How Robust Was the 2001-2007 Economic Expansion?

Proponents of the 2001 and 2003 tax cuts often argue that the economic and employment growth of the past several years establishes that these tax cuts “worked” and had strong beneficial effects. More recently, some have also argued that, with growth slowing, new tax cuts are needed and would reinvigorate the economy.

It now appears likely that the economic expansion that began in 2001 drew to a close in 2007. Whether or not it is ever formally declared a recession, the period since the third quarter of 2007 has seen sub-par growth (including a negative fourth quarter in 2007), shrinking payroll employment, and a rising unemployment rate, and so looks more like an economic slump than an economic expansion. Now is therefore a good time to take stock of the 2001-2007 economic expansion as a whole. We examine the expansion from 2001, when it began, through the third quarter of 2007, before the recent slow-down in economic growth.

The evidence on the 2001-2007 expansion provides no support for the claim that the tax cuts generated especially robust economic growth. Rather, examination of a broad range of key economic indicators indicates that the economic expansion that began in 2001 was, on balance, weaker than average. In fact, with respect to GDP, consumption, investment, wage and salary, and employment growth, the 2001-2007 expansion was either the weakest or among the weakest since World War II.

Moreover, the economy’s performance between 2001 and 2007 was weaker, overall, than its performance in the equivalent years of the 1990s, years following significant tax increases. GDP growth was somewhat weaker than in the 1990s, and job creation, investment, and wage and salary growth all were substantially weaker.

What the Data Show: The Key Findings

We examine Commerce Department, Labor Department, and Federal Reserve Board data on seven economic indicators: the gross domestic product, personal consumption expenditures, private domestic fixed non-residential investment, net worth, income from wages and salaries, payroll employment, and corporate profits. For each indicator, we look at average growth both since the economy hit bottom in November 2001 and since the last business-cycle peak in March 2001. We compare average growth over these periods with the average growth that occurred over comparable periods in the other business cycles since the end of World War II.[1] (Growth is measured after adjusting for inflation, except for employment levels, where such an adjustment is inapplicable.)

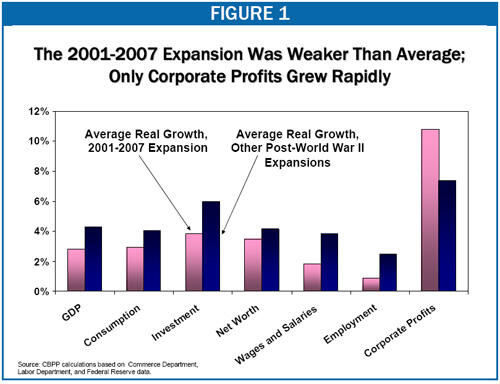

- For six of the seven indicators, the average annual growth rate between 2001 and 2007 was below the average growth rate for the comparable periods of other post-World War II economic expansions. Notably, this expansion was among the weakest since World War II with respect to both overall economic growth and growth in fixed non-residential investment. These two indicators should have captured any positive “growth effects” of the tax cuts.

- The labor market also was weaker during the 2001-2007 expansion. Both employment growth and wage and salary growth were weaker during this expansion as a whole than in any prior expansion since the end of World War II.

- The 2001-2007 expansion outperformed the average post-World War II expansion in only one area: corporate profits, which grew much more rapidly than average.

These conclusions hold whether one focuses on comparisons that examine the period since the expansion began in the fourth quarter of 2001, or comparisons that examine the period since the last business-cycle peak (i.e., since the 1990s expansion ended in the first quarter of 2001).

The 2001-2007 Expansion

As noted above (and as shown in Table 1 on page six), we have examined the performance of these economic indicators in two ways: from the start of the expansion in November 2001 (that is, since the fourth quarter of 2001) through the third quarter of 2007; and from the previous economic peak (the first quarter of 2001) through the third quarter of 2007. This section focuses on the expansion period from the first quarter of 2001 to the third quarter of 2007.

The Gross Domestic Product, consumption, net worth, non-residential investment, wages and salaries, and employment all grew less rapidly than during other comparable expansionary periods.[2] Labor market progress was especially weak, with employment and wage and salary growth far below average and, in fact, lower than in any previous post-World War II expansion. Employment grew at an average annual rate of only 0.9 percent from November 2001 to September 2007, as compared with an average of 2.5 percent for the comparable periods of other post-World War II expansions. In addition, real wages and salaries grew at a 1.8 percent average annual rate in the 2001-2007 expansion, as compared with a 3.8 percent average annual rate for the comparable periods of other post-World War II expansions.

Corporate profits fared exceptionally well. The sole exception to the 2001-2007 period’s lackluster performance was the growth of corporate profits. They experienced average annual growth of 10.8 percent, as compared with average growth of 7.4 percent for other comparable post-war periods.

Comparisons Measuring from Economic Peaks

In the previous section of this analysis, we compared the 2001-2007 expansion with earlier expansions by measuring growth rates for various key economic indicators starting from the trough of the business cycle. Some may argue that this comparison disadvantages the 2001-2007 expansion because it followed a relatively mild recession. All else being equal, one would expect the economy to recover more robustly after a deep recession than after a shallow one.

To account for the possibility that starting from the trough skews the results, we also examined growth in the same indicators starting from the previous economic peak, which in this case was March 2001. Using that approach does not change any of our central conclusions. Measured since the peak, growth still fell short of the post-war average for all indicators except corporate profits (see Table 1), and growth in GDP, investment, wages and salaries, and employment all remained especially weak in comparative terms.

Supporters of the tax cuts generally focus on a different set of statistics: growth rates measured only from 2003-2007, the strongest portion of the expansion. Such an approach is misleading. The fact that growth rates over the expansion as a whole were well below average indicates that the economy never caught up to where it would have been if GDP, consumption, investment, net worth, wages and salaries, and employment had merely grown since the start of the expansion at the average rates for post-war expansions. Moreover, even since 2003, GDP, consumption, investment, wage and salary, and employment growth have been unexceptional by historical standards.[3]

The Duration of the Expansion

One point in favor of the 2001-2007 expansion is its length. The expansion was longer than six of the nine previous post-World War II economic expansions. Even taking its duration into account, however, the 2001-2007 expansion was far from a standout.

- Our analysis of economic indicators compares economic performance in the 2001-2007 expansion with average economic performance for all previous post-World War II expansions, including those that were shorter than the 2001-2007 expansion. This means we have compared the 2001-2007 expansion with past periods of the same duration, some of which included the beginning of a second recession within that time period. This method of comparison confers an advantage on longer expansions: they should look better than other comparison periods that include a period of recession. Yet the 2001-2007 period still is weaker than average with respect to all indicators except corporate profits.

- Another approach is to compare total (percentage) growth during different expansionary periods, rather than average annual growth. This approach also gives longer expansions an advantage, since they include more consecutive quarters of growth. But total growth during the 2001-2007 period was worse than usual for all indicators except corporate profits.

- Finally, if we compare the 2001-2007 expansion with just those three expansions that lasted at least as long as the current expansion (the expansions of the 1960s, 1980s, and 1990s), we find that the 2001-2007 period is even further below average with respect to GDP, consumption, investment, net worth, wage and salaries, and employment growth. It is above average only with respect to growth in corporate profits.

Comparisons to the Economic Cycle of the Early 1990s

Findings from a comparison of the 2001-2007 period with the business cycle of the early 1990s also are of note, since the comparable period of the 1990s expansion followed tax increases.

- The rate of GDP growth was somewhat higher in the 1990s expansion, and net worth grew more rapidly.

- Job growth was much stronger during the 1990s. Job growth between 2001 and 2007, occurred at less than half the pace it did during the comparable period of the 1990s expansion.

- Similarly, fixed non-residential investment grew much more slowly during the 2000s expansion: at a 3.9 percent annual rate, far below the 7.6 percent annual rate at which it grew over the comparable portion of the 1990s expansion. If tax cuts are good for long-term growth because they induce investment, as proponents argue, they should have had a positive impact on non-residential investment (investment in the productive capital stock).

- In contrast, corporate profits increased considerably faster during the 2000s expansion.

It is also worth noting that the 1990s expansion continued for four additional years after the period considered here, whereas the 2001-2007 expansion has already given way to a significant slow-down, if not a recession. Moreover, the economy’s performance during the later part of the 1990s (the part not included in these comparisons) was stronger than in the years of the 1990s expansion that we examine here.

Extending the Tax Cuts Without Paying for Them Is More Likely to Harm Than Help the Economy in the Long Run

These data suggest that the 2001 and 2003 tax cuts did not lead to a shining economic performance. Even relative to the 1990s, when taxes were increased significantly during the early stages of the expansion, the economy’s performance after these tax cuts was disappointing.

But while the tax cuts do not appear to have delivered especially good outcomes for the economy, they have contributed to a sharp deterioration in the fiscal outlook. Since the last economic peak, the budget has swung from surplus to deficit, with the tax cuts accounting for about half of the swing. The cost of the tax cuts in fiscal year 2007 was greater than the entire fiscal year 2007 budget deficit.

If the tax cuts are extended and their cost continues to be deficit-financed, they are more likely to harm the economy over the long run than to help it. A number of studies by highly respected institutions and economists have found that, if major tax cuts are deficit-financed, the negative effects of higher long-term deficits are likely to cancel out or outweigh any positive economic effects that might otherwise result from the tax cuts.[4] For instance, a comprehensive study of the 2001 and 2003 tax cuts by Brookings Institution economist William Gale and then-Brookings Institution economist (now CBO director) Peter Orszag found that making the tax cuts permanent without offsetting their cost would be “likely to reduce, not increase, national income in the long term.”[5] The bottom line is that large deficit-financed tax cuts are more likely to reduce investment and economic growth than to increase them.

| TABLE 1: | |||||||

| Growth Rates Measured from Trough | |||||||

| GDP (a) | Consumption (a) | Non-Residential Fixed Investment (a) | Net Worth (a) | Wages and Salaries (a) | Employment (b) | Corporate Profits (a) | |

| Current Expansion | 2.8% | 2.9% | 3.9% | 3.5% | 1.8% | 0.9% | 10.8% |

| Post-War Average | 4.3% | 4.0% | 6.0% | 4.1% | 3.8% | 2.5% | 7.4% |

| 1990s | 3.3% | 3.2% | 7.6% | 4.1% | 2.7% | 1.9% | 8.0% |

| Growth Rates Measured from Peak | |||||||

| GDP (c) | Consumption (c) | Non-Residential Fixed Investment (c) | Net Worth (c) | Wages and Salaries (c) | Employment (d) | Corporate Profits (c) | |

| Current Expansion | 2.5% | 2.9% | 2.0% | 3.2% | 1.2% | 0.6% | 9.5% |

| Post-War Average | 3.4% | 3.6% | 3.7% | 3.9% | 2.9% | 1.7% | 3.8% |

| 1990s | 2.8% | 2.8% | 6.4% | 4.3% | 2.3% | 1.5% | 8.1% |

| (a) Average growth rate in 23 quarters after trough. Current expansion: 2001-IV:2007-III. 1990s: 1991-I:1996-IV. Post-war average includes 1990s and 1949-IV:1955-III, 1954-II:1960-I, 1958-II:1964-I, 1961-I:1966-IV, 1970-IV:1976-III, 1975-I:1980-IV, 1980-III:1986-II, 1982-IV:1988-III. (b) Average growth rate in 70 months after trough. (c) Average growth rate in 26 quarters after peak. Current expansion: 2001-I:2007-III. 1990s: 1990-III:1997-I. Post-war average includes 1990s and 1948-IV:1955-II, 1953-II:1959-IV, 1957-III:1964-I, 1960-II:1966-IV, 1969-IV:1976-II, 1973-IV:1980-II, 1980-I:1986-III, 1981-III:1988-I. (d) Average growth rate in 78 months after peak. Post-war averages for net worth exclude the 1948 peak and 1949 trough due to lack of data. Sources: GDP, consumption, non-residential investment, wages and salaries, and corporate profits data: Bureau of Economic Analysis. Employment data: Bureau of Labor Statistics. Net worth data: Federal Reserve Board Statistical Release, Flow of Funds Accounts of the United States. | |||||||

End Notes

[1] We take comparable periods to be periods of equal length as measured from the trough or peak of the business cycle, as identified by the National Bureau of Economic Research (the arbiter of the starting and ending points of business cycles).

[2] We examine fixed non-residential investment, as opposed to total gross domestic investment, in order to ensure that we capture growth of the productive capital stock that might be targeted by the tax cuts rather than growth of inventories or housing construction. If tax cuts are good for long-term growth because they induce investment, as proponents argue, then the type of investment that should have increased is investment in business plant and equipment. (Note that the growth in gross investment also has been below average in this expansion, averaging 3.7 percent annually during the current expansion, as compared with a post-war average of 8.0 percent.)

[3] For further discussion of the economy’s performance since 2003, see Aviva Aron-Dine, “The Effects of the Capital Gains and Dividend Tax Cuts on the Economy and Revenues: Four Years Later, a Look at the Evidence,” Center on Budget and Policy Priorities, revised July 12, 2007.

[4] See, for example, Alan J. Auerbach, “The Bush Tax Cut and National Saving,” National Tax Journal, Volume LV, No. 3, September 2003; and Douglas W. Elmendorf and David L. Reifschneider, “Short-Run Effects of Fiscal Policy with Forward-Looking Financial Markets,” prepared for the National Tax Association’s 2002 Spring Symposium; Congressional Budget Office, “Analyzing the Economic and Budgetary Effects of a 10 Percent Cut in Income Tax Rates,” December 2005; and Joint Committee on Taxation, “Macroeconomic Analysis of Various Proposals to Provide $500 Billion in Tax Relief,” JCX-4-05, March 1, 2005.

[5] Williams Gale and Peter Orszag, “Bush Administration Tax Policy: Effects on Long-Term Growth,” Tax Notes, October 18, 2004. See also Gale and Orszag, “Deficits, Interest Rates, and the User Cost of Capital: A Reconsideration of the Effects of Tax Policy on Investment,” Urban Institute-Brookings Institution Tax Policy Center, August 19, 2005.

More from the Authors

Areas of Expertise

Areas of Expertise