rates fall, the less revenue that tax expenditure reform can raise.

Most tax expenditures reduce a taxpayer’s income that is subject to income tax rates, so their cost depends on the taxpayer’s top marginal tax rate. For example, each $1 deduction reduces revenues by 15 cents for a taxpayer in the 15 percent bracket but by 35 cents for a taxpayer in the 35 percent bracket. When tax rates fall, the cost of these tax expenditures also fall — and, as a result, policies to scale them back raise less revenue.

The part of President Obama’s proposed 28 percent limitation that applies to itemized deductions illustrates this effect.[13] If policymakers enacted the proposal and let marginal tax rates rise as scheduled at the end of 2012, the Tax Policy Center (TPC) estimates that it would raise $279 billion over 2013 to 2021. But if policymakers extended the current Bush tax rates, the same proposal would raise just $157 billion over the same period — or more than 40 percent less. That’s because the proposal would have a considerably smaller impact on taxpayers in, for example, the top bracket if the top rate remained at 35 percent than if it rose to 39.6 percent as scheduled. TPC notes that if policymakers extend the current tax rates, “The smaller difference between the statutory rates and the 28 percent limitation would result in smaller tax increases and hence less additional revenue.”[14]

The same pattern holds for many proposals to limit tax expenditures, including the outright repeal of specific exemptions, deductions, and other preferences; they would raise less revenue if policymakers extend the Bush tax rates than if they allow the rates to rise as scheduled. Cutting tax rates belowthe Bush levels would reduce the revenue gains from base-broadening still further.

Base Broadening Can Make the Tax Code More or Less Progressive

If tax reform begins with regressive rate cuts, such as an across-the-board rate cut, then policymakers who want to avoid making the tax code less progressive must offset the regressive impact of the rate cuts. That would not be easy. As discussed above, a large package of base-broadening measures is very hard to enact. A large package of progressive base-broadening measures may be even harder.

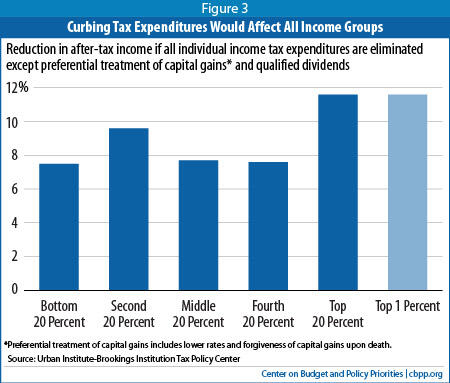

That’s particularly true if policymakers follow the lead of tax reform proponents such as Chairman Ryan, Senator Toomey, and Governor Romney and refuse to scale back the tax expenditure that high-income taxpayers benefit from the most — the preferential rates for capital gains and dividends. The benefits of the other tax expenditures are fairly evenly distributed across income groups, as the chart shows. Crafting and enacting a plan to cut the remaining tax expenditures enough to finance across-the-board rate cuts and reduce the deficit without hitting low- and moderate-income taxpayers harder than those at the top would be all but impossible.

Moreover, some tax reform plans may envision pairing regressive rate cuts with changes in tax expenditures that could themselves be regressive. Senator Toomey’s budget plan, for example, says that one way to finance its large rate cuts is to adopt the proposal by Martin Feldstein and others on how to scale back tax expenditures.[15] The Feldstein proposal would limit the total amount that a tax filer may claim in various tax expenditures — such as the child tax credit, the mortgage interest deduction, the exclusion of employer-sponsored health insurance, and others — to 2 percent of his or her adjusted gross income. That’s regressive mainly because it would protect the preferential capital gains and dividends rates while significantly reducing tax expenditures that low- and middle-income households use extensively. In fact, more than half of the revenue that the Feldstein proposal would generate would come from limiting the tax break for employer-sponsored health insurance, most of the benefit of which goes to middle-class families. Nearly half (45 percent) of the total revenue that the entire Feldstein proposal generates comes from effectively taxing a portion of ESI for households below $200,000.

Efficiency Gains Likely to be Disappointingly Modest

Proponents of base broadening often tout its potential for creating a more efficient tax code and, in turn, stronger economic growth. Policymakers can and should seek to reform tax expenditures in ways that make the tax code more efficient. But the economic gains would likely prove modest.

TPC’s William Gale and Daniel Baneman have cautioned that “the impact of tax expenditures on economic efficiency varies by particular provision.”[16] For example, the mortgage interest deduction fosters economic distortion by favoring investments in housing over other investments and providing the largest subsidies to households that least need a subsidy to afford a home purchase. The best way to boost economic efficiency by reforming tax expenditures is to limit or redesign those expenditures that are most inefficient.[17]

But if a tax reform process starts by locking in costly rate cuts, policymakers will find it harder to target reform on the most inefficient tax breaks. The need for very large revenues to finance both the tax rate cuts and deficit reduction will push policymakers to cut tax expenditures in ways that may not be the most efficient, by curtailing effective tax expenditures as well as inefficient ones.

The Feldstein proposal cited above is an example. To raise significant revenues, it limits effective and inefficient tax expenditures alike. Moreover, because it sets its limit as a percentage of a tax filer’s adjusted gross income, it allows higher-income taxpayers to retain much more, in dollar terms, of their mortgage interest and other deductions than taxpayers who incur similar expenses but have lower incomes. Yet, as noted, the incentive effects that deductions are supposed to provide for various activities (like retirement saving or home buying) are greater if policymakers target the subsidy more heavily on low- and middle-income households, since high-income households will generally engage in these activities anyway.

Even if policymakers take a well-designed, targeted approach to tax expenditure reform, the economic gains are easily overstated. Some studies have found significant efficiency gains from fundamental tax reform, but those studies assume not only the elimination of all tax expenditures but also unrealistic options such as the replacement of part or all of the income tax with value-added taxes.[18]

Further, in a tax reform process that starts with costly rate cuts, any revenues raised from base broadening would go first to finance the rate cuts. In light of current and projected levels of debt, that would be an unfortunate choice: our nation’s future income will be higher if we use the revenues that policymakers raise mainly or exclusively for deficit reduction. That is why CBO has concluded that allowing the Bush tax cuts to expire and dedicating the revenues to deficit reduction would raise U.S. residents’ income in 2020 by more than 1 percent; the boost to national saving would outweigh any efficiency loss from higher tax rates.[19] A tax reform package that achieved modest efficiency gains from base broadening but contributed little if anything to deficit reduction would do less for economic growth than letting the Bush tax cuts for high-income households expire and applying the savings to deficit reduction. (Letting all of the Bush tax cuts expire when the economy has more fully recovered and dedicating the revenue to deficit reduction would do still more for economic growth.)

In short, while base broadening can deliver a more efficient tax code and is surely desirable, the economic gains will not likely be large, and they will be smaller if policymakers use base broadening mainly or entirely to finance rate cuts rather than to reduce the deficit and we achieve less deficit reduction as a result.

Tax Reform Could Become a Trap that Generates Bigger Deficits and More Inequality

An approach to tax reform that some policymakers are heavily promoting — committing to costly and regressive tax rate cuts upfront, with a promise to offset the cost through cuts in unspecified tax expenditures — holds high risk of turning tax reform into a trap that prompts policymakers toward one of two undesirable outcomes.

First, even if policymakers summoned the political will to address the inefficiencies of the mortgage interest deduction, the upside-down tax incentives for retirement saving, the preferential rate for capital gains that induces substantial tax sheltering, and other inefficient tax expenditures, policymakers would apply the resulting revenues first to help finance expensive and regressive tax rate cuts rather than to reduce deficits. Given the magnitude of some current rate-cut proposals, little if any deficit reduction would likely result. In addition, the overall package would likely be regressive, given the difficulty of cutting tax expenditures substantially and in ways that are sufficiently progressive to offset the regressive effects of across-the-board rate cuts.

Second, if policymakers cannot agree on specific measures to broaden the base on a very large scale, they will have committed themselves to specific rate cuts that may prove politically difficult to abandon. The result could be tax reform that produces no deficit reduction or even increases deficits while making the tax code less progressive — the opposite of what the nation needs. Policymakers might try to mask this failure at deficit reduction through “dynamic scoring” — the proposed process by which rate cuts are assumed to generate significant economic growth that drives up tax revenues, despite the lack of strong evidence for such results. Such a move would impair the credibility of the budget process by forecasting an increase in revenues (to finance rate cuts or reduce the deficit) that may very well never materialize.[20]

Neither scenario would help to put the nation on a sustainable fiscal path or ensure that the burden of deficit reduction is equitably shared.

End Notes

[1] See the following CBPP reports: James R. Horney et al., “Toomey Budget Similar to House-Passed Ryan Budget,” May 9, 2012, https://www.cbpp.org/cms/index.cfm?fa=view&id=3771; Robert Greenstein, Chye-Ching Huang, and Chuck Marr, “Can Governor Romney’s Tax Plan Meet Its Stated Revenue, Deficit, and Distributional Goals at the Same Time?,” March 2, 2012, https://www.cbpp.org/cms/index.cfm?fa=view&id=3695; Chuck Marr, “New Tax Cuts in Ryan Budget Would Give Millionaires $265,000 on Top of Bush Tax Cuts,” revised April 12, 2012, https://www.cbpp.org/cms/index.cfm?fa=view&id=3728.

[2] For example, the illustrative plan included taxation of capital gains when an individual dies, elimination of lower tax rates on capital gains and dividend income, elimination of the state and local tax deduction, the inclusion in taxable income of gross interest on newly issued state and municipal bonds, replacement of the mortgage interest deduction with a non-refundable 12 percent credit for principal residences capped at a $500,000 mortgage value, capping and limiting the exclusion for employer-sponsored health insurance, and replacing the charitable deduction with a non-refundable credit applicable only to contributions exceeding 2 percent of a taxpayer’s adjusted gross income.

[3] Federal Reserve Chairman Ben Bernanke, Testimony before Senate Committee on the Budget, February 7, 2012.

[4] Emphasis added. http://www.cbo.gov/sites/default/files/cbofiles/attachments/10-25-HouseholdIncome.pdf

[5] Based on estimates from the Congressional Budget Office and Joint Committee on Taxation. This includes the cost of the additional AMT relief associated with extending the income tax cuts, which is necessary to prevent the AMT from taking back the benefit of those tax cuts for many taxpayers.

[6] James R. Horney, Chye-Ching Huang, Edwin Park and Paul N. Van de Water, “Toomey Budget Similar to House-Passed Ryan Budget: Contains Deep Cuts in Low-Income and Non-Defense Discretionary Programs And Likely Tax Cuts for the Most Well-Off,” Center on Budget and Policy Priorities, May 9, 2012, https://www.cbpp.org/cms/index.cfm?fa=view&id=3771.

[7] This does not assume savings from sequestration.

[8] Urban-Brookings Tax Policy Center Table T10-0132.

[9] Chuck Marr and Brian Highsmith, “Reforming Tax Expenditures Can Reduce Deficits While Making the Tax Code More Efficient and Equitable,” Center on Budget and Policy Priorities, April 15, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3472.

[10] John L. Buckley, “Tax Expenditure Reform: Some Common Misconceptions,” Tax Notes, July 18, 2011.

[11] Jane G. Gravelle and Thomas L. Hungerford, “The Challenge of Individual Income Tax Reform: An Economic Analysis of Tax Base Broadening,” Congressional Research Service, March 22, 2012, http://www.washingtonpost.com/wp-srv/business/documents/crstaxreform.pdf.

[12] See James R. Horney and Jason Levitis, “Limiting Itemized Deductions for Upper-Income Taxpayers Would Have Little Effect on Small Business, Charities, Housing Criticisms of Proposal Are Overblown,” Center on Budget and Policy Priorities, March 12, 2009, https://www.cbpp.org/cms/index.cfm?fa=view&id=2707.

[13] The proposed limitation also would apply to various tax exclusions, such as the exclusions for tax-exempt state and local bond interest, employer-sponsored health insurance paid for by employers or with before-tax employee dollars, and employee contributions to defined contribution retirement plans and individual retirement arrangements. Department of the Treasury, General Explanations of the Administration’s Fiscal Year 2013 Revenue Proposals, February 2012.

[14] Daniel Baneman, Jim Nunns, Jeff Rohaly, Eric Toder, Roberton Williams, “Options to Limit the Benefit of Tax Expenditures for High-Income Households,” Urban-Brookings Tax Policy Center, August 2, 2011.

[15] Senator Pat Toomey, Restoring Balance: Fiscal Year 2013 Budget Resolution, April 18, 2012, http://www.toomey.senate.gov/pdf/restoringbalance.pdf.

[16] Chuck Marr and Brian Highsmith, “Reforming Tax Expenditures Can Reduce Deficits While Making the Tax Code More Efficient and Equitable,” Center on Budget and Policy Priorities, April 15, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3472.

[17] Converting deductions into uniform percentage credits would target them better to low- and moderate-income taxpayers, who are most likely to respond to the subsidy. See Chuck Marr and Brian Highsmith, “Reforming Tax Expenditures Can Reduce Deficits While Making the Tax Code More Efficient and Equitable,” Center on Budget and Policy Priorities, April 15, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3472.

[18] For discussion of “real world” options, See William Gale, Tax Reform Options in the Real World, Chapter 2 in Toward Fundamental Tax Reform by Alan J. Auerbach and Kevin A. Hassett (American Economic Institute Press, 2005). JCT has also analyzed a proposal to broaden the current individual income tax base and use those revenues to lower rates. However the proposal analyzed, while revenue neutral within the budget window, loses revenues in the last six years of the window and increases deficits over the long run. JCT, “Macroeconomic Analysis Of A Proposal To Broaden The Individual Income Tax Base And Lower Individual Income Tax Rates,” December 14, 2006.

[19] Douglas W. Elmendorf, Director, Congressional Budget Office, The Economic Outlook and Fiscal Policy Choices, Testimony before the Senate Committee on the Budget, September 28, 2010, http://www.cbo.gov/ftpdocs/118xx/doc11874/09-28-EconomicOutlook_Testimony.pdf.

[20] Paul N. Van de Water, “Supercommittee Should Reject ‘Dynamic Scoring,’” Center on Budget and Policy Priorities, October 18, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3598.

More from the Authors

Areas of Expertise