Reforming Tax Expenditures Can Reduce Deficits While Making the Tax Code More Efficient and Equitable

Recent Proposals Underscore Bipartisan Support for Reform

With the federal budget on an unsustainable path, our country’s fiscal problems need to be addressed in a way that is both effective and equitable. Scaling back and reforming “tax expenditures” — spending that is delivered through the tax code rather than government programs — should be an important part of that effort.

As the report from the Bowles-Simpson deficit commission stated, “These tax earmarks —amounting to $1.1 trillion a year of spending in the tax code — not only increase the deficit, but [also] cause tax rates to be too high.” [1] Moreover, tax expenditures often reduce economic efficiency by providing the largest subsidies to high-income families, who are least likely to need a financial incentive to engage in the activity the tax incentive is designed to promote, such as buying a home or saving for retirement. In other words, many of these expenditures are “upside-down.”

Several developments suggest growing interest among policymakers in reforming tax expenditures as part of broader tax reform that contributes significantly to deficit reduction. President Bush encouraged tax expenditure reform through his 2005 tax reform panel, as has President Obama through his proposal to limit the value of itemized deductions for high-income families. A recent Government Accountability Office report highlighted tax expenditures as an area of potential significant savings. Most importantly, two recent bipartisan commissions have recommended bold steps that would make many of these “upside-down” tax expenditures more equitable and economically efficient, while contributing to deficit reduction.

These proposals highlight the significant economic and fiscal costs of various tax incentives and offer policymakers an opportunity. By converting various tax deductions into flat-percentage credits, policymakers could improve economic efficiency by increasing the effectiveness of the tax incentives in boosting national saving, college attendance, and the like, even as they achieve deficit reduction and improve the progressivity of the tax code.

Tax Expenditures Cost More Than Any Single Spending Category

The Budget Act of 1974 defines tax expenditures as revenue losses attributable to any provisions in federal tax law that provide special benefits to particular taxpayers or groups of taxpayers.

Although accomplished through the tax code, most experts believe these provisions should generally be viewed as a form of government spending. According to the Joint Committee on Taxation, tax expenditures “may be considered to be analogous to direct outlay programs, and the two can be considered as alternative means of accomplishing similar budget policy objectives.” [2] In addition, as tax expert Leonard Burman and others have pointed out, tax expenditures impose the same “opportunity costs” as federal spending programs in terms of higher tax rates, reduced federal resources for national priorities, and/or higher deficits and national debt. [3]

Appearing before the Bipartisan Commission on Entitlement and Tax Reform in 1994, Alan Greenspan recommended that policymakers, in considering the structure and long-term strength of entitlement programs, extend their scrutiny to what he termed “tax entitlements.” His formulation reflects the fact that, in many ways, tax expenditures operate as spending entitlements that are delivered through the tax code. Whereas discretionary spending programs operate under limited funding and are subject to annual review, tax expenditures are subject to neither constraint. The benefits of tax expenditures are available to any qualifying filer, and because the incentives are written into the tax code, these programs receive much less scrutiny than many spending programs.

Child care provides an example of why tax expenditures generally are the equivalent of spending programs and essentially operate as entitlements. Many low- or moderate-income people receive a subsidy, provided through a spending program, to help cover their child care costs. Many people with higher incomes similarly receive a subsidy that reduces their child care costs, but they receive it in the form of a tax credit. The child-care spending programs that serve lower-income families are not open-ended entitlement programs; they serve only as many people as their capped funding allows. By contrast, the child care subsidies for higher-income families are guaranteed because the child care tax credit operates as an open-ended entitlement provided through the tax code; its costs are not limited or constrained, and all families that are eligible for the tax credit can receive it.

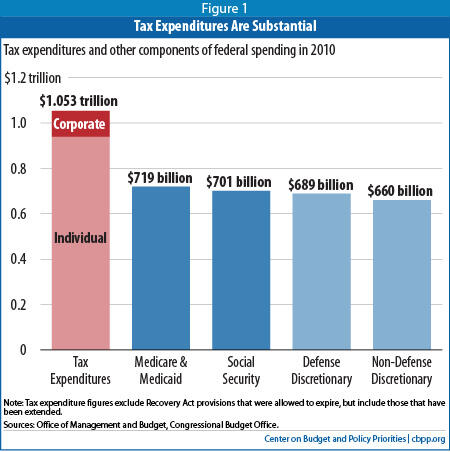

If tax expenditures were classified as spending rather than tax benefits, they would constitute the single largest category of federal spending — consuming more resources annually than Social

Security, or the combined cost of Medicare and Medicaid, or defense or non-defense discretionary spending. Together, these tax incentives and other tax breaks reduce federal revenues by over $1 trillion annually, or roughly 7 percent of the gross domestic product (GDP). [4] These facts have led economist Martin Feldstein, chairman of the Council of Economic Advisers under President Reagan, to conclude that “Cutting tax expenditures is really the best way to reduce government spending.”[5] Feldstein also noted:

[E]liminating tax expenditures does not increase marginal tax rates or reduce the reward for saving, investment or risk-taking. It would also increase overall economic efficiency by removing incentives that distort private spending decisions. And eliminating or consolidating the large number of overlapping tax-based subsidies would also greatly simplify tax filing.

The Government Accountability Office (GAO) highlighted the cost of tax expenditures and the potential savings from reforming them in its recent report on reducing duplication in government programs. The GAO stated:

Improving tax expenditure performance or eliminating tax expenditures could reduce revenue losses, potentially by billions of dollars. For example, improved designs may enable individual tax expenditures to achieve better results for the same revenue loss or the same results with less revenue loss. Also, reductions in revenue losses from eliminating ineffective or redundant tax expenditures could be substantial depending on the size of the eliminated provisions.[6]

Many Tax Expenditures Are Inefficient and Inequitable

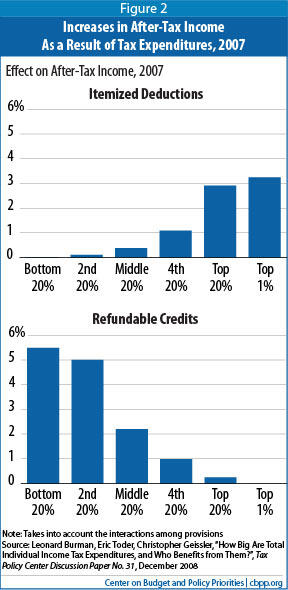

For maximum efficiency, tax expenditures should provide the greatest benefit to taxpayers who are either more responsive to the incentive the tax expenditure provides or whose engagement in the desired activity would generate the greatest social good. But approximately 70 percent of the amount spent each year on individual tax expenditures is provided through tax deductions, exemptions, or exclusions, the value of which rises as household income increases — the higher one’s tax bracket, the greater the tax benefit for each dollar deducted, exempted, or excluded. As a result, the wealthiest households often receive the largest tax subsidies, while the benefits to middle-class families are considerably smaller and many of the most vulnerable families are left out entirely. This structure generally reduces both the efficiency and the fairness of these tax incentives.

Consider how the home mortgage interest deduction affects two households’ decisions to purchase a home:

- An affluent investment banker who has a $1 million mortgage and pays $40,000 in mortgage interest each year receives a housing subsidy of $14,000 annually. The banker pays 65 cents of every dollar of mortgage interest, and taxpayers pick up the remaining 35 cents.

- By contrast, a typical middle-class family, such as a welder or a nurse making $60,000 and paying $10,000 a year in mortgage interest on a more modest home, will receive a housing subsidy worth $1,500 annually. Here, the family pays 85 cents of every dollar of mortgage interest and taxpayers pick up just 15 cents.

In other words, the high-income household receives a substantially larger benefit, both per dollar of interest cost and in terms of the total tax benefit. And a low- or modest-income household with no federal income tax liability would receive no benefit from the tax subsidy, even though its total tax burden — including payroll and other federal taxes and state and local taxes (which tend to be regressive) — is likely to be positive.

| Table 1: Refundable Credits Are More Equitable Than Deductions or Exclusions | |||

| Marginal Tax Bracket | $10,000 Deduction or Exclusion Reduces Tax Liability By:** | $2,000 Non-Refundable Credit Reduces Tax Liability By: | $2,000 Refundable Credit Reduces Tax Liability By: |

| 0%* | $0 | $0 | $2,000 |

| 15% | $1,500 | $2,000 | $2,000 |

| 25% | $2,500 | $2,000 | $2,000 |

| 35% | $3,500 | $2,000 | $2,000 |

| * Taxable income is $0 because total income is less than the standard deduction and personal exemption. ** Calculated as the amount of the deduction ($10,000) multiplied by the marginal tax rate | |||

Such a structure could make sense if a substantially greater monetary incentive were required to encourage higher-income people to take the desired action — in this case, purchasing a home — or if their doing so provided a relatively greater benefit to society. The reality, however, is frequently the reverse: high-income families generally would buy a home, send their children to college, save for retirement, and contribute to charitable causes with or without the current costly tax incentives. By contrast, lower-income families are less likely to take these desirable actions without significant financial incentives, largely because of their financial constraints (e.g., low-income families’ decisions to send their children to college are more heavily influenced by tuition prices and financial aid than higher-income families’).

In short, through tax expenditures, we devote a significant amount of resources to subsidizing behavior that would have occurred anyway, while we exclude the very families that likely would be the most responsive to the incentive. As tax experts Lily Batchelder, Fred Goldberg, and Peter Orszag explained in a major paper on these issues several years ago, the structure of such tax incentives is economically inefficient for these reasons.[8]

Unlike tax deductions and exclusions, tax credits do not link the tax incentive to households’ marginal tax brackets and generally reduce the costs of the economically desired activity by an equal percentage for most households. Thus, they are often more economically efficient. Refundable tax credits often are the most economically efficient way to use the tax code to encourage socially valued behavior because they reduce the price of the desired activity by an equal amount for all households, regardless of their income or tax liability during the year in question. Non-refundable tax credits are not available to the more than one-third of American families that owe no individual income taxes, despite the fact that most of these households have positive tax liability when payroll and other taxes are considered. As Batchelder, Goldberg, and Orszag observed:

If policymakers wish to use the tax system to create incentives for certain socially-valued behavior, it makes no sense to exclude more than a third of American individuals and families from their reach, or to provide smaller benefits to some households than others, absent evidence that those Americans would be relatively unresponsive [to the tax incentive] or that their behavior generates fewer societal benefits. [9]

In sum, our system of tax expenditures often provides the greatest benefits and incentives to those households who least need them, while failing to reach most low- and moderate-income households who often are the people who would be likely to respond most strongly to the tax incentives. This fundamental design flaw makes these incentives ripe for reform that could improve economic efficiency and promote greater equity, while generating budget savings.

Tax Expenditure Reform Can Also Lean Against Rising Inequality

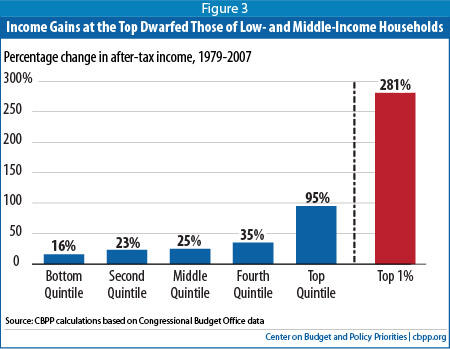

During the early post-World War II decades, economic growth was robust and widely shared: economy-wide productivity improvements were accompanied by significant increases in the living standards of most Americans. In recent decades, by contrast, the benefits of economic growth have not been widely shared. Congressional Budget Office data show that between 1979 and 2007, average incomes grew by 281 percent, after adjusting for inflation, for the top 1 percent of Americans, compared to just 25 percent for the middle 20 percent of Americans.

Public policy in general, and tax policy in particular, can mitigate the human consequences of the global trends that have played a large role in suppressing wage growth among lower- and middle-class Americans. Unfortunately, our country’s recent record on this matter has not been stellar. For example, the Urban-Brookings Tax Policy Center estimates that the large tax cuts enacted in 2001 and 2003 now provide people who make over $1 million a year with an average annual tax cut of more than $125,000, more than 140 times (in dollar terms) the average tax cut for households in the middle 20 percent of the income scale. The gap narrows when the tax cuts are measured as a percentage of after-tax income, but remains large: TPC data show that the average tax cut for people making over $1 million is nearly three times larger as a share of after-tax income than the tax cuts received by families in the middle 20 percent of the income scale.

Tax policy ought to lean against the trend of rising inequality, not exacerbate it. Both the deficit commission chaired by Erskine Bowles and Alan Simpson and the separate commission chaired by Alice Rivlin and Pete Domenici sought to ensure that the tax measures they proposed improved the progressivity of the system. The Bowles-Simpson report set forth a basic principle in this respect: “Though reducing the deficit will require shared sacrifice, those of us who are best off will need to contribute the most. Tax reform must continue to protect those who are most vulnerable, and eliminate tax loopholes favoring those who need help least.” Since the majority of current tax expenditures provide the greatest benefit to households that least need it, while excluding many of those who would be most likely to respond to the tax incentive, reforming many tax expenditures — by decoupling the subsidies they provide from marginal tax rates — would be fully consistent with this principle.

Growing Support for Tax Expenditure Reform

In 2005, President George W. Bush established an Advisory Panel on Federal Tax Reform, instructing it to offer proposals that would “deliver a simpler, fairer, and more pro-growth tax system.” [10] Though its proposals would have worsened the nation’s fiscal problems, [11] the panel made the reduction of costly and inefficient tax preferences — in order to create a “cleaner” tax base — one of its primary goals. The reform panel set stringent criteria for tax expenditures, requiring that they “provide incentives to change behavior in ways that benefit the economy and society, rather than representing a windfall to targeted groups of taxpayers for activity they would be likely to undertake even without a tax subsidy.”

For example, the panel recommended replacing the home mortgage interest deduction with a tax credit equal to 15 percent of the interest paid on a principal residence. Also, noting that tax incentives targeted at low-income families must be made refundable to have the intended incentive effects, the panel proposed replacing the existing non-refundable “saver’s credit” (which provides a tax subsidy for qualified contributions to retirement accounts made by people with incomes below $55,000) with a refundable saver’s credit. Additionally, the panel endorsed the view that the tax system should provide substantial refundable credits to encourage and reward work by low-income families. [12]

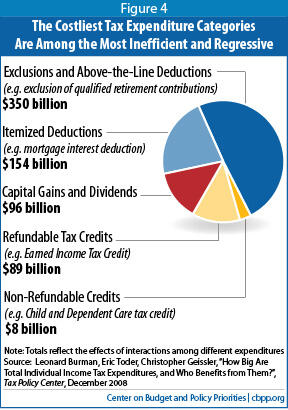

The Obama Administration, most recently in its 2012 budget, has focused on tax expenditures that take the form of itemized deductions. Like exemptions, exclusions, and “above-the-line” deductions, itemized deductions reduce taxable income by amounts that depend on a taxpayer’s tax bracket, thereby giving high-income individuals larger tax subsidies. Moreover, only taxpayers who “itemize” their deductible expenditures (rather than using the standard deduction) may receive the benefits of itemized deductions, which further concentrates those tax benefits on affluent households, since most low- and middle-income households use the standard deduction rather than itemizing.

Indeed, only 30 percent of all taxpayers itemize — but 89 percent of those in the highest income bracket do. [13] Because high-income individuals are more likely to itemize — and receive a higher per-dollar tax benefit when they do — itemized deductions tend to be among the most regressive types of tax expenditures.

The Obama proposal would place a 28 percent cap on the value of itemized deductions. This would affect only those households that both itemize deductions and are in the top two marginal tax brackets (the brackets where the marginal tax rate exceeds 28 percent) — about 2 percent of all taxpayers in 2012, according to the Tax Policy Center. [14] The proposal would promote both economic efficiency and equity while contributing to deficit reduction. (The Treasury Department estimates it would save $321 billion over ten years.) Nevertheless, it is an incremental step: even at a capped level of 28 percent, tax subsidies for high-income taxpayers would still be provided at a subsidy rate nearly double that provided to middle-class families in the 15 percent bracket.

Most recently, both the Bowles-Simpson and Rivlin-Domenici commissions focused their revenue proposals on reforming and scaling back tax expenditures, consistent with their goals of reducing budget deficits, increasing economic efficiency and growth, and protecting the nation’s most vulnerable citizens. Furthermore, in devoting tax expenditure savings to a combination of reducing the deficit and lowering tax rates, both plans recognize that spending through the tax code both contributes to budget deficits and leads to marginal tax rates higher than they would otherwise need to be.

The Rivlin-Domenici panel placed a particularly high priority on reforming “upside-down” tax expenditures, especially itemized deductions. Noting that the broad majority of tax expenditures provide their largest subsidies to households of the greatest means, who least need these incentives to take the desired actions, the panel concluded that the structure of the subsidies is “perverse.” Accordingly, it proposed such measures as converting the mortgage interest deduction to a 15 percent refundable tax credit, available to all homeowners for mortgage interest of up to $25,000 on a principal residence. The panel also proposed replacing the current deduction for charitable giving with a similar 15 percent refundable tax credit.

In the same vein, the Bowles-Simpson commission’s illustrative tax reform plan would eliminate or restructure many of the most “upside-down” tax expenditures, including itemized deductions, many exclusions, and preferential tax rates on capital gains and dividends, while maintaining or expanding key tax credits.[15] Thus, Bowles-Simpson calls for replacing the mortgage interest deduction with a 12 percent tax credit on the first $500,000 in mortgage value, and replacing the charitable deduction with a 12 percent non-refundable credit on charitable contributions in excess of 2 percent of adjusted gross income.

Structuring Tax Expenditures as Credits Would Improve Economic Efficiency

The current structure of many tax expenditures — which often provide the highest tax benefits to households that both need them least and are the least likely to change their behavior in response to the tax incentives — is both economically inefficient and inequitable. This structural flaw in current tax expenditure design presents policymakers with opportunity to simultaneously pursue the goals of deficit reduction, improved economic efficiency, and greater equity.

By converting various existing tax deductions into uniform-percentage tax credits, policymakers can improve economic efficiency by increasing the effectiveness of the tax incentives in boosting retirement saving, college attendance, and the like even as they achieve deficit reduction and improve the progressivity of the tax code. In addition, in some cases, such tax credits would be more efficient if the maximum tax credit amount were capped, so that more of our limited resources could be channeled into effective incentives for homeownership, retirement saving, and college education, and fewer resources used to subsidize more lavish homes or more generous health insurance.

What policymakers should not do is scale back inefficient tax expenditures but then devote the bulk of the savings to large rate reductions, which would do nothing to help address our fiscal challenges. Nor should they weaken, in the name of deficit reduction, programs that are vital to promoting work over welfare and helping low-income working families make ends meet, such as the EITC and Child Tax Credit. Past deficit reduction agreements have shrunk deficits while protecting low-income working families: in fact, the 1990 bipartisan deficit reduction agreement expanded the EITC, and the bipartisan 1997 agreement established the Child Tax Credit. Both the Bowles-Simpson and Rivlin-Domenici commissions, as well, would protect these credits. Congress should maintain this commitment and assure that the EITC and refundable Child Tax Credit are maintained in any agreements on deficit reduction and tax reform.

Conclusion

Recent policy developments suggest a growing interest in scrutinizing and reforming the array of tax expenditures in the federal tax code. The Bowles-Simpson and Rivlin-Domenici panels, President Bush’s 2005 tax reform panel, and the Obama Administration’s most recent budget all propose some fairly bold reforms of itemized deductions and other tax expenditures. A common emerging structure is uniform credits that decouple the rate of a given tax subsidy from a taxpayer’s marginal tax rate. Such a structure holds the promise of improving economic efficiency and equity, as well as raising additional revenue.

The proposals that have emerged from these various panels and commissions reflect a growing sentiment that as long as we continue to use the tax code as a vehicle to encourage socially beneficial behavior, we should take steps to make sure that the subsidies the tax code provides are effective and efficient and serve important purposes, rather than being unnecessary or inefficient measures that constitute wasteful spending.

Moreover, if we are going to step up to the plate and pursue deficit reduction, all parts of the budget — including the tax code and its costly tax expenditures — should be on the table. And as the Bowles-Simpson and Rivlin-Domenici plans indicate, tax reform cannot be deficit-neutral today, given the gravity of the fiscal challenges the nation faces. The bulk of the savings from scaling back and restructuring tax expenditures should go toward reducing the federal budget deficit, rather than financing still more tax cuts.

Finally, if we seek to reduce less-efficient government spending, tax expenditures are a key place to focus. Tax expenditure reform, if done responsibly and well, has the potential to help shrink budget deficits and promote economic efficiency, while also making the tax code more progressive.

End Notes

[1] The Moment of Truth: Report of the National Commission on Fiscal Responsibility and Reform , December 1, 2010, http://www.fiscalcommission.gov/news/moment-truth-report-national-commission-fiscal-responsibility-and-reform .

[2] Joint Committee on Taxation, “Background Information on Tax Expenditure Analysis and Historical Survey of Tax Expenditure Estimates,” March 1, 2011, http://www.jct.gov/publications.html?func=startdown&id=3740.

[3] Leonard Burman, Eric Toder, and Christopher Geissler, “How Big Are Total Individual Tax Expenditures, and Who Benefits from Them?” Tax Policy Center Discussion Paper, December 2008, http://www.taxpolicycenter.org/UploadedPDF/1001234_tax_expenditures.pdf .

[4] The estimated costs of the tax expenditures listed in the President’s FY2012 budget sum to just under $1.1 trillion, not including the roughly $50 billion of additional outlay effects. These component costs, however, are not strictly additive; the presence or absence of a specific tax expenditure often has a significant impact on the cost of others. Current estimates do not account for these interaction effects. Some researchers estimate that the interaction effects increase the total cost of individual tax expenditures by about 5 to 8 percent. See Burman, Toder, and Geissler, 2008.

[5] Martin Feldstein, “The ‘Tax Expenditure’ Solution for Our National Debt,” Wall Street Journal, July 20, 2010, http://online.wsj.com/article/SB10001424052748704518904575365450087744876.html .

[6] Government Accountability Office, “Opportunities to Reduce Potential Duplication in Government Programs, Save Tax Dollars, and Enhance Revenue,” March 1, 2011, http://www.gao.gov/new.items/d11318sp.pdf.

[7] The structure of a given tax expenditure also largely determines how regressive or progressive it is. Specifically, because a given dollar of tax incentive is in most cases likely to have great effects on low-income families, economic efficiency generally mirrors progressivity with respect to tax expenditures, although this is not always the case.

[8] “[P]roviding a larger incentive to higher-income households is economically inefficient unless policymakers have specific knowledge that such households are more responsive to the incentive or that their engaging in the behavior generates larger social benefits.” Lily L. Batchelder, Fred T. Goldberg, Jr., and Peter R. Orszag, “Reforming Tax Incentives into Uniform Refundable Tax Credits,” Brookings Institution Policy Brief #156, August 2006 http://www.brookings.edu/comm/policybriefs/pb156.pdf/t_blank

[9] Batchelder, Goldberg, and Orszag, 2006.

[10] The President’s Advisory Panel on Federal Tax Reform, “Simple, Fair, & Pro-Growth: Proposals to Fix America’s Tax System,” November 1, 2005, http://govinfo.library.unt.edu/taxreformpanel/.

[11] Although the panel described its recommendations as being revenue-neutral, the panel’s proposals would have raised far less revenue than current law; they were revenue-neutral only relative to a baseline that assumed the permanent extension of all of the 2001 and 2003 tax cuts as well as several other proposed tax cuts. See Jason Furman, “The Tax Reform Panel’s Costly Proposal,” Center on Budget and Policy Priorities, November 2005.

[12] For a more complete analysis of the proposals, see Aviva Aron-Dine and Joel Friedman, “Effects of the Tax Reform Panel’s Proposals on Low- and Moderate-Income Households,” Center on Budget and Policy Priorities, February 3, 2006.

[13] Benjamin H. Harris and Daniel Baneman, “Who Itemizes Deductions?,” Tax Notes, January 17, 2011.

[14] If the Bush tax cuts are extended beyond 2012 for households with incomes below $250,000 ($200,000 for single filers), then approximately 2 percent of households would be affected by the Obama proposal. This 2 percent figure would hold whether the Bush tax cuts for people over $250,000 ($200,000 for single filers) were extended or not. If the Bush tax cuts were allowed to expire for all households (not just those with high incomes), the proposal would affect 4.8 percent of households. Tax Policy Center, “Limit Value of Itemized Deductions to 28 Percent,” February 4, 2010, http://www.taxpolicycenter.org/numbers/Content/PDF/T10-0065.pdf.

[15] The Bowles-Simpson illustrative tax plan, which the staff of the fiscal commission that Bowles and Simpson co-chaired provided to the Tax Policy Center to analyze, would retain the Child Tax Credit (CTC) and Earned Income Tax Credit (EITC), while extending the CTC and EITC provisions included in the 2009 Recovery Act that are scheduled to expire at the end of 2012. The Bowles-Simpson plan also would establish a refundable saver’s credit equal to 12 percent of the retirement contributions that a qualifying tax filer makes (so long as the contributions are not deducted from taxable income). Capital gains and qualified dividends would be taxed as ordinary income, and the value of capital gains that had not been realized when an individual died would be subject to capital gains tax when the individual’s affairs were settled after the person’s death.

More from the Authors

Areas of Expertise