Commentary: Growing Evidence Shows Need for Stronger Rules for Short-Term Health Plans

Mounting evidence shows that short-term health plans, which the Trump Administration is promoting as a harmless alternative to comprehensive health insurance under the Affordable Care Act (ACA), engage in deceptive marketing practices, aggressively search for reasons to deny claims, and make comprehensive plans more expensive for those who need them. The Administration weakened federal standards for short-term plans two years ago, and it argues that the plans just represent a cheaper option for informed consumers who understand the risks. But as enrollment in these plans rises, they are leaving more people without comprehensive coverage.

"Short-term plans can deny coverage or charge higher prices to people with pre-existing conditions, and they typically don’t cover medical services related to a pre-existing condition."

Short-term plans can deny coverage or charge higher prices to people with pre-existing conditions, and they typically don’t cover medical services related to a pre-existing condition. They don’t have to cover all the essential health benefits required by the ACA, so they often leave out maternity and mental health care, substance use disorder treatment, and prescription drugs.[1]

The Administration’s rule changes allowed short-term plans to last up to a year (instead of three months) and be extended even longer. Since then, enrollment is up. Some 3 million people were enrolled in short-term plans offered by nine major companies in 2019, about 600,000 more than when the rule took effect the previous year.[2] Unfortunately, comparable data aren’t available on enrollment before the rule change.

Greater enrollment in short-term plans exposes more people to the risk of catastrophically high out-of-pocket costs. A hypothetical person who, thinking she is healthy, enrolls in a short-term plan and is then diagnosed with breast cancer would pay $40,000-$63,000 out of pocket, compared to less than $8,000 in a marketplace plan that meets ACA standards, according to analysis by the American Cancer Society Cancer Action Network.[3] Patients experiencing lymphoma, a heart attack, or a hospitalization for mental health care would likewise face tens of thousands of dollars if they had a short-term plan rather than an ACA plan.[4] Short-term plans often severely limit how much they will pay for certain services, such as $250 for an emergency room visit or $1,000 per day for a hospital stay, leaving enrollees to pay exorbitant amounts out of pocket after receiving needed medical care.[5]

And while a healthy person might find the premiums for a short-term plan to be cheap, they may also get far less value for their money than they would with an ACA plan. Insurers selling ACA plans in the individual market must spend at least 80 cents of every premium dollar they collect on enrollees’ medical claims and quality improvements, and they must refund any excess to enrollees. In contrast, insurers selling short-term plans reported spending just 62 cents of every premium dollar on medical claims in 2019, on average, and several top sellers spent about 35 cents on the dollar. [6]

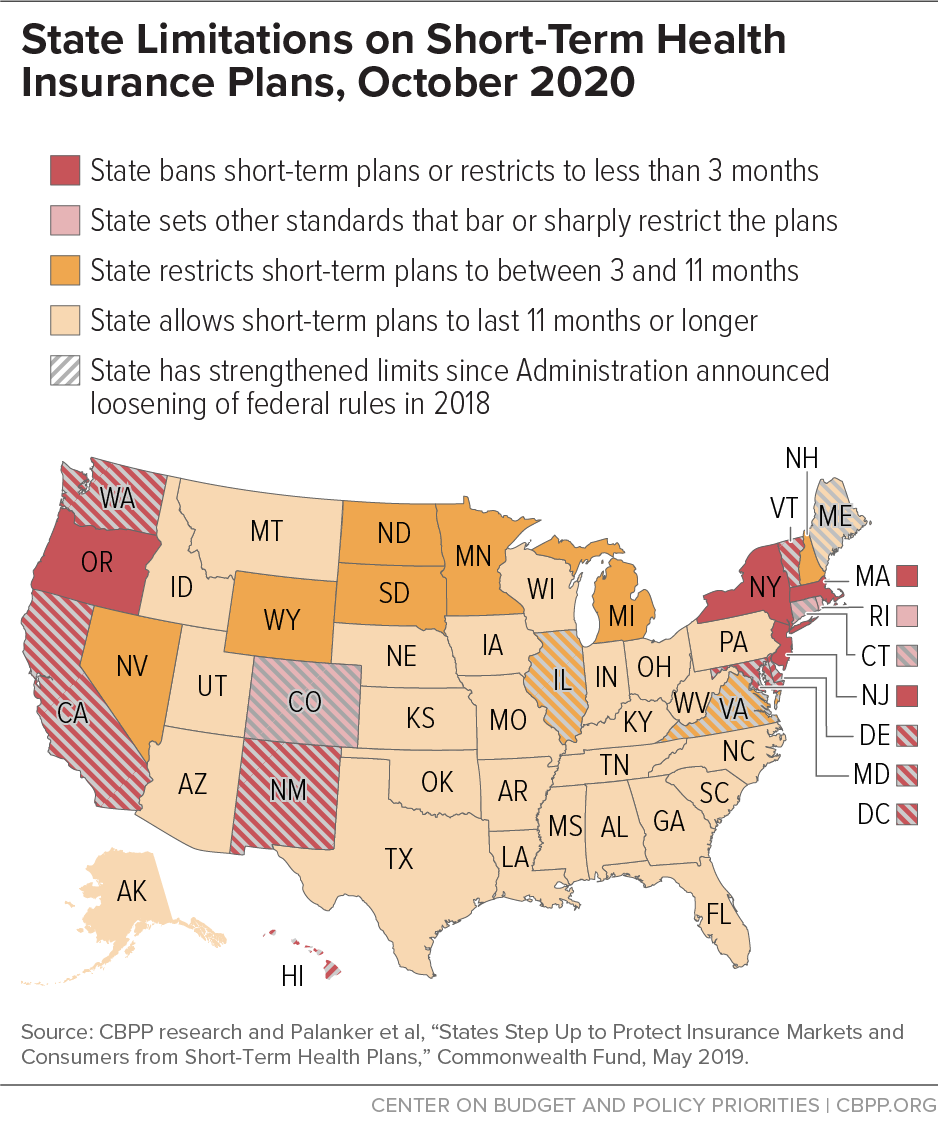

More than a dozen states ban or sharply limit short-term plans, and many states have increased protections for their residents since the federal changes. (See Figure 1.)

Proponents of short-term plans argue that enrollees freely choose the skimpier coverage, willingly taking some risks to save money. But in reality, the short-term market is rife with deceptive marketing tactics and aggressive strategies to avoid paying for care, which makes it challenging, if not impossible, for people to understand what they are buying:

-

Marketing is often misleading. Multiple reports document inaccurate marketing of short-term plans and other non-ACA coverage. Consumers searching online for comprehensive ACA plans often are directed instead to the site of a short-term plan, for example. And brokers sometimes push for a quick sale and refuse to provide written details about the short-term plan.[7]

The COVID-19 pandemic has created new opportunities for misleading marketing. In five of the nine calls that Brookings researchers had with brokers, they received false information about the extent of coverage for COVID treatment and testing and incorrect information about coverage of pre-existing conditions.[8]

In another example, the Government Accountability Office’s (GAO) recent “secret shopper” investigation of non-ACA plans found that brokers engaged in potentially deceptive practices in 8 out of 31 calls. Examples include falsely claiming the plans would cover treatment for a pre-existing condition and omitting information about the condition when submitting an application on the consumer’s behalf, which would enable the insurer to refuse to cover services related to that condition. In two other calls, brokers provided information that GAO deemed merely off base, such as selling shoppers various types of subpar plans without telling them that they could instead buy an ACA plan with $0 in premiums.[9] In a market lacking clear and consistent rules, insurers and brokers have strong financial incentives to use such misleading tactics; merely providing better disclosure to consumers wouldn’t likely stem the problem.[10]

-

Plans use heavy-handed tactics to avoid paying for care. People who buy a short-term plan and then try to use their coverage may have their claims denied or their coverage revoked after their insurer examines their medical history and deems them to have a pre-existing condition after the fact.

A recent investigation documented a “common industry practice” of requiring enrollees who submit claims for costly care to provide years of medical records in a short time frame and then denying their claim if their medical provider doesn’t provide the records in time or, sometimes, retroactively cancelling the plan due to a supposed pre-existing condition.[11] In January, for example, a short-term health plan enrollee in Miami got sick after a trip to China and feared he had the novel coronavirus. He got tested, and the insurer billed him more than $3,000 and demanded that he submit three years of medical records to prove the flu he tested positive for was not related to a pre-existing condition.[12]

Going forward, many more short-term plan enrollees may be at risk for claims denials if insurers can argue that their future health problems are due to COVID-19.[13]

- Short-term plans increase premiums for other consumers. Proponents of short-term plans portray them as a harmless option for people who want to pay lower premiums. But as short-term plans proliferate, they push up premiums for people who want or need ACA-compliant plans by luring healthy enrollees away from the market for comprehensive coverage, leaving a less healthy and thus costlier group behind. In states where the rules for short-term plans are looser (consistent with the 2018 federal changes), 2020 premiums for comprehensive health plans in the individual market are 4 percent (about $25 a month) higher, the actuarial firm Milliman estimates.[14] ACA premium tax credits shield many people from paying these higher rates, but that’s not the case for people not eligible for the credits.

The many pitfalls of short-term plans, and the fact that many more people are now exposed to their risks, are compelling reasons to reinstate stronger federal rules and for additional states to pursue stronger consumer protections.

End Notes

[1] Karen Pollitz et al., “Understanding Short-Term Limited Duration Health Insurance,” Kaiser Family Foundation, April 23, 2018, https://www.kff.org/health-reform/issue-brief/understanding-short-term-limited-duration-health-insurance/.

[2] “E&C Investigation Finds Millions of Americans Enrolled in Junk Health Insurance Plans That Are Bad for Consumers & Fly Under the Radar of State Regulators,” House Committee on Energy & Commerce, June 25, 2020, https://energycommerce.house.gov/newsroom/press-releases/ec-investigation-finds-millions-of-americans-enrolled-in-junk-health.

[3] American Cancer Society Cancer Action Network, “Inadequate Coverage: An ACS CAN Examination of Short-Term Health Plans,” May 13, 2019, https://www.fightcancer.org/sites/default/files/ACS%20CAN%20Short%20Term%20Paper%20FINAL.pdf.

[4] Dane Hansen and Gabriela Dieguez, “The impact of short-term limited-duration policy expansion on patients and the ACA individual market,” Milliman Research Report, February 2020, https://www.lls.org/sites/default/files/National/USA/Pdf/STLD-Impact-Report-Final-Public.pdf.

[5] “E&C Investigation,” op. cit.

[6] Shelby Livingston, “Short-Term Health Plans Promoted by Trump Spent Relatively Little on Claims in 2019,” Modern Healthcare, September 29, 2020, https://www.modernhealthcare.com/insurance/short-term-plans-spent-little-medical-claims-2019 and National Association of Insurance Commissioners, “2019 Accident and Health Policy Experience Report,” 2020, https://www.naic.org/prod_serv/AHP-LR-20.pdf.

[7] Sabrina Corlette et al., “The Marketing of Short-Term Health Plans,” Georgetown University Health Policy Institute, January 31, 2019, https://www.rwjf.org/en/library/research/2019/01/the-marketing-of-short-term-health-plans.html; and Reed Abelson, “Without Obamacare Mandate, You ‘Open the Floodgates’ to Skimpy Health Plans,” New York Times, November 30, 2017, https://www.nytimes.com/2017/11/30/health/health-insurance-obamacare-mandate.html.

[8] Christen Linke Young and Kathleen Hannick, “Misleading marketing of short-term plans amid COVID-19,” USC-Brookings Schaeffer on Health Policy, March 24, 2020, https://www.brookings.edu/blog/usc-brookings-schaeffer-on-health-policy/2020/03/24/misleading-marketing-of-short-term-health-plans-amid-covid-19/.

[9] Government Accountability Office, “Private Health Coverage: Results of Covert Testing for Selected Offerings,” August 24, 2020, https://www.gao.gov/assets/710/708967.pdf.

[10] Consumer Representatives to the National Association of Insurance Commissioners, “Report on Testing Consumer Understanding of a Short-Term Health Insurance Plan,” March 15, 2019, https://healthyfuturega.org/wp-content/uploads/2019/04/Consumer-Testing-Report_NAIC-Consumer-Reps.pdf.

[11] “E&C Investigation,” op cit.

[12] Ben Conarck, “A Miami man who flew to China worried he might have coronavirus. He may owe thousands,” Miami Herald, February 24, 2020, https://www.miamiherald.com/news/health-care/article240476806.html.

[13] Emily Curran et al., “In the Age of COVID-19, Short-Term Plans Fall Short for Consumers,” Commonwealth Fund, May 12, 2020, https://www.commonwealthfund.org/blog/2020/age-covid-19-short-term-plans-fall-short-consumers.

[14] Hansen and Dieguez, op cit.

More from the Authors