The Effects of the Capital Gains and Dividend Tax Cuts On the Economy and Revenues

Four Years Later, a Look at the Evidence

Summary

With the fourth anniversary of the 2003 capital gains and dividend tax cuts just past and the Office of Management and Budget’s Mid-Session Review released today, supporters of making these tax cuts permanent are reiterating their claim that the tax cuts boosted the economy and increased federal revenues. For example, a release from the Senate Republican Policy Committee contends that the tax cuts “contributed to today’s strong pro-growth economy” and “have also led to a surge in tax receipts” and that allowing these tax cuts to expire as scheduled would “have devastating consequences for the economy.”[1]

Claims like these raise three basic questions. First, has the economic and revenue growth of the past few years really been unusually strong? Second, are there good reasons to think that the capital gains and dividend tax cuts caused whatever economic and revenue growth has occurred, as opposed to just coinciding with it? Third, would extending these tax cuts boost economic and revenue growth on a longer-term basis?

The last four years of data, as well as some important new academic research, suggest that the answer to each of these questions is No.

Economic and Revenue Growth Unexceptional

Since supporters of the capital gains and dividend tax cuts routinely appeal to the economic and revenue growth of the past few years as evidence of these tax cuts’ success, one might assume that the recent economic performance has been stronger than typical. In fact, the opposite is the case.

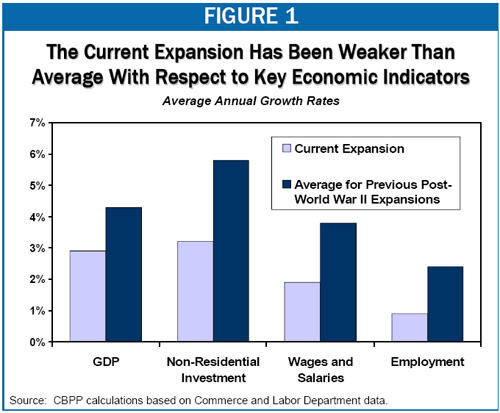

- Growth in key indicators such as the Gross Domestic Product (GDP), non-residential investment, wages and salaries, and employment has been below average during the current economic expansion, relative to previous post-World War II expansions. (See Figure 1.) The current recovery has also been weaker overall than the equivalent period of the 1990s, during which there were tax increases rather than tax cuts.[2]

- Those who argue that the capital gains and dividend tax cuts had powerful economic effects often discount the first two (very weak) years of the current economic expansion and focus on growth since 2003. But even since 2003, the growth in GDP, wages and salaries, and employment has been below average for a post-World War II recovery. Growth in non-residential investment has only matched the historical norm.

- Despite claims that the tax cuts have generated a revenue surge and have thus “paid for themselves,” revenues, too, have grown at below-average rates — exactly as one would expect in the aftermath of two large tax cuts. Based on the new Office of Management and Budget projections, revenues at the end of fiscal year 2007 will be only 3.1 percent higher than when the current business cycle began in 2001, after adjusting for inflation and population growth. This is far below the 12 percent average revenue increase over comparable periods of previous post-World War II business cycles and the 16 percent increase during the 1990s. (Revenue growth since 2003 is discussed below.)

Tax Cuts Coincided With Improvement in the Economy But Didn’t Cause It

Advocates of the 2003 tax cuts frequently emphasize that the economy’s performance improved around the time that these tax cuts were enacted, and they imply that the tax cuts caused the improvement in the economy. But as nine out of ten prominent economists told the New York Times in a recent informal survey, the economy’s improvement was most likely attributable to factors other than the tax cuts.[3]

- Asked to name the main reason for stronger growth after 2003, several economists cited “super-low interest rates caused by the Federal Reserve.” Others chalked the growth up to the “regular business cycle,” with economist Robert Hall of the Hoover Institution pointing out that, “the U.S. economy recovered from every single recession it ever had, so the growth in 2003-2006 was generally part of the normal cyclical recovery.”

- The 1990s recovery provides a useful comparison. Like the current recovery, the 1990s recovery was initially relatively weak, with investment growth in particular resuming only about eighteen months into the recovery. But in the 1990s, investment growth recommenced without any tax cuts — and then strengthened modestly following a tax increase. Moreover, overall investment growth during the 1990s business cycle, with its large tax increases in 1990 and 1993, was substantially stronger than during the current business cycle, with its large tax cuts in 2001 and 2003. If major economic developments were generally attributable to tax policy, then the 1990s experience could lead one to conclude that tax increases provide more potent economic stimulus than tax cuts. The more appropriate lesson to draw, however, is probably that weak recoveries tend to return to historical norms, whether taxes are cut, increased, or left unchanged.

- There is particular reason to doubt that the capital gains and dividend tax cuts were responsible for the 2003 economic improvement given that these tax cuts were not expected to yield short-run economic gains. For example, conservative economist and Nobel Laureate Gary Becker, a strong supporter of the dividend tax cut, wrote that it “will not yield immediate benefits… Any short-run stimulus from eliminating the dividend tax would be too weak to have a significant benefit to the economy.”[4]

Claims that the revenue growth (as distinguished from the economic growth) that has occurred since 2003 was due to the tax cuts are even less believable. In large part, stronger revenue growth after 2003 resulted from the stronger economy. But since, as discussed above, the tax cuts were not responsible for the improvement in the economy, they could not have been responsible for the portion of the revenue increase due to stronger economic growth.

Apart from the stronger economy, several other factors also have helped increase revenues since 2003. But these factors appear to have been independent of the capital gains and dividend tax cuts, and in some cases they reflect developments for which supporters of these tax cuts are unlikely to want to claim credit.

- A recent Congressional Budget Office analysis attributes a significant share of the remaining revenue growth (the growth not due to a growing economy) to a large increase in the share of national income going to corporate profits.[5] When corporate profits increase at the expense of other forms of income, some of which are not subject to tax or are taxed at very low rates, revenues rise. In addition, new data from economists Thomas Piketty and Emmanuel Saez show that the share of the nation’s pre-tax income going to the top 1 percent of households jumped dramatically between 2003 and 2005 (the latest year for which data are available). Increased income concentration tends to raise revenues because it puts more income in the hands of those who pay taxes at higher rates.

Supporters of the capital gains and dividend tax cuts cannot claim credit for the revenue growth that resulted from these developments unless they also claim credit for the developments themselves. That is, they would have to argue that the tax cuts caused the share of the nation’s income going to corporate profits and high-income households to increase — and consequently caused the share going to employee compensation and middle- and low-income households to fall. Tax-cut supporters have been notably silent on this score. - CBO’s analysis does attribute a small share of the increase in revenues since 2003 to an increase in capital gains receipts resulting from higher capital gains realizations; much of this increase likely reflects the growth in the stock market that has occurred since 2003. Here, too, the challenge is to determine whether stock market growth that followed the capital gains and dividend tax cuts was caused by these tax cuts. A careful study by three Federal Reserve economists refuted this contention, finding that the tax cuts were not the reason the stock market rose in 2003. The study compared the performance of taxable stocks in the United States to the performance of European stocks, which did not benefit from the tax cuts. It found that European markets, which were unaffected by the U.S. capital gains and dividend tax cuts, behaved similarly to the U.S. market, casting serious doubt on the idea that the tax cuts were a crucial factor behind the improvement in the U.S. market.[6]

Making Tax Cuts Permanent Would Likely Have Negligible Economic Impact, But Would Cost About $30 Billion A Year

While most of the debate among policymakers and journalists has focused on whether the capital gains and dividend tax cuts boosted the economy in the short run, the more credible argument for these tax cuts has always been that they might boost long-run growth by inducing Americans to increase personal saving or investment at the expense of consumption or by making the allocation of investment more efficient. The evidence on these arguments remains inconclusive, however, and early studies of the 2003 tax cut raise fresh doubts about such claims. In addition, the tax cuts thus far enacted — and most proposals to extend them — rely on deficit financing, which has negative long-term economic effects potentially large enough to outweigh any economic gains from the tax cuts.

- Early evidence on the capital gains and dividend tax cuts’ impact on savings, investment, and efficiency is not especially encouraging. Investment growth since 2003 has been average by historical standards; meanwhile, the personal saving rate has swung from positive to negative.

Furthermore, two important academic studies of the 2003 dividend tax cut found evidence that cutting taxes on dividends does not improve economic efficiency. One study, by Harvard Professor Mihir Desai and University of Chicago Professor Austan Goolsbee, concluded, “[T]he dividend tax cut, despite its high revenue cost, had minimal, if any, impact on marginal investment incentives.”[7] - Unless the cost of the capital gains and dividend tax cuts is offset by cuts in services or increases in other taxes, extending these tax cuts will add to deficits, thereby reducing both national saving and future national income. The non-partisan Congressional Research Service concluded that, under most plausible assumptions, the dividend tax cut “would harm long-run growth as long as it is based on deficit finance[ing].”[8]

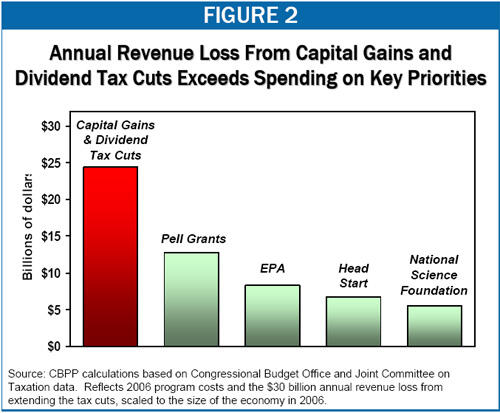

- The Joint Tax Committee projects that making the capital gains and dividend tax cuts permanent would reduce revenues by about $30 billion a year, or about $25 billion a year in 2006 terms. This amounts to about twice what the federal government spent last year on Pell Grants to help low-income students attend college and more than twice what it spent on the Environmental Protection Agency, the Head Start Program, or the National Science Foundation. (See Figure 2.)

Tax-cut supporters have challenged the Joint Tax Committee cost estimates, arguing that extending the capital gains and dividend tax cuts would produce such large economic gains that it would more than pay for itself and would actually raise revenue. But as discussed above, it is not clear that extending the tax cuts would yield any significant economic benefits over the long run, much less economic gains large enough to fully offset the cost.

The remainder of this analysis examines the evidence in more detail, first regarding the capital gains and dividend tax cuts and the economy, and then regarding these tax cuts and revenues.

End Notes

[1] Senate Republican Policy Committee, “Marking the 4th Anniversary of the 2003 Tax Relief Law: A Boon to Taxpayers, Tax Receipts, and the Economy,” May 15, 2007.

[2] Specifically, GDP growth in the 1990s recovery was slightly stronger than in the current recovery, while growth in investment, wages and salaries, and employment was substantially stronger. For more detailed comparisons, see Aviva Aron-Dine, Chad Stone, and Richard Kogan, “How Robust Is the Current Economic Expansion?” Center on Budget and Policy Priorities, revised June 28, 2007, https://www.cbpp.org/8-9-05bud.htm.

[3] Daniel Altman, “Pop Quiz: Did the Tax Cuts Bolster Growth?” New York Times, May 13, 2007, http://www.nytimes.com/2007/05/13/business/yourmoney/13view.html

[4] Gary S. Becker, “The Dividend Tax Cut Will Get Better With Time,” Business Week, February 10, 2003, http://www.businessweek.com/magazine/content/03_06/b3819038.htm.

[5] Letter from Congressional Budget Office Director Peter R. Orszag to Senate Budget Committee Chairman Kent Conrad, May 18, 2007, http://cbo.gov/ftpdocs/81xx/doc8116/05-18-TaxRevenues.pdf.

[6] Gene Amromin, Paul Harrison, and Steven Sharpe, “How Did the 2003 Dividend Tax Cut Affect Stock Prices?” Federal Reserve Board Discussion Paper, December 2005, http://www.federalreserve.gov/pubs/feds/2005/200561/200561pap.pdf.

[7] Mihir A. Desai and Austan D. Goolsbee, “Investment, Overhang, and Tax Policy,” Brookings Papers on Economic Activity, 2004.

[8] Jane Gravelle, “Dividend Tax Relief: Effects on Economic Recovery, Long-Term Growth, and the Stock Market,” Congressional Research Service, updated Feburary 14, 2005.

More from the Authors